February 21, 2011 - University of Utah

100

February 21, 2011

Transcript of February 21, 2011 - University of Utah

February 21, 2011

©2011 Micron Technology, Inc. | 2February 21, 2011

Safe HarborDuring the course of this meeting, we may make projections or other

forward-looking statements regarding future events or the future financial

performance of the Company and the industry. We wish to caution you that

such statements are predictions and that actual events or results may differ

materially. We refer you to the documents the Company files on a

consolidated basis from time to time with Securities and Exchange

Commission, specifically the Company’s most recent Form 10-K and Form

10-Q. These documents contain and identify important factors that could

cause the actual results for the Company on a consolidated basis to differ

materially from those contained in our projections or forward-looking

statements. These certain factors can be found at

http://www.micron.com/certainfactors. Although we believe that the

expectations reflected in the forward-looking statements are reasonable, we

cannot guarantee future results, levels of activity, performance or

achievements. We are under no duty to update any of the forward-looking

statements after the date of the presentation to conform these statements

to actual results.

©2011 Micron Technology, Inc. All rights reserved. Products are warranted only to meet Micron‟s production data sheet specifications. Information, products, and/or specifications are subject to change without notice. All information is provided on an “AS IS” basis without warranties of any kind. Dates are estimates only. Drawings are not to scale. Micron and the Micron logo are trademarks of Micron Technology, Inc. All other trademarks are the property of their respective owners.

©2011 Micron Technology, Inc. | 3

Steve Appleton

Chairman and CEO

2011 Micron Winter Analyst Conference

February 21, 2011

©2011 Micron Technology, Inc. | 4

Micron Evolution

February 21, 2011

► Decrease in Long Term DRAM Annual Bit Growth to < 50% year

► First Bankruptcy and Liquidation of a DRAM Company in History

► Customer Consolidation in Computing

► Government Subsidized Companies

2005

IMFTAll NOR Resources to NAND

2001

Photobit(Aptina)

2002

Toshiba DRAM

2008

MeiYa / Inotera

2006

FY2006Revenue $5.3BIncome $408ME.P.S. $0.57

Lexar

2010

Numonyx

FY2010Revenue $8.4BIncome $1.85BCash Flow $3.0BE.P.S. $1.85

► Recognized Need for Strategic Shift

► Leverage Technology Expertise

► Pursue Efficient Capital Deployment (cheap assets with scale & partnerships)

► Product Portfolio Expansion

©2011 Micron Technology, Inc. | 5February 21, 2011

33% 34%40%

27%

5%6%

10%

24%

26%26%

20%15%

23% 18%15%

15%

9% 11% 11% 17%

4% 5% 4% 2%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY08 FY09 FY10 FY11

AIMM

Networking

& Storage

Server

Consumer

Mobile

Personal

Systems

Includes DRAM, NAND, and NOR; NOR does not include purchase accounting adjustments

Application Revenue Diversification

©2011 Micron Technology, Inc. | 6February 21, 2011

Segment Revenue Diversification

77%

65%

54%50%

57%

47%

6%

23%

35%39%

34%

31%

5%

19%

17%12% 11% 11%

4% 3%

0%

20%

40%

60%

80%

100%

FY 2006 FY 2007 FY 2008 FY 2009 FY 2010 FQ1 2011

% o

f M

icro

n T

ota

l R

eve

nu

es

DRAM NAND NOR Imager

©2011 Micron Technology, Inc. | 7

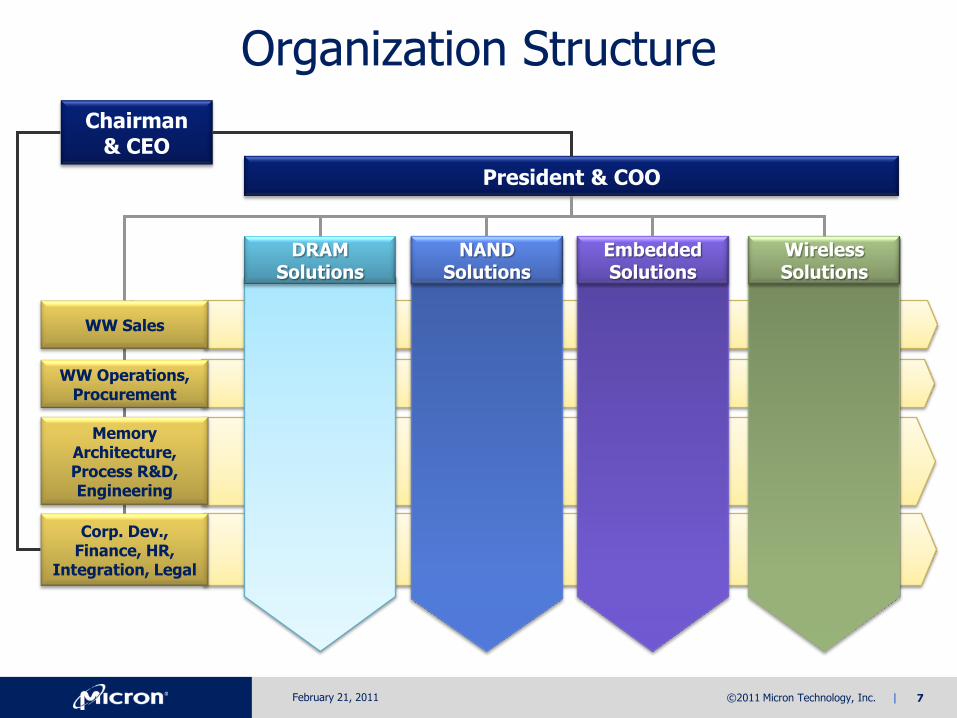

Organization Structure

WW Operations,Procurement

WW Sales

Memory Architecture,Process R&D, Engineering

Chairman& CEO

DRAM Solutions

NAND Solutions

Embedded Solutions

Wireless Solutions

President & COO

Corp. Dev., Finance, HR,

Integration, Legal

February 21, 2011

February 21, 2011

©2011 Micron Technology, Inc. | 9

DRAM Solutions Group

Brian ShirleyVice President

February 21, 2011

©2011 Micron Technology, Inc. | 10

►Cloud computing and virtualization driving need for more cores

►Further drives DRAM density, performance needs, and power concerns

► Intel’s Romley launchin 2H’11

Server

DRAM Solutions Group - DSG

February 21, 2011

►High-end routers running past traditional DRAM limits

►Customer premise equipment market exploding (CPE)

