Final work: specific problems related to inventories ... · 8 . Use with The Audit Process:...

29

Use with The Audit Process: Principles, Practice and Cases, 6 th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015 Chapter 13 Final work: specific problems related to inventories, construction contracts, trade payables and financial liabilities

-

Upload

nguyenhanh -

Category

Documents

-

view

221 -

download

1

Transcript of Final work: specific problems related to inventories ... · 8 . Use with The Audit Process:...

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Chapter 13

Final work: specific problems related to

inventories, construction contracts, trade payables

and financial liabilities

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Learning objectives • To apply the general principles for determining the validity of the amount attributed to

inventories, construction contracts, trade payables and financial liabilities

• To describe the inherent risks affecting inventories, construction contracts, trade payables and financial liabilities, and explain the controls introduced by management, and the detection procedures carried out by the auditor to keep audit risk to acceptable low levels.

• To evaluate a company’s system for the determination of physical existence, condition and ownership of inventories and construction contracts.

• To explain how identification by the auditor of judgements by management in relation to inventories, construction contracts, trade payables and financial liabilities helps to direct audit effort to critical areas.

• To draft audit programmes to test the amounts attributed to inventories, construction contracts, trade payables and financial liabilities.

2

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Inherent risks affecting inventories • Change in demand for company products

• Production levels may be changed ‘normal’ levels

• Defects in product lines

• Inventories prone to theft

• Cost allocations difficult in complex production process

• Cost allocations arbitrary in joint product situation

• Significant variances from standard costs

• Increased competition

• Complex calculation of overheads

• Unreliable inventory records

• Inventories at locations not of the organization

• Poor physical controls

• Lack of independence and experience of inventory count staff

• Degree to which inventory levels fluctuate

• Inventories requiring special procedures at count 3

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Controls to reduce the impact of inherent risk affecting inventories

• Periodic inventory counts often necessary to establish inventory quantities, condition and ownership and the accuracy of inventory records, if any.

• Apart from a satisfactory control environment, expect controls in the following areas: – Acquisitions of inventories

– Safeguarding inventories

– Determining existence, condition and ownership at period-end dates

– Valuation of inventories

4

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Analytical procedures

• The inventories figure in the financial statements bears direct relationships to other figures, such as: – Inventories to sales or cost of sales

– Raw material inventories to purchases – Impact on gross profit %

– Impact on current ratio

5

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Acquisitions of inventories - controls

• The point at which title in the inventory item passes from the supplier to the company must be known.

• If purchases are properly controlled entry into inventory records, if any, is more likely to be correct.

• Good purchases records will aid cut-off.

6

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Safeguarding inventories – controls

• Physical safeguards over inventories – the more valuable and/or moveable the tighter.

• Restriction of access via documentation – release if properly authorized.

• Environment preventing deterioration and allowing easy identification.

7

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Disposals of inventories whether by sale or otherwise – controls

• Normal sales of inventory have been considered in previous chapters.

• Inventories disposed of outwith the normal sales system to receive special approval at an appropriate level.

8

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Determining existence, condition and ownership at period-end dates – controls

• Adequate procedures for physical inventory counts.

• Reconciliation of quantities counted to inventory records.

• Investigation of significant differences (control risk factor).

• Physical inventory counts prove existence and identify inventories in poor physical condition and help clarify ownership.

• Cut-off procedures – control to establish proper relationship between inventory, purchases and sales.

9

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Valuation of inventories

• The basic principle – lower of cost and net realizable value.

• Controls to ensure the costing and other records are reliable and produce inventory values on a consistent basis.

• If standard costs are used to value – important control is analysis of variances and adjustment of standards.

10

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Inventories – management assertions

11

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Inventory cut-off

• Note basic rules on cut-off

• Typical cut-off points at boundaries (high risk): – Purchase of raw materials and components – Requisitioning of raw materials by production – Requisitioning of components by assembly – Transfer of goods to finished goods store – Sale of finished goods

• Management procedures: – Appoint an individual with special responsibility for ensuring accurate cut-off – Restrict movement of goods during count – If movements – responsible individual consulted

• Auditors test operation of procedures and record numbers of GRNs, and other movement documents

12

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Activity 13.5 – inventory count

• Review the inventory-taking instructions of Greenburn Limited (Case study 13.2) and list those features:

1.That would serve to ensure that the inventories were properly counted and recorded.

