Finance 129 Background on the Financial Crisis. The Big Picture Problems in Mortgage Market Global...

28

Finance 129 Background on the Financial Crisis

-

date post

19-Dec-2015 -

Category

Documents

-

view

219 -

download

2

Transcript of Finance 129 Background on the Financial Crisis. The Big Picture Problems in Mortgage Market Global...

Finance 129

Background on the Financial Crisis

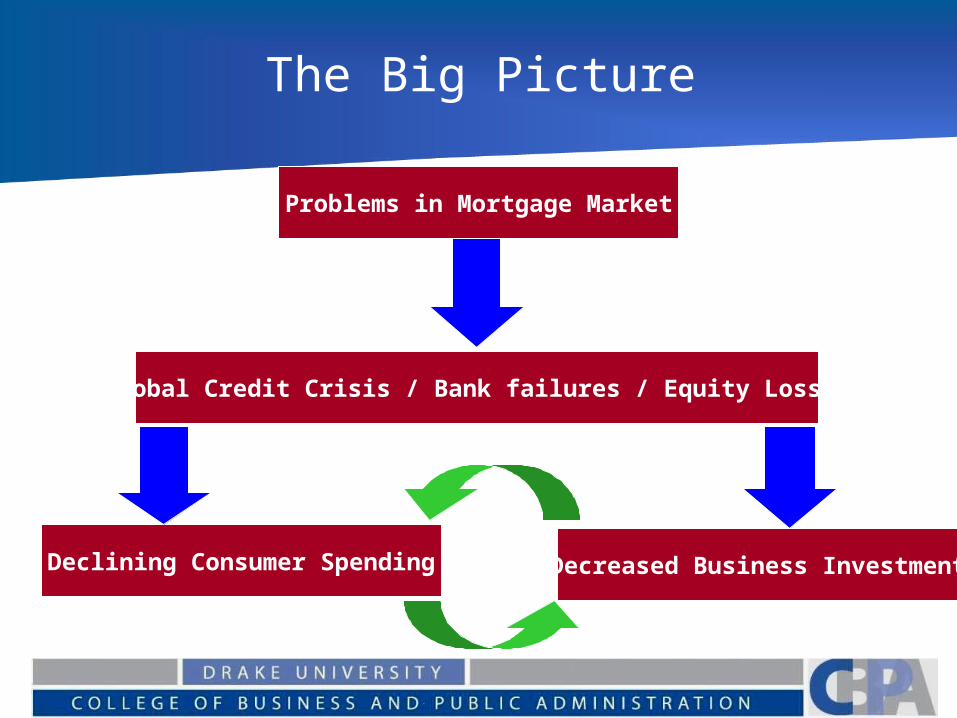

The Big Picture

Problems in Mortgage Market

Global Credit Crisis / Bank failures / Equity Losses

Declining Consumer Spending Decreased Business Investment

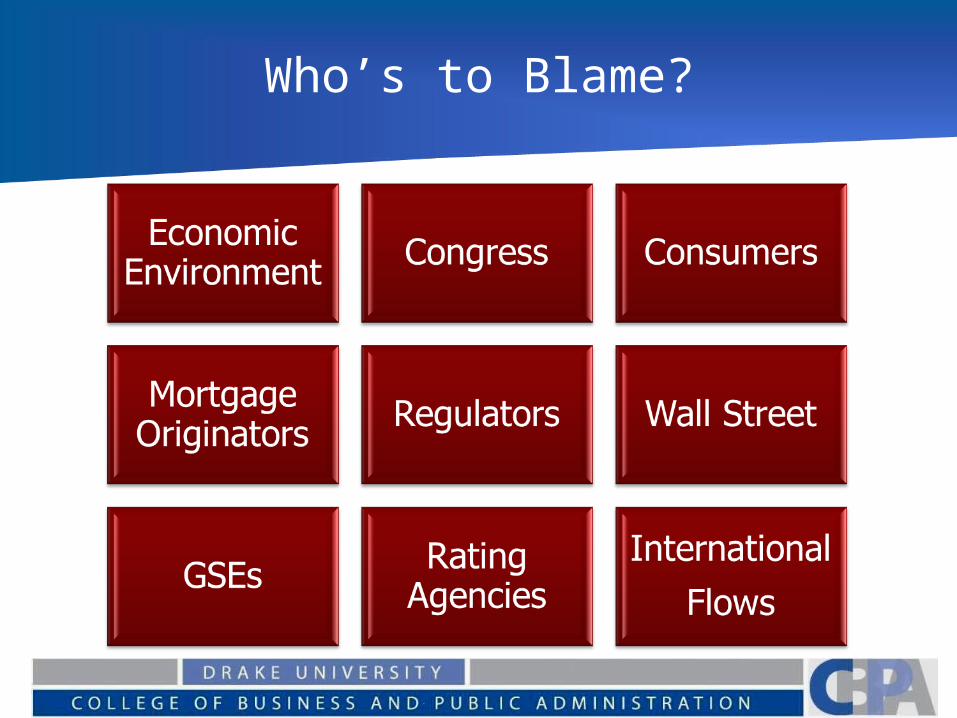

Who’s to Blame?

