Family Business Planning with Chapter 14 Implications€¦ · Family Business Planning with Chapter...

90

/ / 1 © 2016 N. Todd Angkatavanich. All Rights Reserved. London l Geneva l Zurich l Milan l Padua l New Haven l New York Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands Family Business Planning with Chapter 14 Implications RPTE Skills Training, July 2016 N. Todd Angkatavanich, Esq. Marissa Dungey, Esq. Withers Bergman LLP 4728130.1

Transcript of Family Business Planning with Chapter 14 Implications€¦ · Family Business Planning with Chapter...

/ / 1

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Family Business Planning with Chapter 14 Implications

RPTE Skills Training, July 2016

N. Todd Angkatavanich, Esq.Marissa Dungey, Esq.Withers Bergman LLP

4728130.1

/ / 2

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Overview of Chapter 14

Effective Oct 9, 1990 – replacing the repealed 2036(c) – criticized for being overly-vague, complex and unreasonable.

Special valuation rules set forth in Sections 2701, 2702, 2703 and 2704.

Attempts to prevent perceived transfer tax abuses in the context of business or other interests held within a family.

/ / 3

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Where Chapter 14 may come into your practice

• Preferred Partnerships/LLC

• Family Limited Partnerships

• Capital Contributions - Recapitalizations

• Buy-Sell and Shareholder Agreements

• Carried Interest Planning

• Profits Interests

• GRATs/ QPRTs / Sales of Remainder Interests

• Sales to Grantor Trusts

• Valuation Issues

• Joint Purchases

/ / 4

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Overview of Chapter 14

Underlying Assumption - Senior family members will structure ownership and transfer of family business (and other) interests so as to shift value to younger family members at a reduced transfer tax cost.

NOT ALWAYS THE CASE AT ALL!!!! But Presumptions built into provisions. PITFALLS FOR THE UNWITTING!!!

Important to Note – Very broad and can

unexpectedly apply!

/ / 5

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Overview of Chapter 14

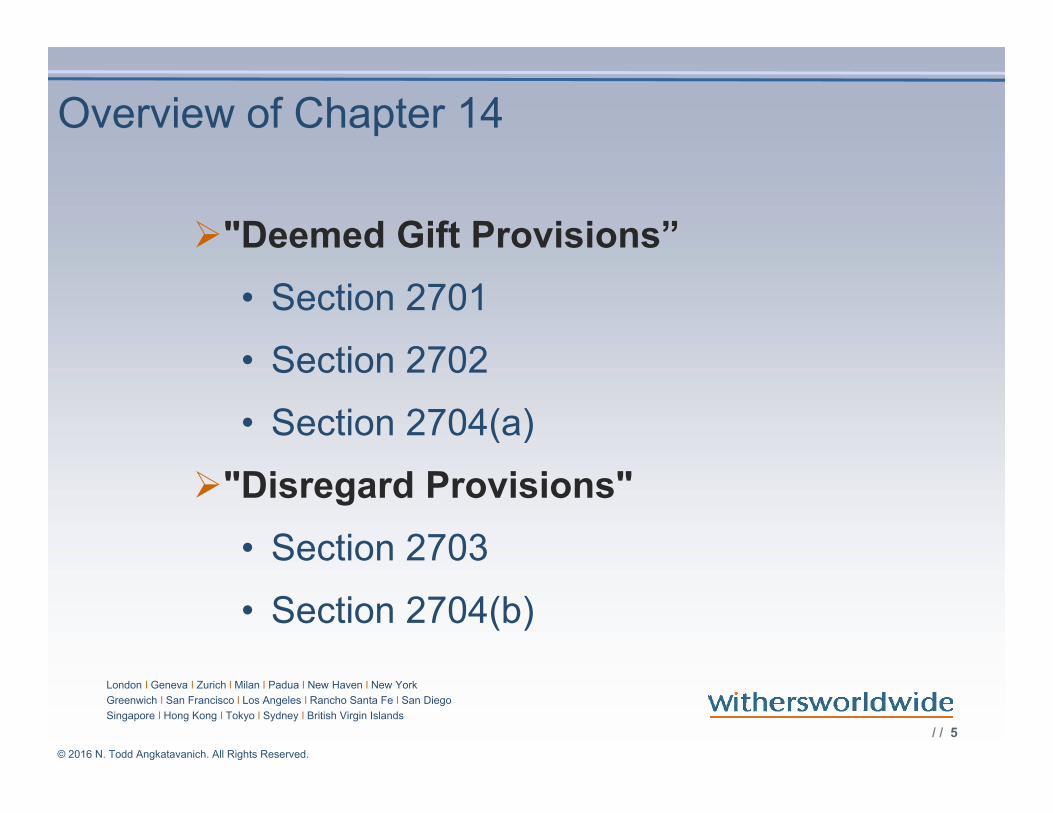

"Deemed Gift Provisions”

