Film Financing in Bollywood

25

Film Financing in Bollywood Scripting a New Saga, Screening an Extravaganza Bollywood is now witnessing a sea change, into its every aspect of functioning, be it film making or Film Financing. The article explains the concept of film financing in the context of Bollywood, and related structures, patterns, formats of film financing. It also offers brief comparison with Hollywood’s film financing to further understand a variety of issues lying unresolved right from the beginning. The penultimate section takes into account the future prospects by detailing the level of professionalism, corporatisation and investment coming from various sources, before drawing conclusion. Gaurav R Wankhade 14 © The Icfai University Press. All rights reserved. H ow accurately someone has depicted the place and importance of ‘Money’ in our life, (see box in next page) showing its different facets and the greediness of all of us for it. Whatever we may say or feel, the truth is undisputable and i.e., the world cannot move without money (gravity is just another thing). Money is that magnet around which today every thing revolves. Our Bollywood (the enchanting glamour world located in the Mumbai) has always showcased different stories related to Money.

-

Upload

iamgaurava -

Category

Documents

-

view

59 -

download

7

description

Article

Transcript of Film Financing in Bollywood

Film Financing in BollywoodScripting a New Saga, Screening an Extravaganza

Bollywood is now witnessing a sea change, into its every aspectof functioning, be it film making or Film Financing. The articleexplains the concept of film financing in the context ofBollywood, and related structures, patterns, formats of filmfinancing. It also offers brief comparison with Hollywood’sfilm financing to further understand a variety of issues lyingunresolved right from the beginning. The penultimate sectiontakes into account the future prospects by detailing the level ofprofessionalism, corporatisation and investment coming fromvarious sources, before drawing conclusion.

Gaurav R Wankhade

14

© The Icfai University Press. All rights reserved.

How accurately someone has depicted the place and importance of ‘Money’ inour life, (see box in next page) showing its different facets and the greediness

of all of us for it. Whatever we may say or feel, the truth is undisputable and i.e., theworld cannot move without money (gravity is just another thing). Money is that magnetaround which today every thing revolves. Our Bollywood (the enchanting glamourworld located in the Mumbai) has always showcased different stories related to Money.

148 BUSINESS OF BOLLYWOOD: THE CHANGING DIMENSIONS

Bollywood dreams, attracts, ponders, and delivers money (in addition to popularity).They are not only the dream merchants but the dream sellers and money makers.Have you not applauded the Gabbar Singh of ‘Sholay’, Vijay Dinannath Chauhan of‘Agnipath’, Prem (Salman), Raj (Shahrukh) of their most of the movies, Dhak Dhakgirl Madhuri or Mahatma Gandhi and Munnabhai’s Gandhigiri in ‘Lagey RahoMunnabhai’. But hey! Bollywood too has, greed and requires money since it is auniversal law that ‘Money Creates Money’. Obviously to craft such spectacular,entertaining and larger than life characters, stories and make them real on reel(onscreen), money is essential. So the first and foremost question that comes to mindis from where does Bollywood generate required finance? The amount of moneyBollywood requires for a grand project runs into some crores. And it delivers manynumber of such extravagant projects, simultaneously. So there must be some method,technique or set of methodologies through which it acquires the required budgetedamount of finance. Since it is now operating as an industry, it has to function as anyother industry. Further success and failures are integral parts of business. But most ofthe time failures overshadow success in the case of Bollywood. So from where doesthe industry get its momentum in such a situation? And what is the exact nature offilm financing in Bollywood?

“Na biwi na bachcha, na baap bada na maiyya, the whole thing is that kebhaiyya Sabse Bada Rupaiya”

(Movie: Sabse Bada Rupaiya [1976], Singer: Mehmood)

Source: http://en.wikipedia.org/wiki/Image:Sabse_Bada_Rupaiya1976.jpg

149Film Financing in Bollywood: Scripting a New Saga, Screening an Extravaganza

This article is an attempt to find out answers to the above stated questions and set ofmany other relative queries, in addition to the gamut of issues, problems arising in thistypical filmy environment characterised by sharp up and downs. Let us first understandthe basics of Hindi Film Industry. The industry is broadly classified into four segments –software (films, music and programs), hardware (studios and other infrastructure servicesthat support the creation of entertainment software) and services (distribution, exhibition,film procurement and banking services) and the front-end media segment (film magazines,video cassettes and promotional tools)1. This classification is incomplete without thehuman factor involved into it, since it is rare to find a Commercial and mainstreamBollywood movie without Lead Actor (Hero: Male Protagonist), Actress (Heroine: FemaleProtagonists) and Villain (Antagonist). They play onscreen. There are other workingsbehind the veil (screen) and the most important ones of them are Producer, Writer,Director, Music Director, Cinematographer and so on.

Film Financing

Film Financing in Bollywood is very different than what has been practiced in otherFilm Industries all over the world. Though the process of movie-making is similar ingeneral, the difference lies in its overall nature which is highly risk oriented,disorganised, disintegrated, and highly unprofessional. There is no particularmethodology or process format regarding film-making, neither any obligation onanybody except the producer to complete the project in time. Though probable timeperiod for completion of a project is pre-planned in some cases, most of the time itoverruns one and a half time or simply double the pre-planned time. Many of thetimes Star-actors non available of date, or lack of cast and crew management are thereasons or unavailability of creative material (Script, Screenplay etc.) or unavailabilityof funds are put forward as the reasons for delay. Because of these reasons the wholeprocess gets too much delayed as compared to the previously planned schedule. Averagetime-frame for the completion of a big-budget film is 15-18 months in Bollywood2,but very less number of film projects get completed in the given time. This againleads to diluting image (whatever the brand image bollywood has awarded earlier).This is the first and foremost reason why Bollywood lacks in competing onInternational level, particularly when compared to Hollywood.

Before going further, it is necessary to understand the different aspects of filmmaking with respect to a typical Bollywood Film. The necessity arises from the fact

150 BUSINESS OF BOLLYWOOD: THE CHANGING DIMENSIONS

that whatever budget allocated to an entire film gets distributed amongst thesub-processes according to their preference and importance (perceived) as there is nowritten rules or norms. So in order to understand the structure of film financing it isessential to have brief about film-making process. The making of a Hindi movie canbe broadly divided into the following Parts:

• Development

• Pre-production

• Production

• Post-Production

• Distribution and Export

• Marketing and Promotion.