2.That might be regarded as weaknesses in the system for counting and recording the inventories.

13

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

The inventory count observation, purposes and procedures

• Auditors observe count

• Test counts (test of controls) performed

• Substantive tests of detail – inventory quantities, condition, cut-off

• Inventory quantities determined from inventory records if: – System of control over the inventory records is adequate. – Inventory records subject to regular, controlled counting. – No significant differences between records and count.

• Audit procedures include: – Observe inventory count during year. – Compare test count with records. – Test for cut-off at the count date and the balance sheet date. – If necessary, restricted test count at balance sheet date.

• Work in progress – auditors may have to rely on experts.

• Inventories at third parties and inventory at branches – special procedures.

14

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Have all production costs and inventory values been properly determined?

• Rules for calculation: cost:

Cost is calculated for different categories

Cost comprises cost of purchase and costs of conversion – Activity 13.6 – direct material costs (p 529) – Activity 13.7 – production overheads (p 530) – Activity 13.8 – overheads to present location and condition (p 531)

• Rules for calculation: net realizable value (NRV):

NRV is actual or estimated selling price less all further costs of production and costs yet to be incurred in marketing, selling and distributing. – Activity 13.9 – questions related to the difficulty of determining NRV (531-2)

15

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Activity 13.9 Net realizable values

a) Explain why the audit of NRV value is more problematic than the audit of inventory cost. What specific steps might the auditor take to check whether valuing at NRV would be appropriate?

b) What audit procedures would the auditor use in determining whether costs of production to complete work in progress at the balance sheet date are appropriate?

c) What matters would the auditor consider in respect of costs yet to be incurred in marketing, selling and distributing the inventory? What audit procedures would be appropriate?

16

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Other matters affecting inventories

• Disclosure of the effect of changes in basis of valuation.

• Have all calculations affecting inventory valuation been properly made?

• Can the inventories be freely disposed of by the company?

17

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Valuation of construction contracts (1)

• Audit objective one: costs incurred to date are genuine, accurate and complete.

• Audit objective two: stages of completion and costs of such stages have been properly determined.

• Audit objective three: invoices issued to customers in respect of construction contracts are properly calculated in accordance with contract and are in respect of all stages completed certified by the surveyor.

• Audit objective four: cash received from clients is genuine, complete and accurate. In particular, cash received has been properly allocated to contracts.

