FINANCIAL ACCOUNTING a user perspective Sixth Canadian Edition Prepared by: Lynn de Grace C.A....

57

FINANCIAL ACCOUNTING a user perspective Sixth Canadian Edition Prepared by: Lynn de Grace C.A. Chapter 10 Long-Term Liabilities

-

Upload

edith-summers -

Category

Documents

-

view

217 -

download

2

Transcript of FINANCIAL ACCOUNTING a user perspective Sixth Canadian Edition Prepared by: Lynn de Grace C.A....

FINANCIAL ACCOUNTING a user perspective

Sixth Canadian Edition

Prepared by: Lynn de Grace C.A.

Chapter 10Long-Term Liabilities

User Relevance

WHAT ARE THE KEY ISSUES?

1.Maturity dates and interest rates of debt:- cash flows must be planned to meet maturity dates and interest payments

- companies commonly replace old debt with new debt;

- high interest rates are detrimental to profitability ratios.

2.Existence of Debt Covenants:- These are special conditions attached to the debt, such as a requirement to maintain a certain ratio of debt to equity or level of retained earnings;

- failure to comply may result in debt becoming due immediately.

John Wiley & Sons Canada, Ltd. ©2011

2

User Relevance

3. Proportion of debt to equity

- Higher debt means greater risk – cash flows must be used at maturity,

- Replacing old debt with new debt may only be possible at higher interest rates;

- Can make lenders reluctant to extend further debt;

- Too much debt results in lower financial leverage and ultimately less shareholder wealth.

4. Is the company using leverage to the advantage of its shareholders ?- This means earning a rate of return on investment that is higher than the cost of debt?

John Wiley & Sons Canada, Ltd. ©2011

3

Long-Term Notes & Mortgages Various markets from which a company

can obtain long term financing Examples:

• Commercial bank loans• often contain conditions or restrictions known

as covenants• Commercial paper – a promissory note sold

to another business• only used by companies with high credit ratings

John Wiley & Sons Canada, Ltd. ©2011

4

Long-Term Notes & Mortgages

Long-term loans with equal blended monthly payments:• Mortgage loans – capital asset is pledged as collateral• Usually structured as instalment loans• Payments are blended – consisting of both interest and

principal• Loan amortization table is usually prepared showing the

allocation of interest and principal payments for the duration of the loan.

John Wiley & Sons Canada, Ltd. ©2011

5

Long-Term Notes & Mortgages

Long-term loans with equal blended monthly payments:

EXAMPLE:

A company that takes out a three-year, $100,000 mortgage on September 30. The interest rate on the loan is 6% per year, and equal blended payments of $3,042.19 are to be made at the end of each month.

Sept 30 Cash 100,000Mortgage payable 100,000

John Wiley & Sons Canada, Ltd. ©2011

6

Long-Term Notes & Mortgages

Long-term loans with equal blended monthly payments:

To record the first three payments:

Oct 31 Interest expense 500.00Mortgage payable 2,542.19

Cash 3042.19

Nov 30 Interest expense 487.29Mortgage payable 2,554.90

Cash 3042.19

Dec 31 Interest expense 474.51Mortgage payable 2,567.68

Cash 3042.19

John Wiley & Sons Canada, Ltd. ©2011

7

Long-Term Notes & Mortgages

Long-term loans with interest only monthly payments:

Oct 31 Cash 100,000.00 Mortgage payable 100,000.00

Oct 31 Interest expense 500.00 Cash 500.00

Nov 30 Interest expense 500.00 Cash 500.00

Dec 31 Interest expense 500.00 Cash 500.00

John Wiley & Sons Canada, Ltd. ©2011

8

Bonds

John Wiley & Sons Canada, Ltd. ©2011

Companies may raise long-term funds through either:

• Equity (stock) market

OR

• Debt market• Borrow money from a commercial bank• Sell bonds to investors

9

Bond Characteristics

John Wiley & Sons Canada, Ltd. ©2011

Formal agreement called an indenture agreement.