In the Development stage an idea is nurtured into a concept and the concept isnourished further to create a storyline, which then will be transformed into a boundscript. A script is a collection of characters, situations and events tightly connectedforming a chronology of screenplay shots. A considerable amount of money, timeand skills are devoted to this phase through proper market analysis and research totest the overall feasibility of the project. This is the most crucial phase of film craftingaccording to world standards, but mostly neglected in the bollywood. The stage afterthis is of Pre-production, during which cast, crew, locations and shooting scheduleswill be decided. During this phase the producers get an overall idea of the requiredbudget for the film. Also to complete the films in time to save the extra cost, one ortwo provisional screenplays and replacements for general staff is also being put inplace. The next step is that of Production, which is the actual making stage for amovie. The stage following production is Post-production stage during which theentire shooting material (Film) will be processed, edited and prepared after whichthe film is ready to release in the form of print. But before releasing a film the finalproduct has to pass through further two stages. The first of this is Distribution ofprints to the screening theatres. Though the Marketing and Promotion stage comesafter distribution, producer can start marketing his project from the time the printsget ready, as its very, very important to promote the film to attract the pre-decidedtarget audience.

151Film Financing in Bollywood: Scripting a New Saga, Screening an Extravaganza

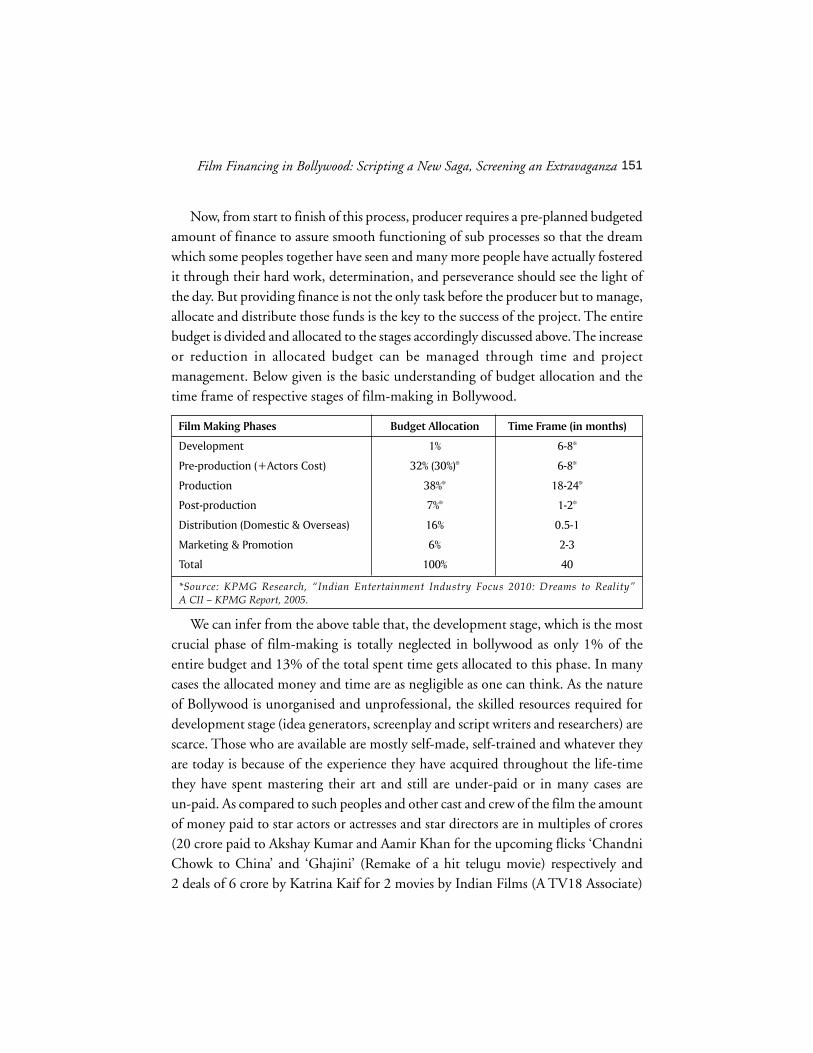

Now, from start to finish of this process, producer requires a pre-planned budgetedamount of finance to assure smooth functioning of sub processes so that the dreamwhich some peoples together have seen and many more people have actually fosteredit through their hard work, determination, and perseverance should see the light ofthe day. But providing finance is not the only task before the producer but to manage,allocate and distribute those funds is the key to the success of the project. The entirebudget is divided and allocated to the stages accordingly discussed above. The increaseor reduction in allocated budget can be managed through time and projectmanagement. Below given is the basic understanding of budget allocation and thetime frame of respective stages of film-making in Bollywood.

Film Making Phases Budget Allocation Time Frame (in months)

Development 1% 6-8*

Pre-production (+Actors Cost) 32% (30%)* 6-8*

Production 38%* 18-24*

Post-production 7%* 1-2*

Distribution (Domestic & Overseas) 16% 0.5-1

Marketing & Promotion 6% 2-3

Total 100% 40

*Source: KPMG Research, “Indian Entertainment Industry Focus 2010: Dreams to Reality”A CII – KPMG Report, 2005.

We can infer from the above table that, the development stage, which is the mostcrucial phase of film-making is totally neglected in bollywood as only 1% of theentire budget and 13% of the total spent time gets allocated to this phase. In manycases the allocated money and time are as negligible as one can think. As the natureof Bollywood is unorganised and unprofessional, the skilled resources required fordevelopment stage (idea generators, screenplay and script writers and researchers) arescarce. Those who are available are mostly self-made, self-trained and whatever theyare today is because of the experience they have acquired throughout the life-timethey have spent mastering their art and still are under-paid or in many cases areun-paid. As compared to such peoples and other cast and crew of the film the amountof money paid to star actors or actresses and star directors are in multiples of crores(20 crore paid to Akshay Kumar and Aamir Khan for the upcoming flicks ‘ChandniChowk to China’ and ‘Ghajini’ (Remake of a hit telugu movie) respectively and2 deals of 6 crore by Katrina Kaif for 2 movies by Indian Films (A TV18 Associate)

152 BUSINESS OF BOLLYWOOD: THE CHANGING DIMENSIONS

each), which eventually took out bulk amount out of the entire budget. Again theexpenses on post-production are very low forcing one to think of the quality oftechnique and technology that got involved into post-production work. Comparingit to the production share, which is nearly around 40% which in turn is very highcompared to the international standards, what we come to know is the level oftechnology involved. Since the post-production is a highly technology-driven process,but doesn’t get its due credit investment share and thus low quality of final output.The distribution part which gets 16% of the film budget is solely managed by adistributor who pays lump sums in advance to the producer for the territory-wisedistribution right of the respective film project. The distributor also have to manageits marketing and promotion which account for nearly 6-8% of the cost incurred.Thus in effect distributor shells out around 22% i.e., 1/4th of the cost incurred in theproject. And if one project fails, he has no money left to go for another one.