How Financial Markets Enabled“Keeping up with the Joneses”

New Products

Poor Underwriting

Public Policies Unintended Consequences

Low Rates and International Capital Flows

Products

Underwriting

Policy

Markets

Mortgage Market Developments

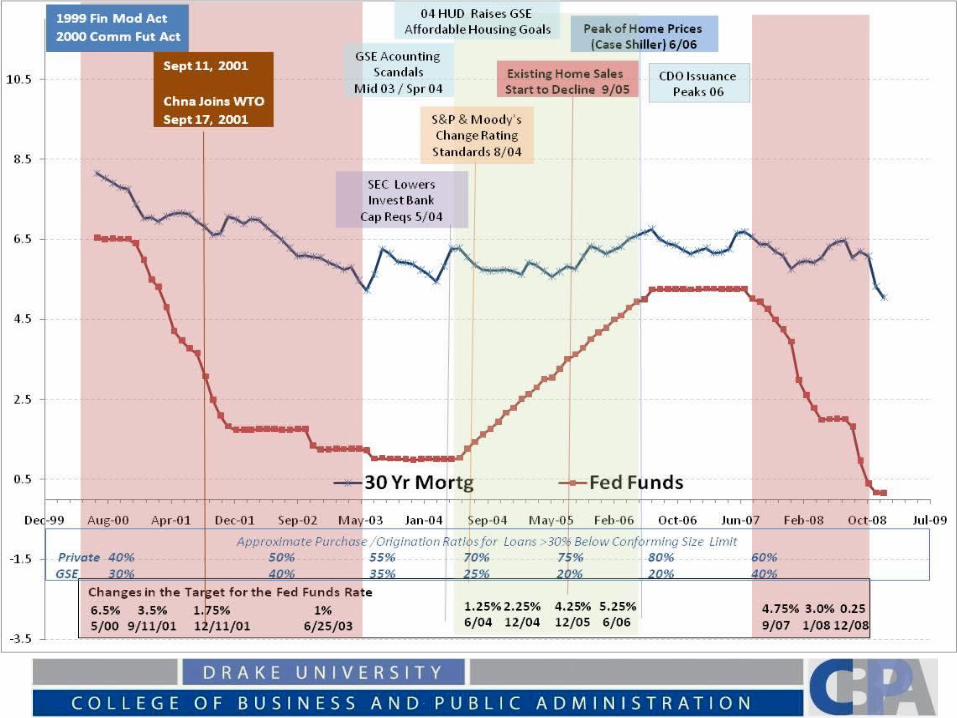

Securitization and new participantsGraham Leach Bliley Financial Modernization Act of 1999Increased Use of Mortgage Brokers2000 Commodity Futures Modernization Act

Increased Access to CreditSubprime, Alt A, Option ARMs

Products

Underwriting

Policy

Markets

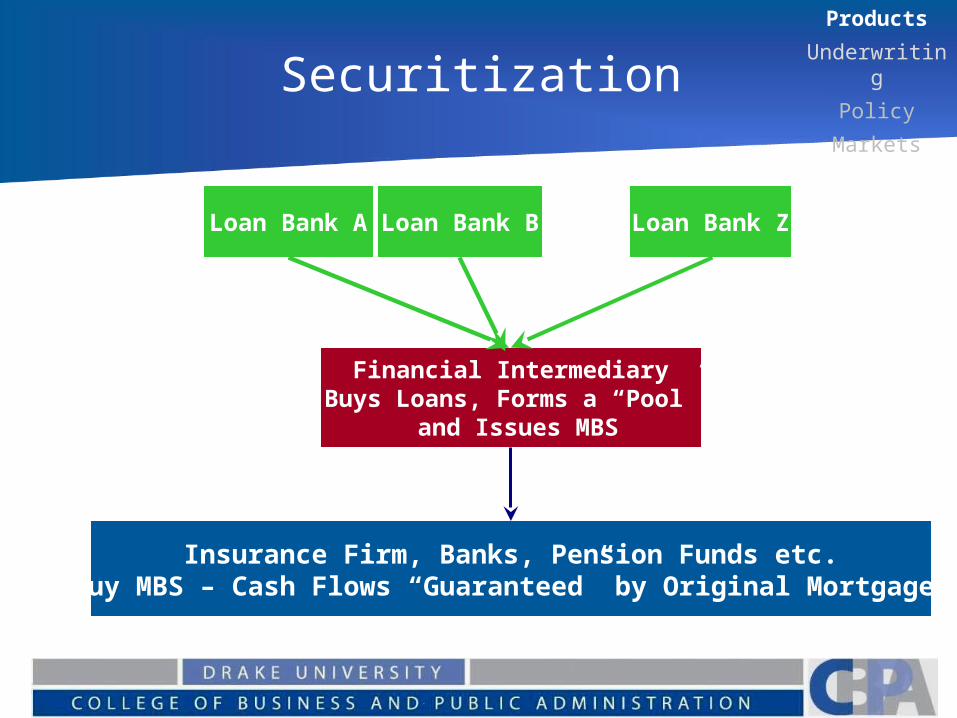

Securitization

Loan Bank B

Financial IntermediaryBuys Loans, Forms a “Pool”

and Issues MBS

Loan Bank A Loan Bank Z

Insurance Firm, Banks, Pension Funds etc.Buy MBS – Cash Flows “Guaranteed” by Original Mortgages

