Feast and Famine: The Situation and Prospects for the ... - Feast... · World Wool Market Chris...

21

Feast and Famine: The Situation and Prospects for the World Wool Market Chris Wilcox Poimena Analysis and Chairman, Market Intelligence Committee of IWTO American Wool Council February 2018

Transcript of Feast and Famine: The Situation and Prospects for the ... - Feast... · World Wool Market Chris...

Feast and Famine:

The Situation and Prospects for the

World Wool Market

Chris Wilcox

Poimena Analysis

and

Chairman, Market Intelligence Committee of IWTO

American Wool Council

February 2018

Topics

1. Recent price trends

2. Global production and supply

3. Demand conditions

4. Summary and prospects

Feast for Fine Merino Wool;

Famine for Broader Wool

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

Aus 18um

Sth Africa 21um

Aus 28um

USc/kgAustralia and South Africa

Source: AWEX, BWMB, NZ Wool Services

Prices to 25th January 2018

NZ Broad crossbred wool is 33-38 micron.

The UK wool price is the British Wool Marketing Board Indicator.

0

100

200

300

400

500

600

700

UK - Broad

NZ Broad Xbred

USc/kgNew Zealand and the UK

50

60

70

80

90

100

110

120

130

140

150

160

170

180

190

200

All Items Food

Metals Oil

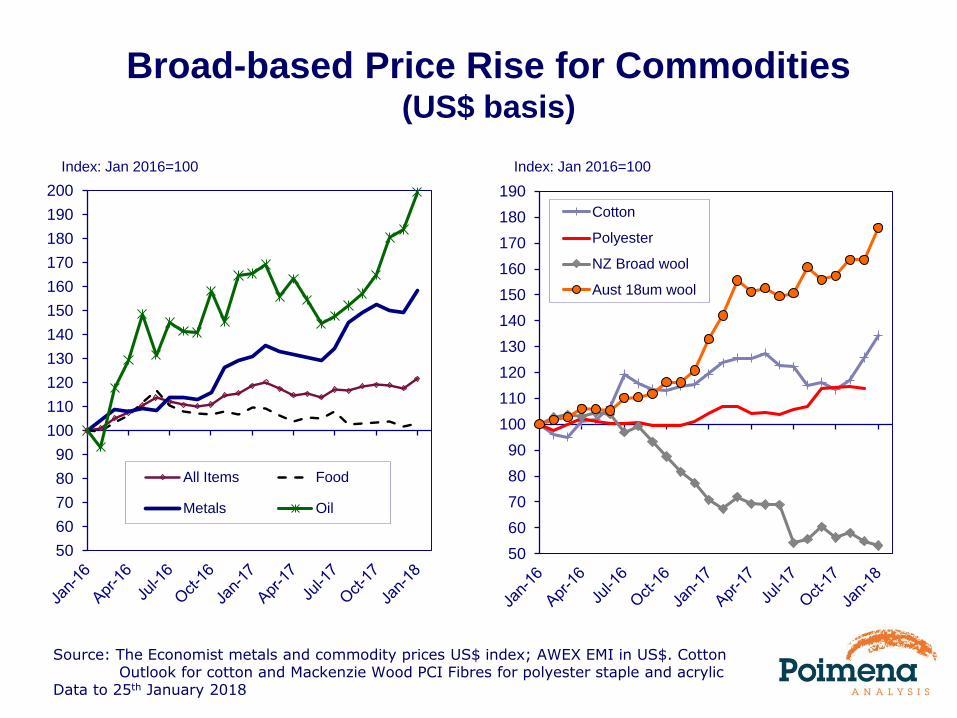

Index: Jan 2016=100

Broad-based Price Rise for Commodities(US$ basis)

Source: The Economist metals and commodity prices US$ index; AWEX EMI in US$. Cotton Outlook for cotton and Mackenzie Wood PCI Fibres for polyester staple and acrylic

Data to 25th January 2018

50

60

70

80

90

100

110

120

130

140

150

160

170

180

190

Cotton

Polyester

NZ Broad wool

Aust 18um wool

Index: Jan 2016=100

0

1

2

3

4

5

6

7

8

9

1018 micron

21 micron

Broad Xbred

Ratio

Fine Merino Wool Price Ratio at Highs;

