FIN 4604 Sample Questions II

40

IN 4604 Sample Questions Set II PART A: 1. Which of the following best describes currency options sold through an options exchange. They grant the buyer a right: a. To buy or sell and are standardized. b. To buy or sell and are tailored to the desire of the owner. c. But not the obligation, to buy or sell and are tailored to owner’s needs. d. But not the obligation, to buy or sell and are standardized. 2. Forward contracts contain: a. A commitment to the owner, and are standardized. b. A commitment to the owner, and can be tailored to the desire of the owner. c. A right but not a commitment to the owner, and can be tailored to the desire of the owner. d. A right but not a commitment to the owner and are standardized. 3. If your firm expects the euro to substantially depreciate, it could speculate by _______ euro call options or _______euros forward in the forward exchange market. a. Selling; selling b. Selling; purchasing c. Purchasing; purchasing d. Purchasing; selling 4. When you purchase ________, there is no obligation on your part; however, when you purchase ________, there is an obligation on your part. a. Call options; put options b. Futures contracts; call options c. Forward contracts; futures contracts d. Put options; forward contracts 1

-

Upload

evelyn-jiewei-li -

Category

Documents

-

view

549 -

download

33

Transcript of FIN 4604 Sample Questions II

IN 4604 Sample Questions Set II PART A:1. Which of the following best describes currency options sold through an options exchange. They grant the buyer a right:

a. To buy or sell and are standardized.b. To buy or sell and are tailored to the desire of the owner.c. But not the obligation, to buy or sell and are tailored to owner’s needs.d. But not the obligation, to buy or sell and are standardized.

2. Forward contracts contain:a. A commitment to the owner, and are standardized.b. A commitment to the owner, and can be tailored to the desire of the owner.c. A right but not a commitment to the owner, and can be tailored to the desire

of the owner.d. A right but not a commitment to the owner and are standardized.

3. If your firm expects the euro to substantially depreciate, it could speculate by _______ euro call options or _______euros forward in the forward exchange market.

a. Selling; sellingb. Selling; purchasingc. Purchasing; purchasingd. Purchasing; selling

4. When you purchase ________, there is no obligation on your part; however, when you purchase ________, there is an obligation on your part.

a. Call options; put optionsb. Futures contracts; call optionsc. Forward contracts; futures contractsd. Put options; forward contracts

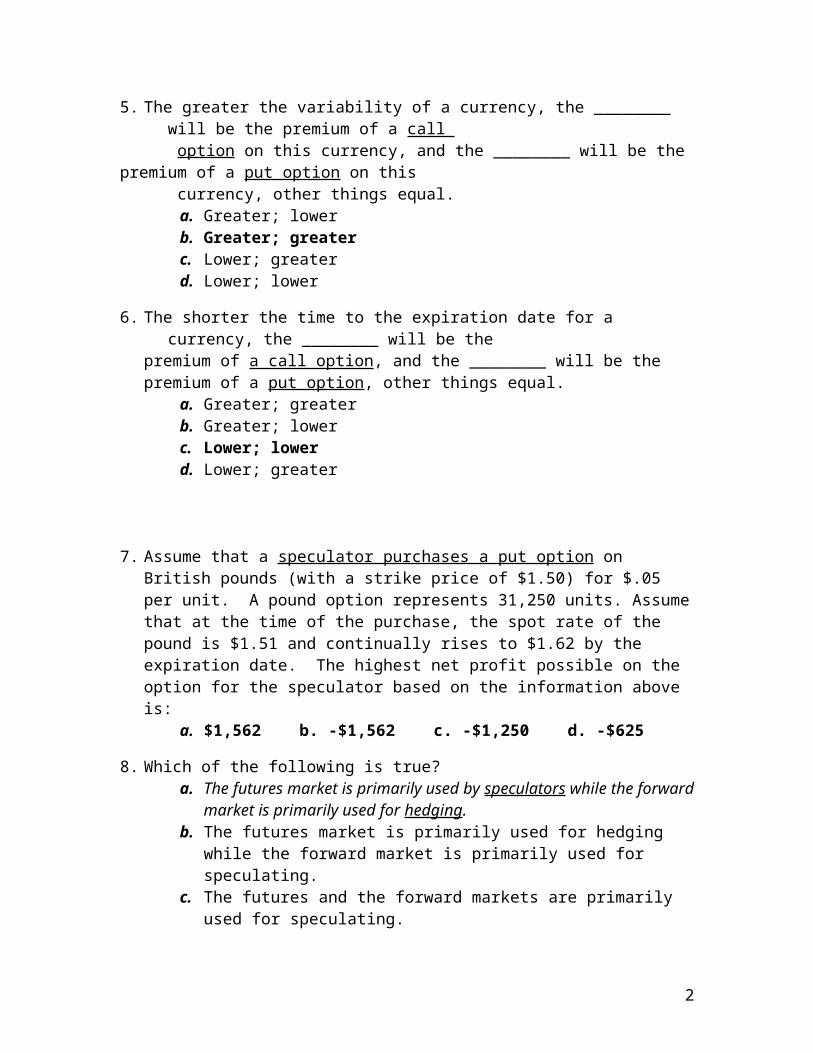

5. The greater the variability of a currency, the ________ will be the premium of a call option on this currency, and the ________ will be the premium of a put option on this currency, other things equal.

a. Greater; lowerb. Greater; greaterc. Lower; greaterd. Lower; lower

6. The shorter the time to the expiration date for a currency, the ________ will be the premium of a call option, and the ________ will be the premium of a put option, other things equal.

a. Greater; greaterb. Greater; lowerc. Lower; lowerd. Lower; greater

1

7. Assume that a speculator purchases a put option on British pounds (with a strike price of $1.50) for $.05 per unit. A pound option represents 31,250 units. Assume that at the time of the purchase, the spot rate of the pound is $1.51 and continually rises to $1.62 by the expiration date. The highest net profit possible on the option for the speculator based on the information above is:

a. $1,562 b. -$1,562 c. -$1,250 d. -$625

8. Which of the following is true?a. The futures market is primarily used by speculators while the forward

market is primarily used for hedging.b. The futures market is primarily used for hedging while the forward market

is primarily used for speculating.c. The futures and the forward markets are primarily used for speculating.d. The futures and the forward markets are primarily used for hedging.

