Featured Articles - CRA Magazine · 2 Canadians Resident Abroad Nov/Dec 2012 Contents Join our...

28

The Basics of Canadian Residency A basic understanding of PPNs 30 Big Ideas: Energy 30 Big Ideas: Financials this issue Tax Issues P.4 PPNs P.7 Energy P.12 Financials P.19 Canadians Resident Abroad ISSUE 6: Nov/Dec 2012 Featured Articles The Basics of Canadian Determining the tax consequences of moving to another country, whether permanently or temporarily, requires some foresight. Since Canadian resi- dents are taxed on worldwide income, maintaining residency in Canada Read more: page 4 Understanding PPNs As the name implies, in a Principal Protected Note, the principal amount invested is generally protected if held until maturity. Read more: page 7

Transcript of Featured Articles - CRA Magazine · 2 Canadians Resident Abroad Nov/Dec 2012 Contents Join our...

The Basics of Canadian Residency

A basic understanding of PPNs

30 Big Ideas: Energy

30 Big Ideas: Financials

this issue

Tax Issues P.4 PPNs P.7

Energy P.12 Financials P.19

Canadians Resident Abroad

ISSUE 6: Nov/Dec 2012

Featured Articles

The Basics of Canadian

Determining the tax consequences of

moving to another country, whether

permanently or temporarily, requires

some foresight. Since Canadian resi-

dents are taxed on worldwide income,

maintaining residency in Canada

Read more: page 4

Understanding PPNs

As the name implies, in a Principal

Protected Note, the principal amount

invested is generally protected if held

until maturity.

Read more: page 7

2

Canadians Resident Abroad Nov/Dec 2012

Contents

Join our Facebook

group

Publisher: Dax Sukhraj Editor: Dax Sukhraj

Editorial Board: Pervez Patel Arun Nagratha

Dax Sukhraj

CRA Magazine is Canada’s first e-magazine designed specifically for Canadians who are presently

living abroad, who have done so in the past or who are contemplating an out-of-country sojourn in

the future.

Our magazine is distributed electronically free of charge to subscribers in 142 countries around the

world. In addition to sound and timely advice in the investment and tax arenas, CRA e-magazine

covers everything from offshore employment, vacation/travel and international real estate informa-

tion to country profiles, medical/insurance and education options for your children.

3

Canadians Resident Abroad Nov/Dec 2012

First Word

Welcome to the Nov/Dec 2012 edition of CRA Magazine.

In this issue, our residency experts Arun and Wayne write an important article about the basics of Canadian residency for

tax purposes. This article has been revised from its original release in 2004. As we receive lots of inquires about these

issues, our readers should find this article very useful.

Abu Nizam writes about Principal Protected Notes (commonly known as PPNs) in a simplistic way to give a general in-

troduction about this sophisticated financial product. This is the first of a two part series as he writes about how the prod-

uct works from a technical point of view.

Fidelity Investments Canada has published 30 big ideas for 2012 and beyond for all 10 sectors. We think readers will

benefit from these themes when making investment decisions. We would like to publish all 30 ideas but it will become so

enormous that it would take three editions of our magazine to cover it. We have decided to publish only 6 ideas from 2

sectors instead.

We sincerely hope that you enjoy this issue. Should you wish to contact us please send an e-mail to

[email protected]. As always, your questions and comments are welcomed.

Dax Sukhraj

Publisher

4

The Basics of Canadian Residency for

Tax Purposes

Arun (Ernie) Nagratha, CA, CPA

Wayne Bewick, CA, CFP, CPA

This article has been revised from its original release in 2004.

Residency and worldwide income

Determining the tax consequences of moving to another

country, whether permanently or temporarily, requires

some foresight. Since Canadian residents are taxed on

worldwide income, maintaining residency in Canada will

require you to file a Canadian tax return on an annual

basis, including in your return income from all sources,

both Canadian and foreign. You may also be required to

file a tax return in the country you are going to live in. If

you sever your Canadian residency for tax purposes, a

final “departure tax return” should be filed in Canada.

Since many other countries around the world have lower

individual income tax rates than Canada, you may want

to sever your residency in order to be in a situation

where you will no longer be taxed on your worldwide in-

come in Canada. It is important that before you make

that decision, you first determine if you are even in a po-

sition to be able to sever residency and whether it makes

sense in your situation. Tax residency does not affect

your citizenship or legal residency status. It is specific to

tax.

Determining if you are a resident of Canada for tax pur-

poses depends on your intention at the time you leave

Canada. You must ask yourself if you plan to return to

Canada in the “foreseeable” future. If your plans are not

to return to Canada, you may be in a position to sever

your residency with Canada if you support your intention

to remain abroad by severing your residential ties with

Canada. There is no specific time period after which you

will be seen to be a non-resident of Canada, so it is im-

portant that the steps you take to prove your intention to

be a non-resident are followed carefully.

Residential ties with Canada

Residential ties with Canada are typically seen as pri-

mary or secondary. It is important that you sever all pri-

mary residential ties when ceasing residency. Maintain-

ing any significant primary ties could be looked at by the

Canada Revenue Agency (CRA) as causing your resi-

dency to be maintained in Canada. Secondary residen-

tial ties are looked at collectively by the CRA.

Page 4

5

The Basics of Canadian Residency for

Tax Purposes

No one secondary tie would likely be cause you to be

viewed as maintaining Canadian residency, however,

efforts should be made to sever all ties with Canada.

Some common examples of primary ties are maintaining

a residence(s) in Canada that is available for your use,

leaving a spouse or common-law partner in Canada and

supporting dependants in Canada. Some common sec-

ondary ties are personal property left behind in Canada,

maintaining Canadian bank accounts, Canadian credit

cards, and professional and/or club memberships in Ca-

nadian organizations.

It is important that you inform any Canadian residents

making payments to you, such as financial institutions

that you have investments with, that you intend to be a

non-resident of Canada. Not only does this show the

CRA your intention to be a non-resident, but it also en-

sures that payments made to you after your departure

are subject to the appropriate non-resident withholding

taxes. If these non-resident withholding taxes are not

withheld by the Canadian payer, you will be required to

voluntarily remit the withholding tax after you have left

Canada.

If your residency status is questioned by the CRA, they

may ask you to submit a form NR73 - Determination of

Residency Status (Leaving Canada). It is advisable that

you fill in this form at the time of your departure and

keep a copy for your records, in case it is requested. It is

not advisable that you submit this form to the CRA

unless you and your tax advisor have difficulty determin-

ing your residency status.

Departure tax

If you become a non-resident of Canada for tax pur-

poses, you must file a final departure tax return in Can-

ada, due April 30th after the year in which you sever

your residential ties with Canada. There are various tax

implications that could arise in this final return.

Page 5

6

The Basics of Canadian Residency for

Tax Purposes

By: Arun Nagratha & Wayne Bewick. Contact: 60 Columbia Way Suite 900, Markham, ON, Canada, L3R 0C9. Tel: 905.709.7911. Fax: 905.946.2207.

E-mail: [email protected]. Web: www.cramagazine.com. Page: 6

The most common example is the deemed disposition of

certain assets you own, based on fair market value. An-

other example is the pro-ration of personal tax credits for

your period of residency. Apart from the departure tax

return itself, rental properties owned by non-residents

have specific filing requirements in Canada as do sales

of property.

This is just a sample of some of the issues that should

be considered on your departure from Canada. It is im-

portant that you seek professional advice to ensure that

all of your departure tax issues are taken into considera-

tion in your final tax return.

Treaty Resident If you are seen as a tax resident of Canada and another

country, that Canada has a tax treaty with, you could be

deemed a non-resident of Canada under the treaty.

Most treaties with Canada have a “tie-breaker” Article 4.

This Article goes through various steps to determine

which of the two countries an individual more a resident

of under the treaty is. The individual would then be a

resident of one of the two countries and deemed a non-

resident of the other. In this sense, one could have ties

to Canada and still be considered a non-resident of Can-

ada depending on how significant these ties are as com-

pared to the other treaty country.

Maintaining Canadian residency

If significant ties to Canada cause you to be seen as a

resident, and you are not deemed a resident of another

country under a treaty, keep in mind that you will still

have to file a Canadian tax return on an annual basis

reporting your worldwide income, even if this income

was earned in another country. In most cases, you will

be allowed a foreign tax credit for foreign taxes already

paid on this income but you must still meet your tax filing

requirements in Canada. If you do not file your tax re-

turn, you may receive a request at some point from the

CRA requesting you to file.

Ernie and Wayne are Tax Advisors with Trowbridge Profes-

sional Corporation, Chartered Accountants | Tax Advisors.

Their firm focuses on international tax services for Canadians

around the world. For further information on their firm and the

services they provide, you can contact them using the contact

details below.

7

A Basic Understanding of Principal

Protected Notes (PPNs): part 1

Abu Nizam, CIM

In my last few articles, I wrote about technical analy-

sis and stock options. In the technical analysis arti-

cle, I wrote about some important and well known

technical analysis and how to use them along with

fundamentals.

In the stock options article, I wrote about call options and

put options and various option strategies. At a minimum,

investors should use some technical analysis because of

the increasing amount of volatility which makes the tim-

ing of an investment more important. Investors should

explore the area of stock options as well. Today, I will

write about Principal Protected Notes, more commonly

known as PPNs. As the name implies, in a Principal Pro-

tected Note, the principal amount invested is generally

protected if held until maturity.

A principal-protected note (“PPN”) is a

debt instrument issued by a creditwor-

thy issuer, the return on which is linked

to the performance of another invest-

ment called the underlying asset.

