Finance Submission 02

86

Summer Internship Report Import Export Financing : IPCA Laboratories Ltd. From:- 2 nd May,2013 to 30 th June,2013 Submitted by, Prathamesh Gharat PGDM 2012-2014 Thakur Institute of Management Studies & Research Thakur Institute of Management Studies and Research Page 1

-

Upload

prathamgharat019 -

Category

Documents

-

view

12 -

download

0

Transcript of Finance Submission 02

Summer Internship

Report

Import Export Financing : IPCA Laboratories

Ltd.

From:- 2nd May,2013 to 30th June,2013

Submitted by,

Prathamesh Gharat

PGDM 2012-2014

Thakur Institute of Management Studies & Research

Thakur Institute of Management Studies and Research Page 1

Acknowledgement

The satisfaction and euphoria that accompanies the successful completion of any task would

be incomplete without mentioning the names of the people who made it possible, whose

constant guidance and encouragement crown all the efforts with success.

I take this opportunity to express my profound gratitude to Mr. Prakash Nayak, General

Manager, Ipca Laboratories Ltd for his exemplary guidance, monitoring and constant

encouragement throughout the training. The blessing, help and guidance given by him time to

time shall carry me a long way in the journey of life on which I am about to embark.

I also take this opportunity to express a deep sense of gratitude to Ms. Jigna Modha, Mr.

Mithilesh Singh & Mr. Rajesh Thakkar for their cordial support, valuable information and

guidance, which helped me in completing this task through various stages.

I am obliged to all other colleagues at Ipca laboratories Ltd, for the valuable information

provided by them in their respective fields. I am grateful for their cooperation during the

period of my assignment.

Thakur Institute of Management Studies and Research Page 2

Table of Contents

Executive Summary 04

Introduction 05

Indian pharmaceutical sector: Overview 06

Company Profile: Ipca Laboratories Ltd 08

Export 11

Import 37

Buyer’s Credit & Supplier’s Credit 50

Modes of Fund Transfer 54

Comparison between PCFC, Buyer’s Credit, Bill Discounting

and Supplier’s Credit 55

Thakur Institute of Management Studies and Research Page 3

Executive Summary

The global pharmaceutical market has grown at a fast pace over the past few years spurred

primarily by the North American market. However, there is a gradual movement towards

growth in the emerging markets, where availability of healthcare is expanding and there is an

increasing need for treatments associated with chronic diseases more typically found in

developed countries till date.

The countries that have shown most potential are Brazil, Russia, India, China and Turkey.

Although the current pharmaceutical market values in these countries are not impressive

compared to more mature markets, most of them are experiencing tremendous growth rates

compared to the modest 4-6% growth seen in the US and Europe.

India is one of the fastest growing economies of the world – it has posted an average growth

rate of more than 7% in the decade since 1996, reducing poverty by about 10%. The GDP

growth in 2007-8 was 8.5% backed by significant expansion in services and manufacturing.

This has resulted in high growth in a number of independent sectors, which are a reflection of

the spending power of the large and growing Indian middle class. The telecommunications

sector, media, FMCG sectors are a few to name so. However in these times of recession, one

such sector which has not beaten down is the pharmaceutical sector.

The objective of this report is to study the procedure of imports and exports in the

pharmaceutical industry and its financing methods. The report gives an overview of the

pharmaceutical industry globally and more specifically in India.

The report then gives a brief idea about Ipca Laboratories Ltd; one of the rising stars in the

Indian pharmaceutical sector. The report also mentions the general import and export process,

its financing and then proceeds to give a description about the process at Ipca Laboratories

Ltd. for imports, exports and financing of these.

Thakur Institute of Management Studies and Research Page 4

Introduction

The Pharmaceutical Industry in India is the world's third-largest in terms of volume and

stands 13th in terms of value. According to Department of Pharmaceuticals, Ministry of

Chemicals and Fertilizers, the total turnover of India's pharmaceuticals industry between

2008 and September 2009 was US$21.04 billion, while the domestic market was worth

US$12.26 billion. Sale of all types of medicines in the country is expected to reach around

US$20 billion by 2015.

Exports of pharmaceuticals products from India increased from US$6.23 billion in 2006-07

to US$8.7 billion in 2008-09 a combined annual growth rate of 21.25%. According to

PricewaterhouseCoopers (PWC) in 2010, India joined among the league of top 10 global

pharmaceuticals markets in terms of sales by 2020 with value reaching US$50 billion. Some

of the major pharmaceutical firms include Ranbaxy, Cipla, Sun, Cadila Healthcare and

Piramal Healthcare.

The government started to encourage the growth of drug manufacturing by Indian companies

in the early 1960s, and with the Patents Act in 1970. However, economic liberalization in the

1990s by the former Prime Minister P.V. Narasimha Rao and the then Finance Minister, Dr.

Manmohan Singh enabled the industry to become what it is today. This patent act removed

composition patents from food and drugs, and though it kept process patents, these were

shortened from a period of seven years to five years.

The lack of patent protection made the Indian market undesirable to the multinational

companies that had dominated the market, and while they streamed out. Indian companies

carved a niche in both the Indian and world markets with their expertise in reverse-

engineering new processes for manufacturing drugs at low costs. Although some of the larger

companies have taken baby steps towards drug innovation, the industry as a whole has been

following this business model until the present.

India's biopharmaceutical industry clocked a 17 percent growth with revenues of Rs.137

billion ($3 billion) in the 2009-10 financial year over the previous fiscal. Bio-pharmaceutical

was the biggest contributor generating 60 percent of the industry's growth at Rs.8,829 crore,

followed by bio-services at Rs.2,639 crore and bio-agri at Rs.1,936 crore.

Thakur Institute of Management Studies and Research Page 5

The Indian Pharmaceutical Industry

The Indian Pharmaceutical industry is highly fragmented with about 24,000 players (with

approximately 250 major players including 5 Central Public Sector units). The top ten

companies make up for more than a third of the market. The Indian pharmaceutical industry

(IPM) grew by 16% YoY in 2012 to Rs. 629 bn. It accounts for about 1.4% of the world's

pharmaceutical industry in value terms and 10% in volume terms.

Besides the domestic market Indian pharmaceutical companies also have a large chunk of

their revenues coming from exports. While some are focusing on the generics market in the

US, Europe and semi-regulated markets, others are focusing on custom manufacturing for

innovator companies. Biopharmaceuticals is also increasingly becoming an area of interest

given the complexity in manufacture and limited competition.

In 1970s, Indian pharmaceutical market was almost non-existent. But today, India has carved

a niche for itself in the pharmaceutical domain. In fact, it has grown into a big mart for the

Pharmaceutical Industry.

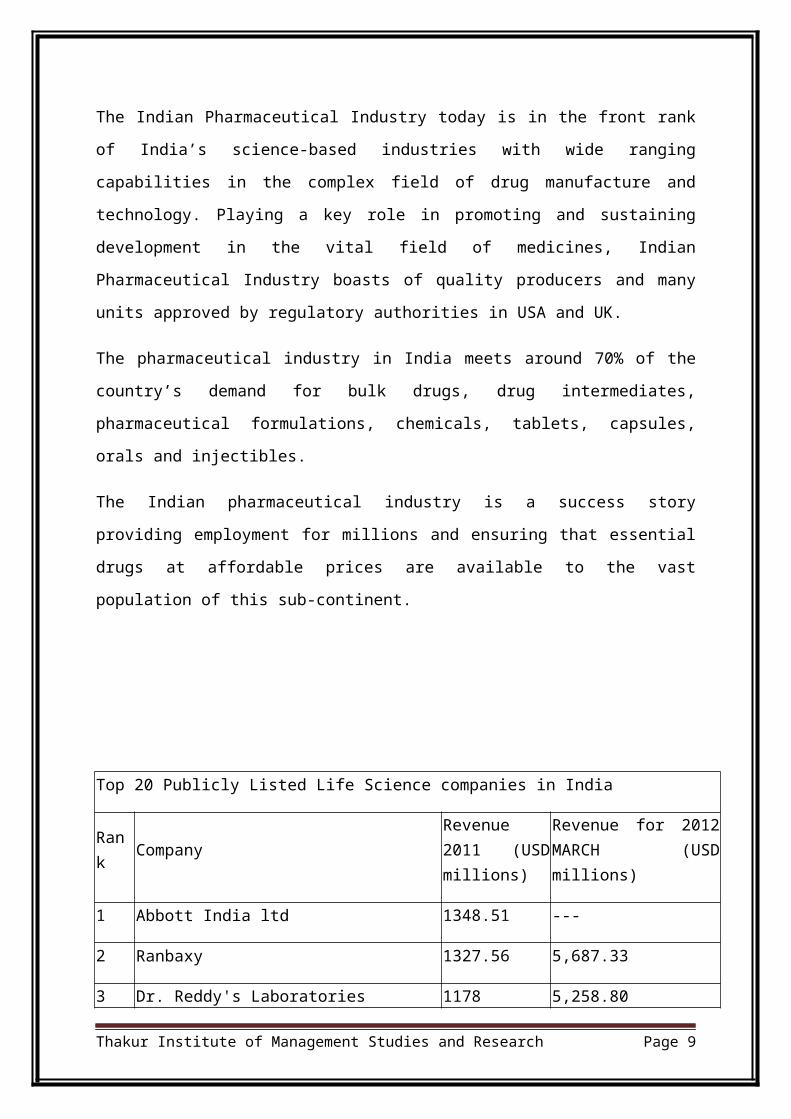

The Indian Pharmaceutical Industry today is in the front rank of India’s science-based

industries with wide ranging capabilities in the complex field of drug manufacture and

technology. Playing a key role in promoting and sustaining development in the vital field of

medicines, Indian Pharmaceutical Industry boasts of quality producers and many units

approved by regulatory authorities in USA and UK.