Specifies• How the money is to be paid back• Conditions that must be met during the

period of the loan• Stated in the indenture agreement• May specify restrictions (debt covenants)

10

Bond Characteristics

John Wiley & Sons Canada, Ltd. ©2011

Bonds traded in public markets are standardized, stating:• Face value: $1,000 per bond

• Specifies the cash payment to be made at the maturity date of the bond

• Usually semi-annual interest payments• Bond interest rate

• Stated as an annual percentage

11

Bond Characteristics

John Wiley & Sons Canada, Ltd. ©2011

Mortgage bond• Has real property as collateral

Collateral trust bond• Provides shares and bonds of other

companies as collateral Debenture bond

• Carries no specific collateral• Senior debenture bonds• Subordinated debenture bonds

12

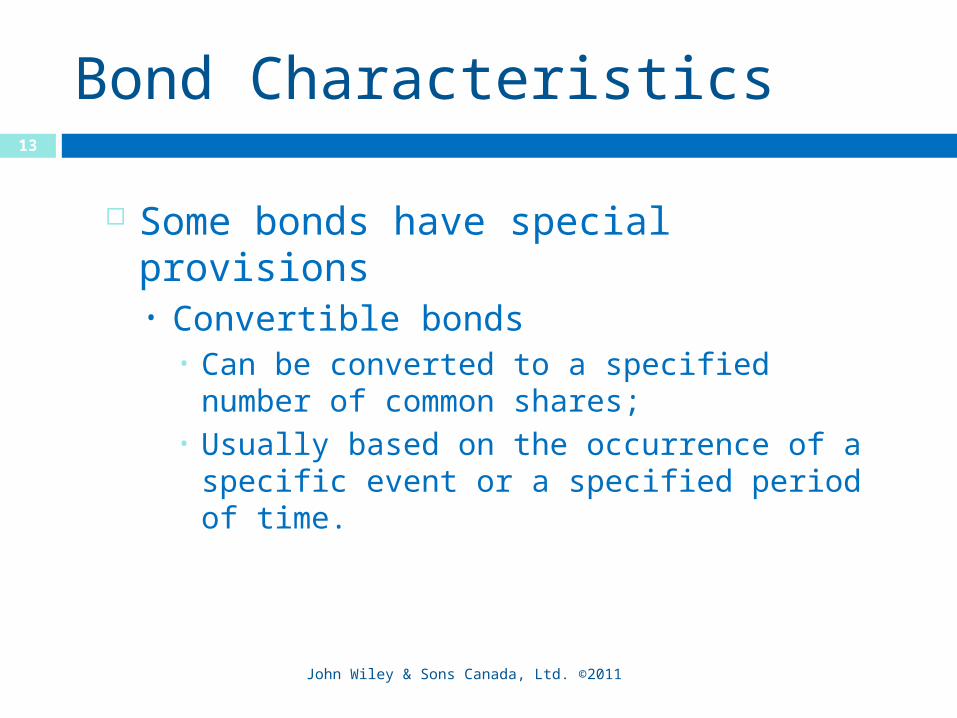

Bond Characteristics

John Wiley & Sons Canada, Ltd. ©2011

Some bonds have special provisions• Convertible bonds

• Can be converted to a specified number of common shares;

• Usually based on the occurrence of a specific event or a specified period of time.

13

Bond Pricing

John Wiley & Sons Canada, Ltd. ©2011

Market price of bonds is determined by discounting two sources of future cash flows:

Repayment of principal – present value of a single sum

PLUS

Periodic interest payments – present value of a series of payments

14

Bond Pricing

John Wiley & Sons Canada, Ltd. ©2011

Example: On December 31, 2011 a company issues bonds

with a total face value of $100,000, a bond interest rate of 8%, maturing on December 31, 2014.

The company expects the investor to demand a return of 10% (the risk-adjusted market rate) compounded semi-annually from this type of investment.

AT WHAT PRICE WILL THE BONDS BE ISSUED ?

15

Bond Pricing

Preliminary calculation: The cash flows must be discounted using the yield

rate* of 10%*Often called the discount rate or market rate

• Number of periods = Time to maturity x 2 = 3 years x 2 = 6 periods

• Yield rate per period = Yield rate ÷ 2 = 10% ÷ 2 = 5% per period

• Interest payments = Face amount x coupon rate x 6/12 = $100,000 x 8% x 6/12 = $4,000

John Wiley & Sons Canada, Ltd. ©2011

16

Bond Pricing

Summary of key data:• Face value 100,000• Bond interest rate* 8%• Time to maturity 3 years• Yield rate 10%• Semi-annual yield rate 5%• Semi-annual interest payments $4,000• Number of semi-annual periods 6 *often referred to as the coupon rate