►Exploding demand from Storage market

Networking & Storage

►Visual enhancements are driving increased DRAM needs

►New game console planning underway with unparalleled speed needs

►Speed requirements increasing to 2Gbps +…

Graphics

►PC’s converted to DDR3 and up to 4GB

►Tablets using DDR2 today, soon DDR3 and early DDR4 due to power

►Sandy Bridge integrates GPU on to CPU, pushing up main memory needs

Personal Computing

©2011 Micron Technology, Inc. | 11

►Cloud computing and virtualization driving need for more cores

►Further drives DRAM density, performance needs, and power concerns

► Intel’s Romley launchin 2H’11

Server

DRAM Solutions Group - DSG

February 21, 2011

►High-end routers running past traditional DRAM limits

►Customer premise equipment market exploding (CPE)

►Exploding demand from Storage market

Networking & Storage

►Visual enhancements are driving increased DRAM needs

►New game console planning underway with unparalleled speed needs

►Speed requirements increasing to 2Gbps +…

Graphics

►PC’s converted to DDR3 and up to 4GB

►Tablets using DDR2 today, soon DDR3 and early DDR4 due to power

►Sandy Bridge integrates GPU on to CPU, pushing up main memory needs

Personal Computing

Increasing need for high density, high speed, low power DRAM solutions:

Micron’s DRAM portfolio drives the world’s infrastructure

©2011 Micron Technology, Inc. | 12

2011 Tablet shipments projected to grow 3x

Projected to out-ship desktops by 2014

Utilize a wide range of DRAM

Power is Key for Tablets

Leading in New Applications: Tablets

February 21, 2011

Mil

lio

ns S

yste

ms S

hip

pe

d

Source: Gartner 4Q‟10; Micron Market Research

Tablet Shipment Growth One of the Hottest Items at CES 2011

MB

/S

yste

m

0

600

1,200

1,800

2,400

3,000

0

50

100

150

200

250

2010 2011 2012 2013 2014

Tablet Systems Shipped Tablet Memory Content

©2011 Micron Technology, Inc. | 13

DDR4 introduction expected in 2012

▶ Main interest in power sensitive applications

Key improvements over DDR3

▶ Higher Bandwidth: Up to 3.2 Gbps

▶ Power Consumption: 1.2V drives big improvement

▶ High Density: 128Gb in single-stack, single-load

Ideal Memory for variety of applications

▶ Server ideal due to power & performance benefits

▶ Tablet PC benefit from low voltage

▶ Fast introduction in Notebooks expected

Micron fully committed to DDR4 introduction

▶ Driving JEDEC standardization

▶ Early development of DDR4 with introduction in 1H‟2012

Leading with New Interfaces: DDR4

February 21, 2011

Source: Gartner 4Q‟10

…optimized for power and performance

DDR4 Market Introduction The next major standard

0%

20%

40%

60%

80%

100%

2009 2010 2011 2012 2013 2014

SDR DDR DDR2 DDR3 DDR4

Potential DDR4 Lead Applications

Notebooks

‣Further power saving due to 1.2V

‣Performance increase to address future applications

Tablet PCs

‣Ideal application to use low power features

‣Fast adoption due to variety of controller vendors

Servers

‣Best solution for high density DIMMs

‣Significant power reduction

©2011 Micron Technology, Inc. | 14

Leading with New Technology: 3x nm

• Key features:‣ High speed operation up to 1866 Gbps DDR3 and 2400 Gbps DDR4‣ Fully 1.50V and 1.35V compatible DDR3 and 1.20V on DDR4‣ Technology and circuit design related power improvements for best-in-class power

• First samples available now

Improved Performance, Power-efficiency and Cost

• High-performance 1Gb, 2Gb and 4Gb DDR3 products for broad range of applications across all market segments

• Further power reductions and functionality down to 1.2V

• ~50% more 4Gb chips per wafer versus 42nm

• Enabling standard module densities of up to 64GB

• Lead Technology for DDR4 Introduction

Key Features and Portfolio Roll-out

February 21, 2011

©2011 Micron Technology, Inc. | 15

Leading with New Form Factors: LRDIMM

February 21, 2011

► IT, virtualization, and datacenters need for higher density

► Standard DIMMS limit scaling of capacity and performance

► Micron‟s new LRDIMM technology delivers a high performance, cost effective solution to address today‟s IT system challenges

► Broad Standard and VLP Portfolio

► Module Densities up to 64GB

► Samples available now

512GB 768GB800 Mbps

Roll-out of Portfolio

1333 Mbps

Higher-density modules at improved performance

Roll-out of Portfolio

Fully Populated System

Micron LRDIMMStandard DIMM

Happening Now

50% Higher System Capacity

67% Higher Bandwidth

©2011 Micron Technology, Inc. | 16

Leading with New Products: RLDRAM3

The best low-latency DRAM gets better

• Unprecedented performance for high-end networking

• Comparable to SRAM access time at superior costand density

• Easy transition path from RL2 platforms

• High interest of customers and key enablers

Extended success of RLDRAM2 with RLDRAM3

• Improved performance:

‣ random access time down to 10ns write and 2.5ns read

‣ doubled sustainable bandwidth of 2133 Gbps

‣ power-efficiency and high memory density

• Memory densities of 576Mb and 1.1Gb

• Samples available mid 2011, production in 2H 2011

• 2nd source partner identified

February 21, 2011

©2011 Micron Technology, Inc. | 17

Leading with New Innovations

• Evolutionary DRAM roadmaps hit limitations of bandwidth and power efficiency

• Micron introduces a new class of memory: Hybrid Memory Cube

• Unique combination of DRAMs on Logic smashes through the wall

• How did we do it?► Micron-designed logic controller

► High speed link to CPU

► Massively parallel “Through Silicon Via” connection to DRAM

• Unparalleled performance: ► Up to 20X the bandwidth of a full DDR3 DIMM

► Using a 10th of the power per bit

► Occupying an 8th of the space of an RDIMM

• Targeting high performance computing and networking, eventually migrating into computing and consumer

