Federal Deposit Insurance Corporation Options Paper August 2000

87

i Federal Deposit Insurance Corporation Options Paper August 2000 Table of Contents I. INTRODUCTION ..................................................................................................................... 1 The Need for Reform........................................................................................................................... 2 How Should the FDIC Price Risk? .................................................................................................. 3 How Should New Deposits be Treated? .......................................................................................... 4 How Should Losses be Funded? ...................................................................................................... 5 How Should the Coverage Levels be Determined? ......................................................................... 5 Overview of Options Paper ................................................................................................................. 6 Review Process and Comments on Options Paper .............................................................................. 7 II. PRICING DEPOSIT INSURANCE FOR INDIVIDUAL BANKS....................................... 9 Textbox: Oliver, Wyman & Company Approach to Bank Level Pricing .................................... 9 Options Relying on Supervisory Evaluations .................................................................................... 12 Options Relying on Objective Factors............................................................................................... 14 Non-Public Bank-Specific Information ......................................................................................... 14 Bank Call Reports .......................................................................................................................... 16 Market Information........................................................................................................................ 17 Hybrid Approaches ............................................................................................................................ 20 Customized Financial Contracts ........................................................................................................ 20 III. FUNDING DEPOSIT INSURANCE LOSSES ..................................................................... 22 User Fee Model ................................................................................................................................. 23 Long-Term Premium Rates Based on Historical Experience ........................................................ 23 Moving Average Approach ........................................................................................................... 24 Analytical Approaches................................................................................................................... 25 Textbox: Oliver, Wyman & Company Analytical Framework................................................. 25 Adjustments for Current Insurance Expenses ............................................................................... 27 Linking Premium Rates to the Insurance Fund ............................................................................. 27

Transcript of Federal Deposit Insurance Corporation Options Paper August 2000

i

Federal Deposit Insurance Corporation

Options Paper

August 2000

Table of Contents

I. INTRODUCTION ..................................................................................................................... 1

The Need for Reform........................................................................................................................... 2How Should the FDIC Price Risk?.................................................................................................. 3How Should New Deposits be Treated?.......................................................................................... 4How Should Losses be Funded?...................................................................................................... 5How Should the Coverage Levels be Determined?......................................................................... 5

Overview of Options Paper ................................................................................................................. 6

Review Process and Comments on Options Paper .............................................................................. 7

II. PRICING DEPOSIT INSURANCE FOR INDIVIDUAL BANKS....................................... 9

Textbox: Oliver, Wyman & Company Approach to Bank Level Pricing .................................... 9

Options Relying on Supervisory Evaluations.................................................................................... 12

Options Relying on Objective Factors............................................................................................... 14Non-Public Bank-Specific Information......................................................................................... 14Bank Call Reports.......................................................................................................................... 16Market Information........................................................................................................................ 17

Hybrid Approaches............................................................................................................................ 20

Customized Financial Contracts ........................................................................................................ 20

III. FUNDING DEPOSIT INSURANCE LOSSES ..................................................................... 22

User Fee Model ................................................................................................................................. 23Long-Term Premium Rates Based on Historical Experience........................................................ 23Moving Average Approach ........................................................................................................... 24Analytical Approaches................................................................................................................... 25 Textbox: Oliver, Wyman & Company Analytical Framework................................................. 25Adjustments for Current Insurance Expenses ............................................................................... 27Linking Premium Rates to the Insurance Fund ............................................................................. 27

ii

Textbox: Solvency Standard – Oliver, Wyman & Company.................................................... 29Setting a Hard Target for the Insurance Fund ............................................................................... 29Setting a Soft Target for the Insurance Fund................................................................................. 30

Mutual Model .................................................................................................................................... 30Rebates........................................................................................................................................... 30Banks Hold Explicit Claims on the Mutual Insurance Fund ......................................................... 31Introducing Private Sector Features to the Deposit Insurance System.......................................... 32

Funding Systemic Risk...................................................................................................................... 33

IV. COVERAGE LIMITS............................................................................................................. 35

Past and Current Coverage Rules ...................................................................................................... 36

Effects of Changing Coverage.......................................................................................................... 37Immediate Effect ........................................................................................................................... 37Longer-Term Effect ....................................................................................................................... 38

Moral Hazard, Implicit Protection and Industry Structure ................................................................ 41

Options............................................................................................................................................... 44Status Quo...................................................................................................................................... 44Formal Indexing ............................................................................................................................ 45Simplification ................................................................................................................................ 46Additional Coverage for Municipal and Other Public Deposits.................................................... 46Optional Excess Coverage............................................................................................................. 48

V. NEXT STEPS ........................................................................................................................... 50

VI. REFERENCES ........................................................................................................................ 51

VII. ATTACHMENTS.................................................................................................................... 53

A. THE BIF AND SAIF SHOULD BE MERGED........................................................................... 53

B. CDIC-LIKE SCORING SYSTEMS............................................................................................. 56B-1. The CDIC System................................................................................................................. 56B-2. CDIC-Style Hybrid Approach .............................................................................................. 57

C. OVERVIEW OF THE RISK-BASED PREMIUM SYSTEM ..................................................... 60

D. DIFFERENTIATING AMONG A-RATED INSTITUTIONS .................................................... 62D-1. Using Prompt Corrective Action Capital Ratios to Distinguish the Risk of Institutionswithin a Capital Subgroup ............................................................................................................. 62D-2. Peer Group Comparisons...................................................................................................... 65D-3. Historical Benchmarks ......................................................................................................... 66

iii

E. EXPECTED LOSS PRICING....................................................................................................... 67E-1. Incorporating Credit Rating Agency Information in Deposit Insurance Pricing.................. 67E-2. Using Default Risk Premiums on Subordinated Debt To Estimate Banking OrganizationExpected Loss................................................................................................................................ 70E-3. Proportion of Insurance Loss Borne by the FDIC ................................................................ 72

F. SIMULATIONS............................................................................................................................ 74F-1. Steady Premium System ....................................................................................................... 74F-2. Simulation of Risk-Related Premiums, 1982 to 1999........................................................... 75F-3. Optimal Fund Size and Premium Adjustment Simulations .................................................. 79

G. EFFECT OF A COVERAGE LIMIT INCREASE TO $200,000 ON BANKS OF DIFFERENTASSET SIZES ................................................................................................................................... 83

1

I. INTRODUCTION

This options paper is part of a comprehensivereview of the U.S. deposit insurance system bythe Federal Deposit Insurance Corporation(FDIC). We are undertaking this review toassure the ability of the system to meet itsresponsibilities over the next decade. Industryconsolidation, expanded activities, global-ization and the use of technology haveadvanced the business of banking and theproducts and services offered to Americandepositors. The FDIC wants to ensure that thedeposit insurance system continues to protectdepositors and contributes to its full extent tothe stability of the banking system.

The United States has the oldest federal depositinsurance system in the world, established in1934 to put an end to the devastating bank runsthat shut down businesses and contributed tothe Great Depression. The system proved to bea success; following its introduction, depositinsurance restored public confidence in thebanking system. For the next threegenerations, the system served its purpose byhelping prevent banking problems frombecoming banking panics. In the 1980s, whenhundreds of banks and thrifts failed, depositinsurance acted as the anchor for publicconfidence in the banking system.

In good times and bad times, deposit insuranceprovides a safe and certain place for people toput their money. By eliminating the disruptioncaused by bank runs, deposit insurancecontributes to the foundation necessary for arobust banking system and by extension, adynamic financial system. In turn the generaleconomy benefits from the stabilizing influenceof deposit insurance.

The success of the U.S. system of federaldeposit insurance is particularly evident incontrasting the U.S. experience during the1980s crisis with recent crises in Asian and

Latin American countries that lacked explicitdeposit insurance systems. During the U.S.crisis, there were no depositor runs on banks,and bank failures were resolved through a well-established, orderly process. This was not thecase for countries without explicit depositinsurance, and it is perhaps sufficient to notethat more than 30 countries chose to implementnew, explicit deposit insurance systems duringthe 1990s. The benefits of deposit insuranceare appreciated worldwide, and the U.S. systemhas become a model for the rest of the world.