The pharmaceutical industry in India meets around 70% of the country’s demand for bulk

drugs, drug intermediates, pharmaceutical formulations, chemicals, tablets, capsules, orals

and injectibles.

The Indian pharmaceutical industry is a success story providing employment for millions and

ensuring that essential drugs at affordable prices are available to the vast population of this

sub-continent.

Thakur Institute of Management Studies and Research Page 6

Top 20 Publicly Listed Life Science companies in India

Rank CompanyRevenue 2011 (USD millions)

Revenue for 2012 MARCH (USD millions)

1 Abbott India ltd 1348.51 ---

2 Ranbaxy 1327.56 5,687.33

3 Dr. Reddy's Laboratories 1178 5,258.80

4 Lupin Ltd 929.84 4,527.12

5 Aurobindo Pharma 865.19 4,229.99

6 Dabur 700.3 ---

7 Sun Pharmaceutical 673.99 1,985.78

8 Cadila Healthcare 629.45 2,213.17

9 Jubilant Lifesciences 561.03 ---

10 Piramal Healthcare 480.26

11 GlaxoSmithKline Pharmaceuticals Ltd 475.8

12 Ipca Laboratories 390

13 Wockhardt 381.23

14 Torrent Pharmaceuticals 380.2

15 Sterling Bio 358.1

16 Biocon 340.38

17 Orchid Chemicals & Pharmaceuticals Limited 320.62

18 ALEMBIC PHARMACEUTICALS LIMITED 270.62

19 Aventis Pharma 263.75

20 Glenmark Pharmaceuticals 260.14

Source:

Company profile: Ipca Laboratories Ltd.

Thakur Institute of Management Studies and Research Page 7

Introduction

The Indian Pharmaceutical Combine Association Limited is a fully integrated

pharmaceuticals company producing branded and generic formulations, APIs and

Intermediates, and one of the leaders in anti-malarial and Rheumatoid Arthritis in the Indian

market; and the company has been expanding its therapeutic coverage, especially in the fast

growing life style related segments. Ipca's APIs and Formulations produced at world class

manufacturing facilities are approved by leading drug regulatory authorities including the

US-Food and Drug Administration (FDA), UK-Medicines and Healthcare products

Regulatory Agency (MHRA), South Africa-Medicines Control Council (MCC), Brazil-

Brazilian National Health Vigilance Agency (ANVISA) and Australia-Therapeutic Goods

Administration (TGA). With operations in over 120 countries, exports account for over 61%

of the company's income. IPCA is also among Top 10 Pharmaceutical exporter from India.

Forbes, a leading US business magazine, selected Ipca for 3 consecutive years– 2003, 2004,

2005 as one of the Best under a billion companies outside US. Forbes Inc. also selected Ipca

as one of the ‘Best under a Billion Forbes Global’s 200 Best Small companies’ in 2007. Over

19,000 companies were considered by Forbes, and of the 18 companies from India that

figured in this list, only four were from the 'Indian Pharmaceutical Sector'. Ipca happens to be

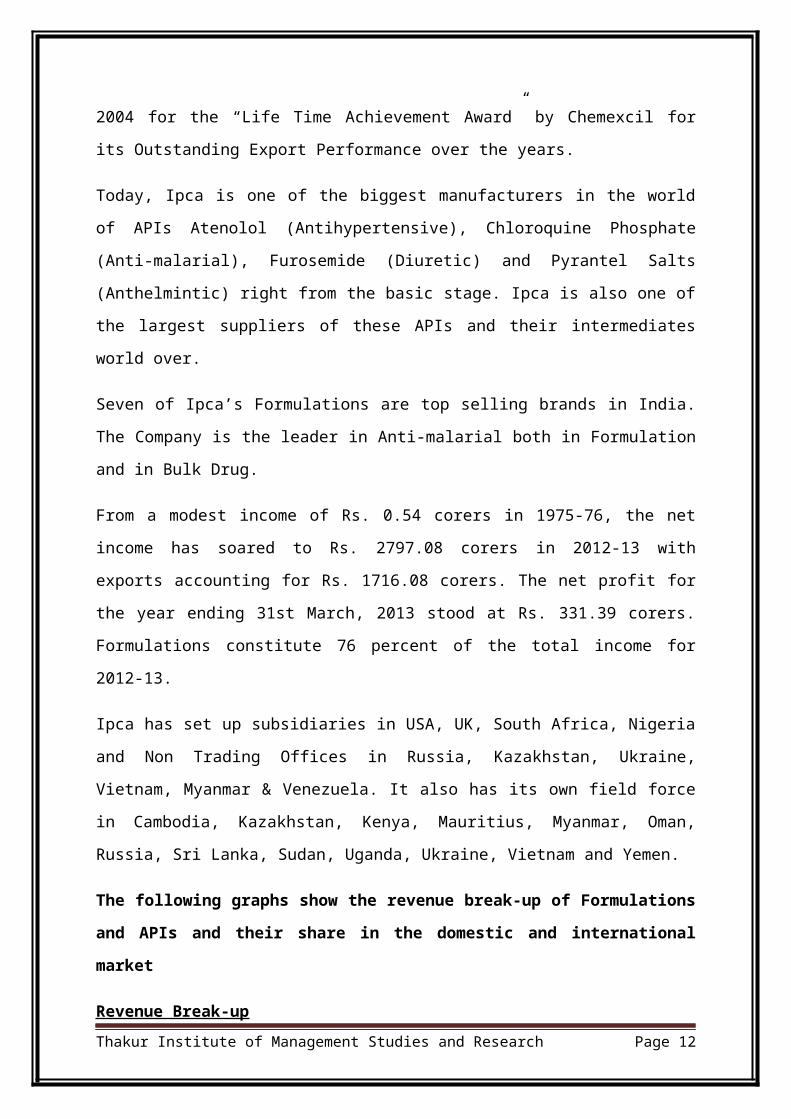

one of them. IPCA is a “Recognised Trading House.” Ipca has been selected in 2004 for the

“Life Time Achievement Award” by Chemexcil for its Outstanding Export Performance over

the years.

Today, Ipca is one of the biggest manufacturers in the world of APIs Atenolol

(Antihypertensive), Chloroquine Phosphate (Anti-malarial), Furosemide (Diuretic) and

Pyrantel Salts (Anthelmintic) right from the basic stage. Ipca is also one of the largest

suppliers of these APIs and their intermediates world over.

Seven of Ipca’s Formulations are top selling brands in India. The Company is the leader in

Anti-malarial both in Formulation and in Bulk Drug.

From a modest income of Rs. 0.54 corers in 1975-76, the net income has soared to Rs.

2797.08 corers in 2012-13 with exports accounting for Rs. 1716.08 corers. The net profit for

Thakur Institute of Management Studies and Research Page 8

the year ending 31st March, 2013 stood at Rs. 331.39 corers. Formulations constitute 76

percent of the total income for 2012-13.

Ipca has set up subsidiaries in USA, UK, South Africa, Nigeria and Non Trading Offices in

Russia, Kazakhstan, Ukraine, Vietnam, Myanmar & Venezuela. It also has its own field force

in Cambodia, Kazakhstan, Kenya, Mauritius, Myanmar, Oman, Russia, Sri Lanka, Sudan,

Uganda, Ukraine, Vietnam and Yemen.

The following graphs show the revenue break-up of Formulations and APIs and their

share in the domestic and international market

Revenue Break-up

2012-13

76%

24%

Total Revenue

FormulationsAPIs

61%

39%

Total Revenue

ExportsDomestic

70%

30%

Exports

FormulationsAPIs

86%

14%

Domestic

FormulationsAPIs

Source:

History

Thakur Institute of Management Studies and Research Page 9

One of the first modern pharmaceutical factories of yesteryears was commissioned by Ipca at

Mumbai in 1969. The company was originally promoted by a group of medical professionals

and businessmen and was incorporated as “The Indian Pharmaceutical Combine Association

Limited in October 1949. The present management took over in November 1975 when the

total turnover of the company was just Rs. 0.54 crores

Products

Ipca offers products in two categories:

Formulations

Active pharmaceutical ingredients & intermediates

Formulations

Being one of the largest pharmaceutical company in India today, Ipca manufactures over 350

formulations representing various therapeutic segments and dosage forms. The dosage form

includes tablets, capsules, oral liquids, dry powders for suspension, and injectibles (liquid &

dry). Some of these formulations are manufactured for many leading companies in the

European Union under supply agreements.

Active Pharmaceutical Ingredients

Ipca produces over 80 API’s for various therapeutic segments. It is one of the world’s largest

manufacturers and suppliers of over a dozen APIs. For over 20 years, Ipca has been playing a

lead role in the Indian APIs market, both in the anti-malarial and anti-hypertensive

therapeutic segments. It is the first manufacturer in India for APIs like Atenolol,

Hydroxycholoquine Sulphate, Morantel Citrate, Pyrantel Pamoate and Zaltoprofen.

Export Procedure & Export Finance

Thakur Institute of Management Studies and Research Page 10

Ipca has its operations in over 120 countries, and thus there is bound to be cross-border

transactions involving export and import of drug raw materials, formulations, finished

products etc. Exports at Ipca account for over 61% of the company’s income.