TSV connections

Revolutionary Approach to Break Through the “Memory Wall”

Key Features and Roll-Out

Full silicon prototypes in siliconTODAY

February 21, 2011

©2011 Micron Technology, Inc. | 18

Hybrid Memory Cube Prototype

18 February 21, 2011

©2011 Micron Technology, Inc. | 19

DRAM Solutions Group

February 21, 2011

► Focus on segments driven by exploding bandwidth and computing needs

► Broad product portfolio focused on optimal solutions across performance, power, and density

► Leadership in next generation solutions, driving enhanced margin opportunities

February 21, 2011

©2011 Micron Technology, Inc. | 21

NAND Solutions Group

Glen HawkVice President

February 21, 2011

©2011 Micron Technology, Inc. | 22

Embedded, AIMM'

PC/Comp (Non-SSD)

Mobile

DSC/VIDEO

USB

MP3/PMP

SSD

Tablets

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2008 2009 2010 2011 2012 2013 2014

GB

(M

)

February 21, 2011

Source: Gartner 4Q10; Cards included in Mobile and DSC

2010 – 2014 NAND

Bit CAGR

71%

140%

118%

46%

59%

36%

97%

85%

NAND Market Diversity

©2011 Micron Technology, Inc. | 23

Embedded, AIMM'

PC/Comp (Non-SSD)

Mobile

DSC/VIDEO

USB

MP3/PMP

SSD

Tablets

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2008 2009 2010 2011 2012 2013 2014

GB

(M

)

February 21, 2011

Source: Gartner 4Q10; Cards included in Mobile and DSC

Micron‟s Business Units focused on NAND

Wireless Solutions Group

Embedded Solutions Group

NAND Solutions Group

SSDs $2.5B market in 2011 going to $7B+ in 2014

©2011 Micron Technology, Inc. | 24

Digitization of Photography

February 21, 2011

©2011 Micron Technology, Inc. | 25

Digitization of Photography

February 21, 2011

©2011 Micron Technology, Inc. | 26

Transformation of File Storage

February 21, 2011

©2011 Micron Technology, Inc. | 27

Transformation of File Storage

February 21, 2011

©2011 Micron Technology, Inc. | 28

Revolution of Music

February 21, 2011

©2011 Micron Technology, Inc. | 29

Revolution of Music

February 21, 2011

©2011 Micron Technology, Inc. | 30

The Next Revolution: Computing

February 21, 2011

©2011 Micron Technology, Inc. | 31

The Next Revolution: Computing

Micron ReadlSSDTM

C400 for ClientP300 for Enterprise

February 21, 2011

©2011 Micron Technology, Inc. | 32

Embedded, AIMM'

PC/Comp (Non-SSD)

Mobile

DSC/VIDEO

USB

MP3/PMP

SSD

Tablets

0.0

20.0

40.0

60.0

80.0

100.0

120.0

2007 2008 2009 2010 2011 2012 2013 2014

GB

(M

)

2010 – 2014 Total NANDBit CAGR:

78%

NAND in New Applications

February 21, 2011

Source: Gartner 4Q10; Cards included in Mobile and DSC

2010 – 2014 NAND

Bit CAGR

71%

140%

118%

46%

59%

36%

97%

85%

©2011 Micron Technology, Inc. | 33

Enterprise Commands Significant ASP Upside

February 21, 2011

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2009 2010 2011 2012 2013 2014

1G

B E

U S

SD

Sh

ipm

en

ts (

M)

Enterprise PC

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

2009 2010 2011 2012 2013 2014

SS

D R

eve

nu

e (

$B

)

Enterprise PC

Source: IDC 3Q10

$21.93

$14.76

$8.41

$5.29

$3.32$2.26$2.47

$1.53$1.07 $0.86 $0.63 $0.47

$0

$5

$10

$15

$20

$25

2009 2010 2011 2012 2013 2014

1G

B E

U S

SD

AS

P

Enterprise SSD PC SSD

©2011 Micron Technology, Inc. | 34

10

20

30

40

50

60

C1Q07 C1Q08 C1Q09 C1Q10

Pro

ce

ss N

od

e (

nm

)

Volume Production Dates

Company A Micron Company B Company C

3x nm

5x nm

2x nm

Data based on publically available information

NAND Silicon Leadership

February 21, 2011

©2011 Micron Technology, Inc. | 35

NAND System Solution Leadership

Enterprise SSD Accolades – P300Client SSD Accolades – C300/C400

“All in all, the P300 deserves a strong look when trying to improve server performance.”

“…delivering 44,000 IOPS for random reads and 16,000 IOPS for random writes to target demanding enterprise applications.”

“…enterprise SSD suppliers lacking a fab partnership, who buy flash chips on the general market, may be at a disadvantage…”

“Dubbed RealSSD P300, this new series comes out of the gates with SATA 6Gbps support -- a first ever for the enterprise market…”

“Memory & Storage: Micron Technology C300 and P300 solid-state drives.”