John Wiley & Sons Canada, Ltd. ©2011

17

Bond Pricing

Calculation:Present value of the interest payments (an

annuity):$4,000 x 5.07569* = 20,302.76*present value interest factor of an annuity in

arrears for 6 periods at 5%PLUSPresent value of the principal sum:($100,000 x 0.74622) = 74,622.00= $20,302.76 + $74,622.00 = $94,924.76 = $94,924.76 Bond is issued at a discount

John Wiley & Sons Canada, Ltd. ©2011

18

Bond Pricing

WHAT IF THE COMPETITIVE INTEREST RATE IN THE MARKET IS 6% ?

If the buyers demand a 6% return on their investment:

PV of bond = PV of interest payments + PV of maturity payment

= PV of annuity of $4,000 for 6 periods at 3% + PV of $100,000 for 6 periods at 3%

= ($4,000 x 5.41719) + ($100,000 x 0.83748) = $105,416.76 Bond is issued at a premium.

John Wiley & Sons Canada, Ltd. ©2011

19

Bond Price Relationship

John Wiley & Sons Canada, Ltd. ©2011

Coupon Rate Bonds Issued at:

• Higher than expected yield Premium

• Lower than expected rateDiscount

• Equal to expected yield Par

20

Bond Price Relationship

Yield Rates

Coupon Rates

6% 8% 10% 12%

6% $1,000.00 $963.70 $929.08 $896.05

8% $1,037.17 $1,000.00 $964.54 $930.70

10% $1,074.34 $1,036.30 $1,000.00 $965.35

12% $1,111.51 $1,072.60 $1,035.46 $1,000.00

John Wiley & Sons Canada, Ltd. ©2011

Bonds Issued at Par

John Wiley & Sons Canada, Ltd. ©2011

Bonds issued at par are said to be issued at 100.

Cash (A) 1,000Bonds Payable (L) 1,000

Because interest accrues as time passes, no interest is recognized on the date of issuance

22

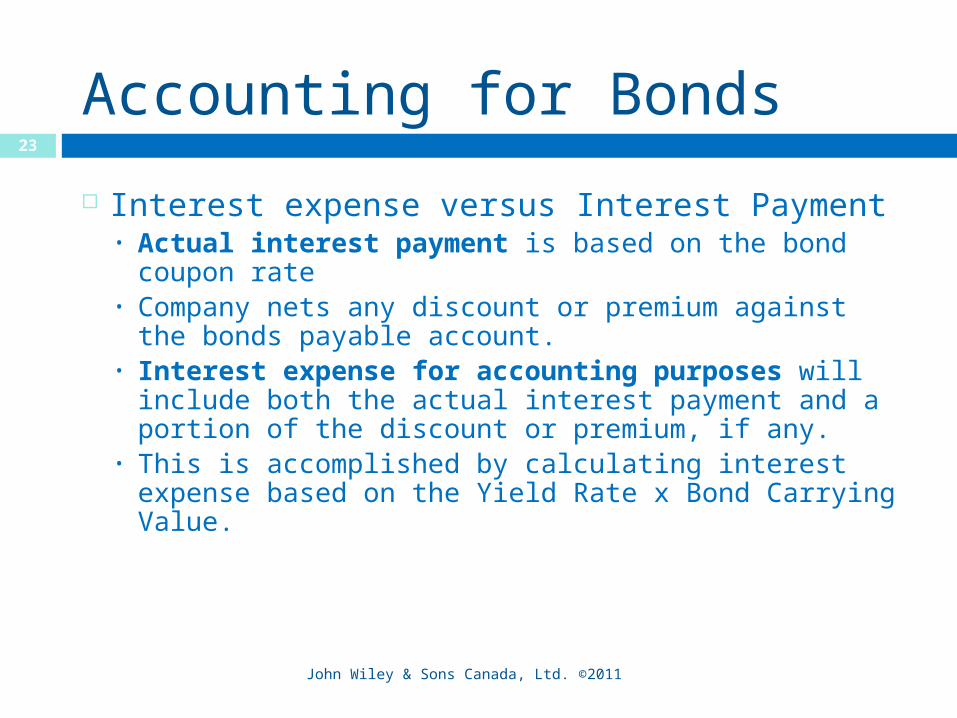

Accounting for Bonds

John Wiley & Sons Canada, Ltd. ©2011

Interest expense versus Interest Payment• Actual interest payment is based on the bond

coupon rate• Company nets any discount or premium against

the bonds payable account.• Interest expense for accounting purposes

will include both the actual interest payment and a portion of the discount or premium, if any.

