Financial Accountability Budgetary Considerations.

19

Financial Accountabil ity Budgetary Considerations

-

Upload

emiliano-pooler -

Category

Documents

-

view

221 -

download

0

Transcript of Financial Accountability Budgetary Considerations.

Financial Accountability

Budgetary Considerations

Today’s Objectives

Increased accountability and scrutiny

How can we help you!?!

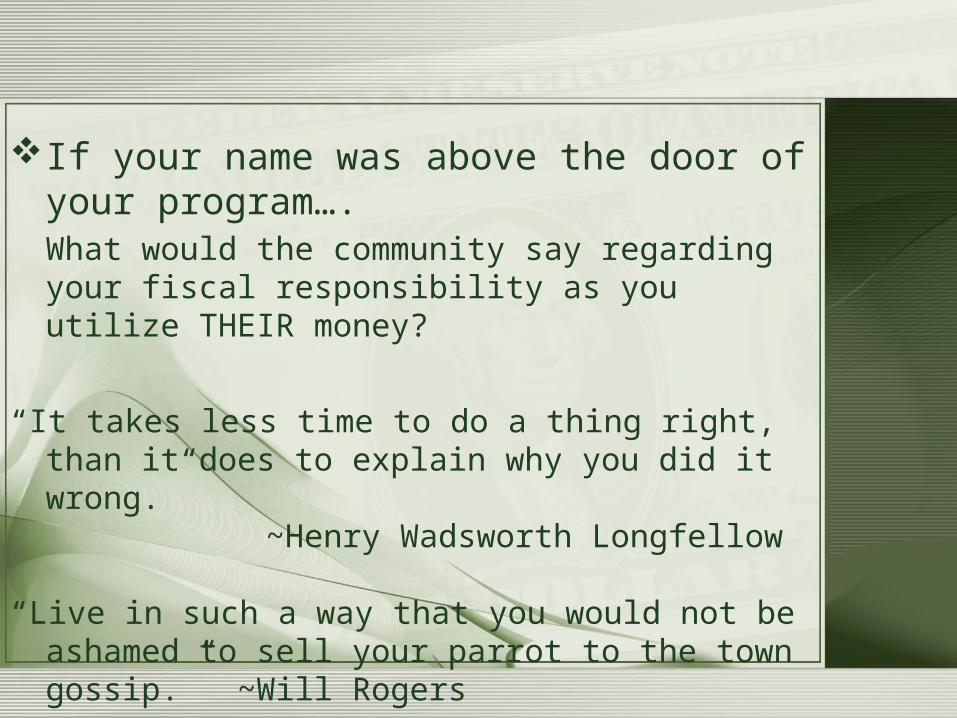

If your name was above the door of your program….What would the community say regarding your fiscal responsibility as you utilize THEIR money?

“It takes less time to do a thing right, than it does to explain why you did it wrong.”

~Henry Wadsworth Longfellow

“Live in such a way that you would not be ashamed to sell your parrot to the town gossip.” ~Will Rogers

Lack of Accountability or Mismanagement

Effectiveness

Remember your resourcesEDGARYour manualYour websiteYour Technical AdvisorOne anotherMarkMe, Chris or JessYour CSFO (more to come on that!)

We’ve got the money ~ Now what?!?!

Complete familiarity and awareness of the initial stipulations and parameters of the grant

Decisions cannot be made outside the intent of the purpose for which the grant was obtained.

Do not rely on the competency of others (CSFO’s, Superintendents, etc.) to navigate through the financial matters of the grant.

You are responsible!!!!

Allowable

Non - Allowable

Basis for Allowable Costs

According to the law, all costs must be – Necessary Reasonable Allocable Legal under all federal, state

and local laws

Just because it’s allowable doesn’t mean it’s prudent nor approvable!

Necessary☼A cost is necessary if –

Needed for the performance or administration of your grant

Follows sound business practices Reflects fair market prices for comparable

goods or services Do I really need this to administer the

program? Is this the minimum/maximum amount

needed to meet the needs of the students?

Reasonable• Is this cost targeted to valid

programmatic/administrative considerations?• Does our program have the sustainable

capacity to use what we are purchasing for this program?

• Did we pay a fair market rate and can we prove it?

