FBI Summary

22

Lecture 1 – Overview (Chpt. 2) & Interest rates / valuing credit instruments (Chpt. 3) Functions of financial markets Financial markets perform the essential economic function of channeling funds from households, firms, and governments that have saved surplus funds by spending less than their income to those that have a shortage of funds because they wish to spend more than their income. This function is shown schematically in the figure below. In direct finance (the route at the bottom of Figure 2.1), borrowers borrow funds directly from lenders in financial markets by selling them securities (also called financial instruments), which are claims on the borrower’s future income or assets. Securities are assets for the person who buys them, but they are liabilities (IOUs or debts) for the individual or firm that sells (issues) them. Financial markets are essential for promoting economic efficiency by linking people with funds to people who have investment opportunities. Overview of financial markets A debt instrument is short-term if its maturity is less than a year and long- term if its maturity is 10 years or longer. Debt instruments with a maturity between one and 10 years are said to be intermediate-term . • Security : is a claim on the issuer’s future income or assets. • Bond : is a debt security that promises to make payments periodically for a specified period of time. • Stock : is a claim on the earnings and assets of the corporation as it represents a share of ownership. A primary market is a financial market in which new issues of a security, such as a bond or a stock, are sold to initial buyers by the corporation or government agency

Transcript of FBI Summary

8/12/2019 FBI Summary

http://slidepdf.com/reader/full/fbi-summary 1/22

Lecture 1 – Overview (Chpt. 2) & Interest rates / valuing credit instruments (Chpt. 3)

Functions of financial marketsFinancial markets perform the essential economic function of channeling funds fromhouseholds, firms, and governments that have saved surplus funds by spending less

than their income to those that have a shortage of funds because they wish to spendmore than their income. This function is shown schematically in the figure below.

In direct finance (the route at the bottom of Figure 2.1), borrowers borrow fundsdirectly from lenders in financial markets by selling them securities (also calledfinancial instruments), which are claims on the borrower’s future income or assets.Securities are assets for the person who buys them, but they are liabilities (IOUs or

debts) for the individual or firm that sells (issues) them.

Financial markets are essential for promoting economic efficiency by linking people

with funds to people who have investment opportunities.

Overview of financial marketsA debt instrument is short-term if its maturity is less than a year and long- term if

its maturity is 10 years or longer. Debt instruments with a maturity between one and10 years are said to be intermediate-term .

• Security : is a claim on the issuer’s future income or assets.• Bond : is a debt security that promises to make payments periodically for a

specified period of time.• Stock : is a claim on the earnings and assets of the corporation as it

represents a share of ownership.

A primary market is a financial market in which new issues of a security, such as abond or a stock, are sold to initial buyers by the corporation or government agency

8/12/2019 FBI Summary

http://slidepdf.com/reader/full/fbi-summary 2/22

borrowing the funds. A secondary market is a financial market in which securities

that have been previously issued can be resold. The secondary market serves twoimportant functions:

• Provide liquidity, making it easy to buy and sell the securities of the companies• Establish a price for the securities

There are two types of secondary markets:Exchanges: Buyers and sellers meet in central locations (New York StockExchange, CBT)Over-the-Coun ter OTC) Markets : Dealers at different locations buy and sell

(U.S. government bond market)

Money market: a financial market in which only short-term debt instruments

(generally those with original maturity of less than one year) are traded.Capital market : the market in which longer- term debt (generally with originalmaturity of one year or greater) and equity instruments are traded.

Foreign bonds are sold in a foreign country and are denominated in that country’scurrency. A Eurobond is a bond denominated in a currency other than that of thecountry in which it is sold (e.g. bond denominated in U.S. dollars sold in London).

Financial intermediariesFinancial intermediaries are important for several reasons. They:

• Reduce transaction costs by developing expertise and taking advantage of

economies of scale• Provide its customers with l iquidity services, services that make it easier for

customers to conduct transactions (e.g. checking accounts that enable them

to pay their bills easily)• Reduce the exposure of investors to risk, through risk sharing . This is done

by:! Performing asset transformation, intermediaries create and sell

assets with risk characteristics that people are comfortable with, and the

intermediaries then use the funds they acquire by selling these assets topurchase other assets that may have far more risk.

