FEDERAL FARM CREDIT BANKS CONSOLIDATED SYSTEMWIDE BONDS ...

72

OFFERING CIRCULAR FEDERAL FARM CREDIT BANKS CONSOLIDATED SYSTEMWIDE BONDS AND DISCOUNT NOTES The terms “we,” “us,” “our,” and the “Banks,” as used throughout this Offering Circular, mean the Farm Credit System Banks, acting by and through the Federal Farm Credit Banks Funding Corporation. We propose to offer for sale from time to time Federal Farm Credit Banks Consolidated Systemwide Bonds and Federal Farm Credit Banks Consolidated Systemwide Discount Notes (collectively, the “Securities”) by means of this Offering Circular and a Term Sheet or an Offering Announcement. The Securities are the general unsecured joint and several obligations of the Banks and will be issued under the authority of the Farm Credit Act of 1971, as amended, and the regulations of the Farm Credit Administration. THE SECURITIES ARE THE JOINT AND SEVERAL OBLIGATIONS OF THE BANKS AND ARE NOT OBLIGATIONS OF AND ARE NOT GUARANTEED BY THE UNITED STATES GOVERNMENT. THE SECURITIES ARE NOT REQUIRED TO BE REGISTERED AND HAVE NOT BEEN REGISTERED UNDER THE U.S. SECURITIES ACT OF 1933, AS AMENDED. IN ADDITION, THE BANKS ARE NOT REQUIRED TO REGISTER OR FILE, AND DO NOT FILE, PERIODIC REPORTS UNDER THE U.S. SECURITIES EXCHANGE ACT OF 1934, AS AMENDED. For a discussion of certain of the risks relevant to an investment in the Securities, see “Risk Factors” herein and “Risk Factors” in the Annual Information Statement of the Farm Credit System and as may be set forth in other Incorporated Information. Unless otherwise specified by us with respect to a particular issue of Securities, the following terms and conditions generally apply to the Securities which we may offer. The applicable Offering Announcement or Term Sheet will contain the specific information about the Security offered thereby and may contain additional or different terms and conditions related to that Security. For more detail, see “Terms and Conditions of the Securities.” BONDS DISCOUNT NOTES • Maturity of 3 months to 30 years • Maturity of 1 to 365 days • Fixed or floating interest rate or discounted from the amount to be paid at maturity • Discounted from the amount to be paid at maturity • May be eligible for separation into Interest and Principal Components • Not eligible for separation into Interest and Principal Components • May be subject to redemption at the option of the Banks or otherwise as specified in the Term Sheet • Not subject to redemption • Book-entry form • Book-entry form • Fixed-Rate Bonds and Zero-Coupon Bonds — minimum denomination of $1,000, increased in integral multiples of $1,000 • Minimum denomination of $1,000, increased in integral multiples of $1,000 • Fixed-Rate Bonds with highly structured feature(s) and Floating-Rate Bonds — minimum denomination of $100,000, increased in integral multiples of $1,000 • No maximum aggregate principal amount outstanding • Maximum aggregate par amount outstanding of $60 billion • Final terms set forth in a Term Sheet • Final terms set forth in an Offering Announcement The date of this Offering Circular is October 18, 2010.

Transcript of FEDERAL FARM CREDIT BANKS CONSOLIDATED SYSTEMWIDE BONDS ...

OFFERING CIRCULAR

FEDERAL FARM CREDIT BANKSCONSOLIDATED SYSTEMWIDE BONDS AND DISCOUNT NOTES

The terms “we,” “us,” “our,” and the “Banks,” as used throughout this Offering Circular, mean the FarmCredit System Banks, acting by and through the Federal Farm Credit Banks Funding Corporation.

We propose to offer for sale from time to time Federal Farm Credit Banks Consolidated Systemwide Bondsand Federal Farm Credit Banks Consolidated Systemwide Discount Notes (collectively, the “Securities”)by means of this Offering Circular and a Term Sheet or an Offering Announcement. The Securities are thegeneral unsecured joint and several obligations of the Banks and will be issued under the authority of theFarm Credit Act of 1971, as amended, and the regulations of the Farm Credit Administration.

THE SECURITIES ARE THE JOINT AND SEVERAL OBLIGATIONS OF THE BANKS AND ARE

NOT OBLIGATIONS OF AND ARE NOT GUARANTEED BY THE UNITED STATES

GOVERNMENT. THE SECURITIES ARE NOT REQUIRED TO BE REGISTERED AND HAVE

NOT BEEN REGISTERED UNDER THE U.S. SECURITIES ACT OF 1933, AS AMENDED. IN

ADDITION, THE BANKS ARE NOT REQUIRED TO REGISTER OR FILE, AND DO NOT FILE,

PERIODIC REPORTS UNDER THE U.S. SECURITIES EXCHANGE ACT OF 1934, AS

AMENDED.

For a discussion of certain of the risks relevant to an investment in the Securities, see “Risk Factors”

herein and “Risk Factors” in the Annual Information Statement of the Farm Credit System and as may

be set forth in other Incorporated Information.

Unless otherwise specified by us with respect to a particular issue of Securities, the following terms andconditions generally apply to the Securities which we may offer. The applicable Offering Announcement orTerm Sheet will contain the specific information about the Security offered thereby and may containadditional or different terms and conditions related to that Security. For more detail, see “Terms andConditions of the Securities.”

BONDS DISCOUNT NOTES

• Maturity of 3 months to 30 years • Maturity of 1 to 365 days• Fixed or floating interest rate or discounted

from the amount to be paid at maturity• Discounted from the amount to be paid at

maturity• May be eligible for separation into Interest

and Principal Components• Not eligible for separation into Interest and

Principal Components• May be subject to redemption at the option of

the Banks or otherwise as specified in theTerm Sheet

• Not subject to redemption

• Book-entry form • Book-entry form• Fixed-Rate Bonds and Zero-Coupon Bonds —

minimum denomination of $1,000, increasedin integral multiples of $1,000

• Minimum denomination of $1,000, increased inintegral multiples of $1,000

• Fixed-Rate Bonds with highly structuredfeature(s) and Floating-Rate Bonds —minimum denomination of $100,000, increasedin integral multiples of $1,000

• No maximum aggregate principal amountoutstanding

• Maximum aggregate par amount outstanding of$60 billion

• Final terms set forth in a Term Sheet • Final terms set forth in an OfferingAnnouncement

The date of this Offering Circular is October 18, 2010.

The Securities will be offered and sold by us through Dealers acting as principal, whether individually or ina syndicate, or, if so designated by us, as agent. Bonds may be offered for sale through a single Dealer or agroup of Dealers through syndication, negotiation or a competitive bidding process. Discount Notes will beoffered for sale through a limited group of Dealers. In addition, Designated Dealers may be appointed toparticipate through Discount Note Dealers in the distribution of Discount Notes. We may appointadditional Bond Dealers, Discount Note Dealers and Designated Dealers and either we or a Dealer or aDesignated Dealer may terminate an appointment at any time.

Dealers may be paid underwriting concessions in connection with the distribution of Bonds and DiscountNotes and Designated Dealers may be paid selling concessions in connection with the distribution ofDiscount Notes. Dealers purchasing certain Bonds from us may offer a selling concession to other Dealersor to securities dealers that are not members of a selling group in connection with the sale of such Bonds,subject to certain requirements. Discount Note Dealers may pay a selling concession to Designated Dealers.Dealers and Designated Dealers may share their underwriting or selling concession, as applicable, with theiraffiliates, subject to certain requirements.

In connection with any particular issue of Securities, one or more of the Banks may enter into interest rateswaps or other hedging transactions with, or arranged by, a Dealer or Designated Dealer participating in theissuance, an affiliate of the Dealer or Designated Dealer or an unrelated third party. The Dealer,Designated Dealer or other party may receive compensation, trading gain or other benefits in connectionwith the hedging transactions. The interest rate swaps or other hedging transactions may reference theSecurities, other obligations of the Banks or obligations of other issuers.

The Securities may be sold directly by us to investors and no concessions will be payable on these directsales. See “Plan of Distribution.”

The Securities will not be listed on any securities exchange and there can be no assurance that theSecurities described in this Offering Circular will be sold or that there will be a secondary market for theSecurities. See “Risk Factors.” We reserve the right to withdraw, cancel or modify any offer of Securitieswithout notice.

Capitalized terms used in this Offering Circular are defined in the Glossary. All references to the OfferingCircular are as amended or supplemented. All references to agreements, statutes, regulations, guidelines orother similar documents are as amended as of the date of the Offering Circular as most recently amendedor supplemented.