Sources of Funding

From the above discussion it is more or less clear that the whole and sole in acquiringfinance and managing, allocating and distributing the acquired funds in additionto the entire project management load, is the producer. A producer is the personwho carries all the responsibilities from start to finish during the film-makingprocess and looks after the entire functioning. The simple question that may ariseat this time is from where the producer arranges the finances required for a typicalbig-budget mainstream Hindi movie, which ranges between $5 million to $10million i.e. on an average INR 20-25 crore. Let us take a look at the availablefunding sources to the producer.

There are multiple sources of funding which might be available on paper to filmproducers in bollywood, but how many are really there, can be a matter of debate.The share of each source varies on case to case basis. But the most prominent sourcesof financing in general are producer (Self ), private financer (Charging different interestrate to different borrowers), promoters equity, music & home entertainment rightsand distributors (Is available presently in limited quantum, only for big banner filmswith reputed producers, directors and star cast [Sunil Kheterpal, 2004]). After beingawarded the status of an Industry by the Government of India, the options availableto producers increased tenfold. The options include banks and institutional financing,venture capital funding, IPOs, insurance companies, and international studios.

153Film Financing in Bollywood: Scripting a New Saga, Screening an Extravaganza

The banks which now provide Hindi Film Project Finance include IDBI, EXIMBank and Bank of Baroda etc. The Industrial Development Bank of India (IDBI),which started off by investing Rs.70 million in the industry, is seen as the leader inthis sector and has decided to double its investments to the tune of Rs.2 billion3.This also prompted large non-banking institutions and corporate entities in the formof private equity funds to make a foray into Hindi Film Financing. Some of the bigstudios now operating in this sector are Yash Raj Films (YRF), Mukta Arts (SubhashGhai Productions), Dharma Production (Karan Johar), UTV Motion Pictures (RonnieScrewvala), Adlabs (Dhirubhai Ambani), Eros International (Kishor Lulla), SaharaOne Entertainment etc. Then there are companies that have gone public, 12 since2000, which have raised another Rs.1,000-odd crores through their IPOs4. Betweenthem, Eros, United Television (UTV) and Indian Films, an affiliate of TV18, haveraised $45 million, $70 million and $110 million, respectively, from the AlternativeInvestment Market (AIM) in London.5 A shift from Unorganised to Organisedfinancing has definitely served various benefits, decreased average production costper film being one of the most prominent of these benefits. Other benefits includemore lucid financing patterns, enhanced transparency in the financial transactions

Commercial Big-Budget Mainstream Hindi Film Project

Producer

Private Financers

Distributors (Domestic and Overseas)

IPO’s (Public Fi )

Venture Capital (Corporate level/ Project level / State L l

Promoters Equity

Studios (Domestic and International)

Banks and Institutional F di

Music and Home Entertainments Rights (in advance)

Insurance Providers

Producer (Self)

Branding & Merchandising

Diagram I: Available Sources of Funding for a Film Producer

Commercial Big-BudgetMainstream

Hindi Film Project

Private Financers

Music and HomeEntertainments

Rights (in advance)

Studios(Domestic andInternational)/

Large Producers

Venture Capital(Corporate level/

Project level/State)

Promoters EquityPromoters Equity

Banks andInstitutional

Branding andMerchandisingIPOs

(Public Finance)InsuranceProviders

Distributors(Domestic and Overseas)

Producer(Self)

Producer

154 BUSINESS OF BOLLYWOOD: THE CHANGING DIMENSIONS

and accounting (with corporate’s insisting on electronic ticketing in even territoriessuch as north Bihar now), greater quality of technology (Special Effects for ‘LoveStory 2050 are being executed by 4 international firms, of which two special effects’houses—Weta Workshop (New Zealand) and John Cox (Brisbane, Australia)—havealready won an Academy Award for their work on international projects), reducedtime-frames because of the corporate interventions etc.

Trends in Film Financing

Financing films in India is still a risky preposition. The whole concept has undergonea dramatic change from the beginning in 1913 with a silent mythological film named“Raja Harishchandra” made by Dadasaheb Phalke (Kohinoor Imperial Production)with maybe a miniscule budget. Nowadays, Hindi films are made on a much higherbudget ranging from $0.1 million and scaling up to $15 million. An average Bollywoodfilm is budgeted at $1.3 million. “Monsoon Wedding” (2002) by Meera Nair wasmade with a budget of $0.16 million6 and “Jodha Akbar” (2008) by AshutoshGowarikar was made with a budget of $15 million7. More ambitious projects arereportedly planned, the most expensive of which is an epic film Mahabharata, byRavi Chopra, estimated to cost upto $30 million8. Almost after ninety years, theMainstream Hindi film industry irksomely termed as ‘Bollywood’ was awarded itsdue status i.e., of an industry in the new millennia of 21st century i.e., in the year

Source: http://arts.guardian.co.uk/image/0,,1857620,00.html

A Scene from ‘Raja Harishchandra’

155Film Financing in Bollywood: Scripting a New Saga, Screening an Extravaganza

2003. This was a late act from the Government, which had a maligned and murkyimage of this art-form. Obviously, it is only during the last eight years that organisedfinancing from banks, financial institutions, corporates and venture funds becamepossible9. Till 2000, films were mostly financed through private sources, sincecommercial lending agencies considered the industry to be a risky and low-prioritysector10. The two major sources for finance were11:

• Distributors and music companies, who would pay advances to establishedfilm-makers and films with reputed star casts to acquire the theatrical/music rights.

• Financiers (High-net worth individuals).