February 21, 2011

©2011 Micron Technology, Inc. | 36

Enterprise HDD and SSD Revenue

February 21, 2011

Sources: iSuppli 4Q10; IDC 3Q10; Micron Market Research

$0.05

$0.16

$0.39

$0.49

$0.00

$0.35

$0.70

$2.00

$6.00

2009 2010 2014

En

terp

rise

Re

ve

nu

e (

$B

)

$4.80$2.5 - $3.1

$5.13

$6.08

$5.2 $5.8

$8.0-9.0

Enterprise SSD (NAND Producers) Enterprise SSD (3rd Parties) Enterprise HDD

©2011 Micron Technology, Inc. | 37

NAND Solutions Group

February 21, 2011

► Business unit dedicated to the rapidly growing NAND data storage market

► Exploiting technology leadership, from Silicon to Systems

► Targeting incremental margin opportunities in premium segments, as a complete storage system provider

February 21, 2011

©2011 Micron Technology, Inc. | 39February 21, 2011

Wireless Solutions Group

Mario LicciardelloVice President

©2011 Micron Technology, Inc. | 40

Market Dynamics

February 21, 2011

Segmentation Technology Trends

SmartPhone & Premium ASP >$150 Growth accelerator for both NAND and DRAM (LPDDR1LPDDR2)

Entry ASP < 150$High Volume, long term market for NOR/PSRAM & Growth Driver for PCM & Low Density LPDDR2

Source: iSuppli 4Q10; Flash memory forecast 2012 and beyond and DRAM forecast from Micron WSG Q4 2010

0

200

400

600

800

1,000

1,200

2009 2010 2011 2012 2013 2014

Un

its (

M)

Smart Phone Non Smart Phone

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Fla

sh

DR

AM

Fla

sh

DR

AM

Fla

sh

DR

AM

Fla

sh

DR

AM

Fla

sh

DR

AM

Fla

sh

DR

AM

2009 2010 2011 2012 2013 2014

Un

its (

M)

NOR PCM NAND mDRAM pSRAM

©2011 Micron Technology, Inc. | 41

Mobile Memory Market

Source: Isuppli Q4 2010

Source: iSuppli, 4Q10

11$B

6$B

2$B1$B

NAND

NOR

pSRAM

mDRAM

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

$14.0

$16.0

$18.0

$20.0

2009 2010 2011 2012

Mo

bil

e M

em

ory

Re

ve

nu

e (

$B

) DRAM Market sustained

LPDDR1 LPDDR2 LPDDR3 / Wide I/O

Density Growth per Handset 128Mb8Gb

NAND Market strong growth

Density (GB) growing faster than litho migration

NOR + PCM Market stable

PCM compensating NOR Market erosion starting early 2012

PSRAM Market declining

Strongly associated to low Density NOR

PSRAMLPDDR

February 21, 2011

©2011 Micron Technology, Inc. | 42

• Micron memory present in more than

550 million phones in 2010

• Key memory supplier of all top leading phone manufacturers

• Well positioned to capitalize on SmartPhone market growth

• Full range of optimized Memory Solutions

• Driving and committed to next generation standards

Leading Wireless Memory Supplier

February 21, 2011

©2011 Micron Technology, Inc. | 43

Micron Addresses All Mobile Market Sub-Segments

February 21, 2011

Smart PhonesEntry / Connectivity Media Tablet

• NOR+ PSRAM MCP

• NOR +LPDDR MCP

• OneNAND + LPDDR MCP

• NAND + LPDDR MCP

• PCM+LPDDR2MCP*

• NAND + LP DDR MCP

• e.MMC + LP DDR2 MCP

• e.MMC Discrete

• LP DDR1/LP DDR2 PoP

• LP DDR3*

• Wide I/O*

• e.MMC Discrete

• LP DDR1

• LP DDR2

• LP DDR3*

• Wide I/O*

*In Design and/or Development

©2011 Micron Technology, Inc. | 44

Industry‟s Most Advanced Mobile Memory Solutions

1Gb 2Gb 256Mb 1Gb 512MB - 2GB (SLC)

Mobile DRAM DiscreteLPDDR1 or LPDDR2

(POP)

e.MMC 4.41 Discrete(BGA)

e.MMC4.41 + LPDDR1/2

SLC NAND + LPDDR1/2

34 / 25 nmNAND (SLC)

50 / 42 nmMobile DRAM

(LPDDR1 or LPDDR2)

25 nme.MMC4.41

NAND MCP

Packaging Options

32 Mb 256Mb 16Mb 128Mb PSRAM

65 / 45 nmNOR

65 / 45 nmNOR

50 nm

Mobile RAM

NOR + PSRAM

NOR MCP

Packaging Options

128Mb 512Mb LPDDR NOR + LPDDR512 Mb 1Gb

2Gb 4Gb4Gb 16Gb 4GB - 32GB (MLC)