2

IN MAKING AN INVESTMENT DECISION INVESTORS MUST RELY ON THEIR OWN

EXAMINATION OF THE ISSUER AND THE TERMS OF THE OFFERING, INCLUDING THE

MERITS AND RISKS INVOLVED. THIS OFFERING CIRCULAR FOR THE SECURITIES HAS

NOT BEEN REVIEWED BY ANY FEDERAL OR STATE SECURITIES COMMISSION OR

REGULATORY AUTHORITY. FURTHERMORE, THESE AUTHORITIES HAVE NOT

CONFIRMED THE ACCURACY OR DETERMINED THE ADEQUACY OF THIS DOCUMENT.

ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

This Offering Circular relates only to the Securities and not to any other securities of the Banks which

have been or will be issued on behalf of the Banks pursuant to a different disclosure document, including,

but not limited to, those securities issued under the Federal Farm Credit Banks Consolidated Systemwide

Master Notes Offering Circular dated December 21, 1999, as amended by the supplement dated

August 20, 2001, or under the previous Federal Farm Credit Banks Consolidated Systemwide Bonds and

Discount Notes Offering Circular dated June 18, 1999, as amended by supplements dated August 20,

2001, November 26, 2003, March 8, 2007 and September 30, 2008 (“Prior Offering Circular”). This

Offering Circular replaces and supersedes the Prior Offering Circular for issues of Securities priced on

and after the date of this Offering Circular. Systemwide Debt Securities are no longer being offered under

the Prior Offering Circular, the Federal Farm Credit Banks Global Debt Program Offering Circular dated

October 10, 1996, or the Federal Farm Credit Banks Consolidated Systemwide Medium-Term Notes

Offering Circular dated July 19, 1993, as amended by the supplements dated February 26, 1997 and

June 11, 1999. No securities previously offered under the Global Debt Program Offering Circular or the

Master Notes Offering Circular are currently outstanding.

No person is authorized by us to give any information or to make any representation not contained in this

Offering Circular (and any supplements hereto), the Incorporated Information (as defined below) and, if

applicable, the Offering Announcement or the Term Sheet with respect to a particular issue of Securities,

and, if given or made, such information or representation must not be relied on as having been authorized

by us, the Dealers or the Designated Dealers. The distribution of this Offering Circular or any other

offering materials and the offer, sale, and delivery of the Securities in certain jurisdictions may be

restricted by law. Persons into whose possession offering material comes must inform themselves about

and observe any such restrictions. This Offering Circular does not constitute, and may not be used for or

in connection with, an offer or solicitation of the Securities in any jurisdiction where, or to any person to

whom, it is unlawful to make such an offer or solicitation by anyone not authorized so to act. This

Offering Circular does not constitute an offer to sell or a solicitation of an offer to buy any securities

other than the Securities. Neither the delivery of this Offering Circular, any supplement to this Offering

Circular, or any Offering Announcement or Term Sheet, nor any sale hereunder, shall under any

circumstances create any implication that the information in these documents is correct as of any time

subsequent to the respective dates of the documents.

This Offering Circular has not been approved as a base prospectus for the purpose of Directive

2003/71/EC by the competent authority of any Member State of the European Economic Area. Securities

may only be offered in a Member State of the European Economic Area in the limited circumstances

specified in the “Plan of Distribution.” In addition, we have not authorized the Offering Circular to be

used as offering material for any secondary market offering and/or sales of Securities by any person,

including any Dealer(s) or Designated Dealer(s).

We, any Dealer or Designated Dealer may only communicate or cause to be communicated and will only

communicate or cause to be communicated any invitation or inducement to engage in investment activity

(within the meaning of Section 21 of the Financial Services and Markets Act 2000 (the “FSMA”))

received by it in connection with the issue or sale of any Securities in circumstances in which

Section 21(1) of the FSMA does not apply to us.

This Offering Circular has not been submitted for clearance to the Autorité des marchés financiers in

France.

3

The Securities may not be suitable investments for all investors, and some of the Securities are complex

financial instruments. The Securities are intended for purchase only by investors capable of understanding

the risks involved in such an investment. You should not purchase any of the Securities unless you

understand and are able to bear the price, yield, market, liquidity, structure, redemption and other risks

associated with that Security. You should consult your own financial and legal advisors about the risks

arising from an investment in a particular issue of Securities, the appropriate tools to analyze that

investment, and the suitability of that investment in your particular circumstances. See “Risk Factors”

herein for a discussion of certain risks that should be considered in connection with an investment in the

Securities as well as “Risk Factors” in the Annual Information Statement of the Farm Credit System and

as may be set forth in other Incorporated Information. Neither this Offering Circular nor any applicable

Offering Announcement or Term Sheet describes all of the risks of any investment in the Securities,

including, but not limited to, Bonds with principal or interest determined by reference to one or more

interest rate indices, currencies, other indices or formulae, Bonds that include redemption features, caps,

floors or other rights or options or an investment in the Securities (which are all U.S. dollar-

denominated) where the investor’s principal currency is other than the U.S. dollar. We disclaim any

responsibility to advise investors of those risks as they exist at the date of this Offering Circular or any

related Offering Announcement or Term Sheet or as they may change from time to time.

Additional Securities may be issued and sold as part of an existing issue of Securities. Certain Bonds may

be subject to redemption in whole or in part prior to maturity and may be eligible for separation into

Interest Components and Principal Components. Any secondary market for particular issues of Securities

may be adversely affected by such additional issuance, the full or partial redemption of an issue of Bonds

or the separation of Bonds into Interest Components and Principal Components.

In view of the foregoing and the risks that should be considered in connection with an investment in the

Securities, investors may not be able to sell their Securities readily or at prices that will enable them to

realize their desired return.

In connection with the offering of any issue of Securities, Dealers, Designated Dealers or any other entity

through which such Securities are sold may over-allot or effect transactions that seek to stabilize or

maintain the market price of the Securities at levels above those which might otherwise prevail in the open

market which may include taking a short position in the Securities. Such transactions, if commenced, may

be discontinued at any time.

4

TABLE OF CONTENTS

Page

Documents Incorporated by Reference and Available Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5Summary. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7Risk Factors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13The Farm Credit System . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17Systemwide Debt Securities. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18Terms and Conditions of the Securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

General . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19Bonds. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20Discount Notes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Modifications and Amendments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26Book-Entry System . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27Governing Law . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28Use of Proceeds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28Certain Tax Considerations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

General . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29United States Owners . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29Non-United States Owners . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

Plan of Distribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37Glossary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46Reference Rates Supplement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . S-1

This Offering Circular applies only to Bonds and Discount Notes issued pursuant to OfferingAnnouncements or Term Sheets dated on or after the date hereof. This Offering Circular may be updatedor amended through supplements.

DOCUMENTS INCORPORATED BY REFERENCE AND AVAILABLE INFORMATION

Documents Incorporated by Reference

Important information regarding the Banks and the System, including combined financial information, iscontained in disclosure information made available by the Funding Corporation. This information consistsof the most recent Farm Credit System Annual Information Statement and the most recent Farm CreditSystem Quarterly Information Statement issued after the Annual Information Statement (collectively,“Information Statements”) and certain press releases that relate to financial results or to otherdevelopments affecting the System issued by the Funding Corporation since the publication of the mostrecent Information Statement (the “Press Releases”). The Information Statements, other than the sectionentitled “Description of Debt Securities,” and the Press Releases are incorporated by reference into thisOffering Circular and the information therein is considered to be part of this Offering Circular (suchinformation is referred to herein as the “Incorporated Information”). This Offering Circular should be read

in conjunction with the Incorporated Information. You should rely only on the information incorporated byreference or provided in this Offering Circular, any supplement to this Offering Circular, and the applicableOffering Announcement or Term Sheet for a particular issue of Securities. We have not authorized anyoneelse to provide investors with different information.

Available Information

Neither the Funding Corporation nor the Banks are required to and do not file reports or other informationwith the United States Securities and Exchange Commission.

5

Copies of the Information Statements and Press Releases for the current and two preceding fiscal years, theOffering Circular as amended or supplemented, the Term Sheets for each issue of Bonds hereunder, and acurrent list of the Dealers and Designated Dealers are available without charge by writing or telephoningthe Federal Farm Credit Banks Funding Corporation, Financial Management Division, at 10 ExchangePlace, Suite 1401, Jersey City, New Jersey 07302; Telephone: (201) 200-8000. These documents are alsoavailable from the Dealers. In addition, the Funding Corporation maintains a Web site that posts thesedocuments. The Internet address of the Funding Corporation’s Web site is www.farmcredit-ffcb.com.

Copies of quarterly and annual reports of each Bank and, as applicable, each Bank combined with itsaffiliated Associations (collectively referred to as a District) may be obtained from the individual Bank.Bank addresses and telephone numbers where copies of these documents may be obtained are listed in theInformation Statements. These documents and further information on each Bank and/or District are alsoavailable on each Bank’s Web site as follows:

AgFirst Farm Credit Bank — www.agfirst.com;

AgriBank, FCB — www.agribank.com;

CoBank, ACB — www.cobank.com;

Farm Credit Bank of Texas — www.farmcreditbank.com; and

U.S. AgBank, FCB — www.usagbank.com.

