Final Mohit Project

46

MALWA COTTON SPINNING MILLS LIMITED Working Capital Management Page 1 PROJECT REPORT ON WORKING CAPITAL MANAGEMENT OF MALWA COTTON SPINNING MILLS LTD IN PARTIAL FULFILMENT OF THE REQUIREMENTS FOR THE AWARD OF DEGREE OF MASTER OF BUSINESS ADMINISTRATION Submitted To Submitted By Mr.V.J. Mahajan Mohit Bembi MBA Roll No. 2312

-

Upload

sonabeta07 -

Category

Documents

-

view

222 -

download

0

Transcript of Final Mohit Project

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 1/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 1

PROJECT REPORT

ON

WORKING CAPITAL MANAGEMENT OF

MALWA COTTON SPINNING MILLS LTD

IN PARTIAL FULFILMENT OF THE REQUIREMENTS

FOR THE AWARD OF DEGREE OF

MASTER OF BUSINESS ADMINISTRATION

Submitted To Submitted By

Mr.V.J. Mahajan Mohit Bembi

MBA

Roll No. 2312

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 2/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 2

PREFACE

This project report entitled as WORKING CAPITAL MANAGEMENT in MALWA

COTTON SPINNING MILLS LTD., LUDHIANA that is well known in hosiery

industry was undertaken by me in partial fulfilment of Master of Business

Administration.

The main purpose of this report is to analyse working capital management in Malwa

Cotton Spinning Mills Ltd.I hope this study will prove useful for both academic as

well as practiacal purpose.

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 3/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 3

ACKNOWLEDGEMENT

Acknowledgement is an endless ocean and one requires to be supported,

guided, inspired and criticized by several specialists in order to drive-out a handful

pearls from its depth. As it comes wordlessly, it cannot be acknowledged in words.At the very outset, I hereby express my gratitude to the management of Malwa

Cotton Spinning Mills Ltd., for granting me permission to undertake my project work

in the organisation and providing me a rich intellectual environment and adequate

facilities which are so essential for writing a project of this kind and also enlighten me

with real working of the company.

I also owe my sincere thanks to Mr.V.J. Mahajan (Asst. Vice President

Finance) for providing me the capable guidance and willing help to undertake my project work.

I am very greatful to finance department for their valuable co-operation, all

employees were friendly towards me and helped me in completing my project report.

At last but not the least I am thankful to my parents and friends who provided

moral support and contributed in completion of my project.

Mohit Bembi

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 4/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 4

MALWA GROUP

The foundation of Malwa Group (formerly called the VSO Group) was laid by Late

Lala Vidya Sagar Oswal - a visionary known as much for his perspicacity and sharp

business acumen as for his philanthropic pursuits. Driven by a strong desire to achieve

what few in his day & time could have dreamt of, he sowed the seeds of the textile

powerhouse that Malwa has come to be today, built around the cornerstones of

Dedication to Work, Excellence in Product quality & Work Practices, Commitment to

its Customers and Daring to think beyond the ordinary. Today, after having been in

existence for seven decades, Malwa Group has become an over 10,000-member

strong Institution.

The Group is fully integrated in Textiles with interests in Ginning, Spinning,

Weaving, Processing and Garmenting, and is one of the biggest Textile

Conglomerates in the Country. The significant business diversification and the major

international forays towards expansion are proof of the growing international presence

of the Malwa Group.

Further, in line with the vision of its founder, Malwa Group also runs India's secondlargest charitable Cancer Hospital.

GROUP COMPANIES

MALWA INDUSTRIES LIMITED (MIL)

MALWA INDUSTRIES LIMITED (MIL) - Denim arm of the Malwa Group.

In 1997, Mr. Rishi Oswal, the scion of the Oswal family and the Managing Director

of Malwa Industries Limited started the denim manufacturing facility in response tothe increased market demand for Jeans in the 1990's. Commercial operations started

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 5/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 5

in FY97-98 and since then the company has been growing at a fast pace. Malwa's

premier denim manufacturing plant is located at Ludhiana in the Punjab region, the

heart of the Indian cotton producing belt. Its operations span India (where it is

headquartered), Jordan & Italy. Through these operations, its products are exported to

over 40countries worldwide where these are sold under some of the biggest denim

brands & designer labels that come to mind. With Quality certifications such as the

ISO9001, ISO14001, Oekotex & Woolmark, the name Malwa has, today, become

synonymous with superlative quality & product excellence. In recognition of its

excellent track record in Exports, it has been honoured with Export Performance

Awards by the Govt. of India in recent years.

Equipped with the latest machines imported from Switzerland , Germany , Belgium ,

Italy , Japan & the US , the facility boasts of some of the best equipment the industry

has to offer. With this state-of-the-art technology, MIL achieves a current production

capacity of 20 million meters of denim fabrics & 4.50 million pairs of Jeans annually.

The Jeans manufacturing facility at Jordan (Third Dimension Apparel LLC or more

popularly Petra) boasts of an annual capacity of 4.0million pieces. It has the most

advanced CAD system which helps in optimizing fabric consumption that minimizes

cost, making the product affordable.

The Italian venture (Emmetre) is a fully automated state-of-the-art facility for

Garment Dyeing & Finishing. It caters to the top end of the market and has a client

base comprising of leading designer labels & fashion brands. The facility brings to

Malwa's fold, prized knowledge of emerging fashion trends in denim making MIL a

trendsetter by virtue of this knowledge. This facility also adds 2.5million pieces

annually in capacities to Malwa's denim stable.

Malwa today stands tall & proud of its stature as one amongst a handful of denim

suppliers, globally, to possess capabilities in offering Total Solutions in Denims and

that too from a single point interface.

Oswal Knit India Ltd

Established in 1992, Oswal Knit is the market leader for winter wear in the premiumsegment. Sole Licensee for 'Pringle of Scotland' in India, since 1994, the company

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 6/55

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 7/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 7

Malwa Cotton Spinning Mills Ltd. (MCSM)

Malwa Cotton Spinning Mills Ltd or MCSM is among the top ten textile mills in the

Indian sub-continent. The Mills are situated amidst the rich cotton growing belts of

India namely Punjab and Himachal Pradesh in Northern India. The total spindleage of

both the units is around 140000.

The mills are equipped with hi-tech state-of-the-art machineries from world-renowned

textile machinery manufacturers like Rieter, Trutszler, Crossrol, Schlafhorst and

Savio.

All the above process machines are also equipped with latest on-line quality control

equipments combined with computerized information system. World wide recognized

& accepted high-reliability Uster quality control equipments form the core of our

R&D and constant monitoring quality control department.

A strong, skilled workforce of 5000 persons including highly experienced textile

professionals under the dynamic & able leadership of Mr. Jangi Lal Oswal, the Group

Chairman, is committed to meeting the challenges of exacting Global textile

standards. Malwa yarn is well sought after by domestic & international markets. An

ever-growing demand for our products in the global markets is evident from our

expanding export base. Malwa yarn conforms to the most stringent International

Quality standards in production. Thus knotless, flawless & high quality yarn

confirming to uster standards is produced.

We procure the best quality acrylic fiber from world-renowned manufacturers and

produce Acrylic cotton yarn & high bulk Acrylic yarn. Dye house facility at our

Works enables us to produce dyed yarn of exact shades. We also produce polyester

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 8/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 8

yarn, polyester cotton yarn, viscose yarn, dyed viscose yarn and viscose cotton yarn.

Raw materials like polyester& viscose too are procured only from reputed

manufacturers.

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 9/55

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 10/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 10

HISTORY & BRIEF INTRODUCTION OF THE COMPANY

Malwa cotton spinning mills ltd was incorporated in 1976 by Punjab state

development corporation limited and came under joint sector with own group in 1980.

The company has ceased to be in joint sector with this investment by PSIDC of its

shareholding since 1987.

At present the company has spinning unit at Barnala dist. Sangrur. two Unit worsted

spinning and threads unit at Machhiwara, dist. Ludhiana, Punjab and one spinning

unit at Paonta Sahib, Himachal Pradesh.

In 1980 the implementation of spinning unit with a complement of 25000 spindles for

manufacturing of synthetic yarns was taken in hand and completed in March 1983.

After gradual expansion over a period, the capacity of Barnala unit was raised to

49696 spindles in 1990. Looking into good response in the domestic and international

market, in may 1995, the management decided to expand with 25200 spindles at

Barnala under 100% export oriented unit is now deboned.

1 April 1988 the company started implementation of new spinning project with 12480

spindles at Ponta Sahib and with various expansion up to 1995 the capacity of the unit

increased to 63920 spindles.