! Helping investors to diversify their asset holdings. Low transaction costs

allow financial intermediaries to do this by pooling a collection of assetsinto a new asset and then selling it to individuals

Financial intermediaries help reduce the impact of asymmetric information .

Adverse selection is the problem created by asymmetric information before thetransaction occurs. Adverse selection in financial markets occurs when the potentialborrowers who are the most likely to produce an undesirable (adverse) outcome—the

bad credit risks—are the ones who most actively seek out a loan and are thus mostlikely to be selected. Because adverse selection makes it more likely that loans mightbe made to bad credit risks, lenders may decide not to make any loans even thoughthere are good credit risks in the marketplace. Moral hazard is the problem

created by asymmetric information after the trans- action occurs. Moral hazard in

financial markets is the risk (hazard) that the borrower might engage in activities that

are undesirable (immoral) from the lender’s point of view, because they make it lesslikely that the loan will be paid back. Because moral hazard lowers the probability

8/12/2019 FBI Summary

http://slidepdf.com/reader/full/fbi-summary 3/22

that the loan will be repaid, lenders may decide that they would rather not make a

loan. With financial intermediaries in the economy, small savers can provide theirfunds to the financial markets by lending these funds to a trustworthy intermediary—say, the Honest John Bank—which in turn lends the funds out either by making loansor by buying securities such as stocks or bonds. Successful financial intermediaries

have higher earnings on their investments than small savers, because they are betterequipped than individuals to screen out bad credit risks from good ones, therebyreducing losses due to adverse selection. In addition, financial intermediaries havehigh earnings because they develop expertise in monitoring the parties they lend to,

thus reducing losses due to moral hazard.

Types of financial intermediaries

Regulation of the financial systemThe government regulates financial markets for two main reasons: to increase theinformation available to investors and to ensure the soundness of the financial

system.

Government regulation can reduce adverse selection and moral hazard problems infinancial markets and increase their efficiency by increasing the amount of

information available to investors. For example: The SEC requires corporations

issuing securities to disclose certain information about their sales, assets, and

earnings to the public and restricts trading by the largest stockholders (known asinsiders) in the corporation

8/12/2019 FBI Summary

http://slidepdf.com/reader/full/fbi-summary 4/22

To protect the public and the economy from f inancial panics (the widespread

collapse of financial intermediaries), the government has implemented six types ofregulations:

• Restrictions on entry: There is a need to obtain a charter from the state orthe federal government when wanting to set up a financial intermediary.

• Disclosure : stringent reporting requirements for financial intermediaries.Their bookkeeping must follow certain strict principles, their books aresubject to periodic inspection, and they must make certain informationavailable to the public.

• Restrictions on assets and activit ies : There are restrictions on whatfinancial intermediaries are allowed to do and what assets they can hold. (e.g.commercial banks and other depository institutions are not allowed to hold

common stock because stock prices experience substantial fluctuations.)• Deposit Insurance: The government can insure people’s deposits so that

they do not suffer great financial loss if the financial intermediary that holds

these deposits should fail.

• Limits on competit ion: Politicians have often declared that unbridledcompetition among financial intermediaries promotes failures that will harm

the public. Although the evidence that competition has this effect is extremelyweak, state and federal governments at times have imposed restrictions onthe opening of additional locations (branches).

• Restrictions on interest rates: Competition has also been inhibited byregulations that impose restrictions on interest rates that can be paid ondeposits. These regulations were instituted because of the widespread beliefthat unrestricted interest- rate competition helped encourage bank failuresduring the Great Depression. Later evidence does not seem to support this

view, and Regulation Q has been abolished (although there are stillrestrictions on paying interest on checking accounts held by businesses).

Interest ratesFour basic types of credit instruments which incorporate present value concepts:

• Simple loan

• Fixed payment loan• Coupon bond• Discount bond

Simple loan

The last two regulations are not mentioned on the slide, probablybecause there is less evidence to support these regulations.

8/12/2019 FBI Summary

http://slidepdf.com/reader/full/fbi-summary 5/22

Fixed payment loan

Principal and interest are repaid often monthly and in equal amounts over the loanterm. Examples: auto loans and home mortgages.

E x a m p l e q u e s t io n

Consider a 30-year, fixed-rate mortgage for $100,000 at an interest rate of 9%. What

is the monthly mortgage payment?