Exports:

The major income of Ipca group of companies comes from exports, contributing to about

61% of the turnover, export earning being about Rs 1716.08 crores. It exports to about 120

countries all over the world. It has a wide infrastructure for exports with offices opened in

different strategic locations, which provide the much needed support and impetus in

increasing the exports. Ipca has been a net foreign exchange earner for last several years (i.e.

where exports > imports). Ipca’s products are marketed to leading pharmaceutical and

chemical manufacturers worldwide including reputed multinationals in USA, UK, France,

Germany and many other parts in Europe, in fact several reputed companies have entrusted

Ipca with toll manufacturing for their bulk active requirements under strict secrecy

agreement.

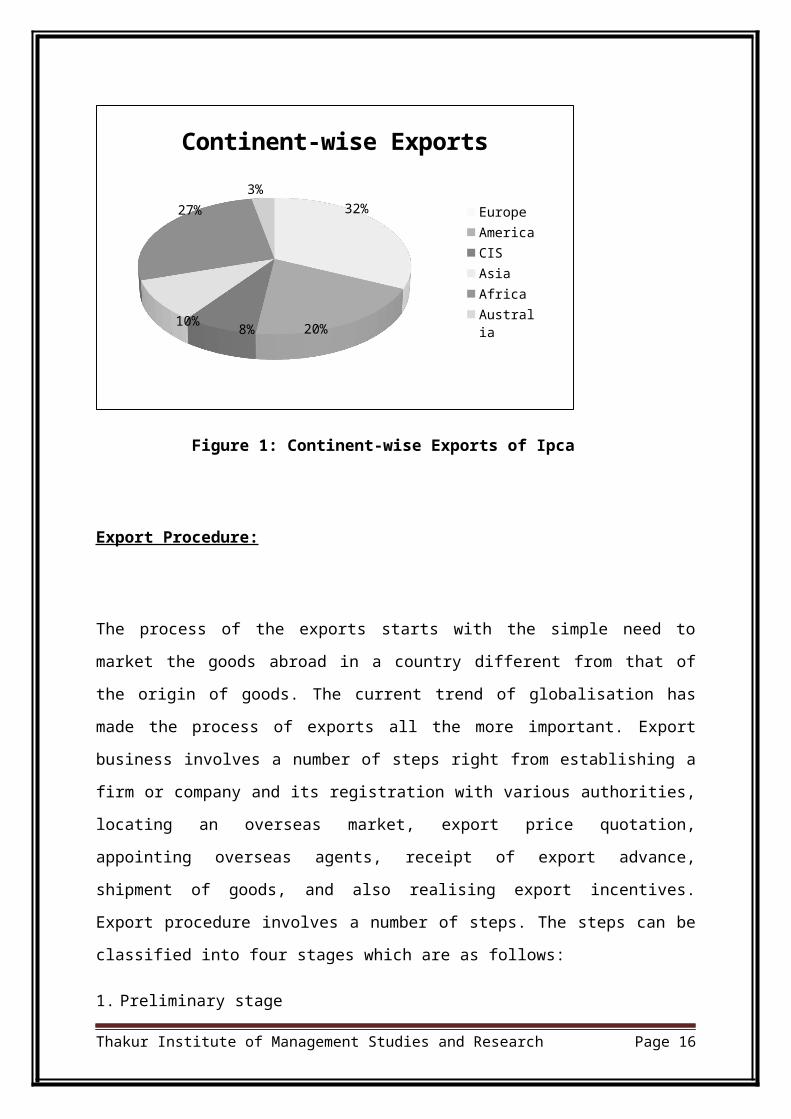

Following chart shows continent wise exports of Ipca Laboratories Ltd.

32%

20%8%10%

27%3%

Continent-wise Exports

Europe

America

CIS

Asia

Africa

Australia

Figure 1: Continent-wise Exports of Ipca

Export Procedure:

Thakur Institute of Management Studies and Research Page 11

The process of the exports starts with the simple need to market the goods abroad in a

country different from that of the origin of goods. The current trend of globalisation has made

the process of exports all the more important. Export business involves a number of steps

right from establishing a firm or company and its registration with various authorities,

locating an overseas market, export price quotation, appointing overseas agents, receipt of

export advance, shipment of goods, and also realising export incentives. Export procedure

involves a number of steps. The steps can be classified into four stages which are as follows:

1. Preliminary stage

2. Pre-shipment stage

3. Shipment stage

4. Post-shipment stage

Stage 1: Preliminary/Registration Stage

It is basically the foundation stage of export business. It is at this stage that the actual needs

to market the goods abroad blossoms up. The exporter decides on the products that are to be

exported, arranges to register the product with the various authorities, appoints overseas

agents and distributors and may even sometimes open up offices in strategically important

locations. The exporter may also tie up with some important customers so as to export them

on a regular basis.

The registration stage includes:-

(a) Registration of the Organisation: The form of organisation selected by the exporter

must be registered under the appropriate Act of the country.

A joint stock company under the Companies Act, 1956

A partnership firm under the Partnership Act, 1932

A sole trader should seek permission from the local authorities, as required

(b) Opening of Bank Account: The exporter should open a current account in the name

of the firm or company with a commercial bank which is authorised by the Reserve

Thakur Institute of Management Studies and Research Page 12

Bank of India (RBI) to deal in foreign exchange. Such bank also serves as a source of

pre-shipment and post-shipment finance for the exporter.

(c) Obtaining Importer-Exporter Code Number (IEC No.): Prior to 01.01.1997, it

was obligatory for every exporter to obtain CNX number from RBI. However, since

then, the CNX number has been replaced by IEC number issued by the Director

General for Foreign Trade (DGFT). The application form for obtaining IEC number

should be accompanied by fee of Rs. 1000.

(d) Obtaining Permanent Account Number (PAN): Export income is subject to a

number of exemptions and deductions under different sections of the Income Tax Act.

For claiming such exemptions and deductions, the exporter should register his

organisation with the Income Tax Authorities and obtain the Permanent Account

Number (PAN).

(e) Obtaining Sales Tax Number: Exportable goods are exempted from sales tax,

provided the exporter or his firm is registered with the Sales Tax Authorities. For this

purpose, the exporter is required to make an application in the prescribed form to the

Sales Tax Office (STO) in whose jurisdiction his (exporter’s) office is situated.

(f) Registration with Export Promotion Council (EPC): It is obligatory for every

exporter to register with the appropriate Export Promotion Council (EPC) and obtain

the Registration-cum-Membership Certificate (RCMC). The benefits provided in the

current EXIM policy are extended only to the registered exporters having valid

RCMC.

(g) Registration with ECGC: The exporter should also register with the Export Credit

and Guarantee Corporation of India (ECGC) in order to secure overseas payments

against political and commercial risks. It also helps the exporters in obtaining the

financial assistance from commercial banks and other financial institutions.

(h) Registration with other Authorities: The exporter should also register with various

other authorities such as:

Thakur Institute of Management Studies and Research Page 13

Federation of Indian Export Organisation (FIEO)

Indian Trade Promotion Organisation (ITPO)

Chambers of Commerce (COC)

Productivity Councils, etc

Stage 2: Pre-Shipment Stage

(a) Order Acquisition & Finance arrangement: The exporter keeps a regular contact

with the customers and if the client or the customer is satisfied he may place an order

with the exporting company. This involves Approaching Foreign buyers, inquiry

by buyer and prospective offer, Confirmation of Order, Opening of Letter of

Credit and Arrangement of Pre-shipment Finance. These are followed by:

(b) Production or Procurement of Goods: On securing the pre-shipment finance from

the bank, the exporter either arranges for the production of the required goods or

procures them from the domestic market as per the specifications of the importer.

(c) Packing, Marking & Clearance: The goods to be exported are properly packed

depending upon the type of product, the mode of transit, quantity of product etc. The

exporter prepares a packing list and the goods are appropriately marked with country

of origin, net and gross weight, port of destination, port of shipment etc. If required,

assistance can be taken from the Indian Institute of packing (IIP). This is followed by

Pre-Shipment Inspection and Central Excise Clearance.

(d) Obtaining Insurance Cover: The exporter obtains an ECGC cover (it is a type of

cover or protection that is provided to the exporter against the credit risk arising out of

non payment from the importing party.)

The exporter also obtains a marine insurance policy if the price quotation agreed upon

is CIF. The insurance policy is obtained in duplicate and other formalities like

Certificate of Origin, Consular Invoice are also completed at this stage

Thakur Institute of Management Studies and Research Page 14

(e) Appointment of C&F Agent: Since exporting is a complex and time consuming

process, the exporter should appoint a Clearing & Forwarding (C&F) agent for the

smooth clearance of goods from the customs and preparation and submission of

various export documents.

Stage 3: Shipment Stage

Export cargo can be exported to the overseas buyer by sea, air or land. However, shipment by

sea is the most popular and generally resorted to, as it is comparatively cheaper. Besides, the

ship’s capacity is far greater than other modes of transportation. Nevertheless, transportation

by air is utilised for export of expensive items like, diamonds, gold, etc. The shipment stage

includes the following steps

Reservation of Shipping Space, Arrangement of Internal Transportation up to the Port

of Shipment. This is followed by

Preparation and Processing of Shipping Documents: As the goods reach the port of

shipment, the exporter should issue detailed instructions of the C&F agent for the shipment of

cargo along with a complete set of the documents listed below:

Letter of Credit along with the export contract or export order

Commercial invoice (2 copies)

Packing list

Certificate of Origin

GR Form (original & duplicate)

ARE-I Form

Certificate of Inspection, where necessary (original copy)

Marine Insurance Policy

Customs Clearance: After the documents are received from the exporter, the C&F agent

prepares the shipping bill in 5 copies and presents bill and other documents to Customs

Appraiser. The documents are returned to the C&F agent after verification.