18

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

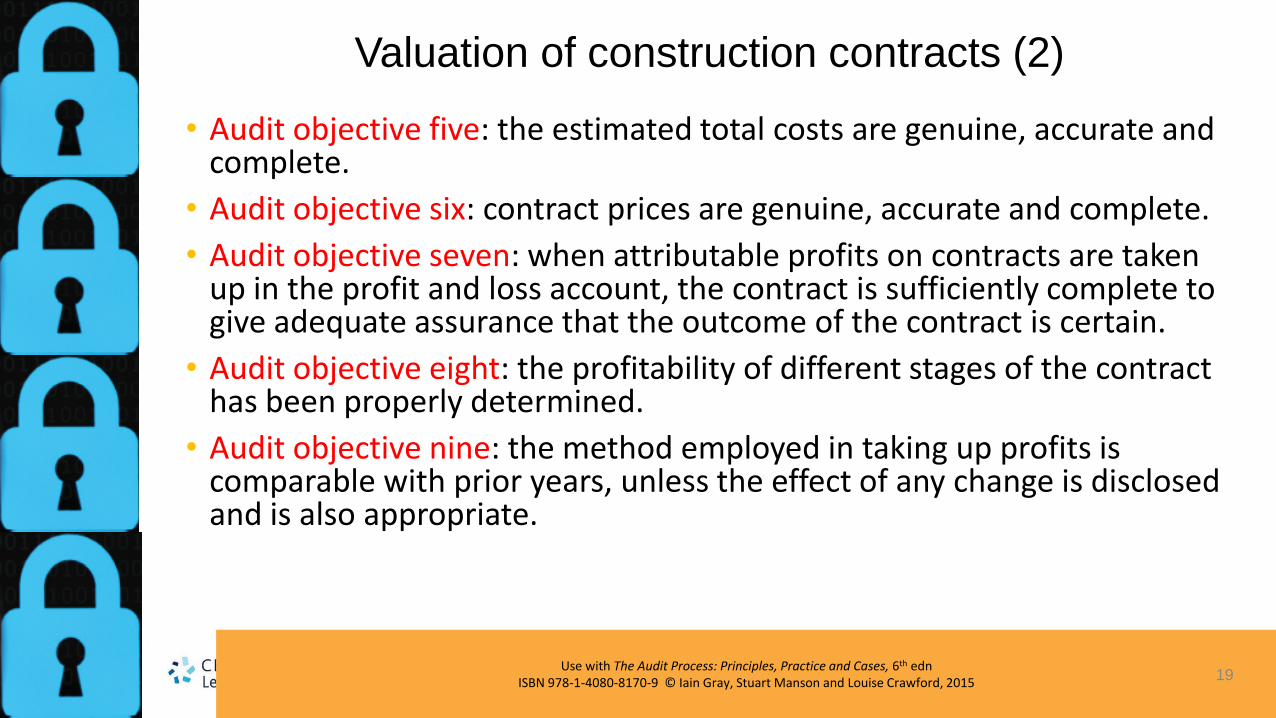

Valuation of construction contracts (2)

• Audit objective five: the estimated total costs are genuine, accurate and complete.

• Audit objective six: contract prices are genuine, accurate and complete.

• Audit objective seven: when attributable profits on contracts are taken up in the profit and loss account, the contract is sufficiently complete to give adequate assurance that the outcome of the contract is certain.

• Audit objective eight: the profitability of different stages of the contract has been properly determined.

• Audit objective nine: the method employed in taking up profits is comparable with prior years, unless the effect of any change is disclosed and is also appropriate.

19

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Trade payables and purchases- inherent risks