To give further inputs to profitability & strengthen the bottom lines the management

decided to go for value addition of yarn the company took in hand implementation of

dyeing & processing unit for dyeing of fabric yarns & fiber with a capacity of tonnes

per day at village Harridan, Machhiwara and distt. Ludhiana(Punjab) in april 1998.

The project was completed in 2000 also to harmonize and optimise the operation ; the

hank dyeing unit at Paonta Sahib is also shifted to Machhiwara. The company took up

diversification by setting up of threads capacity in 2001-2002 with 3 tonnes per day

which is increased to 9 tonnes peer day in 2004-2005 for polyester,cotton & other

high value threads. The threads division is set up to consolidate its existing operation

and manufacturing of high value added products.

The company is equipped with most modern plant & machinery like blow roomfrmTRUTZCHLER of Germany, cards froms CROSSROLL of united kingdom, reiter of

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 11/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 11

Switzerland & Indigenous cards from lakshmi machine works limited, comibatore,

india, autoconers from savio of Italy, draw frames from cherry hara of Japan

indigenous speed frames ang ring frames from lakshmi machine work ltd.

Coimbatore,India and other quality testing facilities like uster tester3 evenness tester,

teno rapid, spinlab, compusoter & classimate 2 from zwelleger uster of Switzerland.

Mcsml is manufacturing a wide range of yarn made from cotton, acrylic, plyster,

viscose woos and other synthetic fibers, the company is manufacturing cotton yarn

bothcarded and combed, acrylic yarn viscose yarn and other blended in dyed and

grey. The production capacity of Barnala unit is 38 tonnes per day and Paonta Sahib

unit 30 tonnes per day. The capacity of dyeing unit at Machhiwara is 12 tpd for cone

dyeing , hank dyeing and fabric dyeing. The sewing threads unit capacity is 9 tonnes

per day. At present the capacity of worsted is 4 tpd.

SOCIAL RESPONSIBILITY

CPP

In 2006 Malwa Commissioned its very own Captive Power

Plant with a capacity of 6 MW. It uses renewable and non

polluting rice husk as fuel. The Plant provides uninterrupted

power supply to Malwa Industries Limited thereby reducing the

high cost of power. Electrostatic Precipitator is installed in

Captive Power Plant for reduction of particulate matter. Air

Pollution Control Devices are also installed in Boiler &

Electrostatic Precipitator (ESP) in order to curb & prevent air

pollution. Green Fuel usage reflects Malwa's dedication towards

cleaner & pollution free environment, while making us more

competitive.

ETP

State of the art Effluent Treatment Plants helps us in using the

effluent treated waters which confirms to the WHO portable

standards. Treated water is used for Horticulture within the acres

of premises thereby maintaining the sprawling green belt in and

around the factory. Malwa in a first of its kind initiative in this

part of the country has partnered with the state government and

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 12/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 12

local village community wherein treated water from our ETP

shall irrigate about 600 Acres of land in nearby agricultural

fields, leading to conservation of both Water & Electricity.

Cotton Waste generated during manufacturing is diverted tohand Carpet Industry for making World Class Carpets. This

helps in the optimum utilization of resources.

Rain Water Harvesting – Rain water harvesting Plant is installed

within factory premises at Machhiwara near Ludhiana. It stocks

rain water which is provided for irrigation in the near by

agricultural fields, free of cost. Rain water harvesting is believed

to be one of the best methods of replenishing the water table

there by giving back to nature what we take from it. It is yet

another contribution of Malwa towards balancing the ecological

system.

Malwa in a first of its kind initiative in this part of the country

has partnered with the state government and local village

community wherein treated water from our ETP shall irrigate

about 600 Acres of land in nearby agricultural fields, thereby

supporting the local farming community to over come irrigation

problem.

Malwa Group runs a 300 bed Charitable Cancer Hospital at

Ludhiana (Mohan Dai Cancer Hospital ) which has State of Art

facilities. This is second largest Cancer Hospital in the country.

Malwa is also running a School to provide subsidized education

for the children of its employees & workers

Malwa Management organizes Yearly Health Camps for

Community Welfare, attended in large numbers .

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 13/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 13

Malwa is committed to community development. It actively

participated in the construction of the village Community Hall,

apart from organizing regular sport events for the local village

community.

Women Empowerment : Malwa has employed around 800

women workers from near by villages. These Dependent Girls

who have come from a conservative background from families of

Land Lords & Farmers are now very happy with the step they

have taken to come out and work for Malwa. These girls in their

young age have now transformed themselves into a Confident,

Motivated, Self Independent and Outshining Personalities, apartfrom financially contributing towards their families. Malwa

pursues the policy of No Discrimination on the basis of physical

disability which has resulted in the upliftment of the needy & the

oppressed.

HOSPITAL

MOHAN DAI OSWAL CHARITABLE CANCER HOSPITAL

As part of its philanthropic activities, Malwa also runs a fully equipped

charitable Cancer Hospital atLudhiana (Mohan Dai Oswal Charitable Cancer Hospital

), which is the country's second largest CancerResearch& Care Hospital.

Health Awareness

Mohan Dai Oswal Cancer Treatment & Research Foundation, Ludhiana

· A Charitable Organization· At present it is the biggest cancer center of the northern India equipped with latest state

of art diagnostic & therapeutic equipment

· Marches Ahead by Approaching the Unapproachable by announcing the opening up of

the new City Center – Purana Bazar, Ludhiana

· A Charitable free dispensary at Inder Nagar - Ludhiana

· A Comprehensive Cancer Care Centre &Multispeciality Hospital With continuous

dedication and Commitment for the suffering humanity

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 14/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 14

Mohan Dai Oswal Cancer Treatment & Research Foundation was established in 1984

as a charitable institution to extend comprehensive quality treatment for cancer to the

masses at an affordable price. It is a 300 bedded hospital located on the Amritsar -

New Delhi G.T. Road near Sherpur bye pass,Ludhiana. It is housed in a multistoried

building. Patient care area is approx. 16,000 sq. Yards spread over 4 floors. In

addition there is a

mechanical laundry, a workshop, shopping areas, residential accommodation for

medical, nursing & paramedical staff and a sarai for poor patients (Free of cost stay).

All these are located at convenient distances from each other. The hospital is located

in an 8-acre plot & has adequate space for future expansion. Over the period the

hospital has developed into a modern, well-equipped comprehensive cancer treatment

center and multispeciality hospital. Clinical services are adequately backed by

investigative and diagnostic divisions.

The hospital registers nearly one-lakh patients in different OPD services every year

and nearly over 8000 annual admission in different specialties yearly.

Being by the specialized comprehensive care center:-

On an average 3, 000 to 3,500 new cancer patients are registered in the hospital

besides regular follow up patients. This number increases by 10% every year. Daily

OPD attendance ranges from 350 to 400 patients (Old and New) These patients

include people from all walks of life not only from Punjab but adjacent northern states

of India including J&K, HP, UP and Haryana.

The hospital has made special endeavors to have outreach programme in the rural as

well as urban areas by opening up free urban dispensary at InderNagar , Ludhiana,

and Charitable City Center at Purana bazaar Ludhiana .The hospital is also having

Collaboration with different charitable hospitals and rural centers, where

postgraduates participate independently for the diagnosis and treatment of the

patient.The post-graduate also take active part in the free medical checkup camps

organized in the rural and urban areas from time to time and they also participate in

the health awareness activities.

It may be of interest to note that we provide the cheapest cancer treatment facilities in

the region. Today the hospital is recognized as a centre of excellence and this

encourages us to make better efforts to reach greater heights in all fields of patientcare. We are thankful to the medical fraternity and people at large without whose faith

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 15/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 15

and support it would never have been possible, for us to achieve and maintain our

objective of “Maximum Benefits, to largest number at minimum cost ".

Mohan Dai Oswal Cancer Institution is doing a great service to the patients suffering

from dreaded disease of cancer. Besides this it has acquired the status of the

postgraduate institute for having been affiliated by the Diplomat National Board in

various specialties for the post graduate courses.

Karam Yogi Lala Vidya Sagar Oswal

The great warrior, the centurion man Lala vidya Sagar Oswal was born at village

Jodhan, Ludhiana in 1908. Lalaji had a long stressfull journey from a simple layman

to a successful business Tycoon. He started his life as a simpleemployee in a shope.

With his hardwork, patince and intelligence he reached to the higest level of being

cosidered as a doyen of industrial revolution in hosiery in Ludhiana and was

instrumental in bringing Ludhiana on the Industrial manpof the world, known as

Manchester of India.