The main appeal of PPNs as an invest-

ment lies in the fact that they protect

investors’ principal while at the same

time providing them with an opportu-

nity to participate in a possible increase

in the value of the underlying asset.

- “Due Diligence Guidelines on Principal-protected

Notes” by Andre Fok Kam, Investment Dealers Associa-

tion of Canada (Now IIROC), Mar 28, 2007

Readers should know that even though it says the princi-

pal is protected, the protection comes only if it is held

until maturity, which is generally 5 to 7 years after the

investment has been made. That means that in an infla-

tion adjusted basis, investors who only recover their prin-

cipal are exposed to an erosion of the purchasing power

of their investment over the term of the PPN.

Page 7

8

A Basic Understanding of Principal

Protected Notes (PPNs): part 1

Types of PPNs:

Besides the protection, PPNs typically are linked to a

mutual fund or hedge fund (or other financial instrument)

and fall into the four broad categories listed below:

1. Mutual Fund-Linked Notes

The return is linked to a particular mutual fund or portfo-

lio of mutual funds.

2. Hedge Fund-Linked Notes

The return is linked to the performance of an underlying

hedge fund, or more commonly, a portfolio of hedge

funds.

3. Index-Linked Notes

The return is linked to the performance of an equity in-

dex, such as the S&P/TSX Composite Index or S&P

500.

4. Alternative Investment-Linked Notes

The return may be linked to different commodities, man-

aged futures or income-producing notes. This is a new

version of PPN, designed to satisfy investors’ income

need.

Who should consider purchasing PPNs?

The following points are taken from the RBC Structured

Notes website FAQ and are generally applicable to all

investors:

RBC Principal Protected Notes are created for investors

who want any of the following:

The potential to earn a return that is greater than

what is available from traditional fixed income invest-

ments with similar risks.

Exposure to equity or commodity markets with the

potential for a principal guarantee.

Exposure to foreign equity and commodity markets

without the foreign currency risk.

Exposure to equity and commodity markets that are

otherwise difficult to access.

To protect previous investment gains but remain ex-

posed to equity or commodity markets.

How it works:

To understand how it works one has to understand a

zero-coupon bond first. This debt instrument is the heart

of any PPN. A zero-coupon bond is a debt security that

doesn't pay interest (a coupon) but is traded at a dis-

count. At maturity, when the bond is redeemed for its full

face value, the holder earns a return which is the differ-

ence between the purchase price and the face value. So

let’s say for a simplistic example, a $1000 dollar face

value bond is purchased at $900 and the investor re-

deems it one year later. The return would be $100.

Page 8

9

A Basic Understanding of Principal

Protected Notes (PPNs): part 1

With this understanding, let’s talk about the two struc-

tures used by PPNs:

1. Zero-coupon bond plus call option

2. Constant Proportion Portfolio Insurance (CPPI)

Zero-coupon bond plus call option:

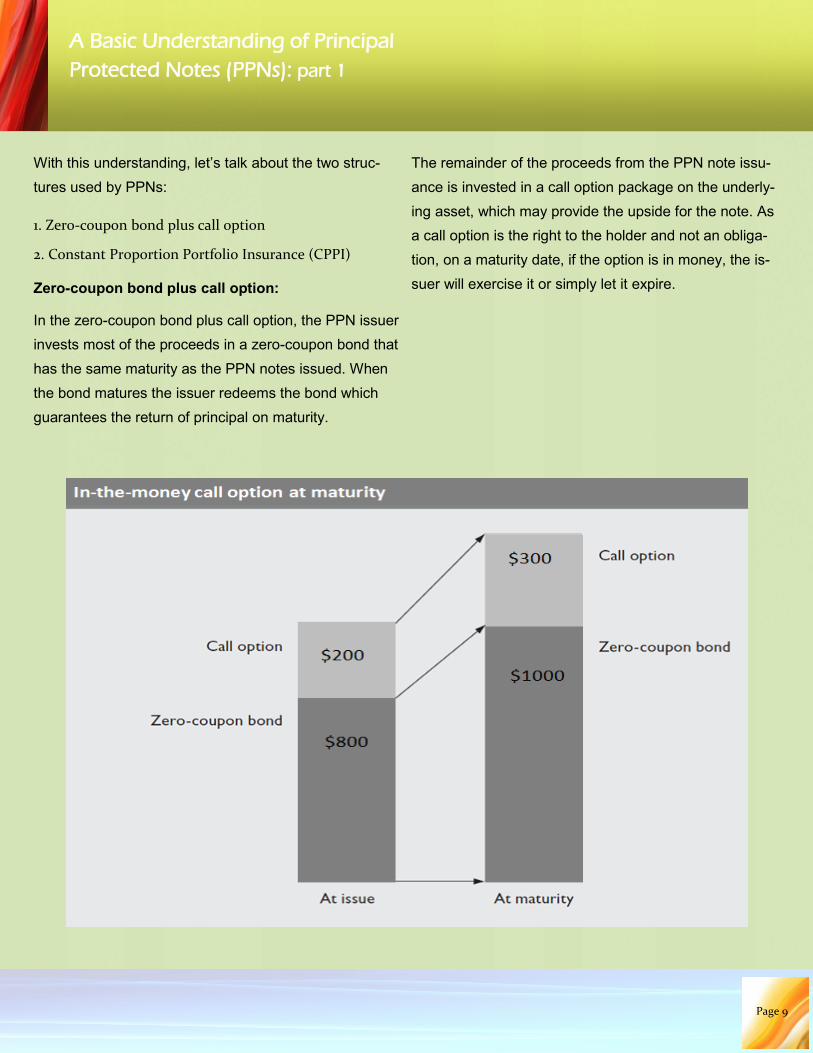

In the zero-coupon bond plus call option, the PPN issuer

invests most of the proceeds in a zero-coupon bond that

has the same maturity as the PPN notes issued. When

the bond matures the issuer redeems the bond which

guarantees the return of principal on maturity.

The remainder of the proceeds from the PPN note issu-

ance is invested in a call option package on the underly-

ing asset, which may provide the upside for the note. As

a call option is the right to the holder and not an obliga-

tion, on a maturity date, if the option is in money, the is-

suer will exercise it or simply let it expire.

Page 9

10

A Basic Understanding of Principal

Protected Notes (PPNs): part 1

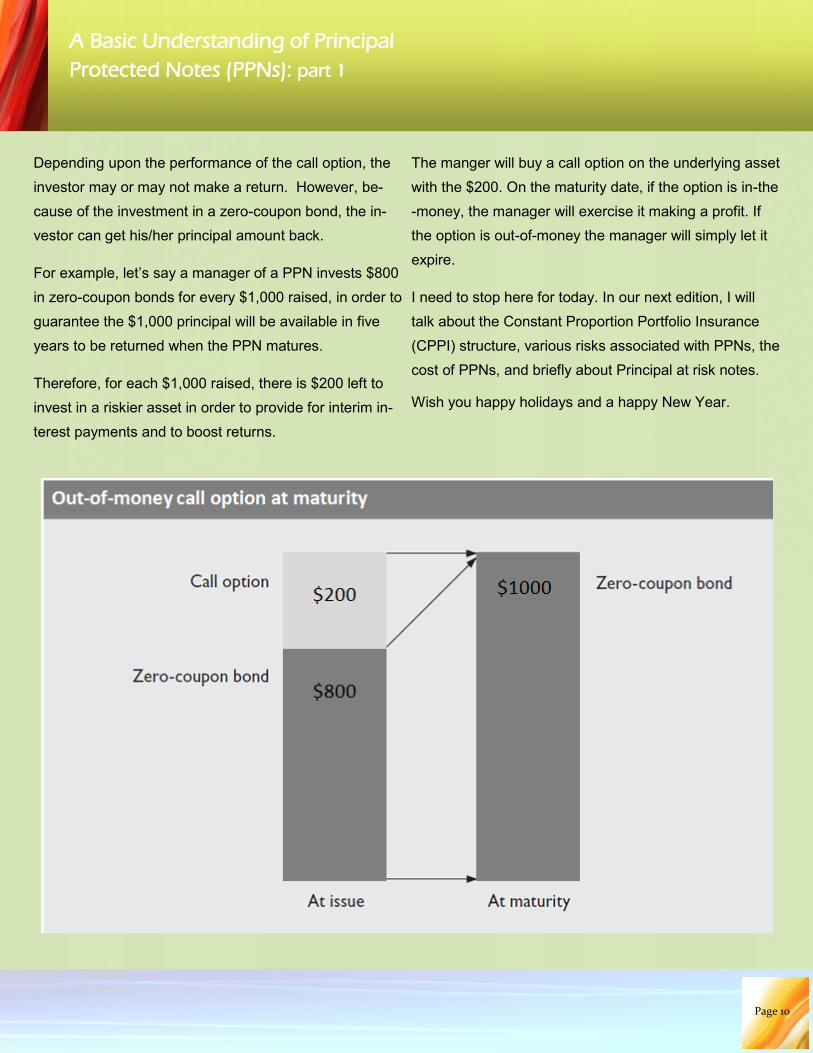

Depending upon the performance of the call option, the

investor may or may not make a return. However, be-

cause of the investment in a zero-coupon bond, the in-

vestor can get his/her principal amount back.

For example, let’s say a manager of a PPN invests $800

in zero-coupon bonds for every $1,000 raised, in order to

guarantee the $1,000 principal will be available in five

years to be returned when the PPN matures.

Therefore, for each $1,000 raised, there is $200 left to

invest in a riskier asset in order to provide for interim in-

terest payments and to boost returns.

