Filing Season 2018 and direct communication was sent to taxpayers who may not have to submit a...

58

26 June 2018 Filing Season 2018

-

Upload

vuongxuyen -

Category

Documents

-

view

216 -

download

0

Transcript of Filing Season 2018 and direct communication was sent to taxpayers who may not have to submit a...

26 June 2018

Filing Season 2018

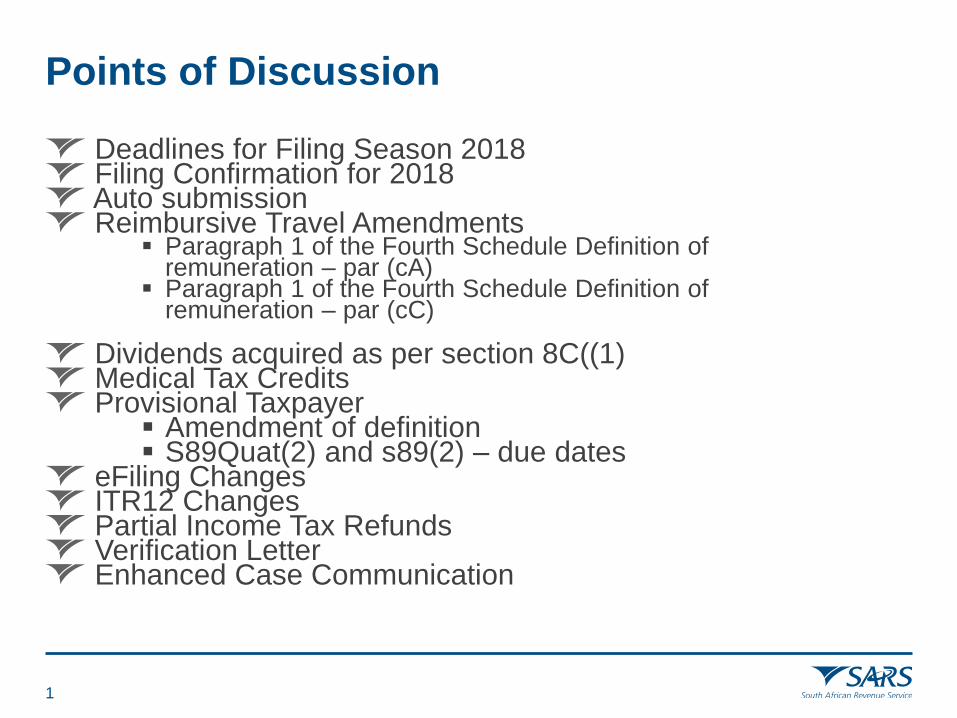

Points of Discussion

1

Deadlines for Filing Season 2018 Filing Confirmation for 2018 Auto submission Reimbursive Travel Amendments

Paragraph 1 of the Fourth Schedule Definition of remuneration – par (cA)

Paragraph 1 of the Fourth Schedule Definition of remuneration – par (cC)

Dividends acquired as per section 8C((1) Medical Tax Credits Provisional Taxpayer

Amendment of definition S89Quat(2) and s89(2) – due dates

eFiling Changes ITR12 Changes Partial Income Tax Refunds Verification Letter Enhanced Case Communication

Deadlines for Filing Season 2018

2

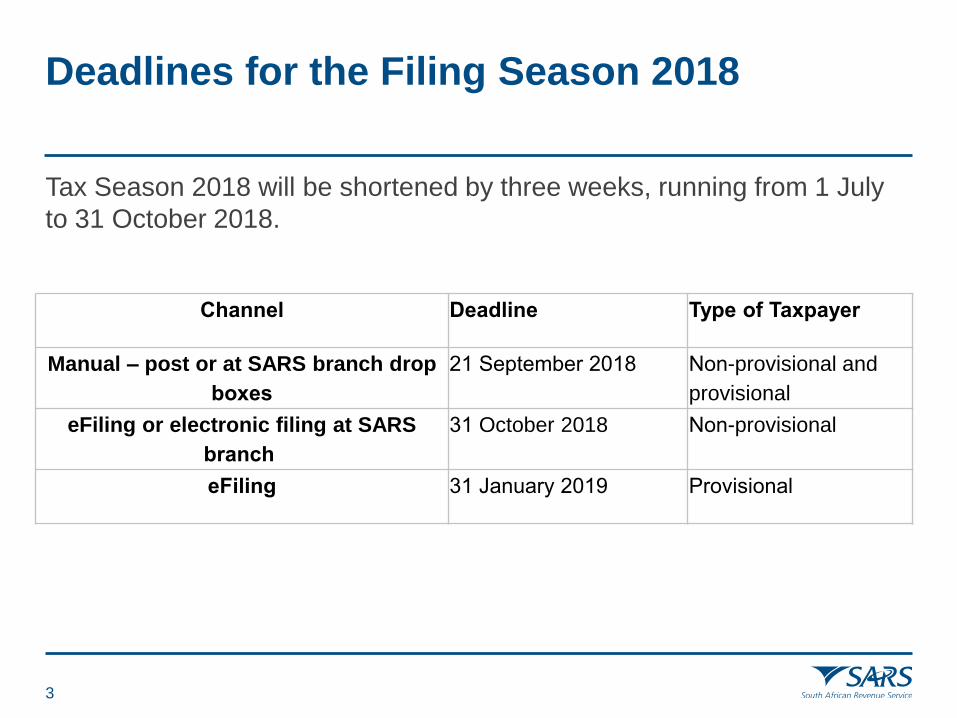

Deadlines for the Filing Season 2018

3

Tax Season 2018 will be shortened by three weeks, running from 1 July

to 31 October 2018.

