Farmers Long Term Care Original seminar design by: Benefits Services Inc. Reisterstown, Md.

25

Farmers Long Term Care Original seminar design by: Benefits Services Inc. Reisterstown, Md.

-

Upload

cecil-weaver -

Category

Documents

-

view

216 -

download

1

Transcript of Farmers Long Term Care Original seminar design by: Benefits Services Inc. Reisterstown, Md.

Farmers Long Term Care

Original seminar design by:Benefits Services Inc.Reisterstown, Md.

Do You NeedLong Term Care

Protection?

Do You NeedLong Term Care

Protection?

Four Major QuestionsMust be Answered

Do you need it?

Can you afford it?

Which combination of benefits is right for you?

Which policy can best provide those benefits for you?

What is Long Term Care?

Day in, day out assistance you need when you have a serious illness or disability that lasts for a period of time causing you to be unable to completely care for yourself

A continuum of care...

Long Term Care Services: More Than Just Nursing Homes

Adult Day Care CentersRespite CareHome Health Care AidePersonal Care Attendant or

Chore ServicesAssisted Living FacilitiesHospice Care

What Are The Chances of Needing Long Term Care?

Age 55: The chances are 1 in 10

Age 65: The chances are 4 in 10

Age 75: The chances are 6 in 10

Source: National Nursing Home Study, Source: National Nursing Home Study, National Center for Health Statistics, 1985National Center for Health Statistics, 1985

Two Aspects of Long Term Care Insurance

Home and Community Based Care

Nursing Home Care

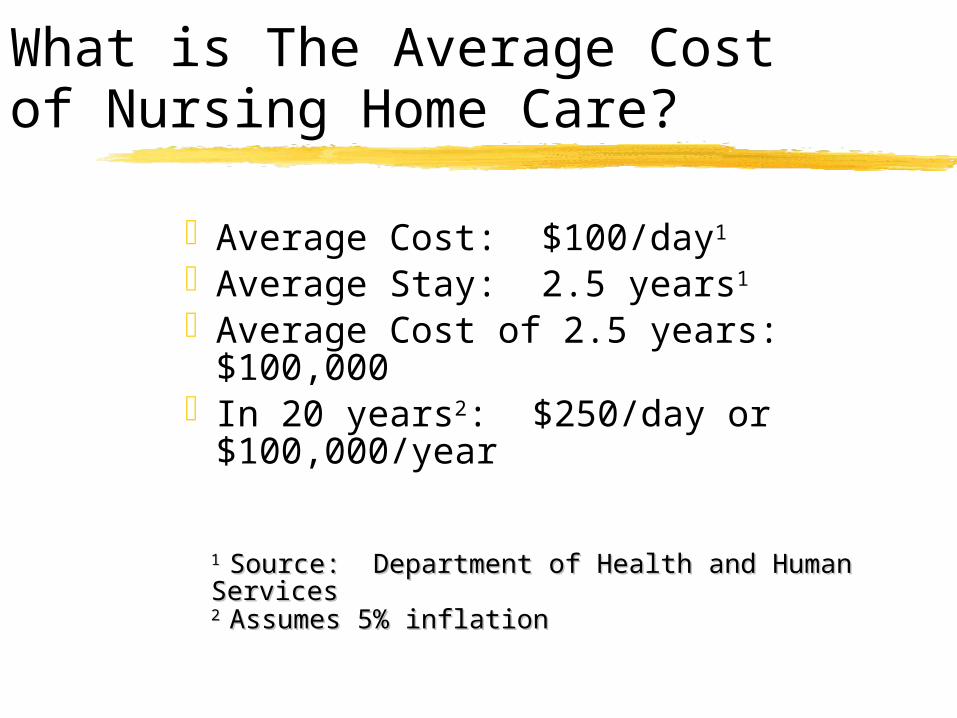

What is The Average Cost of Nursing Home Care?

Average Cost: $100/day1

Average Stay: 2.5 years1

Average Cost of 2.5 years: $100,000In 20 years2: $250/day or

$100,000/year

1 1 Source: Department of Health and Human ServicesSource: Department of Health and Human Services2 2 Assumes 5% inflationAssumes 5% inflation

Four Sources of Funds to Pay for

Long Term Care

Who Will Pay for Long Term Care?Who Will Pay for Long Term Care?