Use the formula with n=360 and i=0.09/12Answer should be FP=$804.62

Coupon bond

E x a m p l e q u e s t io n

Consider a coupon bond that has a $1,000 face value, a coupon rate of 7%, a 9% yieldto maturity and 8 years to maturity. What is the bond’s price?

8/12/2019 FBI Summary

http://slidepdf.com/reader/full/fbi-summary 6/22

Discount bond

Three interesting facts about bonds1. When the coupon bond is priced at its face value, the yield to maturity equals

the coupon rate.

2.

The price of a coupon bond and the yield to maturity are negatively related;that is, as the yield to maturity rises, the price of the bond falls. If the yield tomaturity falls, the price of the bond rises.

3. The yield to maturity is greater than the coupon rate when the bond price isbelow its face value.

Distinction between real and nominal interest ratesNominal interest rate is the interest rate that is not adjusted for inflation. The

real interest rate is the interest rate is the rate that is adjusted by subtractingexpected changes in the price level (inflation) so that it more accurately reflects thetrue cost of borrowing. This interest rate is more precisely referred to as the ex ante

real interest rate because it is adjusted for expected changes in the price level. The exante real interest rate is most important to economic decisions, and typically it iswhat financial economists mean when they make reference to the “real” interest rate.The interest rate that is adjusted for actual changes in the price level is called the expost real interest rate . It describes how well a lender has done in real terms after the

fact .

E x a m p l e q u e s t io n

What is the real interest rate if the nominal interest rate is 8% and the expectedinflation rate is 10% over the course of a year?

8/12/2019 FBI Summary

http://slidepdf.com/reader/full/fbi-summary 7/22

Distinction between interest rates and returns

Impact of interest rate changes and maturityThe figure above leads to the following conclusions:

• A rise in interest rates is associated with a fall in bond prices, resulting incapital losses on bonds whose terms to maturity are longer than the holdingperiod.

• The more distant a bond’s maturity, the greater the size of the price changeassociated with an interest-rate change.

• The more distant a bond’s maturity, the lower the rate of return that occurs asa result of the increase in the interest rate.

• Even though a bond has a substantial initial interest rate, its return can turnout to be negative if interest rates rise.

Prices and returns for long-term bonds are more volatile than those for shorter-termbonds. The riskiness of an asset’s return that results from interest-rate changes iscalled interest-rate risk.

If an investor’s holding period is longer than the term to maturity of the bond, the

investor is exposed to a type of interest-rate risk called reinvestment risk .

Reinvestment risk occurs because the proceeds from the short-term bond need to bereinvested at a future interest rate that is uncertain.