• Material variances from standard costs

• Suppliers experiencing difficulties

• Significant changes in terms of trade with suppliers

• Material increase in the age of trade payables

• Major changes in the nature of purchases

• Entity has a history of above average returns of goods purchased

20

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

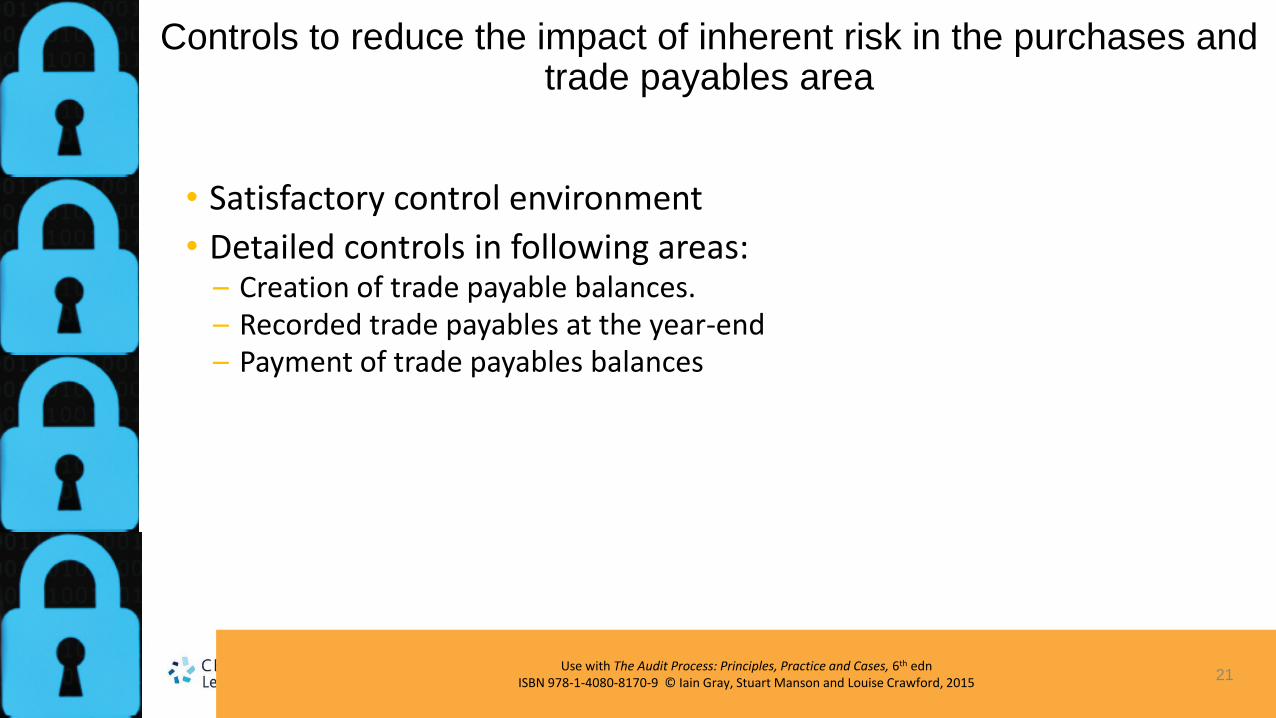

Controls to reduce the impact of inherent risk in the purchases and trade payables area

• Satisfactory control environment

• Detailed controls in following areas: – Creation of trade payable balances. – Recorded trade payables at the year-end – Payment of trade payables balances

21

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Analytical procedures in the purchases and trade payables area

• Purchases and trade payables bear direct relationships to other figures: – Cost of goods sold to trade payables (days) – Purchases affect cost of goods sold and GP% – Purchases affect other expense headings – Impact of trade payables on the acid test ratio – Sales to related support expenditure (e.g. expected claims) – Material unrecorded purchases/trade payables cause ratios to vary from

expectation and would prompt the auditor to be particularly careful

• See Kothari Limited (Case study 12.1) and Powerbase plc (Case study 10.1)

22

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Purchases and trade payables – management assertions and audit work

• Recorded trade payables at the year-end – see table on page 544.

• Search for unrecorded liabilities.

• Consistency in application of accounting standards.

• Is cut-off accurate?

• Disclosure of trade payables payable in the short, medium and long term.

• Payment of trade payables balances.

• Purchases and trade payables audit programme at the year-end – see short audit year-end situations affecting purchases and trade payables in this section.