Channel Deadline Type of Taxpayer

Manual – post or at SARS branch drop

boxes

21 September 2018 Non-provisional and

provisional

eFiling or electronic filing at SARS

branch

31 October 2018 Non-provisional

eFiling 31 January 2019 Provisional

Filing confirmation 2018

4

Filing confirmation 2018

5

Personalised and direct communication was sent to taxpayers who may

not have to submit a return, based on information submitted during tax

season 2017, setting out their specific tax obligations.

A new IVR option will be introduced at the SARS Contact centre to reduce

the number of SARS branch office visits during the 2018 filing season.

This service will allow taxpayers to verify if they are required/not required to

file the 2018 personal income tax return via IVR.

The filing confirmation self help service is only applicable to PIT taxpayers

with a valid ID number and tax reference number. Available in 6 languages

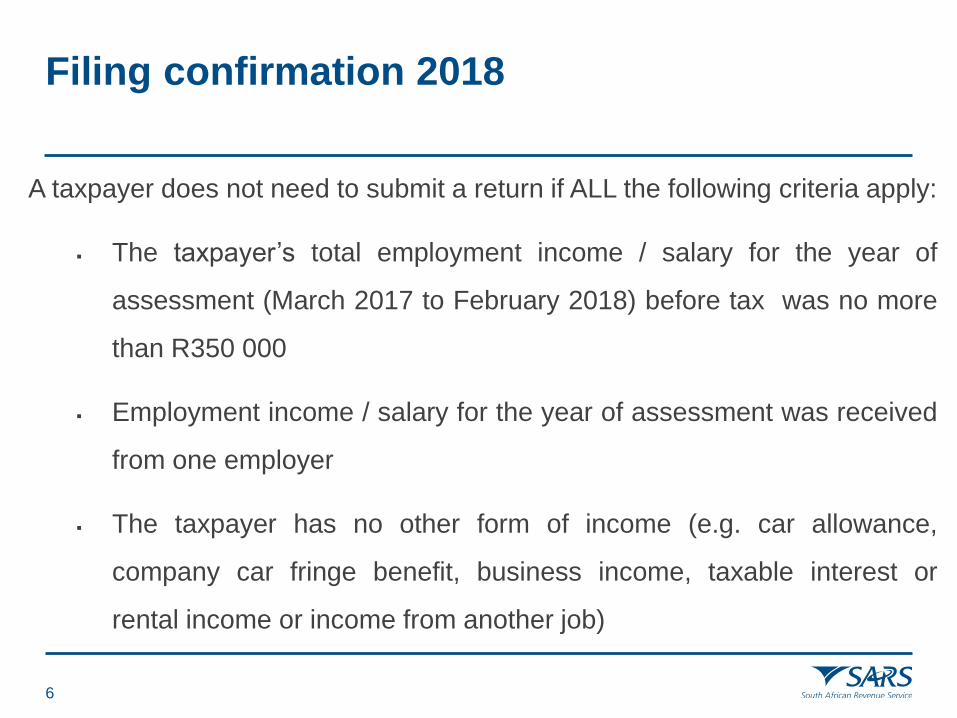

Filing confirmation 2018

6

A taxpayer does not need to submit a return if ALL the following criteria apply:

The taxpayer’s total employment income / salary for the year of

assessment (March 2017 to February 2018) before tax was no more

than R350 000

Employment income / salary for the year of assessment was received

from one employer

The taxpayer has no other form of income (e.g. car allowance,

company car fringe benefit, business income, taxable interest or

rental income or income from another job)

