Finance, and monetary policies in the globalized market capitals in economic growth …... and the...

24

Finance, and monetary policies in the globalized market capitals in economic growth … ... and the problem of controlling a “sensitive” commodity Histories of capital markets and of financial and monetary rules overlap being the former (capitals) strongly influenced by the latter (rules)

-

Upload

estella-snow -

Category

Documents

-

view

217 -

download

0

Transcript of Finance, and monetary policies in the globalized market capitals in economic growth …... and the...

Finance, and monetary policies in the globalized market

capitals in economic growth …

... and the problem of controlling a “sensitive” commodity

Histories of capital markets and of financial and monetary rules overlap

being the former (capitals) strongly influenced by the latter (rules)

Finance, and monetary policies in the globalized market

a stylized timeline:(1) before 1870: strict rules and minor integration(2) 1870-1914: a multilateral system of rules fosters high integration(3) 1914-1945: new restrictions and a trend of capital market dis-integration(4) 1945-1971: a new multilateral set of norms supports a slow integration(5) post-1971: deregulation and the globalization of capital markets

Finance, and monetary policies in the globalized market

once again, a non-linear patterndetermined by three variables that

hardly can be combined together(1) international freedom of capital movements (2) a fixed/stable exchange rate (3) an independent economic policy

one variable must be sacrificed

19th Century: the birth of a global capital market

16th-18th c.: finance’s tecniques transfer and a slow volume increase

1870-1914: market-integrationLondon the financial capitalconsistent increase in capital flowsexpansion to Europe and W. offshhoots

evidence of integration: convergence in interest rates

19th Century: the Age of Gold standard and central banks

two pillars: gold standard and national central banks

(1) The gold standarda call for a common monetary

standard: Conference of Paris (1867)

in the framework of the post Cobden-Chevalier high increase of international trade

19th Century: the Age of Gold standard and central banks

(1) The gold standard

ideas in the air:

(a) monetary coordination does not threat international trade;

(b) an extension of a broader trend to economic standardization

19th Century: the Age of Gold standard and central banks

(1) The gold standard

no formal agreement:

gold vs bi-metallic monetary standard

gold becomes the standard through market integration

1879: Gold standard de facto

19th Century: the Age of Gold standard and central banks

(2) National central bank

two main functions:bank to the government steward of the financial system =

“lender of last resort”

c) coordination among National banks: an idea that slowly becomes common

Between two wars: the disintegration of capital markets

a framework of competitive policies involving finance and currency

global capital considered responsible for 1929 crisis

a decrease in volumes and a non-convergent trend in interest rates

the gold standard “great escape”

Before 1929: the failed attempt

bad legacies from WWI:failure of the Gold standard

competitive devaluation

war reparations

c) searching for a multilateral agreement: Brussels and Genoa conferences

Before 1929: the failed attempt

main issue: fighting currency depreciation to foster free-trade

solutions put forward: (1) gold convertibility, (2) central banks independency, (3) discipline in taxation, (4) assistance for countries with depreciated currency

problem: outdated framework (re-establish the prewar model)

Before 1929: the failed attempt

minor results and big failures: no international trading system rebuilding ... yet, opens to future developments

a wider discipline of a multilateral free-trade, including:fiscal policiesmultilateral finance institutions

BIS: a first “world bank” candidate

During the “Great Depression”

1929 crisis and BIS weakness

London Conference (1933):

the last call for multilateral discipline

a failure determined by crossfire vetos and lack of leadership

After WW 2: the rebuilding of international capital networks

until the 1960s, commodity market integration is not coupled by finance

because capital flows are kept under control

massive public investments (ERP)

but small space for private capital

Bretton Woods and the Age of multilateral institutions

a recap of Bretton Woods agreements

new leaders of world economy: USA (and UK)

a negative target to aim:

