FINAL STUDY GUIDE Accounting 1120. 1. What is depreciation? Which plant asset is not depreciated?...

28

FINAL STUDY GUIDE Accounting 1120

-

date post

21-Dec-2015 -

Category

Documents

-

view

226 -

download

2

Transcript of FINAL STUDY GUIDE Accounting 1120. 1. What is depreciation? Which plant asset is not depreciated?...

FINAL STUDY GUIDE

Accounting 1120

1. What is depreciation? Which plant asset is not depreciated?

Depreciation is the allocation of a plant asset’s cost to expense over its useful life. It is NOT a process of valuation It does NOT mean that the business sets aside cash to

replace an asset when it is used up

LAND is not depreciated.

2. Amount of accumulated Depreciation

32,000-4,000=28,00028,000 / 4 (years of useful life) = 7,000

Year Accumulated Depreciation

Total

May 1, 2008 – April 30, 2009 7,000 7,000

May 1, 2009 – April 30, 2010 7,000 14,000

May 1, 2010 – April 30, 2011 7,000 21,000

May 1, 2011 – December 31, 2011 (8 months) = 7,000 / 12=583.333* 8 = 4,666.67

4,666.67 25,666.67

(B)

3. Long-Term/Short-Term Liabilities

Long Term Liabilities Obligations not expected to be paid within the longer

of one year or the company's operating cycle

Short Term Liabilities Obligations that will be paid within one year or less

4. Accrued Interest Expense

4,000*.06*2/12 = $40

5. Characteristics of a Partnership

Characteristic Advantage/Disadvantage

Limited Life Disadvantage

Mutual Agency Disadvantage

Unlimited Liability Disadvantage

Co-Ownership of Property Advantage

No Partnership Income Tax Advantage

6. Balance of Retained Earnings

Beginning Retained Earnings + Net Income = New Balance Retained Earnings 72,000+8,000 = $80,000

Retained Earnings – Dividend Payment 80,000-7,450 = 72,550

7. Journal Entry for Sale of Common Stock

Journal Entry – Sale of Common Stock

Cash (12,000 shares * $11 market price) 132,000

Common Stock (12,000*8 (par value)) 96,000

Paid-in Capital in Excess of Par (12,000 *3)

36,000

8. Journal Entry for Issuance of Bonds

Journal Entry – Issuance of Bonds

Cash 183,750*

Premium on Bonds Payable 8,750

Bonds Payable 175,000

*175,000*1.05

9. Statement of Cash Flow Sections

Cash flows from operating activities Depreciation, increases and decreases in inventory,

accounts receivable, accounts payable, accrued liabilities

Cash flows from investing activities Acquisition or sale of plant assets

Cash flows from financing activities Notes payable, stocks (including dividends, treasury

stock), bonds – borrowing money and repaying creditors

10. Journal Entry to Record Warranty Expense

Journal Entry – Warranty Expense

Warranty Expense (225,000*.03) 6,750

Estimated Warranty Payable (or Liability) 6,750

11. Amounts Received in Advance

Amounts received in advance from customers for future products or services are __liabilities___.

12. Partnership Equity Balance

$72,000 (agreed upon market value of the asset) – 15,000 (note payable secured by the asset) = 57,000

13. Cumulative Preferred Stock Dividends

1,500 (shares) * 25 (par value) * .04 = 1,500 dividends owed to preferred stockholders

First year – paid 1,100 dividends – still owe 400

Second year – paid 400 from last year + 1,500 from this year = 1,900

14. Stock Split

The par value = $4 ($12 / 3)Number of shares outstanding = 45,000

(15,000 * 3)Market Value = $8 ($24 /3)

15. Journal Entry to Record Stock Dividend

Journal Entry – Stock Dividend Declaration

Retained Earnings 25,000 (shares) * 18 (market value) * .12 (stock dividend %)

