Final Exam 3 questions: Question 1 (20%). No choice Question 1 (20%). No choice Question 2 (40%)....

24

Final Exam Final Exam 3 questions: 3 questions: Question 1 (20%). No choice Question 1 (20%). No choice Question 2 (40%). Answer 8 out Question 2 (40%). Answer 8 out of 10 short questions. of 10 short questions. ONLY THE ONLY THE FIRST 8 ATTEMPTED ANSWERS IN YOUR ANSWER FIRST 8 ATTEMPTED ANSWERS IN YOUR ANSWER BOOK WILL BE GRADED BOOK WILL BE GRADED Question 3 (40%). Answer 2 out Question 3 (40%). Answer 2 out of 4. of 4. ONLY THE FIRST 2 ATTEMPTED ANSWERS ONLY THE FIRST 2 ATTEMPTED ANSWERS IN YOUR ANSWER BOOK WILL BE GRADED IN YOUR ANSWER BOOK WILL BE GRADED

-

Upload

vivian-welch -

Category

Documents

-

view

220 -

download

2

Transcript of Final Exam 3 questions: Question 1 (20%). No choice Question 1 (20%). No choice Question 2 (40%)....

Final Exam Final Exam

3 questions:3 questions: Question 1 (20%). No choiceQuestion 1 (20%). No choice Question 2 (40%). Answer 8 out of Question 2 (40%). Answer 8 out of

10 short questions. 10 short questions. ONLY THE FIRST 8 ONLY THE FIRST 8 ATTEMPTED ANSWERS IN YOUR ANSWER ATTEMPTED ANSWERS IN YOUR ANSWER BOOK WILL BE GRADEDBOOK WILL BE GRADED

Question 3 (40%). Answer 2 out of 4. Question 3 (40%). Answer 2 out of 4. ONLY THE FIRST 2 ATTEMPTED ANSWERS IN ONLY THE FIRST 2 ATTEMPTED ANSWERS IN YOUR ANSWER BOOK WILL BE GRADEDYOUR ANSWER BOOK WILL BE GRADED

Topic 3: Topic 3: Adjustment within the Adjustment within the euro areaeuro area

European Monetary Union (EMU) European Monetary Union (EMU) launched in 1999launched in 1999

Ireland adopted the euroIreland adopted the euro Interest rates in the euro area set by Interest rates in the euro area set by

the European Central Bank (ECB)the European Central Bank (ECB) ECB’s target is to keep average euro-ECB’s target is to keep average euro-

area inflation below, but close to, 2 area inflation below, but close to, 2 percentpercent

Pros and Cons of joining Pros and Cons of joining EMUEMU

ProsPros Lower risk premium on interest rates Lower risk premium on interest rates

greater investment greater investment higher income higher income ConsCons

Domestic interest rates and exchange Domestic interest rates and exchange rate no longer respond to shocks to the rate no longer respond to shocks to the Irish economy Irish economy

Optimal Currency Area Optimal Currency Area (OCA)(OCA)

Members can perform well using a Members can perform well using a common currencycommon currency

Asymmetric shocksAsymmetric shocks Shocks that affect some economies but Shocks that affect some economies but

not others, or common shock that not others, or common shock that affects economies in different waysaffects economies in different ways