VSO Group has opened a Institute of information Technology a charitable (No Fee)

Institution in the Memory of Lala Vidya Sagar Oswal.

Opp. Fire Brigade, G.T. Road, Miller Ganj, Ludhiana

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 16/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 16

As founder of Malwa Group, I feel a strong sense of

pride and honour to head such an exceptional

organization. Exceptional in every regard, be it dedication to work, a sense of

commitment to the customer or maintaining quality standards. Most of all, in winning

over customers confidence which to us is the prime reason for our success day after

day, year after year.

Achievement brings with it a sense of pride which further encourages the growth of

the people, the company and the product line. As we look back over the years, we

have come a long way from whence we began. The road to success has not always

been easy to tread but each hurdle overcome gave us strength to go one more step a

head. We took each challenge as a part of the bigger process which prepared us for

greater things in time to come.

The Malwa Group, a vision of the future that is continually expanding itself by the

basic qualities, necessary to growth and holds a promise of even greater things to

come.

I thank every one at the Malwa Group for their unwavering faith and conviction

which had made it possible for the vision to come true. Its my distinct privilege to

share it with you.

Lala Vidya Sagar Oswal

THE MANAGEMENT

BOARD OF DIRECTORS

MR. JANGI LAL OSWAL (Chairman-cum Managing Director)

MR. RISHI OSWAL

MR. RAHUL OSWAL MR. SURENDRA PRASAD BHATT (Nominee of IFCI)

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 17/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 17

MR.YASHPAL BARAR (Nominee od PNB)

MR.SANJAY KUMAR SUROYA (Nominee of IDBI)

MR.G.BANSAL

MR.SURINDER KUMAR VIGAUDITORS

S.C. VASUDEVA & CO., NEW DELHI

BANKERS

Punjab National Bank

State Bank of India

Vijaya Bank

The Jammu & Kashmir Bank Ltd.

IDBI Bank LTd.

IFCI Ltd.

REGISTERED OFFICE

Industrial Area –“A”,

Ludhiana-141003

Punjab

WORKS

1) Village Harigarh,

Raikot Road, Barnala (Punjab)

2) Village Patlian,

Paonta Sahib (Himachal Pradesh)

3) Village Harian, Kohara-Machhiwara Road,

Distt. Ludhiana (Punjab)

AWARDS & RECOGNITION

YEAR AWARDS & RECOGNITION

March 2001 Obtained ISO 9002 certification from BVQI, London

April 2001 Achieved Export-House Status under Government of India

Guidelines

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 18/55

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 19/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 19

the Paonta Sahib unit spins out 38 tonnes per day. The product is versatile and finds

use in many different ways in the textile and clothing industry of which it forms the

essential ingredient.

The high quality of the product has carved for itself an export market where all kinds

of cotton yarns, synthetic yarns and their blends are exported. Export growths have

been phenomenal and predict the future trends. Malwa Cotton Spinning Mills Ltd.

have been marked from the beginning to spin a success story of their own.

Our experienced cotton selectors are spread over the cotton belt of Punjab. Control on

quality of cotton is exercised right to keep it contamination free from picking stage.

Cotton is ginned in our modern Ginning Unit comprising of both Saw and Roller Gin.

Each bale passes o ut of Ginning Factory after it meets Malwa s Quality Standards. All

thecontamination free bales produced in our Ginning Factory meet Uster HV1900

Grade.

Cotton is produced in our mills under controlled conditions created by sophisticated

State of Art, Humidity and Textile Air Engineering system produced by Luwa

Humidification System. Each process conforms to stringent quality norms specified

by Textile Research Associations of India.

Our quality assurance department (QAD) has latest equipment like:

Uster HVI-900

Uster Tester-111 with Hairiness Tester

Uster Auto sorter

Uster Tensorapid uster Classimat

Mini Uster

We constantly monitor the quality of the product at various stages of yarn

manufacturing. Our Savio winders are equipped with third generation contamination

control Uster cleaners & coupled with Air spliceIn Lacs.

The Knotless, Flawless & High Quality yarn confirming to Uster Standards is

produced. We procure Acrylic Fiber from world renowned manufactures and we

produce Acrylic Yarn, Acrylic Cotton Yarn & High Bulk Acrylic Yarn.

Dye House Facility at our works enables us to produce dyed yarn of Exact Shades.

We also produce Polyester Cotton Yarn, Viscose Yarn and Viscose Cotton Yarn,

Dyed Viscose Yarn. Raw materials like Polyester, Viscose are produced from reputed

manufactureIn Lacs.

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 20/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 20

MIL Technology

Malwa's premier denim plant in India and itsfacilities across Jordan & Italy are state-of-the-art

units equipped with the latest machines from

Switzerland, Germany, Belgium, Italy, Japan & the

US. These include:

Morrisons of USA for Rope-Dyeing & Finishing,

Zinser Ring-frames from Germany for Spinning,Picanols (from Belgium) and Sulzers (from Switzerland) for Weaving

VI Be Mac, Juki, Pegasus & Brother for Garment manufacturing and the world

famous Tonellos from Italy for Garment Washing

(which also make Malwa the finest denim washing facility in India)

The most advanced CAD system from Gerber & Lectra, that helps keep

production costs low that eventually gets passed down to its customers.

With state-of-the-art technology such as this, Malwa is able to consistently maintain

high productivity and quality levels Malwa continuously strives to upgrade our

technology according to the latest trends in the denim industry. As a result of it now

has the latest technological addition in the development, processing and finishing of

our denim fabrics:

1. ORGANIC

Organic Denim is made of organically grown cotton.Organic cotton is grown without use of harmful

chemicals & pesticides, etc as such it is completely

natural and free of chemicals. Even during fabric and

finishing stages, special treatment is given to these

fabrics to retain the organic character by using

environment friendly chemicals. The colours are

deeper and nicer and the fabric feel is amazing!!!

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 21/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 21

2. JAPANESE CHIMICA FINISH

The finishing machine used for this finish is one of its

kinds. It gives a special finish to the fabric, soft to feel

& better to handle. The character or drape of the fabric

gives a better lusture and sheen to the fabric. The

colors are embedded deeper, as the denim fades

naturally it gives an excellent depth to the fabric color.

The process is innovative & requires special

chemicals & expertise for finishing the fabric.

3. MOLECULAR FINISH

Molecular finish is a high blend and combination o

chemicals & colors whereby it gives a very fine coat

on the fabric. The finish penetrates deep in the fabric,

deep to the molecular level, to give the fabric a new

look.

MILESTONES TO SUCCESS

Mcsml is flagship Company of Malwa Group. The company is looked after by sh.

Jangi lal Oswal, chairman cum managing director who has varied experience & well

known in industry. Mcsml is regular exporter & exporting all type of yarn & their

blends. Its exports have grown over last twenty yeaIn Lacs. From Rs 7.84 lacs in

1989 to Rs 8854 lacs in 2007- 08.

The company had come under top 100 companies of India & awarded corporate

excellence awards of year 1995. The company has been awarded special status of

export house by govt of India

The cotton textile export promotion Council (texprocil) of India awarded two silver

trophies to company for the year 1996-97 for outstanding performance in yarn

amongst.

1. for top exporters (mills)

2. for non-quota exports

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 22/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 22

The company has awarded a quality system Certificate of ISO-9002 for

manufacturing for its products.

PRODUCTS

DENIM

Malwa made a foray into cotton denims almost a decade ago in 1997. Since then,

there has been no looking back and Malwa's presence

in denims has gone from strength to strength. Being

situated in the heart of the cotton producing belt in

India, Malwa has access to a consistent and

uninterrupted supply of best quality raw material

thereby ensuring finest cotton Denim fabrics to its

valued customers. In sync with the emerging trends in

Denim, Malwa's in-house Design team works closely

with leading International Design Consultants to come

out with an array of breathtaking designs & finishes in denim a year ahead for every

season.

Through its state-of-the-art denim plant in India , Malwa rolls out premium and basic

denim fabrics employing

- Ring yarns ,

- Open-end yarns ,

- Slubs ,

- Mixed Warps ,

- Multi-count yarns &- Colored yarns in weft as well as in warp .

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 23/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 23

From classical to contemporary, basic twills to fil-a-fils , cross-hatches to stripes and

from vintage to raw, Malwa belts out a staggering range of denims through clever

variations that are sometimes pronounced and sometimes subtle ; each variation

distinct & different from the other and unique in its own right. Add to this Malwa's

vast repertoire of advanced wash effects & finishes and you step into a world of

infinite possibilities to choose from.