Products

Underwriting

Policy

Markets

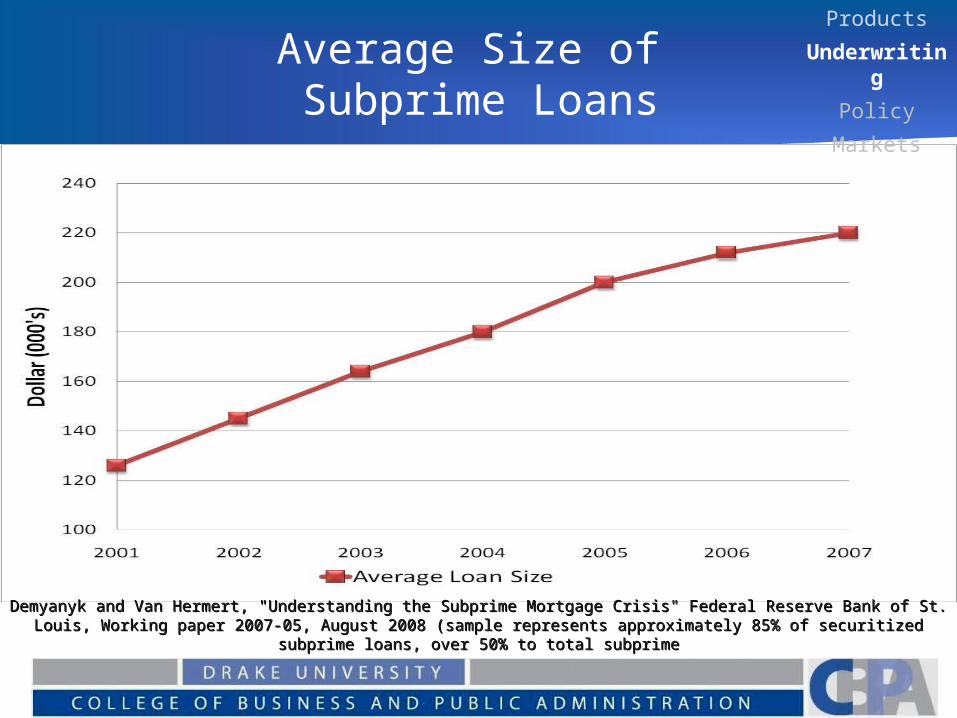

Average Size of Subprime Loans

Demyanyk and Van Hermert, "Understanding the Subprime Mortgage Crisis" Federal Reserve Bank of St. Louis, Demyanyk and Van Hermert, "Understanding the Subprime Mortgage Crisis" Federal Reserve Bank of St. Louis, Working paper 2007-05, August 2008 (sample represents approximately 85% of securitized subprime loans, over Working paper 2007-05, August 2008 (sample represents approximately 85% of securitized subprime loans, over

50% to total subprime50% to total subprime

Products

Underwriting

Policy

Markets

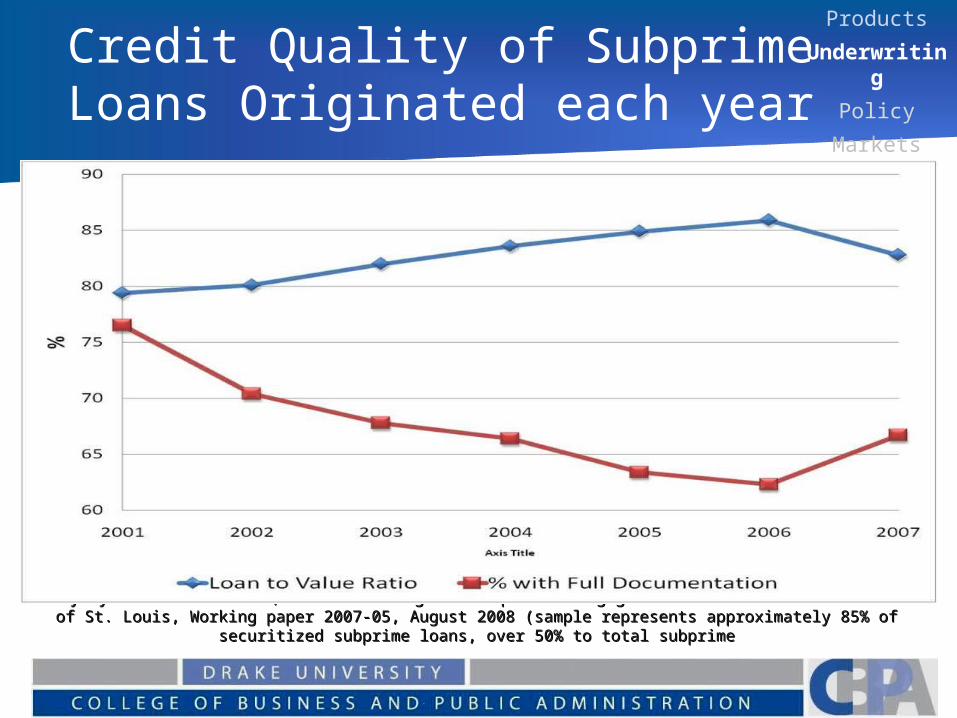

Credit Quality of Subprime Loans Originated each year

Demyanyk and Van Hermert, "Understanding the Subprime Mortgage Crisis" Federal Reserve Bank of St. Louis, Demyanyk and Van Hermert, "Understanding the Subprime Mortgage Crisis" Federal Reserve Bank of St. Louis, Working paper 2007-05, August 2008 (sample represents approximately 85% of securitized subprime loans, Working paper 2007-05, August 2008 (sample represents approximately 85% of securitized subprime loans,