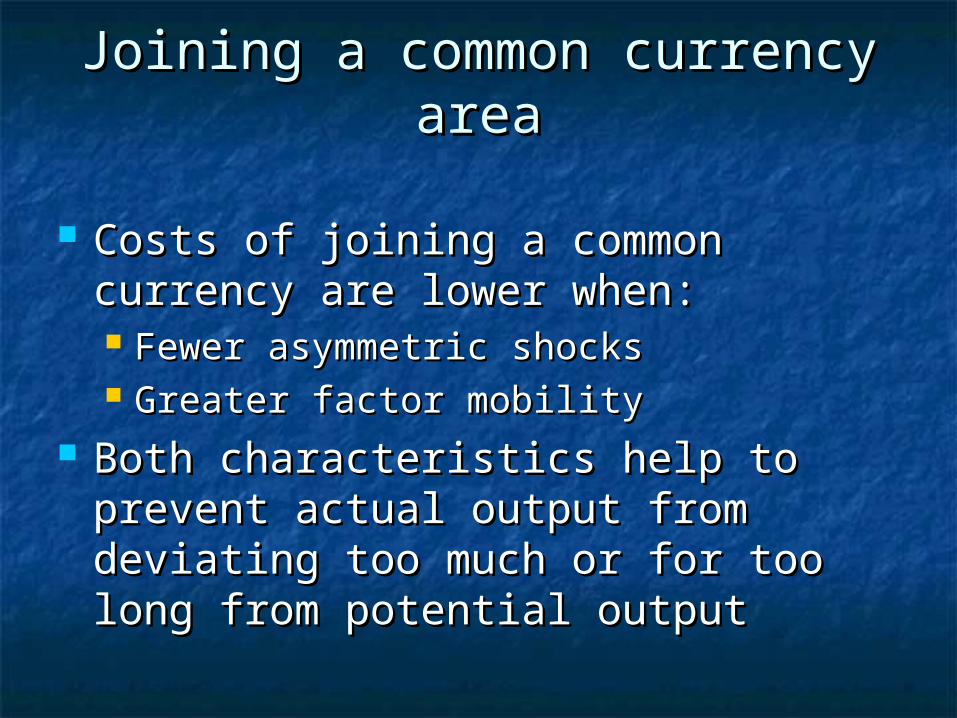

Joining a common currency Joining a common currency areaarea

Costs of joining a common currency Costs of joining a common currency are lower when:are lower when: Fewer asymmetric shocksFewer asymmetric shocks Greater factor mobilityGreater factor mobility

Both characteristics help to prevent Both characteristics help to prevent actual output from deviating too actual output from deviating too much or for too long from potential much or for too long from potential outputoutput

Asymmetric shocksAsymmetric shocks

When bad shocks hit a country that When bad shocks hit a country that is not part of a currency union:is not part of a currency union: Central bank cuts interest rates to spur Central bank cuts interest rates to spur

domestic demand domestic demand Exchange rate depreciates which helps Exchange rate depreciates which helps

to boost international competitivenessto boost international competitiveness Opposite occurs when good shocks Opposite occurs when good shocks

hithit

Asymmetric shocksAsymmetric shocks

Euro-area interest rates and the euro Euro-area interest rates and the euro exchange rate will respond to exchange rate will respond to common (symmetric) shocks to the common (symmetric) shocks to the euro areaeuro area

But they will not respond to But they will not respond to asymmetric shocks that hit Irelandasymmetric shocks that hit Ireland

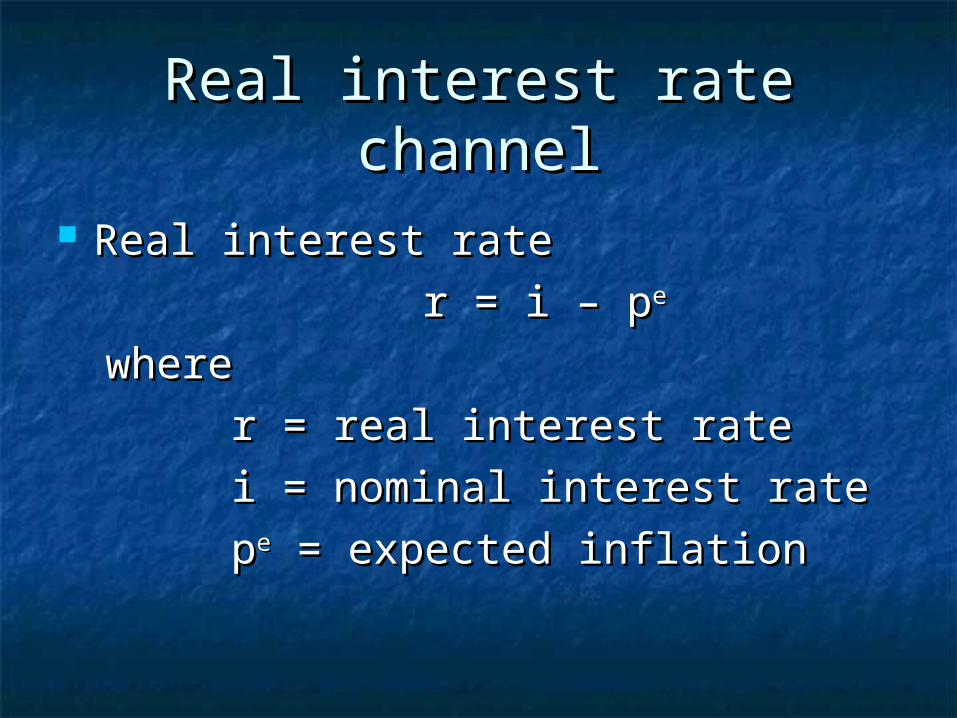

Real interest rate channelReal interest rate channel

Real interest rateReal interest rate

r = i – pr = i – pee

wherewhere

r = real interest rater = real interest rate

i = nominal interest ratei = nominal interest rate

ppee = expected inflation = expected inflation

Real interest rate channelReal interest rate channel

Low real interest rates boost Low real interest rates boost economic activityeconomic activity

High real interest rates depress High real interest rates depress economic activityeconomic activity

Dilemma: faster growing members of Dilemma: faster growing members of EMU may have higher inflation rates EMU may have higher inflation rates and thereby face lower real interest and thereby face lower real interest rates rates

Divergence Divergence

Divergence in inflation rates Divergence in inflation rates divergence in economic performance divergence in economic performance further divergence in inflation further divergence in inflation rates rates … etc. … etc.