• This is accomplished by calculating interest expense based on the Yield Rate x Bond Carrying Value.

23

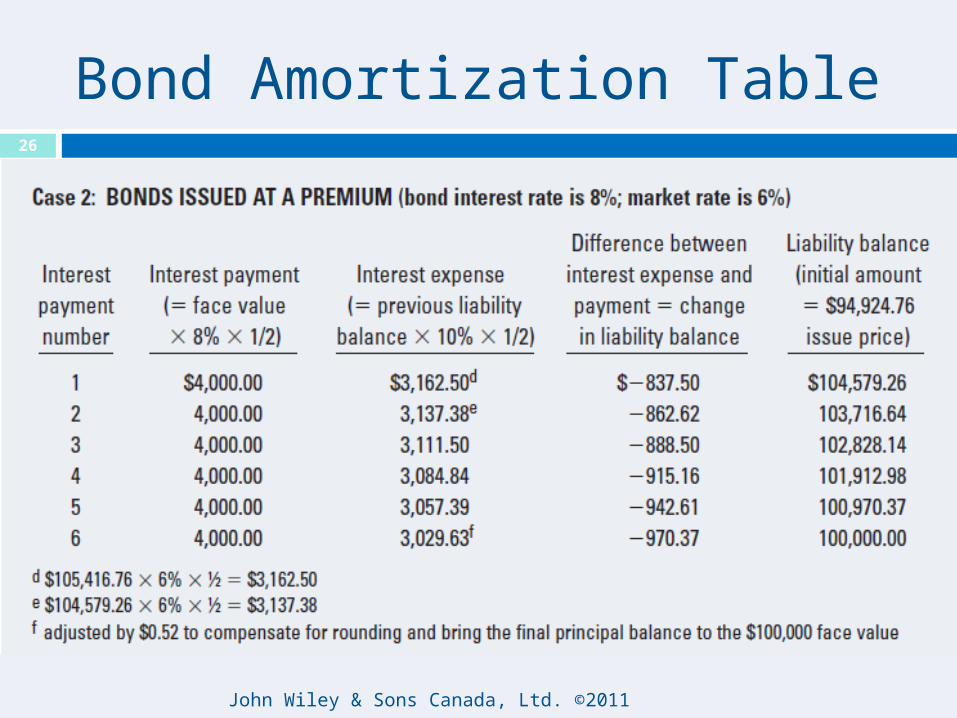

Bond Amortization Table

John Wiley & Sons Canada, Ltd. ©2011

24

Accounting for Bonds

John Wiley & Sons Canada, Ltd. ©2011

Case 1 Bonds Issued at a Discount:Issue date:

Cash (A)94,924.76Bond liability (L) 94,924.76

First interest payment:Interest expense (SE) 4,746.24

Bond liability (L) 746.24Interest payable (L) 4,000.00

Second interest payment:Interest expense (SE) 4,783.55

Bond liability (L) 783.55Interest payable (L) 4,000.00

25

Bond Amortization Table

John Wiley & Sons Canada, Ltd. ©2011

26

Accounting for Bonds

John Wiley & Sons Canada, Ltd. ©2011

Case 2 Bonds Issued at a Premium:Issue date:

Cash (A)105,416.76Bond liability (L) 105,416.76

First interest payment:Interest expense (SE) 3,162.50Bond liability (L) 837.50

Interest payable (L) 4,000.00Second interest payment*:

Interest expense (SE) 3,137.38Bond liability (L) 783.55Interest payable (L) 4,000.00

(*Difference due to rounding)