Broad Wool Price Ratio at LowsUS$ terms

0

1

2

3

4

5

6

7

8

9

1018 micron

21 micron

Broad Xbred

Ratio Synthetics Cotton

Source: AWEX, Cotton Outlook, PCI Fibres, CIRFS, Woolmark, Poimena Analysis, Wool Services

International NZ

Data to January 2018

Note: For 18 micron and 21 micron wool it is Australian wool

For Broad Xbred it is New Zealand broad wool and the ratio is against acrylic fibre

0

200

400

600

800

1,000

1,200

1,400

1,600

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

US cents/kg

Source: AWEX – 2017/18 basis

Data to 25th January 2018

World Economic Events and Wool PricesAustralian Eastern Market Indicator

321 311

921

709

481

World economic

recovery, ‘dead-cat’

bounce post-RPS

706

World economic recovery,

cotton prices to records,

very strong A$

1508

trend

Asian Financial

Crisis

Global

Financial

Crisis

461

Stockpile sold,

supply squeeze

1400

Euro debt

crisis

918

Double-faced

woollen

fabric mania

1074

Commodity

prices rise –

superfine wool

prices up

Merino Wool Price Supercycles

DatePeak Price*

Price change - start

to peak*Weeks -

start to

peak

Comments

UScents Acents UScents Acents

February 1986

to May 19881203 1582

+743

(+162%)

+925

(+140%)111

Strong co-ordinated economic

growth, Soviet Union buying, China

begins, positive fashion styles

April 1993 to

March 1995707 949

+379

(+116%)

+496

(+107%)97

World economic recovery, post

Reserve Price Scheme collapse

“bounce”, China emerges

November 2001

to January 2003709 1211

+350

(+97%)

+501

(+71%)59

Last bale of the Australian wool

stockpile sold – kicks off price rise

May 2010 to

June 20111512 1434

+789

(+109%)

+564

(+65%)57

Global economic recovery after

GFC and cotton prices to 100+

year highs

April 2016 to

January 20181439 1818

+540

(+60%)

+586

(+48%)91

Solid economic growth in US & EU,

general commodity price rise.

Constrained Merino wool

production.

* Based on the Australian Eastern Market Indicator, 2017/18 basis

Total World Production Stable

But Broad Wool Production Rising

400

500

600

700

800

mkg clean

Apparel wool

Interior textiles wool

Source: IWTO, Country statistics, Poimena Analysis

Updated January 2018

2016 total production

1,140.5 mkg clean

2017 total production

1,147.9 mkg clean

Near 70 year lows

2018 total production

1,158.6 mkg clean

Stocks:Use ratio

~11%

Australia Dominates Global Merino Wool

Production% share

Source: AWTA, NZWTA, CapeWools, FLA, estimates by Poimena Analysis

Australia

South Africa

Argentina

Uruguay

New Zealand

USA

China CIS

SpainRest of world

Australian Wool Production Remains Near

Century Lows

0

200

400

600

800

1000

1200

19

01

19

06

19

11

19

16

19

21

19

26

19

31

19

36

19

41

19

46

19

51

19

56

19

61

19

66

19

71

19

76

19

81

19

86

19

91

19

96

20

01

20

06

20

11

20

16

mkg greasy

Source: Australian Bureau of Statistics, Australian Wool Production Forecasting Committee

Based on a season. 2018 = 2017/18

Forecast for 2017/18

345 mkg

Source: The US Conference Board, the European Commission and www.tradingeconomics.com