Nevertheless, the 1980s crisis in the U.S. alsoprovides a sobering reminder that a flaweddeposit insurance system can be extremelycostly. U.S. taxpayers were billed for morethan $130 billion to clean up the savings andloan crisis following the demise of the FederalSavings and Loan Insurance Corporation(FSLIC). This demonstrates that depositinsurance raises complicated issues andrequires a careful balancing of competingpublic policy concerns.

Today, the bank and thrift industries have neverbeen healthier. Bank capital levels are at an alltime high, profitability has climbed for theninth year in a row, and the insurance fundshave substantial combined reserves of $42billion. There will never be a better time toaddress the latent flaws in the system. Reformsnow will also help us maintain the properincentives for risk and reward to insuredinstitutions, as well as fairness amonginstitutions that present different levels of riskto the system.

The FDIC has identified three fundamentalareas for review: the processes for pricing risks,funding insurance losses, and setting coveragelimits. This options paper describes variousways in which we might make improvements

2

to the deposit insurance system. The optionsare intended to prompt analysis and commentfrom individuals and organizations that have aninterest in the issue.

1. The Need for Reform

With the Federal Deposit InsuranceCorporation Improvement Act of 1991(FDICIA), Congress passed a number ofsignificant reforms to shore up the depositinsurance system. These included promptcorrective action, least-cost resolutions, scalingback of too-big-to-fail, the introduction of risk-based premiums, and a mandate to maintainadequate insurance funds. With the DepositInsurance Funds Act of 1996 (DIFA), Congressensured that members of the Bank InsuranceFund (BIF) and the Savings AssociationInsurance Fund (SAIF) would not facesignificant and arbitrary differences in depositinsurance pricing.

Despite these significant improvements, thecurrent deposit insurance system has severalfeatures that work against the effective andequitable functioning of the system:

• The continued existence of two separateinsurance funds based on an anachronisticdistinction;

• The current pricing system that createsinappropriate incentives and raises fairnessissues;

• The requirement that banks are required tofund insurance losses when they can leastafford it; and

• Uncertainty for depositors as to the futurereal value of FDIC coverage.

Over the past decade the FDIC has stated itsview that the two insurance funds the FDICadministers should be merged. The distinction

between the funds is increasingly arbitrary; acombined fund would be stronger and moreefficient; and the time to merge them is whenthey are both healthy. These arguments arelaid out in detail in Attachment A. This optionspaper will not address this flaw, other than tostate the FDIC’s position that a merger of thefunds is good public policy either on a stand-alone basis or as the prerequisite for any otherchanges to the deposit insurance system.

The second and third of these problems resultfrom the conflicting mandates of the FDICIA:to price deposit insurance premiums accordingto the risk posed by individual institutions, andto maintain a target level of reserves within theinsurance funds. The tension between the dualmandates of risk-based pricing and a fixed fundlevel became far more explicit in 1996 as DIFAseverely limited the FDIC's ability to priceaccording to risk.

Because of current restrictions on pricingdeposit insurance, most banks and thrifts payno insurance premiums when they are doingwell, but pay high premiums when the industryis weak and banks are failing. This does notmake sense for the banks or for thecommunities they serve. It is possible that, indifficult times, deposit insurance premiumscould reduce the pre-tax net income of insuredinstitutions by almost $9 billion. Based oncurrent average capital and loan-to-assets ratiosfor all insured institutions, this reduction inincome could lead to a contraction in lending ofmore than $65 billion at the precise time in thebusiness cycle when loans are most needed.

The current process for setting depositinsurance coverage limits has brought the issuebefore Congress on a somewhat arbitrary andad hoc basis. This has resulted in significantfluctuation in the real value of insurance fordepositors. The current coverage limit of$100,000 has declined in real value by halfsince it was established in 1980. This raises thequestion of whether Congress wishes to

3

continue providing the same level of insuranceprotection for consumers in real terms, or toallow the coverage level to erode in value bymaintaining the status quo.

The current deposit insurance arrangementslead to several questions:

How Should the FDIC Price Risk?

Through a combination of legislative changes,regulatory choices and economic events, thepricing and funding of deposit insuranceevolved during the 1980s and 1990s intosomething fundamentally different from whatexisted during the first 50 years of the FDIC’shistory. Banks that are paying for depositinsurance at the end of the 1990s are those thathave run afoul of capital regulations or thesupervisory process. This is a significantdeparture from past practice. Pricing of depositinsurance has evolved into a penalty system forthe few, rather than a priced service for all.

Thus, a decade that began with a legislativemandate for risk-based insurance premiumsended with the FDIC providing a freeguarantee of almost three trillion dollars inbank and thrift liabilities. As a result, themoral hazard problems FDICIA intended toaddress with risk-based deposit insurance mayhave become more firmly entrenched than ever.(Moral hazard problems are discussed in moredetail in Section IV, "Coverage Limits.")

A striking feature of a zero premium is that notonly may the rate paid by vastly disparatebanks be identical, but the dollar amount aswell: a bank with $100 billion in deposits and acomplex risk profile can be billed the sameamount for its insurance as the smallest andmost conservatively run community bank.Presumably, the rationale behind a statutoryzero premium is that, as long as a fund is aboveits target level, it does not need additionalfunds. However, aside from raising money for

the insurance funds, premiums also serve toalign economic incentives. When a valuableproduct is offered at zero cost, it leads to thatproduct being overused, causing distortionsthroughout the marketplace and, in the case ofdeposit insurance, potentially exacerbatingmoral hazard.

If deposit insurance were priced according torisk, it is likely that every bank in the U.S. withinsured deposits would pay something fordeposit insurance, for the same reason thatevery bank pays at least some spread overTreasuries for unsecured debt. However, sinceshortly after the BIF was recapitalized in May1995, its members that are in the best-rated,1A-assessment category have not been requiredto pay deposit insurance premiums. Membersof the SAIF that are rated 1A have paid nopremiums since January 1997.1

At year-end 1999, only 7 percent of all banksand thrifts paid premiums into the depositinsurance funds. Ninety-three percent, or morethan 9,500 institutions, do not pay premiums.This stands in stark contrast to the first 50 yearsof the federal deposit insurance program, whenevery insured institution paid an annual rate of3.3 to 8.3 cents for every $100 of insureddeposits.

Despite the uniform assessment ratings given tothese 1A institutions, they do not all presentuniform risks to the deposit insurance funds.The current premium matrix does not recognizeinstitutions that, by objective measures andhistorical experience, have a higher risk profile,unless the institution fails to maintain theminimum level of capitalization to beconsidered "well-capitalized" as defined forprompt corrective action purposes or is subjectto heightened supervision.2 In a less favorable

1 More details on the risk categories in the currentpremium system are presented in Attachment C.2 Federal supervisors rate insured institutions on sixfactors: Capital; Asset Quality; Management; Earnings;Liquidity; and Sensitivity to market risk (CAMELS).

4

economic environment, many of these 1A-ratedinstitutions would deteriorate faster than others,yet that higher degree of risk is not built intothe current assessment scheme.

How Should New Deposits be Treated?

Most banks and thrifts established since therecapitalization of the insurance funds havenever paid for deposit insurance. ThroughMarch 2000 this included 844 new banks andthrifts whose insured deposits totaled more than$44 billion. The responsibility for maintainingthe $550 million needed to capitalize thesedeposits at a 1.25 percent DRR falls on theother members of the deposit insurance system.

Similarly, institutions that are rated 1A cangrow their insured deposits without payingassessments. This zero marginal cost ofinsurance clearly differs from the privateinsurance industry, in which higher coverageamounts entail higher charges. With themarginal cost of deposit insurance at zero, thesame issues of fairness arise that occur underthe new bank scenario: all insured institutionseventually are assessed to cover deposit growthat the fastest-growing, 1A-rated institutions. Ina deteriorating financial environment, it will benecessary to raise assessment rates earlier or bya greater amount to make up for the dilution ofthe reserve ratio attributable to unfundedinsured-deposit growth.

Under some circumstances, insured-depositgrowth could occur rapidly, accelerating the

Institutions receive an overall rating ranging from 1 to 5,with 1 being the best rating.