Thakur Institute of Management Studies and Research Page 15

This is followed by Obtaining ‘Carting Order’ from the Port Trust Authorities, Customs

Examination and Issue of ‘Let Export Order’, Obtaining ‘Let Ship Order’ from the

Customs Preventive Officer and Obtaining Mate’s Receipt and Bill of Lading.

Obtaining Mate’s Receipt and Bill of Lading: After this the goods are loaded on the board

for which the Mate of the ship issues Mate’s Receipt. This receipt is handed over to the

shipping company and Bill of Lading is obtained. The Shipping Company issues two to three

negotiable and two to three non-negotiable copies of Bill of Lading.

Stage 4: Post-Shipment Stage

The Post-Shipment stage consists of the following Steps

(a) Submission of Documents by the C&F Agent to the Exporter: On the completion

of the shipping procedure, the C&F agent submits the following documents to the

exporter

A copy of invoice duly attested by the Customs

Drawback copy of the shipping bill

Export promotion copy of the shipping bill

A full set of negotiable and non-negotiable copies of Bill of lading

The original L/C, export order or contract

Duplicate copy of the ARE-I Form

(b) Shipment Advice to Importer: After the shipment of goods, the exporter intimates

the importer about shipment of goods giving him details about the date of shipment,

the name of the vessel, the destination, etc. He should also send one copy of non-

negotiable Bill of Lading to the importer.

(c) Presentation of Documents to Bank for negotiation: Submission of relevant

documents to the banks and the process of getting the payment from the bank is called

‘Negotiation of the Documents’ and the documents are called ‘Negotiable Set of

Documents’. The set normally contains:

Thakur Institute of Management Studies and Research Page 16

Bill of Exchange, Sight Draft or Usance Draft

Full set of Bill of Lading or Airway Bill

Original Letter of Credit

Customs Invoice

Commercial Invoice including one copy duly certified by the Customs

Packing list

Foreign Exchange declaration forms, GR/SOFTEX/PP forms in duplicate

Exchange control copy of the Shipping Bill

Certificate of Origin

Marine Insurance policy, in duplicate.

(d) Dispatch of Documents: The bank negotiates these documents to the importers bank

in the manner as specified in the L/C. Before negotiating documents, the exporter's

bank scrutinizes them in order to ensure that all formalities have been complied with

and all documents are in order.

(e) Acceptance of the Bill of Exchange: Bill of Exchange accompanied by the above

documents is known as the Documentary Bill of Exchange. It is of two types:

Documents against Payment (Sight Draft): In case of sight draft, the drawer

instructs the bank to hand over the relevant documents to the importer only

against payment

Documents against Acceptance (Usance Draft): In case of usance draft, the

drawer instructs the bank to hand over the relevant documents to the importer

against his ‘acceptance’ of the Bill of Exchange.

(f) Letter of indemnity: The exporter can get immediate payment from his bank on the

submission of documents by signing a letter of indemnity. By signing the letter of

indemnity, the exporter undertakes to indemnify the bank in event of non-receipt of

payment from the importer along with accrued interest

Thakur Institute of Management Studies and Research Page 17

(g) Realisation of Export Proceeds: On receiving the documentary bill of exchange, the

importer releases payment in case of sight draft or accepts the usance draft

undertaking to pay on maturity of the bill of exchange. The exporter’s bank receives

the payment through importer’s bank and is credited to exporter’s account.

(h) Processing of GR Form: On receiving the export proceeds, the exporter’s bank

intimates the same to the RBI by recording the fact on the duplicate copy of GR. The

RBI verifies the details in duplicate copy of GR with the original copy of GR received

from the customs. If the details are found to be in order then the export transaction is

treated to be completed.

(i) Realisation of Export Incentives: If the exporter is eligible for export incentives,

then he should submit claim for the same accompanied by the bank realisation

certificate to the appropriate authority.

Export Finance

Introduction

Institutional Framework

Pre-Shipment Finance

Thakur Institute of Management Studies and Research Page 18

o Packing Credit

o Pre-Shipment Credit in foreign Currency

Post-Shipment Finance

o Negotiation of Export Documents under Letter of Credit

o Advance against Bills sent on Collection

o Post-Shipment Credit in Foreign Currency

Recent development in Export Financing

Introduction:

Export finance refers to the credit facilities extended to the exporters at the pre-shipment and

post-shipment stages. It includes any loan to an exporter for financing the purchase,

processing, manufacturing or packing of goods meant for overseas markets. Credit is also

extended after the shipment of goods to the date of realisation of export proceeds.

Institutional Framework:

Institutional framework for providing finance comprises Reserve Bank of India, Commercial

banks, Export Import Bank of India and Export Credit and Guarantee Corporation. Reserve

Bank of India, being the central bank of the country, lays down the policy framework and

provides guidelines for implementation.

Short or medium term finance, is provided exclusively by the Indian and foreign commercial

banks which are members of the Foreign Exchange Dealers Association of India (FEDAI)

The RBI functions as a refinancing institution for short and medium term loans, provided by

commercial banks. Export Import (EXIM) Bank of India, in certain cases, participates with

commercial banks in extending medium term loans to exporters. Commercial banks provide

bank finance at a concessional rate of interest and in turn are refinanced by the Reserve

Bank/Export Import Bank of India at concessional rate. In case they do not wish to avail

refinance, they are entitled for an interest rate subsidy. Export Credit & Guarantee

Thakur Institute of Management Studies and Research Page 19

Corporation (ECGC) also plays an important role through its various policies and guarantees

providing cover for commercial and political risks involved in export trade.

Pre-shipment Finance

Pre-shipment finance is provided to the exporters for the purchase of raw materials,

processing them and converting them into finished goods for the purpose of export. The

various pre-shipment advances available to the exporters are.

Packing Credit:

The basic purpose of packing credit is to enable the eligible exporters to procure, to process,

manufacture or store the goods meant for export. Packing credit refers to any loan to an

exporter for financing the purchase, processing, manufacturing or packing of goods as

reframed by the Reserve Bank of India. It is a short term credit against exportable goods.

Packing credit is normally granted on secured basis. Sometimes clean advance may also be

granted. Many advances are clean at their initial stage when goods are not yet acquired. Once

the goods are acquired and are in the custody of the exporter banks usually convert the clean

advance into hypothecation/pledge.

The detailed procedure of packing credit is as follows:

(a) Eligibility: Packing credit is available to all exporters whether merchant exporter,

Export/Trading/Star Trading/Super Star Trading Houses and manufacturer exporter.

Manufacturers of goods supplying to Export/Trading/ST/SST houses and Merchant

Exporters are eligible for packing credit. The exporters can avail PC against

irrevocable letter of credit issued in their favour by a reputed foreign bank. It is also

available against a confirmed or firm export order/contract placed by the buyer for

export of goods from India.

(b) Running Account Facility: The RBI has permitted banks to grant packing credit

advances even without lodgement of L/C or firm-order/contract under the scheme of

Running Account Facility subject to, the following conditions;

Thakur Institute of Management Studies and Research Page 20

i) The facility may be extended, provided the need for Running Account facility

has been established by the exporters to the satisfaction of the bank.

ii) The bank may extend this facility only to those exporters whose track record

has been good.

iii) L/C or firm order is produced within a reasonable period of time. For

commodities under selective credit control, banks should insist on production

of L/Cs or firm order within one month from the date of sanction

iv) The concessive credit available in respect of individual pre-shipment credit

should not go beyond 180 days.

Packing credit may also be given under the Red Clause letter of Credit. In this method, credit

is given at the instance and responsibility of the foreign banks establishing the L/C. Here, the

Packing credit advance is made against a simple receipt and is unsecured.

(c) Amount: The loan amount is decided on the basis of export and the credit rating of

the exporter by the bank. Generally the amount of packing credit will not exceed the

FOB value of the export goods or their domestic value whichever is less. It can be to

the extent of domestic value of the goods even though such value is higher than their

FOB value provided the goods are entitled to duty draw back and also covered by the

Export Production Finance Guarantee of the ECGC.

(d) Period: The packing credit can be granted for a maximum period of 180days from the

date of disbursement. The banks are authorised by RBI to extend this period. This

period can be extended for a further period of 90 days, in case of non-shipment of

goods within 180 days. The extension can be done provided the banks are satisfied

that the reasons for extension are due to circumstances beyond the control of the

exporters. Pre-shipment credit may be given for a longer period up to a maximum of

270 days, if the banks are satisfied about the need for longer duration of credit.

(e) Rate of Interest: The interest payable on pre-shipment finance is usually lower than

the normal rate, provided the credit is extinguished by lodging the export bills on

remittances from abroad. If the exporter fails to do so they would not be able to avail

concessional rate of interest.

Thakur Institute of Management Studies and Research Page 21

In order to avail the packing credit, exporters are expected to make a formal

application to the bank giving details of credit requirements along with the required

documents.