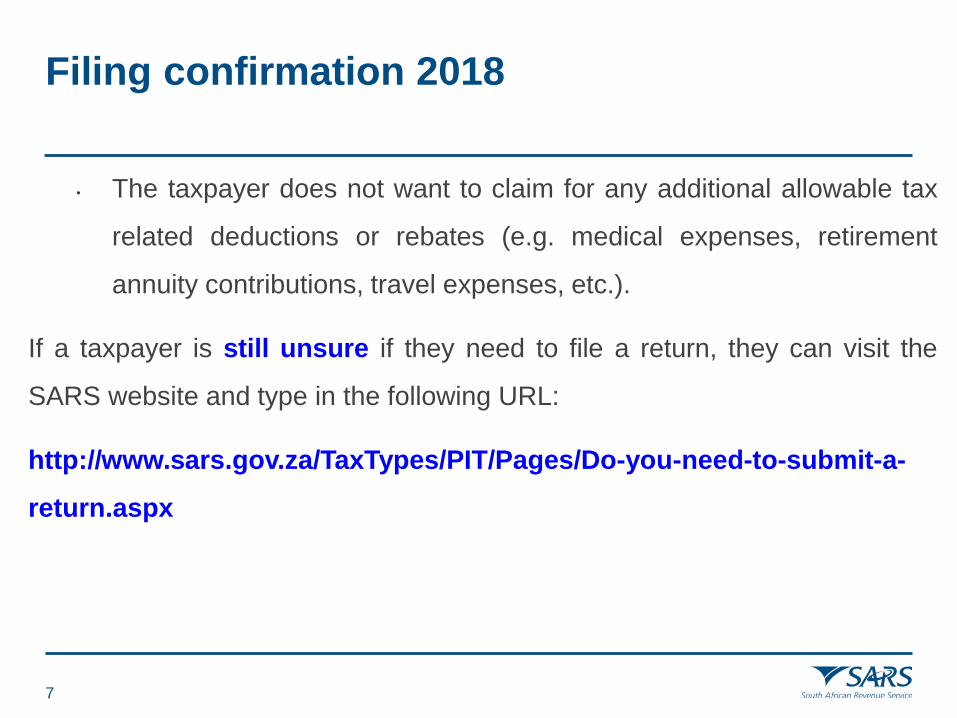

Filing confirmation 2018

7

• The taxpayer does not want to claim for any additional allowable tax

related deductions or rebates (e.g. medical expenses, retirement

annuity contributions, travel expenses, etc.).

If a taxpayer is still unsure if they need to file a return, they can visit the

SARS website and type in the following URL:

http://www.sars.gov.za/TaxTypes/PIT/Pages/Do-you-need-to-submit-a-

return.aspx

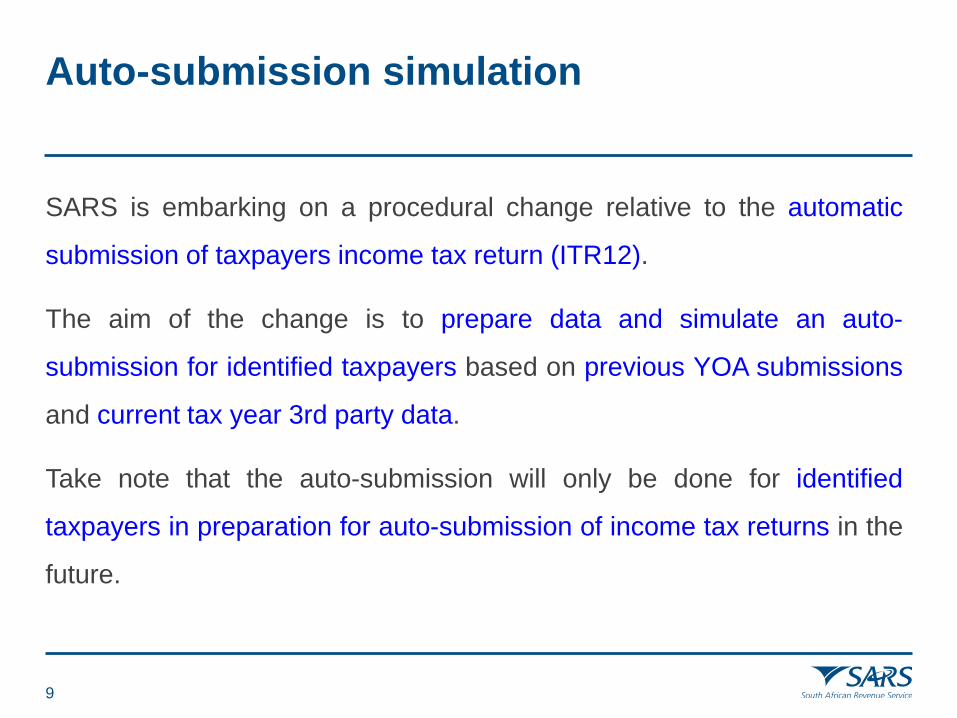

Auto-submission simulation

8

Auto-submission simulation

9

SARS is embarking on a procedural change relative to the automatic

submission of taxpayers income tax return (ITR12).

The aim of the change is to prepare data and simulate an auto-

submission for identified taxpayers based on previous YOA submissions

and current tax year 3rd party data.

Take note that the auto-submission will only be done for identified

taxpayers in preparation for auto-submission of income tax returns in the

future.

Auto-submission simulation

10

The data preparation done by the case selection engine will take into

consideration taxpayers with the following return 3rd party information:

Taxpayer employed for the full year of assessment

IRP5 data

Medical expenditure

Retirement annuity contributions

No claim for a deduction against a travel allowance

Reimbursive Travel Amendments Paragraph 1 of the Fourth Schedule Definition of remuneration – par (cA)

11

Paragraph 1 of the Fourth Schedule Definition of remuneration – par (cA)

12

This amendment indicates that a reimbursive travel allowance is

excluded from the 80/20 split which applies to travel allowances (3701).

Changes are effective from 1 March 2018.

Paragraph 1 of the Fourth Schedule – Definition of remuneration – travel reimbursement

13

The current SARS practice is that travel reimbursement is not subject to

Employees’ Tax, even though the legislation states that a portion of the

reimbursement must be subject to PAYE.

This was done to reduce the administrative burden for employers as it

involved a burdensome calculation. The employee was required to

account on the travel reimbursement on assessment.