27

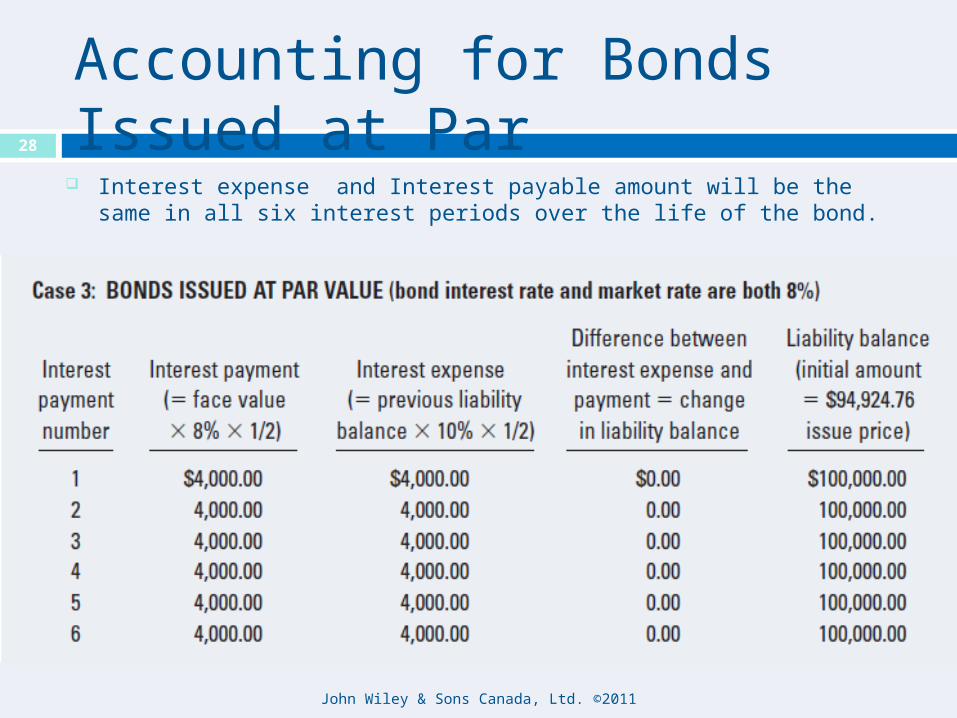

Accounting for Bonds Issued at Par

John Wiley & Sons Canada, Ltd. ©2011

Interest expense and Interest payable amount will be the same in all six interest periods over the life of the bond.

28

Early Retirement of Debt

Sometimes makes sense to pay off debt early Callable bonds – a feature that allows the

company to buy them back at a predetermined price before maturity

Usually a gain or loss will arise because the price paid to retire the bonds differs from their carrying value.

John Wiley & Sons Canada, Ltd. ©2011

29

WestJetLong Term Debt Note

Long Term Debt with No Explicit Interest Often, long term assets are purchased under arrangements

whereby interest expense is not explicitly stated in the loan agreement.

Loan agreement specifies the amounts and timing of the payments

If payment is not due until a later period, more appropriate to record the initial debt at present value.

Present value represents the true value of the asset at the time of purchase if the company does not have to pay for it until later.

The appropriate discount rate should be the rate at which the company would have to borrow to buy the asset.

Interest expense is calculated each period using the discount rate times the carrying value of the debt.

John Wiley & Sons Canada, Ltd. ©2011

30

Long Term Debt with No Explicit Interest

EXAMPLE: A company negotiates the purchase of some equipment for $100,000, which is to be paid at the end of three years with no interest added. The company would normally have been charged an interest rate of 6% annually for a three-year loan.PVIF 6%, 3 = 0.83962

Purchase Date:Equipment 83,962

Long term note payable 83,962

First year’s interest expense:Interest expense 5,038

Long term note payable 5,038[$83,962 x 6% = 5,038]

John Wiley & Sons Canada, Ltd. ©2011

31

Leases

John Wiley & Sons Canada, Ltd. ©2011

What is a lease agreement?

One party (the lessor) buys the asset and the second party (the lessee) makes periodic payments in exchange for the use of the asset over the lease term.

32

Owning Versus Leasing

John Wiley & Sons Canada, Ltd. ©2011

Ownership pros: Company can use the CCA to reduce income

taxes. Investment tax credits may also be available

Benefits from the increase in value of the asset

Ownership cons: Ties up capital that could have been used for

something else Financing the assets will negatively impact

debt ratios and interest coverage ratios.

33

Owning Versus Leasing

John Wiley & Sons Canada, Ltd. ©2011

Leasing: Favourable terms can mean a low cost form of financing Frees up capital for other purposes Not necessary to incur debt – less impact on debt ratios Lowers lessee’s risk that the asset will become obsolete Lessee may opt to use the asset for less than its useful

life.