“bad” financial and monetary policies of the loosers

Bretton Woods and the Age of multilateral institutions

a different framework: no immediate crisis

a clear target: reconstructing multilateral free-trade

spillovers: a discipline of monetary and financial policies

the birth of multilateral institutions

Bretton Woods and the Age of multilateral institutions

sparring partners negotiate to reduce agreements impact

obtaing a period of transition for par value system enforcement

increasing IMF’s and World Bank’s resources (and later ERP)

delaying the return of fixed exchange rates among currencies

After 1971: a new period of capital market integration

after the 1960s continuing growth of international capital movements

a process coupled by liberalization

investments (public and private) flow around involving the periphery

evidence of strong integration, rapid convergence in interest rates

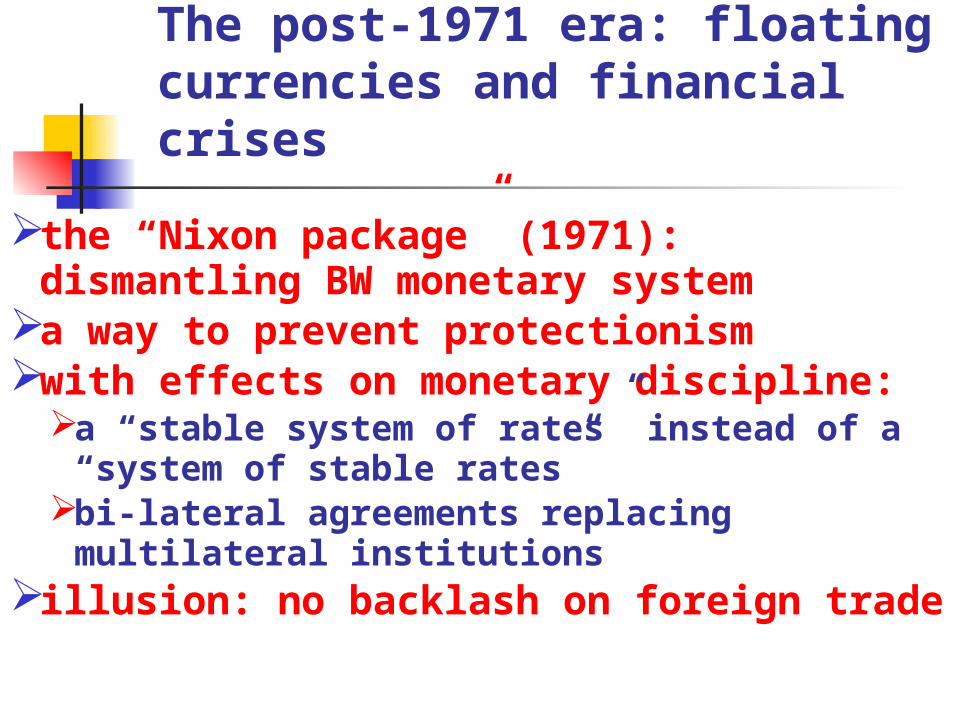

The post-1971 era: floating currencies and financial crises

the “Nixon package” (1971): dismantling BW monetary system

a way to prevent protectionismwith effects on monetary discipline:

a “stable system of rates” instead of a “system of stable rates”

bi-lateral agreements replacing multilateral institutions

illusion: no backlash on foreign trade

The post-1971 era: floating currencies and financial crises

features of the new monetary “non-system”:fixed exchange rates in small countries

Europe’s mini-Bretton Woods: EMS’ “monetary Snake”

coordinated devaluations: Plaza Hotel (1985) the Louvre (1987) agreements

The post-1971 era: floating currencies and financial crises

missing the point: an uncontrolled growth of capital flows

the first sign: the Latin American debt crisis (1982)

and its heavy backlash on tradethe following crises:

Mexico (1994-95); Asian crisis (1997-98); Wall Street crisis (2008-?)

Recent trends in financial and monetary policies: the late 20th c.

a summary of main trends in finance and currency exchange:integration of financial market

new tools and new players

no barriers, no controls, no national solutions

Recent trends in financial and monetary policies: the late 20th c.

a summary of main trends in finance and currency exchange:the new strategy of existing

multilateral institution

IMF tools: conditional loans

the widening of pre-conditions asked for