To make it easier for employers to determine remuneration on travel

reimbursement, the definition of remuneration has been amended by the

introduction (cC) in the definition of remuneration.

Reimbursive Travel Amendments Paragraph 1 of the Fourth Schedule Definition of remuneration – par (cC)

14

Paragraph 1 of the Fourth Schedule Definition of remuneration – par (cC)

15

For employees' tax and reimbursement of travel expenses; the new

paragraph (cC) of the definition of remuneration provides that 100% of the

travel reimbursement in excess of rate per km fixed by the minister of

finance in the Gazette used for the simplified method, is included in

remuneration.

The prescribed rate per km for the simplified method is; either R3.61(as

from 1 March 2018 in Gazette No. 41473 on 2 March 2018) or the

determined rate (also referred to as the fixed cost rate).

Paragraph 1 of the Fourth Schedule Definition of remuneration – par (cC)

16

As from 1 March 2018 the limitation of the 12 000 km has been removed

from the rate per km regulation.

The following rules apply to reimbursive travel allowances:

Where the reimbursive allowance does not exceed the prescribed

rate per km AND no other compensation is paid to the employee

(travel allowance 3701(3751 for foreign)), the amount is not subject

to employees tax or neither taxable on assessment and code 3703

(3753 for foreign) must be used on the IRP5 certificate.

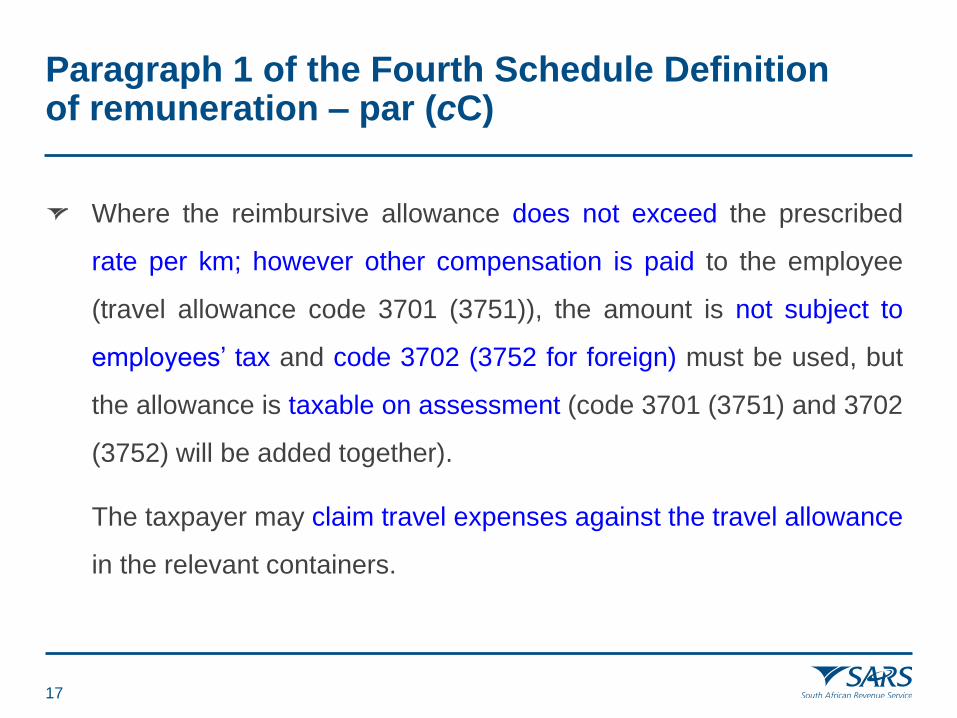

Paragraph 1 of the Fourth Schedule Definition of remuneration – par (cC)

17

Where the reimbursive allowance does not exceed the prescribed

rate per km; however other compensation is paid to the employee

(travel allowance code 3701 (3751)), the amount is not subject to

employees’ tax and code 3702 (3752 for foreign) must be used, but

the allowance is taxable on assessment (code 3701 (3751) and 3702

(3752) will be added together).

The taxpayer may claim travel expenses against the travel allowance

in the relevant containers.

Paragraph 1 of the Fourth Schedule Definition of remuneration – par (cC)

18

Where the reimbursive allowance exceeds the prescribed rate per

km (irrespective of the km travelled), the amount above the

prescribed rate is subject to employees’ tax and reflected under code

3722 (3772 for foreign). The portion below the prescribed rate will be

reflected under code 3702 (3752). Upon assessment; codes 3701

(3751) (if applicable), 3702 (3752) and 3722 (3772) will be added

together to determine the limitation and the taxpayer may claim

travel expenses against the travel allowance in the relevant travel

containers.

Paragraph 1 of the Fourth Schedule Definition of remuneration – par (cC)

19

For employees’ tax purposes, code 3702 will not be included in 4582

in respect of section 11F , however code 3722 (3772) will be

included in code 4582.

Reimbursive travel allowance Example 1

20

Required:

Calculate the reimbursed amounts and indicate the applicable source

codes which should be used for the taxable and non-taxable amounts.

No. Prescribed

rate

Actual

rate

Actual km Amount Source

code

Taxable/Non-

taxable

1.