The trends in Hindi film financing can be well understood if we divide history.By 1920, film making had taken the shape of an industry12, but still in its infancyand under the direct control of colonial rule (The British Raj) faced severe issues infinancing. Mostly dependent on external support and under colonialism financingfilms remained a problem – state funding, except for propaganda films, was non-existent and the substantial black money became available only after the second worldwari. Then came the period of large studios (many of which were owned by largeFilm Producing Company) pursuing Hollywood’s format, dominating the market ofthose times. This trend lasted for a decade until the 1960s. These studios used toemploy highly skilled artistes and technicians (writers, directors, and music directors)on a salary basis for their projects. Some of them were also contracted on long-termbasis i.e., for 4 to 5 years allowing production houses to work on various projectssimultaneously. However, most performers went the freelance way, resulting in thestar system and huge escalations in film production costs13. Financing deals in theindustry also started becoming murkier since then14. The drift from legal to illegal(illicit) business activities within the Hindi film industry may have started in the late60s. Until the 1960s, film producers would get loans from film distributors against aminimum guarantee: (this meant that the distributors had to ensure that the filmwas screened in cinemas for a fixed minimum period)15. If this minimum guaranteewas fulfilled, the producers had no further liability and profit or loss, whatever thecase would be the destiny of the distributors16.

i Article, “Indian Cinema and the Bourgeois Nation State”, Anirudh Deshpande, Economic & Political Weekly, Dec15, 2007, page 95-103.

156 BUSINESS OF BOLLYWOOD: THE CHANGING DIMENSIONS

The cost of film production has risen tremendously since the financing trendwhich up to mid 70s was totally relying on finance from distributor collapsed, givingaway a new pattern i.e., the so called ‘Star System’; In this system actors and actressesceased to have long-term contractual obligations towards any studio or film productionfirm (such as the now defunct Bombay Talkies, New Theatres and Prabhat Studios)17:Since they began to function independently, and because of their excellent past trackrecord and the popularity they enjoyed among the Indian audience, these star actors/actresses started asking for more and more money from the producers. Thissubsequently resulted in shooting up of the overall film budgets to some crores. Butagain the major contributor to the entire budget remains the distributor i.e., raisinghalf of the production budget has become distributor’s responsibility; and remainingamount is the task of producer. Now though distributor has to arrange the said shareon his own with other option availability being negligible, the case was different withthe producer as there were many options available to him for raising capital. The‘other’ sources thus available to the producer were18:

• Conventional moneylenders (who lend at an interest rate of 36-40 percentannually);

• Non-conventional but corporate resources,

• Promissory note system (locally called ‘hundi’ system): this was the most widelyprevalent source, and

• Underworld money: about 5 percent of the movies were suspected to befinanced by these sources in the initial period of 90s.

Thus what could be a point of notice is that film financing in those days wascompletely unorganised and disintegrated, in most of the cases unethical. The industrystructure also was totally unregulated lacking any type of vertical or horizontalintegration in the value chain. The value chain in respect to the bollywood can bedefined as a link of film making stages (development, pre-post production anddistribution, marketing and exhibition) through which a product is constantlydeveloped and furnished, until it reaches to the ultimate customer (Audiences). Insuch disorganised, unhealthy environment with overall negligence from the respectiveGovernment, it was but obvious that there could be no presence of transparency. Itleads to the higher and higher risk involvement. There are many cases where producersor distributors at that time have raised collateral by practically selling out all of their

157Film Financing in Bollywood: Scripting a New Saga, Screening an Extravaganza

property and earnings for a film project and many have gone bankrupt. (India’s mostcelebrated film-maker, the late Satyajit Ray, is known to have pawned his wife’sjewellery to part-finance his first film19).Over the years, the studio system andsubsequent star system gradually gave way to a new system i.e., independenproducers20. Earlier, as finances were not regulated, some funding used to come fromillegitimate sources, such as the Mumbai underworld. Also before the reform, thefilmmakers were hugely dependent on diamond merchants and underworld forfinances21. In the 90s, criminal sources financed an estimated 40% of film production(Kripalani and Grover, 2002). Slowly this trend has minimised but has not completelyvanished. Today, tax evasion practice is still widespread among film producers andstar actors and it is even estimated that below 10% of film finance is illegal (Kripalaniand Grover, 2002). May be it will diminish with the time as the Government hastaken prominent actions in this regards.

Changing Norms in Financing of Hindi Movies

Change is concurrent to the time. Everything keeps changing so also the Bollywoodand its film financing pattern. It has thrown away its old stuff in many ways andtrying to shade apart its tag of unprofessionalism. Financing patterns are slowlytransforming into Organised Financing System thus giving a fresh breeze of legitimateand corporatized functioning to the industry. However, the basic nature of businessstill looks riskier. Corporate and institutionalized financing option still comes withhigh interest rates tag, limiting the available options. Limited or non-recoursefinancing, akin to project financing, is not common22. A past trend in last 2-3 yearshas shown that business of Bollywood is favourable if managed professionally. If thesaid professionalism (completion of bonds, well-structured agreements, transactionaltransparency and a complete integration in value chain) is accepted by producersand absorbed correctly into the system, more sophisticated options like bank loans,non-banking institutional funds, insurance, well-defined deals, securitisation, creditenhancing bonds etc., will be definitely available. The production houses’ mutualunderstanding with corporate finance providers will determine the actual level of theinvestments and finances. With cheaper sources of financing becoming availablefrom legitimate sources and the industry becoming more disciplined, the quantumof unorganised financing is expected to shrink23.

In such a healthy and competitive scenario the unfeasible projects will be thrownaway out of the race, leading to an increase in production of average number of

158 BUSINESS OF BOLLYWOOD: THE CHANGING DIMENSIONS

mainstream films around 100 over the next few years, and increasing the average cost

of production per film. This will comprise an increased spend on script development

stage (research and analysis), pre-production, incubation of advanced technology,

enhanced recovery procedures and better marketing and promotion and slower spent

during actual production stage. It will also change the ratio of organised to unorganised

financing in a positive way increasing the percentage of film produced through

organised resource financing in the industry. Through a combination of private equity,

IPOs and media-related corporate investments, a new breed of film companies are

emerging as the future leaders of a transformed Indian content industry24. The major

players are from old generation as well as new generation too, most of them functioning

from ages in different aspect(s) of the film making profession. Having started their

business with a typical traditional approach, but sensing the changing scenario of

more technology driven mechanisms, increasing competitive market setups have

changed their style to more professional one, through strategic investment methods

over the past few years. In doing so, they have been leveraging new growth and

helped lead the industry towards its much delayed (and much debated)

“corporatisation” stage25.