9. If you expect the euro to depreciate, it would be appropriate to ________ for speculative purposes.

a. Buy a euro call and buy a euro putb. Buy a euro call and sell a euro putc. Sell a euro call and sell a euro putd. Sell a euro call and buy a euro put

10. If you expect the British pound to appreciate, you could speculate by ________ pound call options or ________ pound put options.

a. Purchasing; sellingb. Purchasing; purchasingc. Selling; sellingd. Selling; purchasing

11. Which of the following is correct about a currency option, other things equal?a. The longer the time to maturity, the less the value of a call option.b. The longer the time to maturity, the less the value of a put option.c. The higher the spot rate relative to the exercise price, the greater the value of

a put option.d. The lower the exercises price relative to the spot rate, the greater the value

of a call option.

12. Assume no transactions costs exist for any futures or forward contracts. The price of British pound futures with a settlement date 180 days from now will:

a. Definitely be above the 180-day forward rate.b. Definitely be below the 180-day forward rate.c. Be about the same as the 180-day forward rate.d. There is no relation between the futures and forward prices.

2

13. A firm sells a currency futures contract and then decides before the settlement date that it no longer wants to maintain such a position. It can close out its position by:

a. Buying an identical futures contract.b. Selling an identical futures contract.c. Buying a futures contract with a different settlement date.d. Selling a futures contract for a different among of currency.e. Purchasing a put option contract in the same currency.

14. If the spot rate of the euro increased substantially over a one-month period, the futures price on euros would likely ____________over that same period.

a. Increase slightlyb. Decrease substantiallyc. Increase substantiallyd. Stay the same

15. A U.S. firm is bidding for a project needed by the Swiss government. The firm will not know if the bid is accepted until three months from now. The firm will need Swiss francs to cover expenses but will be paid by the Swiss government in dollars if it is hired for the project. The firm can best insulate itself against exchange rate exposure by:

a. Selling futures in francs.b. Buying futures in francs.c. Buying franc put options.d. Buying franc call options.

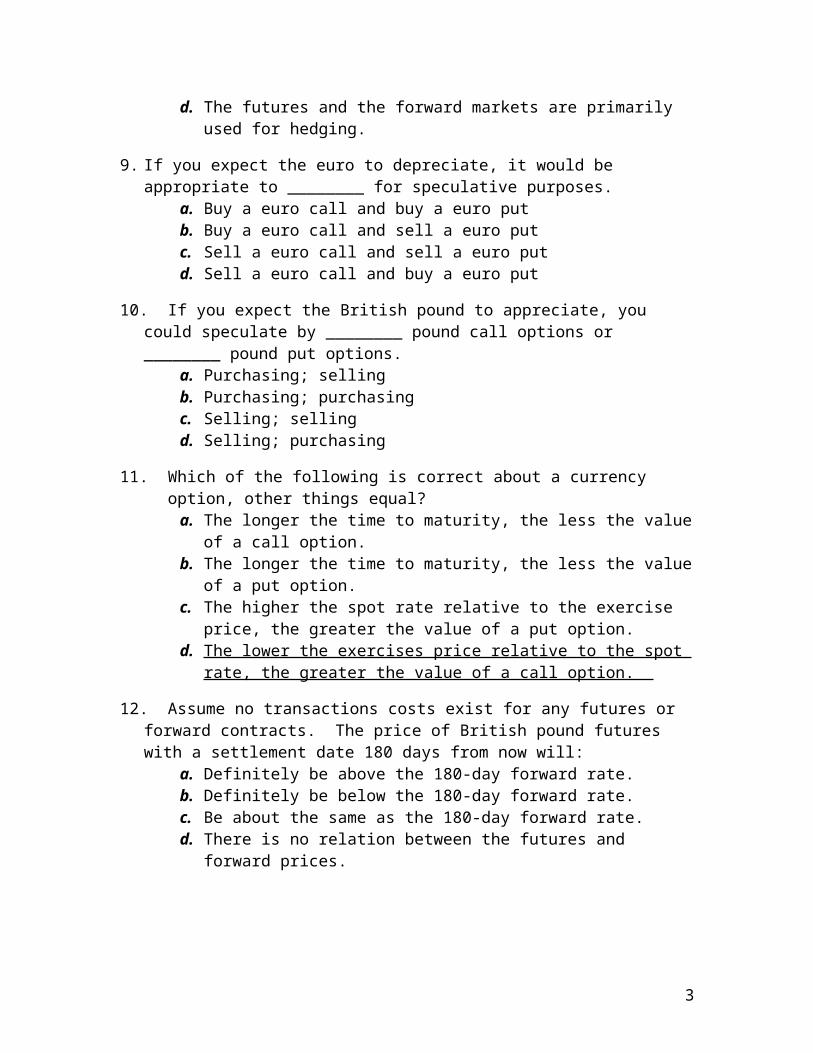

16. The premium on a pound put option is $.03 per unit. The exercise price is $1.60. The break-even point is ________ for the buyer of the put, and ________ for the seller of the put. (Assume zero transactions costs and that the buyer and seller of the put option are speculators.)

a. $1.63; $1.63b. $1.63; $1.60c. $1.63; $1.57d. $1.57; $1.63e. $1.57; $1.57

Solution: 1(-.03 +1.60 –X) = 0 for buyer of a put. 1(.03 - 1.60+X) = 0 for seller of a put.

17. You purchase a call option on pounds for a premium of $.03 per unit, with an exercise price of $1.64; the option will not be exercised until the expiration date, if at all. If the spot rate on the expiration date is $1.65, your net profit per unit is:

a. -$.03b. -$.02c. -$.01d. $.02e. None of the above

3

18. You purchase a put option on Swiss francs for a premium of $.02, with an exercise price of $.61. The option will not be exercised until the expiration date, if at all. If the spot rate on the expiration date is $.58, your net profit per unit is:

a. -$.03.b. -$.02.c. -$.01.d. $.02.e. None of the above.

19. You are a speculator who sells a call option on Swiss francs for a premium of $.06, with an exercise price of $.64. The option will not be exercised until the expiration date, if at all. The spot rate of the Swiss franc is $.69 on the expiration date, your net profit per unit is:

a. -$.02.b. -$.01.c. $.01d. $.02e. None of the above.