23

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

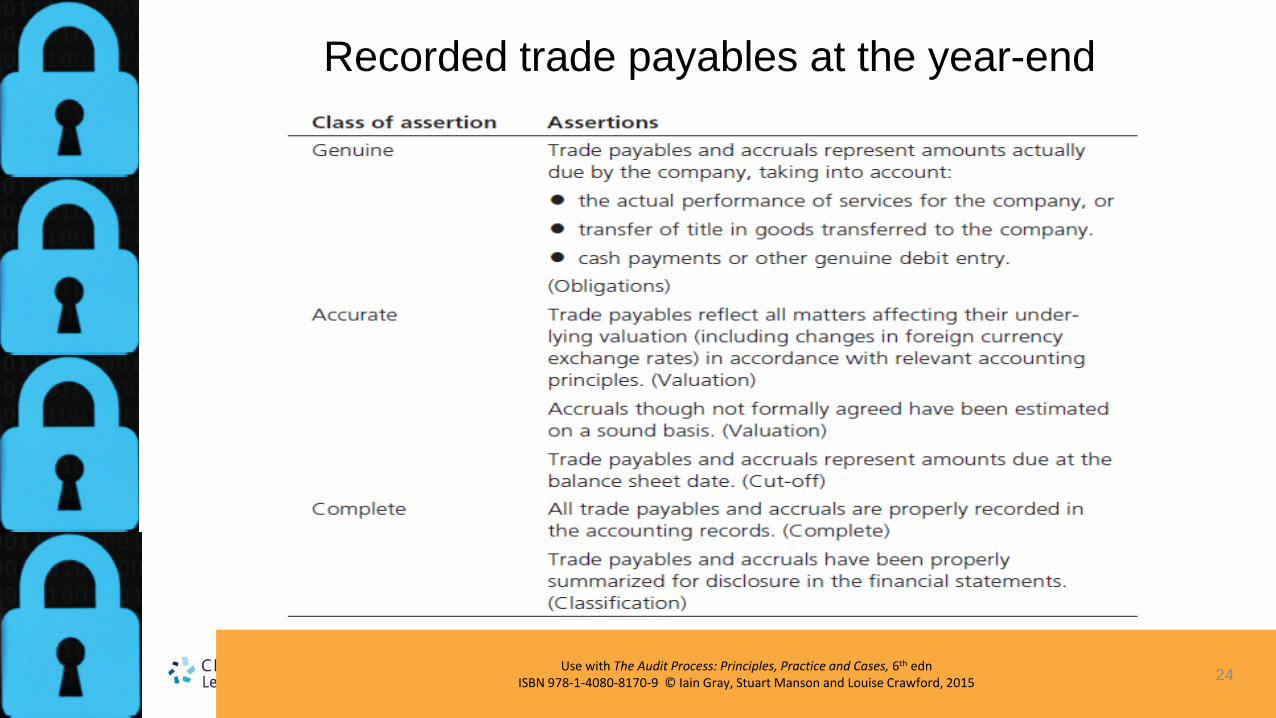

Recorded trade payables at the year-end

24

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Activity 13.7 – year-end situations (1)

• Situation 1: A is a glass manufacturer and requires high-quality sand from Australia for its production of special precision glass products. At the year-end, sand is on board a ship in the middle of the Indian Ocean. What audit steps would you take to ensure related liabilities have been properly recorded and reflected in the financial statements?

• Situation 2: the audit programme for purchases and trade payables of B includes the following: Examine the company’s reconciliations between suppliers’ statements and purchase ledger balances. You discover that company B has not made such reconciliations and on selecting suppliers’ statements for comparison with purchase ledger balances you find many material differences between the two. Suggest further audit steps.

25

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Activity 13.7 – year-end situations (2)

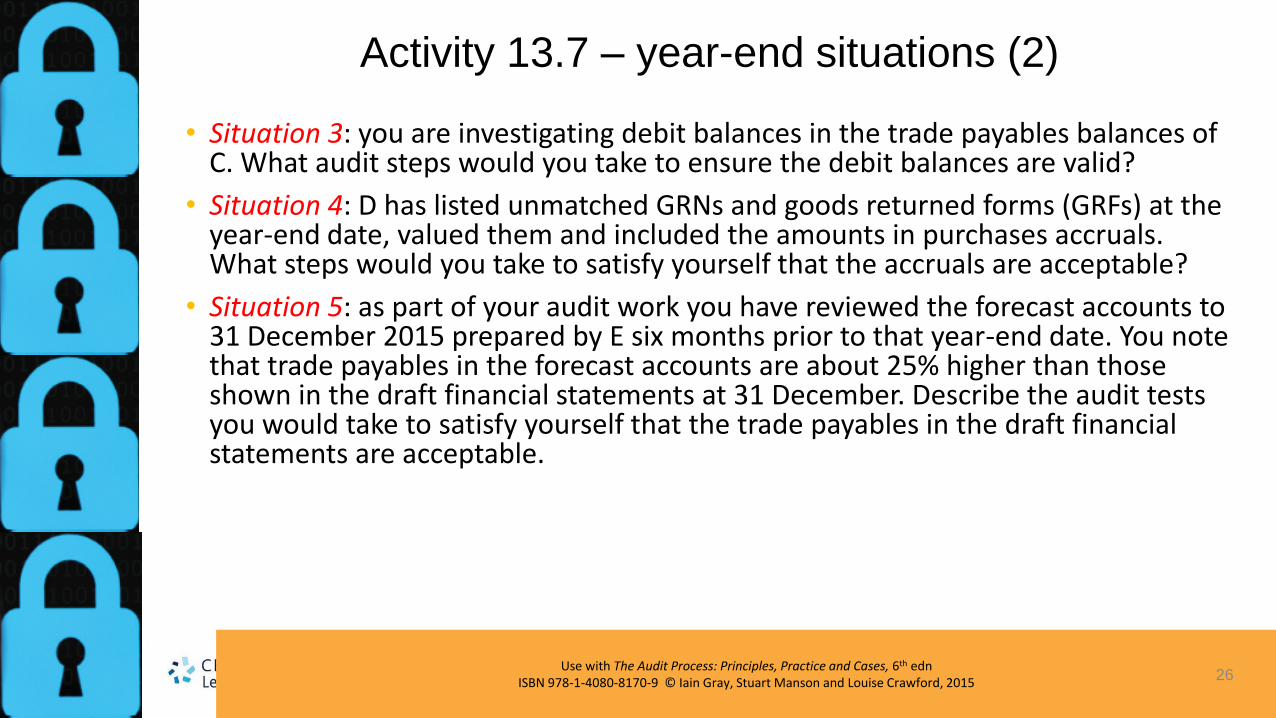

• Situation 3: you are investigating debit balances in the trade payables balances of C. What audit steps would you take to ensure the debit balances are valid?