• Section 2701

• Section 2702

• Section 2704(a)

"Disregard Provisions"

• Section 2703

• Section 2704(b)

/ / 6

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

IRC SECTION 2701

/ / 7

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

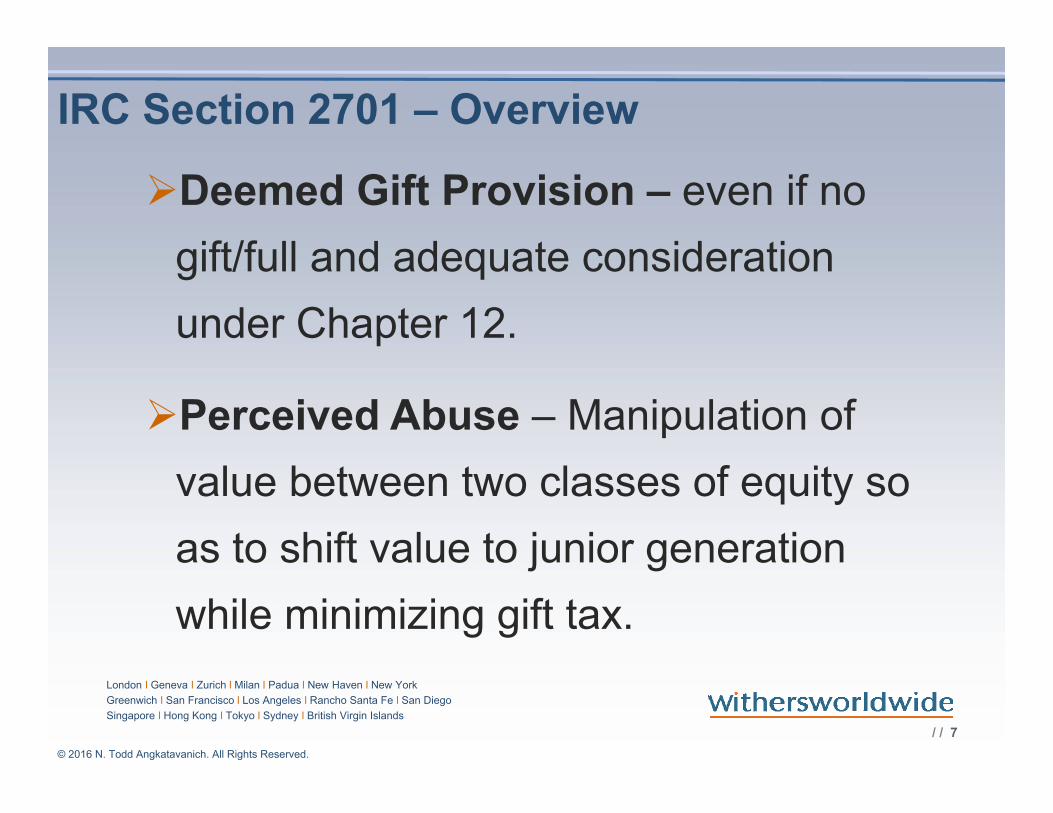

IRC Section 2701 – Overview

Deemed Gift Provision – even if no

gift/full and adequate consideration

under Chapter 12.

Perceived Abuse – Manipulation of

value between two classes of equity so

as to shift value to junior generation

while minimizing gift tax.

/ / 8

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Pitfalls and planning opportunities

• *Preferred entities

• *Profits interests

• *Capital contributions and recaps

• *Carried interest “vertical slice”

• Different classes of equity

• Pro-active planning:

• * Freeze partnerships to shift growth

• (GRATs, QTIPs, NON-Exempt Trusts)