20. You are a speculator who sells a put option on Canadian dollars for a premium of $.03 per unit, with an exercise price of $.86. The option will not be exercised until the expiration date, if at all. If the spot rate of the Canadian dollar is $.78 on the expiration date, your net profit per unit is:

a. -$.08.b. -$.03.c. $.05.d. $.08.e. None of the above.

21. Macomb Corporation is a U.S. firm that invoices some of its exports in Japanese yen. If it expects the yen to depreciate, it could ________ to hedge the exchange rate risk on those exports.

a. Sell yen put optionsb. Buy yen call optionsc. Buy futures contracts on yend. Sell futures contracts on yen

22. A call option on Australian dollars has a strike (exercise) price of $.56. The present exchange rate is $.59. This call option can be referred to as:

a. In the money .b. Out of the money.c. At the money.d. At a discount.

4

23 A put option on British pounds has a strike (exercise) price of $1.48. The present exchange rate is $1.55. This put option can be referred to as:

a. In the moneyb. Out of the money c. At the moneyd. At a discount

24 A U.S. corporation has purchased currency put options to hedge a 100,000 Canadian dollar (C$) receivable. The premium is $.01 and the exercise price of the option is $.75. If the spot rate at the time of maturity is $.85, what is the net amount received by the corporation if it acts rationally?

a. $74,000 b. $84,000 c. $75,000 d. $85,000

25 A U.S. corporation has purchased currency call options to hedge a 62,500 British pounds payable. The premium is $.02 per unit and the exercise price of the option is $1.50. If the spot rate of the pound at maturity is $1.65, what is the total amount paid by the corporation if it acts rationally?

a. $101,875 b. $103,125 c. $104,375 d. $95,000 e. $93,750

26 Your company expects to receive 5,000,000 Japanese yen 60 days from now. You decide to hedge your position by selling Japanese yen forward. The current spot rate of the yen is $.0089, while the forward rate is $.0095. If the spot rate turns out to be $.0090 in 60 days, how many dollars will you receive for the 5,000,000 yen at that time?

a. $44,500 b. $45,000 c. $526m d. $47,500 e. $556m

27 Due to ________, market forces should realign the relationship between the interest rate differential between two countries and the forward premium or discount on the exchange rate between their two currencies.

a. Uncovered interest arbitrageb. Triangular arbitragec. Covered interest arbitraged. Locational arbitrage

28 Due to ________, market forces should realign the spot rate of a currency among banks.

a. Uncovered interest arbitrageb. Triangular arbitragec. Covered interest arbitraged. Locational arbitrage

29 Due to ________, market forces should realign the difference between the cross exchange rate for a currency from, say points A and B, and the quoted rate for the same currency at point C.

a. Uncovered interest arbitrageb. Triangular arbitragec. Covered interest arbitraged. Locational arbitrage

5

30 If interest rate parity holds, then ________ is not feasible.a. Uncovered interest arbitrageb. Triangular arbitragec. Covered interest arbitraged. Locational arbitrage

31 In which case will locational arbitrage be most likely feasible? Bank A’s:a. Ask price for a currency is greater than Bank B’s bid price for the currency b. Bid price for a currency is greater than Bank B’s ask price for the currencyc. Ask price for a currency is less than Bank B’s ask price for the currencyd. Bid price for a currency is less than Bank B’s bid price for the currency

32 Assume that the interest rate in for Currency X is much higher than the U.S. interest rate. According to Interest Rate Parity Theory, the forward rate of Currency X should:

a. Exhibit a discount.b. Exhibit a premium.c. Be equal its spot rate.d. Be equal to its future spot rate.

33 If interest rate is higher in the U.S. than in the U.K. and the forward rate of the British pound is the same as its spot rate, then:

a. Arbitrage flow of funds takes place from U.S. to U.K.b. Arbitrage flow of funds takes place from U.K. to U.S.c. No arbitrage flow of funds takes place between the U.S. and the U.K. d. A and B.

34 Assume that U.S. investors are benefiting from covered interest arbitrage due to high interest rate on euro. Which of the following adjustments should result from covered interest arbitrage?

a. Downward pressure on the euro’s spot rate.b. Downward pressure on the euro’s forward rate.c. Downward pressure on the U.S. interest rate.d. Upward pressure on the euro’s interest rate.

35 Assume that a U.S. firm can invest funds for one year in the U.S. at 12% or invest funds in Mexico at 14%. The spot rate of the peso is $.10 while the one-year forward rate of the peso is $.10. If a U.S. firm uses covered interest arbitrage, which of the following price adjustments should result?

a. Spot rate of peso increases; forward rate of peso decreases.b. Spot rate of peso decreases; forward rate of peso increases.c. Spot rate of peso decreases; forward rate of peso decreases.d. Spot rate of peso increases; forward rate of peso increases.

36 Assume the bid rate of a New Zealand dollar is $.33 while the ask rate is $.335 at Bank X. Assume the bid rate of the New Zealand dollar is $.32 while the ask rate is $.325 at Bank Y. Given this information what would be your gain if you use $1,000,000 and execute locational arbitrage? That is, how much will you end up with over and above the $1,000,000 you started with?

a. $15,385 b. $15,625 c. $22,136 d. $31,250

6

37. Based on interest rate parity, the larger the degree by which the foreign interest rate exceeds domestic interest rate, the: a. Larger will be the forward discount of the foreign currency.

b. Larger will be the forward premium of the foreign currency.c. Smaller will be the forward premium of the foreign currency.d. Smaller will be the forward discount of the foreign currency.

38. Assume the following information. You have $1,000,000 to invest.Current spot rate of pound = $1.3090-day forward rate of pound = $1.283-month deposit rate in U.S. = 2.25%3-month deposit rate in U.K. = 4%If you use covered interest arbitrage for a 90-day investment, what will be the amount of U.S. dollars you will have after 90 days?

a. $1,024,000. b. $1,030,000 c. $1,040,000 d. $1,034,000 e. None of above

39. Assume the following information:Current spot rate of New Zealand dollar = $.41Forecasted spot rate of New Zealand dollar 1 year from now = $.43One year forward rate of the New Zealand dollar = $.42Annual interest rate on New Zealand dollars = 8%Annual interest rate on U.S. dollars = 9%Compute the return from covered interest arbitrage by a U.S. investor with $500,000 to invest.

a. 11.97 % b. 9.63% c. 11.12% d. 11.64% e. 10.63%

40. If annualized nominal interest rates in the US and Switzerland are 12% and 8% respectively and the 90-day forward rate for the Swiss franc is $1.0218, at what current spot rate will interest rate parity hold?

a. $1.0418. b. $1.0215. c. $1.4184.

d. $1.0022e. None of the above.