The changing pattern of film financing

Source: KPMG Research.

Corporatised films Other films Average cost of a mainstream film

Num

ber

of fi

lms

INR m

illion

159Film Financing in Bollywood: Scripting a New Saga, Screening an Extravaganza

Currently, if we take a close look at the market size of bollywood around 30percent of the films generate 90 percent of the industry revenues. It is because,around 50-60 percent films out of the 150-160 major (typical commercial andbig-budget) films produced annually in the bollywood are overall unfeasible laggardswho otherwise would be completely unacceptable in a highly professional set-up.To know the exact situation of film financing profile we have to go down deeperinto categorization of films.

Based on a research study conducted in 2005 by CII-KPMG, here is theclassification of films from 2003 and 2004 into the following four categories basedon cost, production value, artists and technicians, and content.

* Gross collections include domestic and overseas theatrical receipts, domestic and overseassatellite and video rights, music rights and in-film advertising and merchandising revenues.

Source: KPMG Research (“Indian Entertainment Industry Focus 2010: Dreams to Reality” A CII-KPMGReport, 2005)

Category AA films are the ‘big banner’ films having high level of technologicalintegration. Up till now, the standard of technology involved was below average withsome exceptions like “Dhoom 2”, “Krrish” etc., but now the situation is graduating.The most prominent feature of such films is the excellent past record and substantialexperience of the respective production company or producer in producing blockbusterfilms. The budget for these types of films generally ranges between INR 150 to 300million. Category A films have total amount of budget, which is assumed to be rangingbetween INR 80-150 million. The budget is inclusive of variables like type of shoot,locations, number of shifts, the type of agreements with artists, post-production costs,capitalised interest, and so on26. Third category i.e., Type B films are produced byrelatively unknown and financially weaker producers. In many cases, the completionof the film gets delayed due to the lack of last-mile finance. Without their own sourceof finance, the producers of such films usually tap the market for funds. Often, thesefilms are not completed due to lack of funds. Their budgets are assumed to range fromINR 30-80 million. Category C films comprise of a heterogeneous mix of low budget,

Categories Lowest Cost (INR) Highest Cost (INR)

AA 150,000,000 300,000,000

A 80,000,000 150,000,000

B 30,000,000 80,000,000

C 10,000,000 30,000,000

160 BUSINESS OF BOLLYWOOD: THE CHANGING DIMENSIONS

high quality content films at one end with a high profit potential, to still-born projectscharacterised by a lack of quality, content, and good artists fashioned on run-of-the-mill subjects, espousing mediocre music and virtually no market. Their costs are assumedto be between INR 10-30 million.

All things changed except the way trade is conducted in Bollywood. Here, aproducer starts a film, distributors from various territories like Mumbai, Overseasetc., join in and promises to pay a certain amount during the making of the film anda certain amount at the time of the delivery of the released prints27 . The distributorsare joined in by financers (institutional and non-institutional), music companies,and home entertainment providers (to acquire satellite and TV, home video rights).These distributors then strike deals with exhibitors, who screen films, and receivecertain sum of amount towards a deposit/advance, which they then pay to the filmmakers28, taking out their cut, if possible. This is the way Bollywood functions.

Comparison with Hollywood (International) Film Financing

From its beginning Bollywood has a strong affection towards it western counterpartHollywood. The affection was inherent as films entered India in the pre-Independenceera. Many films in Bollywood are either exact replica (for e.g., “Kaante: ReservoirDogs”, “My Best Friend’s Wedding: Mere Yaar ki Shaadi Hai” etc.) or inspired (Fore.g., “Raaz”, “Zinda” and so on) from Hollywood. But the one system they haven’tcopied is their professionalism in doing business in its true sense. In fact for manydecades it was another dirty business. The lack of professionalism can be found infilm financing also. What dominates in Hollywood is the Studio System; [an integratedentity that oversees all aspects of the value chain (from production to distributionand at times, even exhibition)]. Due to this film making style, the project in theHollywood has been tested before actually starting the project for its viability totarget it appropriately since there are less numbers of options available within thevalue network to transfer whatever the risk arising at each stage. On the other hand,the scenario is different in Bollywood and the overall structure is such that there isgeneral practice to avoid or deny and transfer the risk on to the subsequent levelsfunctioning in the network. Also since there is neither type of integration present inits format, much higher portions of risk rests with small number of third parties.This risk increase tenfold with misallocation coupled with mismanagement of themoney spent on the film-making. The lack of allocation of time and budget towards