February 21, 2011

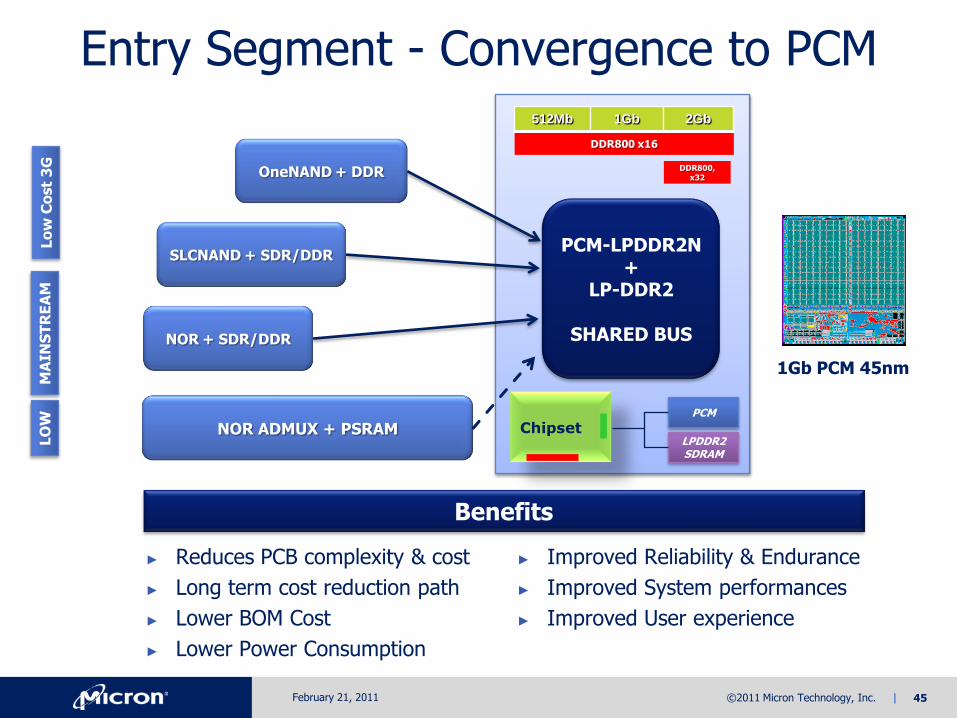

©2011 Micron Technology, Inc. | 45

► Reduces PCB complexity & cost

► Long term cost reduction path

► Lower BOM Cost

► Lower Power Consumption

Entry Segment - Convergence to PCM

ChipsetPCM

LPDDR2SDRAM

NOR ADMUX + PSRAM

LO

WM

AIN

ST

RE

AM

Lo

w C

ost

3G

NOR + SDR/DDR

SLCNAND + SDR/DDR

OneNAND + DDR

DDR800 x16

DDR800, x32

512Mb 1Gb 2Gb

► Improved Reliability & Endurance

► Improved System performances

► Improved User experience

PCM-LPDDR2N+

LP-DDR2

SHARED BUS

1Gb PCM 45nm

Benefits

February 21, 2011

©2011 Micron Technology, Inc. | 46

Smart Phone‟s Dependence on NAND Leverages Micron‟s Strengths

Category / 2011 needs

Density

Raw NAND LP-DRAM e.MMC

High-end Smartphone 4-16Gb 4Gb+ 16-64GB

Low-end Smartphone 4Gb 2Gb 4-16GB

Feature Phone 1-2Gb 512-1Gb 2-8GB

February 21, 2011

©2011 Micron Technology, Inc. | 47

• Strong Market Reaction

▶ Expected 57Mu Tablet in „11, > 100Mu expected in 2012

• Total Convergence between Computing & Consumer in Mobile Environment

▶ Connectivity & Mobility are the Key success factors

Tablets, the Next Major Opportunity

• Mobile BOM fully supported by Micron‟s Memory Portfolio:

▶ LPDDR1/2: 4Gb+ LPDDR3 , Wide I/O

▶ e.MMC: 32GB+ UFS

▶ System Memory for 3G+ modem NAND / NOR PCM

0

100

200

300

400

500

600

700

800

900

PC

Wir

ele

ss

PC

Wir

ele

ss

PC

Wir

ele

ss

PC

Wir

ele

ss

PC

Wir

ele

ss

PC

Wir

ele

ss

PC

Wir

ele

ss

2008 2009 2010 2011 2012 2013 2014

Un

it S

hip

me

nts

(M

)

Desktop PC Mobile PC Smartphone Tablet

Source: iSuppli, 4Q10

February 21, 2011

©2011 Micron Technology, Inc. | 48

Wireless Solutions Group

February 21, 2011

►Industry‟s broadest portfolio of DRAM, NAND, and NOR products to address the wireless market

►Targeting growth and market share opportunities in smart phones and tablets

►Focusing on technology leadership, customer satisfaction, and execution excellence for margin optimization across the spectrum of wireless markets

February 21, 2011

©2011 Micron Technology, Inc. | 50

Embedded Solutions Group

Tom EbyVice President

February 21, 2011

©2011 Micron Technology, Inc. | 51

The Embedded Memory Market

Sources: iSuppli, Micron Market Research

Technology Diversity

Customer Diversity

2011

$9.5B Opportunity

*IMM: Industrial, Medical, Mil/Aero

Segment Diversity

ConsumerNetworking

IMM*

Automotive

PC (NOR)

DRAM NAND

NOR

3000+ Customers

Top 50 Customers

February 21, 2011

©2011 Micron Technology, Inc. | 52

Need for Leading Edge Technology AND Longevity

ESG Outlook

Normalized to 300mm wafers

Ramp Next Node

Leading Edge ProductsInitial Ramp• DSG: PC • NSG: Storage, Removable, PMP

Mainstream Products• ESG: Consumer, PC • DSG: Server, Networking• NSG: Storage, SSD• WSG: Smart Phones

Legacy ProductsLong Lifecycles• ESG: Automotive, IMM, Networking

2011 2012 2013

Micron estimates

K W

afe

rs

Leading Lithos

Legacy Lithos

February 21, 2011

©2011 Micron Technology, Inc. | 53

Micron‟s Competitive Advantage inthe Embedded Markets

February 21, 2011

Competitor Ranking

Product Line Breadth

Segment Focus

Leading Edge Technology

Longevity

Cost

©2011 Micron Technology, Inc. | 54

Embedded Applications

February 21, 2011

$0

$1,300

2011 2012 2013

$M

Infotainment Other Automotive Segments

$0

$2,500

2011 2012 2013

$M

Medical Mil/Aero Industrial

Networking: Wireless Data Drives Bit Growth Consumer: Explosive NAND/DRAM Bit Growth

Automotive: Infotainment Drives Growth IMM: $2B Market, New Focus for Micron

0

90

2011 2012 2013

Mil

lio

ns o

f M

B

DRAM NAND NOR

Sources: iSuppli, Infonetics, Micron Market Research

0

1,600

2011 2012 2013

Mil

lio

ns o

f M

B

NAND DRAM NOR

©2011 Micron Technology, Inc. | 55

Micron‟s Strategy to Win in Embedded

February 21, 2011

Product Breadth

©2011 Micron Technology, Inc. | 56

Micron‟s Strategy to Win in Embedded

February 21, 2011

Technology Leadership

©2011 Micron Technology, Inc. | 57

Micron‟s Strategy to Win in Embedded

Stability

February 21, 2011

©2011 Micron Technology, Inc. | 58

Micron‟s Strategy to Win in Embedded

February 21, 2011

Trusted Memory Advisor

©2011 Micron Technology, Inc. | 59

Embedded Solutions Group

February 21, 2011

► Targeting growth opportunities in this high-margin segment addressing a large and diverse customer base

► Broad product portfolio and technology leadership across DRAM, NAND, and NOR

► Strong customer support capabilities with supply stability and world-class service for direct and indirect sales