34

Classification of Leases

John Wiley & Sons Canada, Ltd. ©2011

OPERATING LEASE:• If the lease term is a relatively short period of time

compared to the life of the assets, then:• Lessee is not buying, but renting the asset• Payments are recorded as rent expense CAPITAL/FINANCE LEASE:• Lease is for a major part of the asset’s useful life• Lease is effectively a financing arrangement with

installments• Asset is recorded at its cost – measured at the

present value of the future lease payments;• Obligation to the lessor is recorded as a non-current

liability and interest is recognized over the term of the lease.

35

Classification of Leases

John Wiley & Sons Canada, Ltd. ©2011

A lease qualifies as a capital/finance lease if any one of the following criteria is met:

1.The lease transfers ownership of the asset to the lessee by the end of the lease term;2.The lessee has a “bargain purchase” and it is reasonably certain that this “bargain purchase option” will be exercised;3.The lease term is for the major part of the asset’s economic life;4.The present value of the minimum lease payments is equal to substantially all of the fair value of the asset;5.The leased asset is of such a specialized nature that, without major modifications, only the lessee can use it.

36

Accounting For Leases

John Wiley & Sons Canada, Ltd. ©2011

Example:

• Asset is leased for 3 years• Monthly lease payments of $1,000, payable

at the end of each month• Interest rate is 12%

Under an operating lease, the monthly journal entry is:

Equipment rental/lease expense (SE) 1,000Cash (A) 1,000

37

Accounting For Leases

John Wiley & Sons Canada, Ltd. ©2011

Under a capital/finance lease:• Asset and liability are recorded at present

value Key data:

• 36 periods, 1% per periodPVIFA1%, 36 = 30.10751

Journal entry to record lease transaction:Leased equipment (A) 30,107.51

Lease obligation (L)30,107.51

38

Accounting For Leases

John Wiley & Sons Canada, Ltd. ©2011

Capital/finance lease (cont’d): At the end of the first month:

Interest expense (SE) 301.08Lease obligation (L) 698.92

Cash (A) 1,000.00[Interest = 1% x 30,107.51]

At the end of the second month:Interest expense (SE) 294.09Lease obligation (L) 705.91

Cash (A) 1,000.00[Interest = 1% x (30,107.51-698.92)]

39

Accounting For Leases

John Wiley & Sons Canada, Ltd. ©2011

Capital/finance lease (cont’d): Assuming straight-line amortization

over 36 months At the end of each month:Depreciation expense (SE) 836.32

Accumulated depreciation (XA) 836.32 - leased equipment

40

Pensions

John Wiley & Sons Canada, Ltd. ©2011

Agreements between employers and employees that provide employees with specified benefits (income) upon retirement

Represents an estimated future obligation for the services that the employee is rendering to the company presently,

Makes sense to include the costs of this obligation in the same period as the benefits received

41

Pensions

John Wiley & Sons Canada, Ltd. ©2011

Defined contribution pension plans:• Employer agrees to make a pre-defined

contribution to a retirement fund for the employee.

• Risk of increases or decreases to the plan’s market value is borne by the employee.

• Pension expense is generally equal to the contribution.

42

Pensions

John Wiley & Sons Canada, Ltd. ©2011

Defined benefit pension plans:• Employee is guaranteed a certain amount of money

during each year of retirement.• Risk of increases or decreases to the plan’s market

value is borne by the employer.• Employer must continually assess plan assets to

determine if the current contributions to the plan will be sufficient to meet the future obligation.

• Pension obligation is determined as the present value of the future obligation.

• Pension expense consists of both the current pension expense (determined by an actuary) plus/minus any adjustments or contributions required to fund plan assets in order to meet the present value of the future obligation.

43

Pension Plan Disclosure

For a defined contribution plan, the contributed amounts must be disclosed.

For a defined benefit plan disclosure is usually extensive and can be complex.• Generally, in order to determine whether

the pension plan is underfunded, overfunded, or fully funded, it is necessary to read the notes to the financial statements

John Wiley & Sons Canada, Ltd. ©2011

44

Deferred Income Taxes

Basic Concepts:• Income tax expense is an accrual

accounting concept since it is based on accounting income from the income statement

• Income taxes payable must be calculated according to the rules established by Canada Revenue Agency (CRA)

• Difference is deferred income tax – it can be either an asset or a liability, depending on the cause of the difference.

Canadian practice uses the liability method to account for these differences.