Neither the reports of the Banks nor the information contained on their Web sites is incorporated by

reference into this Offering Circular and you should not consider information contained in those reports

or on those Web sites to be part of this Offering Circular.

We are not making an offer of these Securities in any jurisdiction where such an offer is not permitted. Youshould not assume that the information in this Offering Circular, any supplement to this Offering Circular,or any Offering Announcement or Term Sheet is accurate as of any date other than the respective date onthe front cover of these documents.

6

SUMMARY

This Summary highlights selected information from this Offering Circular and may not contain all of theinformation that you should consider before purchasing any Securities. For a more complete description ofthe Securities, you should read carefully this entire Offering Circular and the documents referred to in“Documents Incorporated by Reference and Available Information,” together with the applicable OfferingAnnouncement or Term Sheet. Terms not defined in this Summary are defined in the Glossary.

ISSUERS . . . . . . . . . . . . . . . . . . . . . . The Banks are instrumentalities of the United States, federallychartered under the Act and are subject to supervision,examination and regulation by the FCA. The Banks are part ofthe Farm Credit System. The System is a federally charterednetwork of borrower-owned lending institutions comprised ofcooperatives and related service organizations. We provide creditand related services nationwide to American farmers, ranchers,producers or harvesters of aquatic products, their cooperatives,and certain farm-related businesses. We also make ruralresidential real estate loans, finance rural communication, energyand water infrastructures, and make loans to support agriculturalexports, and to finance other eligible entities.

FUNDING CORPORATION . . . . . . . The Funding Corporation is a corporation established under thelaws of the United States and acts as agent for the Banks in theissuance of debt securities and related matters.

ISSUE . . . . . . . . . . . . . . . . . . . . . . . . . The Bonds and the Discount Notes (collectively, the“Securities”). The terms and conditions set forth in this OfferingCircular generally apply to the Securities. We will offerSecurities by means of an Offering Announcement or TermSheet that will contain the specific information and the finalterms and conditions for that Security. In the case of anydiscrepancy between the terms and conditions of a Security asdescribed in this Offering Circular and as described in theapplicable Offering Announcement or Term Sheet, you shouldrely on the terms and conditions as described in the OfferingAnnouncement or Term Sheet. In the case of any discrepancybetween the terms and conditions of a Discount Note asdescribed on a nationally recognized financial news service andany electronic order management application system or electronictrading platform of the Funding Corporation, (“Electronic OrderManagement System”), the terms and conditions as described onsuch Electronic Order Management System will take precedence.

Bonds will be offered through a single Dealer or a group of BondDealers through syndication, negotiation or a competitive biddingprocess. Bonds may be offered with fixed rates of interest, withfloating rates of interest or at a discount from the amount to bepaid at maturity with no periodic payments of interest. Thespecific terms and conditions of an issue of Bonds will be setforth in a Term Sheet.

Discount Notes will generally be offered each Business Day.Discount Notes will be offered at a discount from the amount tobe paid at maturity with no periodic payments of interest. The

7

specific terms and conditions of an issue of Discount Notes willbe set forth in an Offering Announcement.

We may discontinue offering Bonds and Discount Notes at any time.

The Securities may also be sold directly by us to investors.

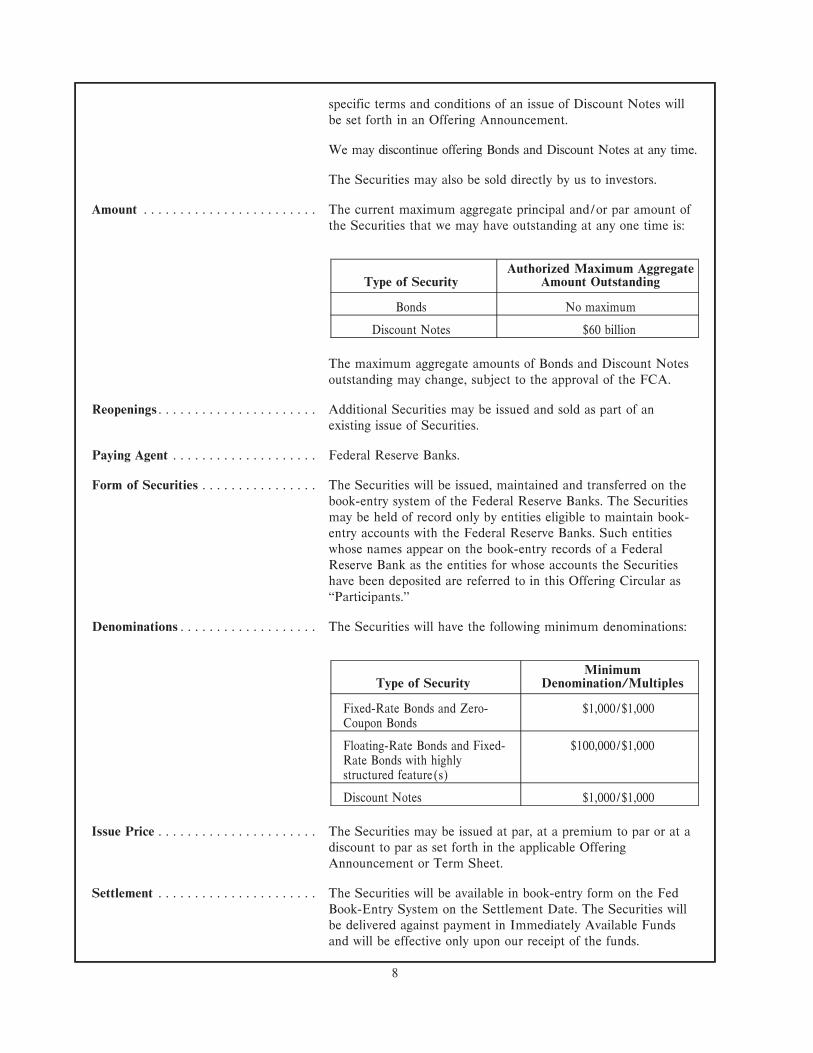

Amount . . . . . . . . . . . . . . . . . . . . . . . . The current maximum aggregate principal and/or par amount ofthe Securities that we may have outstanding at any one time is:

Type of SecurityAuthorized Maximum Aggregate

Amount Outstanding

Bonds No maximum

Discount Notes $60 billion

The maximum aggregate amounts of Bonds and Discount Notesoutstanding may change, subject to the approval of the FCA.

Reopenings . . . . . . . . . . . . . . . . . . . . . . Additional Securities may be issued and sold as part of anexisting issue of Securities.

Paying Agent . . . . . . . . . . . . . . . . . . . . Federal Reserve Banks.

Form of Securities . . . . . . . . . . . . . . . . The Securities will be issued, maintained and transferred on thebook-entry system of the Federal Reserve Banks. The Securitiesmay be held of record only by entities eligible to maintain book-entry accounts with the Federal Reserve Banks. Such entitieswhose names appear on the book-entry records of a FederalReserve Bank as the entities for whose accounts the Securitieshave been deposited are referred to in this Offering Circular as“Participants.”

Denominations . . . . . . . . . . . . . . . . . . . The Securities will have the following minimum denominations:

Type of SecurityMinimum

Denomination/Multiples

Fixed-Rate Bonds and Zero-Coupon Bonds

$1,000/$1,000

Floating-Rate Bonds and Fixed-Rate Bonds with highlystructured feature(s)

$100,000/$1,000

Discount Notes $1,000/$1,000

Issue Price . . . . . . . . . . . . . . . . . . . . . . The Securities may be issued at par, at a premium to par or at adiscount to par as set forth in the applicable OfferingAnnouncement or Term Sheet.

Settlement . . . . . . . . . . . . . . . . . . . . . . The Securities will be available in book-entry form on the FedBook-Entry System on the Settlement Date. The Securities willbe delivered against payment in Immediately Available Fundsand will be effective only upon our receipt of the funds.

8

Interest Rate . . . . . . . . . . . . . . . . . . . . The rates of interest payable on the Securities will be as follows:

Type of Security Interest Rate

Bonds Fixed or Floating Rate ordiscounted from the amountto be paid at maturity

Discount Notes Discounted from the amountto be paid at maturity

The rate of interest or discount will be specified in the applicableOffering Announcement or Term Sheet. The interest rate forFloating-Rate Bonds may be based on one or more of the followingReference Rates as described in the Reference Rates Supplement,which is attached to and is a part of this Offering Circular:

• the Designated Maturity rate for U.S. Treasury Notes;• the London Interbank Offered Rate;• the Federal Funds effective rate;• the U.S. Treasury Bill rate; and• the prevailing commercial banking industry prime loan

rate.