161Film Financing in Bollywood: Scripting a New Saga, Screening an Extravaganza

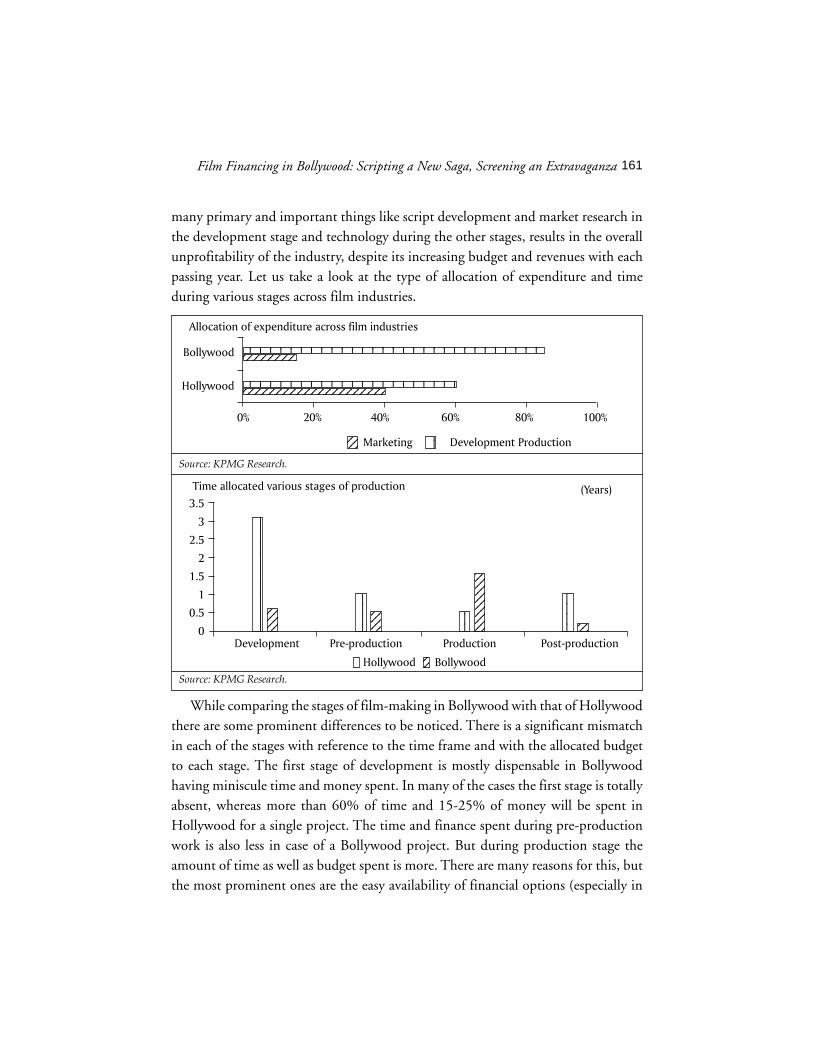

many primary and important things like script development and market research inthe development stage and technology during the other stages, results in the overallunprofitability of the industry, despite its increasing budget and revenues with eachpassing year. Let us take a look at the type of allocation of expenditure and timeduring various stages across film industries.

While comparing the stages of film-making in Bollywood with that of Hollywoodthere are some prominent differences to be noticed. There is a significant mismatchin each of the stages with reference to the time frame and with the allocated budgetto each stage. The first stage of development is mostly dispensable in Bollywoodhaving miniscule time and money spent. In many of the cases the first stage is totallyabsent, whereas more than 60% of time and 15-25% of money will be spent inHollywood for a single project. The time and finance spent during pre-productionwork is also less in case of a Bollywood project. But during production stage theamount of time as well as budget spent is more. There are many reasons for this, butthe most prominent ones are the easy availability of financial options (especially in

Allocation of expenditure across film industries

Bollywood

Hollywood

12345678901234567890123456789011234567890123456789012345678901123456789123456789

1234567890123456789012123456789012345678901123456789012345678901

0% 20% 40% 60% 80% 100%

Marketing Development Production1212

1212

Source: KPMG Research.

Time allocated various stages of production3.5

3

2.5

2

1.5

1

0.5

0 Development Pre-production Production Post-production

121212121212121212121212

12121212

12121212

123123123

121212

123123123123123123123123123

1212

121212

Source: KPMG Research.

121212121212

(Years)

Hollywood Bollywood

162 BUSINESS OF BOLLYWOOD: THE CHANGING DIMENSIONS

the case of 20-30% big budget, and 70-90% of small and medium budget filmprojects) and negligence on planning during developmental and pre-production stagesleading to the cost overruns and decreasing the feasibility of project. One good exampleof this is the Movie ‘Cash’ (Aug 2007) which was a huge commercial failure.Cash has gone over-budget and one of the two producers, Sohail Maklai, hasmortgaged the negatives to a South African film processing lab29. The negatives ofthe film had been held up in South Africa for non-payment of dues. When the filmprints were finally brought back to India Adlabs took over the film for distribution.30

Also in the post-production stage relatively lesser amount of time and money

has been spent because of the reasons stated above. In addition to these there is

certain high amount of anxiety in releasing the film to recover the money in a

hurry (Because of the pressure from financers and promoters), thus unfulfilling

the basic post productions requirements. Another important difference between

Bollywood and Hollywood is that the latter places considerable significant attention

and funds to marketing of films31. On the other hand, in Bollywood there are

distributors who make wrong notions from whatever short clips of the film they

have. This may reduce the feasibility of project. These are the various areas where

the cost distribution and resource allocation structure of Bollywood films can bemanaged more proficiently.

Source: http://media.movietalkies.com/posters/bollywood/movies/2007/cash/cash-2007-1b.jpg

163Film Financing in Bollywood: Scripting a New Saga, Screening an Extravaganza

The difference between Bollywood and Hollywood in different terms can be wellunderstood from the chart given below.

Parameters Bollywood Hollywood

No. of Films Produced 24432 (In 2007) (Avg.250-300) 607 (In 2006) (500 on an Average)

Hit/Flop Ratio 5:19 13:7

Total No. of Ticket Sold (Attendance) $ 3.9 Billion $ 1.7 Billion

Revenue $ 1.75 Billion (In 2006) $ 26.7 Billion (In 2007)

Share of International Market 20% 50%in the Revenue

Annual Growth Rate 16-18% 5-7%

Average Cost of Production/Film $ 5-10 Million $ 60-80 million

Share of Organised Financing 5-10% 95-97%

Share of Unorganised Financing 90-95% 3-5%

Compiled from Various Sources.

From the above chart some points, which should be noticed are:

• The overall profitability of the Bollywood is carried on by a fraction of the

total industry i.e., in one year Bollywood produces only 12-15 successful

projects in terms of box office collection.

• Out of the other total failed projects most are either low budget or medium-

budget projects (Average Cost of Production is very less).

• Though the growth rate is 3 times for Bollywood and a good share of

International audience what it lacks is professionalism and organised nature

of industry.

• Yes, Bollywood got the status of an industry on the paper but in practice it’s

still a highly risky business and hence lacks funding (Organised financing),

thus it has to depend mostly upon unorganised and unauthorised (sometimes

illegal) sources of money.

• Though the total revenue it collects is a mere fraction of what Hollywood

collects annually, but the part of population it impacts upon (Attendance;

Total No. of Ticket Sold) is double as compared to Hollywood. It means it has

an underlying potential to get across the boundaries, but lacks that support

which is much essential to any industry to prosper.

164 BUSINESS OF BOLLYWOOD: THE CHANGING DIMENSIONS

• Need Support but from whom? – From Government, from the people earningtheir bread and butter from Bollywood and from those who really concernsabout the industry.