over 50% to total subprimeover 50% to total subprime

Products

Underwriting

Policy

Markets

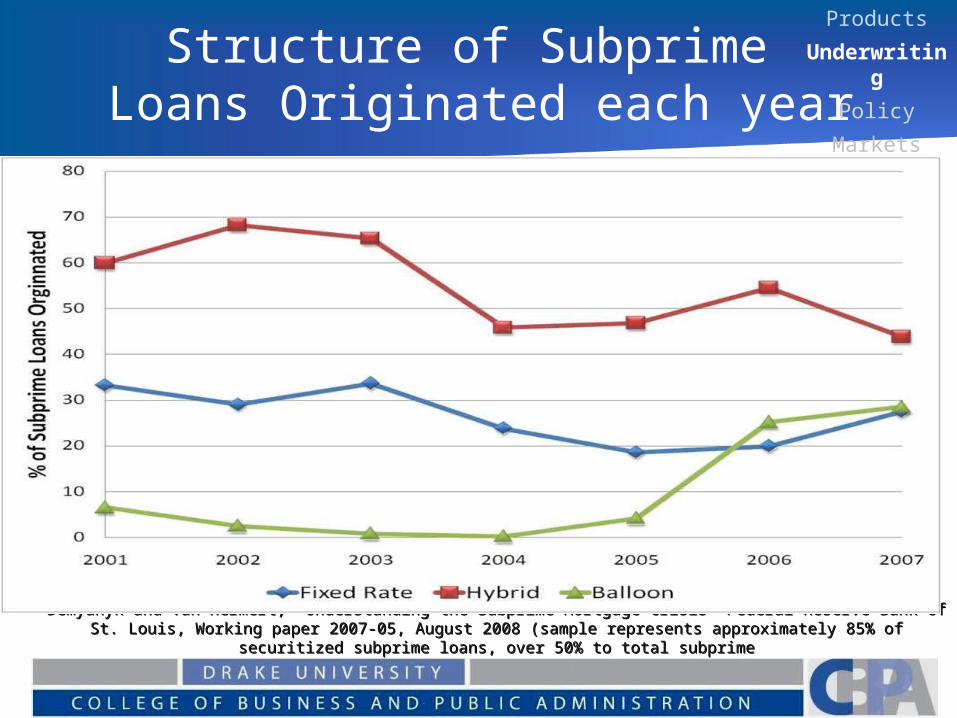

Structure of Subprime Loans Originated each year

Demyanyk and Van Hermert, "Understanding the Subprime Mortgage Crisis" Federal Reserve Bank of St. Louis, Demyanyk and Van Hermert, "Understanding the Subprime Mortgage Crisis" Federal Reserve Bank of St. Louis, Working paper 2007-05, August 2008 (sample represents approximately 85% of securitized subprime loans, Working paper 2007-05, August 2008 (sample represents approximately 85% of securitized subprime loans,

over 50% to total subprimeover 50% to total subprime

Products

Underwriting

Policy

Markets

Impact of Subprime Loans on Home Ownership

"SubPrime Lending: A Net Drain on Homeownership," Center for Responsible Lending: March 2007"SubPrime Lending: A Net Drain on Homeownership," Center for Responsible Lending: March 2007

Products

Underwriting

Policy

Markets

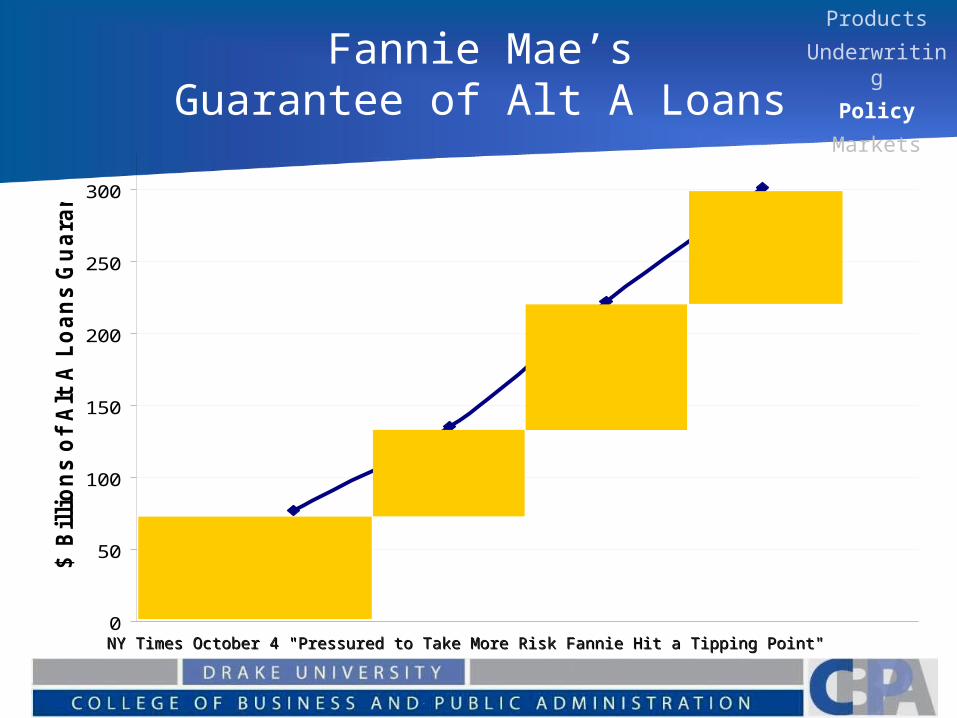

NY Times October 4 "Pressured to Take More Risk Fannie Hit a Tipping Point"NY Times October 4 "Pressured to Take More Risk Fannie Hit a Tipping Point"

Fannie Mae’sGuarantee of Alt A Loans

0

50

100

150

200

250

300

$ B

illions o

f Alt

A L

oans G

uara

nte

ed

2005$58

Billion Added

2006$87

BillionAdded

2007$79

BillionAdded

2004 & Before$77 Billion Total

Products

Underwriting

Policy

Markets

Blaming Fannie and Freddie?

No - Fannie and Freddie were small relative to the entire market.

Combined Subprime Purchases (% of Market)**Consumer demand created rapid prince increase

Yes – Overall Size put them at risk for any Mortgage Market problem

Securitizing more risky loans opened door for Private securitization

Gramlich, E. "Subprime Loans: America's Latest Boom an Bust" 2007 ** "how HUD Mortgage Gramlich, E. "Subprime Loans: America's Latest Boom an Bust" 2007 ** "how HUD Mortgage Policy Fed the Crisis", Washington Post June 10, 2008Policy Fed the Crisis", Washington Post June 10, 2008