The manger will buy a call option on the underlying asset

with the $200. On the maturity date, if the option is in-the

-money, the manager will exercise it making a profit. If

the option is out-of-money the manager will simply let it

expire.

I need to stop here for today. In our next edition, I will

talk about the Constant Proportion Portfolio Insurance

(CPPI) structure, various risks associated with PPNs, the

cost of PPNs, and briefly about Principal at risk notes.

Wish you happy holidays and a happy New Year.

Page 10

11

30 Big Ideas for 2012 and Beyond

Fidelity Investments, Canada

Fidelity Investments Canada has published 30 big

ideas for 2012 and beyond for all 10 sectors

(consumer discretionary, consumer staples, energy,

health care, financials, industrials, materials, infor-

mation technology, utilities and telecommunica-

tions).

We think readers will benefit from these themes when

making investment decisions. We would like to publish

all 30 ideas but it will get so enormous that it would take

three editions of our magazine to cover it. We have de-

cided to publish only 6 ideas from 2 sectors instead.

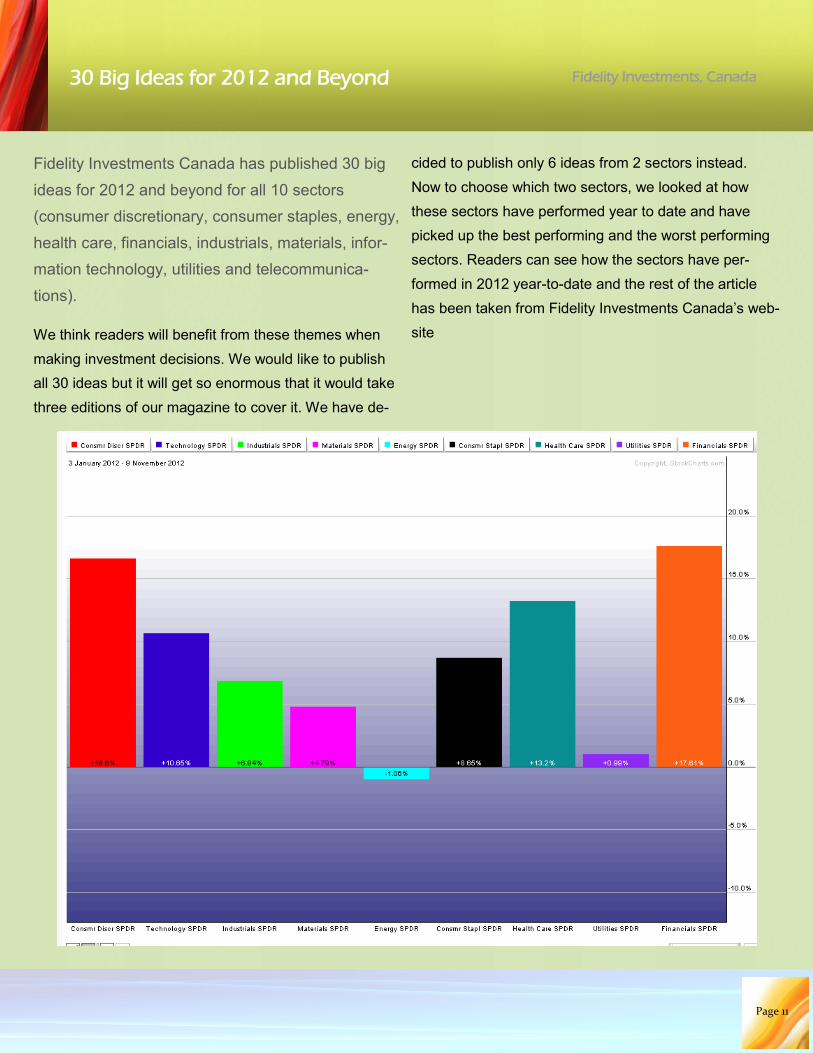

Now to choose which two sectors, we looked at how

these sectors have performed year to date and have

picked up the best performing and the worst performing

sectors. Readers can see how the sectors have per-

formed in 2012 year-to-date and the rest of the article

has been taken from Fidelity Investments Canada’s web-

site

Page 11

12

30 Big Ideas for 2012 and Beyond

Intro

What trends will shape the investment landscape in

the years ahead?

A special report from Fidelity Investments, our U.S. part-

ner, highlights the top 30 investment themes the firm’s

equity sector specialists believe are likely to have the

greatest influence on the performance of each sector in

2012 and beyond.

Energy:

The performance of energy stocks historically has been

cyclical in nature, meaning they tend to outperform the

broader market during periods of economic expansion

and lag during economic deceleration. More specifically,

energy stocks historically have outperformed at the mid

and late stages of an economic cycle, when an expan-

sion is firmly entrenched and demand for energy com-

modities and energy services is at or near peak levels.

During the past couple of years, the energy sector has

become increasingly more complex. Geopolitical ten-

sions in the Middle East and North Africa have raised the

risk of crude oil supply disruptions.

The major crude oil spill in the Gulf of Mexico in the

spring of 2010 raised the probability of increased indus-

try regulation for U.S. oil producers – a source of uncer-

tainty with regard to future earnings. Elsewhere, the

earthquake and tsunami in Japan during the spring of

2011 also posed new challenges to global supply and

demand. Despite this more complex backdrop, we be-

lieve there are a few compelling dynamics underway in

the energy sector that have the potential to significantly

alter the landscape and provide attractive opportunities

for long-term investment.

Three themes for energy: Theme 1: The emergence of more productive new drill-

ing techniques

Theme 2: The growth of the liquid natural gas market

Theme 3: The renaissance in deepwater exploration

Investment theme: The emergence

of new, more productive drilling

techniques

Key takeaways

New techniques for extracting natural gas and crude oil from the earth have helped ease concerns about the inability of U.S.-based

energy producers to grow domestic supply and offset the country’s heavy dependence on foreign sources for these commodities.

These unconventional new drilling techniques have lowered the overall cost structure for companies engaged in the exploration of

traditional energy sources, such as crude oil and natural gas.

More productive drilling techniques have led to an overall increase in mid-continent U.S. oil production, which has led to lower pric-

ing for refiners.

Page 12

13

30 Big Ideas for 2012 and Beyond

New drilling technologies

Advances in horizontal drilling and hydraulic fracturing

techniques (commonly referred to as “fracking”) are al-

lowing U.S. exploration companies to tap natural gas

and crude oil reserves embedded in previously impene-

trable rock and trapped thousands of feet underground.

Hydraulic fracturing involves blasting huge volumes of

water, sand and chemicals deep underground, which

creates fissures or fractures that allow the natural gas

trapped inside shale rock to flow out. This new drilling

technology was initially adopted and applied to improve

the extraction of natural gas in shale rock formations. Its

success led to an increase in the supply of – and lower

prices for – natural gas. More recently, exploration com-

panies have begun to apply the same fracking tech-

niques in old conventional crude oil basins that had been

viewed as unproductive based on traditional drilling

methods. The results have been favourable, leading to

what many in the industry are referring to as a

“renaissance” in domestic oil and natural gas drilling.

During the past decade, the long-term bull case for the

stocks of U.S. companies involved in the exploration and

discovery of crude oil has been largely premised on ris-

ing global demand, the inability to grow domestic supply

and rising prices. There has been little production growth

outside of the Organization of the Petroleum Exporting

Countries (OPEC) during this period. As a result, we’ve

seen rising crude oil prices, followed by an increase in

drilling to stave off rising global demand growth. More

recently, energy exploration and production companies

have been adding new unconventional wells to existing

crude oil reservoirs, resulting in extensions of proved

reserves (Exhibit 1, below).

The productivity of fracking for both commodities has

been beneficial for integrated energy producers, but also

for companies focused primarily on drilling. The number

of drilling rigs has increased substantially during the past

couple of years (see Exhibit 2, below). Elsewhere, en-

ergy services companies are benefiting from increased

service demand and higher service intensity associated

with these new techniques.