The original decision by the FDIC to lump CAMELS 1-and 2-rated institutions into the same risk category forpremium purposes was largely codified into law in 1996by the DIFA. Federal Deposit Insurance Funds Act, Pub.L. No. 104-208, §§ 2708(b) and 2708(c) (1996) (codifiedat 12 U.S.C. §§ 1817(b)(2)(A)(iii) and (v)). As a result,the FDIC is largely prohibited from distinguishingbetween CAMELS 1- and 2-rated institutions fordetermining premiums.

need to raise assessment rates for all insuredinstitutions. This could happen even in afavorable economic environment in whichdeposit-insurance losses remain low. In early2000, an investment company announced plansto convert some of its customers’ funds intoFDIC-insured accounts. Reports in the mediasuggested that as much as $100 billion could beconverted in this manner in a relatively shortperiod of time. Sudden growth of thismagnitude at 1A-rated banks, with nocorresponding growth in the fund balance,would dilute the fund’s reserve ratio. In thisexample, the BIF reserve ratio would fall by 5basis points. With a reserve ratio of 1.35percent as of March 31, 2000, such a declinewould leave the fund’s reserve ratio above thestatutory minimum of 1.25 percent, but theindustry would be closer to mandatory rateincreases for all insured institutions, dependingon insured-deposit growth and insurance losses.From March 31, 2000, through June 30, 2000,insured deposits at the banks affiliated with theinvestment company grew by $12 billion.

There is also the possibility of a large shift ofhousehold assets into insured deposit accountsin the event of financial market volatility.There is currently more than $11 trillionoutstanding in U.S. equity holdings (includingmutual fund shares) alone. In a protracted bearmarket, some of these funds could betransferred to insured deposits. And it is stilltoo early to gauge the probable impact ofelectronic banking on insured deposit growth.Obviously, the likelihood of deposit inflowsfrom these examples, as from a myriad of otherpossibilities in an era of financial modern-ization, cannot be known. The question iswhether the current deposit insurance system iscapable of addressing the issues raised by thesepossibilities.

Conversely, institutions that shrink theirdeposits are not compensated for the indirectbenefit they confer on other members of thesystem. Most BIF members have paid no

5

premiums since 1995, and most SAIF membershave paid none since 1996, but all insuredinstitutions paid very high rates in the earlier1990s. The issue of deposit growth andshrinkage becomes important in any discussionof rebates (other than the refunding of currentassessment income). Any such program wouldrequire legislation, but the question of who isentitled to how much is complicated by theexistence of institutions whose deposit growthor shrinkage was atypical. For example,aggregate BIF-insured deposits grew by 10.5percent from year-end 1995 to year-end 1999,during which time one bank grew its insureddeposits (without any acquisitions) from $19million to $1.2 billion (up 6,140 percent), andanother bank reduced its insured deposits from$763 million to $423 million (down 45percent). Of these two banks today, the onewith a lower level of insured deposits paidconsiderably higher total assessments in the1990s.

How Should Losses be Funded?

In reaching a point where the FDIC does notcollect assessment revenue from mostinstitutions during good times, we have clearlydeparted from any concept of spreadinginsurance losses over time by collectingrevenue on an ex ante or long-run expected lossbasis. In contrast, prior to 1989 it could beargued that Congress intended the FDIC tooperate under a form of long-term expectedloss pricing. During the period 1933-1989,when premiums were set by statute and neverdeparted from a range of between 3 and 8.3basis points per annum, accumulated premiumsand the investment income on those balancesenabled the system to roughly pay for itself.The system in place today, in contrast, amountsessentially to charging nothing in times ofprosperity, and a lot in times of adversity,thereby potentially magnifying swings in thebanking cycle.

The current “cushion” in the BIF, the amountby which the fund exceeds 1.25 percent, is $2.3billion.3 If insurance losses not covered by thesystemic risk exception were to exceed thisamount—as they did in each year from 1988through 19924—and the fund fell below 1.25percent and was expected to remain there for ayear or more, the FDIC would be forced toraise average assessment rates to a minimum of23 basis points. Therefore, all banks would beforced to pay substantially higher premiums ata time when many banks were under stress. Ona strict pay-as-you-go basis, banks would havehad to pay approximately 62 basis points in1991.

If the FDIC had more latitude in setting rateswhen the reserve ratio falls short of the DRR,the recapitalization period could be extendedwith rates less than 23 basis points. This wouldhelp to avoid a credit crunch and to moderatethe negative impact of deposit insurancepremiums on real economic activity.

How Should the Coverage Levels beDetermined?

The current process for setting depositinsurance coverage limits has brought the issuebefore Congress on a somewhat arbitrary andad hoc basis. This has resulted in significantfluctuation in the real value of insurance fordepositors. Deposit insurance has a simple, butimportant purpose: to provide a safe place fordepositors to keep their money, as a way toprevent bank runs and maintain the stability ofthe banking and financial system.

Since 1934, the basic coverage amount hasincreased five times, from $5,000 to $100,000. 3 Despite growth of the fund during the first quarter of2000, this cushion fell from $2.5 billion at year-end 1999because of insured-deposit growth in the first quarter.4 Annual losses ranged from $2.7 billion to $6.9 billionduring this five-year period. These are actual losses andnot loss provisions, which were even higher but werepartially recovered when many projected failures did notoccur.

6

Most of the increases more or less reflectedcost-of-living adjustments, but the most recentincrease is an exception. The 1980 jump from$40,000 to $100,000 had more to do withattracting deposits to insured institutions in acompetitive market of very high interest rates.Today, 20 years later, $100,000 of depositinsurance has lost about half its value, based onthe Consumer Price Index.

The next several decades will be a time inwhich the population is aging, retirement costsare increasing, and the supply of federally-backed investment vehicles, such as Treasurynotes and bonds, may decline. Thus, a long-term perspective may argue for allowing for thecoverage limit to keep up with changes in theprice level, household wealth, or othermeasures relevant to households.

However, there are trade-offs to consider.Higher coverage limits can increase moralhazard. The 1980 increase is widely viewed ascontributing to the high cost of the savings andloan crisis. Also, the impact of higher coveragelimits on insured deposit growth is difficult topredict, and the likely distribution of benefits issubject to debate.

2. Overview of Options Paper

This remainder of this paper organizes thediscussion into three major areas: pricing risk,funding insurance losses, and coverage levels.

Section II of this paper discusses the pricing ofdeposit insurance for individual banks. Ifdeposit insurance is viewed as a service thatbanks use, the question is how this serviceshould be priced. One answer is that the priceshould reflect the risk that the bank presents tothe deposit insurance system. This expectedloss approach to pricing is consistent with thebest practices that have developed in thebanking industry in recent years.

The next question is what information shouldserve as the basis for pricing. Supervisoryratings are appealing because they are based onquality information and reflect the judgment ofexperienced supervisors; however, too great areliance on ratings raises concerns aboutconsistency and subjectivity. This suggests theappeal of more objective information, whichcould include non-public information (such ascredit exposures), Call Report information, andmarket information. Finally, the FDIC couldgenerate pricing information through risk-sharing contracts with market participants.

Section III deals with how deposit insurancelosses are funded from an aggregateperspective. The funding of FDIC losses hasevolved over the years from a system thatfeatured steady premiums with a fluctuatingreserve ratio to a system that targets a specificreserve ratio and results in volatile premiums.The mandate to maintain a particular ratio canlead to steep premiums during bad times andcalls for rebates during good times.

One general approach is a user fee system inwhich banks have no claim on past premiums.Under such an approach, the question iswhether premiums will be relatively stable andconsistent with expected loss pricing, orwhether premiums will be more closely tied tocurrent losses or the reserve ratio in order toguard against premiums that are too high or toolow.

A mutual approach would differ from the userfee system in that banks would have someclaim on past premiums. This could take theform of rebates when the insurance fund isviewed as too large; this raises the question ofhow to allocate these rebates. Alternatively,banks could hold claims on the insurance fund,similar to mutual fund shares. This couldaddress concerns about free rider and pricingproblems. Under mutual arrangements, thecash flow between a bank and the insurancefund could have two components: one to price

7

risk at the margin and the other to reflect thebank’s claim on the fund.

Section IV discusses the appropriate extent ofdeposit insurance coverage. The section beginswith a review of the history of coverage levelsin nominal and real terms. This is followed bypreliminary estimates of how an increase in thecoverage limit would be expected to increasethe amount of insured deposits. This dependson the behavior of households and businesses,and further study would allow more confidencein these estimates.