Data to December 2017

20

30

40

50

60

70

80

90

100

110

120

130

140

150

US

EU

Index

Jan 2008 = 100

60

70

80

90

100

110

120

130

140China

Japan

South Korea

Index

Jan 2008 = 100

Consumer Confidence Lifts in the Major Wool

Consuming Countries

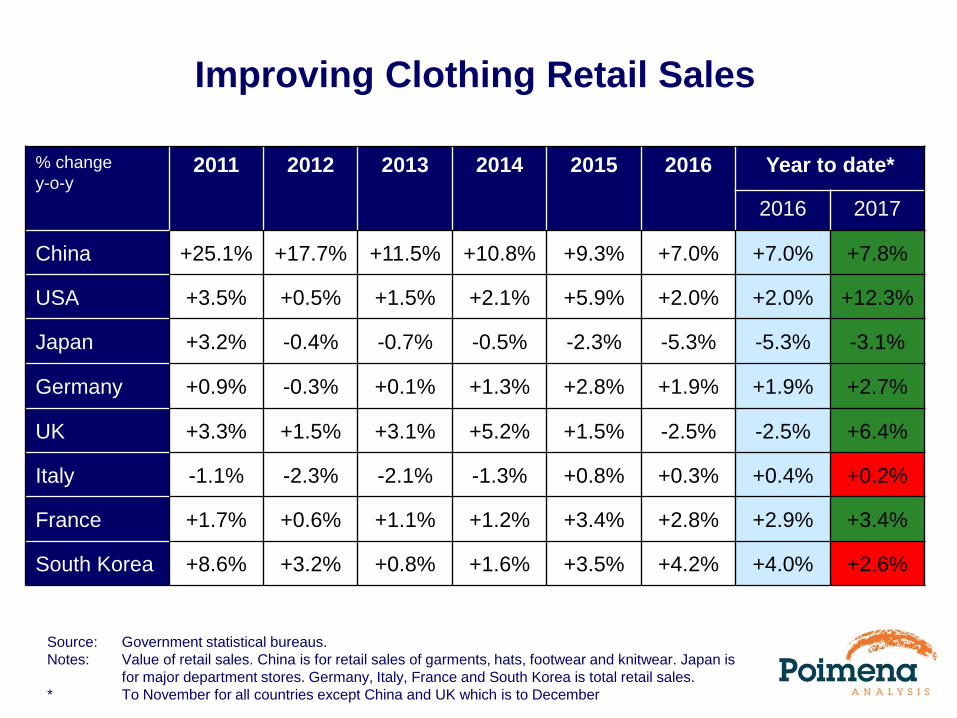

Improving Clothing Retail Sales

% change

y-o-y2011 2012 2013 2014 2015 2016 Year to date*

2016 2017

China +25.1% +17.7% +11.5% +10.8% +9.3% +7.0% +7.0% +7.8%

USA +3.5% +0.5% +1.5% +2.1% +5.9% +2.0% +2.0% +12.3%

Japan +3.2% -0.4% -0.7% -0.5% -2.3% -5.3% -5.3% -3.1%

Germany +0.9% -0.3% +0.1% +1.3% +2.8% +1.9% +1.9% +2.7%

UK +3.3% +1.5% +3.1% +5.2% +1.5% -2.5% -2.5% +6.4%

Italy -1.1% -2.3% -2.1% -1.3% +0.8% +0.3% +0.4% +0.2%

France +1.7% +0.6% +1.1% +1.2% +3.4% +2.8% +2.9% +3.4%

South Korea +8.6% +3.2% +0.8% +1.6% +3.5% +4.2% +4.0% +2.6%

Source: Government statistical bureaus.

Notes: Value of retail sales. China is for retail sales of garments, hats, footwear and knitwear. Japan is

for major department stores. Germany, Italy, France and South Korea is total retail sales.

* To November for all countries except China and UK which is to December

Improving Furnishings and Interior Textiles Retail Sales

% change y-o-y 2011 2012 2013 2014 2015 2016 Year to date*

2016 2017

China +32.8% +27.0% +21.0% +13.9% +16.1% +12.7% +12.7% +12.8%

USA +9.6% +4.7% +6.6% -1.2% +6.5% +4.1% +4.8% +7.4%

Japan -1.8% -1.8% -2.5% -1.8% -14.8% -19.2% -20.2% -8.4%

Germany +0.9% -0.3% +0.1% +1.3% +2.8% +1.9% +1.9% +2.7%

UK -22.1% +28.9% +14.5% -3.1% -29.3% -6.9% -6.9% +16.3%

Italy -1.1% -2.3% -2.1% -1.3% +0.8% +0.3% +0.4% +0.2%

France +1.7% +0.6% +1.1% +1.2% +3.4% +2.8% +2.9% +3.4%

South Korea +8.6% +3.2% +0.8% +1.6% +3.5% +4.2% +4.0% +2.6%

Source: Government statistical bureaus.

