Fiduciary Duty and the Responsible Trustee - SHARE · Topics 1. What is a fiduciary? 2. Who is a...

35

Fiduciary Duty and the Responsible Trustee Pension Sense Conference November 27, 2003

Transcript of Fiduciary Duty and the Responsible Trustee - SHARE · Topics 1. What is a fiduciary? 2. Who is a...

Fiduciary Duty and the

Responsible Trustee

Pension Sense ConferenceNovember 27, 2003

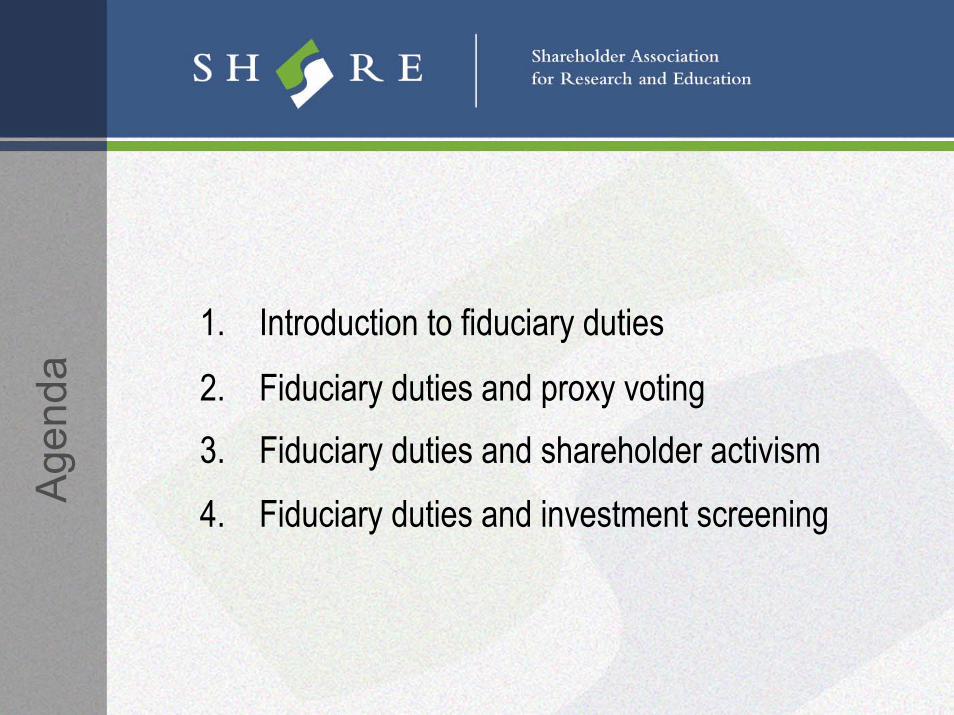

Agen

da

1. Introduction to fiduciary duties

2. Fiduciary duties and proxy voting3. Fiduciary duties and shareholder activism4. Fiduciary duties and investment screening

Topi

cs

1. What is a fiduciary?2. Who is a fiduciary?3. Types of fiduciaries4. Sources of fiduciary duties5. Fiduciary principles6. Liabilities and protections7. Fiduciary duties in the DC context8. Four-step fiduciary cycle

1.1

A person in whom trust, reliance or confidence is reposed.Fiduciaries exercise discretion in managing theassets of beneficiaries.Fiduciaries are in a power relationship withbeneficiaries. The Fiduciary relationship is the highest level of obligation at law.

What is a fiduciary?

1.2

Board of trustees

Who is a fiduciary?