It is widely recognized that there is a tradeoffbetween the stability that deposit insurancebrings and the potential for distortion of themarket process. Coverage levels speak directlyto that tradeoff: higher coverage may providegreater stability during difficult times, whilelower coverage may enhance market disciplineand minimize distortion. The section addressesthis tradeoff with a discussion of moral hazard,implicit protection, and industry structure.

The options in the coverage section includecontinuing the existing system of ad hocstatutory adjustments; indexing for inflationaryadjustments; or simplifying the current systemto limit a particular level of coverage to oneaccount per person. Other ideas for changes tocoverage include extending higher coverage tomunicipal and other public deposits; this raisesissues similar to those posed by brokereddeposits. The section ends with excesscoverage options including increased use ofprivate coverage, new excess coverage throughthe FDIC, FDIC-backed private insurance, orcoinsurance systems.

3. Review Process and Comments onOptions Paper

This paper is one step in the FDIC’scomprehensive review of the deposit insurancesystem. FDIC Chairman Donna Tanoue

publicly announced the review on March 7,2000, in a speech before the IndependentCommunity Bankers of America. On April 25,2000, the FDIC held a Deposit InsuranceRoundtable with bankers, their trade grouprepresentatives, consumer group represent-atives, and industry experts. The Roundtableprovided an opportunity for interested parties toraise issues and discuss broad policy optionsfor consideration in the FDIC’s review. Atranscript of the proceedings may be viewed atwww.fdic.gov. The Roundtable was followedby outreach meetings with bankers during Mayand June in Minneapolis, Dallas, and KansasCity. The FDIC also held discussions withmembers of state banking organizations duringtheir annual spring visits to Washington andwith several leadership groups and staff of thenational trade associations.

In addition, the FDIC has held discussions withacademics and other outside experts. Toprovide a more explicit “market perspective”on deposit insurance pricing and fundexposure, the FDIC retained the risk-management consulting firm of Oliver, Wyman& Company (Oliver, Wyman). Oliver, Wymanemployed an analytical framework similar tothat used by the largest financial institutions foranalyzing their credit exposures. The purposewas to explore ways to incorporate "bestpractices" from private-sector risk managementinto the consideration of FDIC pricing andfunding issues.

The ideas and perspectives that werecommunicated through these various effortshave been incorporated into the options paper.The FDIC will carefully review comments andweigh feedback from the options paper in orderto narrow the policy choices and guide theadditional analytical work necessary to developa set of policy recommendations that isappropriately balanced, workable, and fair. Asstudies conducted by FDIC staff and others arecompleted, additional discussion—perhaps a

8

new set of roundtables or outreach meetings—will be arranged with interested parties.

Because this paper is not intended to advocatespecific approaches but to solicit comment, wehave presented a wide range of concepts fordealing with the policy issues under discussion.Examples of how these conceptual approachesmight work in practice are included, andreaders are encouraged to comment both on thespecific examples and on broad conceptualapproaches.

Comments on the options paper may beregistered on the FDIC web site atwww.fdic.gov. The Internet version of theoptions paper will include a survey which willbecome available on August 31. Readers areinvited to respond to the specific questions thatwill be posted on the FDIC web survey foreach topic and to provide any additionalcomments relating to the survey questions.

Comments may also be addressed to Robert E.Feldman, Executive Secretary, Attention:Comments/OES, Federal Deposit InsuranceCorporation, 550 17th Street, N.W.,Washington, D.C. 20429. Comments may alsobe hand-delivered to the guard station at therear of the 550 17th Street Building (located onF Street) between 7:00 a.m. and 5:00 p.m. onbusiness days. In addition, comments may befaxed to (202) 898-3838, or sent via theInternet to [email protected].

FDIC staff will review comments as they arereceived and summarize them each monththrough the fall of 2000, beginning withSeptember. Comments will be available forinspection and photocopying at the FDICPublic Information Center, Room 100, 80117th Street, N.W., between 9:00 a.m. and 4:30p.m. on business days.

9

II. PRICING DEPOSIT INSURANCE FOR INDIVIDUAL BANKS

Depositors value the simplicity and certaintythat deposit insurance provides, and banksbenefit from being able to offer insureddeposits to customers. Like other servicesbanks use, a financial guarantee such as depositinsurance is not costless to provide. Thestarting point for the discussion in this sectionis that it is equitable and reasonable for a bankto compensate the parties who bear the risk ofproviding this benefit.

In this section we will consider ways ofdifferentiating among the risk profiles of themore than 9,000 insured institutions currentlyin the 1A category for deposit insurance. Themost straightforward conceptual approach isfor a bank to pay an amount equal to theexpected loss the deposit insurer faces fromproviding deposit insurance to that bank. An“expected loss” pricing system would 1) reflectthe differences in risk across banks and 2)generate revenue sufficient to pay for the costsof insuring deposits. The expected loss pricefor a bank would depend on three things:

• the probability of default for that bank;

• exposure; and

• severity, or loss given default.

At least in principle, every bank could beassigned something similar to a credit rating,with an associated range of default probabilitiesderived from experience. These defaultprobabilities, combined with customized orstandardized assumptions about loss givendefault, would yield the FDIC’s expected lossper dollar of assessable deposits, and theappropriate premium, for that institution. Suchan approach also would provide the rawmaterial to construct hypothetical distributions

of FDIC loss exposure using standard creditrisk measurement tools, as discussed in thefollowing text box.

Oliver, Wyman & Company Approach toBank Level Pricing

Expected loss pricing has two key benefits: atthe systemic level, setting the price for eachbank equal to its expected loss ensures that thepremium inflows to the fund are ultimatelyequal to average long-term loss. This ensuresthat the fund is self-financing over time.Additionally, risk-based pricing helps to relievemoral hazard problems: Banks that try to usethe availability of insured deposits to increaserisk will be penalized through higherpremiums.

Under Oliver, Wyman's proposed pricingstructure, expected loss would be calculated“bottom-up” at the level of individual banks.This can be done by breaking expected loss foreach bank into its components: expecteddefault frequency; exposure; and severity.Approaches for estimating each of thesebuilding blocks are suggested below:

Expected Default Frequency

Expected default frequency (EDF) is the mostsignificant of the expected loss buildingblocks.5 There are two basic approaches theFDIC could use to quantify the default

5 EDF is "expected default frequency," or probability ofdefault. The EDF is one of the three components thatdetermine expected loss, which is described by thefollowing relation:

Expected loss = (EDF) x (exposure) x (loss givendefault).

10

probability of individual banks. The firstmethod is a fundamental analysis of a bank’scondition, encompassing risk profile, financialstrength, management, market position, andfuture prospects. The second method is toleverage the analysis of others by interpretingmarket price information.

Fundamental analysis

A private sector company that underwrotedeposit insurance would need to have a processfor evaluating the riskiness of each customer.This process would likely resemble that whichlarge banks use in evaluating the risks oftrading counterparties and correspondentbanks. Typically, such an analysis incorporatesa number of elements, including the risk profileof the institution (credit, trading, asset/liability,event, and business risks), its financialresources (capital, reserves, subordinated debt,unrealized gains, sellable goodwill) and thequality of its management.

The FDIC already has access to many of thefactors that go into a fundamental analysis,either through Call Reports or through theexamination process. A key difference fromexisting CAMELS ratings, however, is howthis information is processed. In order to beuseful for pricing purposes, the fundamentalanalysis needs to be summarized in a score orgrade which, in turn, is directly calibrated to anabsolute measure of default risk (EDF). Atmany leading institutions, this is done bymapping the results of fundamental analysis tothe external agency ratings of rated financialinstitutions. This mapping is then used tocalibrate all scores (for both rated and unratedinstitutions) to their EDF equivalents.

At a minimum, such an approach can beundertaken with the elements of the existingCAMELS ratings. Oliver, Wyman would,however, advocate that the resulting gradesshould be more granular and provide for a

much greater dispersion of exposure than thecurrent risk buckets.

Market analysis

As an alternative (or supplement) tofundamental analysis, the FDIC could also seekto leverage market price information. In sodoing, the FDIC would be outsourcingcounterparty evaluation to the credit markets,using the premiums they are charging banks asan indicator of risk.