Season Theme

The Spring / Summer 2009 collection is a unique blend of sophisticated and raw lookscreated through an intriguing play of Colors, Weaves, Yarns & Fibers.

With real time knowledge of the latest trends, finishes & looks in denimwear from its

Italian promises to leave you spellbound).

Spring / Summer '11/12

Autumn / Winter '10/11

Spring / Summer '10 INDIGO WOOL

Indigo wool is a range of indigo, warp dyed wool products that have been developed

and produced by unique manufacturing techniques. Introduced by Malwa to enable

the consistent commercial production of wool and wool blend garments,this new

breakthrough in wool products uses unique modern technology and advanced indigo

dyestuffs.

Commercially developed by Malwa, in conjunction with The Wool Mark Company,

the method takes thousands of yarn ends at one time and dyes them through a

commercial continous wrap dyeing system. After dyeing, the yarns are woven using

technically challenging methods which are adapted to process the softer wool yarns.

Following an extensive trial period, Malwa has now created a continous method of

producing indigo dyed wool – Indigo Wool.

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 24/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 24

KNITWEAR Oswal Knit offers a range of premium woolen

knitwear and clothing through “Pringle of

Scotland” and “Casablanca” lines. As the sole

licencee of international brand “ Pringle of

Scotland” it manufactures top -of-the-line

Woolen Knitwear, T-shirts, Shirts, Trousers,

Jackets and Accessories to complement the

life-style of the crème-de-la-crème segment. Its home-grown brand 'Casablanca'

offers winter wear to the customer in the mid and upper mid-price segment and gives

the company, presence across all major price segments. A strategic tie-up with an

Italian Design Studio ensures that Oswal Knit has access to the latest international

designs, trends and styles which gets translated into a line of high fashion

contemporary clothing for the Indian consumer. To ensure quality of the highest

order, raw materials are sourced from the topmost Italian manufacturers and the

technology is replenished and updated from time to time to ensure that it has the

requisite cutting edge.

YARNS

Malwa Cotton Spinning Mills Limited (MCSM) is a major yarn producer andmanufactures a wide range of yarns at its state-of-the-art units across Punjab &

Himachal Pradesh. Yarns ranging from Ne 10 to 40 in single, double and multi folds

are manufactured. These include

100 % Cotton Combed Raw White Yarns (range includes 20, 24, 30, 32, 34 & 40)

100 % Cotton Carded Raw White Yarns (range includes 10, 12, 16, 20, 30 & 36)

100 % Cotton Dyed Yarns (ranging from Ne 10 to 40)

100 % Cotton Mélange Dyed Yarns (range includes 16, 24, 30 & 40) Cotton-Viscose blended Dyed Mélange Yarns (range includes Ne 16, 24 & 30)

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 25/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 25

Yarns in blends of Lycra & Cotton and Lycra & Acrylic

Acrylic-Cotton yarns (Dyed & Grey) in any blend ratio using Combed as well as

Carded Cotton {For Combed category, yarn range includes 30 & 2/18. For Carded

category, yarn range includes 10, 12, 16, 20, 30 & 2/16, 2/18 & 2/30}. Polyester-Cotton yarns (Dyed & Grey) in any blend ratio using Combed as well as

Carded Cotton (range includes Ne 20/1, 24/1, 30/1, 34/1, 36/1, 40/1 & 42/1 )

100% Acrylic High bulk dyed yarns on Hanks/Cones ( range includes 2/10, 2/19,

2/24, 2/28, 2/32, 3/8, 4/8, 1/15 etc)

100% Acrylic Raw white yarns suitable for Bulking (range includes 2/10, 2/19, 2/24,

2/28, 2/32, 3/8, 4/8, 1/15 etc)

100% Acrylic non-bulk Raw white & Dyed yarns (range includes 33/1, 40/1, 50/1,2/40, 2/30 etc).

100% Polyester Raw White & Dyed yarns

Polyester-Viscose Raw White & Dyed yarns in any blend ratio

Worsted yarns for suiting fabrics

MARKETS

Malwa s exports span America, Europe, Middle East, Far East & Africa and are well accepted

by discerning customers across the world on the strength of their exemplary quality, range &

design. The major countries where our products are being exported include:

Asia Europe Africa America

Japan

China

Korea

U.A.E.

Hongkong

Singapore

Germany

U.K.

Russia

Spain

Italy

Switzerland

South Africa

Egypt

Kenya

Mauritius

Nigeria

Sudan

USA

Canada

Panama

Cuba

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 26/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 26

Cyprus

Israel

Malaysia

Taiwan

Turkey

Vietnam

Bangladesh

Belgium

Greece

Portugal

Slovenia

Sweden

Tanzania

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 27/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 27

WORKING CAPITAL MANAGEMENT

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 28/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 28

OBJECTIVES

The main objectives to undertake this project to study:-

Analyse the operating cycle of the company.

To study management of working capital by the company. To study which factors affects the working capital of the company

To properly and effectively operate the working capital cycle of the management.

To analyze the day-to-day working of the company, whether they are able to meet

their daily expenses.

To determine the liquidity position of the company.

DATA COLLECTION Primary as well as secondary data is used for the project. The research management.

Secondary data is collected from annual reports, relevant records of Avon Cycle

Limited.

ANALYSIS OF DATA

Analysis is done in terms of theoretical concepts. Analysis of working capital

performance is done with help of percentages by showing graphs, ratios ets.

INTRODUCTION

“Working capital means the part of the total assets of the business that change from

one form to another from in the ordinary course of business”

The word working capital is made of two words:-

Working

Capital

The word working means day to operation of the business, whereas the word capital

means monetary value of all assets of the business.

WORKING CAPITAL

Working capital may be regarded as the life blood of business. working capital is of major

importance to internal and external analysis because of its close relationship with the current

day-to-day operations of a business.

Every business needs funds for two purpose:-

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 29/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 29

Long-term funds are required to create production facilities through purchase of fixed assets

such as plants, machineries, lands, buildings etc.

Short-term funds are required for the purchase of raw materials, payments of wages, and other

day-to-day expenses. It is otherwise known as revolving or circulating capital.

In other words, working capita l refers to that part of the firm s capital, which is required for

financing short-term current assets such as cash, marketable securities, bill receivable,

debtors, inventories etc. However, working capital is also known as Revolving or circulating

Capital. Businesses use capital for construction, renovation, furniture, software, equipment, or

machinery. It also commonly used to purchase inventory, or to make payroll. Working capital

is essential for any business to succeed. It is becoming increasingly important to have access

to more working capital when we need it.

NEED FOR WORKING CAPITAL

The basic objectives of financial management is to maximize shareholders wealth. This is

possible only when the company earns sufficient profit. The amount of such profit largely

depend upon the magnitude of sales. However, sales do not convert into cash instantaneously.

There is always time gap between the sale of goods and receipt of cash. Working capital is

required for this period in order to sustain the sales activity.

Working capital is needed for the following purpose:

For purchase of raw material, components and spares.

To pay wages and salaries.

To incur daily expenses and overhead cost such as fuel, power and office expenses etc.

To maintain the inventories of raw material, work in progress, spares and finished stock.

To provide credit facility to customeIn Lacs.

To meet the selling costs.

MANAGEMENT OF WORKING CAPITAL

Working capital, in general practice, refers to the excess of current assets over current

liabilities positions are bad for any business. Management of working capital therefore, is

concerned with the problems that arise in attempting to manage the current assets, the current

liabilities and the inter relationship that exits between them. In other words, it refers to all

aspects of administration of both current assets and current liabilities. The basic goal of

working capital management is to manage the current assets and current liabilities of the firm

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 30/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 30

in such a way that a satisfactory level of working capital is maintained, i.e., it is neither

inadequate nor excessive. This is so because both inadequate as well as excessive working

capital positions are bad for any business. Inadequacy of working capital may lead a firm to

insolvency and excessive working capital implies idle funds, which earn no profits for the

business. Working capital management policies of a firm have a great effect on its

profitability, liquidity and structural health of the organization.

In this context, working capital management is three dimensional in nature:-

Dimension I is concerned with the formation of the policies with regard to profitability, risk

and liquidity.

Dimension II is concerned with the decisions regarding the composition and level of current

assets.

Dimension III is concerned with the decisions about the composition and level of current

liabilities.

There is a definite inverse relationship between the degree of risk and profitability.

A conservation management prefers to minimize risk by maintaining a higher level of current

assets while a liberal management assumes greater risk by reducing working capital.