February 21, 2011

©2011 Micron Technology, Inc. | 61

Efficient Operating Model

Mark DurcanPresident and COO

February 21, 2011

©2011 Micron Technology, Inc. | 62

Organization Structure

Chairman& CEO

DRAM Solutions

NAND Solutions

Embedded Solutions

Wireless Solutions

President & COO

Corp. Dev., Finance, HR,

Integration, Legal

February 21, 2011

WW Operations,Procurement

WW Sales

Memory Architecture,Process R&D, Engineering

©2011 Micron Technology, Inc. | 63

Efficient and Effective Partnerships

MP MASK

February 21, 2011

©2011 Micron Technology, Inc. | 64

Global Scale, Resources, and Capital

February 21, 2011

Idaho

Utah

Texas

Minnesota

Virginia

Puerto Rico

Scotland

England Switzerland

Italy

Singapore

India

China

Taiwan

S. Korea

Japan

China

Idaho Utah Virginia Puerto Rico Italy Singapore Japan

Taiwan

ColoradoCalifornia

Israel

Malaysia

Israel Singapore MalaysiaItalyCalifornia

Philippines

©2011 Micron Technology, Inc. | 65

IM Flash Singapore

February 21, 2011

©2011 Micron Technology, Inc. | 66

20 nm

25 nm

-

20,000

40,000

60,000

80,000

100,000

120,000

Wa

fer

Ou

ts

Pe

r M

on

th (

30

0m

m E

U)

Additional capacity is dependant on market

conditions

Today 1Q ‘11

IM Flash Singapore Update

Source: Micron LPI WW02

2010 2012

February 21, 2011

©2011 Micron Technology, Inc. | 67

25nm NAND Prime Die Wafer MapIMFS 97% Yield 25nm Wafer

February 21, 2011

©2011 Micron Technology, Inc. | 68

2x nm

3x nm

42 nm

50 nm

Trench

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

Wa

fer

Sta

rt P

er

Mo

nth

Today 1Q11

Inotera Update

Source: Company Data

2010 2012

February 21, 2011

©2011 Micron Technology, Inc. | 69

Manassas Fab

February 21, 2011

©2011 Micron Technology, Inc. | 70

MTV Capacity

3x nm (DRAM)

50 nm (DRAM)

70 nm (DRAM)

20 nm (NAND)25 nm (NAND)

34 nm (NAND)

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Wa

fer

Ou

ts P

er

Mo

nth

(3

00

mm

EU

)

Today 1Q ‘11

2010 2012

200mm includes DRAM and NOR 200mm Capacity

February 21, 2011

©2011 Micron Technology, Inc. | 71

200mm

IMFT

MTV

TECH

Inotera

IMFS

IMFS (based on market)

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

Wa

fer

Ou

ts P

er

Mo

nth

(3

00

mm

EU

)

Today 1Q ’11

Micron Fab Capacity

February 21, 2011

2010 2012

200mm includes DRAM and NOR 200mm Capacity

©2011 Micron Technology, Inc. | 72

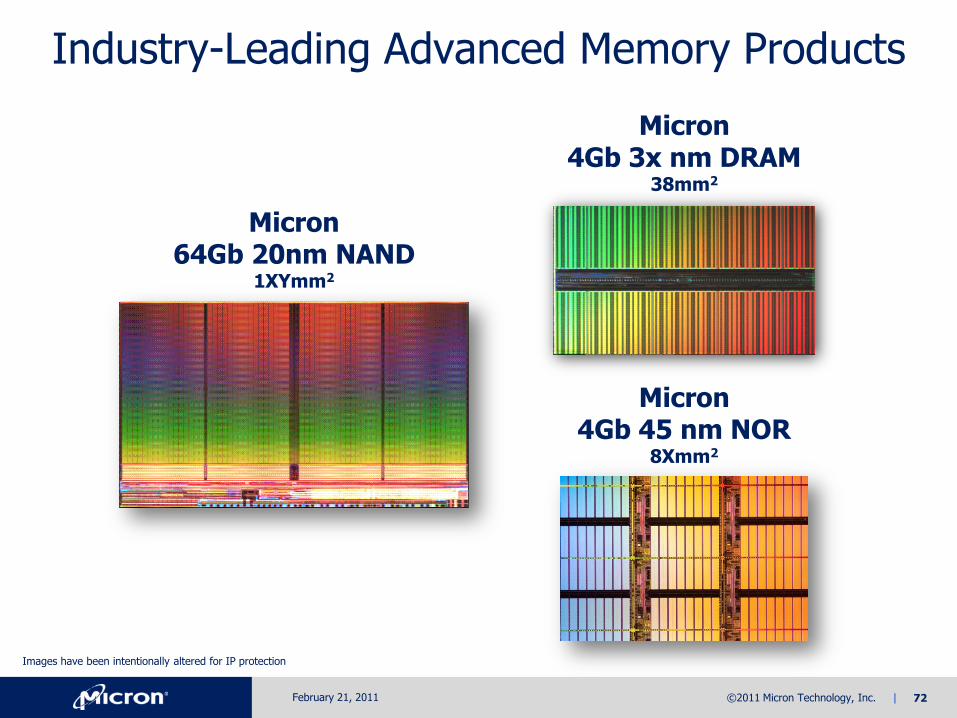

Industry-Leading Advanced Memory Products

February 21, 2011

Images have been intentionally altered for IP protection

Micron 4Gb 3x nm DRAM

38mm2

Micron 64Gb 20nm NAND

1XYmm2

Micron 4Gb 45 nm NOR

8Xmm2

©2011 Micron Technology, Inc. | 73

Emerging Memory Strategy

February 21, 2011

• A very large number of emerging memory technologies with different strengths (table below)

• Careful evaluation, strategic partnerships, and internal evaluations to achieve successful positioning

NAND PCM PCMS MVO CBRAM STT-RAM FeRAM MRAM Molecular

DataRetention

Bit Density(Cost)