Products

Underwriting

Policy

Markets

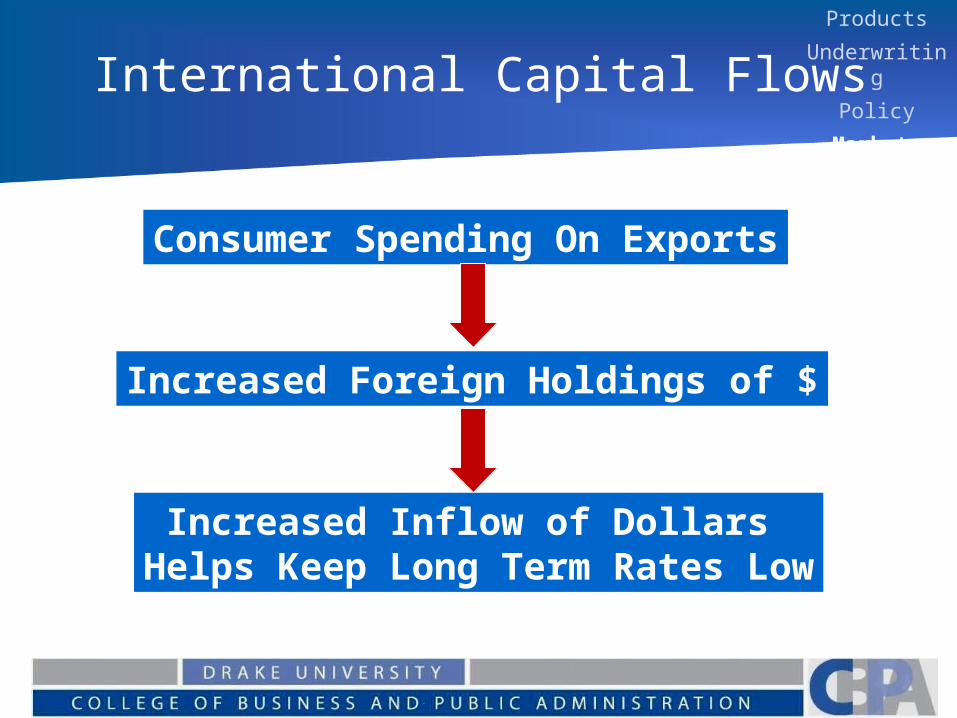

International Capital Flows

Consumer Spending On Exports

Increased Foreign Holdings of $

Increased Inflow of Dollars Helps Keep Long Term Rates Low

Products

Underwriting

Policy

Markets

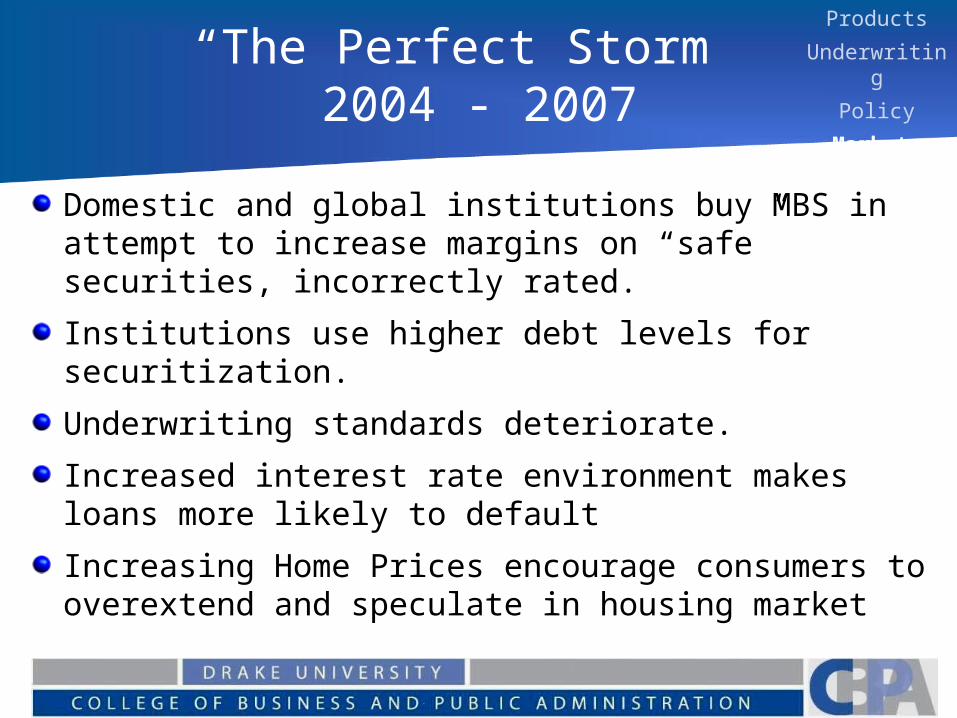

“The Perfect Storm” 2004 - 2007

Domestic and global institutions buy MBS in attempt to increase margins on “safe” securities, incorrectly rated.

Institutions use higher debt levels for securitization.

Underwriting standards deteriorate.

Increased interest rate environment makes loans more likely to default

Increasing Home Prices encourage consumers to overextend and speculate in housing market