Page 13

14

30 Big Ideas for 2012 and Beyond

The impact of productive drilling

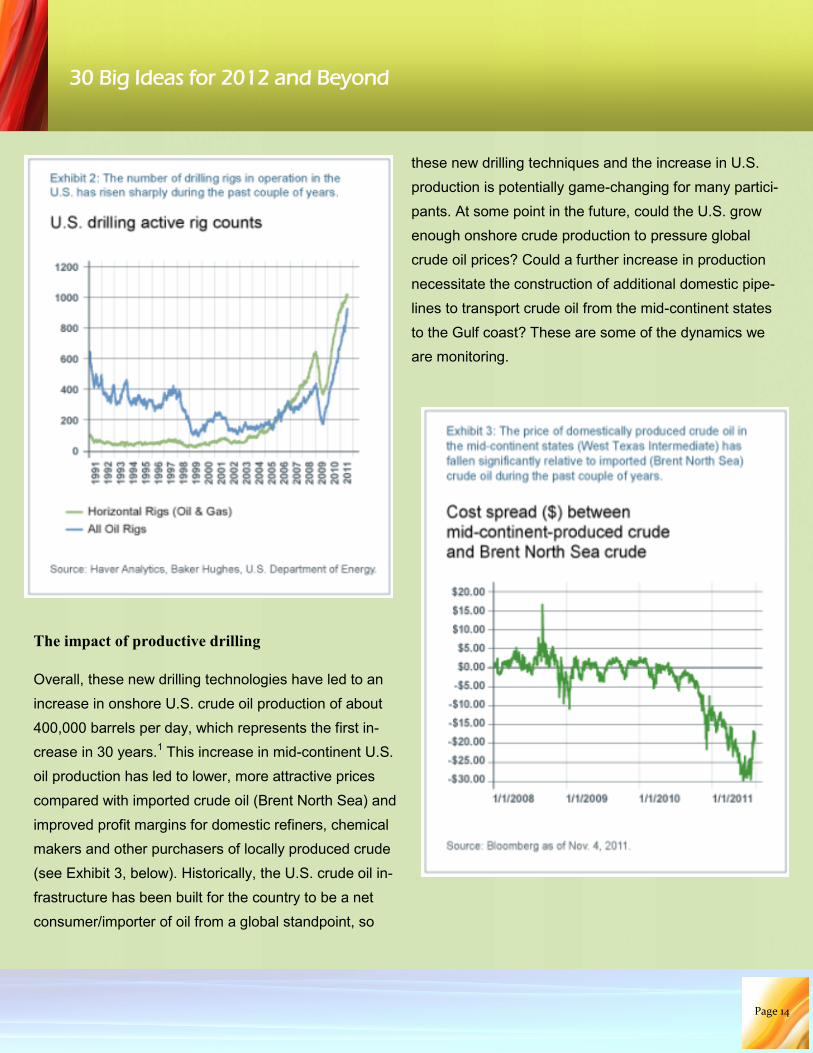

Overall, these new drilling technologies have led to an

increase in onshore U.S. crude oil production of about

400,000 barrels per day, which represents the first in-

crease in 30 years.1 This increase in mid-continent U.S.

oil production has led to lower, more attractive prices

compared with imported crude oil (Brent North Sea) and

improved profit margins for domestic refiners, chemical

makers and other purchasers of locally produced crude

(see Exhibit 3, below). Historically, the U.S. crude oil in-

frastructure has been built for the country to be a net

consumer/importer of oil from a global standpoint, so

these new drilling techniques and the increase in U.S.

production is potentially game-changing for many partici-

pants. At some point in the future, could the U.S. grow

enough onshore crude production to pressure global

crude oil prices? Could a further increase in production

necessitate the construction of additional domestic pipe-

lines to transport crude oil from the mid-continent states

to the Gulf coast? These are some of the dynamics we

are monitoring.

Page 14

15

30 Big Ideas for 2012 and Beyond

Investment implications

Unconventional drilling is likely to have a major impact

on supply growth and future energy consumption around

the world over the next decade. With respect to natural

gas, the U.S. Energy Information Administration esti-

mates there are 2,552 trillion cubic feet of natural gas in

the United States, or 110 years of use at 2009 consump-

tion levels, due largely to the application of new drilling

practices.² With U.S. politicians and entrepreneurs alike

looking to leverage such an abundant resource, the ef-

fects of more productive unconventional drilling could

spread throughout the entire global energy paradigm.

This trend is already being seen in the retirement of

older coal-generating power plants in places such as

China, and the adoption of natural gas vehicles in Asia,

Latin America and the Middle East.

Meanwhile, unconventional drilling techniques also could

have a significant impact on crude oil markets. Today,

this drilling technology is being adopted in oil fields in

Canada, Argentina and Eastern Europe, and may lead to

a significant global increase in non-OPEC production in

the years ahead. We recognize that new unconventional

drilling technologies have the potential to put downward

pressure on energy commodity prices around the world

over the long term, which may be helpful at various

times for some industry participants and detrimental to

others. We are also mindful that falling energy prices

would have a significant destabilizing effect and geopo-

litical ramifications for major energy-producing countries.

Overall, the energy sector is potentially on the cusp of

making the transition from a resource-constrained world

to one that has a much better production profile due to

improvements in drilling techniques.

Investment theme: The growth of

the liquid natural gas market

Key takeaways

Global demand for natural gas has increased in recent years due to greater interest in its more environmentally friendly properties,

compared with coal and crude oil, and the increased adoption of natural gas-fired power generation plants.

Improvements in the technology that harnesses and liquefies natural gas from reserves has led to increased production, transporta-

tion and usage of liquefied natural gas (LNG) throughout the world.

Page 15

16

30 Big Ideas for 2012 and Beyond

A bounty of natural gas

For many decades, the primary focus of exploration for

energy sources had been the search for crude oil depos-

its. More recently, large integrated energy producers are

putting a greater emphasis on the exploration and pro-

duction of natural gas, for the following reasons:

New technology has allowed companies to more efficiently

harness, liquefy and transport natural gas to new and ex-

isting markets.

Stricter environmental regulations and a greater aware-

ness of the cleaner properties of natural gas, compared

with other energy commodities such as coal and crude oil,

have led to rising global demand for natural gas.

New hydraulic fracturing drilling techniques have led to an

abundant global supply of natural gas. Companies can

more effectively extract natural gas from shale rock forma-

tions in the earth, both in new locations and stranded loca-

tions and in older wells that had been drilled and viewed

as less productive using traditional drilling techniques.

Increasing demand for natural gas-generated electricity in

emerging market countries has increased amid escalating

economic growth.

Regions with large reserves of natural gas, such as Aus-

tralia, Qatar, the U.S. and Russia, have been at the fore-

front of the development of liquefied natural gas. In

2009, the U.S. became the largest natural gas producer

in the world, with shale accounting for about 20% of do-

mestic production.

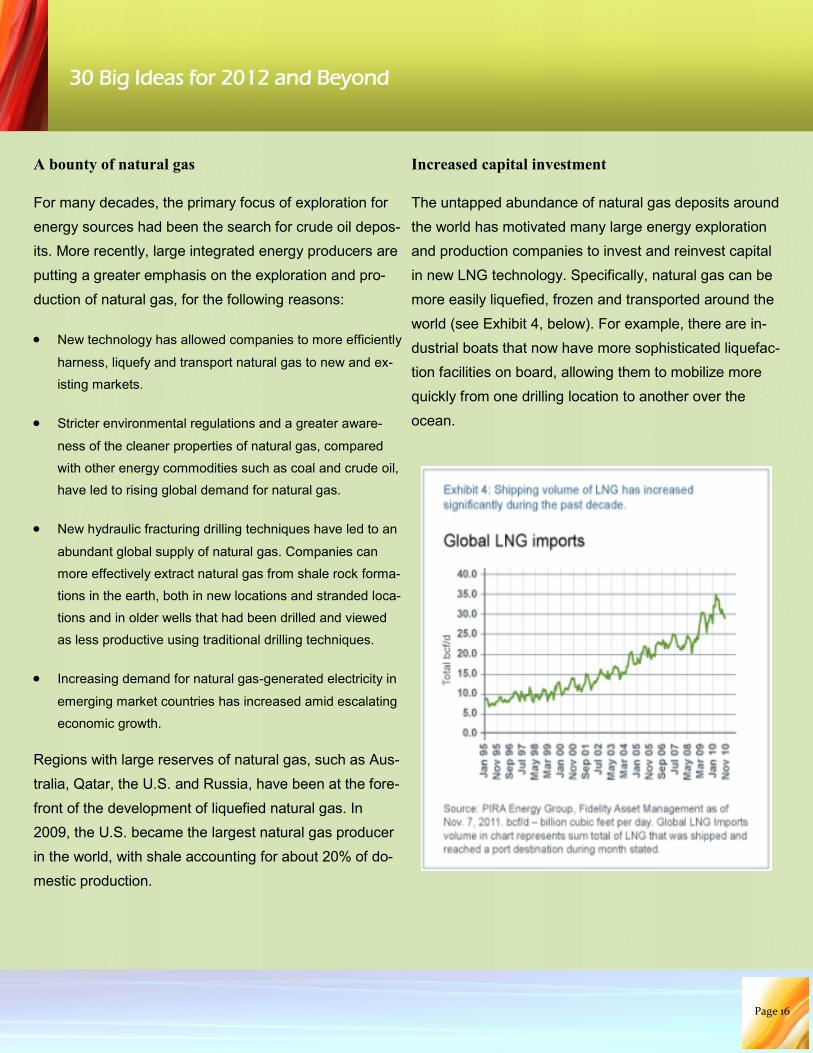

Increased capital investment

The untapped abundance of natural gas deposits around

the world has motivated many large energy exploration

and production companies to invest and reinvest capital

in new LNG technology. Specifically, natural gas can be

more easily liquefied, frozen and transported around the

world (see Exhibit 4, below). For example, there are in-

dustrial boats that now have more sophisticated liquefac-

tion facilities on board, allowing them to mobilize more

quickly from one drilling location to another over the

ocean.

Page 16

17

30 Big Ideas for 2012 and Beyond

Many of these large integrated energy producers have

shifted a greater percentage of their infrastructure portfo-

lios to focus more on LNG production, because the

plants and facilities are projected to have longer produc-

tion cycles and slower rates of decline than those for

conventional oil. For example, a state-of-the-art crude oil

facility may run its course and deplete a reserve’s oil ca-

pacity in five to six years, which is a rough average.

Some modern LNG operations are expected to be in use

for as long as 30 years, with significantly slower annual

rates of declining productivity. In addition, many large

energy producers have legacy assets (e.g., onshore or

offshore fields) that are maturing and fading in productiv-

ity, and have thus repositioned their portfolios in newer,

untapped natural gas assets. As a result, growth in the

production and servicing of liquefied natural gas has in-

creased significantly during the past couple of years.

Rising global demand for LNG

There are a couple of sources for rising global demand

for LNG. First, demand for LNG has increased in emerg-

ing market countries, which have generally experienced

stronger economic growth rates. For example, imports of

LNG have surged in China during the past year.