A number of market instruments could be usedas barometers of credit risk, including:

• (Uninsured) interbank deposits• Senior debentures• Subordinated debt• Interest rate swaps• Credit derivatives• Equity

In addition, the FDIC could encourage thedevelopment of new products for the purposeof providing market price information tailoredto FDIC’s pricing needs. For example, bankscould be required to purchase private depositinsurance in addition to that from the FDIC,either on a separate class of deposits, or as co-insurance to the FDIC. Recent proposals for aspecial class of subordinated debt could alsoserve as a market price indicator.

The main drawback to the use of market pricesis that they are limited to banks that are largeenough to attract an active market in theirsecurities. While regulatory encouragementcould increase the number of banks withappropriate instruments, it is likely that for themajority of smaller banks, even if they were toissue market debt, there would be little trading,and thus relevant price information. Forpractical purposes, a market-pricing regimewould have to be limited to larger banks.Nevertheless, market prices could still beuseful as external benchmarks of credit risk,

11

particularly to establishing relative risk on thebases of observed premiums.

Exposure

Exposure measurement is the moststraightforward of the expected loss buildingblocks. For each bank, this should be theamount of insured deposits. An alternativewould be to base exposure measurement ontotal deposits (insured plus uninsured) on thetheory that this would also capture exposure in“too big to fail” (TBTF) cases. However, sinceTBTF coverage would presumably affect onlyan unspecified number of large banks, insureddeposits remains the best single measure ofexposure.

Severity

Severity is the size of the loss to the FDIC, as apercentage of the total defaulted exposure to allinsured deposits. While important, differencesin the expected severity among banks aresmaller than differences in EDF. We wouldthus recommend a simpler treatment of severityestimation. The FDIC experience shows thatthe severity of loss from small banks is usuallygreater than that for larger banks. This shouldbe priced into risk-based premiums, eitherdirectly, or by investigating the underlyingdrivers of this difference. Factors which mightprove to be good indicators of severitydifferentiation include business mix, loanconcentration, and the structure of liabilities.6

The FDIC faces some practical constraints onits pricing of deposit insurance. There arelimits on the extent to which risk distinctions

6 Oliver, Wyman would normally recommend that theseverity rates used in pricing be based on historicalexperience. However, the changes in early resolutionbrought on by FDICIA, if successful, should lowerexpected severity. Unfortunately, the experience of bankdefaults since FDICIA is too limited to determine if thisis the case, and if so, how much loss severity has beenreduced.

can or should be made using either objective orsubjective measures. Within those limits,however, setting deposit insurance premiumsbased on expected loss is over the long termlikely to minimize the distortions and moralhazard problems associated with depositinsurance, and minimize the cross subsidizationof the weakest banks by the strongest.

Conceptually, the question of how depositinsurance is priced at a point in time can beviewed in two ways. As discussed in thepreceding text box, a "bottom-up" view wouldset pricing at the individual bank level and letoverall revenue result from the sum ofpayments across banks. A "top-down" viewwould instead attempt to estimate appropriateaggregate funding needs and then allocateprices across banks based on risk.

The next section of the paper takes anaggregate perspective and discusses howinsurance losses are funded over time. Thissection deals with how to assess risk at theindividual bank level; the discussion here isconsistent with either a bottom-up approach topricing or a top-down approach that features abase price with adjustments for individualbanks based on differences in risk.

Options for moving toward expected losspricing or otherwise differentiating among therisk profiles of institutions in the 1A categorycan be broadly classified into approaches thatrely on supervisory judgment, those that rely onother information, and hybrid approaches. Afew specific examples of how some of theseapproaches could be used to develop “expectedloss prices” for individual banks are includedfor illustrative purposes. We have notattempted to derive expected loss prices forevery risk-differentiation option, but inprinciple one could do this. One could derivehistorical failure rates and loss rates for groupsof banks and use such information to form thefirst and third elements of the FDIC’s expectedloss discussed above. The third element, the

12

proportion of loss borne by the FDIC, couldeither be based on a historical rule of thumb or,alternatively, could be based on a moresophisticated analysis tailored to an individualbank’s liability composition. (See AttachmentE-3 for a full discussion.)

Some of the risk differentiation methods wediscuss below are not amenable to historicalloss analysis because historical informationdoes not exist. Examples would include usinglarge bank supervisory risk matrices moreexplicitly, using a newly developed supervisoryrisk rating, or using elements of non-publicbank-specific information that have not beencollected in the past. In most of these cases,the risk differentiation methods discussedbelow are best viewed as tools to help allocateassessments on a risk-related basis. In somecases, for example, by differentiating risk basedon specific elements of risk-relatedinformation, and depending on the informationcollected, one could conceivably developestimates of expected loss at the bank level asdescribed in the preceding text box.

Because all of the methods considered have thepotential to distinguish more effectively amongA-rated banks, the likely result regardless of

Chart 1

the method selected would be that the safestbanks pay less over the long run.

Options Relying on Supervisory Evaluations

The case for relying on supervisory judgmentas the cornerstone of any attempt to enhancerisk differentiation is easy to state: onsiteexamination provides the most in-depthinformation available. The options for such anapproach include:

• Composite CAMELS ratings;

• Components of the CAMELSratings;

• Risk matrix results; and

• Uniform risk management ratings.

Composite examination ratings. It would bequite simple to achieve additional riskdifferentiation by application of existingsupervisory tools. Specifically, the FDIC coulddifferentiate for insurance purposes betweenbanks with examination ratings of 1 and 2.This would be clearly supportable from a risk

Failure Rates By Composite Rating*

0.7 1.8

16.2

5.1

49.7

0.0

10.0

20.0

30.0

40.0

50.0

60.0

1 2 3 4 5Composite Rating

Pe

rce

nt

*Average cumulative f ive-year failure rates by composite CAMELS rating among commercial and savings banks. Savings and loan associations are excluded.

13

perspective given the relative historical failurerates of these two groups of banks. As shownin Chart 1, the 5-year failure rate for CAMELS2-rated institutions since 1984 was more thantwo-and-a-half times the failure rate for 1-ratedinstitutions.

Component ratings. Other currently usedsupervisory tools could readily be put to use forpricing deposit insurance. For example, thecomponent ratings in the CAMELS systemcould play a greater role. The componentratings are ratings of the individual elements ofthe CAMELS acronym that are assigned in theexaminations: capital, asset quality, manage-ment, earnings, liquidity and sensitivity tomarket risk. The component ratings range from1 to 5, and 1 is the best rating. There is at leastconceptual appeal to greater use of theseratings for setting premiums. Purely toillustrate the concept, one could imagine, forexample, a rating of “2 minus” for 2-ratedbanks with a sufficient number of componentsrated 3 or worse.

Table 1

One concern with this approach is that greaterreliance on subjective information couldcompromise consistency in determiningpremiums, and more so the finer thedistinctions that supervisors are asked to make.This is a general concern that applies to alloptions involving supervisory information andis discussed further below.

Risk matrix results. For the largest banks,results from the Office of the Comptroller ofthe Currency (OCC) and the Federal ReserveBoard risk matrices could be used moreexplicitly. As a supervisory tool, largecomplex banks supervised by the OCC and theFederal Reserve Board are assigned ratings fora variety of risk-management factors. Bankswith the same composite CAMELS rating canhave substantial differences in these risk ratingsand these differences do not affect the premiumpaid by the institution. One could imagineassigning scores based on these matrices.Again, purely to illustrate the concept, a “2minus” could be a bank with a sufficientnumber of high or rising key risk elements inthese matrices.

An impediment to this approach is that there isa lack of uniformity at the agency level, withthe OCC and Federal Reserve using differentmatrices and the FDIC and Office of ThriftSupervision not using a matrix approach. Anexample of the OCC’s Risk Matrix is displayedin Table 1.

Uniform risk management rating. If weconsider approaches that require more time toimplement, the possibilities expand. Forexample, one could imagine an interagencyeffort to develop a uniform risk ratingexplicitly designed to differentiate among thelevels of risk implicit in a 1 or 2 rating. Such arating could consider such factors as the extentof credit concentrations and the quality ofunderwriting standards and internal controls—irrespective of the current financialperformance and condition of the institution—

Risk Types Level Direction

Credit High SteadyPrice Moderate Falling Interest Rate Low SteadyForeign Exchange Moderate RisingLiquidity High SteadyReputation - -Transaction - -Compliance - -Strategic - -

For each of the nine risk types, the OCC risk matrix

indicates the level (High, Moderate, or Low) and

direction (Rising, Steady, or Falling) of the risk.