41. Assume the following information:Spot rate today of Swiss franc = $.601-year forward rate as of today for Swiss franc = $.63Expected spot rate 1 year from now = $.64Rate on 1-year deposits denominated in Swiss francs = 7%Rate on 1-year deposits denominated in U.S. dollars = 9%From the perspective of a U.S. investor with $1,000,000, covered interest arbitrage would yield a rate of return of ________.

a. 5 % b. 12.35% c. 15.50% d. 14.13% e. 11.22%

7

42. Assume the British interest rates are higher than U.S. rates, and that the spot rate for the pound equals the forward rate, then covered interest arbitrage puts ______ pressure on the pound’s spot rate, and ______ pressure on the pound’s forward rate.

a. Downward; downwardb. Downward; upwardc. Upward; downwardd. Upward; upwarde. Zero; zero

43. Assume the following information. You have $1,000,000 to invest. Current sport rate of pound = $1.60 90-day forward rate of pound = $1.57 3-month deposit rate in U.S. = 3% 3-month deposit rate in U.K. = 4% If you use covered interest arbitrage for a 90-day investment, what will be the amount of U.S. dollars you will have after 90 days?

a. $1,020,500. b. $1,045,600 c. $1,073,330 d. $1,094,230 e. $1,116,250

44. Assume the following information: Current spot rate of Australian dollar = $.64 Forecasted spot rate of Australian dollar 1 year from now = $.59 1-year forward rate of Australian dollar = $.62 Annual interest rate for Australian dollar deposit = 9% Annual interest rate in U.S. = 6%

Given the above information, the return from covered interest arbitrage by a U.S. investor with $500,000 to invest is: ________. a. 6 % b. 9% c. 7.33% d. 8.14% e. 5.59%

45. Given that annual deposit rates for Dollars and Euros are 6% and 4% respectively for the next 5 years. If the current spot rate of the Euro is $1.4015, obtain the implied rate for the Euro five years from now if International Fisher Equation holds exactly. a. $1.5415 b. $1.2742 c. $1.4284 d. $1.3750 e. None of the above.

46. According to interest rate parity (IRP), the: a. Forward rate differs from the spot rate by a sufficient amount to offset

the inflation differential between two countries. b. Future spot rate differs from the current spot rate by a sufficient amount to offset the interest rate differential between two countries. c. Future spot rate differs from the current sport rate by a sufficient amount to offset the inflation differential between two countries. d. Forward rate differs from the spot rate by a sufficient amount to offset the interest rate differential between two countries.

47. Assume that interest rate parity (IRP) holds. The Mexican interest rate is 5%, and the U.S. interest rate is 8%. Subsequently, the U.S. interest rate decreases to 7%. If IRP is to continue to hold, then the peso’s forward ________ will ________. a. Premium; increase b. Discount; decrease c. Discount; increase d. Premium; decrease

8

48. The Purchasing Power Parity (PPP) suggests that a home currency will: a. Depreciate if home inflation rate exceeds foreign interest rate. b. Appreciate if home interest rate exceeds foreign interest rate. c. Appreciate if home inflation rate exceeds foreign inflation rate. d. Depreciate if home inflation rate exceeds foreign inflation rate.

49. The International Fisher Equation (IFE) suggests that a home currency will: a. Depreciate if home interest rate exceeds foreign interest rate. b. Appreciate if home interest rate exceeds foreign interest rate. c. Appreciate if home inflation rate exceeds foreign inflation rate. d. Depreciate if home inflation rate exceeds foreign inflation rate.

50. Because there are a variety of factors in addition to inflation that affect exchange rates, this will tend to: a. Reduce the probability that PPP shall hold. b. Increase the probability that PPP shall hold. c. Increase the probability the IFE will hold. d. Increase the probability that FE will hold. e. Both (a) and (c)

51. According to the IFE, if British interest rates exceed U.S. interest rates,a. The British pound’s value will remain constant.b. The British pound will depreciate against the dollar.c. The British inflation rate will decrease.d. The forward rate of the British pound will contain a premium.e. Today’s forward rate of the British pound will equal today’s spot rate.

52. The International Fisher Equation (IFE) suggests that:a. Nominal interest rates for domestic and foreign countries are the sameb. Inflation rates for domestic and foreign countries are the samec. Exchange rates for both domestic and foreign currencies will move in the same direction.d. None of the above.

53. If interest rates on the euro are consistently below U.S. interest rates, then for the International Fisher Equation (IFE) to hold,

a. The value of the euro will appreciate against the dollar.b. The value of the euro will depreciate against the dollar.c. The value of the euro will remain constant with respect to the dollard. The value of the euro will appreciate in some periods and depreciate in other periods, but on average have a zero rate of appreciation.

54. Under Purchasing Power Parity, the future spot exchange rate is a function of the initial spot rate in equilibrium and:

a. The income differential.b. The forward discount or premium.c. The inflation differential.d. The Interest rate differentiale. None of the above.

9

55. According to the Fisher Equation, if U.S. investors expect a 5% rate of domestic inflation over one year and require a 3% real return on investments over one year, the exact nominal interest rate on one-year U.S. treasury security would be:

a. 2 % b. 3 % c. 8.15 % d. 5 %

e. 8 %

56. Assume that the Fisher Equation holds approximately for domestic and foreign countries. If investors in all countries require the same real return, then the difference in nominal interest rates between any two countries is:

a. Equal to the exchange rate between their two currencies.b. Equal to their inflation differential.c. Equal to zerod. Constant over time.e. Both a and d.

57. Assume U.S. and Swiss investors require a real rate of return of 3%. Assume the nominal U.S. interest rate is 6% and the nominal Swiss rate is 4%. According to the International Fisher Equation, the Swiss franc will _____ by about ______.

a. Appreciate; 3%b. Appreciate; 1%c. Depreciate; 3%d. Depreciate; 2%e. Appreciate; 2%

58. According to the International Fisher Equation and the Generalized Fisher Equation, if Venezuela has a much higher nominal interest rate than other countries, its inflation rate will be ______ than other countries, and its currency will _______. a. Lower; strengthen

b. Lower; weakenc. Higher; weakend Higher; strengthen

59. According to the “law of one price,” a. The price of an identical product should be equal across markets when measured in a common currency. b. Interest rates across markets should be equal over the same period. c. Inflation rates across markets should be equal over the same period. d. The forward rate should be an unbiased predictor of future spot rate.