• Situation 4: D has listed unmatched GRNs and goods returned forms (GRFs) at the year-end date, valued them and included the amounts in purchases accruals. What steps would you take to satisfy yourself that the accruals are acceptable?

• Situation 5: as part of your audit work you have reviewed the forecast accounts to 31 December 2015 prepared by E six months prior to that year-end date. You note that trade payables in the forecast accounts are about 25% higher than those shown in the draft financial statements at 31 December. Describe the audit tests you would take to satisfy yourself that the trade payables in the draft financial statements are acceptable.

26

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Financial liabilities

• In the first place a financial liability would be stated at its original value.

• However, IFRS 9 states that ‘an entity shall classify all financial liabilities as subsequently measured at amortized cost using the effective interest method’.

• although there are certain exceptions, including where a ‘fair value’ of the liability is available.

27

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

Financial liabilities

• Assertions on page 552

28

Use with The Audit Process: Principles, Practice and Cases, 6th edn ISBN 978-1-4080-8170-9 © Iain Gray, Stuart Manson and Louise Crawford, 2015

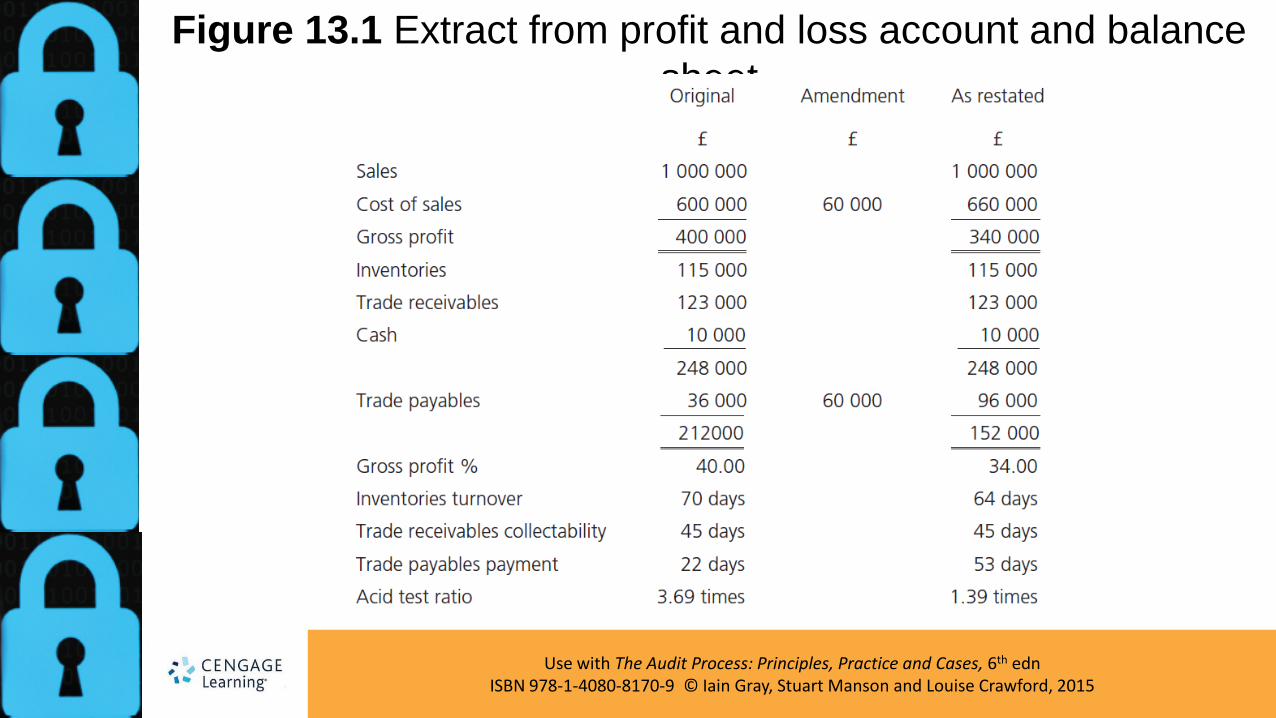

Figure 13.1 Extract from profit and loss account and balance

sheet