The applicable Term Sheet will indicate the Reference Rate(s)and any Spread. In addition, a Floating-Rate Bond may have amaximum and/or minimum interest rate limitation. Other rates,indices or formulas may be used and will be described in theapplicable Term Sheet.

Interest Payments. . . . . . . . . . . . . . . . . Payments of interest on the Securities will be made as follows:

Bonds — In arrears on the dates specified in the applicable TermSheet and/or on the Maturity Date. No periodic payments ofinterest will be made on Zero-Coupon Bonds.

Interest on Fixed-Rate Bonds will be calculated using a 30/360Day Count Convention. Interest on Floating-Rate Bonds will becalculated using the Day Count Convention specified in thisOffering Circular or in the applicable Term Sheet.

Discount Notes — No periodic payments of interest; a discountfrom the par amount to be paid at maturity will be calculatedbased on the actual number of days from the Issue Date to theMaturity Date based on a 360-day year.

Principal Payments . . . . . . . . . . . . . . . The outstanding principal amount of each Bond, together withany accrued and unpaid interest, and the par amount of eachDiscount Note will be payable as follows:

Type of Security Principal/Par Payment

Bonds Maturity Date orRedemption Date*

Discount Notes Maturity Date

* May be subject to redemption in whole or in part at our option or otherwise asspecified in the Term Sheet.

9

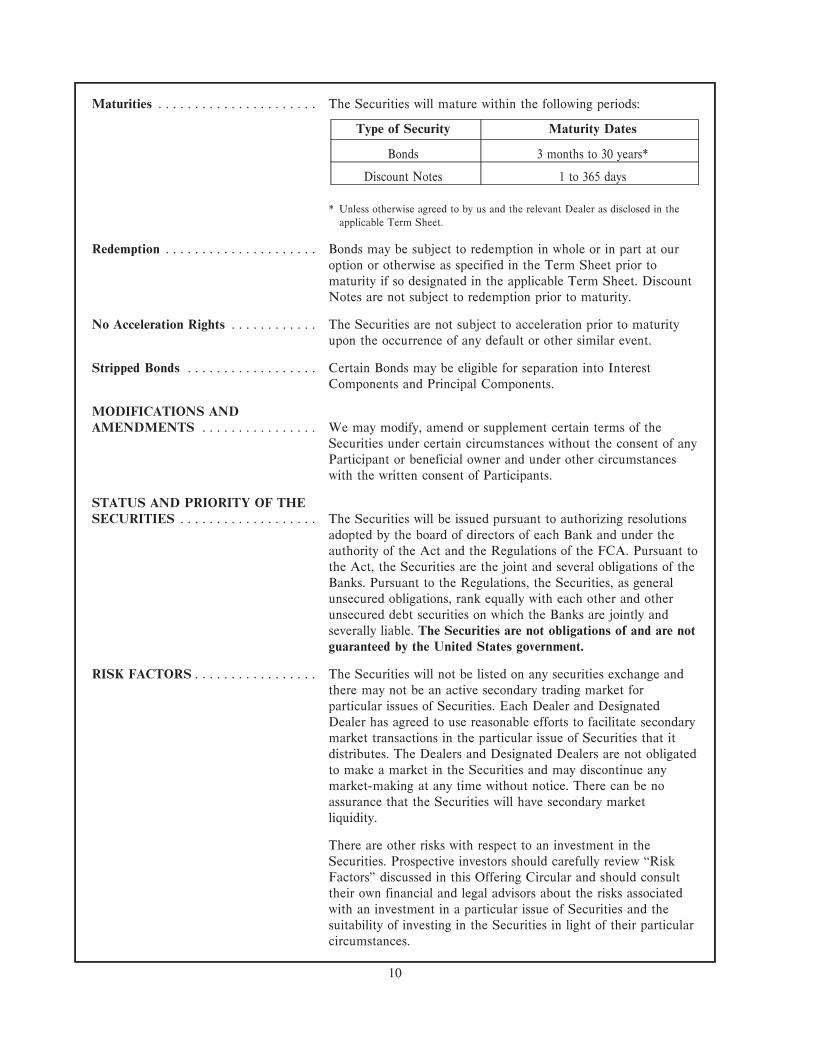

Maturities . . . . . . . . . . . . . . . . . . . . . . The Securities will mature within the following periods:

Type of Security Maturity Dates

Bonds 3 months to 30 years*

Discount Notes 1 to 365 days

* Unless otherwise agreed to by us and the relevant Dealer as disclosed in theapplicable Term Sheet.

Redemption . . . . . . . . . . . . . . . . . . . . . Bonds may be subject to redemption in whole or in part at ouroption or otherwise as specified in the Term Sheet prior tomaturity if so designated in the applicable Term Sheet. DiscountNotes are not subject to redemption prior to maturity.

No Acceleration Rights . . . . . . . . . . . . The Securities are not subject to acceleration prior to maturityupon the occurrence of any default or other similar event.

Stripped Bonds . . . . . . . . . . . . . . . . . . Certain Bonds may be eligible for separation into InterestComponents and Principal Components.

MODIFICATIONS AND

AMENDMENTS . . . . . . . . . . . . . . . . We may modify, amend or supplement certain terms of theSecurities under certain circumstances without the consent of anyParticipant or beneficial owner and under other circumstanceswith the written consent of Participants.

STATUS AND PRIORITY OF THE

SECURITIES . . . . . . . . . . . . . . . . . . . The Securities will be issued pursuant to authorizing resolutionsadopted by the board of directors of each Bank and under theauthority of the Act and the Regulations of the FCA. Pursuant tothe Act, the Securities are the joint and several obligations of theBanks. Pursuant to the Regulations, the Securities, as generalunsecured obligations, rank equally with each other and otherunsecured debt securities on which the Banks are jointly andseverally liable. The Securities are not obligations of and are not

guaranteed by the United States government.

RISK FACTORS . . . . . . . . . . . . . . . . . The Securities will not be listed on any securities exchange andthere may not be an active secondary trading market forparticular issues of Securities. Each Dealer and DesignatedDealer has agreed to use reasonable efforts to facilitate secondarymarket transactions in the particular issue of Securities that itdistributes. The Dealers and Designated Dealers are not obligatedto make a market in the Securities and may discontinue anymarket-making at any time without notice. There can be noassurance that the Securities will have secondary marketliquidity.

There are other risks with respect to an investment in theSecurities. Prospective investors should carefully review “RiskFactors” discussed in this Offering Circular and should consulttheir own financial and legal advisors about the risks associatedwith an investment in a particular issue of Securities and thesuitability of investing in the Securities in light of their particularcircumstances.

10

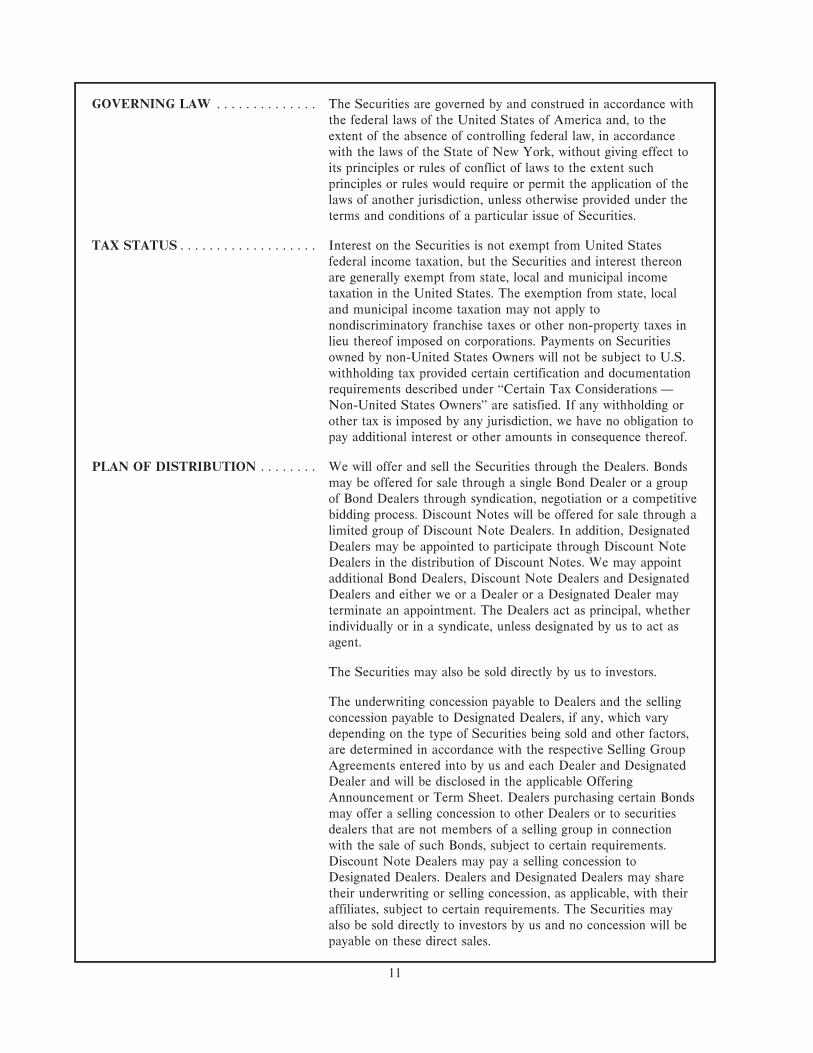

GOVERNING LAW . . . . . . . . . . . . . . The Securities are governed by and construed in accordance withthe federal laws of the United States of America and, to theextent of the absence of controlling federal law, in accordancewith the laws of the State of New York, without giving effect toits principles or rules of conflict of laws to the extent suchprinciples or rules would require or permit the application of thelaws of another jurisdiction, unless otherwise provided under theterms and conditions of a particular issue of Securities.