8/12/2019 FBI Summary

http://slidepdf.com/reader/full/fbi-summary 8/22

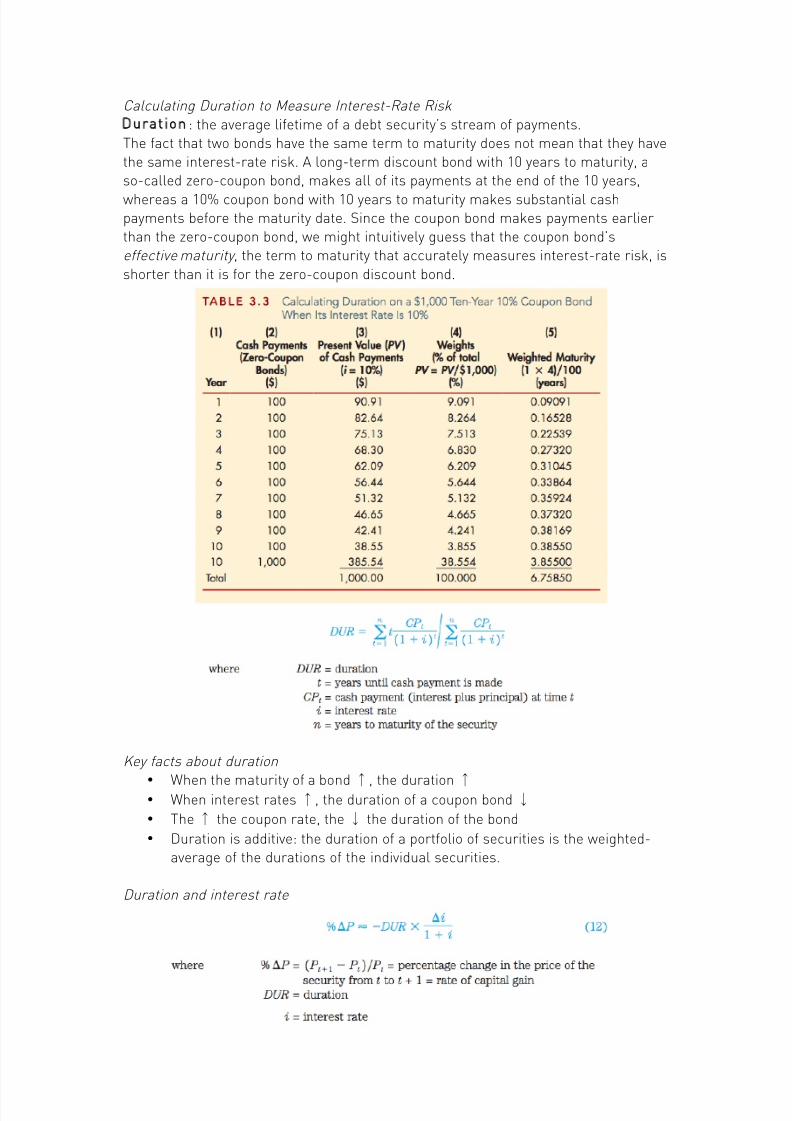

Calculating Duration to Measure Interest-Rate Risk

Duration : the average lifetime of a debt security’s stream of payments.The fact that two bonds have the same term to maturity does not mean that they havethe same interest-rate risk. A long-term discount bond with 10 years to maturity, aso-called zero-coupon bond, makes all of its payments at the end of the 10 years,

whereas a 10% coupon bond with 10 years to maturity makes substantial cashpayments before the maturity date. Since the coupon bond makes payments earlierthan the zero-coupon bond, we might intuitively guess that the coupon bond’seffective maturity , the term to maturity that accurately measures interest-rate risk, is

shorter than it is for the zero-coupon discount bond.

Key facts about duration•

When the maturity of a bond↑, the duration↑ • When interest rates↑, the duration of a coupon bond↓

• The↑ the coupon rate, the↓ the duration of the bond

• Duration is additive: the duration of a portfolio of securities is the weighted-average of the durations of the individual securities.

Duration and interest rate

8/12/2019 FBI Summary

http://slidepdf.com/reader/full/fbi-summary 9/22

Lecture 2 - Interest Rates /determinants (Chpt. 4&5)

Determinants of asset demand• Wealth , the total resources owned by the individual, including all assets• Expected return (the return expected over the next period) on one asset

relative to alternative assets• Risk (the degree of uncertainty associated with the return) on one asset

relative to alternative assets• Liquidity (the ease and speed with which an asset can be turned into cash)

relative to alternative assets

8/12/2019 FBI Summary

http://slidepdf.com/reader/full/fbi-summary 10/22

Market equilibrium

8/12/2019 FBI Summary

http://slidepdf.com/reader/full/fbi-summary 11/22

Shift in demand and supply curves

8/12/2019 FBI Summary

http://slidepdf.com/reader/full/fbi-summary 12/22

Risk structure of interest rates

It is possible that bonds offer similar payment streams, but differ in price. This is dueto the risk structure of interest rates. There are a couple of factors that affectthe risk structure of interest rates.

D e f a u l t Default occurs when the issuer of the bond is unable or unwilling to makeinterest payments when promised or pay off the face value when the bond matures.Bonds with no default risk are called default-free bonds (e.g. U.S. treasury bonds).The spread between the interest rates on bonds with default risk and default-free

bonds, both of the same maturity, called the risk premium , indicates how muchadditional interest people must earn to be willing to hold that risky bond.

Because default risk is so important to the size of the risk premium, purchasers ofbonds need to know whether a corporation is likely to default on its bonds. This

information is provided by credit-rating agencies, investment advisory firms that ratethe quality of corporate and municipal bonds in terms of the probability of default.

8/12/2019 FBI Summary

http://slidepdf.com/reader/full/fbi-summary 13/22

L i q u i d i t y A liquid asset is one that can be quickly converted into cash. The more

liquid an asset is, the more desirable it is. Risk premium reflects not only default riskbut also lower liquidity. This is why a risk premium is sometimes called a risk andliquidity premium .