Packing Credit in Foreign Currency (PCFC):

This is an additional window to rupee packing credit scheme. This credit is available to cover

both the domestic and imported inputs of the goods exported from India. The Facility is

available in any of the convertible currencies. The credit will be self-liquidating in nature and

accordingly after the shipment of goods the bills will be eligible for

discounting/rediscounting or for post-shipment in foreign currency. The exporters can avail

this finance under the following two options

i) The exporters may avail pre-shipment credit in rupees and then the post-shipment

credit either in rupees or in foreign currency denominated credit or

discounting/rediscounting of export bills.

ii) The exporters may avail pre-shipment credit in foreign currency and

discounting/rediscounting of the export bills in foreign currency.

PCFC credit will also be available both to the supplier units of EPZ/EOU and the receiver

units of EPZ/EOU. The credit in foreign currency shall also be available on exports to Asian

Clearing Union (ACU) countries. This will be extended on the basis of confirmed firm export

orders or confirmed L/Cs. The Running account facility will not be available under the

scheme.

Post-Shipment Finance

It may be defined as any loan or advance granted or any other credit provided by a bank to an

exporter of goods from India after shipment of goods till the date of realisation of export

Thakur Institute of Management Studies and Research Page 22

proceeds. It includes any loan or advance granted to an exporter on consideration of or on the

security of, any duty drawback or any cash receivables by way of incentive from the

government.

While granting post-shipment finance, banks are governed by the guidelines issued by the

RBI, the rules of the Foreign Exchange Dealers Association of India (FEDAI), the Trade

Control and Exchange Control Regulations and the International Conventions and Codes of

the International Chambers of Commerce. The exporters are required to obtain credit limits

suitable to their needs. The quantum of credit depends on Export sales and receivables.

Post-shipment finance is granted under various methods. The exporter may choose the type of

facility as per his requirement. The banks scrutinize the documents submitted for compliance

of exchange control provisions.

The various types of Post Shipment Finance are:

(a) Negotiation of Export Documents under Letters of Credit

Where the exports are under letter of credit arrangements, the banks will negotiate the

export bills provided it is drawn in conformity with the letter of credit. When

documents are presented to the bank for negotiation under L/C, they should be

scrutinized carefully taking into account all the terms and conditions of the credit. All

the documents tendered should be strictly in accordance with the L/C terms. It is to be

noted that the L/C issuing bank undertakes to honour its commitment only if the

beneficiary submits the stipulated documents. Even the slightest deviation from the

conditions, those specified in the L/C can give an excuse to the issuing bank of

refusing the reimbursement of the payment that might have been already made by the

negotiating bank.

(b) Advance against Bills sent on Collection

Post-shipment finance is granted against bills sent on collection basis in the following

situations;

When the accommodation available under the foreign bills purchase limit is

exhausted

Thakur Institute of Management Studies and Research Page 23

When some export bills dawn under L/C have discrepancies

Where it is customary practice in the particular line of trade and in the case of

exports to countries where there are problems of externalisation

Under the above situation, the bank may send the bill on collection basis and finance

the exporter to some extent out of the total bill amount. The amount advanced will be

liquidated out of the export proceeds of the export bill and the balance paid to the

exporter.

(c) Post-Shipment Credit in Foreign Currency

The exporters have the option of availing exports credit at post-shipment stage either

in rupee or in foreign currency. The credit is granted under the Rediscounting of

Export Bills Abroad Scheme (EBR) at LIBOR linked interest rates. The scheme

covers export bills with usance period up to 180 days from the date of shipment.

Discounting of bills beyond 180 days requires prior approval from RBI. The exporters

have the option to avail pre-shipment credit and post-shipment credit either in rupee

or in foreign currency. If pre-shipment credit has been availed in foreign currency; the

post-shipment credit necessarily to be under the EBR scheme. This is done because

the foreign currency pre-shipment credit has to be liquidated in foreign currency.

Recent Developments in Export Financing:

As stated earlier, offer of attractive credit terms is a crucial factor in winning export

contracts. Hence, financial institutions are offering several innovative financial services to

exporters. Some of these services are as below:

Factoring: It is an attractive way of providing export finance to exporters. In this system,

factor bears the complete credit risk. A factor is a special type of agent who, depending upon

the type of agreement offers a variety of services. These services include coverage of credit

risk, collection of export proceeds, and maintenance of accounts receivables and advance of

funds. Purchase of receivables without recourse is the most important service of the factor. A

big advantage to the exporter is that it is without recourse financing. This means that the risk

Thakur Institute of Management Studies and Research Page 24

of non-payment by the importer is to be borne entirely by the factor. Factoring is generally

availed against export collection bills.

In India, International Export Factoring services on with recourse basis have been approved

by the RBI. It provides a new dimension to management of export receivables. SBI Factors

and Commercial Services Pvt. Ltd., Mumbai have been permitted to provide International

Export Factoring. In this system, the exporter enters into an export factoring agreement with

exporter’s factor. The exporters ship goods to approved foreign buyers. Each invoice is made

payable to specific factor in importer’s country. Copies of invoices and shipping documents

are sent to the importer’s factor. Exporter’s factor will make prepayment to the export against

approved export receivables. On receipt of payments from the importers on due date of

invoice, importer’s factor remits the fund to the exporter’s factor. The exporter’s factor pays

to the exporter after deducting the amount of prepayments.

Forfaiting: Forfaiting refers to non-recourse discounting of export receivables. It is a

mechanism of financing exports that involves less risk and enhances international

competitiveness. It converts a credit sale into cash sale for an exporter. In this system

forfaiting agency discounts international trade receivables of the exporter. The forfaiter pays

the exporter in cash and undertakes the risk associated with the export deal. The exporter

surrenders, without recourse to him, his rights to claim for payments on goods delivered to an

importer. Generally the documents required are Under L/C or backed by Bank Guarantee.

All exports of capital goods and other goods made on medium to long term credit are eligible

to be financed through forfaiting. In India, EXIM bank plays an intermediary role between

the Indian exporter and the overseas forfaiting agency. The exporter approaches EXIM bank

for forfeiting transaction. The bank receives bills of exchange or promissory notes from the

exporter and sends them to the forfaiter for discounting. Subsequently, the bank arranges for

the discounted proceeds to be remitted to the Indian exporter. The bank issues appropriate

certificates to enable Indian exporters to remit commitment fees and other charges. RBI has

allowed authorised dealers to undertake forfeiting of medium term export receivables.

Exports–Ipca Laboratories Ltd.

Thakur Institute of Management Studies and Research Page 25

It is at the Post-Shipment stage that the role of the finance department comes into play. The

shipping department prepares the documents and then forwards it to the finance department.

The documents are generally prepared in 2 sets.

(a) Internal Set: This set is kept by the exporter for his reference

(b) External Set: This Set of documents is generally sent to the importer i.e., it is sent

outside the country.

The following documents are prepared:

1) Commercial Invoice

2) Packing List

3) Freight documents

4) Certificate of Origin

5) Insurance Certificate

6) Certificate of Analysis

7) Exchange Control Declaration (GR)

8) Shipping Bill

i) Commercial Invoice: An invoice is very important as it contains the names of the

exporter, importer, and the consignee, the value and the description of goods. It

has to be signed by the exporter. Other documents are prepared by deriving

information from the invoice. It is required to be presented before different

authorities for different purposes. This document is prepared by the exporting

company.

ii) Packing List: This statement gives the packing details of goods in a prescribed

format. It is a very useful document for customs at the time of examination and for

warehouse keeper of the buyer to maintain a record of inventory and to effect

delivery. The packing list contains the details of the goods their gross weight, net

weight, quantity, description of the package or cartons in which they are packed,

Thakur Institute of Management Studies and Research Page 26

the shipping marks they bear etc. This document is also prepared by the exporting

company.

iii) Freight document/ Bill of lading: The Bill of lading is prepared by the

transportation firm through which the goods are being transported. It is a bill

which contains the freight charges, terminal handling charges, documentation

charges and other charges which are charged by the transportation firm for

transporting the goods from their country of origin or country where they are

presently held to country of their destination. Details are also mentioned about the

Bill of lading date and the Shipped on Board date in case of transportation by sea

and the Airway bill date and the flight date in case of transportation by air.

iv) Certificate of Origin: This certificate issued by the local Chamber of Commerce

indicates that the goods, which are being exported, are actually manufactured in a

specific country mentioned therein. It is sent by the exporter to the importer and is

useful for the clearance of the goods from the customs authority of the importing

country.

v) Insurance Certificate: This document, obtained from the freight forwarder, is

used to assure the consignee that insurance will cover the loss or damage to the

cargo during transit (marine/air insurance). The certificate contains details about

the goods and also about the premium paid.

vi) Certificate of Analysis: Certificate of Analysis is prepared by the exporting

company. It is an important document as it contains the analytical details of the

goods i.e. technical details like the composition of the goods, the weight of the

goods, their shape and size etc.

vii) Exchange Control declaration (GR): The RBI has prescribed a GR form (SDF),

a PP form, and SOFTEX forms to declare the export Transactions. The GR form

Contains:

(a) Name and address of the exporter and description of goods.

Thakur Institute of Management Studies and Research Page 27

(b) Name and address of the authorised dealer through whom proceeds of the

exports have been or will be realised.

(c) Details of commission and discount due to foreign agent or buyer.