Medicare andMedicare Supplements

Pays less than 8% of Long Term Care costs

Covers only skilled care

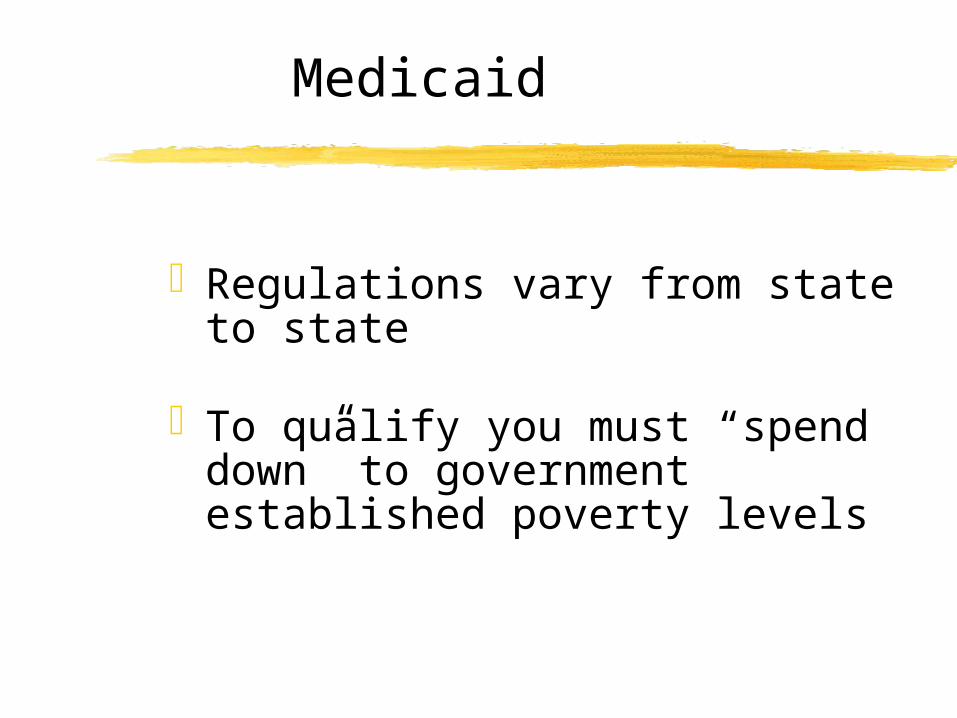

Medicaid

Regulations vary from state to state

To qualify you must “spend down” to government established poverty levels

The Health Insurance Portability and Accountability Act of 1996

The Government has sent a

clear message that it is your

responsibility to take care of

your Long Term Care needs.

The Health Insurance Portability and

Accountability Act of 1996: A Closer Look

LTC premiums are deductible as a medical expense

LTC benefits received are tax-free

LTC expenses not covered by insurance are deductible

The Health Insurance Portability and

Accountability Act of 1996: A Closer Look

Employers who pay premiums for an employee are entitled to deduct that premium as a business expense, as they do for medical insurance.

Premiums paid by an employer on behalf of an employee will not be treated as income to that employee.

The Health Insurance Portability and

Accountability Act of 1996: A Closer Look

Self-employed individuals can

deduct 45% of premiums as a

business expense.

Who Will Pay the Cost of Long Term Care?

Your Personal Savings Can you afford to gamble?

Long Term Care Insurance Share the risk with the

insurance company

What Are The Financial Risks You Face Today?

Your home destroyed by fire:1 chance in 1,200

An auto accident liability suit:1 chance in 240

A major medical expense: 1 chance in 15A major long term care expense:

1 chance in 4

Source: Sadler and Newman, LAN, November, 1993Source: Sadler and Newman, LAN, November, 1993

Each of these risks could result Each of these risks could result in a loss of $100,000 or more:in a loss of $100,000 or more:

Most people have insurance to cover the first three risks –

What about the Fourth?

Four Questions You Need To Be Able To Answer

Do you have longevity in your family?Do you think you could spend down your

savings if there was a long term care illness?

Do you think long term care expenses can be one of the single most greatest risks one may face in their lifetime?

Do you want a family member to take care of you? Will they and can they?

Five Factors that Impactthe Premium....

Benefit Length

Daily Benefit

Elimination Period

Home Health Care Protection

Inflation Protection

The Essential Factors in a Good Long Term Care Policy...

Financially stable company

Guaranteed renewable

No prior hospitalization

Well-defined benefit triggers

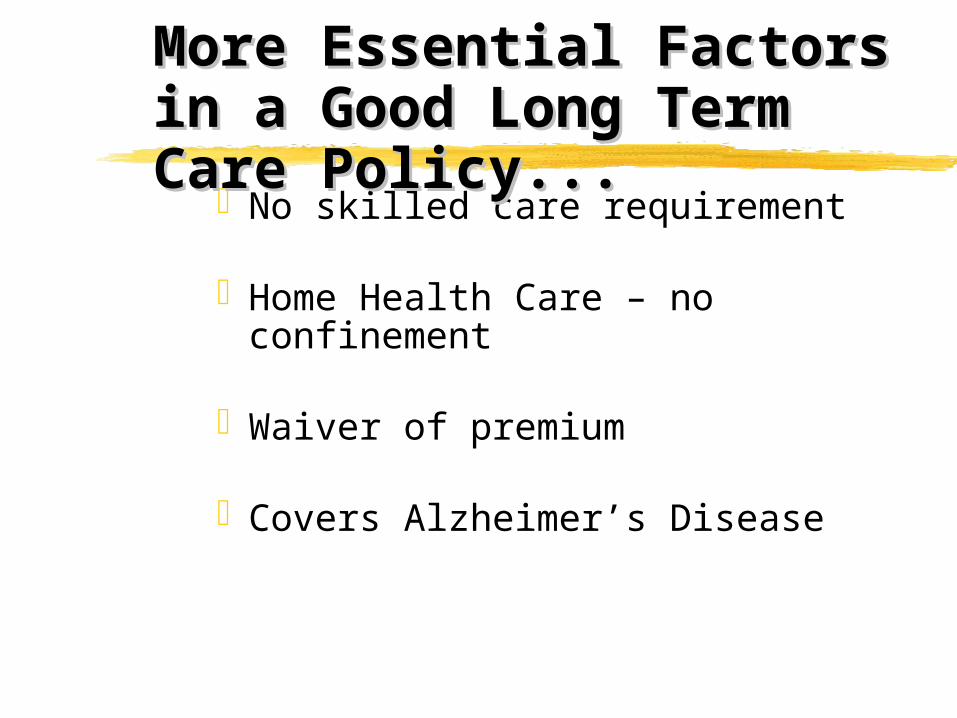

No skilled care requirement

Home Health Care – no confinement

Waiver of premium

Covers Alzheimer’s Disease

More Essential Factors in a More Essential Factors in a Good Long Term Care Policy...Good Long Term Care Policy...

The Top Six Reasons Why You Need LTC Insurance

IndependenceHelps protect your familyProvides you with choices Helps protect your retirement

savings and family assetsFavorable tax treatmentPeace of mind

Thank You!