Second, since the earthquake and tsunami that hit Ja-

pan in the spring of 2011 shut down a portion of its nu-

clear power generation capacity, the country has made

LNG a greater focus of its current and future plans for

power generation.

Investment implications

The abundance of global natural gas and the advent of

new technology to harness the commodity support engi-

neering and construction companies that can produce

the LNG capabilities needed by large integrated energy

companies. Energy producers’ greater emphasis on in-

vesting in the technology needed to develop and trans-

port LNG is a theme that we expect to be relevant for

some time.

Investment theme: The renaissance

in deepwater exploration

Key takeaways

The combination of more sophisticated drilling techniques, deepwater rigs, and seismic wave and imaging technology has provided en-

ergy producers with greater opportunity to explore for energy commodities in previously inaccessible deepwater regions.

Many energy producers view deepwater drilling as a relatively untapped frontier that could provide a source of production growth over

the next several years.

Page 17

18

30 Big Ideas for 2012 and Beyond

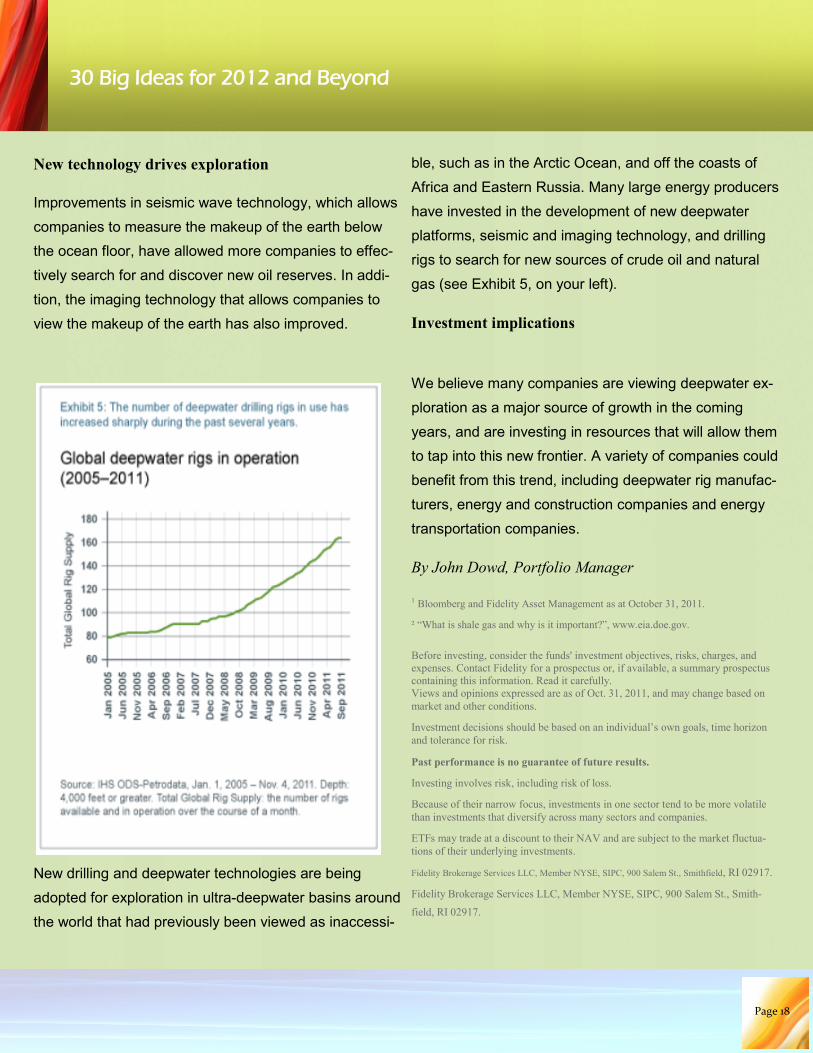

New technology drives exploration

Improvements in seismic wave technology, which allows

companies to measure the makeup of the earth below

the ocean floor, have allowed more companies to effec-

tively search for and discover new oil reserves. In addi-

tion, the imaging technology that allows companies to

view the makeup of the earth has also improved.

New drilling and deepwater technologies are being

adopted for exploration in ultra-deepwater basins around

the world that had previously been viewed as inaccessi-

ble, such as in the Arctic Ocean, and off the coasts of

Africa and Eastern Russia. Many large energy producers

have invested in the development of new deepwater

platforms, seismic and imaging technology, and drilling

rigs to search for new sources of crude oil and natural

gas (see Exhibit 5, on your left).

Investment implications

We believe many companies are viewing deepwater ex-

ploration as a major source of growth in the coming

years, and are investing in resources that will allow them

to tap into this new frontier. A variety of companies could

benefit from this trend, including deepwater rig manufac-

turers, energy and construction companies and energy

transportation companies.

By John Dowd, Portfolio Manager

1 Bloomberg and Fidelity Asset Management as at October 31, 2011.

² “What is shale gas and why is it important?”, www.eia.doe.gov.

Before investing, consider the funds' investment objectives, risks, charges, and

expenses. Contact Fidelity for a prospectus or, if available, a summary prospectus

containing this information. Read it carefully.

Views and opinions expressed are as of Oct. 31, 2011, and may change based on

market and other conditions.

Investment decisions should be based on an individual’s own goals, time horizon

and tolerance for risk.

Past performance is no guarantee of future results.

Investing involves risk, including risk of loss.

Because of their narrow focus, investments in one sector tend to be more volatile

than investments that diversify across many sectors and companies.

ETFs may trade at a discount to their NAV and are subject to the market fluctua-

tions of their underlying investments.

Fidelity Brokerage Services LLC, Member NYSE, SIPC, 900 Salem St., Smithfield, RI 02917.

Fidelity Brokerage Services LLC, Member NYSE, SIPC, 900 Salem St., Smith-

field, RI 02917.

Page 18

19

30 Big Ideas for 2012 and Beyond

Financials

The financials sector continues to face several chal-

lenges. Continued economic improvement is critical to

ongoing repair of the U.S. financial system, but the

global economy’s deceleration in the third quarter of

2011 has raised concerns about a double-dip recession

in the U.S. This decelerating global growth outlook has

led to increased financial distress in the eurozone, mak-

ing it more difficult for fiscal austerity measures to re-

duce debt burdens relative to underlying economic out-

put. The aftermath of the 2008–2009 financial crisis left a

different environment than most post-war economic re-

coveries, with de-leveraging in the financial, consumer

and housing sectors creating deflationary pressures. As

a result, unlike in most mid-cycle expansions, monetary

policy has yet to tighten, and credit has recovered

slowly. Elsewhere, the U.S. housing market remains

challenged and consumer debt levels remain elevated.

Several financial regulatory reform proposals also

threaten to reduce profitability in the sector. In addition,

core inflation is accelerating across the globe, which his-

torically has been a negative for financial assets.

On the positive side of the ledger, credit conditions have

improved during the past year; historically, this has been

a favourable driver for financial stocks, especially banks.

On average, loan growth has turned positive, the ratio of

non-performing loans has declined, and delinquency

rates have fallen – even for the most toxic loan books.

From a valuation perspective, stocks on average have

been trading roughly in line with the market on a forward

-earnings basis, but are significantly discounted on a

cash-flow and book-value basis. This is particularly true

for large U.S. banks, which generally are very well capi-

talized but have been universally punished by the macro

market dynamics influencing investor behaviour.

Despite this mixed backdrop, our financials equity re-

search team believes there are a few interesting invest-

ment themes that bear monitoring over the course of

2012 and beyond.

Three themes for financials: Theme 1: The growth of Chinese banks

Theme 2: The age of austerity

Theme 3: Potential restructuring of the GSEs

Investment theme: The growth of

Chinese banks

Key takeaways

During the past decade, the largest banks in China have grown to be among the largest in the world in terms of market capitalization,

total loans outstanding and earnings.

The percentage of non-performing loans in the Chinese banking sector has fallen to an all-time low.

If the current growth trajectory for the largest Chinese banks continues, it may shift the competitive landscape in the industry and lead to

greater appreciation for the Chinese currency.

Page 19

20

30 Big Ideas for 2012 and Beyond

The rise of China’s banks

During the past five years, while other large global banks

were forced to write down loan and securities losses,

recapitalize themselves and de-leverage their balance

sheets, China quietly became the home of three of the

world’s largest banks, based on market capitalization. A

decade ago, none of these banks were publicly traded

entities.

The growth of the Chinese banks is astonishing in terms

of other metrics as well. The Chinese banking system

had about $3 trillion in total loans outstanding in 2006.

Since then, loans in the Chinese bank system have dou-

bled, in part due to a government stimulus boost in 2009.

Earnings have followed as well. In 2010, one major Chi-

nese bank generated net income of $24 billion, up from

$6 billion in 2006, and above the $17 billion in net in-

come generated by a major U.S. bank in 2010.1

Projected growth at current run-rate

The largest Chinese banks have estimated that their re-

spective annual loan growth will continue in the 10%–

20% range over the next few years.1 Given that the big-

gest U.S. and European banks are likely to be shrinking

their balance sheets in the coming years, the largest

Chinese banks could potentially be twice the size of the

largest U.S. and European banks by the middle of the

current decade.