• If this expense were in the local newspaper ‘HEADLINES,’ would I be comfortable or completely embarrassed?

AllocableWhat does that mean?!?!?

Is everything properly allocated and accounted for, and can we prove the program benefited

accordingly? Are we within the appropriate % parameters for

Administrative functions, Indirect Costs, Travel, External Evaluator, Professional Development?

Services Rendered(Contracts and Compensation) Are all expenditures (supplies, materials, hardware, software, etc.) correctly recorded and

trackable?

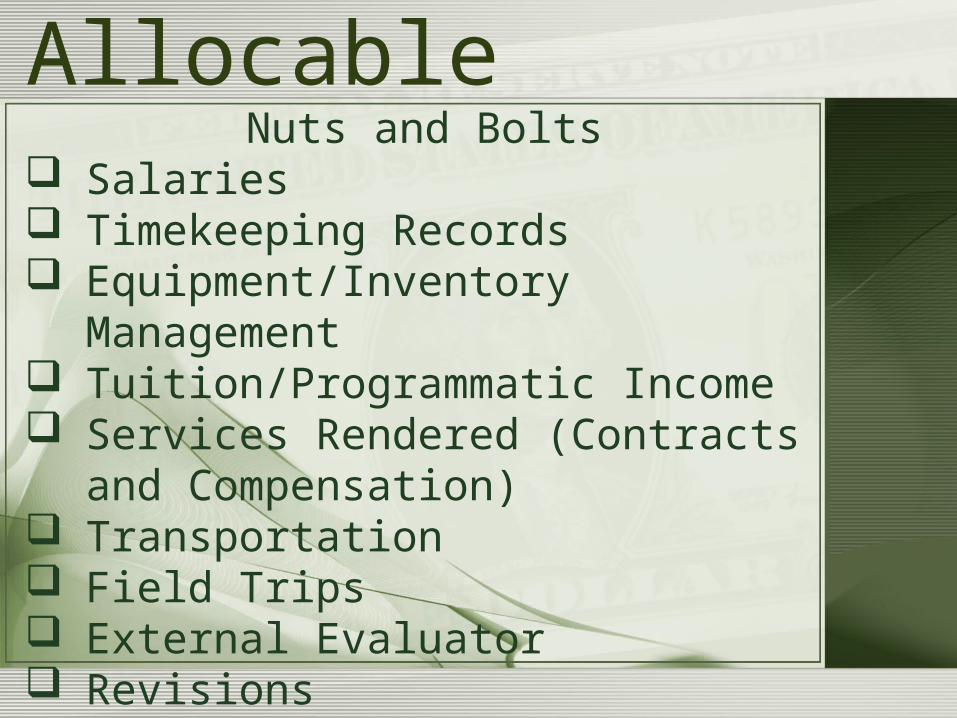

AllocableNuts and Bolts

Salaries Timekeeping Records Equipment/Inventory Management Tuition/Programmatic Income Services Rendered (Contracts and

Compensation) Transportation Field Trips External Evaluator Revisions

Allocable• Collaboration and Cooperation Can we prove through thorough

documentation how we are effectively supporting the program with the cooperation of funding?

Narrative explanation ensuring the co-existing and coordination of funds, authorized usage, incidental benefits, etc.

AVOID at all cost….the appearance of impropriety, conflict of interest, and lack of accountability!

The Sandbox

Help?!?!?!?!?!?!?!?!?!?!?!?!?!

Your assigned consultant Mark Yolanda Chris

[email protected] / 334.844.5781 Me (Paul)

[email protected] / 404.694.0436 CBO’s/FBO’s – Tina Heartsill at

CBO’s For the purposes of budgetary and financial accountability of

Community Based Organizations (CBO's), all expenses incurred with the utilization of 21st CCLC funding must be well documented and maintained.

The following are examples of documentation which must be maintained and submitted to the Alabama State Department of Education (ALSDE):

InvoicesReceiptsPurchase OrdersInventory RecordsCopies of all Payroll recordsTravel claims and expensesSub-contract Agreements and payments

**Anything purchased or paid out 21st CCLC funding must be documentable and traceable.**

Practical Advise?!

Questions/Concerns?!?