54,000

Common Stock (25,000*10*.12) 30,000

Paid-in-Capital in Excess, Common 24,000

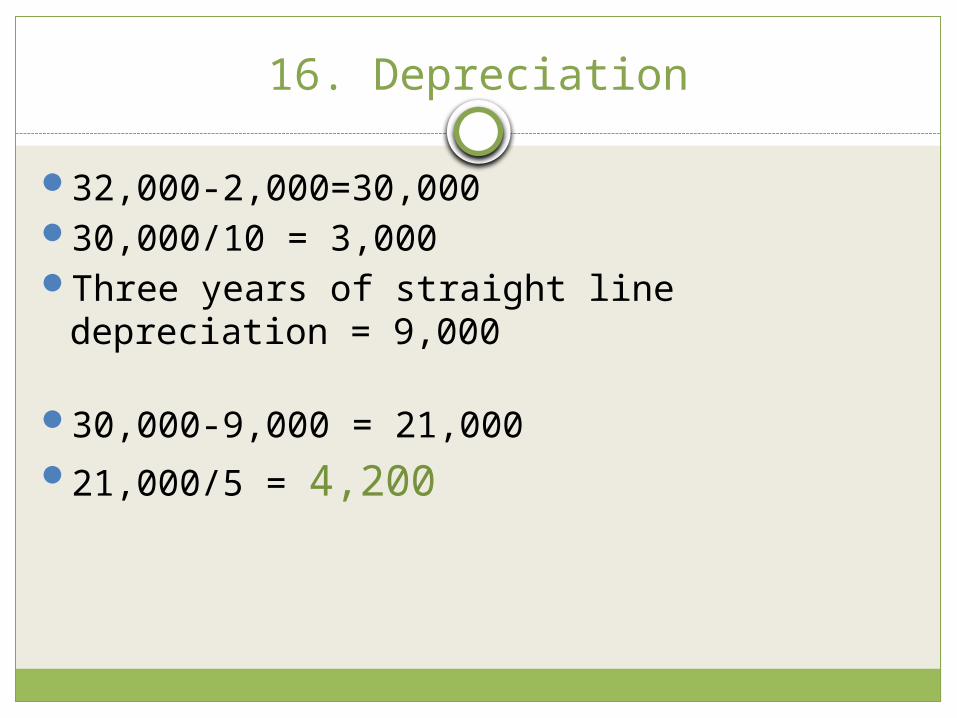

16. Depreciation

32,000-2,000=30,00030,000/10 = 3,000Three years of straight line depreciation =

9,000

30,000-9,000 = 21,00021,000/5 = 4,200

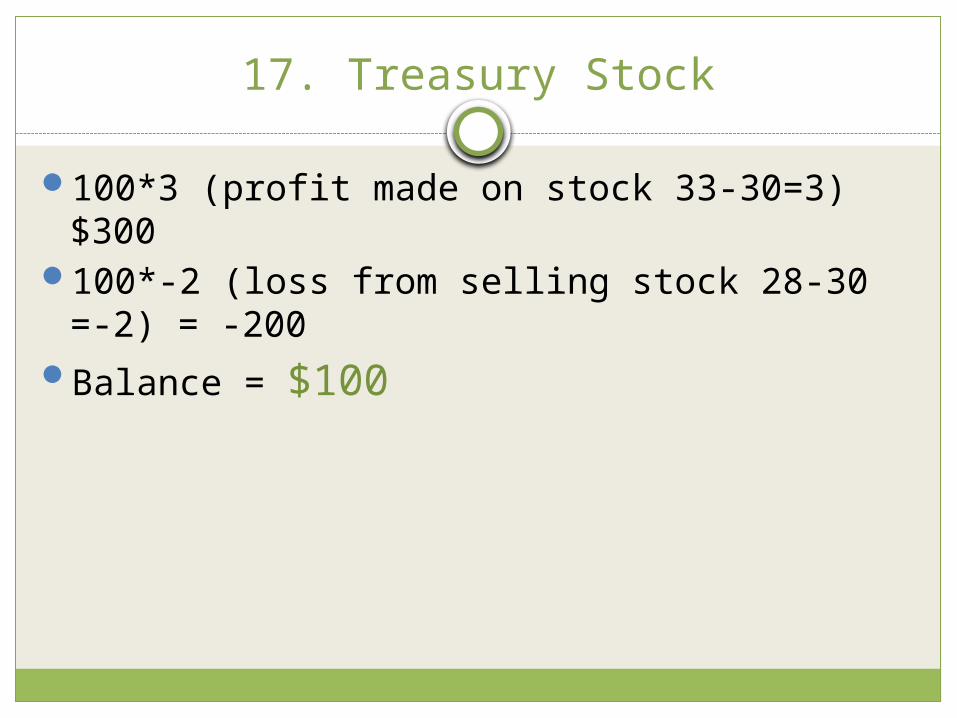

17. Treasury Stock

100*3 (profit made on stock 33-30=3) $300100*-2 (loss from selling stock 28-30 =-2) = -