Historical loan crises and Chinese government re-

sponse

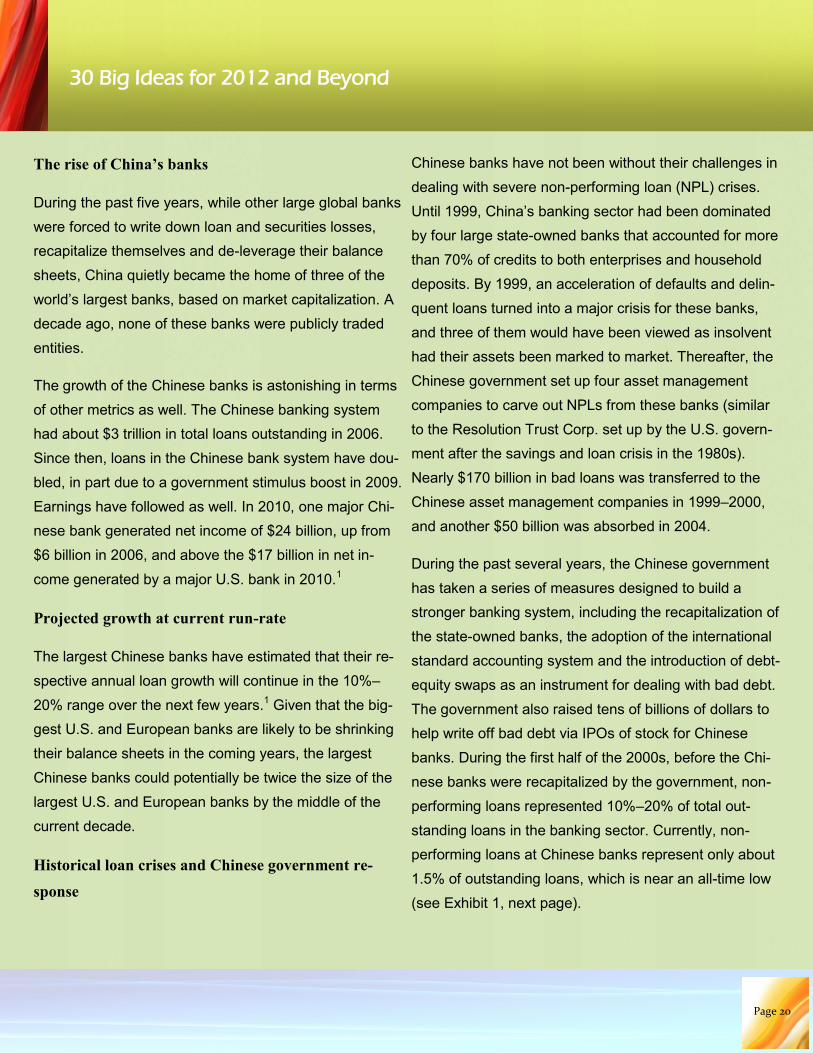

Chinese banks have not been without their challenges in

dealing with severe non-performing loan (NPL) crises.

Until 1999, China’s banking sector had been dominated

by four large state-owned banks that accounted for more

than 70% of credits to both enterprises and household

deposits. By 1999, an acceleration of defaults and delin-

quent loans turned into a major crisis for these banks,

and three of them would have been viewed as insolvent

had their assets been marked to market. Thereafter, the

Chinese government set up four asset management

companies to carve out NPLs from these banks (similar

to the Resolution Trust Corp. set up by the U.S. govern-

ment after the savings and loan crisis in the 1980s).

Nearly $170 billion in bad loans was transferred to the

Chinese asset management companies in 1999–2000,

and another $50 billion was absorbed in 2004.

During the past several years, the Chinese government

has taken a series of measures designed to build a

stronger banking system, including the recapitalization of

the state-owned banks, the adoption of the international

standard accounting system and the introduction of debt-

equity swaps as an instrument for dealing with bad debt.

The government also raised tens of billions of dollars to

help write off bad debt via IPOs of stock for Chinese

banks. During the first half of the 2000s, before the Chi-

nese banks were recapitalized by the government, non-

performing loans represented 10%–20% of total out-

standing loans in the banking sector. Currently, non-

performing loans at Chinese banks represent only about

1.5% of outstanding loans, which is near an all-time low

(see Exhibit 1, next page).

Page 20

21

30 Big Ideas for 2012 and Beyond

Signs of caution

However, there are increasing concerns about lending

quality in China’s local government segment. During the

past year, Chinese authorities have tightened monetary

policy, which has slowed the pace of bank credit ex-

tended to mortgage applicants, small and medium enter-

prises, and other entities. Nevertheless, China’s building

boom has largely continued, and residential construction

starts have far outpaced sales.

With supply outstripping demand, extreme property

valuations in major cities and initial signs of financial dis-

tress among property developers, China may be at the

front end of a decelerating real estate market. Whether

these property sector imbalances lead to a large-scale

real estate slump and widespread loan losses for banks

in China remains to be seen, but it’s something we’re

monitoring closely.

Investment implications

A world dominated by Chinese banks could have several

important investment implications. First, large Chinese

banks could become aggressive acquirers of foreign

banks, a potentially beneficial event for shareholders of

acquired institutions. Second, with vastly larger balance

sheets, the Chinese banks could force competitive

downward pressure on pricing across the spectrum of

products and services in an attempt to gain market

share, which would be a positive for customers but a

negative for the earnings and stock prices for some U.S.

and European banks. Third, the sheer projected size of

Chinese banks in a few years' time (relative to global

peers and the Chinese economy) might encourage regu-

lators to facilitate the development of China’s capital

markets. This maturation could drive the appreciation

and convertibility of the Chinese currency, as well as its

rise as an alternative to the U.S. dollar – a dynamic that

would significantly influence the global financial and geo-

political spectrum.

Page 21

22

30 Big Ideas for 2012 and Beyond

Investment theme: The age of aus-

terity

Understanding the need for fiscal austerity

The escalating fiscal government deficits and high sover-

eign debt levels of many developed countries during the

past few years have been a driving source of increased

volatility in the financial markets. While the size of a

country’s fiscal deficit and debt level is critical to its cred-

itworthiness, a country’s ability to grow its economy fast

enough to service its debt is also important. Accordingly,

highly indebted countries with bleak outlooks for eco-

nomic growth have watched the yields on their out-

standing debt rise as market participants begin to ques-

tion their growth prospects and their ability to pay. In a

self-fulfilling feedback loop, higher interest rates make a

country’s fiscal challenges even greater, leading to even

greater concerns about these countries’ ability to service

their outstanding debt.

Peripheral eurozone countries have been facing these

challenges most acutely during the past couple of years,

while other countries with large deficits and high debt

levels, such as the U.S. and Germany, are seen as less

challenged, due to their relatively more favourable

growth prospects. Generally speaking, countries facing

these fiscal challenges have three main options: 1) un-

dertake fiscal austerity policy measures, which include

spending cuts, tax increases and benefit reductions; 2)

pursue monetary policy measures, such as currency de-

valuation to spur export growth, or inflationary money

policy to make domestic debt easier to pay; or 3) debt

restructuring (de facto default, through altering the terms

of repayment to bondholders).

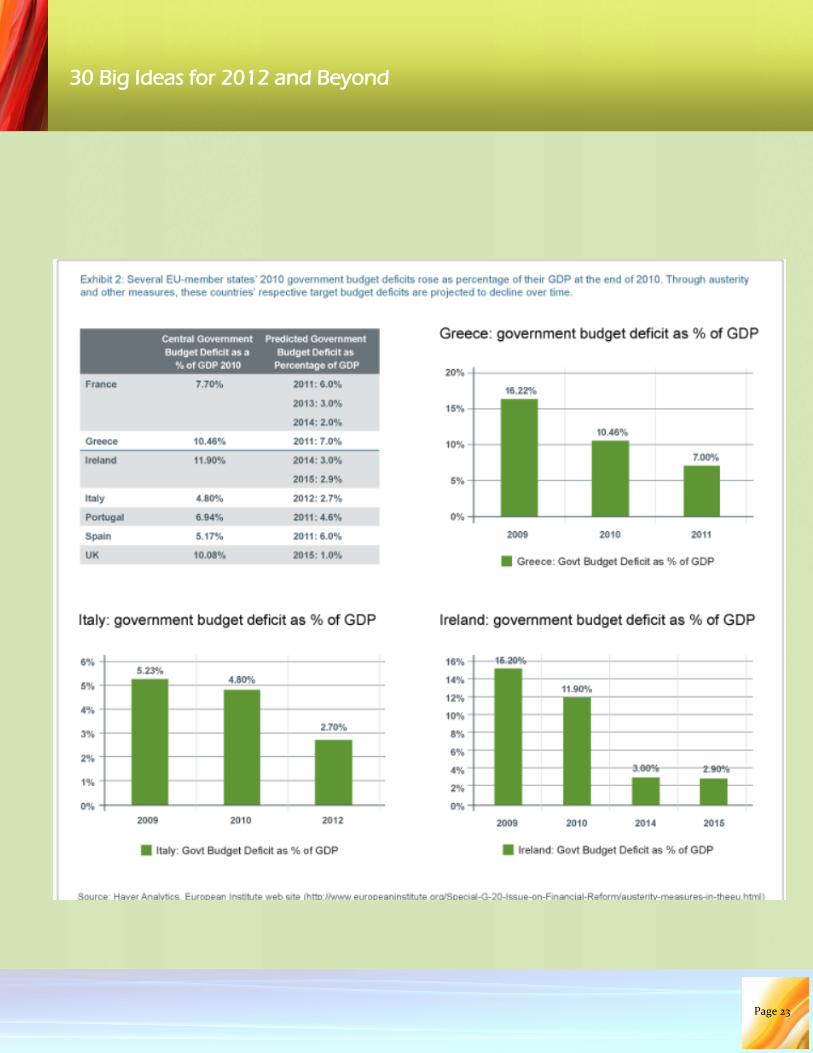

The implementation of fiscal austerity

When the U.K. became the first major country to imple-

ment widespread austerity initiatives in the spring of

2010, Prime Minister David Cameron coined this era

“The Age of Austerity.” According to the European Un-

ion’s Treaty of Maastricht criteria, European Union (EU)

member states may not have a budget deficit that ex-

ceeds 3.0% of their gross domestic product (GDP). Sev-

eral countries exceeded that threshold in 2010, and have

since been implementing austerity measures (see Ex-

hibit 2, next page).