45

John Wiley & Sons Canada, Ltd. ©2011

Deferred Income Tax - Liability Method

A calculation of the income tax that will be payable in the future or deductible in the future, based on the temporary differences (the differences between the accounting records and the tax records) that exist in the current period.

46

John Wiley & Sons Canada, Ltd. ©2011

Deferred Income Tax - Liability Method

EXAMPLE - Warranties For accounting purposes, the company estimates

the probable costs associated with the warranty and records the total amount as warranty expense in the year of the sale, as well as a liability (warranty obligation). For tax purposes, the CRA does not permit a company to deduct the estimated warranty expense in calculating its taxable income; the company can only claim a tax deduction for the actual costs that it incurs each year to settle claims under the warranty.

47

John Wiley & Sons Canada, Ltd. ©2011

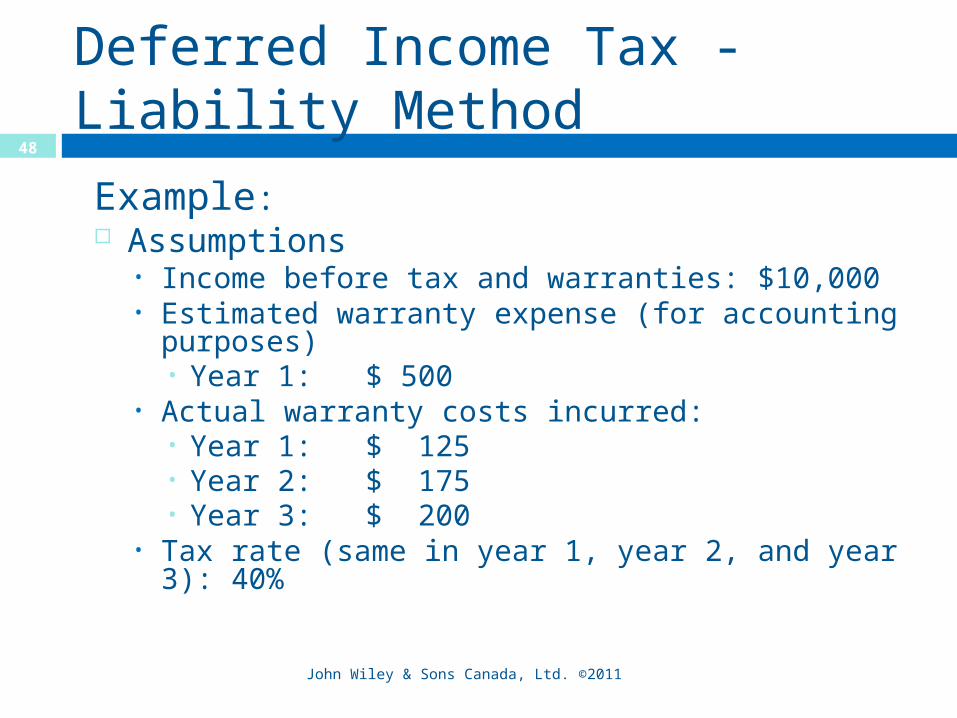

Deferred Income Tax - Liability Method

Example: Assumptions

• Income before tax and warranties: $10,000• Estimated warranty expense (for accounting

purposes)• Year 1: $ 500

• Actual warranty costs incurred:• Year 1: $ 125• Year 2: $ 175• Year 3: $ 200

• Tax rate (same in year 1, year 2, and year 3): 40%

48

John Wiley & Sons Canada, Ltd. ©2011

Deferred Income Tax - Liability Method

Year 1 Year 2 Year 3

Income before warranty expense & income taxes

10,000 10,000 10,000

Actual warranty costs incurred

(125) (175) (200)

Taxable income 9,875 9,825 9,800

40% 40% 40%

Taxes payable $3,950 $3,930 $3,920

Income tax currently payable:

John Wiley & Sons Canada, Ltd. ©2011

49

Deferred Income Tax - Liability Method

Year 1 Year 2 Year 3

Beginning warranty obligation

$ 500 $ 375 $ 200

Actual warranty costs incurred

125 175 200

Ending warranty obligation (Temporary difference)

$ 375 $ 200 $ -0-

Tax rate 40% 40% 40%

Deferred tax asset $ 150 $ 80 $ -0-

Increase (decrease) in deferred tax asset

$ 150 ( $70) ( $80)