Plan administratorPension committee membersInvestment ManagersAdvisors (lawyers, consultants)

Custodial TrusteeAgents

1.3

Governing (board of trustees/ pension committee)

Types of fiduciaries

Operating (staff/managers/custodians)

Managing (pension sub-committees/staff)

1.4

The plan’s trust agreementSources of fiduciary duties

Legislation (Pension Benefits Standards Act)

Common Law

1.5

Duty of Prudence: to apply the care, skill and diligence that a prudent person would apply in the management of another person’s assets

– Standard of Care Rule– Invest Trust Property Rule– Rate of Return Rule– Diversification Rule– Investment Advice Rule

Fiduciary principles

1.6

Duty of Loyalty: to act honestly, in good faith, and in the best interest of the beneficiaries, treating all beneficiaries with an even hand.

– Good Faith Rule– Delegation Rule– Conflict of Interest Rule– Even-Handed Rule

Fiduciary principles (cont…)

1.7

Oversee administration of the planDraft, approve & annually review investment policySet process for selection and review of investment managersEnsure voting of proxies is retained or delegatedReview plan performance as per regulationsRequire actuarial valuation every three yearsFile & update documents with Superintendent of Pensions

Examples of fiduciary responsibilities

1.8

Act in accordance with the plan’s trust agreement, investment policy and the lawConsult and obtain adequate expert advice when making decisionsDocument all proceedings to demonstrate steps taken when making a decision (Prudence is process)Act in what you determine to be the best interests of plan members and beneficiariesLiability insurance

Liabilities and protections

1.9

Select and monitor advisors– Knowledge and performance of providers and members– Who’s giving advice?

Fiduciary duties in the DC context

Select and review options – Number of choices may create additional responsibilities

– Dealing with members who don’t make selections

Communication with members – Advice v. education

– Document decisions and educational initiatives

1.10

“Prudence is process”

Four-step fiduciary cycle

1. Understand

2. Plan

3. Do

4. Review

Proxy Voting

Prox

y vo

ting

Proxy voting is a fiduciary responsibilityPBSA requires investment policies state whether proxies are retained or delegated by the plan. Proxies are a valuable asset of the plan and should be voted. (OSFI)If delegated, plan should instruct investment manager(s) or proxy voting service how to vote.100’s of shareholder proposals voted annuallyManagers voting records vary widely on key votes

Prox

y vo

ting

Four areas of responsibility

(1) Establishing guidelines(2) Assessing issues(3) Voting proxies(4) Monitoring results

Prox

y vo

ting

New developments - disclosureU.S. SEC Regulations require all investment managers to disclose proxy voting guidelines and voting recordsMany OECD countries require disclosure of proxy voting guidelines and voting recordsIn Canada, National Instrument 81-106 would require managers of mutual funds to report how they “voted on matters relating to issuers of portfolio assets of the investment fund, other than routine business of those issuers.” (not adopted)

Shareholder Activism

Shar

ehol

der A

ctiv

ism Elements

Letter writingFace-to-face meetings with corporate executivesDrafting and filing shareholder proposalsSupporting other proposals at corporate AGMsLitigation

Shar

ehol

der A

ctiv

ism

Shareholder activism is prudent trusteeshipKirby Report of the Senate Standing Committee on Banking, Trade and CommerceCBCA rules (BCCA in 2004)US Department of Labour “Avon” lettersUK Myners Review on Institutional InvestmentIndustry practiceEmpirical evidence suggest positive correlation between shareholder activism and corporate financial performance

Shar

ehol

der A

ctiv

ism

New developmentsInstitutional investor coalitions: Canadian Coalition on Good Governance, KAIROS, Council of Institutional Investors, SHAREIndividual union pension plan activismBroader engagementLinkage between corporate governance and social and environmental corporate practicesLegitimacy

Investment Screening

Inve

stm

ent S

cree

ning Traditional view:

Must maximize returns Act in the best interests of members/ beneficiaries – best interests = financial interestsMust treat all members/beneficiaries equallyMust maintain maximum diversificationCowan v. Scargill consistently cited as leading case

Fidu

ciar

y D

utie

s an

d SR

II Cowan v. Scargill:

Bad facts

Plaintiff not represented by counsel

Not properly argued

Unclear statements

Lowest court

Qualification for constituencies with shared values

Inve

stm

ent S

cree

ning Developments since Scargill:

A. Legal and Regulatory

1. FSCO Statement

2. PBSA Schedule of permissible investments

3. OECD country pension regulations

4. Alternate view of US common law

5. Statements by English legal counsel

Inve

stm

ent S

cree

ning

Developments since Scargill:

B. Market

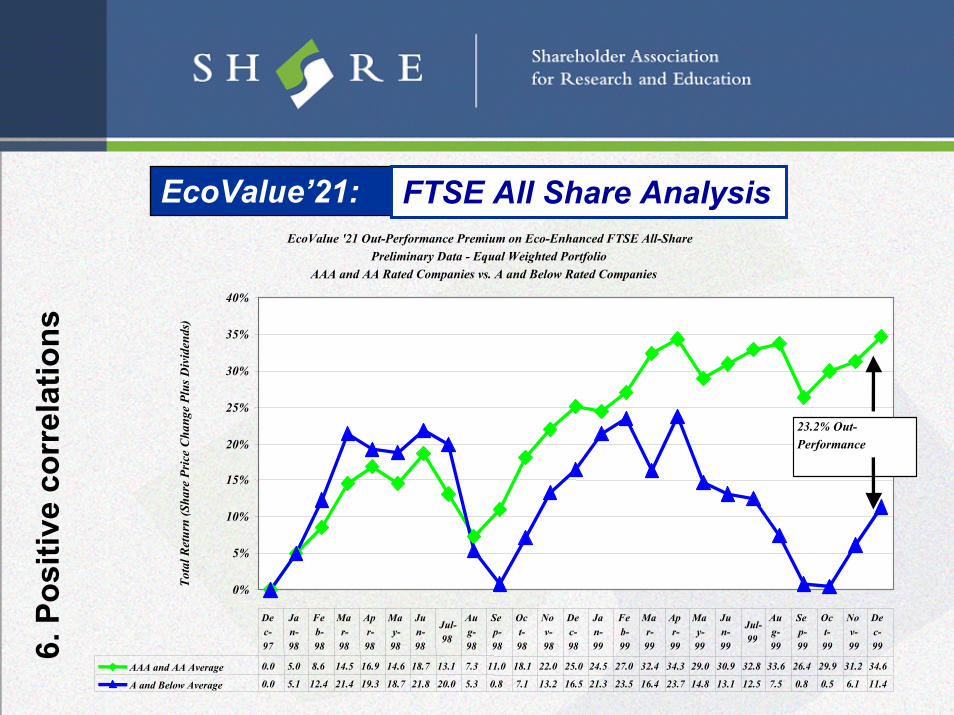

1. Positive correlations between social, environmental and financial performance of corporations

2. Surveys of beneficiaries’ opinion

3. Industry practice

4. SRI performance data

EcoValue '21 Out-Performance Premium on Eco-Enhanced FTSE All-SharePreliminary Data - Equal Weighted Portfolio

AAA and AA Rated Companies vs. A and Below Rated Companies

0%

5%

10%

15%

20%

25%

30%

35%

40%

Tota

l Ret

urn

(Sha

re P

rice

Cha

nge

Plus

Div

iden

ds)

AAA and AA Average 0.0 5.0 8.6 14.5 16.9 14.6 18.7 13.1 7.3 11.0 18.1 22.0 25.0 24.5 27.0 32.4 34.3 29.0 30.9 32.8 33.6 26.4 29.9 31.2 34.6

A and Below Average 0.0 5.1 12.4 21.4 19.3 18.7 21.8 20.0 5.3 0.8 7.1 13.2 16.5 21.3 23.5 16.4 23.7 14.8 13.1 12.5 7.5 0.8 0.5 6.1 11.4