No other compensation

R3.61 R3.00 10 000 30 000 3703 No PAYE

Not taxable on

assessment

2. 20 000 3701 PAYE

Taxable on

assessment

R3.61 R3.20 10 000 32 000 3702 No PAYE

Taxable on

assessment

Reimbursive travel allowance Example 1

21

No. Prescribed

rate

Actual

rate

Actual

km

Amount Source

code

Taxable Non-

taxable

3. No other compensation

R3.61 R3.00 15 000 45 000 3703 No PAYE

Not Taxable on

assessment

4. No other compensation / other compensation

R3.61 R4.61 17 000 61 370 3702 No PAYE

Taxable on

assessment

17 000 3722 PAYE

Taxable on

assessment

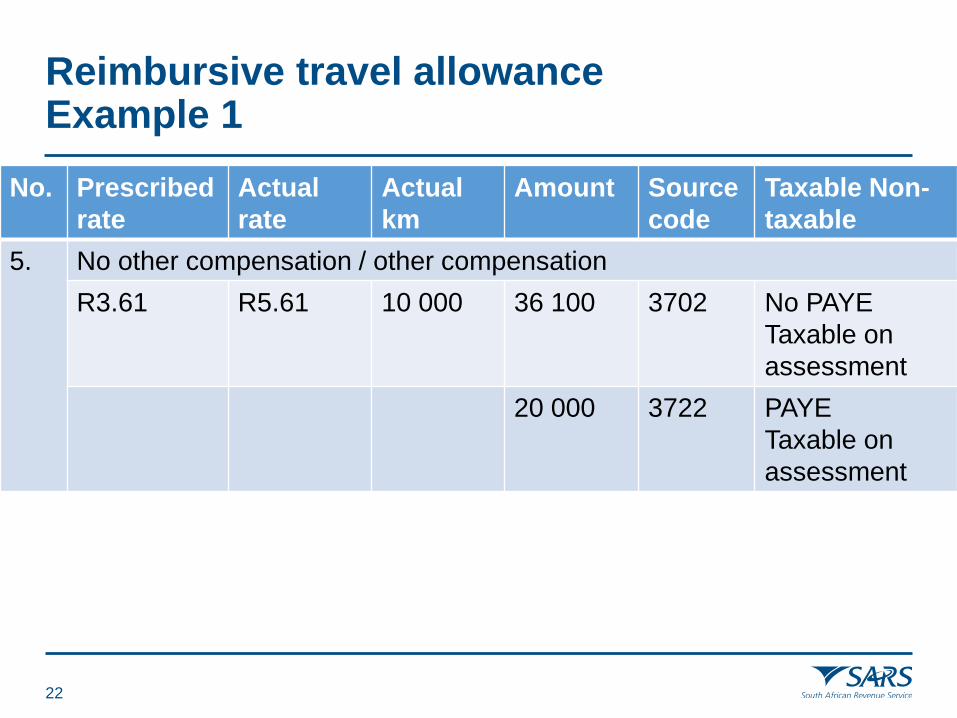

Reimbursive travel allowance Example 1

22

No. Prescribed

rate

Actual

rate

Actual

km

Amount Source

code

Taxable Non-

taxable

5. No other compensation / other compensation

R3.61 R5.61 10 000 36 100 3702 No PAYE

Taxable on

assessment

20 000 3722 PAYE

Taxable on

assessment

Dividends acquired as per section 8C((1)

23

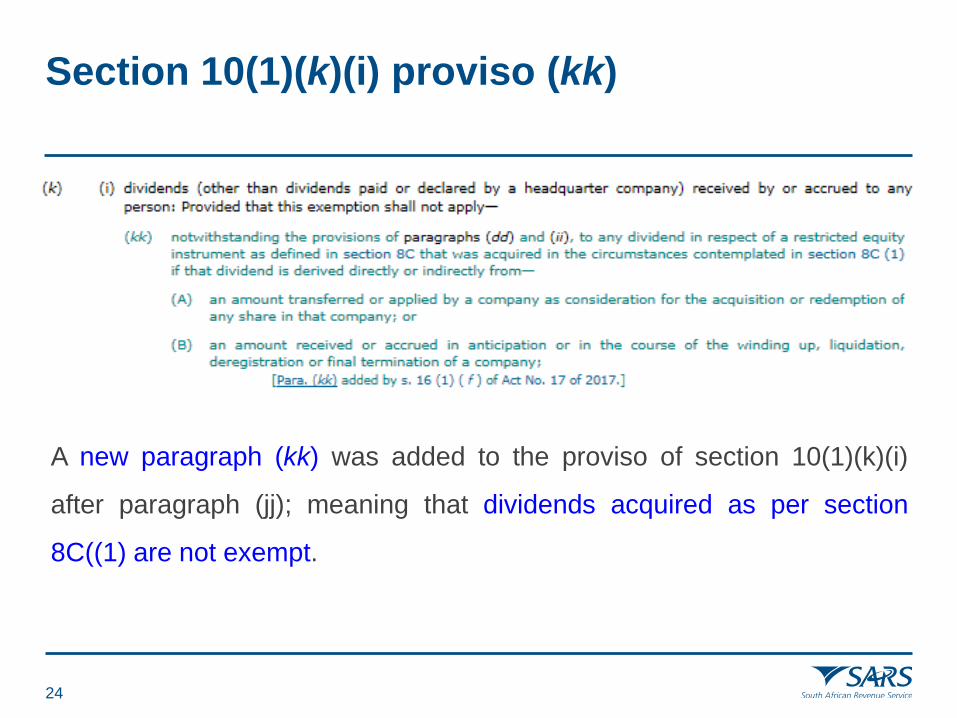

Section 10(1)(k)(i) proviso (kk)

24

A new paragraph (kk) was added to the proviso of section 10(1)(k)(i)

after paragraph (jj); meaning that dividends acquired as per section

8C((1) are not exempt.