(d) The full export value, giving break up of FOB, Freight Insurance, Discount,

and Commission etc.

viii) Shipping Bill: Shipping bill is a mandatory document for export of any goods out

of India. It is only on the basis of it; one gets all the incentives including

drawback/DEPB & other benefits. The CHA-clearing agent prepares it on

exporter’s behalf and files with Customs. After export Customs gives Export

Promotion copy to the agent giving all the details of flight no. & EGM.

The role of finance department commences after it receives the final documents from the

shipping department. The shipping department forwards the documents to the finance

department for scrutiny and for further negotiation and dealing with the banks.

Export Procedures and Finance: Ipca Laboratories Ltd.

Part 1: Documentation:

Thakur Institute of Management Studies and Research Page 28

1. Enter the details on receipt of documents from the shipping department into the export

invoicing system.

2. Check whether the document is for collection, discounting or advance payment.

3. All documents are normally sent for collection; however if there is a requirement of

immediate funds and if the importing party has a good track record of making the

payments on time then the documents may be negotiated with the bank by discounting

the bill. However if the importing party has a poor track record of irregular payments,

then the documents may just be sent for collection.

4. The ECGC limit available is then checked for since it is an important protective

safeguard against default risk.

5. However in certain cases ECGC cover is not mandatory (in case of exports to wholly

owned subsidiaries etc.)

a. In case there is no ECGC cover prior approval of the Managing Director is

required.

b. If ECGC is not taken for some specific parties then it should be checked that

whether it is as per the instructions of the Managing Directors.

6. Now the documents attached with the invoice are checked for .The following

documents are checked

a. Freight certificate

b. Bill of Lading or Airway Bill

c. Insurance certificate

d. Certificate of Origin

e. Certificate of analysis

f. Packing list

g. Exchange control declaration (G.R)

h. BOE (in case documents are sent directly to the party BOE not required)

Thakur Institute of Management Studies and Research Page 29

These documents have to be checked based on the terms of trade and other details

mentioned in the invoice

E.g. if the terms of trade are CIF the insurance copy is present with the invoice.

However if the terms of trade are C&F then the insurance copy is not present with the

invoice.

7. The details of these documents are entered in the export invoicing system.

8. Next the following details are checked for and corresponding entries be made in the

export invoicing system:

a. The invoice value is checked with the value as mentioned in the G.R and if there

are more than one G.R, then the total of all the G.R is taken and matched with the

Invoice value.

b. The commission as declared in the G.R. is mentioned in the register.

c. The Freight and the Terminal handling charges along with the documentation or

other charges if any are entered in the register.

d. The scheme under which all the documents go is also made note of i.e. DEPB,

DEEC, DFRC, DBK and ADVANCE LICENCE. These schemes are necessary

for claiming a refund of some part of the amount, a benefit which is provided by

the government of India.

9. After filling up all the details in the register and completing all the necessary

requirements, a covering letter is prepared with purchase/ discount/ negotiation/

collection instructions and if there is any PC recovery that details are also mentioned

in the covering letter.

10. If any discrepancies i.e. errors are found in the documents, the shipping department is

contacted for clarifications and the necessary corrections are made.

11. The documents are then sent to the authorized signatories for their signature and after

their signatures the documents are submitted to the respective banks for processing.

Thakur Institute of Management Studies and Research Page 30

12. The dispatch details, Bank Ref Number are also taken and entered in the Oracle

Export system.

Part 2: Receipts of Payments:

13. Regular follow-up is kept with the bank on a day to day basis for the receipt of

payment from the parties. If any payment matures then the exchange rate is taken

from the bank for the corresponding currency and the relevant amount is credited to

the company’s account.

14. The types of accounts, which are maintained by IPCA, are

a. OCC A/C – Overdraft Cash Credit

b. EEFC A/C- Exchange Earners Foreign Currency.

15. Corresponding letters are also sent to the bank for the issue of FITT (Foreign Inward

Telegraphic Transfer), vouchers in case of advance payments where no payment

instructions are received.

16. The bank after receiving the documents scrutinizes it properly and sends it to the

importer, upon the receipt of which the exporter’s bank collects the export proceeds

from the importer’s bank. Generally, the export proceeds, in India, must be realised

within 180 days from the date of shipment, in case of the payment term extending

beyond the stipulated period special permission needs to be sought from the R.B.I.

17. The bank also sends a copy of Bank Certificate and attested copies of commercial

invoice to the exporter, which is handed over to finance department.

18. After realising the export proceeds, the bank after deducting its charges makes

necessary credit in the account of Ipca. The bank also records the realised payment on

the duplicate copy of GR and then forwards it to RBI. The RBI then cross checks the

original copy of GR, which it has received through the customers (The amount

Thakur Institute of Management Studies and Research Page 31

mentioned in the original GR must match with the amount realised by the exporter’s

bank)

Reports and Follow-ups:

The finance department has to maintain a regular follow up to see that the payments are

received on time. If the payment is not received on time the company would suffer losses in

the form of overdue interests, which can eat up a sizeable amount of the profits earned.

So the finance department regularly prepares reports, which is forwarded to the concerned

export manager. The reports show the outstanding balance of each party under the

supervision of the concerned export manager

Follow- up is kept to see whether the export managers are taking necessary action to recover

the amount or not. The export manager contacts the parties and asks them to make the

payment. The bank also sends requests to its correspondent bank in the importing country

asking them to make the payment. Such a report is prepared through the exporting system and

the follow up generally occurs at the managerial level.

When the payment is received the bankers intimate the Finance Department and also ask

them to take the exchange rates for the concerned currency. After taking the rates the bank

account is credited with the equivalent amount.

Other reports like Bank wise outstanding/deposits etc. are also prepared to have a clear view

of the transactions and deposits in each of the transacting banks Ipca laboratories maintains

accounts with.

Part 3: EXPORT FINANCE

Thakur Institute of Management Studies and Research Page 32

The government of India, in order to boost exports, is liberalizing the tariffs and duties on

exports; in fact it is encouraging banks to provide working capital assistance to exporter at

concessional rates for procuring raw material and satisfy other small term capital needs. Ipca

Laboratories also avails of the same. Generally the finance provided is for the pre and the

post-shipment period

The short-term finance is required to meet “Working Capital” needs. The working capital is

used to meet regular and recurring needs of a business firm. The regular and recurring needs

of a business firm refer to purchase of raw material, payment of wages and salaries, expenses

like payment of rent, advertising etc.

The exporter may also require “Term Finance”. The term finance or term loans, which is

required for medium and long term financial needs such as purchase of fixed assets and long

term working capital.

Export finance is short-term working capital finance allowed to an exporter. Finance and

credit are available not only to help export production but also to sell to overseas customers

on credit.

(A) Pre-Shipment Finance

Definition:

Pre-shipment finance or Packing Credit is a working capital made available for specific

purpose of purchasing, manufacturing, packing, transportation and warehousing of goods

meant for exports. This credit is given for a period up to 180 days within which the exporter

has to recover the packing credit. This packing credit is valid for a period of 6 months. Ipca

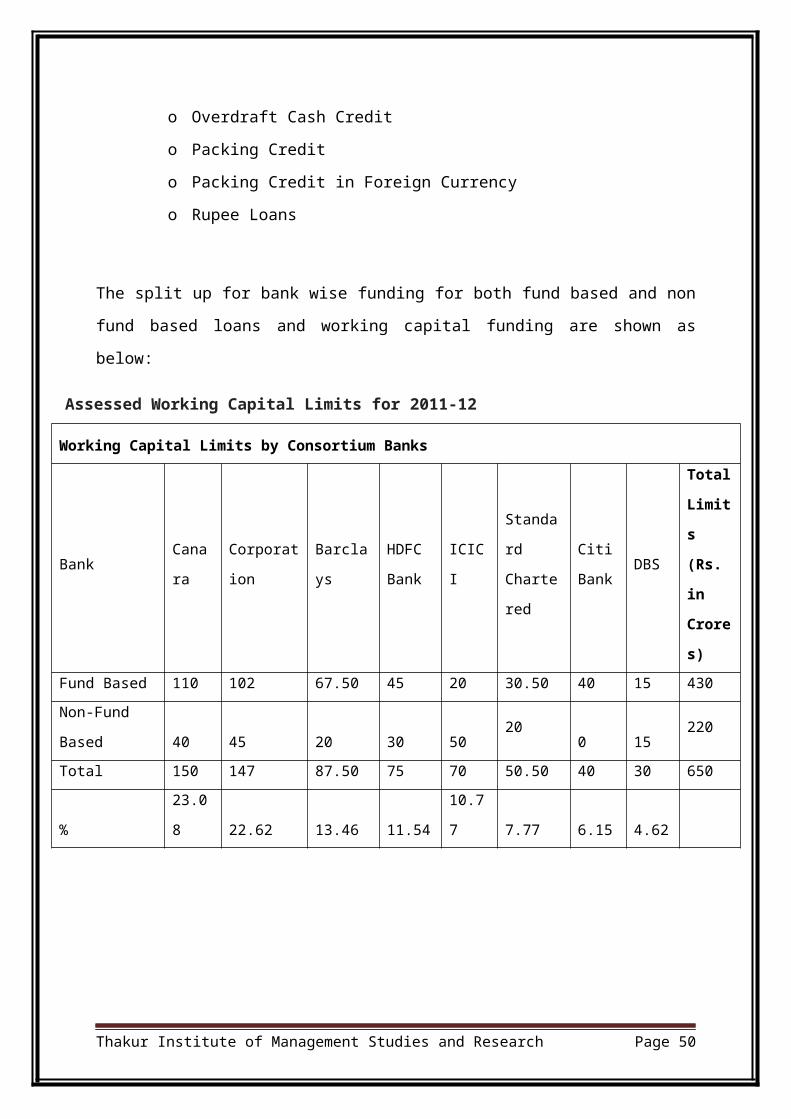

for the financial year 2011-12 had an arrangement of using Rs. 430 Crore as fund based loans

from the consortium of banks that it transacts with.