TYPES OF WORKING CAPITAL

ON THE BASIS OF BALANCE SHEET CONCEPT

There are two interpretation of working capital under the balance sheet concept:-

Gross Working Capital

Net Working Capital

Types of WorkingCapital

On the basis of B/S Concept

Gross WorkingCapital

Net WorkingCapital

On the basis of time

PermanentWorkingCapital

TemporaryWorkingCapital

SeasonalWorkingCapital

SpecificWorkingCapital

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 31/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 31

a) Gross Working Capital

In the board sense, the term working capital refer to the gross working capital and represents

the amount of funds invested in current assets. Thus, the gross working capital is the invested

in total current assets of the enterprise. Current assets are those assets, which in the ordinary

course of business can be converted into cash with in a short period of normally one

accounting year.

Gross Working Capital = Current Assets

Particulars As at

31.3.2012

(in Lacs)

As at

31.3.2011

(in Lacs)

As at

31.3.2010

(in Lacs)

As at

31.3.2009

(in Lacs)

Current Assets

Inventories

Sundry Debtors

Cash and Bank balance

Loan and Advances

1400.52

13777.00

504.79

2406.65

15139.52

12265.29

315.53

2283.85

12395.91

13060.05

339.94

2310.12

10588.42

12847.03

402.33

2471.31

Gross Working capital and Total

Current Assets

31088.96 30004.19 28105.42 26309.09

INTERPRETATION

The above figures indicate the gross working capital is increasing every year. In 2009

it was 26309.09 which increase to Rs. 28105.42 lac, Rs. 30004.19 lac and Rs.

31088.96 lac in the year 2010, 2011 and 2012 respectively. As sales are increasing

so not much funds are blocked in current assets as gross working capital, which

indicate that it is not alarming situation.

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 32/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 32

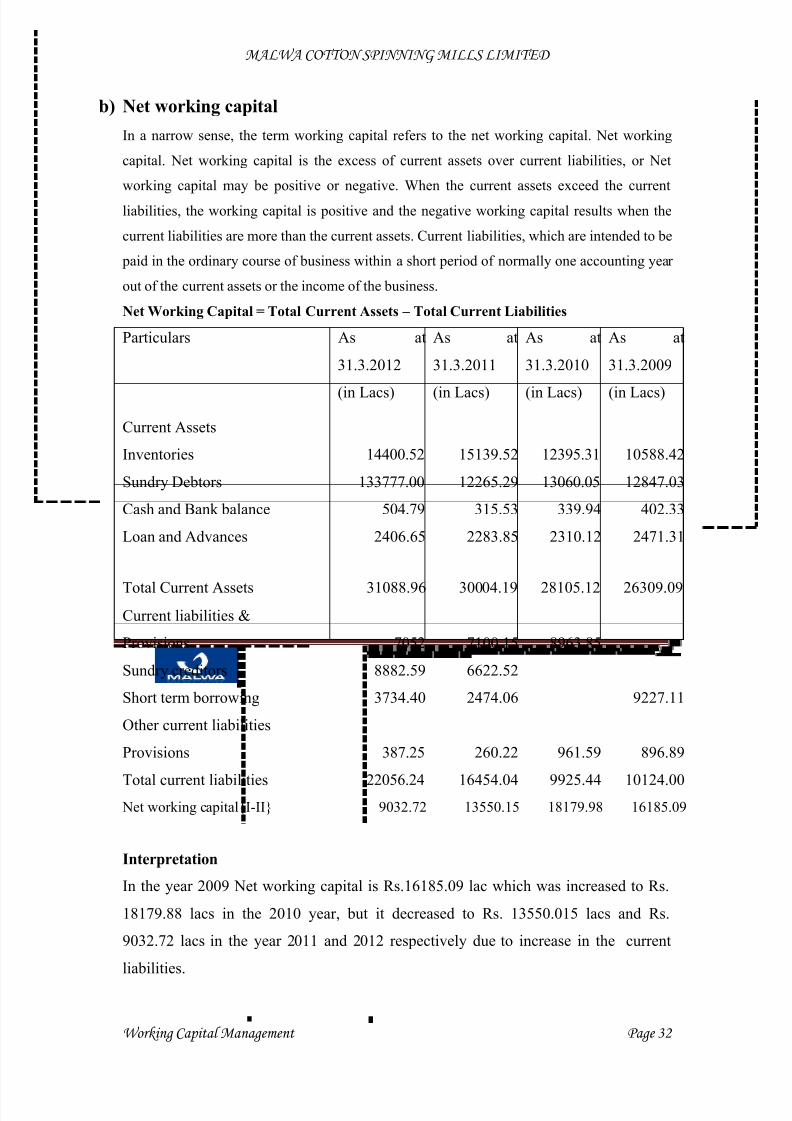

b) Net working capital

In a narrow sense, the term working capital refers to the net working capital. Net working

capital. Net working capital is the excess of current assets over current liabilities, or Net

working capital may be positive or negative. When the current assets exceed the current

liabilities, the working capital is positive and the negative working capital results when the

current liabilities are more than the current assets. Current liabilities, which are intended to be

paid in the ordinary course of business within a short period of normally one accounting year

out of the current assets or the income of the business.

Net Working Capital = Total Current Assets – Total Current Liabilities

Particulars As at

31.3.2012

(in Lacs)

As at

31.3.2011

(in Lacs)

As at

31.3.2010

(in Lacs)

As at

31.3.2009

(in Lacs)

Current Assets

Inventories

Sundry Debtors

Cash and Bank balance

Loan and Advances

14400.52

133777.00

504.79

2406.65

15139.52

12265.29

315.53

2283.85

12395.31

13060.05

339.94

2310.12

10588.42

12847.03

402.33

2471.31

Total Current Assets 31088.96 30004.19 28105.12 26309.09Current liabilities &

Provisions

Sundry creditors

Short term borrowing

Other current liabilities

Provisions

Total current liabilities

7052

8882.59

3734.40

387.25

22056.24

7100.15

6622.52

2474.06

260.22

16454.04

8963.85

961.59

9925.44

9227.11

896.89

10124.00 Net working capital{I-II} 9032.72 13550.15 18179.98 16185.09

Interpretation

In the year 2009 Net working capital is Rs.16185.09 lac which was increased to Rs.

18179.88 lacs in the 2010 year, but it decreased to Rs. 13550.015 lacs and Rs.

9032.72 lacs in the year 2011 and 2012 respectively due to increase in the current

liabilities.

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 33/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 33

ON THE BASIS OF TIME Permanent working capital

Temporary or variable working capital

a) Permanent Working Capital

The refers to that minimum amount of investment in all current assets which is required to all

times to carry out minimum level of business activities. It represents the current assets

required on a continuing basis over the entire year.

The following are the characteristics of this type of working capital:-

Amount of permanent working capital remains in the business in one form or another. This is

particularly important from the point of view of financing. The suppliers of such working

capital should not expect its return during the lifetime of the firm. It also grows with the size of the business.

Permanent working capital is permanently needed for the business and therefore it should be

financed out of long-term funds.

Permanent working capital is permanently needed for the business and therefore it should be

financed out of long-term funds.

This is the reason why the current ratio has to be substantially more than „I .

b) Temporary or Variable Working Capital

The amount of working capital is required to meet the seasonal demands and some special

exigencies. The amount of such working capital keeps on fluctuating from time to time on the

basis of business activities.

In another words, it represents additional current assets required at different times during the

operating year.

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 34/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 34

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 35/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 35

OPERATING CYCLE

Cash

Rawmaterial

Work inProgress

FinishedGoods

Sales

Debtors

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 36/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 36

Operating cycle is the time duration required to convert sales, after the conversion of resources,

into cash. Cash inflows are not certain because sales & collection, which give rise to cash

inflows, are difficult to forecast accurately. Cash outflows, on other hand are relatively certain.

The firm is, therefore, required to invest in current assets for smooth, uninterrupted functioning.

It needs to maintain liquidity to purchase raw material liquidity to purchase raw materials &

pay expenses such as wages & taxes as there is hardly a matching between cash inflows and

cash outflows.

Cash is hold to meet any future exigencies. Stock of raw material and work – in-progress and

kept to ensure smooth production and to guard against non-availability of raw material and

other components. The firm holds stock of finished goods to meet the demand of customers on

continuous basis and sudden demand from some customerIn Lacs. Thus, a firm makes adequate

investment in inventories, for smooth, uninterrupted production and sale.

Operating Cycle Analysis

In order to understood the length of times which reports are committed to various components

of working capital, operating cycle analysis has been done. The operating cycle of a firm with

the acquisition of raw material and ends with the collection of receivable. There are four

aspects of operating cycle, which involves commitment of resources, a material stage, and

accounts finished stage.