Definition of remuneration – new par (g)(iv)

25

The definition of “remuneration” in paragraph 1 of the Fourth Schedule has

been amended by adding paragraph (g)(iv) to include paragraph (kk) of the

proviso to section 10(1)(k)(i).

This means that dividends from restricted equity instruments acquired in

accordance with section 8C(1), are not exempt as per section 10(1)(k)(i)

proviso (kk) and are included in the definition of “remuneration” for

employees’ tax purposes.

New source code 3723 (3773) to be included for purposes of in section 11F.

Changes effective from 18 December 2017 onwards.

Medical Tax Credits

26

Section 6A and 6B medical tax credits

27

If a taxpayer declares retirement (accrual date from 1 October 2007) and/or

withdrawal (accrual date from 1 March 2009) related lump sums, including

severance benefit from 1 March 2011 then the medical tax credits will be

allowed where there was no other income.

This means that irrespective that retirement / withdrawal lump sums are

taxed separately, the SARS system will be changed to allow the medical tax

credits against retirement/withdrawal lump sums.

Applicable to all assessments in respect of 2012 onwards.

Section 6A and 6B medical tax credits and ITA34’s changes

28

New

Retirement fund lump sum benefit tax liability (Before Medical Tax

Credits)

Less balance of Medical Tax Credits below the above field

Withdrawal fund lump sum benefit tax liability (Before Medical Tax

Credits)

Less balance of Medical Tax Credits” below the above field

Retirement fund lump sum benefit tax liability (After Medical Tax

Credits)

Withdrawal fund lump sum benefit tax liability (After Medical Tax

Credits

Provisional Taxpayer Amendment of definition

29

Definition of provisional taxpayer paragraph 1 of the Fourth Schedule

30

The paragraph 1(a)(i) of the definition of “provisional taxpayer” has been

amended to include employees who are employed by employers who are

not registered in terms of paragraph 15 of the Fourth Schedule.

Definition of provisional taxpayer paragraph 1 of the Fourth Schedule

31

On assessment, if one or more income is received by the taxpayer and

manually completed in the IRP5 section, where there is no prepopulated

data from a third party, no PAYE number and does not include code 4102

and/or 4115 (PAYE on Lump sum); the taxpayer will be coded as a

provisional taxpayer. The provisional taxpayer exemption rules will also be

applied accordingly.

The amendment will be effective from 1 March 2017.

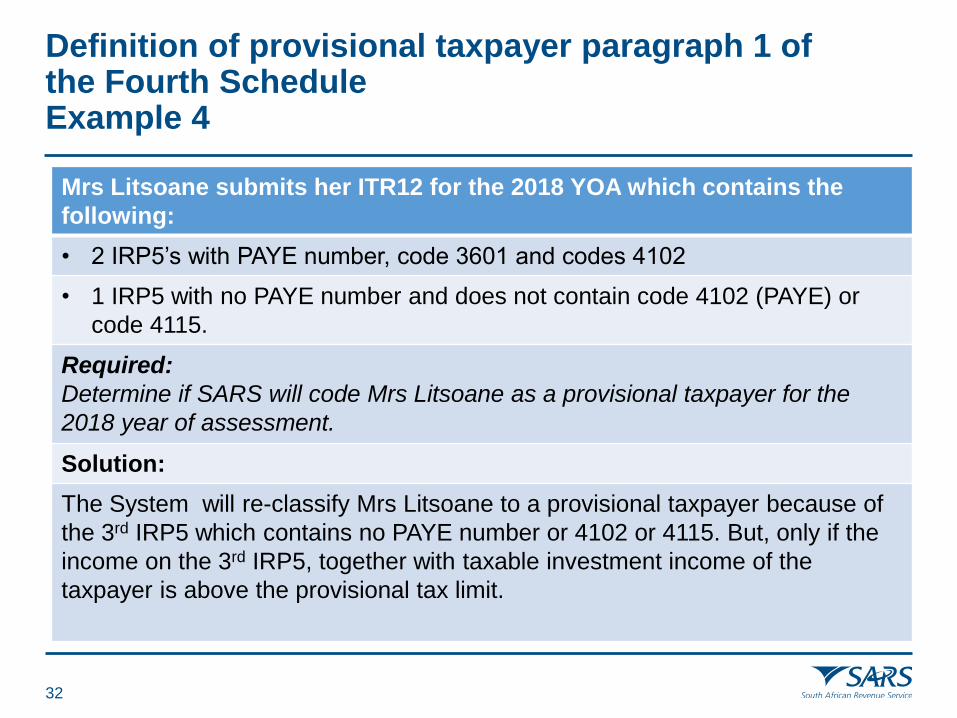

Definition of provisional taxpayer paragraph 1 of the Fourth Schedule Example 4

32

Mrs Litsoane submits her ITR12 for the 2018 YOA which contains the

following:

• 2 IRP5’s with PAYE number, code 3601 and codes 4102

• 1 IRP5 with no PAYE number and does not contain code 4102 (PAYE) or

code 4115.