Endurance

PowerPer Bit

Manufac-turability

Low Medium High Extreme

RISK

©2011 Micron Technology, Inc. | 74

Micron Global Sales Channels

OEM DistributionRetail

MicronSales Channels

E-commerce

• Optimized to support four business units

• Support diverse and differentiated businesses

• Covering the full spectrum of available sales channels

February 21, 2011

©2011 Micron Technology, Inc. | 75

Operations

February 21, 2011

► Scaling and technology development through partnerships

► Cost reduction runway

► Advanced technology leadership

► Sales channels optimized to support diverse and differentiated businesses

February 21, 2011

©2011 Micron Technology, Inc. | 77

Financial Strengthand Leverage

Ron FosterCFO

February 21, 2011

©2011 Micron Technology, Inc. | 78

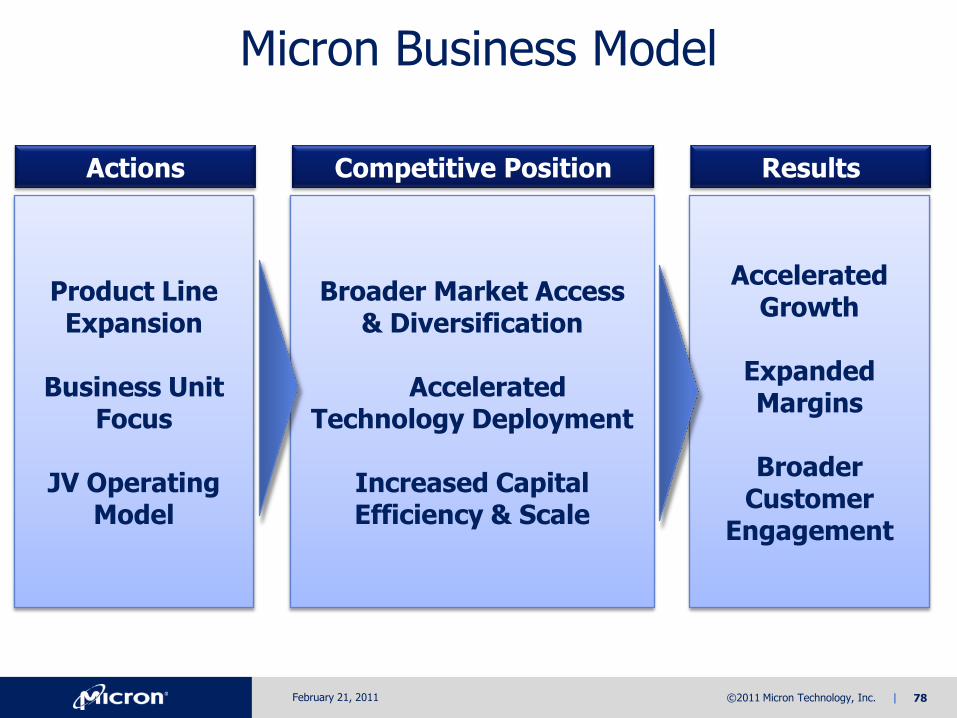

Product Line Expansion

Business Unit Focus

JV Operating Model

Broader Market Access & Diversification

Accelerated Technology Deployment

Increased Capital Efficiency & Scale

Accelerated Growth

Expanded Margins

Broader Customer

Engagement

Actions Competitive Position Results

Micron Business Model

February 21, 2011

©2011 Micron Technology, Inc. | 79

Micron‟s Business Unit Structure

February 21, 2011

EmbeddedSolutions

Group

DRAM Solutions

Group

WirelessSolutions

Group

NAND Solutions

Group

DRAM only

High-volumeDRAM sold to:

• PC

• ConsumerElectronics

• Networking

• Server

DRAM, NAND, NOR

Sold to:

• Automotive

• Industrial

• Networking

• Server

NOR, NAND to:• Consumer

Electronics

• Networking

• PC, Server

NAND only

High-volume NAND sold to:

• Data Storage

• Personal Music Players

• Foundry salesto Intel (IMFT)

DRAM, NAND, NOR

Sold to:

• Mobile

Business Units by Market

©2011 Micron Technology, Inc. | 80

FQ1‟11 by Business Unit

February 21, 2011

40%

22%

23%

12%

3%

Revenue

(Estimate)

©2011 Micron Technology, Inc. | 81

Manufacturing and Technology JVs

February 21, 2011

OwnershipOutput Share

Output Share

NAND Micron Micron Intel

51% 51% 49%

78%2 78%1 22%1

DRAM Micron Micron Nanya

30% 50%3 50%

1 With delay of 12 months following change in ownership 2As of December 2010 3Not tied to Ownership

©2011 Micron Technology, Inc. | 82February 21, 2011

Joint Venture StrategyLeverage through Scale and Shared Investment

* DRAM partner funding includes $84M for royalties and other R&D services recorded as 2010 revenue

$624M

$104M

$135M

DRAM Partner Funding*

NAND Partner Funding

Micron R&D

R&D 2010

©2011 Micron Technology, Inc. | 83

Micron87%

Canon10%

HP3%

TECH Buyout

Micron100%

Small Impact to P&L (Minority Interest)

Q1 ‘10 Q2 ‘10 Q3 ‘10 Q4 ‘10 2010 Q1 ‘11

$(2) $14 $21 $17 $50 $17

February 21, 2011

Balance Sheet Impact

Assets Equity

Cash $(159)

Non-controlling Interest $224

Additional Paid in Capital $(65)

Total $M $(159) $159

©2011 Micron Technology, Inc. | 84

15%

35%

42%

56% 57%

60%

66%

82%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

MicronFQ1-11

WinbondCQ4-10

HynixCQ4-10

ElpidaCQ4-10

InoteraCQ4-10

PowerchipCQ3-10

NanyaCQ3-10

ProMOSCQ3-10

De

bt

to C

ap

ita

lDebt to Capital Ratio

(Most Recent Quarter)Debt to Capital = (LT Debt + Current Portion of LT Debt + ST Borrowings) / (LT Debt + Current Portion of LT Debt + ST Borrowings + Balance Sheet Equity + Minority Interest)