Key takeaways

Elevated fiscal budget deficits and debt levels, rising borrowing costs and sluggish economic growth have caused some European sov-

ereigns to implement austerity measures during the past couple of years to improve their creditworthiness and meet debt service pay-

ments.

If successful, fiscal austerity can provide a more favourable backdrop for financial assets over the long term, but it typically has led to

slower economic growth in the short term – an environment that historically has not been favourable for bank stock performance.

Page 22

23

30 Big Ideas for 2012 and Beyond

Page 23

24

30 Big Ideas for 2012 and Beyond

Investment implications

Austerity creates a challenging environment for banks.

Austerity is unequivocally negative for banks in the short

term because it generally results in weaker economic

growth. For example, when governments reduce spend-

ing on development projects, welfare and other pro-

grams, it can hinder employment and GDP growth. At

the same time, an increase in taxes and fees on port and

road transportation, licensing and permits can put pres-

sure on consumer spending. A lower-spending, slower-

growth environment typically means reduced revenue for

banks, as well as higher credit costs.

If austerity is successful over the long term, history

shows that the result will be more sustainable economic

growth – which is positive for banks. In the early 1990s,

both Canada and Sweden made large fiscal adjustments

to reduce their deficits and stabilize their government

debt-to-GDP ratios over multi-year periods.

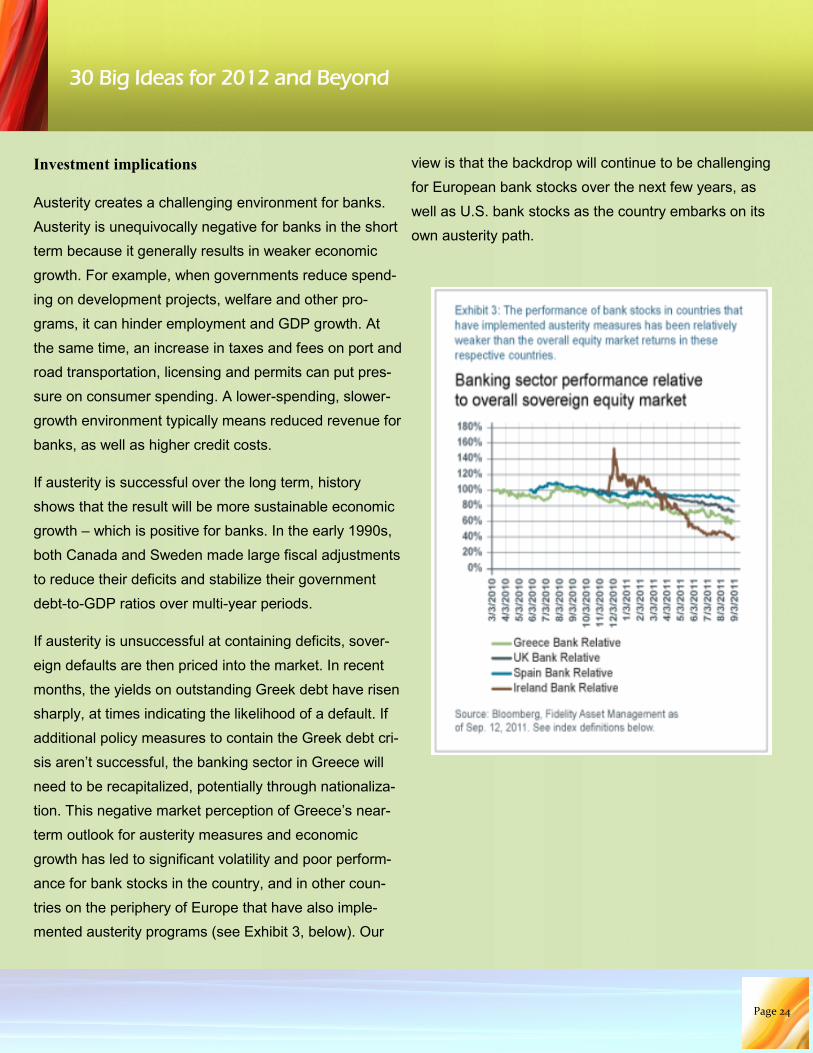

If austerity is unsuccessful at containing deficits, sover-

eign defaults are then priced into the market. In recent

months, the yields on outstanding Greek debt have risen

sharply, at times indicating the likelihood of a default. If

additional policy measures to contain the Greek debt cri-

sis aren’t successful, the banking sector in Greece will

need to be recapitalized, potentially through nationaliza-

tion. This negative market perception of Greece’s near-

term outlook for austerity measures and economic

growth has led to significant volatility and poor perform-

ance for bank stocks in the country, and in other coun-

tries on the periphery of Europe that have also imple-

mented austerity programs (see Exhibit 3, below). Our

view is that the backdrop will continue to be challenging

for European bank stocks over the next few years, as

well as U.S. bank stocks as the country embarks on its

own austerity path.

Page 24

25

30 Big Ideas for 2012 and Beyond

Investment theme: Potential restruc-

turing of the GSEs

The role of the GSEs

The Federal National Mortgage Association (Fannie

Mae) and the Federal Home Loan Mortgage Corporation

(Freddie Mac) were originally established by the U.S.

government to enable the growth of affordable home-

ownership. They accomplish this objective by buying

mortgage loans (from originators, such as banks), pack-

aging mortgages into mortgage-backed securities (MBS)

and guaranteeing the payments of “conforming” mort-

gages (those meeting certain guidelines, such as debt-to

-income ratio). Through these activities, the GSEs help

to increase the availability of mortgages, provide liquidity

to the mortgage security markets and ultimately lower

the cost of financing for mortgage borrowers.

Since Fannie Mae was privatized in 1968 (and Freddie

created in 1970), the GSEs have operated as quasi-

private entities with implicit government backing. They

possessed the dual objectives of trying to generate prof-

its for stockholders while still fulfilling their initial public

objective of boosting U.S. homeownership. Both sides

benefited from the quasi-government status of the two

GSEs, with Fannie and Freddie being able to borrow

more cheaply, while passing along the cost savings in

the form of cheaper mortgage financing to American

homeowners. However, the delicate balance they main-

tained as both profit-seeking companies and public ser-

vice agencies has been the source of recent troubles.