TAX STATUS . . . . . . . . . . . . . . . . . . . Interest on the Securities is not exempt from United Statesfederal income taxation, but the Securities and interest thereonare generally exempt from state, local and municipal incometaxation in the United States. The exemption from state, localand municipal income taxation may not apply tonondiscriminatory franchise taxes or other non-property taxes inlieu thereof imposed on corporations. Payments on Securitiesowned by non-United States Owners will not be subject to U.S.withholding tax provided certain certification and documentationrequirements described under “Certain Tax Considerations —Non-United States Owners” are satisfied. If any withholding orother tax is imposed by any jurisdiction, we have no obligation topay additional interest or other amounts in consequence thereof.

PLAN OF DISTRIBUTION . . . . . . . . We will offer and sell the Securities through the Dealers. Bondsmay be offered for sale through a single Bond Dealer or a groupof Bond Dealers through syndication, negotiation or a competitivebidding process. Discount Notes will be offered for sale through alimited group of Discount Note Dealers. In addition, DesignatedDealers may be appointed to participate through Discount NoteDealers in the distribution of Discount Notes. We may appointadditional Bond Dealers, Discount Note Dealers and DesignatedDealers and either we or a Dealer or a Designated Dealer mayterminate an appointment. The Dealers act as principal, whetherindividually or in a syndicate, unless designated by us to act asagent.

The Securities may also be sold directly by us to investors.

The underwriting concession payable to Dealers and the sellingconcession payable to Designated Dealers, if any, which varydepending on the type of Securities being sold and other factors,are determined in accordance with the respective Selling GroupAgreements entered into by us and each Dealer and DesignatedDealer and will be disclosed in the applicable OfferingAnnouncement or Term Sheet. Dealers purchasing certain Bondsmay offer a selling concession to other Dealers or to securitiesdealers that are not members of a selling group in connectionwith the sale of such Bonds, subject to certain requirements.Discount Note Dealers may pay a selling concession toDesignated Dealers. Dealers and Designated Dealers may sharetheir underwriting or selling concession, as applicable, with theiraffiliates, subject to certain requirements. The Securities mayalso be sold directly to investors by us and no concession will bepayable on these direct sales.

11

There are restrictions on the sale of the Securities and thedistribution of the offering material relating to the Securities incertain jurisdictions. Each Dealer and Designated Dealer mustdetermine the application of and comply with all relevant lawsand regulations in each jurisdiction in which it purchases, offers,sells or delivers Securities or has in its possession or distributesthis Offering Circular, or any part thereof including any OfferingAnnouncement or Term Sheet, or any such other material.

In connection with the offering of any issue of Securities,Dealers, Designated Dealers or any other entity through whichsuch Securities are sold may over-allot or effect transactions thatseek to stabilize or maintain the market price of the Securities atlevels above those which might otherwise prevail in the openmarket which may include taking a short position in theSecurities. Such transactions, if commenced, may bediscontinued at any time.

12

RISK FACTORS

The following does not describe all the risks and other ramifications of an investment in the Securities. Youshould consult your own financial and legal advisors about risks associated with investing in a particularissue of Securities, should utilize the appropriate tools to analyze that investment and should assess thesuitability of investing in the Securities in light of your particular circumstances. The Securities may not besuitable investments for certain investors. Risks associated with the purchase of the Securities are, ingeneral, similar to those associated with owning other comparable debt securities.

Credit Risk

Our financial condition can be directly impacted by factors affecting the agricultural, rural and othereconomies, since these factors impact the demand for loans and financial services offered by the System andthe ability of System customers to make payments on loans. These factors may include but are not limited to:

• weather-related, disease, and other adverse climatic or biological conditions that impact theagricultural productivity and income of System borrowers;

• changes in production expenses, particularly fuel and fertilizer;

• changes in land values;

• irrigation water availability and cost, and environmental standards;

• availability and cost of agricultural workers;

• changes in United States government support of the agricultural sector, including expenditures onagricultural programs, that may affect the level of income of some System borrowers;

• political, legal, regulatory, financial markets and economic conditions and developments in theUnited States and abroad that can affect such things as the price of commodities or products usedor sold by System borrowers, including the volatility thereof, as well as changes in the relative valueof the U.S. dollar;

• changes in the general economy that can affect the availability of off-farm sources of income andprices of real estate; and

• the development of alternative uses and markets for agricultural commodities, including ethanol andother biofuel production, and the resulting impact on the prices of commodities sold or used bySystem borrowers.

These and certain additional risks impacting the System and our creditworthiness are set forth under “RiskFactors” in the System’s Annual Information Statement and may be set forth in other IncorporatedInformation. In addition to the risks related to our aggregate creditworthiness, the market value of theSecurities will be affected by a number of risks that are independent of our creditworthiness. See theIncorporated Information.

One or more independent credit rating agencies may assign credit ratings to the Securities. The ratings maynot reflect the potential impact of all risks related to the structure of, or the market for, the Securities, orthe additional factors that may impact the Securities. A credit rating is not a recommendation to buy, sellor hold securities and may be revised or withdrawn by the rating agency at any time. In the event a creditrating is assigned to the Securities, it only reflects a particular rating agency’s evaluation of the probabilitythat the Banks will default on the Securities. A credit rating does not reflect the potential impact of risksassociated with an investment in the Securities, including, without limitation, the price, market, liquidity,structure, redemption and other risks associated with the Securities.

Structure Risks

Interest rate risks include risk arising from changes in market rates of interest, spread risk arising fromchanges in the relationship of market yields for the Securities relative to U.S. Treasury issues of similar

13

maturities, and basis risk arising from changes in the relationships of other indices utilized to originallyprice, or to reprice, the Securities. In particular, an investment in an issue of the Securities with interestpayments determined by reference to one or more interest rates or other indices, either directly or inversely,may entail significant risks not associated with an investment in a conventional fixed or floating rate debtsecurity. Changes in an applicable index may not correlate with changes in interest rates generally or withchanges in other indices. Two or more Reference Rates or formulas that may be expected to move intandem or in any other relation to each other may unexpectedly converge or diverge or otherwise not moveas expected. Furthermore, Securities with more complex formulas or other terms may have more volatileperformance results. These risks include but are not limited to:

• the possibility that Reference Rates or applicable indices may be subject to significant changes;

• changes in the applicable indices may not correlate with changes in interest rates or indicesgenerally;

• the resulting interest rate will be less than that payable on a comparable conventional fixed orfloating rate debt security issued by the Banks at the same time;

• no interest will be payable;

• the repayment of principal can occur at times other than that expected by the investor; or

• the possibility that the investor may lose a substantial portion of the principal of a Security(whether payable at maturity, upon redemption or otherwise).

These risks depend on a number of factors, including financial, economic and political events, over whichthe Banks have no control. In addition, if the formula used to determine the amount of interest payablewith respect to an issue of Securities contains a multiple or leverage factor, the effect of any change in aReference Rate may be magnified. Certain Reference Rates and other indices may be highly volatile.Fluctuations in any particular Reference Rate or other index that have occurred in the past are notnecessarily indicative, however, of fluctuations that may occur in the future.

Any redemption (call) feature of an issue of the Securities will affect the market value of the Securities.Since the Banks may be expected to redeem the Securities when prevailing market rates are lower than theinterest rates of certain Securities, an investor might not be able to reinvest the redemption proceeds at aneffective interest rate as high as the interest rate on the redeemed Securities.