Required:

Determine if SARS will code Mrs Litsoane as a provisional taxpayer for the

2018 year of assessment.

Solution:

The System will re-classify Mrs Litsoane to a provisional taxpayer because of

the 3rd IRP5 which contains no PAYE number or 4102 or 4115. But, only if the

income on the 3rd IRP5, together with taxable investment income of the

taxpayer is above the provisional tax limit.

Provisional Taxpayer S89Quat(2) and s89(2) – due dates

33

S89Quat(2) and s89(2) – due dates Background

34

Prior to the implementation of the Tax Administration Act, 2011, the

definition of the “date of assessment” read as follows: “..…in relation to

any assessment, means the date specified in the notice of such

assessment as the due date or, where a due date is not specified , the

date of such notice”..

S89Quat(2) and s89(2) – due dates Background

35

According to the Tax Administration Act, 2011, the definition of the “date

of assessment” reads as follows:

(a) in the case of an assessment by SARS, the date of the issue of

the notice of assessment; or

(b) in the case of self-assessment by the taxpayer—

(i) if a return is required, the date that the return is

submitted; or

(ii) if no return is required, the date of the last payment of

the tax for the tax period or, if no payment was made in

respect of the tax for the tax period, the effective date;

The Tax Administration Act, 2011 references only the date of issue of the

notice of assessment and not the due date.

S89Quat(2) and s89(2) – due dates

36

Changes on the SARS system with regards to section 89Quat(2)

[interest on underpayment or overpayment of provisional tax] and

section 89(2) [interest on late payment of assessed tax] will be

implemented.

Changes will occur in phases:

The payment due date on the SARS system to be the last day of the

next month. Therefore the rule which checks if the assessment was

processed before or after the 15th of that specific month will be removed.

S89Quat(2) and s89(2) – due dates

37

The calculation of 89 Quat(2) interest and 89(2) interest only as it pertains

to the calculation of payment due dates will be updated on the SARS

system to reflect changes regarding the due date calculation. Regardless of

when the taxpayer is assessed (before or after the 15th), the payment due

date is the last day of the next month following the date of assessment.

Both original and revised assessments will be impacted by the changes.

The changes to the due dates will have an impact on the ITA34 Look and

Feel, and will only reflect a date of assessment and payment due date for

original assessments processed in July 2018.

S89Quat(2) and s89(2) – due dates Example 5

38

The following information is provided:

FYE 2015/02/28

Effective date 2015/09/30

s89Quat(2) interest calculated from 2015/10/01

Assessment processed on 2016/06/29

Required:

Determine the payment due date of the assessment , the dates for which section

89Quat(2) and the dates from when section 89(2) interest will be charged.

Solution:

• The payment due date of the assessment is 2016/07/31 (the last day of the

following month).

• 89Quat(2) interest should be charged from 2015/10/01 to 2016/06/30 (the day

following the last day of the month up until the date that the assessment was

processed).

• 89(2) will be calculated from 2016/07/01, if the payment is not made by the

payment due date 2016/07/31.

eFiling Enhancements

39

eFiling Enhancements

40

All legal, form and other filing season enhancements to be included.

2018 YOA warning message if the 2018 return is overdue.

New refresh RA data:

Uploading of supporting documents: Changes will be made with the

2018 Filing season release to increase the size for all the tax types

to 5MB per file and a maximum of 50MB per upload.

ITR12 changes 2018

41

ITR12 changes

42

Changing of wording; “Moderate” to “temporary” and “severe” to

“permanent” within the disability medical container.

RAF contributions container: moving of question “To how many RA

policies did you….” to above “Total contributions”, pre-population of

number of policies (editable), 3rd party data details of policies and

auto calculation of total.

ITR12 changes

43

Foreign income container: Additional wizard questions “did you

receive any form of remuneration for foreign services rendered?” and

“Was any portion of this foreign services remuneration subject to tax

in another country?”. If the answer is “yes” the “Foreign Income

(excluding amounts received/accrued as a beneficiary of a trust, or

deemed to have accrued in terms of s7) ” container will be displayed.

New field within “Foreign income container”:

ITR12 changes

44

Foreign income reflected on a SA IRP5 on any foreign income

source code (taxable or not taxable) which was taxed in the foreign

country will be excluded from the total remuneration, calculated for

S11F purposes.

If the amount in 4235 exceeds the foreign remuneration source

codes declared on any IRP5, then the system

will reduce 4235 to zero.

Note: Where 4235 is completed, the return will be routed for manual

assessment.

ITR12 changes

45

Tax free investments container:

The value captured into this field must be greater than nil. Applicable

for 2016 YOA only and not subsequent years.

Increase employment income, allowances and tax credits source

codes on IRP5/IT3(a) to allow for 100 source codes.