Gross Operating Cycle Period = RMCP + WIPCP + FMCG + RCP

RMCP = Raw Material Conversion Period

WIPCP = Work-in-Progress Conversion Period

FMCG = Finished Goods Conversion PeriodRCP = Receivables Conversion period

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 37/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 37

A. Raw Material Conversion Period

a) Average Stock of Ram Material = (Opening Stock + Closing Stock) / 2

ParticularsAs at

31.3.2012 (InLacs.)

As at31.3.2011 (In

Lacs.)

As at31.3.2010 (In

Lacs.)

As at31.3.2009 (In

Lacs.)

I Opening Stock of RawMaterial 1839.63 2044.41 1054.42 1980.05

II Closing Stock of RawMaterial 1396.94 1839.63 2044.41 1054.42

Average Stock of RawMaterial [ (I + II ) / 2} 1618.285 1942.02 1549.415 1517.235

b) Raw Material Consumption per Day = (Opening Stock + Purchases - Closing Stock) / 365

I Opening Stock of RawMaterial 1839.63 2044.41 1054.42 1980.05

II Purchases 23550.96 28914.83 28616.74 28074.76

III Closing Stock of RawMaterial 1396.94 1839.63 2044.41 1054.42

Raw Material ConsumptionPer Day [(I + II - III) / 365} 66 80 76 79

A) Raw Material Conversion Period {a / b} 25 daysapprox.

24 daysapprox.

20 daysapprox.

19 daysapprox.

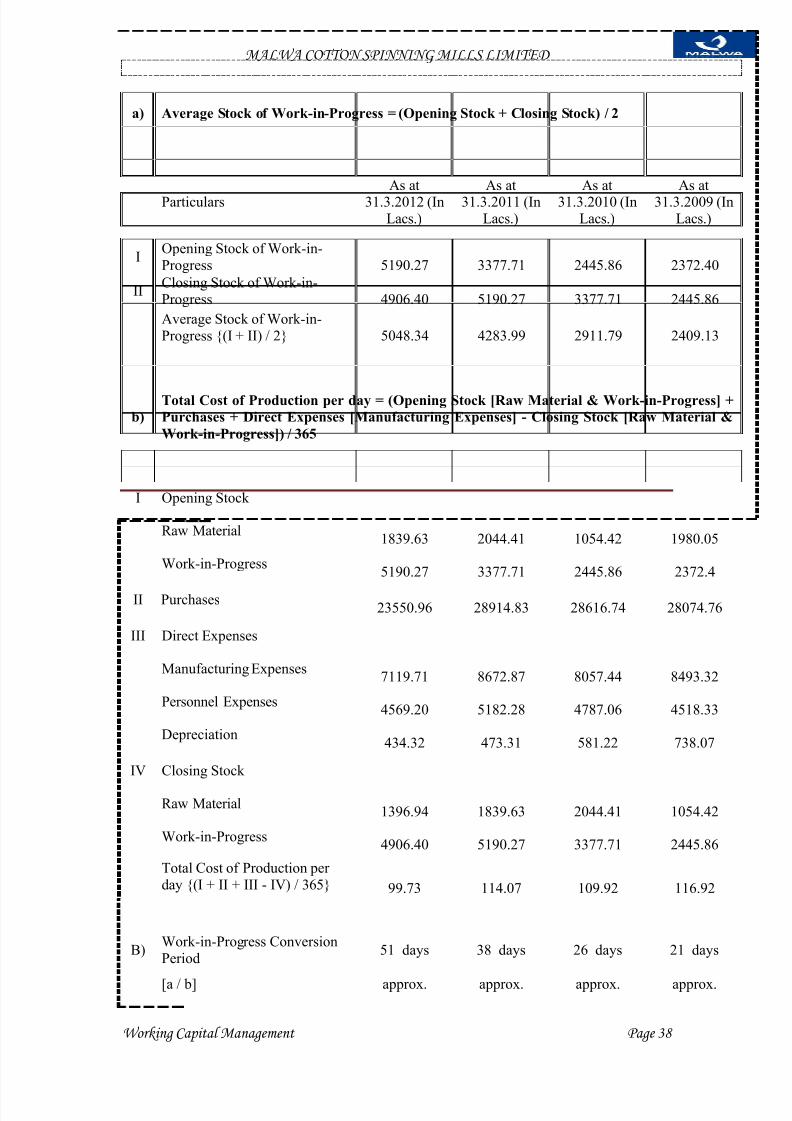

B. Work-in-progress conversion period

Average Stock of Raw MaterialRMCP = -----------------------------------------

Raw Material Consum tion er Da

Average Stock of Work-in-ProgressWIPCP = ---------------------------------------------

Total Cost of Production per day

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 38/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 38

a) Average Stock of Work-in-Progress = (Opening Stock + Closing Stock) / 2

ParticularsAs at

31.3.2012 (InLacs.)

As at31.3.2011 (In

Lacs.)

As at31.3.2010 (In

Lacs.)

As at31.3.2009 (In

Lacs.)

I Opening Stock of Work-in-Progress 5190.27 3377.71 2445.86 2372.40

II Closing Stock of Work-in-Progress 4906.40 5190.27 3377.71 2445.86Average Stock of Work-in-Progress {(I + II) / 2} 5048.34 4283.99 2911.79 2409.13

b)Total Cost of Production per day = (Opening Stock [Raw Material & Work-in-Progress] +Purchases + Direct Expenses [Manufacturing Expenses] - Closing Stock [Raw Material &Work-in-Progress]) / 365

I Opening Stock

Raw Material 1839.63 2044.41 1054.42 1980.05

Work-in-Progress 5190.27 3377.71 2445.86 2372.4

II Purchases 23550.96 28914.83 28616.74 28074.76

III Direct Expenses

Manufacturing Expenses 7119.71 8672.87 8057.44 8493.32

Personnel Expenses 4569.20 5182.28 4787.06 4518.33

Depreciation 434.32 473.31 581.22 738.07

IV Closing Stock

Raw Material 1396.94 1839.63 2044.41 1054.42

Work-in-Progress 4906.40 5190.27 3377.71 2445.86

Total Cost of Production per day {(I + II + III - IV) / 365} 99.73 114.07 109.92 116.92

B) Work-in-Progress ConversionPeriod 51 days 38 days 26 days 21 days

[a / b] approx. approx. approx. approx.

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 39/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 39

C. Finished Goods Conversion Period

a)Average Stock of Finished Goods = (Opening Stock + Closing Stock) / 2

Particulars As at 31.3.2012(In Lacs.)

As at 31.3.2011(In Lacs.)

As at31.3.2010 (In

Lacs.)

As at31.3.200

9 (InLacs.)

IOpening Stock of Finished Goods 7413.81 6256.18 6404.42 7888.35

II Closing Stock of FinishedGoods 7456.17 7413.81 6256.18 6404.42

Average Stock of Finished Goods [(I + II) /2}

7434.99 6835.00 6330.30 7146.39

b)Total Cost of Goods Sold per Day = (Opening Stock [Raw Material, Finished Goods &Work-in-Progress] + Purchases + Direct Expenses [Manufacturing Expenses] -Closing Stock [Raw Material, Finished Goods & Work-in-Progress]) / 365

I Opening Stock

Raw Material 1839.63 2044.41 1054.42 1980.05

Finished Goods 7413.81 6256.18 6404.42 7888.35

Work-in-Progress 5190.27 3377.71 2445.86 2372.4

II Purchases 23550.96 28914.83 28616.74 28074.76

III Direct Expenses

Manufacturing 7119.71 8672.87 8057.44 8493.32

Personnel Expenses 4569.20 5182.28 4787.06 4518.33

Depreciation 434.32 473.31 581.22 738.07

IV Closing Stock

Raw Material 1396.94 1839.63 2044.41 1054.42

Finished Goods 7456.17 7413.81 6256.18 6404.42

Average Stock of Finished Goods

FGCP = ---------------------------------------------Total Cost of Goods Sold per day

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 40/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 40

Work-in-Progress 4906.40 5190.27 3377.71 2445.86

Total Cost of Goods Sold per day {(I + II + III - IV)/ 365}

100 111 110 121

C) Finished Stock Conversion Period {a / b} 74 daysapprox.

62 daysapprox.

58 daysapprox.

59 daysapprox.

D. Receivables Conversion Period

a) Average Debtors = (Opening Stock + Closing Stock) / 2

ParticularsAs at

31.3.2012 (InLacs.)

As at31.3.2011 (In

Lacs.)

As at31.3.2010 (In

Lacs.)

As at31.3.2009 (In

Lacs.)