If the rate of interest on a Floating Rate Bond includes a maximum (cap) interest rate limitation, theinterest payable on that Bond may be less than that payable on a conventional Floating Rate Bond issuedby us without such cap. Two issues of Securities issued at the same time and with interest rates determinedby reference to the same applicable Reference Rate or index and otherwise comparable terms andconditions may have different interest rates and yields when issued or thereafter if the frequency of eachissue’s interest rate adjustments is different.

In order to hedge their exposure to certain of the foregoing risks in connection with any particular issue ofSecurities, one or more of the Banks may enter into interest rate swaps or other hedging transactions with, orarranged by, a Dealer or Designated Dealer participating in the issuance, an affiliate of the Dealer or DesignatedDealer or an unrelated third party. The Dealer, Designated Dealer or other party may receive compensation,trading gain or other benefits in connection with the hedging transactions. The interest rate swaps or otherhedging transactions may reference the Securities, other obligations of the Banks or obligations of other issuers.

Investors in certain Securities should have knowledge of and access to appropriate analytical tools toanalyze quantitatively the effect (or value) of any redemption, cap or floor, or certain other features of theSecurities, and the resulting impact on the value of the Securities.

Secondary Market Risks

The Securities will not be listed on any securities exchange. Generally, there is an active secondary marketfor Discount Notes and certain Bonds. However, other Bonds may not have an established trading market

14

upon issuance. Each Dealer and Designated Dealer has agreed to use reasonable efforts to facilitatesecondary market transactions in the Securities. Although the Dealers and Designated Dealers may make amarket in the Securities, they are not obligated to do so and may discontinue any market-making at anytime without notice. The Dealers and Designated Dealers have agreed to advise us promptly of any materialdevelopment known to them in the secondary market for the Securities. The Dealers and DesignatedDealers have also agreed to advise us promptly of their decision to withdraw from secondary market-makingin the Securities. However, there can be no assurance that the Securities will have secondary marketliquidity. As a result, an investor may not be able to sell its Securities easily or at prices that will provide ayield comparable to similar investments that have a developed and liquid secondary market.

To the extent the Securities have secondary market liquidity, the secondary market for the Securities willbe affected by a number of factors independent of our creditworthiness and the level of any applicable indexor indices, which may include:

• the complexity and volatility of Reference Rates or indices;

• the method of calculating the principal or any interest to be paid on the Securities;

• the time remaining to the maturity of the Securities;

• the outstanding amount of the Securities;

• any redemption feature of the Securities;

• the amount of other Securities linked to the index or indices; or

• the level, direction and volatility of market interest rates generally.

These factors also will affect the market value of the Securities. In addition, certain Securities may be designedfor specific investment objectives or strategies and therefore may have a more limited secondary market andexperience more price volatility than conventional debt securities. Investors may not be able to sell theSecurities readily or at prices that will enable investors to realize their anticipated yield. You should notpurchase the Securities unless you understand and are able to bear the risk that certain Securities may not bereadily saleable, that the value of the Securities may fluctuate over time and that the fluctuations may besignificant.

The prices of structured securities and Zero-Coupon Bonds, as well as other instruments issued at asubstantial discount from their principal amount payable at maturity, generally tend to fluctuate in thesecondary markets more in relation to general changes in interest rates than do such prices for conventionalinterest-bearing securities of comparable maturities.

Factors That Could Adversely Affect the Trading Value and Yield of the Securities

Fixed/Floating Rate Securities

Fixed/floating rate Securities may bear interest at a rate that we may elect to convert from a fixed rate to afloating rate, or from a floating rate to a fixed rate. Our ability to convert the interest rate will affect thesecondary market and the market value of the Securities since we may be expected to convert the ratewhen it is likely to produce a lower overall cost of borrowing. If we convert from a fixed rate to a floatingrate, the Spread on the fixed/floating rate Securities may be less favorable than the prevailing spreads onour comparable floating rate debt securities tied to the same Reference Rate. In addition, the new floatingrate at any time may be lower than the rates on other Securities. If we convert from a floating rate to afixed rate, the fixed rate may be lower than the prevailing rates on the Securities.

Securities Eligible for Stripping

Some issues of fixed rate Securities and Step Rate Securities will be eligible to be separated (“stripped”)into Interest Components and Principal Components. The secondary market, if any, for the Componentsmay be more limited and less liquid than the secondary market for Securities of the same issue that have

15

not been stripped. The liquidity of an issue of Securities also may be reduced if a significant portion of theSecurities are stripped. See “Eligibility for Stripping” for more information on stripping.

Securities Issued at a Substantial Discount or Premium

The market values of Securities issued at a substantial discount or premium from their principal amounttend to fluctuate more in relation to general changes in interest rates than prices for conventional interest-bearing securities. Generally, the longer the remaining term of the Securities, the greater the price volatilityas compared to conventional interest-bearing Securities with comparable maturities. As a result, the marketvalues of Discount Notes, Zero-Coupon Bonds, Interest Components and some Principal Components couldbe subject to substantial fluctuation.

Legality of Investment

Each investor should consult its own legal advisors in determining whether and to what extent theSecurities constitute legal investments for that investor and whether and to what extent the Securities canbe used as collateral for various types of borrowings. In addition, financial institutions should consult theirlegal advisors or regulators in determining the appropriate treatment of the Securities under any applicablerisk-based capital or similar rules.

Investors whose investment activities are subject to legal investment laws and regulations or to review orregulation by certain authorities may be subject to restrictions on investments in certain types of debtsecurities, which may include some or all of the Securities. Investors should review and consider thoserestrictions prior to investing in the Securities. In addition, any investor that is subject to the regulatoryjurisdiction of any government agency should review and consider the applicability of rules, guidelines,regulations and policy statements adopted by its regulators prior to purchasing or pledging the Securities.

Suitability

Investors in any particular issue of Securities should have sufficient knowledge and experience in financialand business matters to evaluate the Securities, the merits and risks of investing in the Securities and theinformation contained and incorporated by reference in the Offering Circular, any Offering Announcementor Term Sheet or any supplement or amendment to this Offering Circular. In addition, investors shouldhave access to, and knowledge of, appropriate analytical tools to evaluate, in the context of the investor’sfinancial situation, the Securities, the merits and risks of investing in the Securities and the impact theSecurities will have on their overall investment portfolio. Not every Security is suitable for every investor.You should not purchase a Security unless you understand and have sufficient financial resources to bearthe price, yield, market, liquidity, structure, redemption and other risks associated with the Security. Youalso should not purchase any Security without sufficient experience, financial resources and liquidity,relative to the potential risks, to manage your investments, including your investment in the Security.Before purchasing any Security, you should understand thoroughly the terms and conditions of the Security,be familiar with the behavior of the relevant financial markets, and consider (possibly with the assistance ofa financial advisor) possible scenarios for economic, interest rate and other factors that may affect yourinvestment and your ability to bear the associated risks under a variety of such scenarios. You also shouldconsider and understand any legal restrictions that may apply to your investments in the Securities. See“Risk Factors — Legality of Investment.”

Certain Securities are complex financial instruments. Sophisticated institutional investors generally do notpurchase complex Securities as stand-alone investments, but rather as a means of reducing risk orenhancing yield with an understood, measured, appropriate addition of risk to their overall portfolio.Investors in the Securities should possess the expertise, either alone or with a financial advisor, to evaluatethe manner in which the Securities will perform under changing conditions, the resulting effects on theirvalue, and the impact any investment in the Securities will have on the investor’s overall investmentportfolio.

16

THE FARM CREDIT SYSTEM

Overview

The System is a federally chartered network of borrower-owned lending institutions comprised of cooperativesand related service organizations. Cooperatives are organizations that are owned and controlled by theirmembers who use the cooperative’s products or services. The U.S. Congress authorized the creation of thefirst System institutions in 1916. Our mission is to provide sound and dependable credit to American farmers,ranchers, producers or harvesters of aquatic products, their cooperatives, and certain farm-related businessesin all 50 states, the Commonwealth of Puerto Rico and, under conditions set forth in the Act, U.S. territories.Consistent with our mission of serving rural America, we also make rural residential real estate loans, financerural communication, energy and water infrastructures, and make loans to support agricultural exports and tofinance other eligible entities. System institutions may also provide a variety of services to their borrowers,including credit and mortgage life insurance, disability insurance, various types of crop insurance, estateplanning, record keeping services, tax planning and preparation, cash management products and services, andconsulting. In addition, some System institutions also provide leasing and related services to their customers.

Congress established the FCA as the System’s independent federal regulator to examine and regulateSystem institutions, including their safety and soundness. System institutions are federal instrumentalities.