60. The ________ is also referred to as the “law of one price.” a. International Fisher Equation

b. Absolute Purchasing Power Parityc. Relative Purchasing Power Parityd. Covered Interest Arbitragee. Interest Rate Parity Theory

10

61. Latin American countries have historically experienced relatively high inflation rates and their currencies have weakened accordingly. This experience is consistent with the concept of: a. Interest rate parity. b. Locational arbitrage. c. Purchasing power parity. d. The exchange rate mechanism.

62. Assume that during a given period the nominal interest rate in Cyprus was 7% while the nominal interest rate in the US was 5%. The spot rate for the Cyprus pound ($/CYP) started at $1.50. At the end of the period, according to the IFE, the Cyprus pound should adjust to a new level of: a. $1.47 b. $1.53 c. $1.43 d. $1.57

63. Translation exposure reflects the exposure of a firm’s: a. Ongoing international transactions to exchange rate fluctuations.

b. Local currency value to transactions between foreign exchange traders. c. Financial statements to exchange rate fluctuations. d. Future cash flows to exchange rate fluctuations. 64. Transaction exposure reflects the exposure of a firm’s: a. Ongoing international transactions to exchange rate fluctuations. b. Local currency value to transactions between foreign exchange traders.

c. Financial statements to exchange rate fluctuations. d. Future cash flows to exchange rate fluctuations.

65. Economic exposure refers to the exposure of a firm’s: a. Ongoing international transactions to exchange rate fluctuations. b. Local currency value to transactions between foreign exchange traders. c. Financial statements to exchange rate fluctuations. d. Future cash flows to exchange rate fluctuations. e. Income statement to exchange rate fluctuations.

66. Which of the following operations benefits from an appreciation of a firm’s local currency?

a. Borrowing immediately in a foreign currency and converting the funds to the local currency. b. Receiving future dividends from foreign subsidiaries.

c. Purchasing future supplies locally rather than overseas. d. Exporting to foreign countries.

67. Economic exposure can affect: a. MNC only. b. Purely domestic firms only. c. Both MNC and Purely domestic firms. d. None of the above.

11

68. Generally, MNC with less foreign costs than foreign revenue will be _____ affected by a _____ foreign currency.

a. Favorably; strongerb. Adversely; strongerc. Favorably; weakerd. Adversely; weakere. A and D

69. A firm produces goods for which substitute goods are produced in other countries. An appreciation of the firm’s local currency should: a. Increase local sales as it reduces competition in local markets. b. Increase the firm’s exports denominated in the local currency. c. Increase the returns earned on the firm’s foreign bank deposits. d. Increase the firm’s cash outflow required to pay for imported supplies

denominated in a foreign currency. e. None of the above.

70. A firm produces goods for which substitute goods are produced in other countries. A depreciation of the firm’s local currency should:

a. Decrease local sales as it decreases competition in local markets.b. Decrease the firm’s exports denominated in the local currency.

c. Decrease the returns earned on the firm’s foreign bank deposits.d. Decrease the firm’s cash outflow required to pay for imported supplies denominated in foreign currency.

e. None of the above.

71. Which of the following is not a form of exposure to exchange rate fluctuations?a. Transaction exposure.b. Credit exposure / Transnational exposurec. Economic exposure.d. Translation exposure.

72. ________ is not a determinant of translation exposure.a. The MNCs degree of foreign involvementb. The locations of foreign subsidiariesc. The local (domestic) earnings of the MNCd. The accounting methods (FASB rules)used

73. Assume the following information: U.S. deposit rate for 1 year = 11% U.S. borrowing rate for 1 year = 12% Swiss deposit rate for 1 year = 8% Swiss borrowing rate for 1 year = 10% Swiss forward rate for 1 year = $.40 Swiss franc spot rate = $.39 Also assume that a U.S. exporter denominates its Swiss exports in Swiss francs and expects to receive SF600,000 in 1 year. Using the information above, what will be the approximate value of these exports in 1 year in U.S. dollars given that the firm executes a forward hedge?

a. $234,000. b. $238,584. c. $240,000. d. $236,127

12

74. Assume the following information: U.S. deposit rate for 1 year = 11% U.S. borrowing rate for 1 year = 12% New Zealand deposit rate for 1 year = 8% New Zealand borrowing rate for 1 year = 10% New Zealand dollar forward rate for 1 year = $.40 New Zealand dollar spot rate = $.39 Also assume that a U.S. exporter denominates its New Zealand exports in NZ$ and expects to receive NZ$600,000 in 1 year. Using the information provided, what will be the approximate value of these exports in 1 year in U.S. dollars given that the firm executes a money market hedge? a. $238,584. b. $240,000 c. $234,000. d. $236,127.

75. If a U.S. firm desired to lock in the maximum amount it would have to pay for its net payables in euros but still wanted to be able to capitalize if the euro depreciates substantially against the dollar by the time payment is to be made, the most appropriate hedge would be: a. A money market hedge. b. Purchasing euro put options. c. A forward purchase of euros.

d. Purchasing euro call options. e. Selling euro call options.

76. If a U.S. firm desired to lock in a minimum rate at which it could sell its net receivables in Japanese yen but wanted to be able to capitalize if the yen appreciates substantially against the dollar by the time payment arrives, the most appropriate hedge would be:

a. A money market hedge.b. A forward sale of yen.c. Purchasing yen call options.d. Purchasing yen put options.e. Selling yen put options.

77. Use the following information to calculate the dollar cost of using a money market hedge to hedge 200,000 pounds of payables due in 180 days. Assume the firm has no excess cash. Assume the spot rate of the pound is $2.02, the 180-day forward rate is $2.00, the British interest rate is 5%, and the U.S. interest rate is 4% over the 180- day period.

a. $391,210. b. $396,190. c. $388,210. d. $384,761. e. None of the above.