Products

Underwriting

Policy

Markets

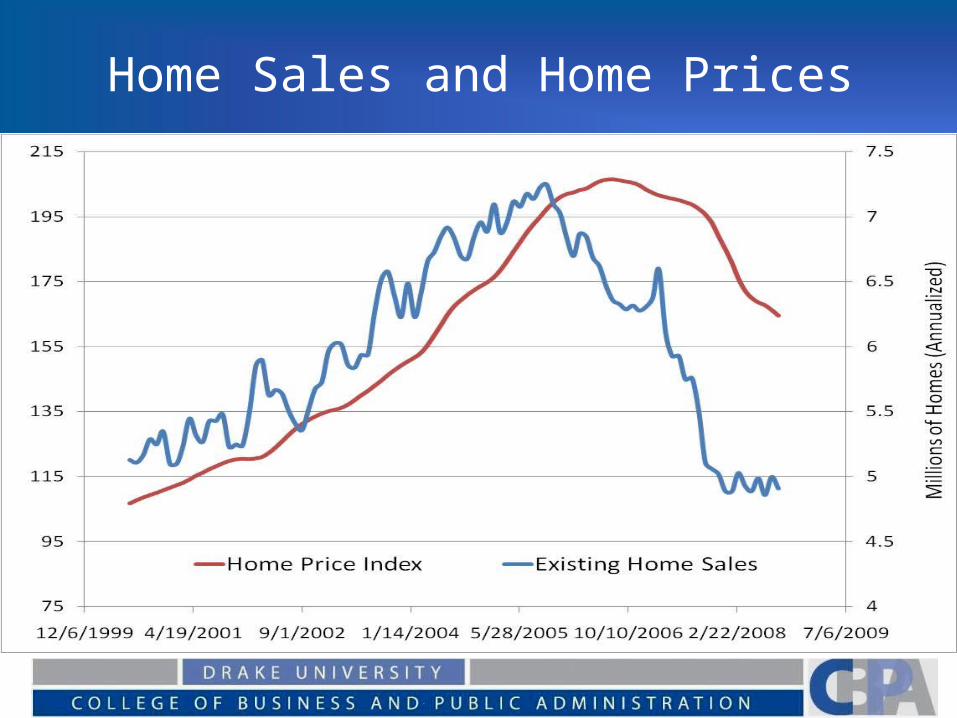

Home Sales and Home Prices

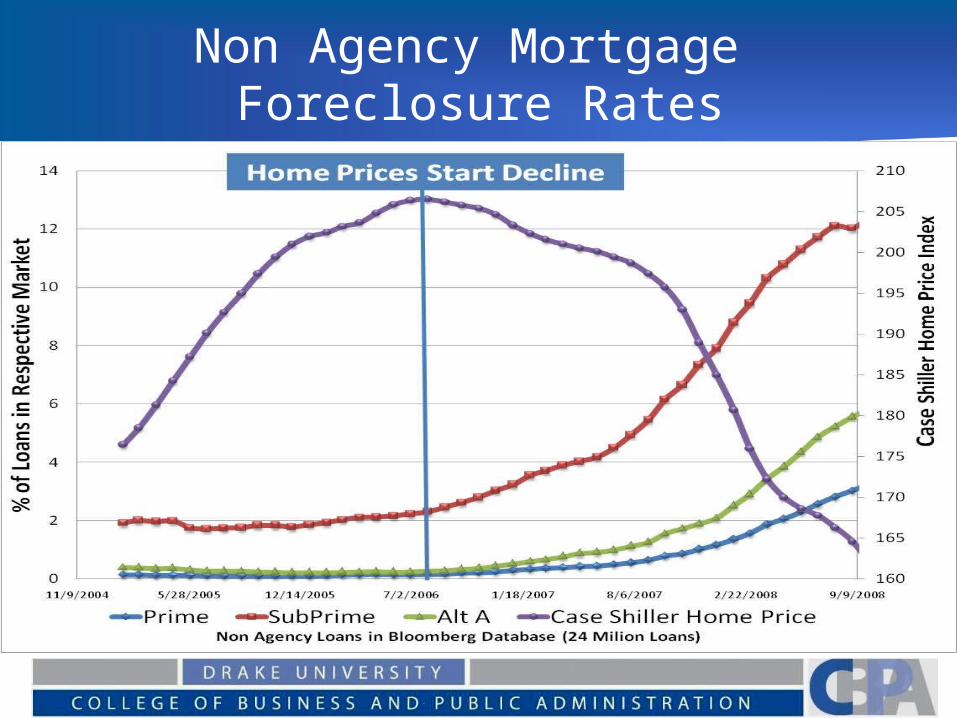

Non Agency Mortgage Foreclosure Rates

Response of Consumers

Increased access to credit and delusional optimism resulted in:

Short-Term Speculative FocusBorrowing More and Saving Less

Case Study: Natalie Brandon

1985 Buys $105,000 house 30 Year fixed rate loan Payment = $770

2000-2006Paid penalties to Refi 5 times in 5 years Yearly income = $100,000 2006 New Loan $625,500 2/28 7.99% teaserPayment = $4,585