Dec-97

Jan-98

Feb-98

Mar-98

Apr-98

May-98

Jun-98

Jul-98

Aug-98

Sep-98

Oct-98

Nov-98

Dec-98

Jan-99

Feb-99

Mar-99

Apr-99

May-99

Jun-99

Jul-99

Aug-99

Sep-99

Oct-99

Nov-99

Dec-99

23.2% Out-Performance

EcoValue’21: FTSE All Share Analysis

6. P

ositi

ve c

orre

latio

ns

Inve

stm

ent S

cree

ning

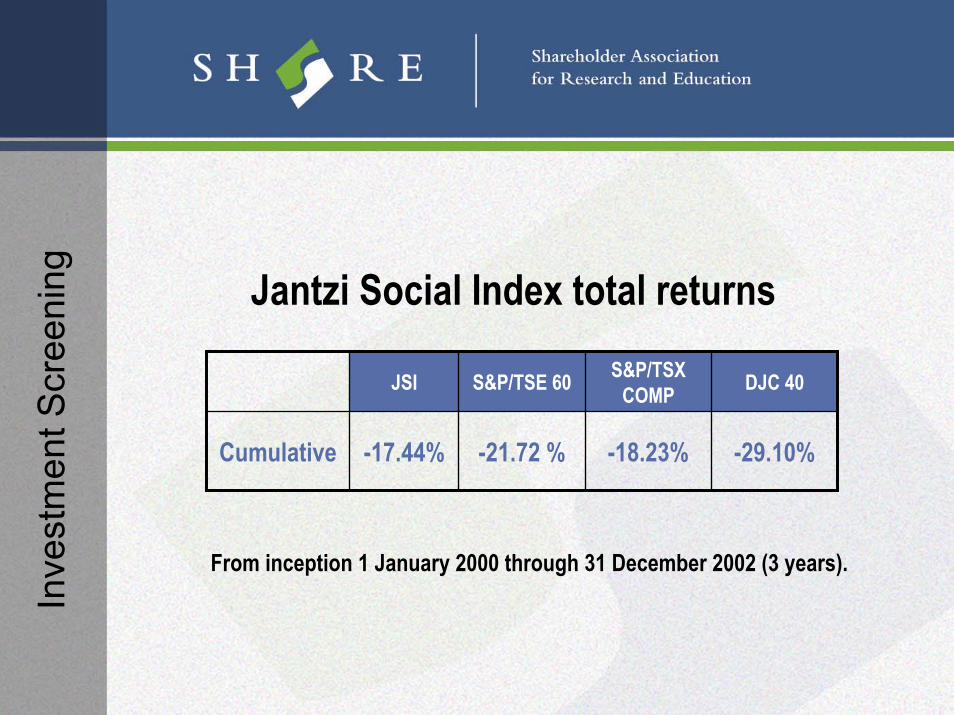

-29.10%-18.23%-21.72 %-17.44%Cumulative

DJC 40S&P/TSX COMPS&P/TSE 60JSI

From inception 1 January 2000 through 31 December 2002 (3 years).