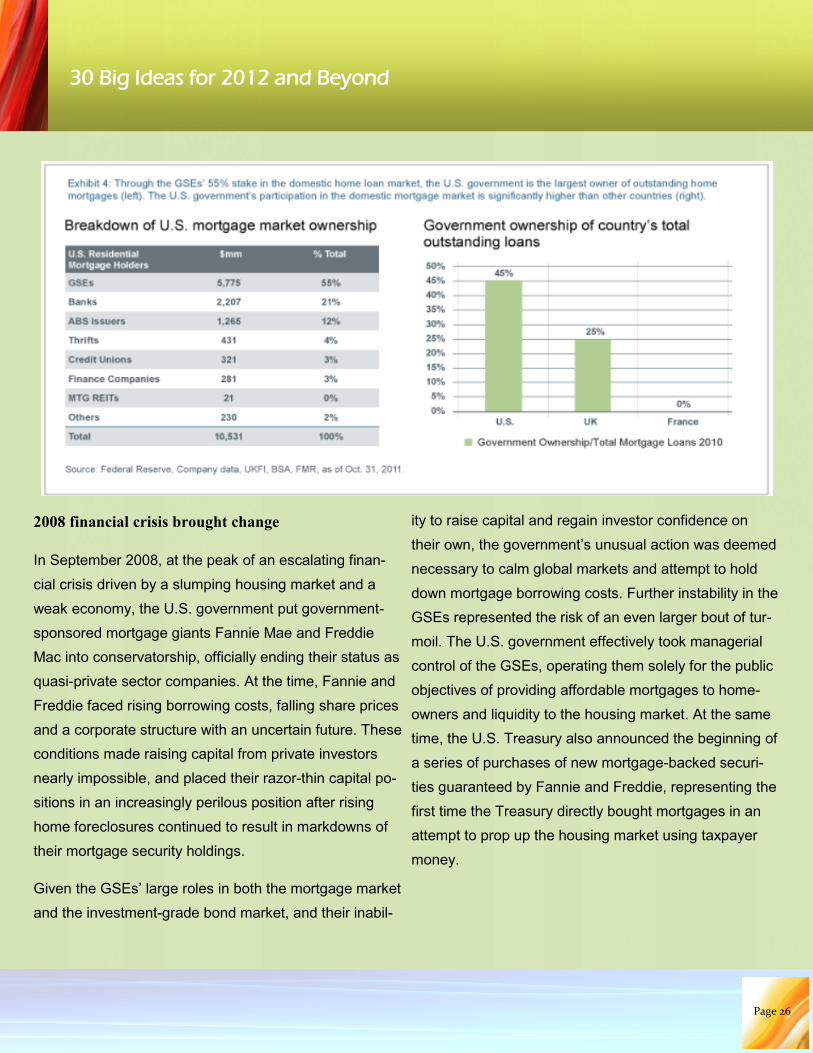

Today, the U.S. government plays a much larger role in

the U.S. housing market than in any other developed

nation, with ownership of more than half of all out-

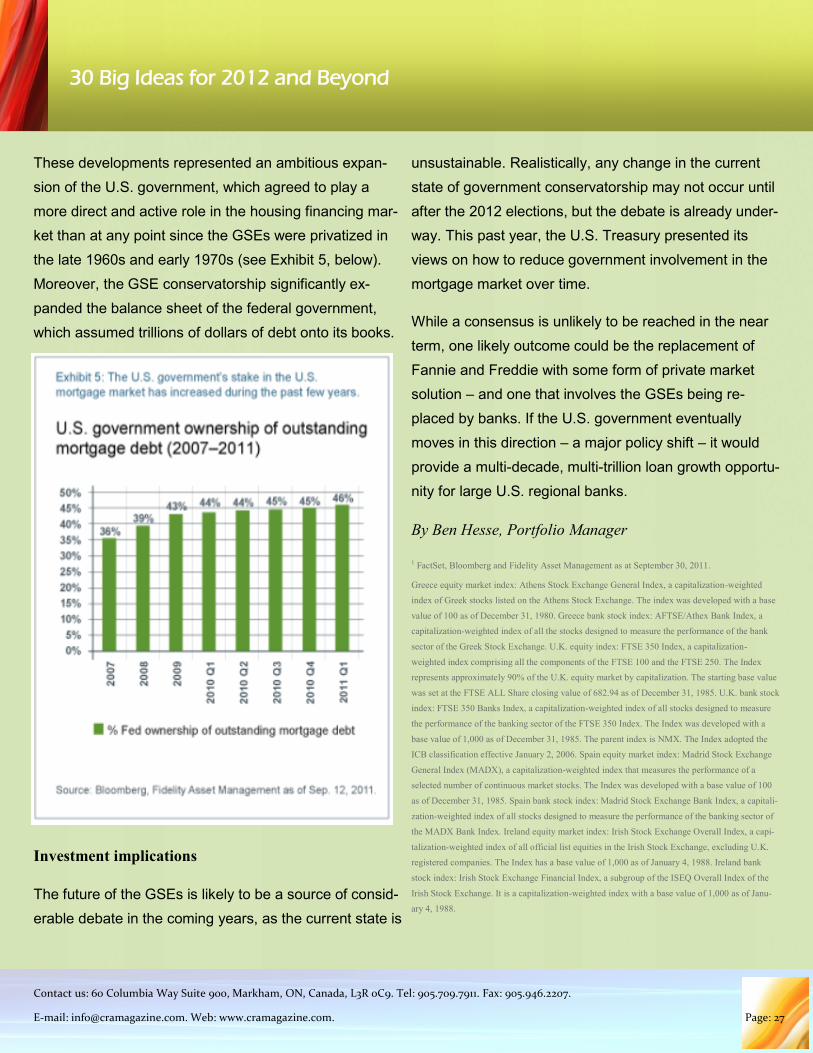

standing home loans (see Exhibit 4, next page).

Key takeaways

Government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac together play an enormous role in the functioning of the U.S.

housing and fixed-income markets, as they own or guarantee more than half of all outstanding U.S. mortgages and are directly or indi-

rectly tied to more than 40% of the investment-grade bond market.

During the past year, the U.S. Treasury expressed views on how it might reduce its significant involvement in the mortgage market

over time, an involvement that escalated in 2008 when the U.S. government placed the GSEs into conservatorship in the midst of fi-

nancial crisis.

Although it is unlikely that the future state of the GSEs and the government’s large role in the mortgage market will be resolved in the

near term, the possibility of a future private market solution may provide banks with a tailwind of loan growth that would support prof-

its and stocks.

Page 25

26

30 Big Ideas for 2012 and Beyond

2008 financial crisis brought change

In September 2008, at the peak of an escalating finan-

cial crisis driven by a slumping housing market and a

weak economy, the U.S. government put government-

sponsored mortgage giants Fannie Mae and Freddie

Mac into conservatorship, officially ending their status as

quasi-private sector companies. At the time, Fannie and

Freddie faced rising borrowing costs, falling share prices

and a corporate structure with an uncertain future. These

conditions made raising capital from private investors

nearly impossible, and placed their razor-thin capital po-

sitions in an increasingly perilous position after rising

home foreclosures continued to result in markdowns of

their mortgage security holdings.

Given the GSEs’ large roles in both the mortgage market

and the investment-grade bond market, and their inabil-

ity to raise capital and regain investor confidence on

their own, the government’s unusual action was deemed

necessary to calm global markets and attempt to hold

down mortgage borrowing costs. Further instability in the

GSEs represented the risk of an even larger bout of tur-

moil. The U.S. government effectively took managerial

control of the GSEs, operating them solely for the public

objectives of providing affordable mortgages to home-

owners and liquidity to the housing market. At the same

time, the U.S. Treasury also announced the beginning of

a series of purchases of new mortgage-backed securi-

ties guaranteed by Fannie and Freddie, representing the

first time the Treasury directly bought mortgages in an

attempt to prop up the housing market using taxpayer

money.

Page 26

27

30 Big Ideas for 2012 and Beyond

Contact us: 60 Columbia Way Suite 900, Markham, ON, Canada, L3R 0C9. Tel: 905.709.7911. Fax: 905.946.2207.

E-mail: [email protected]. Web: www.cramagazine.com. Page: 27

These developments represented an ambitious expan-

sion of the U.S. government, which agreed to play a

more direct and active role in the housing financing mar-

ket than at any point since the GSEs were privatized in

the late 1960s and early 1970s (see Exhibit 5, below).

Moreover, the GSE conservatorship significantly ex-

panded the balance sheet of the federal government,

which assumed trillions of dollars of debt onto its books.

Investment implications

The future of the GSEs is likely to be a source of consid-

erable debate in the coming years, as the current state is

unsustainable. Realistically, any change in the current

state of government conservatorship may not occur until

after the 2012 elections, but the debate is already under-

way. This past year, the U.S. Treasury presented its

views on how to reduce government involvement in the

mortgage market over time.

While a consensus is unlikely to be reached in the near

term, one likely outcome could be the replacement of

Fannie and Freddie with some form of private market

solution – and one that involves the GSEs being re-

placed by banks. If the U.S. government eventually

moves in this direction – a major policy shift – it would

provide a multi-decade, multi-trillion loan growth opportu-

nity for large U.S. regional banks.

By Ben Hesse, Portfolio Manager

1 FactSet, Bloomberg and Fidelity Asset Management as at September 30, 2011.

Greece equity market index: Athens Stock Exchange General Index, a capitalization-weighted

index of Greek stocks listed on the Athens Stock Exchange. The index was developed with a base

value of 100 as of December 31, 1980. Greece bank stock index: AFTSE/Athex Bank Index, a

capitalization-weighted index of all the stocks designed to measure the performance of the bank

sector of the Greek Stock Exchange. U.K. equity index: FTSE 350 Index, a capitalization-

weighted index comprising all the components of the FTSE 100 and the FTSE 250. The Index

represents approximately 90% of the U.K. equity market by capitalization. The starting base value

was set at the FTSE ALL Share closing value of 682.94 as of December 31, 1985. U.K. bank stock

index: FTSE 350 Banks Index, a capitalization-weighted index of all stocks designed to measure

the performance of the banking sector of the FTSE 350 Index. The Index was developed with a

base value of 1,000 as of December 31, 1985. The parent index is NMX. The Index adopted the

ICB classification effective January 2, 2006. Spain equity market index: Madrid Stock Exchange

General Index (MADX), a capitalization-weighted index that measures the performance of a

selected number of continuous market stocks. The Index was developed with a base value of 100

as of December 31, 1985. Spain bank stock index: Madrid Stock Exchange Bank Index, a capitali-

zation-weighted index of all stocks designed to measure the performance of the banking sector of

the MADX Bank Index. Ireland equity market index: Irish Stock Exchange Overall Index, a capi-

talization-weighted index of all official list equities in the Irish Stock Exchange, excluding U.K.

registered companies. The Index has a base value of 1,000 as of January 4, 1988. Ireland bank

stock index: Irish Stock Exchange Financial Index, a subgroup of the ISEQ Overall Index of the

Irish Stock Exchange. It is a capitalization-weighted index with a base value of 1,000 as of Janu-

ary 4, 1988.

28

E-mail: [email protected] Website: www.cramagazine.com

60 Columbia Way, Suite 900, Markham, ON, Canada, Tel: 905.709.7911 Fax: 905.946.2207

Canadians Resident Abroad Inc. is part of the Keybase Financial Group Inc.

CRA magazine is published bi-monthly by Canadians Resident Abroad Inc. All rights reserved. No

part of this publication or any part of it may be reproduced, stored in a retrieval system, or

transmitted in any form or by any means, electronic, mechanical, photocopying, recording, or

otherwise for commercial purposes, without the permission of Canadians Residents Abroad Inc.

Every effort has been made to ensure the accuracy of the contents of the magazine. All articles

represent the opinions of the authors. Canadians Resident Abroad Inc. makes no warranty, ex-

press or implied, concerning the content of this publication.

Creative Director: Abu Nizam Creative Assistant: Mike Beaudoin

Circulation: Jerome Pare & Lindsay Penner Web Site Manager: Keith Sutherland