200Balance = $100

18. Gain/Loss

$7,500 – 6,800 = $700 loss

19. Journal Entry to Record Payment of Note

Journal Entry – Payment of Note

Note Payable 8,000

Interest Expense 120

Interest Payable 120

Cash 8,240

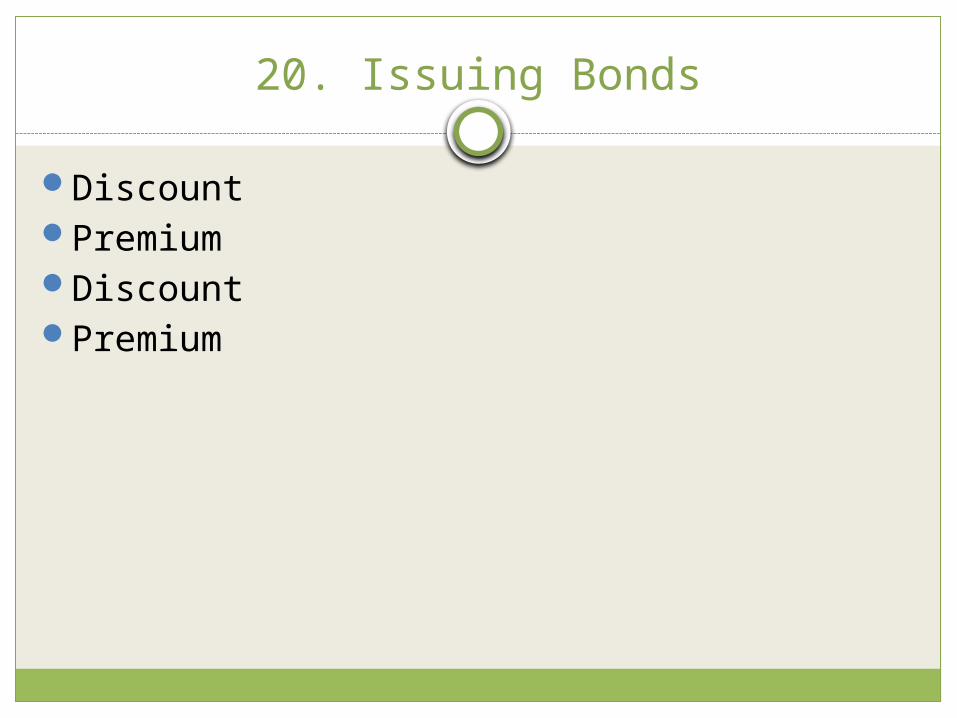

20. Issuing Bonds

DiscountPremiumDiscountPremium

21. Depreciation

Use the depreciation worksheet in Excel

22. Net Income - Partnership

Stephanie

Jennifer Lori

Salaries 40,000 60,000 47,000

10% Interest Allowance 30,000 22,000 26,000

70,000 82,000 73,000 = 225,000

300,000-225,000 = 75,000 25,000 25,000 25,000

TOTAL SALARY 95,000 107,000 98,000 =300,000

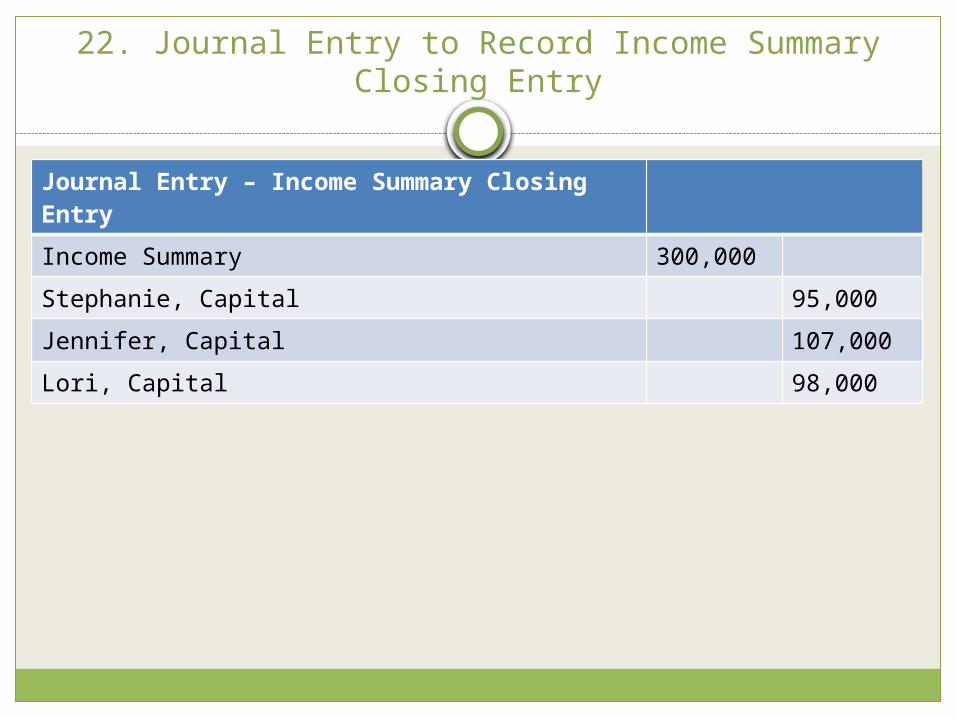

22. Journal Entry to Record Income Summary Closing Entry

Journal Entry – Income Summary Closing Entry

Income Summary 300,000

Stephanie, Capital 95,000

Jennifer, Capital 107,000

Lori, Capital 98,000

23. Payroll