/ / 9

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

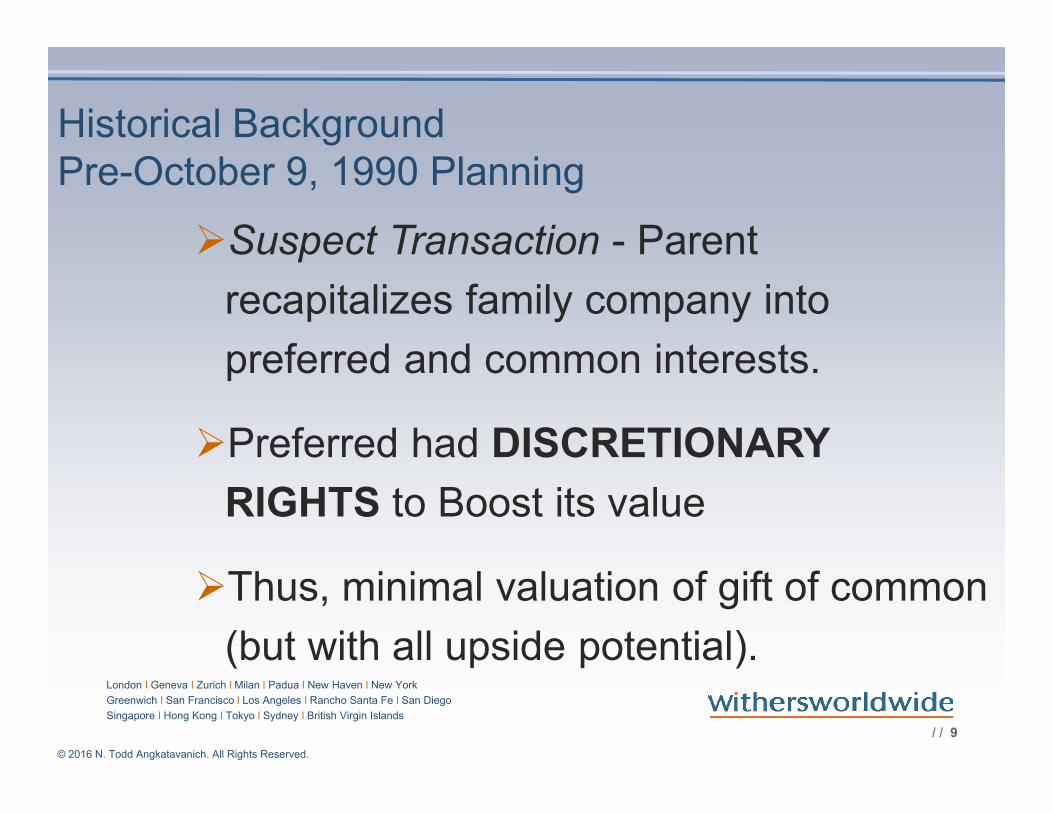

Historical BackgroundPre-October 9, 1990 Planning

Suspect Transaction - Parent

recapitalizes family company into

preferred and common interests.

Preferred had DISCRETIONARY

RIGHTS to Boost its value

Thus, minimal valuation of gift of common

(but with all upside potential).

/ / 10

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

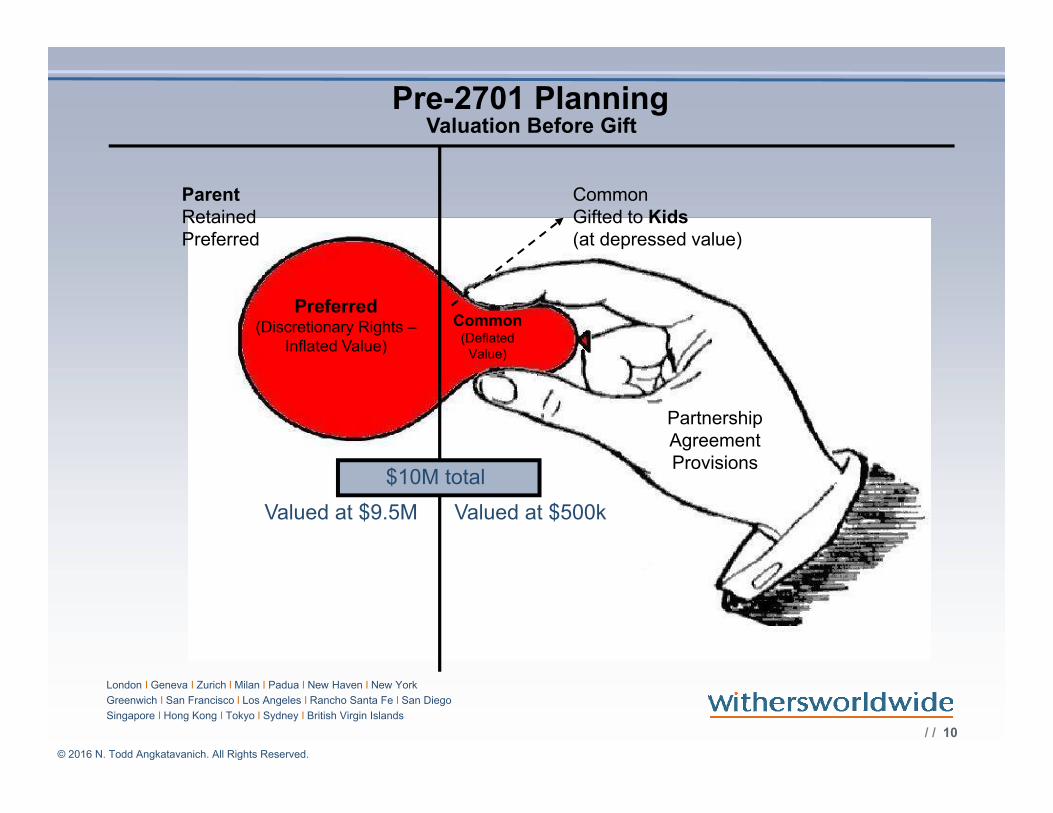

Pre-2701 Planning

Parent RetainedPreferred

Preferred (Discretionary Rights –

Inflated Value)