I n c o m e t a x c o n s i d e r a t i o n s Municipal bonds tend to have a lower rate than theTreasury bonds although they have default risk and they are less liquid. Theexplanation lies in the fact that interest payments on municipal bonds are exemptfrom federal income taxes, a factor that has the same effect on the demand for

municipal bonds as an increase in their expected return.

Term structure of interest rates

Bonds with identical risk, liquidity, and tax characteristics may have different interestrates because the time remaining to maturity is different. A plot of the yields on bondswith differing terms to maturity but the same risk, liquidity, and tax considerations is

called a yield curve.

Expectations theoryKey assumption: Bonds of different maturities are perfect substitutes.Implication: Expected returns on bonds of different maturities are equal.

Two alternative investment strategies for a two-year time horizon:1. Buy $1of one-year bond, and when it matures, buy another one-year bond with

your money.2. Buy $1 of two-year bond and hold it.

Because the expected returns of holding a two-period bond for two years is the sameas holding one-period bonds for two periods bonds, we get the following equation:

This leads to:

The expectations theory is an attractive theory because it provides a simple

explanation of the behavior of the term structure, but unfortunately it has a majorshortcoming: It cannot explain the fact that yield curves usually slope upward. The

typical upward slope of yield curves implies that short-term interest rates are usuallyexpected to rise in the future. In practice, short-term interest rates are just as likely

to fall as they are to rise, and so the expectations theory suggests that the typicalyield curve should be flat rather than upward sloping.

Numerical example expectation theory:One-year interest rate over the next five years are expected to be 5%, 6%, 7%, 8% and9%• Interest rate on two-year bond today: (5% + 6%)/2 = 5.5%

• Interest rate for five-year bond today: (5% + 6% + 7% + 8% + 9%)/5 = 7%

8/12/2019 FBI Summary

http://slidepdf.com/reader/full/fbi-summary 14/22

Market segmentation theory

Key assumption: Bonds of different maturities are NOT substitutes at all .Implication: Interest rates at each maturity are determined separately.

The argument for why bonds of different maturities are not substitutes is that

investors have strong preferences for bonds of one maturity but not for another, sothey will be concerned with the expected returns only for bonds of the maturity theyprefer. This might occur because they have a particular holding period in mind, and ifthey match the maturity of the bond to the desired holding period, they can obtain a

certain return with no risk at all. (We have seen in Chapter 3 that if the term tomaturity equals the holding period, the return is known for certain because it equalsthe yield exactly, and there is no interest-rate risk.)

Liquidity premium theoryKey assumption: Bonds of different maturities are substitutes, but are not perfect

substitutes.

Investors tend to prefer shorter-term bonds because these bonds bear less interest-rate risk. For these reasons, investors must be offered a positive liquidity premium toinduce them to hold longer-term bonds.

Shortcoming: Assumes that all lenders want to lend short and all borrowers want

to borrow long!

8/12/2019 FBI Summary

http://slidepdf.com/reader/full/fbi-summary 15/22

Market predictions of future short rates

8/12/2019 FBI Summary

http://slidepdf.com/reader/full/fbi-summary 16/22

Lecture 3 - Financial Markets (Chapters 11-14)

Money marketsThe term money market is actually a misnomer. Money—currency—is not traded inthe money markets. Because the securities that do trade there are short-term and

highly liquid, however, they are close to being money. Money market securities, whichare discussed in detail in this chapter, have three basic characteristics in common:

• They are usually sold in large denominations.• They have low default risk.• They mature in one year or less from their original issue date. Most money

market instruments mature in less than 120 days.

Why do we need money markets?Bank regulation creates a distinct cost advantage for money markets over banks.Because of reserve requirements banks cannot invest all of the money they receive

and thus they must pay a lower interest rate to de depositor than if the full depositcould be invested. Regulations on the ceiling rate lead to a significant growth inmoney markets. The Glass-Steagall Act, 1933, placed a ceiling on the rates bankcould pay for funds. Because of this people pulled their money out of banks when theinflation pushed short-term interest rates above the level that banks could legally

pay, and put their money into money market security accounts offered by manybrokerage firms. Interest rate ceilings were removed in 1986. Money markets alsoprovide a way to solve cash-timing problems.