Structure/Ownership

The Associations are cooperatives owned by their borrowers, and the Farm Credit Banks (AgFirst, AgriBank,Texas and U.S. AgBank) are cooperatives primarily owned by their affiliated Associations. The AgriculturalCredit Bank (CoBank) is a cooperative principally owned by cooperatives, other eligible borrowers and itsaffiliated Associations. The Banks and Associations each have their own board of directors and are notcommonly owned. Each Bank and Association manages and controls its own business activities, operationsand financial performance. Systemwide Debt Securities are the general unsecured joint and several obligationsof the Banks and are not the direct obligations of the Associations. As a result, the capital of the Associationsmay not be available to support principal or interest payments on Systemwide Debt Securities.

The Banks jointly own the Funding Corporation. The Funding Corporation, as agent for the Banks, issues andmarkets Systemwide Debt Securities in order to raise funds for the lending activities and operations of theBanks and Associations. The Funding Corporation also provides the Banks with certain consulting, accountingand financial reporting services, including the preparation of the System’s Quarterly and Annual InformationStatements and the combined financial statements contained in those information statements. As theSystem’s financial spokesperson, the Funding Corporation is primarily responsible for financial disclosure andthe release of public information concerning the financial condition and performance of the System.

Funding

The System obtains funds for its lending operations primarily from the sale of Systemwide Debt Securities,including the Securities. Each issuance of Systemwide Debt Securities must be approved by the FCA andeach Bank’s participation is subject to:

• the availability of specified eligible assets (referred to in the Act as “collateral” as describedbelow);

• compliance with the conditions of participation as prescribed in an agreement among the Banks andthe Funding Corporation; and

• determinations by the Funding Corporation of the amounts, maturities, rates of interest and termsof each issuance.

The summaries in this Offering Circular of certain provisions of the Act, the Regulations and the Securitiesdo not purport to be complete and are qualified in their entirety by reference to the provisions of the Actand the Regulations.

17

SYSTEMWIDE DEBT SECURITIES

General

Systemwide Debt Securities, including the Securities, will be issued by us pursuant to authorizingresolutions adopted by the boards of directors of each Bank and under the authority of the Act and theRegulations. Pursuant to the Act, the Banks are jointly and severally liable on the Securities and all otherSystemwide Debt Securities. Pursuant to the Regulations, the Securities, as unsecured debt obligations,rank equally with each other and with other unsecured Systemwide Debt Securities.

The Securities are not subject to acceleration prior to maturity upon the occurrence of any default orsimilar event. Certain Securities may be subject to redemption in whole or in part by us prior to maturity asdiscussed below. The Securities will not be issued under an indenture and no trustee is provided withrespect to the Securities.

We may at any time purchase Securities at any price or prices in the open market or otherwise. TheseSecurities may be held, resold or canceled by us.

The outstanding principal amount of any issue of Securities may be increased without the consent of anyParticipant or beneficial owner of the Securities by issuing additional Securities with the same terms andconditions (other than the Issue Price, the Issue Date and the Settlement Date, which may vary).Securities may be reopened one or more times on or following the Issue Date at any time there is arequisite investor demand and the reopening is consistent with the Banks’ funding needs. The evaluation ofthese criteria and, consequently, the decision whether to reopen an issue of Securities will be at our solediscretion. There is no assurance that any issue of Securities will be reopened, or, if reopened, in whatadditional principal amounts.

The Securities are not obligations of and are not guaranteed by the United States government. They are

solely the joint and several obligation of the Banks.

Insurance Fund

As more fully described in the Information Statements, the timely payment of principal and interest onSystemwide Debt Securities is insured by the Insurance Corporation to the extent provided in the Act. TheInsurance Corporation maintains the Insurance Fund for this purpose and for certain other purposes. In theevent a Bank is unable to timely pay principal or interest on any insured debt obligation (as defined in theAct) for which that Bank is primarily liable, the Insurance Corporation must expend amounts in theInsurance Fund to the extent available to insure the timely payment of principal and interest on the debtobligation. The provisions of the Act providing for joint and several liability of the Banks on the debtobligation cannot be invoked until all amounts in the Insurance Fund have been exhausted. However,because of other mandatory and discretionary uses of the Insurance Fund, there is no assurance that therewill be sufficient funds to pay the principal or interest on the insured debt obligation.

The insurance provided through use of the Insurance Fund is provided solely by the Insurance Corporation

and is not an obligation of and is not a guarantee by the United States government.

Joint and Several Liability

The Banks are jointly and severally liable for the payment of principal and interest on Systemwide DebtSecurities. If a Bank is unable to pay the principal or interest on a Systemwide Debt Security and if theamounts in the Insurance Fund have been exhausted, the FCA is required to make calls on all non-defaulting Banks to satisfy the liability. These calls would be in the proportion that each non-defaultingBank’s “available collateral” (“available collateral” is collateral in excess of the aggregate of the Bank’s“collateralized” obligations) bears to the aggregate available collateral of all non-defaulting Banks. If thesecalls were not sufficient to satisfy the liability, then a further call would be made in proportion to each non-defaulting Bank’s remaining assets. In making a call on non-defaulting Banks with respect to a SystemwideDebt Security issued on behalf of a defaulting Bank, the FCA is required to appoint the Insurance

18

Corporation as the receiver for the defaulting Bank. The receiver would be required to expeditiouslyliquidate the Bank.

Collateral

As a condition of a Bank’s participation in the issuance of Systemwide Debt Securities, the Bank musthave, and at all times thereafter maintain, free from any lien or other pledge, specified eligible assets(referred to in the Act as “collateral”) at least equal in value to the total amount of outstanding debtsecurities of the Bank that are subject to the collateral requirement. These securities include SystemwideDebt Securities for which the Bank is primarily liable and investment bonds or other debt securities thatthe Bank has issued individually, except for subordinated debt. The collateral must consist of notes andother obligations representing loans or real or personal property acquired in connection with loans madeunder the authority of the Act (valued in accordance with the Regulations and FCA directives), obligationsof the United States or any agency thereof direct or fully guaranteed, other FCA-approved Bank assets,including eligible marketable securities, or cash. These collateral requirements do not provide holders ofSystemwide Debt Securities with a security interest in any assets of the Banks. The Banks may in thefuture issue Systemwide Debt Securities that are secured by specific assets.

While the collateral requirement limits the circumstances under which Systemwide Debt Securities may beissued by the Banks, as described above, unless specifically provided under the terms of a particular issue,Systemwide Debt Securities will not impose any additional limit on other indebtedness or securities thatmay be incurred or issued by the Banks and will contain no financial or similar restrictions on the Banks.

Status in Liquidation

The Regulations provide that in the event a Bank is placed in liquidation, holders of Systemwide DebtSecurities have claims against the Bank’s assets, whether or not the holders file individual claims. Theclaims of these holders are junior to claims related to costs incurred by the receiver in connection with theadministration of the receivership, claims for taxes, claims of secured creditors and claims of holders ofbonds, including investment bonds, issued by the Bank individually, to the extent the bonds arecollateralized in accordance with the requirements of the Act. Further, claims of holders of SystemwideDebt Securities are senior to all claims of general creditors. If particular Systemwide Debt Securities wereoffered on a secured basis, the holders of these obligations would have the priority accorded securedcreditors of the liquidating Bank. To date, we have not issued secured Systemwide Debt Securities.

TERMS AND CONDITIONS OF THE SECURITIES

References in these Terms and Conditions to terms and conditions specified for a particular issue ofSecurities include references to terms and conditions specified in the applicable Offering Announcement orTerm Sheet issued with respect to such issue of Securities.

General

The following terms and conditions apply generally to the Securities. The Offering Announcement or TermSheet for each issue of Securities will contain the specific information related to that Security and maycontain additional or different terms and conditions for that Security. It is important to consider theinformation in this Offering Circular and the applicable Offering Announcement or Term Sheet in makingan investment decision. In the case of any discrepancy between the terms and conditions of a particularSecurity as described in this Offering Circular and as described in the applicable Offering Announcementor Term Sheet, you should rely on the terms and conditions as described in the Offering Announcement orTerm Sheet. If a particular Security is described in both an Offering Announcement and a Term Sheet, theterms and conditions as described in the Term Sheet will take precedence in the event of any discrepancy.Term Sheets will be issued for all Bonds. The Term Sheet will be provided to the investor by the Dealerthrough which the Bond was purchased or by the Funding Corporation in the case of a Security solddirectly by it. Offering Announcements will be issued for Discount Notes. The Offering Announcement will

19

appear on a nationally recognized financial information service (such as Bloomberg). In the case of anydiscrepancy between the terms and conditions of a Discount Note as described on a nationally recognizedfinancial information service and on any Electronic Order Management System, the terms and conditions asdescribed on the Electronic Order Management System will take precedence.