Source: Company Data, Micron Market Research

February 21, 2011

©2011 Micron Technology, Inc. | 85

$595

-$510

-$1,771 -$1,825 -$1,856

-$2,077

-$3,190 -$3,215

-$3,500

-$3,000

-$2,500

-$2,000

-$1,500

-$1,000

-$500

$0

$500

$1,000

MicronFQ1-11

WinbondCQ4-10

PowerchipCQ3-10

ProMOSCQ3-10

NanyaCQ3-10

InoteraCQ4-10

ElpidaCQ4-10

HynixCQ4-10

Mil

lio

ns o

f U

S$

Net Cash Position(Most Recent Quarter)

Source: Company Data, Micron Market Research

Net Cash = Gross Cash - (Long-term Debt + Short-term Borrowings + Current Portion of LT Debt)

February 21, 2011

©2011 Micron Technology, Inc. | 86

5.2x

1.3x

0.9x

0.6x

0.3x 0.2x 0.2x 0.1x0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

MicronFQ1-11

ElpidaCQ4-10

HynixCQ4-10

WinbondCQ3-10

InoteraCQ4-10

NanyaCQ3-10

PowerchipCQ3-10

ProMOSCQ3-10

Ca

sh

to

Sh

ort

-te

rm D

eb

tCash to Short-Term Debt

(Most Recent Quarter)

Source: Company Data, Micron Market Research

Cash to ST Debt = Cash / (Short-term Borrowings + Current Portion of LT Debt)

Note: Short-term debt includes lease obligations

February 21, 2011

©2011 Micron Technology, Inc. | 87

Revenue by GeographyMicron FY‟10 Sales Revenue

EuropeAsia1 Americas2

Source: Micron Technology, Inc. 2010 Form 10-K1 – Asia includes China, Asia Pacific, Malaysia, and Taiwan2 – Americas includes United States and Other

February 21, 2011

©2011 Micron Technology, Inc. | 88

Micron‟s Total Wafer Production by Geography

February 21, 2011

00%

00%

00%

00%

Americas37%

Europe3%Japan

4%

Asia/Pac56%

CY2012FCY2008

©2011 Micron Technology, Inc. | 89

FY2011 CapEx Guidance

February 21, 2011

DRAM

NAND

NOR&

Other

$2.4B - $2.9B

©2011 Micron Technology, Inc. | 90

Financial Strength and Leverage

February 21, 2011

► Cost and growth leverage with partnership models and increasingly low-cost manufacturing base

► Capital deployment focused on high growth NAND market with positive P&L implications going forward

► Strong financial position versus competitors

February 21, 2011

©2011 Micron Technology, Inc. | 92

Memory Leadership

Steve Appleton

Chairman and CEO

February 21, 2011

©2011 Micron Technology, Inc. | 93

DRAM vs NAND Market Development

February 21, 2011

Source: Gartner 4Q10

$0

$5

$10

$15

$20

$25

$30

1 2 3 4 5 6 7 8 9 10 11 12 13 14

$B

Year

DRAM Revenue: 1981-1994 NAND Revenue: 1998-2011E

©2011 Micron Technology, Inc. | 94February 21, 2011

Memory Industry CapEx

3,870

7,730

15,862

18,877

12,962

6,583 6,229

11,486

6,533

4,3686,066

11,527 11,669

16,395

21,843

11,752

5,351

13,332

9,970

696

5,371

8,707

11,783

7,177

2,669

7,111

9,638

632

1,856

2,165

1,950

1,490

317

706 716

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

NOR

NAND

DRAM

Mil

lio

ns o

f $

US

Source: Gartner 4Q10

©2011 Micron Technology, Inc. | 95February 21, 2011

Forecasts Point to Technology as the Main DRAM Industry Supply Growth Driver

Sources: Gartner, IDC, iSuppli, Merrill Lynch, and Credit Suisse from 2006-2008; Average of Gartner, IDC, and iSuppli 2009-2010, Micron Forecast, Finance Strategy Group – drivers split

1% 3%

-7% -8%

14%

0%2%

26%

46%

20%

-6%

0%

2%5%

25%

37%

50%

36%

31%49% 41%

52%

87%

63%

22%

46%

50%48%

-30%

-10%

10%

30%

50%

70%

90%

2006 2007 2008 2009 2010 2011 2012

DR

AM

Bit

Su

pp

ly G

row

th

Utilization Capacity Technology Supply Growth

©2011 Micron Technology, Inc. | 96February 21, 2011

Forecasts see Technology as the Main NAND Industry Supply Growth Driver

2% -1% -5% 0% 6% 0% 1%

86%

64%

32%

-4%

8% 12%24%

125%

111%

103%

43%

56%71%

55%

213%

174%

130%

40%

70%

82% 80%

-50%

0%

50%

100%

150%

200%

250%

2006 2007 2008 2009 2010 2011 2012

NA

ND

Bit

Su

pp

ly G

row

th

Utilization Capacity Technology Supply Growth

Sources: Gartner, IDC, iSuppli, Merrill Lynch, and Credit Suisse from 2006-2008; Average of Gartner, IDC, and iSuppli 2009-2012, Finance Strategy Group – drivers split

©2011 Micron Technology, Inc. | 97

1%

1%

2%

2%

3%

4%

10%

11%

16%

17%

35%

0% 10% 20% 30% 40%

Macronix

ProMOS

Winbond

Spansion

Nanya

PSC

Elpida

Toshiba/SanDisk

Micron

Hynix

Samsung

Last Twelve Months Memory Revenue (% of Group Total)

Today‟s Memory Industry

DRAM NAND NOR

Single Memory Developers

DRAM + NAND Developers

ProducersJV Producers

DRAM + NAND + NOR Developers

Note: Micron includes Numonyx revenue and NAND sold to Intel from IM Flash; data from FQ2‟10 – FQ1‟11Competitors data from CQ1‟10 – CQ4‟10Source: Company Data, Micron Market Research Estimates

February 21, 2011

February 21, 2011

©2011 Micron Technology, Inc. | 99

Q&A

February 21, 2011