Divergence in the euro areaDivergence in the euro area

Dispersion of inflation much lower Dispersion of inflation much lower during EMU than in early 1990s. during EMU than in early 1990s. Similar dispersion to the United Similar dispersion to the United StatesStates

Growth dispersion not unusually Growth dispersion not unusually largelarge

However, both inflation and growth However, both inflation and growth dispersion are persistentdispersion are persistent

Sources of euro-area Sources of euro-area divergencedivergence

ConvergenceConvergence nominal interest ratesnominal interest rates price levels (though mostly pre-EMU)price levels (though mostly pre-EMU) Balassa-Samuelson effectBalassa-Samuelson effect

Asymmetric shocksAsymmetric shocks National policiesNational policies

Pro-cyclical fiscal policyPro-cyclical fiscal policy

Factor mobilityFactor mobility

Labour and capital move to booming Labour and capital move to booming region, boosting supply of output in region, boosting supply of output in that regionthat region reduces overheating pressuresreduces overheating pressures

Labour and capital move out of Labour and capital move out of depressed region, reducing supply of depressed region, reducing supply of output in that regionoutput in that region reduces excess capacityreduces excess capacity

Real exchange rate channelReal exchange rate channel

If faster growing members of EMU If faster growing members of EMU have higher inflation rates have higher inflation rates real real effective exchange rates are effective exchange rates are appreciating appreciating dampens export dampens export growthgrowth

Converse holds for slower growing Converse holds for slower growing members of EMUmembers of EMU

Real exchange rate channelReal exchange rate channel

This channel requires price and wage This channel requires price and wage flexibilityflexibility

Does not have much effect on Does not have much effect on relatively closed economiesrelatively closed economies

Can take a long time to operateCan take a long time to operate

Cross-country fiscal Cross-country fiscal transferstransfers

The euro area lacks a cross-member The euro area lacks a cross-member fiscal transfer mechanism that could fiscal transfer mechanism that could help to reduce divergenceshelp to reduce divergences

National fiscal policyNational fiscal policy

EMU works best if member countries EMU works best if member countries avoid pro-cyclical fiscal policyavoid pro-cyclical fiscal policy

Stance of fiscal policy measured by Stance of fiscal policy measured by cyclically-adjusted (structural) fiscal cyclically-adjusted (structural) fiscal balancebalance (Actual) budget balances automatically (Actual) budget balances automatically

rise during booms and fall during rise during booms and fall during recessionsrecessions

Structural fiscal balanceStructural fiscal balance

Improvement of the structural fiscal Improvement of the structural fiscal balance implies fiscal contractionbalance implies fiscal contraction

Deterioration of structural fiscal Deterioration of structural fiscal balance implies fiscal expansionbalance implies fiscal expansion

CommentsComments

Overall balance = current balance + Overall balance = current balance + capital balancecapital balance Government is running a large capital Government is running a large capital

deficitdeficit Overall balance = primary balance – Overall balance = primary balance –

interest payments interest payments

Fiscal policyFiscal policy

Sustainability of EMU put at risk if Sustainability of EMU put at risk if national governments do not run national governments do not run counter-cyclical fiscal policiescounter-cyclical fiscal policies Loosen fiscal policy when times are bad, Loosen fiscal policy when times are bad,

and tighten when things are good.and tighten when things are good. Stability and Growth Pact (SGP) limits Stability and Growth Pact (SGP) limits

fiscal deficits to 3% of GDPfiscal deficits to 3% of GDP Some members are violating ruleSome members are violating rule

Fiscal balanceFiscal balance

Government medium-term objective Government medium-term objective is to have the fiscal position close to is to have the fiscal position close to balancebalance

Arguments for large fiscal surplus in Arguments for large fiscal surplus in the short termthe short term Room to manoeuvre if bad shock hitsRoom to manoeuvre if bad shock hits Future age-related spending pressuresFuture age-related spending pressures

National Pension Reserve FundNational Pension Reserve Fund

![Sample Final Question 1 (50 points] Multiple Choice — 10 questions ...](https://static.fdocuments.net/doc/165x107/586a2e181a28ab532e8b8f4c/sample-final-question-1-50-points-multiple-choice-10-questions-.jpg)