Fall 2007Home Value = $450,000Attempt to Refi for 40 years at 6% Fails

Borrowing More & Saving Less

Equity Prices Compared to Past Recessions

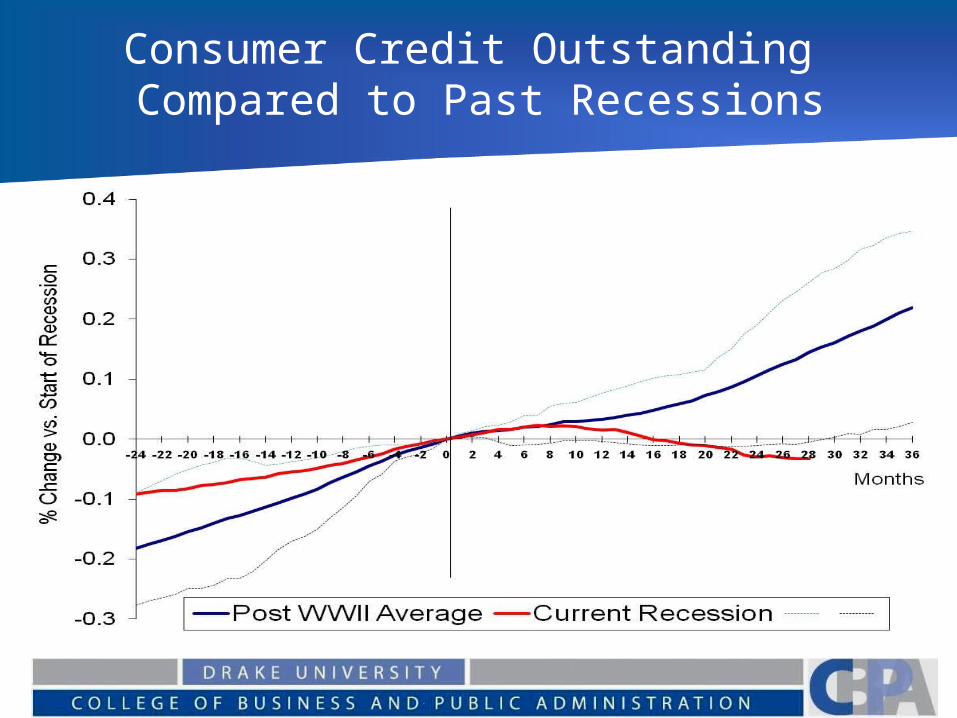

Consumer Credit Outstanding Compared to Past Recessions

Impact of the Crisis

Increase in Precautionary Saving

Lost Wealth from Equity Declines

High Unemployment

Consumer Confidence hits Record Lows

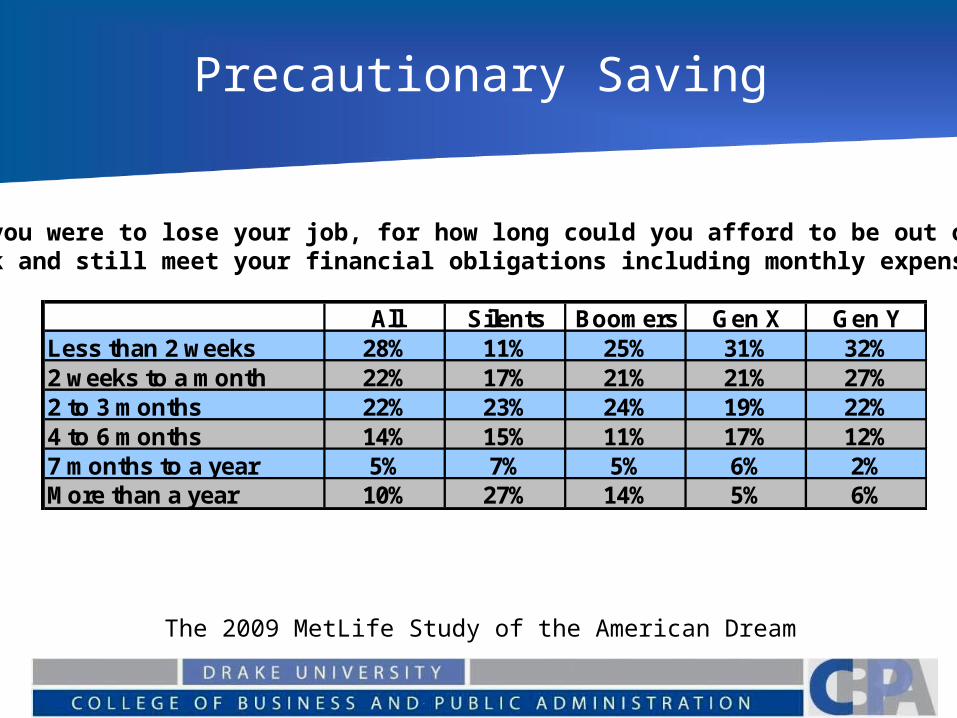

Precautionary Saving

All Silents Boomers Gen X Gen YLess than 2 weeks 28% 11% 25% 31% 32%2 weeks to a month 22% 17% 21% 21% 27%2 to 3 months 22% 23% 24% 19% 22%4 to 6 months 14% 15% 11% 17% 12%7 months to a year 5% 7% 5% 6% 2%More than a year 10% 27% 14% 5% 6%

If you were to lose your job, for how long could you afford to be out of work and still meet your financial obligations including monthly expenses?