78. A firm has 1,000,000 euro receivables due in 30 days, and is certain that the euro will depreciate substantially over time. Assuming that the firm is correct, the ideal strategy for the firm is to:

a. Sell euros forward.b. Sell euro currency put options.c. Purchase euros currency call options.d. Purchase euros forward.e. Remain unhedged.

13

79. A MNC will receive SF1,000,000 in 30 days. Use the following information to determine the total dollar amount received (after accounting for the option premium) if the firm purchases and exercises a put option:

Exercise price = $.61 Premium = $.02 Spot rate = $.60Expected spot rate in 30 days = $.56 30-day forward rate = $.62

a. $630,000. b. $610,000 c. $600,000. d. $590,000 e. $580,000. 80. Assume that Parker Company will receive SF200,000 in 360 days. Assume the following interest rates:

U.S. Switzerland360-day borrowing rate 7% 5%360-day deposit rate 6% 4%

Assume the forward rate of the Swiss franc is $.50 and the spot rate of the Swiss franc is $.48. If Parker Company uses a money market hedge, it will receive ________ in 360 days.

a. $101,904 b. $101,923 c. $98,769 d. $96,914 e. $92,307

81. The forward rate of the Swiss franc is $.50. The spot rate of the Swiss franc is $.48. The following interest rates exist:

U.S. Switzerland360-day borrowing rate 7% 5%360-day deposit rate 6% 4%

You need to pay a sum of SF200,000 in 360 days. If you use a money market hedge, the amount of dollars you need in 360 days is:

a. $101,904 b. $101,923 c. $98,769 d. $96,914 e. $92,307

82. Your company will receive C$600,000 in 90 days. The 90-day forward rate for Canadian dollar is $.80. If you use a forward hedge, you will receive:

a. $750,000 today.b. $750,000 in 90 days.c. $480,000 today.d. $480,000 in 90 dayse. None of the above

83. A call option exists on British pounds with an exercise price of $1.60, 90-day expiration date, and a premium of $.03 per unit. A put option also exists on British pounds with an exercise price of $1.60, 90-day expiration date, and a premium of $.02 per unit. You plan to purchase options to cover your future receivables of 700,000 pounds in 90 days. You will exercise the option in 90 days (if at all). You observe the spot rate of the pound to be $1.57, 90 days later. Determine the amount of dollars to be received, after accounting for the option premium.

a. $1,169,000. b. $1,099,000. c. $1,106,000. d. $1,143,100 e. $1,134,000

14

84. Assume that Smith Corporation needs to purchase 200,000 British pounds in 90 days. A call option exists on British pounds with an exercise price of $1.68, 90-day expiration date, and a premium of $.04. A put option also exists on British pounds, with an exercise price of $1.69, 90-day expiration date, and a premium of $.03. Smith Corporation plans to purchase options to cover its future payables. It will exercise the option in 90 days (if at all). The spot rate of the pound turns out to be $1.76 in 90 days. Determine the dollar cost of the payables, including the cost of the option. a. $360,000. b. $338,000 c. $332,000 d. $336,000 e. $344,000

85. Which of the following is an example of economic exposure?a. An increase in the dollar’s value hurts a U.S. firm’s domestic sales because

foreign competitors are able to increase their sales to U.S. customers.b. An increase in the pound’s value increases the U.S. firm’s cost of British

pound payables.c. A decrease in the peso’s value decreases a U.S. firm’s cost of Mexican peso

payables.d. A decrease in the Swiss franc’s value decreases the dollar value of interest

payments on a U.S. firm’s Swiss franc deposit at a Swiss bank.

86. Any restructuring of operations that ________ the difference between a foreign currency’s

inflows and outflows may ________ economic exposure.a. Reduces; increaseb. Increases; reducec. Reduces; reduced. A and Be. None of the above

87. If an exporter sells his/her accounts receivables off to another firm that becomes responsible for obtaining payments from the various importers. This reflects:

a. Accounts receivable financing.b. Consignment.c. Factoring.d. Letter of credit.

88. If a bank acknowledges that it will make payments on behalf of a beer importer after the beer is delivered to the importer. This reflects the use of:

a. Accounts receivable financing.b. Forfeiting.c. Factoring.d. Letter of credit.

89. An importer issues a promissory note to pay for the imported capital goods over a period of five years. The notes are extended to an exporter who sells them at a discount to a bank. This reflects:

a. Accounts receivable financing.b. Forfeiting.c. Factoring.d. Letter of credit

15

90. An exporter is willing to send goods to the importer, on account, without a guaranteed payment by the bank. The bank provides a loan to the exporter that is backed by the value of the exported good. This reflects:

a. Accounts receivable financing.b. Forfeiting.c. Factoring.d. Letter of credit.

90. A firm that sells products through __________ can reduce (used to be able to reduce) corporate taxes on income generated from foreign sales.

a. Foreign Sales Corporation (FSC)b. Private Export Funding Corporation (PEFCO)c. Export-Import Bankd. Foreign Credit Insurance Association (FCIA)

92. A ________ provides a summary of freight charges and conveys title to the merchandise.

a. Letter of creditb. Banker’s acceptancec. Bill of ladingd. Bill of exchange

93. Which of the following payment terms provides the supplier with the greatest degree of protection?

a. Letters of credit.b. Consignment.c. Prepayment.d. Drafts (sight/time).

94. With _____, the exporter ships the goods to the importer while still retaining actual title to the merchandise.

a. A letter of credit arrangementb. An open account arrangementc. A draft arrangementd. A consignment arrangemente. Factoring

95. With _____, a bank purchases an exporter’s receivables at a discount without recourse to the exporter:

a. Accounts receivable financingb. Factoringc. Banker’s acceptanced. A letter of credite. Forfeiting

16

96. A bill of exchange requesting the bank to pay the face amount upon presentation of a document is a:

a. Banker’s acceptance.b. Time draft.c. Letter of credit.d. Sight draft.

97. A bill of exchange requesting a bank to pay the face amount at a future date is a:a. Banker’s acceptance.b. Time draft.c. Letter of credit.d. Sight draft.

98. An exchange of goods between two parties under two distinct contracts expressed inmonetary terms are:

a. Compensation arrangement.b. Counter purchase.c. Factoring.d. Accounts receivable financing.e. Barter

99. Who bears the payment risk in a letter of credit?a. The exporter.b. The importer.c. The issuing bank.d. The confirming banke. Both c and d.