Increase lump sum income/retirement lump sum/severance benefits

received to 15 certificates per return with 5 lump sum source codes

per certificate.

ITR12 changes

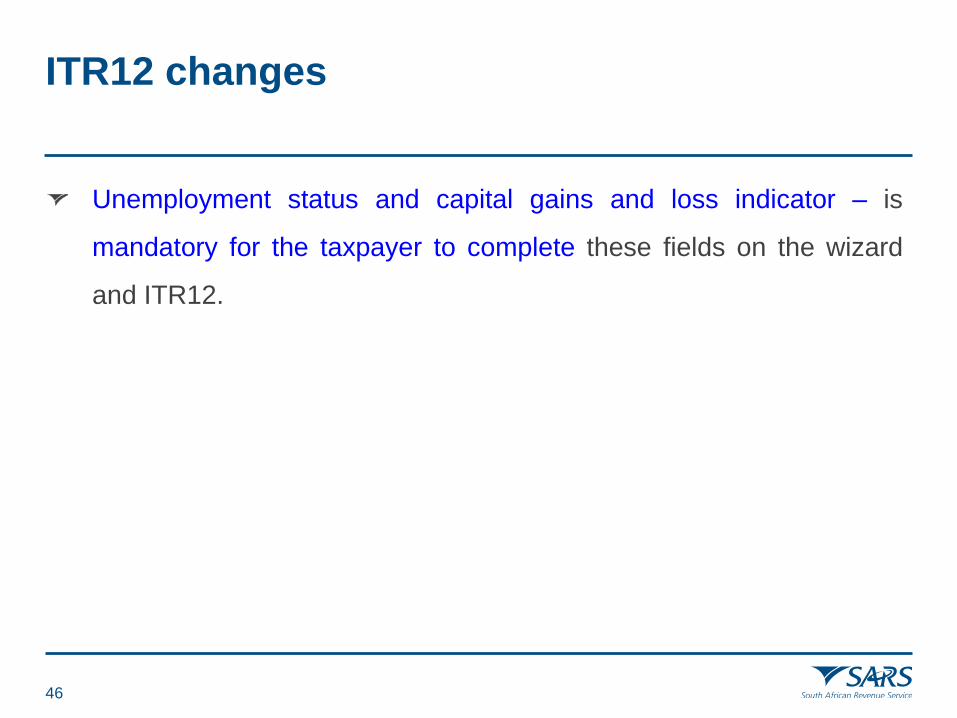

46

Unemployment status and capital gains and loss indicator – is

mandatory for the taxpayer to complete these fields on the wizard

and ITR12.

Partial Income Tax Refunds

47

Partial IT refunds

48

Where an assessment on one return may reflect a refund due, there may

be instances where prior returns may reflect that the taxpayer needs to

make a payment.

These amounts will be offset against each other and the taxpayer will be

notified of the outcome.

It will be indicated on the ITSA( Statement of Account) that only capital

amounts are refunded and that interest will be calculated once the

audit/review has been finalised.

Partial IT refunds Example 2

49

6.1 Credit assessment under audit

Tax period Assessment Amount (R) Audit on period

2015 1 000

2016 -2 500 Yes

2017 -4 000

Balance on account -5 500

Partial refund R5500 – R2500 = R3000

6.2 Debit assessment under audit

Tax period Assessment Amount (R) Audit on period

2015 -1 000

2016 2 500 Yes

2017 -4 000

Balance on account -2 500

Partial refund -R2 500 (Refund of R5 000 less debit of R2 500)

Verification Letter

50

Verification letter enhancements

51

In light of the fact that SARS is actively working on improving public

perception, verification letters have been improved.

Verification letters will be more specific in terms of the supporting

documents that we require from taxpayers who may have been flagged

for a specific risk.

This will assist the taxpayer to respond timeously and accurately.

Enhanced Case Communication

52

Introduction and background

53

To improve the ease of access to information for our taxpayers, through

better customer engagement SARS will introduce notifications that will be

sent via SMS and/or email to the taxpayer.

The notifications will be based on triggered events which will take place in

the workflow process.

SARS will send an SMS and/or an email to the taxpayer or the tax

practitioner if the configured channel is the preferred channel; as per the

contact details on the SARS system. In the case of non-natural entities, the

representatives details as per the entities SARS system details will be used.

Application of the ECC tool

54

The taxpayer will receive a notification via SMS or email which has been

created by the SARS official. E.g. SARS has issued a letter reminding

you to submit supporting documents, Thank you for uploading your

supporting documents, your verification is in process.

The content of the SMS will be added as a note to the affected case or

the content of the email will be attached to the case as an attachment.

eFiling users will also be able to view notifications under “SARS

Correspondence > Letters” based on the tax reference number or under

the “letters” section of the work page of an existing case.

Conclusion

55

Conclusion

56

Taxpayers will be encouraged to file via eFiling on their own.

We will support eFilers with the Help-You-eFile service which connects

the taxpayer to one of our tax agents in real time via the contact centre

while both are online. The taxpayer is then assisted each step of the

way.

Tax practitioners will be requested to strictly use eFiling for submitting

taxpayer returns and avoid doing so at a branch.

Administrative penalties for late submissions will be imposed, as they

have been in previous years.