Calculation of deferred income taxes:

John Wiley & Sons Canada, Ltd. ©2011

50

Deferred Income Tax - Liability Method

Year 1 Year 2 Year 3

Income taxes payable (3,950) (3,930) (3,920)

Future income taxes 150 (70) (80)

Income tax expense $3,800 $4,000 $4,000

Calculation of income tax expense:

51

John Wiley & Sons Canada, Ltd. ©2011

Income Tax Disclosures

Reconciliation of the difference between the tax expense reported on the income statement and the amount that would have been reported if all revenues, expenses, gains, and losses were subject to tax at the stated tax rates

Summary of the temporary differences creating the deferred income tax amounts

Breakdown of the taxes into the amounts that are currently payable and the amounts that are deferred to the future

52

John Wiley & Sons Canada, Ltd. ©2011

West Timber Lumber Co.Income Tax Note

Statement Analysis

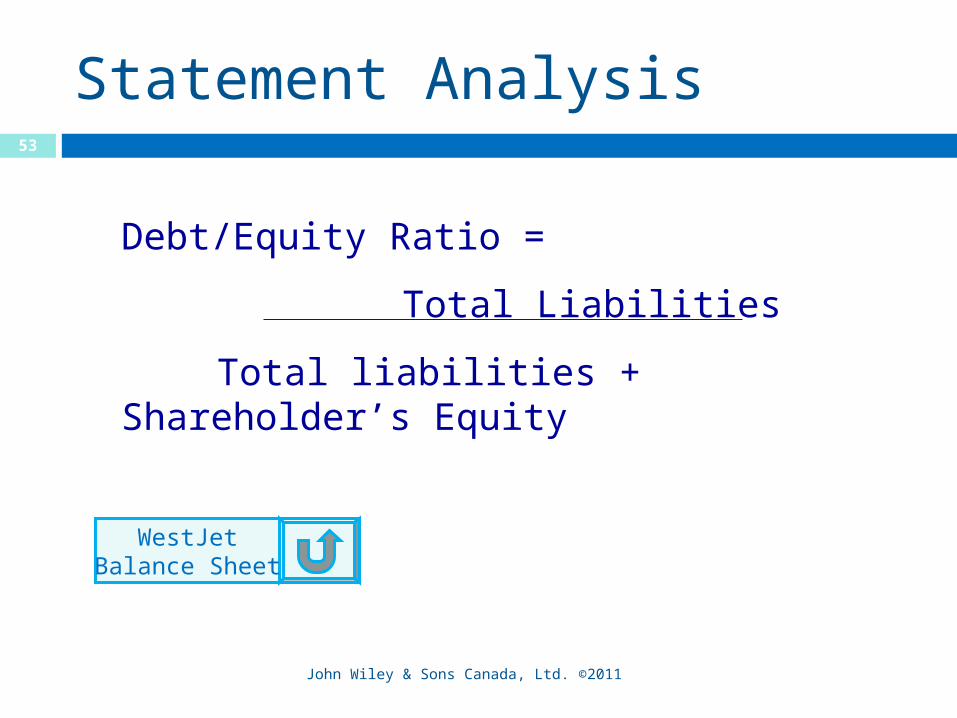

John Wiley & Sons Canada, Ltd. ©2011

Debt/Equity Ratio =

Total Liabilities

Total liabilities + Shareholder’s Equity

53

WestJetBalance Sheet

Statement Analysis

John Wiley & Sons Canada, Ltd. ©2011

54

WestJet Debt to Equity Ratio:

Times-Interest-Earned Ratio

John Wiley & Sons Canada, Ltd. ©2011

Times- interest- earned

Income before interest and taxes

Interest=

=Net income + Taxes + Interest Interest

55

WestJetIncome Statement

Times-Interest-Earned Ratio

John Wiley & Sons Canada, Ltd. ©2011

56

WestJet Times Interest Earned Ratio:

Copyright © 2011 John Wiley & Sons Canada, Ltd. All rights reserved. Reproduction or translation of this work beyond that permitted by Access Copyright (The Canadian Copyright Licensing Agency) is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons Canada, Ltd. The purchaser may make back-up copies for his / her own use only and not for distribution or resale. The author and the publisher assume no responsibility for errors, omissions, or damages, caused by the use of these programs or from the use of the information contained herein.

Copyright57