Issues and Challenges

Other issues are also lurking there. Though GOI has promised a substantial support,and incorporated the policy changes on paper, many of the State Governments arenot actually complying with the norms laid down by Central Government. For e.g.,State Government of Maharashtra, after many request from Bollywood honchos, hasasking for 40% entertainment tax (Many other state governments are asking for60% entertainment tax) which pressurise the operators for discrepancy in theirfinancial statements, thus decreasing the transparency in transactions. TheGovernment’s stance is that of a Protectionist Regulator – by designing tight frameworkwhich is acting as a hindrance and limiting any kind of foreign direct investmentinto vital areas of the value chain further loosening its integrity. These restrictionshave delayed necessary consolidation in the media industries, slowing down theformation of vertically and horizontally-integrated players with critical mass andstrong market access. The next issue is of deficiencies in corporate governance andtransparency – much of the culture of media company management and the filmindustry in particular is in fact much obscure, lacking in core competencies to managethe internal processes effectively and controlling outwards market pressure efficiently.Thus, their inability to perform to their optimum level is very much high. Furtherinvolving profession with personal and family relationship takes the whole companytowards unaccountability, which in effect reduces the transparency. Therefore banksand authorised financial institutions actually hesitate to provide financial support tothe Industry.

Again, one problem which is now an inherent characteristic of the industry is thelack of any kind of integration (vertical or horizontal) or very weak integration ifpresent in the film producing entities. The vertical integration means link betweenvarious stages of film making i.e., development, production, distribution, marketingand exhibition, which if carried out by a single company in turn enhances the smoothfunctioning taking out the extra burden of costs. Horizontal integration exists whenthere are networks in between different production houses on the horizontal leveli.e., if they are sharing their resources (of Cast and Crew) and using same links for

165Film Financing in Bollywood: Scripting a New Saga, Screening an Extravaganza

production and promotional work. Both types of integration can be well understoodfrom the following diagram.

In fact before independence the Hollywood model of vertical integration has alsodeveloped in the Indian film industry which we have already discussed (Studio System).But, over the time, their deployment into a worldwide distribution-driven modelhas secured the companies control over the talent and creative R&D through thecontrol of the majority of revenue streams in all media33. On the other hand verticalintegration in the Indian film industry has first vanished, giving birth to Star Systemand now is again gaining popularity with the corporatisation and increasing pressureof globalisation. Because of the complete absence of this system in middle age ofBollywood history, there remained few studios, which we can say are somewhatprofessional. Otherwise, most film companies, be they primarily in the productionor distribution business are considered to be sub-scale and would require imaginative

Vertical and Horizontal Integration

Compiled by the Author.

Theatrical Release Theatre Association

Exhibition

Marketing & Promotion Media Agency

DistributionMusic, Satellite and

Video rightsDistributors

(Local & International

Production (Pre and Post)Cast & Crew,Music Company

Processing Lab

DevelopmentPlanning Cell Market Research Agency

Production House(Studio)

166 BUSINESS OF BOLLYWOOD: THE CHANGING DIMENSIONS

and bold consolidation strategies in order to attract more substantial and consistentinterest from the private equity sector34. Also obtaining an accurate valuation for thismost idiosyncratic sector (Bertrand Moullier, 2007) is a major hurdle in the path ofa long-term relationship between film producing companies and investment houses.On one side, these companies argue that they need capital to support a move towardsconsolidation, become able to develop entire slates of films at a time, and control IPand returns along the value chain and on the other equity markets are waiting forscale players to appear before establishing an ongoing relationship with the sectorand getting behind its growth35.

Though, today, the link is missing in between Bollywood and Indian capital market(share, equity, stocks and PPP), but still there is a strong probability that a situationwill arrive soon when wind will flow in the opposite direction. The situation is predictablebecause, even with overwhelming presence of liquidity in the markets like China,Japan, Europe and UK, the respective film industries are on a standstill with no furtherhope of growth. Thus there remains only one competitor to Bollywood and i.e.,Hollywood. Indian economy is booming with a continuous growth rate of 9%+ forpast 3 years. With two-digit annual growth set to continue across the media industry(Bertrand Moullier, 2007) also in the foreseeable future. Altogether, they promise thepositive results of a decade-long learning curve during which the Indian film industryhas re-invented itself, espoused new business models based on a more strategic approachto IP, professionalized its management and made full use of new audiovisualtechnologies36. The return on investment for IP holders in Indian films will be improved,and even the lower budget films will have more opportunities to find a wider market ata fraction of the old distribution costs.37

This is an achievement for the entire Indian Film Industry, but the share ofBollywood in this strategic investment in the form of revenues generated is prominent.And with overall improved functioning especially in the increased investment perproject, content quality and global approach, success in important segments likemarketing, promotion and distribution will establish even more accomplishmentfurther in the value chain.

Whatever be the past, the industry has taken its initial steps and is in the stage oftransition from a disintegrated, unorganised and unprofessional framework to an

167Film Financing in Bollywood: Scripting a New Saga, Screening an Extravaganza

integrated, organised and more commercialized structure. But the task has just begun.It has to further adapt and imbibe more such strategic business processes that wouldlay the foundation for that transmutation, which is the ultimate aim of any industry.Simultaneously, it needs to tap alternative investment streams and must have to adaptstrategic revenue generating models. By investing in the advanced technologies, morelucid processes, and optimising resource utilisation it can sustain in such a dynamicand competitive scenario.

It also depends upon the ability of the Bollywood fraternity to answer to the call ofdiversification, customisation, niche marketing and localisation. When it succeeds inmaking this transformation, it will compare favourably with the world’s most developedfilm industry, viz., Hollywood, in terms of functioning and earning potential38.

Future Prospects

So many storms (read trends) have come and gone. Every time Bollywood hasraised on its own. Facing each situation and having passed many such tests it hasjust now entered into the era of globalisation with increasing demand ofprofessionalism. Seeds of corporatisation have already been sown, black clouds ofunderworld; nasty air of clumsiness being fading away, there is surely a dawn ofilluminity somewhere down the line. You can feel it from the current lingo ofBollywood, which has been spoken out by not only film fraternity but critics too.It seems there’s a new dictionary of Bollywood (After receiving a place for itself inOxford Dictionary) getting formed due to overwhelming attention it has beenattracting from almost every corner of this Global village. Stars are called talent,movies are projects, selling films is de-risking and buying them is buildingintellectual property rights39. Listed companies and private producers have alreadypulled up the curtains with a promise to spend Rs.3,000 crore on making movies,in the coming future. Corporate’s also are pumping in more and more money. Theleader is Reliance who alone has an intended fund of $1 billion (Rs 4,000 crore),of which it has committed Rs.500 crore40. From corporate in Hugo Boss suits toindependent producers in Gucci T-shirts (Kaveri Bamzai, 2008), everybody issinging a new tune, and looks ready to screen an extravagant show. DefinitelyBollywood is changing in a positive way. Here is the Big Picture of that change.