OCC Risk Matrix

14

and would essentially gauge the institution’soverall appetite for risk. This approach couldbe applied to all institutions, or, alternatively,only to the largest institutions. One concernhere is that designing a uniform interagencyrisk-rating could take years.

There are arguments against basing riskdifferentiation on supervisory judgment. Theexamination process might require a greaterdegree of management discussion in order forexaminers to work constructively with banks toobtain needed information, and bankers mayhave discomfort with additional supervisorydiscretion. Examiner judgments are subject toseveral layers of review and an elaborateappeals process, and one of the disadvantagesof increasing the reliance on supervisoryjudgments for pricing deposit insurance couldbe an increase in the resources bankers andexaminers might have to devote to suchprocesses. It could also be argued that some ofthe tools described above—notably theindividual component ratings and the largebank risk matrices—were intended assubjective supervisory tools that should not beput to uses for which they were not designed.

For the 99-plus percent of insured institutionsthat do not have a continuous onsite examinerpresence, there also may be significant issuesof timeliness in relying on examiners todifferentiate the risks taken by the vast majorityof well-performing banks. Most banks areexamined on an eighteen-month cycle. Theissue concerning the timeliness of onsite data isreduced in larger insured institutions that aresubject to ongoing targeted examinations or amore frequent examination cycle.

Changes in risk profiles between examspresently are addressed using offsitemonitoring tools, with an onsite exam or othersupervisory review as needed; in particular, adowngrade of a bank to a 3-rating is generally

validated with an onsite examination. If thepremium system were structured todifferentiate more among the 9,000-plusinstitutions not currently subject to heightenedsupervision, and if changes in an institution’srisk category required an onsite supervisoryreview, resource demands on the supervisoryprocess would increase.

Options Relying on Objective Factors

Another general method to consider would be“factual” or data-driven approaches. Severalsources of information could feed suchapproaches: non-public bank specificinformation, bank Call Reports, or marketinformation.

Non-Public Bank-Specific Information

The federal banking regulators have access to asignificant amount of non-public informationabout insured institutions, information that maybe a useful supplement to Call Report data forpurposes of evaluating institution risk profiles.It may be possible to develop a basic packageof objective information that would assist in theprocess of differentiating the risk profiles of themajority of strong-performing institutions.Much as premiums are now assigned based notonly on supervisory evaluations of capitaladequacy, but on the capital ratios themselves,one could imagine the FDIC differentiating riskprofiles directly from non-public informationprovided by banks.

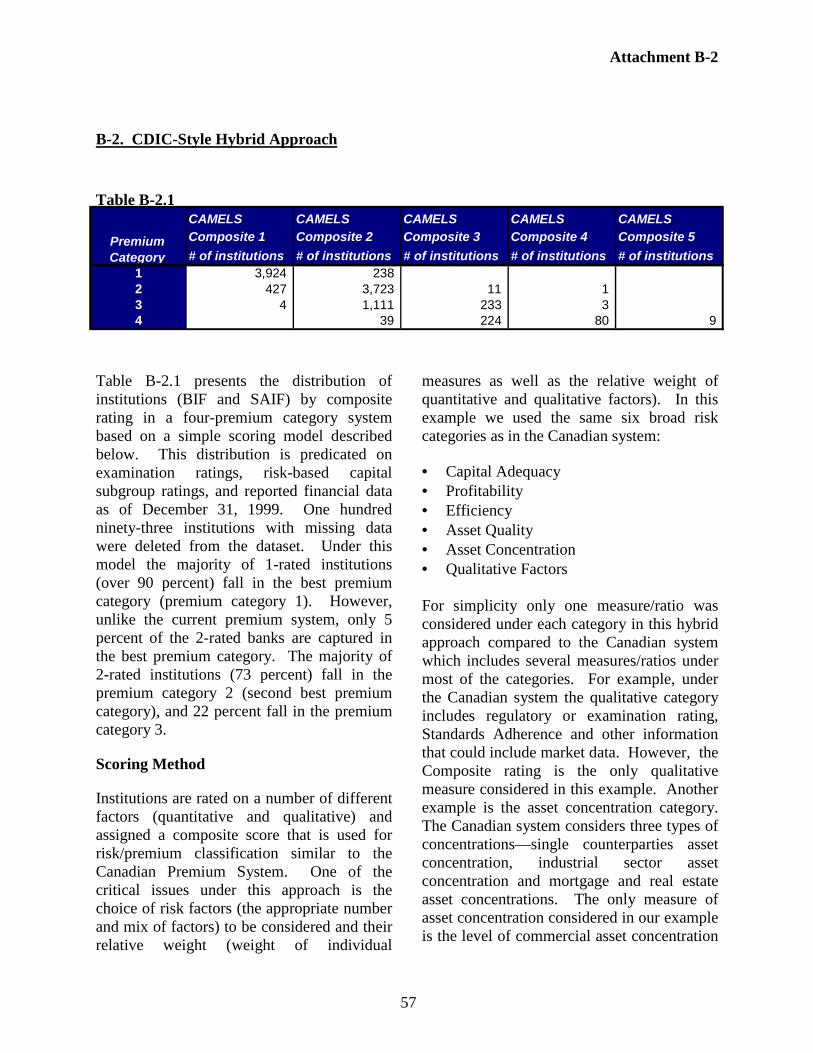

The Canada Deposit Insurance Corporation(CDIC) created a risk scoring system in 1999that is based, in part, on regulatory reportinginformation and partly on information provideddirectly to the CDIC by its member institutions.The score incorporates information on a varietyof risk-related factors including capitalization,significant credit concentrations, and self-certifications of the extent of adherence to

15

defined risk-management standards. Thestandards adherence information is submittedby the banks annually to the CDIC, with a copyprovided to each institution's primarysupervisor. CDIC assigns banks to one of fourrisk categories for insurance purposes based onboth the supervisor’s examination rating andthe information banks provide. (Banks that donot provide information are put in the worstpremium category.) The algorithm forassigning banks to categories based on theinformation provided is known to the memberinstitutions. Attachment B-1 summarizes themajor features of the CDIC risk scoring system.

The CDIC’s experience has been that itsscoring system provides a reasonable balancebetween qualitative and quantitative factors,and that it is relatively transparent and easilyunderstood by member institutions. Thedoubling of premiums payable resulting from adrop from one category to the next appears toprovide incentives to member institutions toeither improve their financial results or theiradherence to the standards.

The CDIC faces issues with its system thatundoubtedly would be faced under any similarscoring system that might be devised. Theselection of a particular scoring methodologycreates the possibility that institutions focusedon maximizing their scores could achieve thebest premium category, but might still beconsidered risky by other measures that are notencompassed by the system. This issue, andthe related question of how, and how often, theinformation the insurer receives is to beverified, are addressed in part through thesupervisory examination process. The detailsof how that occurs are a subject of continuingdiscussion between the CDIC and the primarysupervisor, as would likely also be the case ifthe FDIC were to implement such a system.There is also the tradeoff between reportingburden and comprehensiveness of results. Forexample, the quantitative part of the CDIC’ssystem includes very little off-balance sheet

information, as it was felt that such inclusionwould require excessive filing requirements.

The CDIC’s approach is one among many thatcould be devised along similar lines. Thedesign of a risk scorecard could be exposedboth to public comment and the expertise ofindustry practitioners in both small and largebanks.

The advantage of this approach potentiallywould be in using more detailed risk-relatedinformation without imposing a regime wheresupervisors are asked to make subjectivedistinctions among healthy banks. Moreover, itcould avoid the resource and timeliness issues,described above, that could arise if supervisorswere asked to monitor inter-examinationchanges in risk profiles for over 9,000 banksalong a more finely graduated scale than is nowrequired.

Such an approach could raise concerns aboutthe burdens of creating another layer of bankreporting. Those concerns might be allayed ifthe risk scorecard were either simple, or builton information that is readily available to awell-managed bank. In this regard, acomparison with developments in capitalregulation may be appropriate. The momentumtowards basing large-bank capital requirementson internal credit ratings accommodatesdifferences in banks’ internal ratings scales,provided those ratings can be mapped to acommon rating scale. Thus it may allow forboth flexibility at the bank level and analyticalrigor in the setting of capital requirements.This new direction in capital regulation is anexample of a systematic use of non-publicbank-specific information for a significantpolicy goal. Deposit insurance pricing maysimilarly be able to benefit from such asystematic use of non-public information.