Pre-shipment is also referred as “Packing Credit”. It is working capital finance provided by

commercial banks to the exporter prior to shipment of goods.

The fund based loans are interchangeable in form and can be used as

o Overdraft Cash Credit

Thakur Institute of Management Studies and Research Page 33

o Packing Credit

o Packing Credit in Foreign Currency

o Rupee Loans

The split up for bank wise funding for both fund based and non fund based loans and working

capital funding are shown as below:

Assessed Working Capital Limits for 2011-12

Working Capital Limits by Consortium Banks

Bank Canara Corporation BarclaysHDFC

BankICICI

Standard

Chartered

Citi

BankDBS

Total

Limits

(Rs. in

Crores

)

Fund Based 110 102 67.50 45 20 30.50 40 15 430

Non-Fund

Based 40 45 20 30 5020

0 15220

Total 150 147 87.50 75 70 50.50 40 30 650

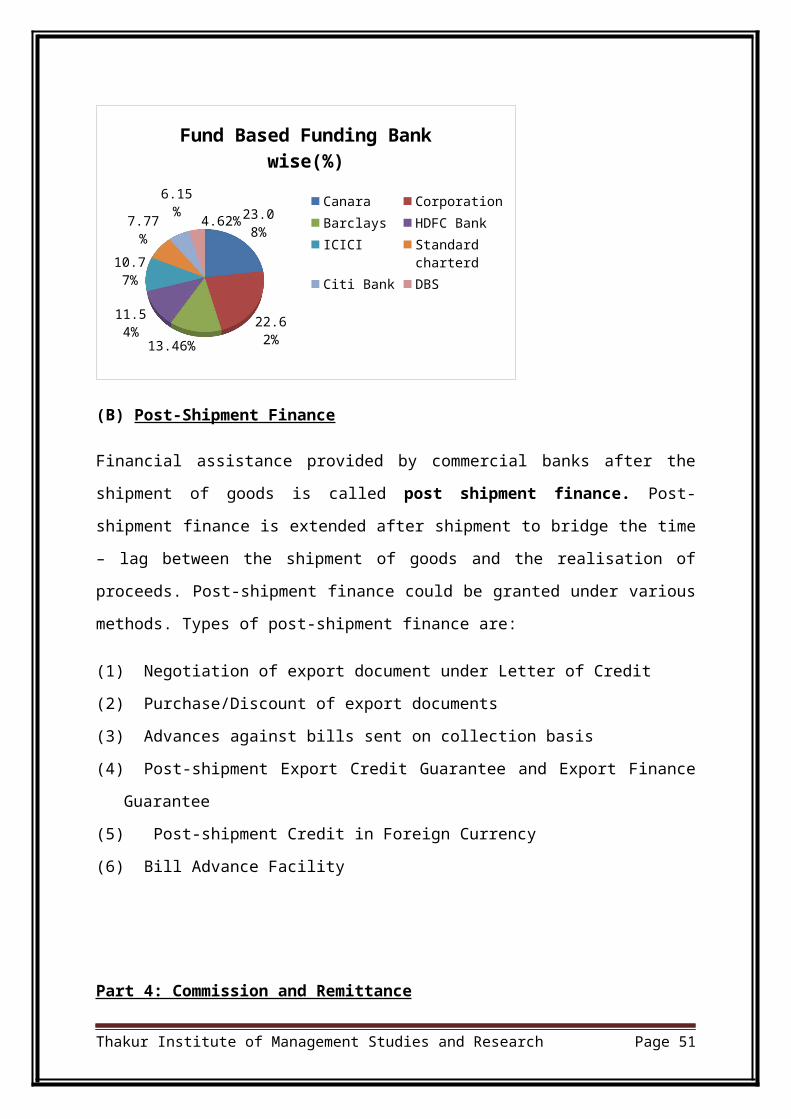

% 23.08 22.62 13.46 11.54 10.77 7.77 6.15 4.62

23.08%

22.62%

13.46%

11.54%

10.77%

7.77%

6.15%

4.62%

Fund Based Funding Bank wise(%)

CanaraCorporationBarclaysHDFC BankICICIStandard charterdCiti BankDBS

(B) Post-Shipment Finance

Thakur Institute of Management Studies and Research Page 34

Financial assistance provided by commercial banks after the shipment of goods is called post

shipment finance. Post-shipment finance is extended after shipment to bridge the time – lag

between the shipment of goods and the realisation of proceeds. Post-shipment finance could

be granted under various methods. Types of post-shipment finance are:

(1) Negotiation of export document under Letter of Credit

(2) Purchase/Discount of export documents

(3) Advances against bills sent on collection basis

(4) Post-shipment Export Credit Guarantee and Export Finance Guarantee

(5) Post-shipment Credit in Foreign Currency

(6) Bill Advance Facility

Part 4: Commission and Remittance

Remittances, also termed as export payment are paid by the exporter to the third party

involved between the exporter and the importer. This payment is made to the middleman,

who acts as a link between the importer and the exporter. Generally the remittance is made in

the form of Commission which may be some percentage of the invoice value or definite

amount as decided between the parties. Inter-firm amounts are also remitted by the parent

company to its various branches situated all over the world. One important thing needed for

overseas commission to be remitted is that the percentage or the amount of commission

should be declared in the Original Exchange control Copy (G.R.) copy.

IPCA has numerous offices in several parts of the world; it also has tie ups and collaborations

with big pharmaceutical companies and agencies for exporting and marketing its products

The non-trading offices of Ipca are at Australia, Columbia, Kazakhstan, Kiev, Kenya,

Malaysia, Moscow, Philippines, Sri Lanka & Vietnam.

Money has to be regularly remitted to these offices for meeting out its various expenses and

also paying off the salaries of the managers and the employees working in the office.

The types of remittances which are regularly made by the finance department are:

Agency commission

Thakur Institute of Management Studies and Research Page 35

Sales promotion

Product registration

Books and subscriptions

Consultancy charges

Remittance to Non-trading offices

PSR salaries

WOS: Wholly Owned Subsidiary company

Generally some of these remittances are directly remitted by the finance department at the

start or during the mid/end of the month i.e. in case of PSR salaries and agency commission.

However these remittances have to be normally made after receiving an intimation or Debit

note from the party or the export managers.

The documents, which need to be attached for the purpose of remittance, are Covering letter,

A2 form, FEMA declaration, ORR FORM (Opening of Offices /Posting of Representatives

Abroad - only for PSR Salaries and non trading offices at start), Invoice copy in case of

Product registration, Books & Subscription, Card payment, Consultation charges, and other

remittances. And any other copy or document that specifies the amount to be remitted.

All these copies have to be attached after which necessary signatures are taken and then these

documents are sent to the bank. Instructions are given to the bank regarding which a/c has to

be debited and through what mode the documents have to be transmitted.

On the other hand the company also receives some inward remittances in the form of:

Export bill realisation

Advance against exports

Debit note

Sample payment

Dossier sale/ Service Invoices

Agency Commission

Thakur Institute of Management Studies and Research Page 36

It is the commission, which is paid to the middleman or the agent for his services. The

commission has to be paid to the agent only and only after the payment has been

realized.

Documents, which need to be checked for Agency commission, are:

Internal Memo letter or Debit note which contains the name of the export manger through

whom it has been sent, notice about the commission which has to be paid along with the

details of the documents which are attached with it.

Annexure: It contains details of the transactions in depth their invoice no, quantity, amount,

bank ref no. Every bank has its own different annexure.

A2 Form & FEMA declaration.

Covering Letter: It is prepared by the company and it contains details of the documents which

are attached.

Thakur Institute of Management Studies and Research Page 37

IMPORT

Importing refers to the purchase of foreign products for use or sale in the home market. It

involves searching foreign markets for acceptable products and sources of supply providing

for transfer of the product to home market, arranging financing negotiating the import

documentation and customs procedure and developing plans for use or resale of the item or

service. Thus successful importing depends on more than good buying, it requires planning

for acceptance of the product and delivery of the promised benefits. The importing firm has

the responsibility to determine whether the foreign product or service meet the needs of the

home

The Import Process:

The Import process essentially comprises the following five stages:

1. Determining market demand and purchase motivation.

2. Locating and negotiating with sources of supply.

3. Securing physical distribution.

4. Preparing documentation and customs processing to facilitate movement among

countries and organization.

5. Developing plan for resale or use.

STAGES IN AN IMPORT TRANSACTION

PRE- IMPORT PROCEDURE:

1. Selecting the Commodity & Selecting the Overseas Supplier

2. Capability and Creditworthiness of Overseas Supplier: Successful completion of

an import transaction mainly depends upon the capability of the overseas supplier to

fulfil his contract. Therefore, it is advisable to verify the creditworthiness of the

overseas supplier and his capacity to fulfil the contract through confidential reports

about him from the banks and Indian embassies abroad. It is advisable to finalize

contract through indenting agents of overseas suppliers situated in India.