I Opening Stock of Debtors 12265.29 13060.05 12847.03 12201.84

II Closing Stock of Debtors 13777.00 12265.29 13060.05 12847.03

Average Debtors {(I +II) / 2} 13021.15 12662.67 12953.54 12524.44

b) Net Credit Sales Per Day = Sales / 365

I Sales 39823.24 45504.23 43241.4 45890.1

Net Credit Sales per Day {I / 365} 109.10 124.67 118.47 125.73

D) Receivables Conversion Period {a / b}119days

approx.

102days

approx.

109days

approx.

100days

approx.

Average DebtorsRCP = ---------------------------------------

Net Credit Sales per day

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 41/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 41

Gross Operating Cycle Period

Gross Operating Cycle Period = RMCP (A) + WIPCP (B) + FGCP © + RCP (D)

Particulars As at 31.3.2012 (InLacs.)

As at31.3.2011(In Lacs.)

As at31.3.2010(In Lacs.)

As at31.3.2009(In Lacs.)

A) Raw Material Conversion Period 25 days approx. 24 daysapprox.

20 daysapprox.

19 daysapprox.

B) Work-in-Progress ConversionPeriod 51 days 38 days 26 days 21 days

C) Finished Stock Conversion Period 74 days approx. 62 daysapprox.

58 daysapprox.

59 daysapprox.

D) Receivables Conversion Period 119 days approx. 102 daysapprox.

109 daysapprox.

100 daysapprox.

Gross Operating Cycle Period [A+ B + C + D} 269 day approx. 226 day

approx.213 dayapprox.

199 dayapprox.

Interpretation

Gross operating cycle is 269 days in 2012 which was decreased to 2011 days in the

year 2010 respectively but in the year 2012 it increased to 269 days.

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 42/55

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 43/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 43

ParticularsAs at

31.3.2012(In Lacs.)

As at31.3.2011(In Lacs.)

As at31.3.2010(In Lacs.)

As at31.3.2009(In Lacs.)

I Gross Operating Cycle Period269 dayapprox.

226 dayapprox.

213 dayapprox.

199 dayapprox.

II Payable Deferred Period 163 dayapprox.

113 dayapprox.

117 dayapprox.

95 dayapprox.

Net Operating Cycle {I - II} 106 daysapprox.

113 daysapprox.

96 daysapprox.

104 daysapprox.

Interpretation

Net Operating Cycle has been from the year 2008-09 is 104 days respectively but in2009-10 it has been decreased to 96 days. In the year 2010-11 net operating cycle has

been also increased to 113 days and 2011-12 it has been decreased to 106 days approx

respectively.

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 44/55

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 45/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 45

A. Current Ratio

The current ratio is very popular financial ratio measure as the ability of the firm to

met current liabilities. Current assets are converted into cash for the payment of

current liabilities. Apparently, higher the current ratio the greater the short termsolvency. The ratio may be expressed as-

ParticularsAs at

31.3.2012(In Lacs.)

As at31.3.2011(In Lacs.)

As at31.3.2010(In Lacs.)

As at31.3.2009(In Lacs.)

I Current Assets

Inventories 14400.52 15139.52 13295.31 10588.42

Sundry Debtors 13777.00 12665.29 13060.05 12847.03

Cash & Bank Balances 504.79 315.53 339.94 402.33

Loans & Advances 2406.65 2283.85 2310.12 2471.31

Total Current Assets 31088.96 30404.19 29005.42 26309.09

II Current Liabilities

Sundry Creditors 12229.74 8931.27 8963.85 9227.11

Total outstanding Dues to small scaleindustrial undertaking - - - -

Total outstanding Dues of creditors other thansmall scale - - - -

Trade deposits and advances 22.29 21.30 25.30 23.30

Other Liabilities 1778.32 1614.01 1474.6 1324.84

Unclaimed Dividends - - - -

Interest accrued but not due 210.49 195.81 18.90 -

Total Current Liabilities 14240.84 10762.39 10482.65 10575.25

Current Ratio {I / II} 2.18 2.83 2.77 2.49

Current AssetsCurrent Ratio = -----------------------------

Current Liabilities

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 46/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 46

INTERPRETATION

As a conventional rule, a current ratio of 2:1 or more is consider satisfactory ratio for

the concern. So the current ratio of firm shows from the year 2006 which is 3:95:1

respectively but in the year 2007 and 2008 it decrease to 3.35:1 to 2.70:1 which is

satisfactory to the firm.

B. Quick or Acid Test or Liquid Ratio

Although current ratio is a valuable indicator of liquidity, yet it may lead to

misleading conclusion, in case of inventories forms a major component of current

assets, the quick ratio is a stringent measure of liquidity. It is based on those current

assets which are the highly liquid or which are easily converted into cash. Inventories

and prepaid expenses are excluded from this category, because these are the best

liquid component of and has the ability to pay its current liabilities in time when these

are due, the ratio may be expressed as :-

Liquid Assets = Current Assets - (Inventories + Prepaid Expenses)

ParticularsAs at

31.3.2012(In Lacs.)

As at31.3.2011(In Lacs.)

As at31.3.2010(In Lacs.)

As at31.3.2009(In Lacs.)

Current Assets

Inventories 14400.52 15139.52 13295.31 10588.42

Sundry Debtors 13777.00 12265.29 13060.05 12847.03

Cash & Bank Balances 504.79 315.53 339.94 402.33

Loan & Advances 2406.65 2283.85 2310.12 2471.31

Quick/Liquid AssetsQuick/Liquid or Acid Test Ratio = -----------------------------

Current Liabilities

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 47/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 47

Total Current Assets 31088.96 30004.19 29005.42 26309.09

Less Inventories (14400.52) (15139.52) (13295.31) (10588.42)

Liquid Inventories 16688.44 14864.67 15710.11 15720.67

II Current Liabilities

Sundry Creditors 12229.74 8931.27 8963.85 9227.11

Total outstanding Dues to small scaleindustrial undertaking - - - -

Total outstanding Dues of creditors other than small scale - - - -

Trade deposits and advances 22.29 21.30 25.30 23.30

Other Liabilities 1778.32 1614.01 1474.60 1324.84

Unclaimed Dividends - - - -

Interest accrued but not due 210.49 195.81 18.90 -

14240.84 10762.39 10482.65 10575.25

Quick/Liquid or Acid Test Ratio {I / II} 1.17 : 1 1.38 : 1 1.5 : 1 1.49 : 1

Interpretation

Quick ratio is generally considered satisfactory if ratio is 1:1. Above figures show that

the quick ratio has been from 2006 is 2.52:1 respectively but in the year 2007 and

2008 it decrease to 1.91:1 to 1.44:1 although it is satisfactory to the firm.

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 48/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 48

CURRENT ASSETS MOVEMENTS OR EFFICIENCY OR

ACTIVITY RATIOS

Funds are invested in various assets in business to make sales and earn profits. The

efficiency with which assets are managed directly affect the value of sales. The better

the management of assets, the larger is the amount of sales and the profits. Activity

ratios measure the efficiency or effectiveness with which a firm manages its resources

or assets. These ratios are also called Turnover Ratios because they indicate the

speed with which assets are converted or turned over into sales.

A). Inventory Turnover Ratio

Inventory turnover ratio is also known as stock velocity. This ratio indicates the

efficiency of the firm in selling its products. It shows how rapidly the inventory is

turning in to receivable through sales. It is calculate by dividing the cost of goods sold

by the average inventory. It can be expressed as:

a) Cost of Goods Sold = Opening Stock [Raw Material, Finished Goods &Work-in-Progress] + Purchases + Direct Expenses [ManufacturingExpenses] - Closing Stock [Raw Material, Finished goods & Work-in-Progress]

ParticularsAs at

31.3.2012(In Lacs.)

As at31.3.201

1 (InLacs.)

As at31.3.2010(In Lacs.)

As at31.3.2009(In Lacs.)