INCOME6,100 (monthly salary) * 12 = 73,20073,200 * .05 = 3,660 BonusTotal Salary and Bonus – 73,200+3,660 = 76,860

DEDUCTIONSFederal Income Tax 810*12 = 9,720+932 = 10,652.00State Income Tax 80*12 = 960+70 = 1,030.00FICA Tax 76,860*.08 = 6,148.80United Fund 76,860*.01 = 768.60Insurance $20*12 = 240.00TOTAL DEDUCTIONS 18,840.00

23. Payroll

Gross Pay = $76,860Total Deductions = -18,840Net Pay = $58,020

24. Issuing Stock

Cash Received 2,000*35 = 70,000Common Stock 2,000*2 = 4,000Paid-in-Capital in Excess of Par = 66,000

(70,000-4,000)

Journal Entry – Issuing Stock

Cash 70,000

Common Stock 4,000

Paid-in-Capital in Excess of Par 66,000

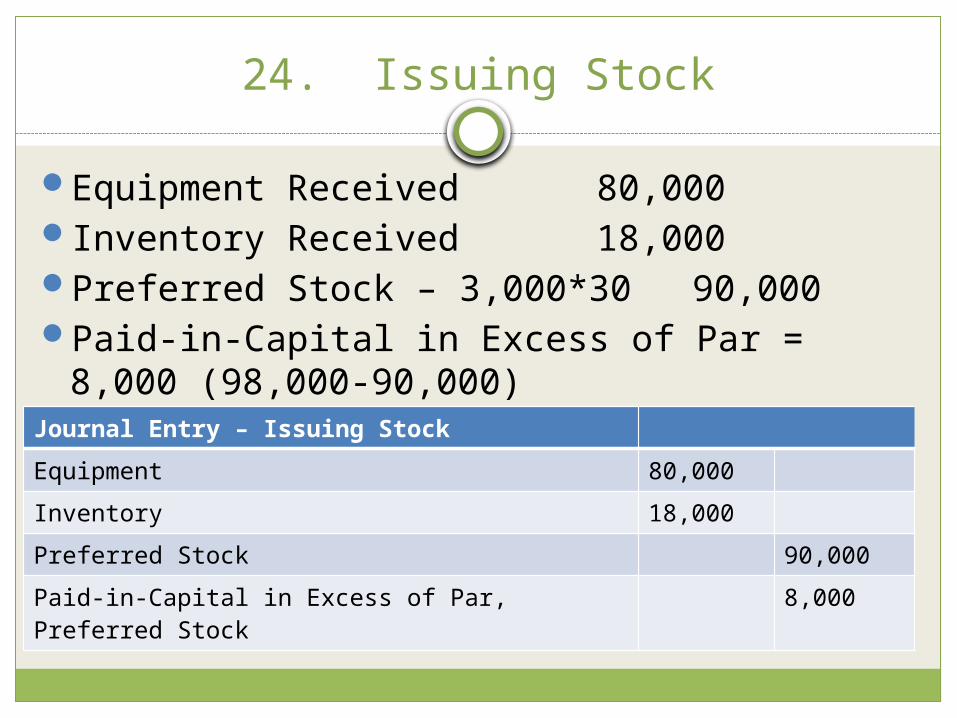

24. Issuing Stock

Equipment Received 80,000Inventory Received 18,000Preferred Stock – 3,000*30 90,000Paid-in-Capital in Excess of Par = 8,000

(98,000-90,000)Journal Entry – Issuing Stock

Equipment 80,000

Inventory 18,000

Preferred Stock 90,000

Paid-in-Capital in Excess of Par, Preferred Stock 8,000