16

Bank Call Reports

Better differentiation of risks in the premiumsystem using public financial reports would beconceptually straightforward. There isconsiderable variation in the financialcharacteristics of the 9,000-plus insuredinstitutions in the highest assessment category.Using figures reported by banks for year-end1999, Table 2 displays differences between 1A-rated banks in the top 10 percent on severalperformance factors and those ranked in thebottom 10 percent. (Attachment C explainsthe nine risk classifications currently used bythe FDIC to assign premiums.) The tablereveals substantial differences between thesegroups that are not reflected in their assessmentratings, since all are rated 1A and currently paynothing for deposit insurance.

Table 2

(See Attachment D-1 for more details on thedispersion of capital ratios for institutions rated1A.) As described below, the difficultquestions relate to choosing from a multitudeof available approaches, and evaluating theusefulness of the results.

A number of financial ratios have been shownto be indicators of the potential for futurefinancial distress, examination downgrade orfailure.7 An FDIC study of the banking crisisof the 1980s found that high loanconcentrations, rapid loan growth and highdependence on volatile liabilities were

7 O'Keefe and Reidhill (1997); Demirguc-Kunt (1991);Gajewski (1989); Whalen and Thomson (1988).

significantly associated with higherprobabilities of failure (FDIC, 1997).

Suppose we identify a set of ratios for whichhigher values often indicate higher risk, otherthings equal. One example of how to use theseratios for pricing would be to use peer analysisto identify outliers. (See Attachment D-2 foran example.)

As another example, a bank’s financial ratiosmight be used as inputs to a statistical creditscore designed to estimate failure probabilitiesbased on historical experience of banks withsimilar characteristics. The resulting scorecould be used as an indicator for the bank’spremium. Both examples are presented forillustrative purposes only, and represent onlytwo among many potential methods for usingreported financial information.

Using Call Report data to better differentiatethe risks of the majority of strong-performinginstitutions has a number of attractive features.Such data are uniform in format and regularlyavailable. At least in theory, such informationis objective. And there is a vast body ofanalytical work to draw from that is expresslydesigned to measure risk of failure using suchinformation.

One of the issues that would need to beaddressed in applying Call Report ratios iswhether to use peer comparisons or absoluteratio thresholds. Under the peer approach, aninstitution could be reclassified because it doespoorly relative to its peers, even if all of itsratios are strong by historical standards.Moreover, using purely relative comparisonswould make it difficult for bank managers todetermine exactly where their institutionswould be classified for insurance purposesprior to their actual classification. Thealternative is to use absolute benchmarks basedupon historical averages. This gives bankersexplicit targets, should they choose to shoot forthem, and ensures that more institutions move

First Decile Average (%)

Tenth Decile Average (%)

Non-Performing Loans/Loans & Leases 0 3.2

Charge-Offs/Loans & Leases 0 10.2

Loan Yield 5.1 11.1

Commercial Loan Growth -42.1 566

Volatile Liability Growth -41.4 721

Total Equity/Assets 23 6

17

into lower premium categories when theindustry is stronger. (See Attachment D-3 foran example of this approach.)

On the other hand, to the extent that the goal ofmaking additional risk distinctions is merely toensure that higher-risk institutions bear agreater share of the costs of deposit insurancethan lower-risk institutions, the purely relativecomparisons accomplish this. In drivingpricing off such peer-based ratio tests,however, attention should always be paid to theabsolute levels of the ratios, in order to avoidmaking pricing distinctions based on negligibleor economically insignificant differences infinancial ratios.

Reported information at times has beennotoriously inaccurate. The FDIC’s mostcostly bank failures in recent years haveoccurred rather abruptly among institutions thathad consistently reported strong earnings andcapital. In these cases, an examination oranother event ultimately revealed that reportedearnings had been artificial and overstatedwhile asset values had been inflatedunrealistically. In some cases, Call Report-based offsite tools were indicating that theseinstitutions should be candidates for upgradingfrom a CAMELS “2” to a “1” at the same timethat examiners were placing the institutions onthe problem list.

Another significant limitation of Call Reportinformation is that it is not detailed enough tofairly compare the risk profiles of insuredinstitutions. As a simple example, consider twoinstitutions whose Call Reports indicateidentical concentrations of consumer andresidential mortgage loans. One of theseinstitutions could be specializing in subprimeloans, and the other in conservativelyunderwritten loans, but the Call Reports wouldnot show the difference (except perhaps byinference based on loan yields or otherindicators). One institution could havesignificant commercial lending concentrations

to a few large counterparties, industries, orgeographic areas, while another, with the sameCall Report numbers, may be prudentlydiversified. Call Reports are useful incapturing some types of quantitative data, butdespite past revisions, fail to capture certainqualitative factors that also merit consideration.Reported financial information does notprovide a picture of the risk profile of thereported loans, the quality of internal controls,or, in some cases, the magnitudes of market-sensitive decisions management has made.

Market Information

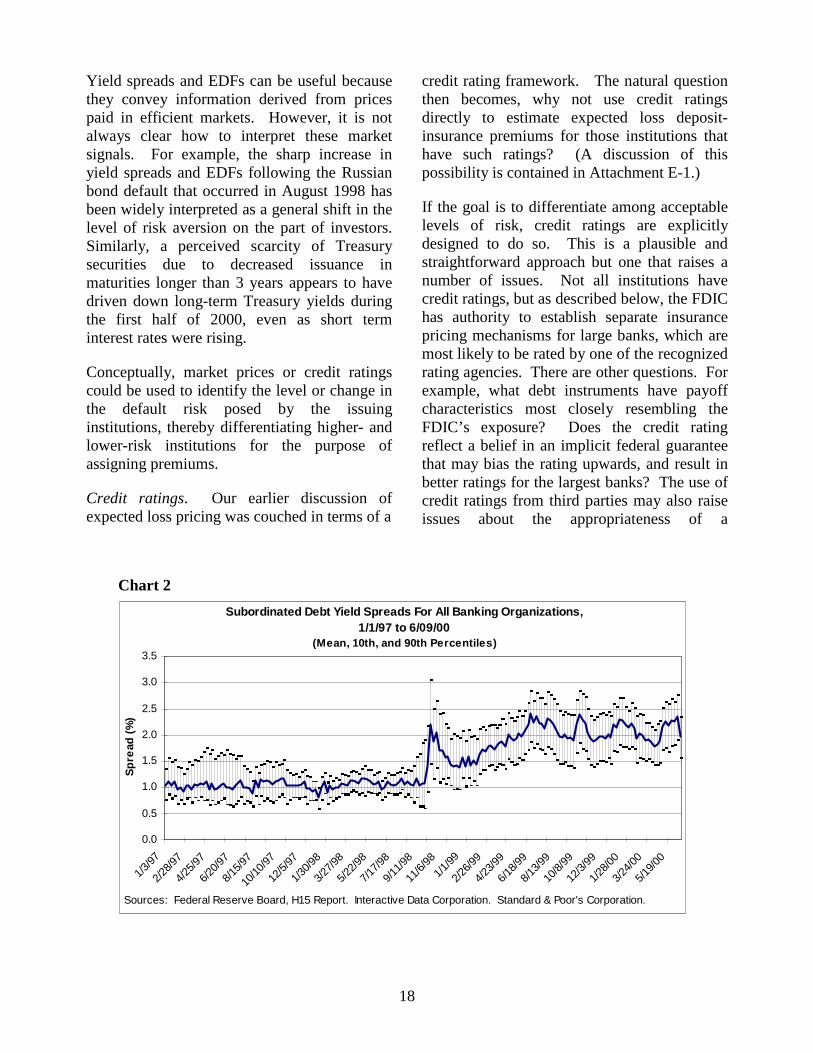

More than 750 insured institutions or theirholding companies, holding over 50 percent ofall insured deposits, currently issue debt orequity instruments that are traded in organizedfinancial markets. As indicated in Chart 2 (seenext page), market prices for these instrumentsappear to reflect a changing aggregate riskprofile over time as well as variations in riskacross institutions.