Notes: Value of retail sales. UK is for retail sales of floorcoverings. China is for furnishings. Japan is sales of

furnishings in department stores. US is personal consumption of carpets and other floor coverings

Germany, Italy, France and South Korea is total retail sales.

* To December for China and UK, to November for all other countries

Source: OTEXA. Data to November 2017

US Imports of Wool Products DropsValue (% year-on-year change of 12 mma)

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Wool

Cotton

Synthetics

% change y-o-y Clothing

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Wool

Cotton

Synthetics

% change y-o-yInterior textiles

China’s Exports of Most Wool Products Decline(Calendar Year to November - % change year on year)

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

% change y-o-y

2014 2015

2016 2017

Wool Product Exports

Source: China Customs and China Wool Textile Association; US Department of Commerce

Wool imports is for raw and semi-processed wool (including wool top)

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

% change y-o-y

2014 2015

2016 2017

Raw and Semi-processed Imports

Wool Imports by Major Processing CountriesCalendar Year to November

0 25 50 75 100 125 150 175 200 225 250 275 300 325 350 375 400

China

India

Italy

Germany

Czech Republic

Other Europe

Other

mkg greasy equiv.

2017 2016 2015

2014 2013

-2%

-5%

+4%

-6%

-2%

+2%

-1%

Note: From the five major exporting countries (Australia, New Zealand, Argentina, Uruguay and

South Africa

Source: Australian Bureau of Statistics, FLA, SUL, Capewools, Beef + Lamb NZ

Wool Export Volumes by Major Exporters12 month rolling aggregate

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Australia

New Zealand

Total

% change y-o-y

Source: Australian Bureau of Statistics, FLA, SUL, Capewools, NZ Beef + Lamb

Data to November 2017

-40%

-20%

0%

20%

40%

60%

Argentina

South Africa

Uruguay

% change y-o-y

Summary of Drivers

Merino

1. Low production of finer wool

2. Virtually no stocks left

3. Increased raw wool demand, notably from

China

4. Higher economic growth leading to upturn in

commodity prices (including Merino wool)

5. High consumer confidence and higher

clothing retail sales growth

6. Increased use of Merino wool in active and

leisurewear?

BUT

1. High price relativity for Merino wool against

competing fibres

2. Lower imports of wool clothing by US

3. Are pipeline stocks growing?

Broad Wool

1. Increased production of broader wool

2. High stocks held in New Zealand

3. Raw wool demand from China fell in 2016/17

4. Substitution of broad wool by acrylic and

nylon?

5. Slowdown in use of broad wool in apparel

products in China?

6. Patchy retail sales for furnishings

7. Trade in wool carpets falls

BUT

1. Broad Crossbred wool price relativity at lows

2. High consumer confidence in key countries

3. New style knitting products using broad wool in

China

Prospects for 2018

➢ Merino wool prices at highs, but

could be near a cyclical peak

➢ Broad wool prices at the bottom?

➢ Longer term demand trends and

prospects positive for Merino wool

➢ Product development will be key

for broad wool

Will it be feast or famine?

Merino Wool Price Supercycles – the Downside

Date

Price change –

peak to low*Low Price* Weeks

– peak

to low

Comments

UScents Acents UScents Acents

May 1988 to

March 1991

-666

(-55%)

-1045

(-66%)418 537 111

Collapse of the Reserve Price

Scheme, Soviet Union falls apart,

Tiananmen Square

March 1995 to

May 1996

-232

(-33%)

-343

(-36%)475 606 97

Market adjusts to massive

stockpile in Australia after ‘dead-

cat’ bounce post-collapse of

Reserve Price Scheme

January 2003 to

December 2005

-229

(-32%)

-562

(-46%)480 649 59

Economic slowdown, excess

stocks in wool textile industry,

SARS outbreak in China triggers

price fall

June 2011 to

September 2012

-549

(-36%)

-501

(-35%)963 933 57

Global cotton prices drop as China

builds up massive cotton stockpile,

causing drop in all fibre prices.

Excess stocks in wool textile

industry

* Based on the Australian Eastern Market Indicator, 2017/18 basis

Thank You!