Money Market Participants• U.S. Treasury Department• Federal Reserve System• Commercial Banks• Businesses• Investment and Securities Firms• Individuals

8/12/2019 FBI Summary

http://slidepdf.com/reader/full/fbi-summary 17/22

Money market instruments • Treasury Bills• Federal Funds: Used by banks to meet reserve requirements. Federal funds

are short-term funds transferred (loaned or borrowed) between financialinstitutions, usually for a period of one day. The term federal funds (or fed

funds) is misleading. Fed funds really have nothing to do with the federalgovernment. The term comes from the fact that these funds are held at theFederal Reserve bank

• Repurchase Agreements: A short-term collateralized loan.• Negotiable Certificates of Deposit: A bank-issued security that documents a

deposit• Commercial Paper: Unsecured promissory notes, issued by corporations, that

mature in no more than 270 days. Because these securities are unsecured,only the largest and most creditworthy corporations issue commercial paper.The interest rate the corporation is charged reflects the firm’s level of risk.

• Banker’s acceptance: A banker’s acceptance is an order to pay a specifiedamount of money to the bearer on a given date. They are used to financegoods that have not yet been transferred from the seller to the buyer. Forexample, suppose that Builtwell Construction Company wants to buy abulldozer from Komatsu in Japan. Komatsu does not want to ship the

bulldozer without being paid because Komatsu has never heard of Builtwelland realizes that it would be difficult to collect if payment were notforthcoming. Similarly, Builtwell is reluctant to send money to Japan before

receiving the equipment. A bank can intervene in this standoff by issuing abanker’s acceptance where the bank in essence substitutes itscreditworthiness for that of the purchaser.

• Eurodollars: Dollar denominated time deposits held in foreign banks

8/12/2019 FBI Summary

http://slidepdf.com/reader/full/fbi-summary 18/22

Capital market

Typically for long-term financing or investments.Primary issuers of securities: Federal and local governments and corporations.Capital market trading: 1) Primary market for initial sale (IPO) 2) Secondary market

Treasury notes and bonds• Treasury bill: less than one year• Treasury note: one to 10 years• Treasury bond: 10 to 30 years

Interest rates are very low because there is no default risk, there is however inflationrisk. The Treasury Department began offering bonds designed to remove inflation

risk. At maturity, these securities are redeemed at the greater of their inflation-adjusted principal or par amount at original issue.

Municipal bondsIssued by local, county, and state governments. Used to finance public interestprojects. May be tax-free. NOT default-free (e.g., Orange County California).

Corporate bonds

Typically have a face value of $1,000, although some have a face value of $5,000 or$10,000. Pay interest semi-annually. Most are callable. Bond indenture states thelender’s rights and the borrower’s obligations.

Since bondholders cannot look to managers for protection when the firm gets intotrouble, they must include rules and restrictions on managers designed to protect the

bondholders’ interests. These are known as restrictive covenants . They usuallylimit the amount of dividends the firm can pay (so to conserve cash for interestpayments to bondholders) and the ability of the firm to issue additional debt. Otherfinancial policies, such as the firm’s involvement in mergers, may also be restricted.Restrictive covenants are included in the bond indenture. Typically, the interest rate

will be lower the more restrictions are placed on management through restrictivecovenants because the bonds will be considered safer by investors.

Most corporate indentures include a call provision , which states that the issuer hasthe right to force the holder to sell the bond back. The price bondholders are paid for

the bond is usually set at the bond’s par price or slightly higher (usually by one year’sinterest cost). For example, a 10% coupon rate $1,000 bond may have a call price of

$1,100. If interest rates fall, the price of the bond will rise. If rates fall enough, theprice will rise above the call price, and the firm will call the bond.

Some bonds can be converted into shares of common stock. This feature permitsbondholders to share in the firm’s good fortunes if the stock price rises. Mostconvertible bonds will state that the bond can be converted into a certain numberof common shares at the discretion of the bondholder. The conversion ratio will be

such that the price of the stock must rise substantially before conversion is likely to

occur. Issuing convertible bonds is one way firms avoid sending a negative signal to

the market. In the presence of asymmetric information between corporate insidersand investors, when a firm chooses to issue stock, the market usually interprets this

8/12/2019 FBI Summary

http://slidepdf.com/reader/full/fbi-summary 19/22

action as indicating that the stock price is relatively high or that it is going to fall in

the future. The market makes this interpretation because it believes that managersare most concerned with looking out for the interests of existing stockholders and willnot issue stock when it is undervalued.