Jantzi Social Index total returns

Inve

stm

ent S

cree

ning

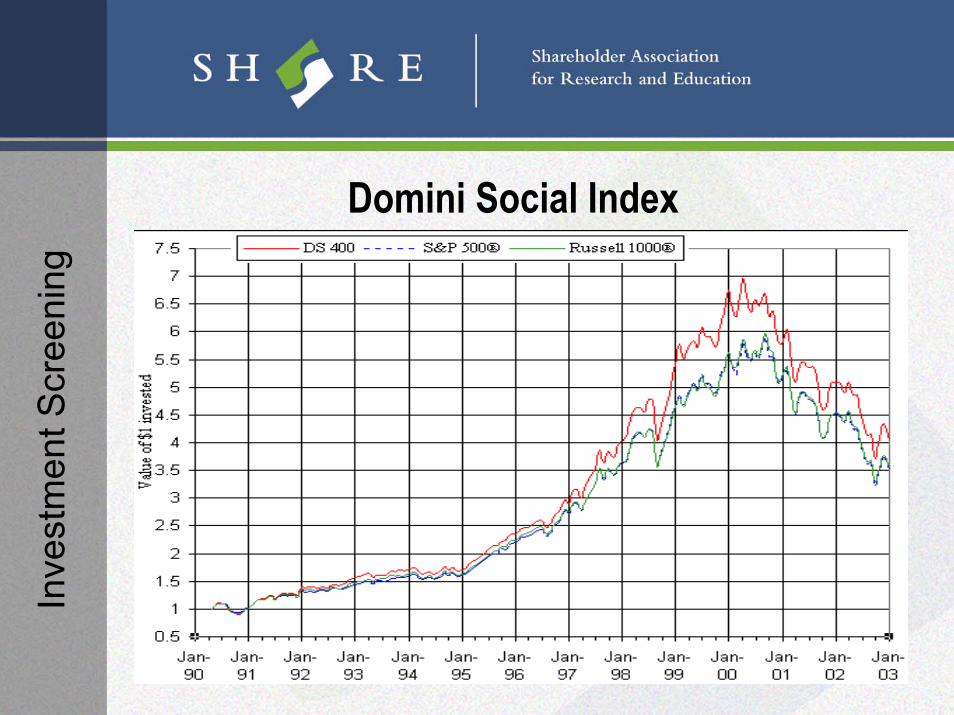

Domini Social Index

Inve

stm

ent S

cree

ning

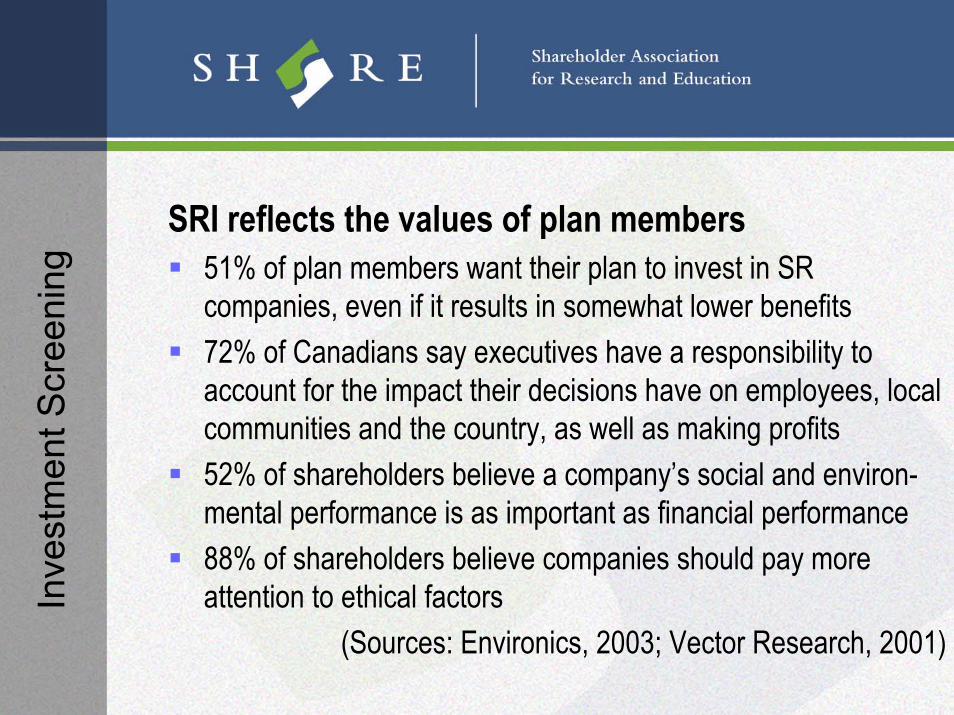

SRI reflects the values of plan members51% of plan members want their plan to invest in SR companies, even if it results in somewhat lower benefits72% of Canadians say executives have a responsibility to account for the impact their decisions have on employees, local communities and the country, as well as making profits52% of shareholders believe a company’s social and environ-mental performance is as important as financial performance88% of shareholders believe companies should pay more attention to ethical factors