The 2009 MetLife Study of the American Dream

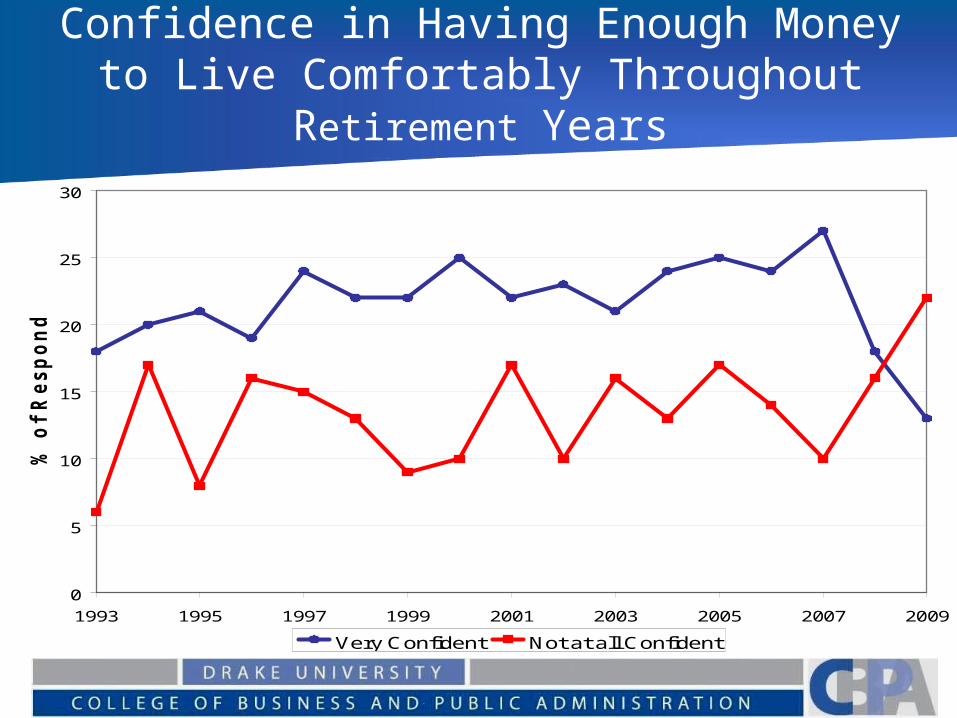

Confidence in Having Enough Money to Live Comfortably Throughout Retirement

Years

0

5

10

15

20

25

30

1993 1995 1997 1999 2001 2003 2005 2007 2009

% o

f R

esp

on

den

ts

Very Confident Not at all Confident

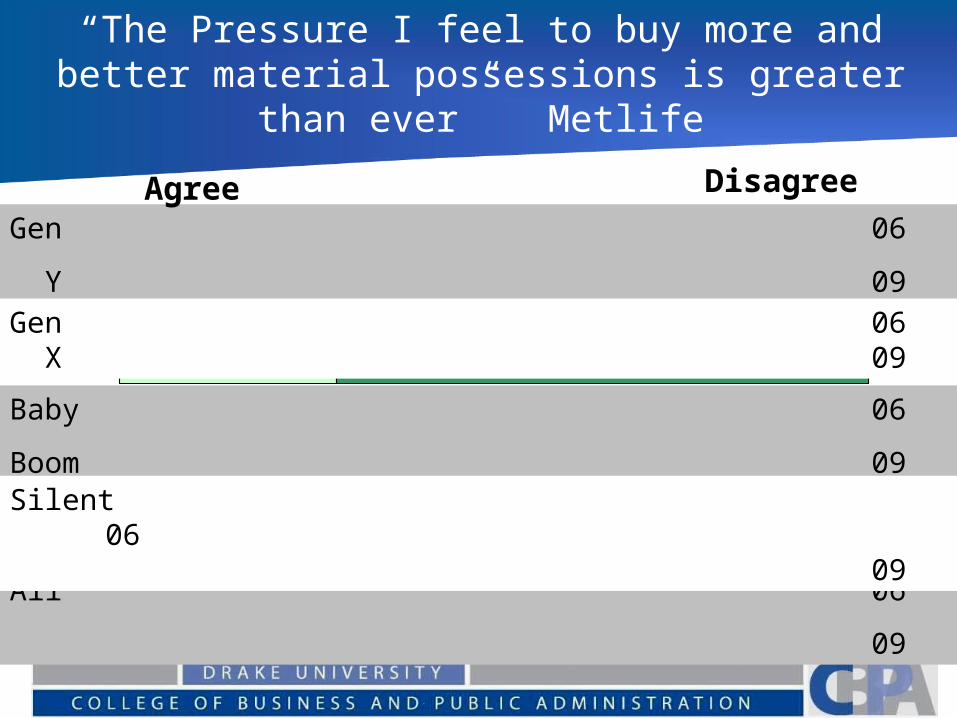

“The Pressure I feel to buy more and better material possessions is greater than ever”

Metlife

26%

46%

10%

25%

18%

39%

29%

53%

47%

66%

74%

54%

90%

75%

82%

61%

71%

47%

53%

34%Gen 06

Y 09

Baby 06

Boom 09

All 06

09

Gen 06 X 09

Silent 0609

Agree Disagree

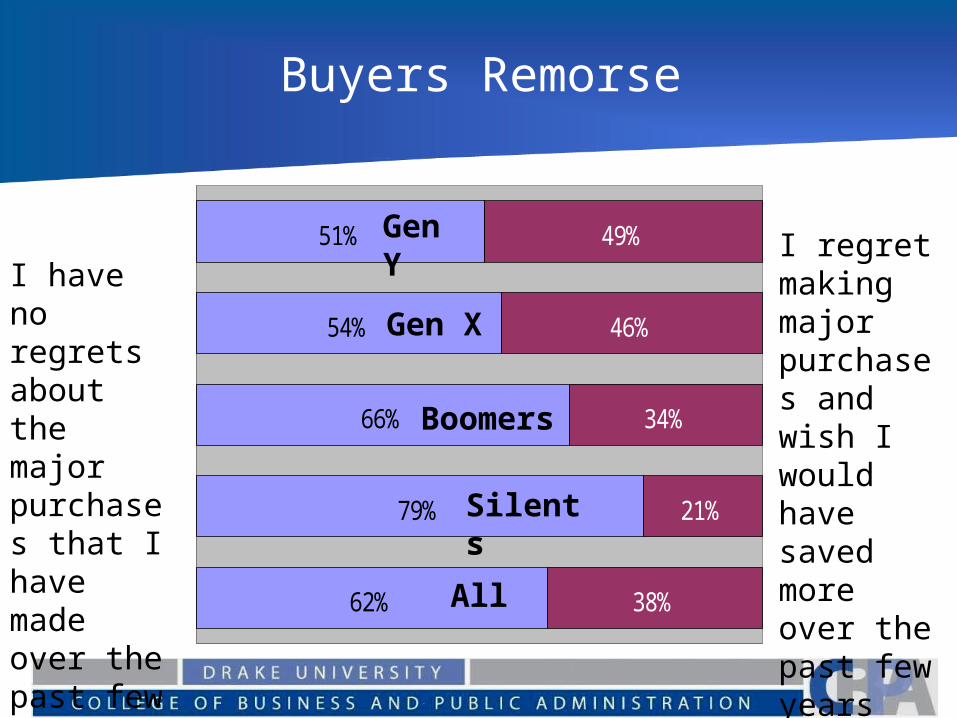

Buyers Remorse

62%

79%

66%

54%

51%

38%

21%

34%

46%

49%

I have no regrets about the major purchases that I have made over the past few years

I regret making major purchases and wish I would have saved more over the past few years

Gen Y

Gen X

Boomers

Silents

All

The Crystal Ball – The Big Picture

How will Consumers Respond?Precautionary or Long Term Savings?Lost Faith in Investment Planning?View of home ownership

Corporate EarningsFinancial Markets and Regulation

Regulatory ChangesLong Term Inflation FearsMonetary and Fiscal PolicyInterest Rates