100. A banker’s acceptance is a draft drawn on and accepted by ________.a. A bankb. An importerc. An exporterd. The Federal Reserve Banke. None of the above

101. Derivatives are used in the following ways except: a. To change nature of an investment or a liability b. To lock in an arbitrage profit c. To reflect a view of the future direction of the market d. To hedge risks e. To exploit relative advantages of economic agents in the marketplace f. None of the above

102. Which of the following is not true concerning regulation of derivatives in the U.S.? a. The SEC regulates OTC, Exchanges, and brokers/dealers b. The FED sets margin requirements on stocks and options c. The Commodity Futures Trading Commission regulates futures trading d. The National Association of Securities Dealers regulates OTC markets

17

e. None of the above103. Which of the following is not a feature of the forward market? a. OTC market traded b. Contract sizes taylor-made c. Delivery and settlement at maturity d. Credit risk exists e. Contracts usually reversed prior to maturity

103B. Which of the following is not a feature of the futures market? a. Exchange traded b. Standardized contracts c. Settled daily d. Credit risk exists. e. Contracts usually reversed prior to maturity

104. Unlike the ________; ___________ are traded on organized exchanges and are marked to the market.

a. Long; Short b. Options; Futures c. Spot; Forward d. Forwards; Futures e. Swaps; Forwards f. Spot; Swaps

105. Similar to the ________; __________ are agreements embodying obligation to buy or sell an asset or commodity for future delivery and settlement. a. Forwards; Futures b. Options; Futures c. Swaps; Forwards d. Options; Swaps e. Spot; Forwards

106. The ____hedge is not a technique used to eliminate transaction exposure by multinational firms. a. Index b. Forward c. Futures d. Options e. Money market

107. Assume that IRP holds. The U.S. five-year interest rate is 5% per year while the Mexican five-year rate is 8% per year. If today’s spot rate of the peso is $.20, what is the approximate five-year forecast of the peso’s spot rate using the five year forward rate?

a. $.131b. $.226c. $.262d. $.140

18

e. $.174108. If interest rate parity holds and the forward rate is expected to be an unbiased estimate (predictor) of the future spot rate, then:

a. Covered interest arbitrage is feasibleb. International Fisher Equation holdsc. Purchasing power parity holdsd. Absolute forecast error would be zero

109. Call and put options premiums are affected by the level of existing spot price relative to the strike price. A ____ spot price relative to the strike price results in relatively ____ premium for a call option but a relatively ____ premium for a put option.

a. High; High; Low b. High; Low; Highc. Low; High; Highd. Low; Low; Lowe. High; High; High

109B. Call and put options premiums are affected by the level of existing spot price relative to the strike price. A ____ spot price relative to the strike price results in relatively ____ premium for a call option but a relatively ____ premium for a put option.

a. High; Low; Highb. Low; High; Highc. Low; Low; High d. Low; Low; Lowe. High; High; High

110. A U.S. corporation has purchased currency put options to hedge a 100,000 Canadian dollar (C$) receivable. The premium is $.02 per unit and the exercise price of the option is $.94. If the spot rate at the time of maturity is $.99, what is the net amount received by the corporation if it acts rationally?

a. $92,000.b. $97,000.c. $96,000.d. $94,000.

111. A U.S. corporation has purchased currency call options to hedge a 70,000 pound payable. The premium is $.02 and the exercise price of the option is $.50. If the spot rate at the time of maturity is $.65, what is the total amount paid by the corporation if it acts rationally?

a. $33,600b. $46,900c. $44,100d. $36,400

19

112. If you have bought the right to sell, you are a:

a. Call writer.b. Put buyer.c. Futures buyer.d. Put writer.e. Call owner

113. Your company expects to pay 5,000,000 Japanese yen 90 days from now. You decide to hedge your position by buying Japanese yen forward. The current spot rate of the yen is $.0089, while the forward rate is $.0095. You expect the spot rate in 90 days to be $.0090. How many dollars will you need to meet your obligation 90 days from now?

a. $44,500.b. $45,000c. $526,315,790.d. $47,500

114. A speculator sells a put option on Canadian dollars for a premium of $.03 per unit. with an exercise price of $.98. The size of the option contact is C$50,000 and will not be exercised until expiration if at all. If the spot rate for Canadian dollar is $.90 on at expiration, the net profit for the speculator is: Profit to speculator = 50,000[.03 +.90 - .98] = 50,000[-.05] = -$2500

a. $2500b. -$2500 c. $49,989d. -$49,989

115. The purchase of a currency put option would be appropriate for a U.S company under which of the following?

a. Company expects to a foreign bond in six monthsb. Company expects to buy foreign current to finance foreign subsidiariesc. Company expects to redeem a Euro bond in six monthsd. Company expects to collect a foreign currency accounts receivable in six

monthse. None of the above

116. Any type of contractual arrangement calling for the delivery (and settlement) of a good or service at a future date at a price agreed upon at the initiation is a /an ________ contract.

a. Options b. Swaps c. Futures d. Forward e. Auction

20

117. If a contract contains a promise that a specified amount of foreign currency will be delivered on a specified date in the future, the contract is a __________

a. Forward contract b. Futures contract c. options contract d. Swap contract

118. If a contract contains a promise that standardized units of foreign currency will be delivered on a specified date in the future, the contract is a __________

a. Forward contract b. Futures contract c. Options contract d. Swap contract

119. If the interest rate on a deposit in the U.K. pound is 6% per year, and the pound is expected to depreciate against the U.S. dollar by 2% , what does the interest rate parity theory imply about the interest rate on a deposit in U.S. dollar?

a. 6% b. 4% c. 8% d. 3% e. 12%

120. Assume that the bid rate for Australian dollar $.60 while the ask rate is $.61 at Bank A. Also assume that the bid rate for the Australian dollar is $.62 while the ask rate is $.625 at Bank B. What would be your profit if have $100,000 and you execute locational arbitrage ?

a. $1000.30 b. $1206.30 c. $1444.10 d. $1639.30 e. $1821.90

21

Answer Key To Sample Questions Set II

1 D 46 D 91 A2 B 47 D 92 C3 A 48 D 93 C4 D 49 A 94 D5 B 50 A 95 B6 C 51 B 96 D7 B 52 D 97 B8 A 53 A 98 B9 D 54 C 99 E

10 A 55 C 100 A11 D 56 B 101 F12 C 57 E 102 E13 A 58 C 103 E14 C 59 A 104 D15 D 60 B 105 A16 E 61 C 106 A17 B 62 A 107 E18 E 63 C 108 B19 C 64 A 109 A20 E 65 D 110 B21 D 66 A 111 D22 A 67 C 112 B23 B 68 E 113 D24 B 69 E 114 B25 D 70 E 115 D26 D 71 B