Chart 2 shows the mean and distribution ofsubordinated debt yield spreads over U.S.Treasury securities with comparable maturitiesfor the period from January 1997 to June 2000.The lower and upper bars of the graphrepresent the 10th and 90th percentile cutoffs,respectively, and are included to show thedegree to which spreads are dispersed aroundthe mean. Yield spreads increased significantlyover the period, and were particularly volatilein 1998. These widening spreads, in part, mayreflect growing investor uncertainty regardingcredit risk. Moreover, the expanding spreadbetween the yields at the 10th and 90th

percentiles suggests that market participantshave perceived an increasing disparity amongindividual institutions in recent periods. This iscorroborated by the disparity in EDFs that arebased upon asset price volatilities, in Chart 3(see page 19).

18

Yield spreads and EDFs can be useful becausethey convey information derived from pricespaid in efficient markets. However, it is notalways clear how to interpret these marketsignals. For example, the sharp increase inyield spreads and EDFs following the Russianbond default that occurred in August 1998 hasbeen widely interpreted as a general shift in thelevel of risk aversion on the part of investors.Similarly, a perceived scarcity of Treasurysecurities due to decreased issuance inmaturities longer than 3 years appears to havedriven down long-term Treasury yields duringthe first half of 2000, even as short terminterest rates were rising.

Conceptually, market prices or credit ratingscould be used to identify the level or change inthe default risk posed by the issuinginstitutions, thereby differentiating higher- andlower-risk institutions for the purpose ofassigning premiums.

Credit ratings. Our earlier discussion ofexpected loss pricing was couched in terms of a

Chart 2

credit rating framework. The natural questionthen becomes, why not use credit ratingsdirectly to estimate expected loss deposit-insurance premiums for those institutions thathave such ratings? (A discussion of thispossibility is contained in Attachment E-1.)

If the goal is to differentiate among acceptablelevels of risk, credit ratings are explicitlydesigned to do so. This is a plausible andstraightforward approach but one that raises anumber of issues. Not all institutions havecredit ratings, but as described below, the FDIChas authority to establish separate insurancepricing mechanisms for large banks, which aremost likely to be rated by one of the recognizedrating agencies. There are other questions. Forexample, what debt instruments have payoffcharacteristics most closely resembling theFDIC’s exposure? Does the credit ratingreflect a belief in an implicit federal guaranteethat may bias the rating upwards, and result inbetter ratings for the largest banks? The use ofcredit ratings from third parties may also raiseissues about the appropriateness of a

Subordinated Debt Yield Spreads For All Banking Organizations, 1/1/97 to 6/09/00

(Mean, 10th, and 90th Percentiles)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

1/3/

97

2/28

/97

4/25

/97

6/20

/97

8/15

/97

10/1

0/97

12/5

/97

1/30

/98

3/27

/98

5/22

/98

7/17

/98

9/11

/98

11/6

/98

1/1/

99

2/26

/99

4/23

/99

6/18

/99

8/13

/99

10/8

/99

12/3

/99

1/28

/00

3/24

/00

5/19

/00

Sp

read

(%

)

Sources: Federal Reserve Board, H15 Report. Interactive Data Corporation. Standard & Poor's Corporation.

19

government agency relying on informationprovided by specific private firms for importantpublic policy decisions, especially when thosefirms may have less information or experiencethan the government agency on which to basetheir judgments.

Subordinated debt. The FDIC currentlymonitors the spreads individual institutions payover comparable U.S. Treasury obligations forvarious debt instruments. Referring again toChart 2, page 18, it is clear that the mean yieldspreads on subordinated debt vary over timeand that the market differentiates observablyamong institutions in its pricing ofsubordinated debt. One could envision asystem in which institutions with the highestspreads are classified into a higher-riskcategory for premium purposes. AttachmentE-2 contains a discussion of this issue.

Subordinated debt has received considerableattention as an instrument that could enhancemarket discipline for large institutions andconvey early warning signals to regulators.Subordinated debt is regarded as particularlyattractive because the incentives of

Chart 3

subordinated debt holders line up with those ofthe FDIC; these debt holders do not share in theupside from any gambles taken by bankmanagement, and subordinated debt pricingtends to discourage imprudent risk-taking.

Owing to these characteristics, there have beenseveral proposals to require large institutions toissue some minimum amount of subordinateddebt on a regular basis. The Gramm-Leach-Bliley Act requires the Treasury Departmentand Federal Reserve Board to conduct a studyof subordinated debt requirements, and thereport is due to Congress on May 12, 2001.One of the primary arguments against asubordinated debt requirement is that itinterferes with management decisionsregarding the optimal liability structure fortheir institution. Subordinated debt is notwidely issued at the bank level, and even whereit is, it may be in amounts or on terms differentfrom those that would be mandated by aregulatory requirement.

Top 50 Institutions (by assets): EDF Values, 1/97 to 4/00 (Mean, 10th, and 90th Percentiles)

0.0

0.2

0.4

0.6

0.8

1.0

1.2

01/9

703

/97

05/9

707

/97

09/9

711

/97

01/9

803

/98

05/9

807

/98

09/9

811

/98

01/9

903

/99

05/9

907

/99

09/9

911

/99

01/0

003

/00

EDF

Source: KMV Corporation. EDF=One Year Expected Default Frequencies, w hich are derived using a proprietary options-pricing model that incorporates asset price volatilities, among other factors.

20

There are at least two broader sets of issues thatarise in connection with the use of market datafor deposit insurance premiums. One is thatthe use of market data would effectively createtwo pricing mechanisms for deposit insurance,one for larger, publicly traded institutions andanother for smaller privately held institutions.The second issue is the difficulty of extractingthe appropriate information from market prices.Price movements often reflect more than purechanges in the individual default risk of theissuing institution. For example, price changescan reflect developments in the broadereconomy or the financial markets that influencethe supply or demand for many types ofinstruments. In analysts’ terms, the “signal-to-noise” ratio associated with price changes issometimes low, and extracting the true marketsignal regarding the institution may not bestraightforward. In addition, even after the truemarket signal about an individual institutionhas been extracted, the result may notcorrespond to supervisory evaluations of thatinstitution.

The differences between large and smallinstitutions have been growing for some time.Large institutions have increasingly complexrisk profiles, global operations, and expandinglines of business, and they are subjected tomarket scrutiny in an increasingly competitiveenvironment. Small institutions remain morecommunity-based, focused on a limited numberof core businesses, and privately held. Inrecognition of these differences, FDICIAexplicitly authorized the establishment of twodistinct premium systems based upon the sizeof institutions. The FDIC has thus far notexercised this authority, given that the 1996statutory constraint effectively precludes anymeaningful distinctions. A well-establishedmovement exists within the bank regulatorycommunity toward separate approaches tosupervision and capital regulation for large andsmall institutions, and it is time to reconsiderwhether a "one-size-fits-all" approach to

deposit insurance pricing will remain suitablegoing forward.

Hybrid Approaches

We have differentiated between subjective andobjective approaches. Our current pricingsystem uses both, namely examination ratingsand capital ratios. (Attachment C provides anoverview.) Market prices are likely toincorporate both subjective and objectiveinformation, as just discussed. Other hybridapproaches could be considered. For example,the subjective factor could continue to be basedon the examination rating, with the objectivefactor being some type of risk score based onCall Report ratios, market risk indicators, orother non-public information.

All three types of information considered in thepreceding sections could be combined into ascoring system for determining premiumclassifications. The approach used by theCDIC is another example of a hybrid approach.Attachment B-2 illustrates the results ofapplying a CDIC-style approach to U.S.institutions using a subset of variables. TheCDIC system is more complicated than theFDIC system in some respects, but it is alsosimpler in that it contains only four premiumcategories.

Customized Financial Contracts

One possible way to use market information todifferentiate risks without imposing a particularfunding structure on insured institutions mightbe to go beyond simply monitoring capitalmarkets and begin entering into financialcontracts that price and share the risk of failureat individual institutions. The FDIC couldenter into financial contracts that, in exchangefor a premium paid to the holder, expose theholder to a defined risk in the event of the

21

failure of a specific institution or pool ofinstitutions. The premium that holders requireon such contracts provides information relevantto expected loss pricing.