Types of corporate bonds• Secured Bonds (with collateral): Mortgage bonds• Unsecured Bonds: Debentures. Have lower priority if the firm defaults. Have

higher interest rates• Junk Bonds: Debt that is rated below BBB

Finding the price of semiannual bonds

StocksStocks represent ownership in a firm. Stockholders can earn a return in two ways: an

increase in the price of the stock or trough dividends. Ownership of stock gives thestockholder certain rights regarding the firm: residual claimant: Stockholders have aclaim on all assets and income left over after all other claimants have been satisfied,

if nothing is left over, they receive nothing. Stockholders also have the right to vote fordirectors and on certain issues such as amendments to the corporate charter andwhether new shares should be issued.

There are two types of stock:• Common stock

! Give the right to vote! Receive dividends

• Preferred stock! Receive a fixed dividend!

Do not usually vote

How are stocks sold?• Organized exchanges

! NYSE is best known! Others: the American Stock Exchange, Nikkei, London Stock Exchange

and DAX.! Auction markets with floor specialists

• Over-the-counter markets ! Best example Is NASDAQ

! Important market for thinly-traded securities

8/12/2019 FBI Summary

http://slidepdf.com/reader/full/fbi-summary 20/22

• ECNs (Electronic communication networks)! A"low to trade without the need of the middleman! Do not work as well with thinly-traded stocks

• Exchange Traded Funds! Represent a basket of securities

! Traded on a major exchange

One period valuation model

The generalized dividend valuation model

Gordon growth model

This model uses two assumptions:1. Dividends are assumed to continue growing at a constant rate2. The growth rate is assumed to be less than the required return on equity

Price earnings valuation method

The price earnings ratio (PE) is a widely watched measure of how much the market iswilling to pay for $1 of earnings from a firm. A high PE has two interpretations.

1. A higher-than-average PE may mean that the market expects earnings to risein the future. This would return the PE to a more normal level.

2.

A high PE may alternatively indicate that the market feels the firm’s earningsare very low risk and is therefore willing to pay a premium for them.

The PE ratio can be used to estimate the value of a firm’s stock. Note thatalgebraically the product of the PE ratio times expected earnings is the firm’s stockprice.

8/12/2019 FBI Summary

http://slidepdf.com/reader/full/fbi-summary 21/22

Errors in valuations• Problems with estimating growth • Problems with estimating required return • Problems with forecasting dividends

What are mortgages?A mortgage is a long-term loan secured by real estate. The loan is amortized : Theborrower pays it off over time in some combination of principal and interest paymentsthat result in full payment of the debt by maturity.

Mortgage interest ratesDetermined by:

• Market Rates: general rates on Treasury bonds• Term: longer-term mortgages have higher rates• Discount Points: a lower rate negotiated for cash upfront.

Mortgage calculation formulas

Monthly mortgage payment:

Remaining balance at end of month t:

Principal payment for month t :

E x a m p l e q u e s t io n

Suppose that you are offered two loan alternatives. In the first, you pay no discount

points and the interest rate is 12%. In the second, you pay 2 discount points butreceive a lower interest rate of 11.5%. Which alternative do you choose?

First calculate the effective annual rate on the no-point loan.

Effective annual rate = (1.01)12 – 1 = 0.1268 = 12.68%

Using the formula for calculating FP (see above) this gives a monthly payment of$1,028.61.

8/12/2019 FBI Summary

http://slidepdf.com/reader/full/fbi-summary 22/22

Now calculate the monthly payment for option 2 (so with an i of 11.5%/12), keeping

the LV at 100.000. This will give a monthly payment of 990.29. When the formula issolved for i this will give an i of 0.009803535. (1.009803535)12 – 1 = 0.1242 = 12.42%.

If you do not pay off early, option 2 is a better choice.

How long do you have to stay in the house for the mortgage with points to be a betteroption?

First, compare the required payments for both options: $1,028.61 - $990.29 = $38.32

Now calculate when the present value of the savings is $2,000.

Using I% = 1 PV = 2000 PMT = -38.32 solve for N -> gives N = 74

So, if you think you will stay in the house and not refinance for at least 74 moths,choose the second option.