Thakur Institute of Management Studies and Research Page 38

3. Role of Overseas Suppliers Agents in India: Some reputed overseas suppliers have

their indenting agents stationed in India. These agents procure orders from the Indian

parties and arrange for the supply of goods from their principal abroad. It is advisable

to import through such agents as they can be readily contacted in case there is any

dispute regarding quality or quantity of goods imported, receipt of payment,

documentation formalities, etc.

4. Inquiry; Offer and Counter-Offer: It is advisable that before finalizing the terms of

import order, one should call for the samples or catalogue and other relevant literature

and the specifications of the items to be imported. Import of samples of goods is

exempted from import duties under 'Geneva' Convention of 7th November 1952.

After satisfying- himself with the samples and the creditworthiness of the overseas

supplier, the importer should proceed to finalize the terms of the contract to be

entered into.

ACTUAL IMPORT TRANSACTION:

The following stages mark the various steps involved in importing goods into India under an

import licence and quota:

5. Placing the Order

6. Obtaining Foreign Exchange: The foreign exchange reserves of any country are

controlled by the Government and are released through the central bank. In India, the

Exchange Control Department of the Reserve Bank of India deals with applications

for the release of foreign currency. However an importer is able to get the foreign

exchange only from an exchange bank approved and recognized by the Reserve Bank

of India for dealings in foreign exchange. The importer has to produce the import

licence along with the prescribed form for securing foreign exchange required to pay

for the goods ordered from another country. The exchange back through which the

payment is proposed to be routed puts its endorsement on the application form. On the

strength of the application and the licence and the exchange policy of the government

Thakur Institute of Management Studies and Research Page 39

of India in force at the time of application the Reserve Bank of India sanction the

release of a certain amount of the desired foreign currency. This paves the way for the

importer to go ahead with the other formalities in connection with an import

transaction. It must be noted that while licence is issued by the Government for all

imports during the period of its validity exchange made available only for a specific

transaction for which an order has been placed.

7. Arrangement for Payment: After the importer has succeeded in securing the

requisite amount of foreign exchange from the Reserve Bank of India, he has to make

arrangements for paying for the goods ordered. This may be done through an L/C

where it is intended to enable the shipper to obtain payment for the goods

immediately on surrendering a documentary bill to a bank in his own country.

Another method will be to request the exporter to forward the documentary bill

through his banker to the importer for being delivered to him either against

acceptance of the bill of exchange or against its payment. In such cases, when the

shipper (exporter) has shipped the goods an advice note to the importer stating the

date of shipment the goods and the probable date when the ship is expected to reach

its destination. At the same time he draws a bill of exchange on the importer (also

called indentor) for the full invoice value of the goods. Various documents like master

document, insurance policy, bill of lading and certificate of origin are attached to this

bill. That is why it is called the ‘Documentary Bill’ A Documentary Bill may either be

D/A or D/P i.e. the banker through which it is sent may be instructed to deliver the

document against the acceptance of the bill by the importer or against the payment by

him. (D/A=Documents against Acceptance: D/P = Documents against payment)

The bank’s branch in the importing country, or its agent there, arranges for the bill to

be presented to the drawee (importer). The attached documents are handed over to

him immediately thereafter if it is a D/A bill in case of a D/P bill, the bank delivers

the documents only after the importer pays the amount of the bill on maturity.

Generally, indent house is mentioned as the ‘Referee in case of need’ on the bill. In

case, the importer cannot comply with the requirements regarding acceptance or

payment the indent house does so on his behalf.

Thakur Institute of Management Studies and Research Page 40

8. Clearing the Goods: Assuming that the importer has taken possession of the various

documents relating to the goods shipped, he will have to comply with the formalities

prescribed for clearing the goods. When the ship carrying the goods touches at a port,

the importer has to secure the release of cargo from the custody of the customs

authorities. The importer then presents the necessary documents like the Port Trust

Dues Receipt, copies of the Bill of Entry etc. to the Port Trust Office to obtain

clearance regarding dock dues, etc. Thereafter, necessary documents to the Customs

office are presented.

9. Bill of Entry: The Bill of Entry, down in triplicates, attests the fact that goods of

specified quantity, value and description are entering the bounds of the country.

Separate forms of the Bill of Entry are used for each one of the three classes of good:

(i) free goods which are exempted from customs duty, (ii) goods for home

consumption, and (iii) bonded goods.

10. Payment of Customs Duties: If the goods are free, no import duty is to be paid at the

Customs Office. On dutiable goods, the importer or his agent will pay the import duty

which may be specified, i.e. based on weight measurements etc. It may be ad-

valorem, i.e. according to the tariff or the market value of the commodity or its

invoice value.

Payment of customs duty can also be made under the system called the “Permanent

Deposit System” Under this system; an importer may maintain a running account with

the Customs Office and make deposits from time to time. The duty payable on a

particular consignment of goods received at the customs is charged to the account and

the importer is informed of this.

In case the importer is not in a position to pay the customs duty on the whole of

imported goods, he may apply to the customs authorities to get when placed in the

‘Bonded Warehouse’. He can then pay the duty on each instalment of goods that he

withdraws from time to time.

To save themselves from the trouble of going through all the above mentioned

formalities, the importers may entrust the hob to clearing and forwarding agents. In

Thakur Institute of Management Studies and Research Page 41

such a case, these agents will take it upon themselves to deliver the goods at the

exporter’s warehouse. Clearing agents charge commission for their services.

LEGAL DIMENSIONS OF IMPORT PROCEDURE:

11. Mode of Pricing and INCO TERMS: While finalising terms of import contract, the

importer should, inter-alia, be fully conversant with the mode of pricing and the

manner of payment for the imports. As regards mode of pricing, the overseas supplier

should quote the terms prevailing in international trade. International Chamber of

Commerce (ICC), Paris, has given detailed definition of a few standard terms

popularly known as 'INCO TERMS'. These terms have almost universal acceptance.

12. Mode of Settlement of Payment: There are mainly three modes of settling

international transactions depending upon the creditworthiness of the importer or

exporter, demand for the commodity in the international market, exchange control

regulations prevailing in the importer or exporter countries and other relevant factors :

a. Advance Payment.

b. Payment or Acceptance against Documentary Collections.

c. Payment under Letter of Credit.

13. Obtaining IEC Number: In India, it is obligatory for every importer and exporter to

register themselves with the Director General of Foreign Trade (DGFT) and obtain

Import-Export Code (IEC) Number. The application form for obtaining IEC number

should be accompanied by a fee of Rs. 1000 and two copies of passport size

photographs of the applicant duly attested by the banker of the applicant and other

relevant documents.

14. Obtaining Import Licence: If the item to be imported falls in the prohibited list, then

such item cannot be imported at all. However, if it falls in restricted list then the

necessary clearance must be obtained from appropriate licensing authority. Similarly,

if it is subject to the canalisation through State Trading Enterprises (STEs), then the

necessary formalities are to be completed pertaining to the same.

Thakur Institute of Management Studies and Research Page 42

15. Obtaining Foreign Exchange: In India, all foreign exchange transactions are

regulated by the Exchange Control Department of the Reserve Bank of India (RBI).

Therefore, every importer is required to make an application to the Reserve Bank of

India (RBI) for getting sanction for making overseas payments. The Exchange

Control Department scrutinises the application and if satisfied, sanctions necessary

foreign exchange for the import transaction.

16. Arranging Finance for Import: It is advisable that the financial planning for imports

should be done in advance in order to avoid huge demurrages on the imported goods

lying uncleared for want of payment. Banks normally do not extend any fund based

assistance to importers. However, they enable industrial units and others to have

access to imported inputs and machinery by establishing letters of credit in favour of

the overseas suppliers.

17. Obtaining Import L/C Limit: Import L/C limits are sanctioned by the banks on

submission of complete loan proposal as in the case of other types of credit facilities.

This requires advance financial planning so as to retire import bills under L/C on

time. Any delay in retirement of bills not only strains the relations is of the importer

with his bank but also results in additional costs by way of penal interest, demurrage

charges, etc.

Import Process and Finance: Ipca Laboratories Ltd.

The process of import begins with the requirements of the factories being forwarded to the

Purchase or Commercial Department. The Purchase Department then places the orders,

selecting and choosing the purchase from the national as well as the International market.

If the goods are imported then the Purchase Order is forwarded to the Import Document. The

Purchase Order contains the details of the purchases. It consists of the following details:

1. Importer Name and Address

2. Address of the factory from where the order is forwarded

Thakur Institute of Management Studies and Research Page 43

3. Payment Terms and Currency

4. Bank Details through which the documents are routed

5. Shipment details like mode of dispatch

6. Purchase details like item code, description, quantity, rate, Interest and Specifications

The finance department, after receiving the purchase order prepares to draw a L.C. if the

exporting party requires so. The exporting party may also send the documents for collection

purpose. If a L.C. is drawn, the details of the same are entered in the register.

The import Department receives intimation or advises from the bank regarding the arrival of

the original set of documents for goods. The bills, which are sent on collection, are entered in

the register after the import department receives the intimation.

The Import department has to take the possession of the documents within three days. The

original documents are necessary for the clearance and possession of the goods from the

customs department. If the payment terms are on sight basis, then making the payments of the

required imports can only make the possession of the documents.

For this purpose the import department prepares an acceptance letter along with the OGL

declaration and the form A1.

OGL or Open General License declaration is a declaration or an undertaking by the importer

that the goods, which are imported, can be imported freely as per the present EXIM policy

and they are free of any restrictions under the ITC classification of exports and import items

or are not under the negative list of the foreign trade policy. The importer also undertakes to