168 BUSINESS OF BOLLYWOOD: THE CHANGING DIMENSIONS

In simple terms, Bollywood is scripting a new tale, with the first chapter ofCorporatisation already been put on the board. Proclaimed film budgets from biggiesas well as small ones are breaking limits with each passing day. For e.g., A smallproducer pair of ‘Harry and Harmeet Baweja’ who were producing mid-scale filmslike ‘Dilwale’ and ‘Qayamat’ till recent past are now coming out with their mostambitious $15-$20 million (Pre-estimated budget) project called “LoveStory 2050”with extravagant visual effects and actions choreographed by international studios.Since the film production is becoming more expensive, innovative forms of financingmust have to creep in to make it available to a broad section of filmmakers41. And itis coming in a big way, which is clear from the above chart with each player investing$100+ crores in Bollywood. But in this hullaballoo about professionalism and technicalsupremacy, Bollywood should scrutinise the amount of money invested in Scriptdevelopment (research and writing), otherwise it will be a repetition of same oldmistake i.e., ‘Only Style no Substance.’

There is no doubt that Bollywood itself is very much eager to tackle the issues andchallenges discussed above with a strong wit and will. The steep learning curve of thepast decade is beginning to set off a critical mass of change in the industry’s approach tothe production risk as well as corporate models and practices42. It seems it has learntand is learning continuously from the past mistakes, which is a good sign. The emergentnew market leaders are applying a new set of skills to the business of film, approachingIP with a more strategic, long-term perspective and boldly embracing the full range ofdigital technology applications43. This is a transformational phase in the film financingpatterns and the operating parameters on which Bollywood has relied for so long.

All said aloud, Bollywood is evolving positively with time. Slowly but surely ‘TheFuture is Coming’.

Source: India Today, Issue April 14th 2008, Article “Bollywood Extralarge”.

Big SpendersWho is investing how much in movies over the next 15 months

Reliance Entertainment Rs.500 cr Shree Ashtavinayak Rs.150 cr

Indian Films Rs.440 cr Dharma Productions Rs.150 cr

YashRaj Films Rs.350 cr Mirchi Movies Rs.120 cr

UTV Rs.280 cr PNC Rs.100 cr

Eros Rs.180 cr PVR Rs.100 cr

169Film Financing in Bollywood: Scripting a New Saga, Screening an Extravaganza

Conclusion

Does it need a conclusion (The Article or the Story itself )? This is the new beginningto an exciting journey of an industry once neglected and felt ashamed of by manystrata of Indian society. It is now witnessing a sea change, since its birth into its everyaspect of film making as well as the other prominent ones like that of film financing,which forms the core of this article. Though there is a great deal of corporatisationand globalisation, there still remains room for enhancement and resolving lot ofissues discussed earlier.

Let the boundaries get shackled, new horizons get touched upon and many moreshores of success get explored. Let us hope for a bigger, better and brighter Bollywood.

(Gaurav R Wankhade, Research Associate, Icfai Research Center, Mumbai.)

Endnotes

1 www.icmrindia.org

2 “Indian Entertainment Industry Focus 2010: Dreams to Reality” A CII-KPMG Report,2005.

3 http://www.bollywoodcountry.com/factoids.php

4 Article, “Bollywood Extra Large”, Kaveree Bamzai, India Today, April 14, 2008.

5 Ibid.

6 “Box Office History for India Movies”, http://www.the-numbers.com/movies/series/India.php, Tuesday, March 25, 2008.

7 News Item, Aishwarya, Abhishek, Hrithik party as Jodha Akbar is finally complete Posted

on Thursday, November 15, 2007 (EST), http://news.sawf.org/Bollywood/45097.aspx.

Source: http://en.wikipedia.org/wiki/Image:Lovest2003.jpg

170 BUSINESS OF BOLLYWOOD: THE CHANGING DIMENSIONS

8 Article “Bollywood”, http://en.wikipedia.org/wiki/Bollywood

9 “Indian Entertainment Industry Focus 2010: Dreams to Reality” A CII-KPMG Report,

2005.

10 Ibid.

11 Ibid.

12 Article “The Film Industry in India: An IndiaOneStop synopsis” by

www.indiaonestop.com

13 Ibid.

14 Ibid.

15 Ibid.

16 Ibid.

17 Ibid.

18 Ibid.

19 Ibid.

20 Ibid.

21 Ibid.

22 KPMG Research, “Indian Entertainment Industry Focus 2010: Dreams to Reality”A CII-KPMG Report, 2005.

23 Ibid.

24 Article, “Whither Bollywood”, Bertrand Moullier, Feb 2007. The George Washington

University Law School.

25 Ibid.

26 KPMG Research, “Indian Entertainment Industry Focus 2010: Dreams to Reality”A CII – KPMG Report, 2005.

27 Newsletter, “A brilliant idea works”, by Shyam Shroff, Sunday. DNA, Mumbai,

11th May, 2008.

28 Ibid.

29 Article,“Cash trouble for novel experiment in filmmaking”, http://timesofindia.indiatimes.com/articleshow/968880.cms

30 Article, “Adlabs took over Anubhav Sinha’s Cash”, http://indiafm.com/news/2007/01/29/8754/index.html

171Film Financing in Bollywood: Scripting a New Saga, Screening an Extravaganza

31 “Indian Entertainment Industry Focus 2010: Dreams to Reality” A CII-KPMG Report,2005.

32 http://lotusnova.blogspot.com/2008/03/bollywood-myths.html?showComment=1206688080000

33 www.law.gwu.edu/Academics/research_centers/ciec/Documents/Notes%20on%20Creativity/WhitherBollywood.pdf

34 Article, “Whither Bollywood”, Bertrand Moullier, February 2007. The George

Washington University Law School.

35 Ibid.

36 Ibid.

37 http://www.law.gwu.edu/nr/rdonlyres/cb1c5fda-6333-49e2-879f-d941a59b5dd5/0/ciecwhitherbollywood.pdf

38 Ibid.

39 Article, “Bollywood Extra Large”, India Today, April 14, 2008.

40 Ibid.

41 Indian Television’s Special Report, “Bollywood banks on corporate route to the big

league”, by Sibabrata Das, 21st March 2006.

42 Ibid.

43 Ibid.