27 C 72 C 116. D28 D 73 C 117. A29 B 74 D 118. B30 C 75 D 119. B31 B 76 D 120. D32 A 77 E33 B 78 A34 B 79 D35 A 80 D36 A 81 C37 A 82 D38 A 83 C39 E 84 E40 D 85 A41 B 86 C42 C 87 C43 A 88 D44 E 89 B45 A 90 A

PART B:

22

1. ABC Inc. and XYZ Inc. face the following borrowing costs in the fixed and floating rate markets (L = LIBOR ; T = Treasury) Fixed-Rate Market Floating-Rate Market

ABC T + 0.75% L – 0.25% XYZ T + 1.50% L + 0.10%

Each firm desires the rate other than for which it has comparative advantage.A dealer stands ready to enter into a swap as either a fixed rate payer or floating rate receiver (or vice versa). The dealer will pay T + 1.22% against L or receive T + 1.30% against L. Assume that each firm borrows in the market in which it has comparative advantage and enters into a swap agreement with the other, analyze the potential gains swapping under the following guidelines:a) At which market does each firm have:

i. absolute advantage? ____________________ii. comparative advantage? _________________

b) How many Basis points represent the potential gains from swapping for all parties? ____________

c) Obtain the effective cost of funding for XYZ ______and ABC_______.d) What does the swap dealer earn? ______

2. Consider counterparties AA and BB. AA desires n-year floating rate on US dollars while BB desires fixed rate on pound sterling. The following borrowing costs are available to the parties:

Floating rate ($) Fixed rate (£) AA 7.75% 12.75% BB 8.10% 13.55%

A swap dealer proposes BP-USD currency swap under which the dealer stands to pay a fixed rate of 13.20% (on BP) against a floating rate of 8% (on USD) or receive a 13.30% fixed against floating rate of 8%.Obtain the savings and effective costs to each party and the dealers pay-receive spread from swapping.

3. The ABC and XYZ corp. seek funding at the lowest possible cost. They face the following structure in the market:

Fixed Floating ABC 10% P + 0.5% XYZ 13% P + 1.0%

Suppose a dealer stands ready to pay a fixed rate of 11.0% Vs Prime (P) or receive 11.25% vs P, what will be the effective (net) cost of funding for ABC and XYZ respectively, if a swap is executed? How will the resulting savings be distributed among the parties?

4. Show whether or not triangular arbitrage is possible in each. Describe the flow and compute the percentage profit possible in each case.

(a) A1: C$/$ = 1.2678. A2: NK/$ = 5.4495. A3: NK/C$ = 4.2984(b) B1: SF/$ = 1.6117. B2: SF/£ = 2.3958. B3: $/£ = 1.5011

23

5. On Dec. 6, a speculator buys a BP call options contract with a strike price of $1.35. The current spot rate ($/BP) is $1.30. The premium is 1.2 cents per BP. Just before expiration he observes that spot BP is $1.42. Find his profit (loss) if he exercises his option. The size of one British pound options contract is £31,250.

6 U.S. speculator sold a call option on Swiss Francs for $.01 per unit. The strike price was $.36, and the spot rate just before expiration was $.42. Assume that there are 62,500 units in a Swiss Franc option contract. Obtain the profit (loss) to the grantor of the call option.

7. Show whether or not covered interest arbitrage is worthwhile in each case and compute the arbitrage profit if any:

(a) Spot Y/$ = 135.606-month forward Y/$ = 138.386-month Euro $ interest rate = 10.6% per year6-month EuroY interest rate = 8.4% per year

(b) Spot SF/$ = 1.8280 90-day forward SF/$ = 1.8120 90-day $ interest rate = 9% per year 90-day SF interest rate = 5% per year

8. If inflation in Sweden is projected at 5% annually for the next 5 years and 12% in Italy. If Lira/Krona is 205.56, calculate the PPP value of the spot rate 5 years from now?

9. Assume that the spot exchange rate (SF/$) is currently 1.8960. U.S. treasury securities with 3 years to maturity are currently yielding 6.68% per year, while the interest rate on comparable Swiss securities is 7.44%. Assuming annual compounding, what is the expected spot exchange rate SF/$ in 3 years if IFE holds exactly?

10. Assume that the annual U.S. interest rate is currently 8% and Canadian annual interest rate is currently 10%. The Canadian dollar one-year forward rate currently exhibits a discount of 2% (try same problem if C$ exhibits a premium of 2%). a. Show whether or not interest rate parity exists b. Can a U.S. firm benefit from CIA in Canada? (why / why not?) c. Can a Canadian company benefit from CIA in U.S.? (why / why not?)

11. Assume that a Big Mac costs $3.06 in the U.S. and £1.85 in the U.K. If the actual exchange rate is $/£ = 1.8519 then according to the absolute PPP, show whether the British Pound is overvalued or undervalued relative to the dollar and whether it costs more or less in dollars to buy Big Mac in the U.K.

12. Assume that a Big Mac costs $3.25 in the U.S. and 2505 Won in Korea. If the actual exchange rate is W/$ = 820 then according to the absolute PPP, show whether or not the Won is undervalued or over-valued relative to the dollar and indicate whether it costs more or less in dollars to purchase Big Mac in Korea.

24

13. The current spot rate ($/Peso) is .0704. Assume that relative PPP holds, and U.S. inflation is expected to be 3% per year for the next two years while Mexican inflation is expected to be 9% per year over the same period. XYZ Corp of USA has a 20 million peso payable at the end of two years. Calculate the expected amount of dollars needed to make the payment at the end of two years.

14. The current spot rate ($/€) is 1.3995. Assume that relative PPP holds between U.S. and Germany, and U.S. inflation is expected to be 3% per year for the next five years while German inflation is expected to be 5% per year over the same period. XYZ Corp of USA has a 10 million Euro receivable at the end of five years. Calculate the expected amount of dollars to be received by XYZ at the end of five years.

25