(Sources: Environics, 2003; Vector Research, 2001)

Inve

stm

ent S

cree

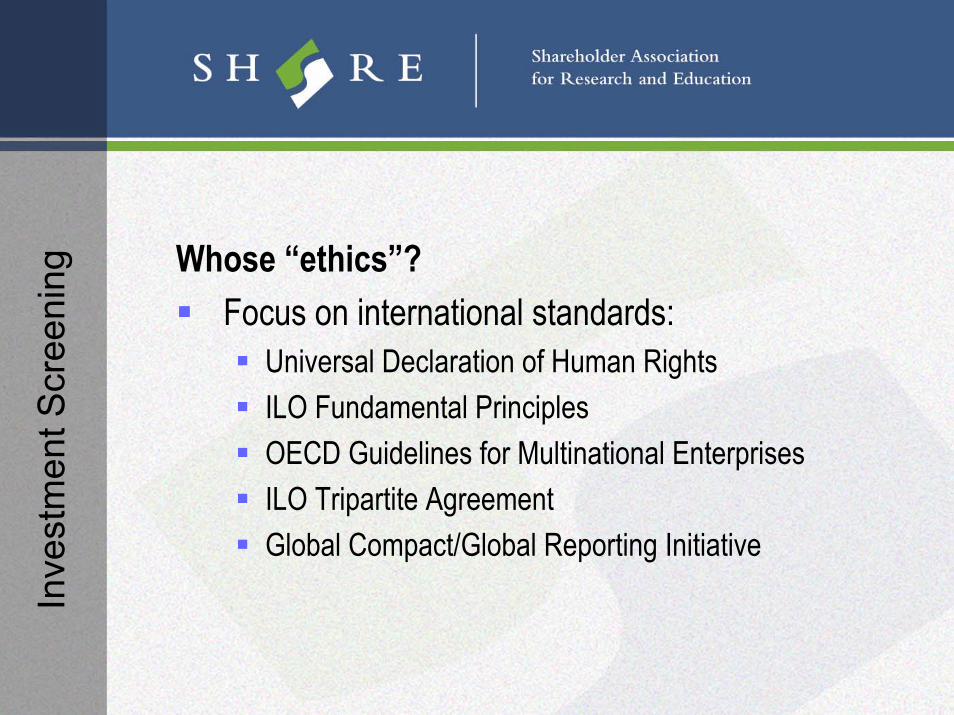

ning Whose “ethics”?

Focus on international standards:Universal Declaration of Human RightsILO Fundamental PrinciplesOECD Guidelines for Multinational EnterprisesILO Tripartite AgreementGlobal Compact/Global Reporting Initiative

Inve

stm

ent S

cree

ning

Restatement of fiduciary obligationsMaintain a reasonable rate of return across the entire portfoliowithin accepted levels of risk.Act in the best long-term interests of plan members and beneficiaries.All members/beneficiaries must be treated equitablyMust maintain adequate diversification within accepted risk parametersCollateral interests of beneficiaries as employees, and third parties may be considered, but subordinate to beneficiaries’interests.

Inve

stm

ent S

cree

ning

Trustee protections:Act in accordance with the plan’s trust agreement, investment policy and the lawConsult and obtain adequate expert advice when making decisionsAct in what you believe to be the best interests of plan members and beneficiariesDocument all proceedings to demonstrate steps taken when making a decisionLiability insurance

Shareholder Association for Researchand Education

702 – 1166 Alberni StreetVancouver, British Columbia V6E 3Z3

Phone: (604) 408-2456Fax: (604) 408-2525Email: [email protected]

Website: www.share.ca