I Opening Stock

Raw Material 1839.63 2044.41 1054.42 1980.05

Finished Goods 7413.81 6256.18 6404.42 7888.35

Work-in-Progress 5190.27 3377.71 2445.86 2372.4

II Purchases 23550.96 28914.83 28616.74 28074.76

Cost of Goods SoldInventory Turnover Ratio = ---------------------------------

Average Inventory at Cost

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 49/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 49

III Direct Expenses

Manufacturing 7119.71 8672.87 8057.44 8493.32

Personnel Expenses 4569.2 5182.28 4787.06 4518.33

Deprection 434.32 473.31 581.22 738.07IV Closing Stock

Raw Material 1396.94 1839.63 2044.41 1054.42

Finished Goods 7456.17 7413.81 6256.18 6404.42

Work-in-Progress 4906.4 5190.27 3377.71 2445.86

Cost of Goods Sold {I +II + III - IV} 36358.39 40477.88 40268.86 44160.58

b) Average Inventory = (Opening Stock + Closing Stock) / 2

I Opening Stock

Raw Material 1839.63 2044.41 1054.42 1980.05

Finished Goods 7413.81 6256.18 6404.42 7888.35

Work-in-Progress 5190.27 3377.71 2445.86 2372.4

II Closing Stock

Raw Material 1396.94 1839.63 2044.41 1054.42

Finished Goods 7456.17 7413.81 6256.18 6404.42

Work-in-Progress 4906.4 5190.27 3377.71 2445.86Average Inventory at Cost [(I +II) / 2} 14101.61 13061.005 10791.5 11072.75

Inventory Turnover Ratio {a / b}3 times 3 times 4 times 4 times

Interpretation

The inventory turnover ratio is decreasing in every yaer i.e. in the year 2005-06 it was

9 which was decreased to 4 and 3 in the year 2006-07 and 2007-08 respectively. It

indicates that the firm is converting its inventory of finished goods into sale

efficiently.

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 50/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 50

B) Inventory Conversion Period

It may be taken to see average time taken for clearing the stocks. This can be possible

by calculating inventory conversion period. The formula may be as :-

ParticularsAs at

31.3.2012(In Lacs.)

As at31.3.2011(In Lacs.)

As at31.3.2010(In Lacs.)

As at31.3.2009(In Lacs.)

I Inventory Turnover Ratio 3 times 3 times 4 times 4 times

Inventory Conversion Period {365 /I} 122 daysapprox. 122 daysapprox. 91 daysapprox. 91 daysapprox.

Interpretation

Inventory conversion period is continuously increasing from 2010-11 to 2012-13 from

91 days to 122 days.

C) Debtors or Receivables Turnover Period

Debtor turnover ratio indicates the velocity of debt collection of the firm. It can be

expressed as:-

a) Net Credit Sales = Sales

ParticularsAs at

31.3.2012(In Lacs.)

As at31.3.2011(In Lacs.)

As at31.3.2010(In Lacs.)

As at31.3.2009 (In

Lacs.)

I Net Credit Sales or Sales 39823.24 45504.23 43241.40 45890.1

b) Average Debtors = (Opening Stock + Closing Stock) / 2

Days in a year (365)Inventory Conversion Period = ---------------------------------

Inventory Turnover Ratio

Net Credit Annual SalesDebtors or Receivables Turnover Period = ---------------------------------

Average Trade Debtors

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 51/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 51

ParticularsAs at

31.3.2012(In Lacs.)

As at31.3.2011(In Lacs.)

As at31.3.2010(In Lacs.)

As at31.3.2009(In Lacs.)

I Opening Stock of Debtors 12265.29 13060.05 12847.03 12201.84

II Closing Stock of Debtors 13777.00 12265.29 13060.05 12847.03

Average Debtors {(I + II) / 2} 13021.15 12662.67 12953.54 12524.44

Debtors or Receivables Turnover Ratio {a / b} 3.06 times 3.59

times3.34times

3.66times

Interpretation

Debtors Turnover Ratio is continuously decreasing from 2009-10 to 2012-13 from3.06 days to 119 days.

D). Average Collection Period

The average collection period represents the average number of days from which a

firm has to wait before its receivable are converted into cash. The ratio can be

calculated as follows:

ParticularsAs at

31.3.2012(In Lacs.)

As at31.3.2011(In Lacs.)

As at31.3.2010(In Lacs.)

As at31.3.2009(In Lacs.)

I Debtors or Receivables Turnover

Ratio3.06 times 3.59

times

3.34

times

3.66

timesAverage Collection Period {365 /I}

119 daysapprox.

102 daysapprox.

109 daysapprox.

100 daysapprox.

Interpretation

Average Conversion is continuously increasing from 2009-10 to 2012-13 days 119.

Days in year (365)Average Collection Period = ------------------------------

Debtors Turnover Ratio

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 52/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 52

E). Creditors/Payable Turnover Ratio

A firm has to make credit purchases and incur short-term liabilities. A supplier of

goods, i.e. credit is naturally interested in finding out how much time the firm is likely

to take in repaying its trade creditor In Lacs. The ratio can be expressed as follows :-

a) Net Crediot Purchases = Purchases

Particulars

As at

31.3.2012(In Lacs.)

As at

31.3.2011(In Lacs.)

As at

31.3.2010(In Lacs.)

As at

31.3.2009(In Lacs.)

I Purchases 23550.96 28914.83 28616.74 28074.76

b) Average Creditors = (Opening Stock + Closing Stock) / 2

I Opening Stock of Creditors 8931.27 8963.85 9227.11 5386.06

II Closing Stock of Creditors 12229.74 8931.27 8963.85 9227.11

Average Creditors {(I + II) / 2} 10580.505 8947.560 9095.480 7306.585

Creditors / Payable Turnover Ratio {a / b} 2.23 times 3.23 times 3.15 times 3.84 times

Interpretation

Creditors Turnover Ratio is continuously decreasing from 2009-10 to 2012-13 from3.84 times to 2.23 times.

Net Credit Annual PurchaseCreditors/Payable Turnover Ratio = -----------------------------------

Average Trade Creditors

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 53/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 53

F). Creditors/Payable Turnover Ratio

The average payment period ratio represents the average number of days taken by the

firm to pay its creditors in Lacs. The ratio can be expressed as :-

ParticularsAs at

31.3.2012(In Lacs.)

As at31.3.2011(In Lacs.)

As at31.3.2010(In Lacs.)

As at31.3.2009(In Lacs.)

I Creditors / Payable Turnover Ratio 2.23 times 3.23 times 3.15 times 3.84 times

Average Payment Period {365 / I} 164 daysapprox. 113 daysapprox. 116 daysapprox. 95 daysapprox.

Interpretation

Creditor conversion period is decreasing in every year. In the year 2009 it was 95

days. But in the year 2012 it was increased to 164 days. It was due to increased in the

creditors and increase in the purchase.

G). Working Capital Turnover Ratio

Net working capital turnover ratio indicates the velocity of the utilization of working

capital. A higher ratio indicates the effective utilization of working capital and a law

ratio indicates otherwise, the ratio can be expressed:

a) Cost of Sale = Cost of Goods Sold

ParticularsAs at

31.3.2012 (InLacs.)

As at31.3.2011(In Lacs.)

As at 31.3.2010(In Lacs.)

As at31.3.2009 (In

Lacs.)

Cost of Sale / Cost of Goods Sold 36358.39 40477.88 40268.86 44160.58

b) Average Working Capital = (Opening + Closing) / 2

Net Credit Annual SalesDebtors or Receivables Turnover Period = ---------------------------------

Average Trade Debtors

Cost of SalesWorking Capital Turnover Period = ---------------------------------

Average Working Capital

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 54/55

MALWA COTTON SPINNING MILLS LIMITED

Working Capital Management Page 54

I Opening WorkingCapital 12265.29 13060.05 12847.03 12201.84

II Closing WorkingCapital 13777.00 12265.29 13060.05 12847.03

Average WorkingCapital {(I + II) / 2} 13021.145 12662.670 12953.540 12524.435

Working CapitalTurnover Ratio {a / b} 2.79 times 3.19 times 3.10 times 3.52 times

Interpretation

Working capital turnover ratio indicate that in the year 2009, ratio was 3.52 times

which means that in a that year 3.10 times working capital is turned over i.e.

converted into cash but it also increased in the year 2010 and 2011 to 3.19 and 2.79

times respectively.

7/27/2019 Final Mohit Project

http://slidepdf.com/reader/full/final-mohit-project 55/55

MALWA COTTON SPINNING MILLS LIMITED

CONCLUSION On making overall analysis of company. We arrive at conclusion that

company s performing satisfactorily. It should make effort to reduce the

operating cycle period, debtors „conversion period and increasing creditorsconversion period so as to realize early profits and cash. The liquidity position

of company is satisfactory. It can pay off its obligation in time. A company is

managing its inventory properly but efforts must be made to reduce the yearly

holding of inventory with the company it is having conservative approach in

financing of working capital.

Current ratio of the firm is according to the rule to which is 2:1 and the quick ratio of the company is also satisfactory.

The working capital turnover ratio of the company is fluctuating year by year.

Inventory turnover ratio is decreased year by year which indicate that its

inventory of finished good convert into sales efficiently.

Management of cash by the company is good.