Bonds

Bonds will be issued with Maturity Dates of not less than three months nor more than 30 years from theIssue Date, unless otherwise specified. Currently, there is no maximum aggregate principal amount ofBonds the Banks may have outstanding at any one time. We may limit the amount outstanding at any time,subject to the approval of the FCA. If we impose such limits, we will report such limits in a supplement tothis Offering Circular. The types of Bonds which may be offered are:

• Fixed-Rate Bonds

• Floating-Rate Bonds

• Zero-Coupon Bonds

In addition, we may offer other types of Bonds which will be described in supplements to this OfferingCircular or in a Term Sheet.

Form and Denomination

Bonds will be issued, maintained and transferred on the Fed Book-Entry System, as described below under“Book-Entry System.” The Bonds will be issued, maintained and transferred only in the following minimumdenominations:

• Fixed-Rate Bonds and Zero-Coupon Bonds — minimum denominations of $1,000 and increased inintegral multiples of $1,000.

• Floating-Rate Bonds and Fixed-Rate Bonds with highly structured feature(s)(as determined by theFunding Corporation) — minimum denominations of $100,000 and increased in integral multiplesof $1,000.

Settlement

Settlement of the Bonds will occur on the Issue Date or such other date as may be agreed to by us and theDealer (i.e., the scheduled Settlement Date). Settlement of the Bonds will be effected by payment of theIssue Price for the Bonds, less the Dealer’s underwriting concession, if any. See “Plan of Distribution.” TheIssue Price of a Bond will be 100% of its principal amount or such other percentage of the principal amountof the Bond as is set forth in the applicable Term Sheet. Bonds will be delivered against payment on theSettlement Date in Immediately Available Funds and will be effected only upon our receipt of funds. See“Book-Entry System.”

Payment of Principal and Interest

General. Payment of the principal and interest on the Bonds will be made on the applicable paymentdates to Participants of the Bonds as of the close of the Business Day preceding the payment dates by thecredit of the payment amount to the Participants’ accounts at the Federal Reserve Banks. The Participantand each other financial intermediary in the chain to the beneficial owner will have the responsibility ofremitting payments for the accounts of their customers.

In any case in which an Interest Payment Date, a Redemption Date, the Maturity Date or other paymentdate is not a Business Day, payment of interest or principal, as the case may be, will be made on the nextsucceeding Business Day and will be treated as if paid on the originally scheduled date.

20

Payment of Interest. Payments of interest will be made on the Interest Payment Date(s) as specified inthe applicable Term Sheet as follows:

• Generally, interest on Fixed-Rate Bonds with maturities of less than one year will be payable on theMaturity Date of the Bonds. Interest on Fixed-Rate Bonds with maturities of one year or longergenerally will be payable semi-annually in arrears on the Interest Payment Dates specified in theTerm Sheet for the Bonds and on the Maturity Date. These Bonds will bear interest from andincluding their Issue Date to but excluding their Maturity Date at an annual fixed interest rate asspecified in the applicable Term Sheet. Interest will be computed using a 30/360 Day CountConvention.

• Interest on Floating-Rate Bonds will be payable in arrears on the Interest Payment Dates specifiedin the applicable Term Sheet for the Bonds and on the Maturity Date. These Bonds will bearinterest from and including their Issue Date to but excluding their Maturity Date based on theirReference Rate or formula as specified in the applicable Term Sheet. Interest will be computed asdiscussed below with respect to each type of Floating-Rate Bond.

• Zero-Coupon Bonds will be sold at a discount from the amount to be paid at maturity with noperiodic payments of interest.

Interest payments on the Bonds will include interest accrued from and including the Issue Date or the mostrecent Interest Payment Date to or for which interest has been paid or duly provided, to but excluding thenext succeeding Interest Payment Date.

Payment of Principal. The outstanding principal amount of each Bond, together with interest accrued andunpaid thereon, will be paid on the Maturity Date, unless designated as Redeemable Bonds or OptionalPrincipal Redemption Bonds. All of the principal amount of Redeemable Bonds and all or a portion of theprincipal amount of Optional Principal Redemption Bonds may be paid prior to the Maturity Date at ouroption or as otherwise specified in the Term Sheet in accordance with the terms and conditions of theBonds.

Interest Rates

Bonds may be offered with interest payable at fixed rates (Fixed-Rate Bonds), with interest payable atfloating rates (Floating-Rate Bonds) or with no periodic interest payments (Zero-Coupon Bonds). Thefloating rate of interest will be calculated pursuant to the Reference Rates set forth below unless otherwiseagreed to by us and the Dealer.

Fixed-Rate Bonds. The fixed rate of interest will be as specified in the applicable Term Sheet. There maybe one fixed rate of interest for the life of the Bond or there may be more than one fixed rate of interest,each for a specified period during the life of the Bond, but in no event will there be more than one fixedrate of interest in effect for a specific Interest Period. Bonds for which there is more than one fixed rate ofinterest will be designated as “Step Rate Bonds” in the Term Sheet relating to the Bonds.

Floating-Rate Bonds. The floating rate of interest will be determined by reference to a specified index rate(a Reference Rate) or to an interest rate formula based on one or more of the following Reference Rates,as specified in the applicable Term Sheet:

• the Designated Maturity rate for U.S. Treasury Notes (“Treasury Rate”);

• the London Interbank Offered Rate (“LIBOR”);

• the Federal Funds effective rate (“Federal Funds Effective Rate”);

• the U.S. Treasury Bill rate (“T-Bill Rate”); and

• the prevailing commercial banking industry prime loan rate (“Prime Rate”).

21

A floating rate of interest based on a Reference Rate that is not described in the Reference RatesSupplement which is attached to and a part of this Offering Circular will be described in a supplement tothis Offering Circular or in the Term Sheet relating to that Bond.

The applicable Term Sheet will also indicate any Spread. In addition, Floating-Rate Bonds may have amaximum and/or minimum rate of interest which may accrue and be payable for the relevant InterestPeriod(s).

Adjustments. Any adjustment to the rate of interest on a Floating-Rate Bond on a Reset Date will beeffective as of that Reset Date to but excluding the next Reset Date, except that during the Rate Cut-OffPeriod the rate of interest will be the rate in effect on the relevant Calculation Date. Amounts to be paid onan Interest Payment Date, a Redemption Date or the Maturity Date will be calculated on the CalculationDate.

Accrued Interest Calculation. The accrued interest for all Bonds will be calculated by multiplying theprincipal amount of the Bond by an accrued interest factor.

An Actual/Actual Day Count Convention will be used to calculate the accrued interest factor on any dayfor a Bond by:

(1) determining the interest rate applicable to each day on which the Bond has been outstandingduring the period from and including the later of the Issue Date or the last date to or for whichinterest has been paid or duly provided, to but excluding the date as of which the accrued interestfactor is being computed;

(2) calculating for each such day the quotient equal to (A) the interest rate applicable to such daydivided by (B) the number of days in the calendar year in which such day falls; and

(3) determining the sum of the quotients calculated pursuant to clause (2) above.

An Actual/360 Day Count Convention will be used to calculate the accrued interest factor on any day for aBond by:

(1) adding the interest rates applicable to each day on which the Bond has been outstanding duringthe period from and including the later of the Issue Date or the last date to or for which interesthas been paid or duly provided, to but excluding the date as of which the accrued interest factor isbeing computed; and

(2) dividing the sum by 360.

A 30/360 Day Count Convention will be used to calculate the accrued interest factor on any day for aBond by:

(1) adding the interest rates applicable to each day on which the Bond has been outstanding duringthe period from and including the later of the Issue Date or the last date to or for which interesthas been paid or duly provided, to but excluding the date as of which the accrued interest factor isbeing computed (it being understood that for purposes of this calculation all months consist of30 days); and

(2) dividing the sum by 360.

Where to Obtain Current Rate of Interest. Information concerning the current rate of interest on aFloating-Rate Bond and the relevant accrued interest factor is available by calling the FundingCorporation’s Securities Operations Division at (201) 200-8000; this information is also available on theFunding Corporation’s Web site at www.farmcredit-ffcb.com.

Redemption

The Bonds will not be subject to redemption prior to maturity, unless designated as Redeemable Bonds orOptional Principal Redemption Bonds.

22

Redeemable Bonds may be redeemed (called), at our option, in whole, on any day as specified in theapplicable Term Sheet. Generally, the redemption price will be 100% of the principal amount and theredemption payment will be in addition to the interest due on the Redemption Date.

Optional Principal Redemption Bonds may be redeemed (called), at our option, in whole or in part, on anyday or days as specified in the applicable Term Sheet. In the event of a partial redemption, a pro rataportion of the then outstanding principal amount will be redeemed. Generally, the redemption price will be100% of the principal amount to be redeemed. The redemption payment, which will be in addition to theinterest due on the Redemption Date, will be derived by multiplying:

(1) the principal amount outstanding prior to the first call by

(2) the difference between the Current Factor in effect prior to the redemption and the CurrentFactor in effect following the redemption.