Common(Deflated

Value)

Common Gifted to Kids(at depressed value)

Partnership Agreement Provisions

Valuation Before Gift

Valued at $9.5M Valued at $500k

$10M total

/ / 11

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

CONGRESSIONAL RESPONSE – Concept of Applicable Retained Interest AND “Zero” Value Rule 2701 causes certain rights associated with Senior equity interests

(“Applicable Retained Interests”) retained by Senior Member to be valued at ZERO Rationale - If Discretionary Rights unlikely to be exercised by G-1,

why give “credit”? Section 2701 creates a Fiction

Resulting increase in value of the transferred interest to Junior Member

Subtraction method

/ / 12

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

“Transfers” -- Broader than you think

• Traditional Gift “Transfers”

• Capital Contributions

• Recapitalization

• Change in Capital Structure

/ / 13

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Terminology: “Junior” and “Senior” –• Family Members:

“Applicable Family Member” “Senior” Member and Spouse (T’s Spouse, Ancestor of T or T’s Spouse, and Spouse

of Ancestor)

“Member of the Family” “Junior” Member and Spouse (T’s Spouse, Lineal Descendants of T or Spouse, any

spouse of a Lineal Descendants )

• Equity Interests in a Controlled Entity “Senior” interest generally “Preferred” “Junior” interest generally “Common”

/ / 14

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

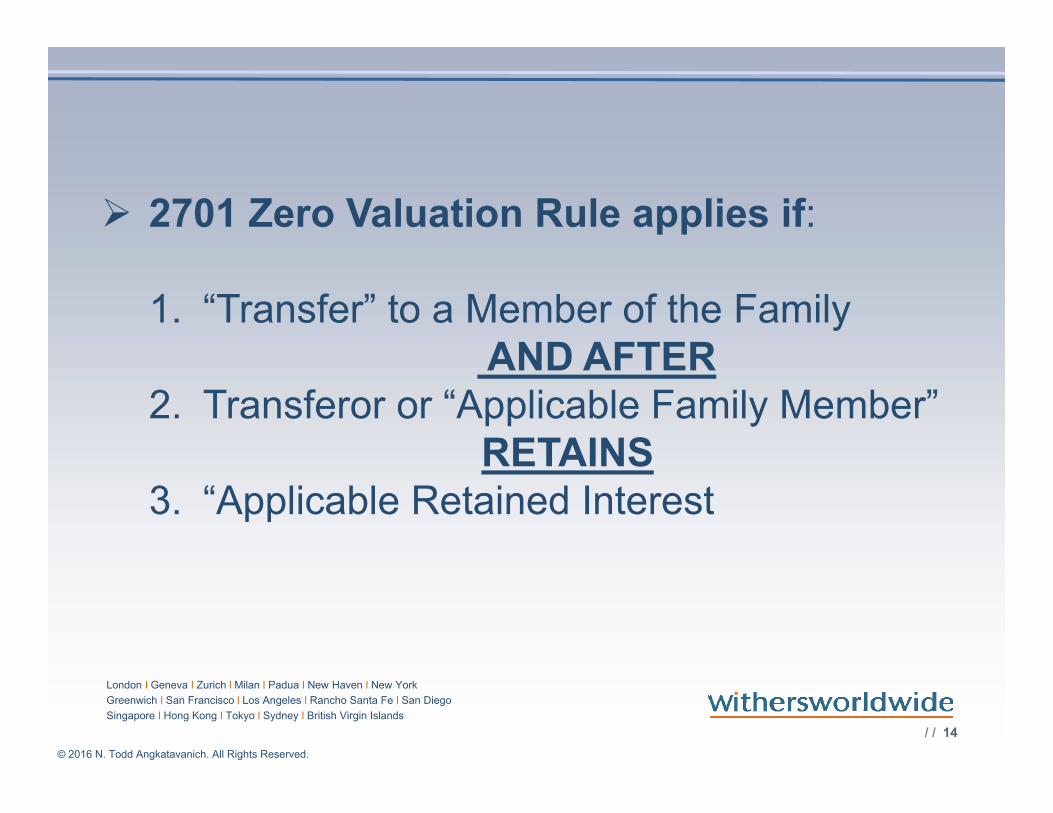

2701 Zero Valuation Rule applies if:

1. “Transfer” to a Member of the Family AND AFTER

2. Transferor or “Applicable Family Member”RETAINS

3. “Applicable Retained Interest

/ / 15

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

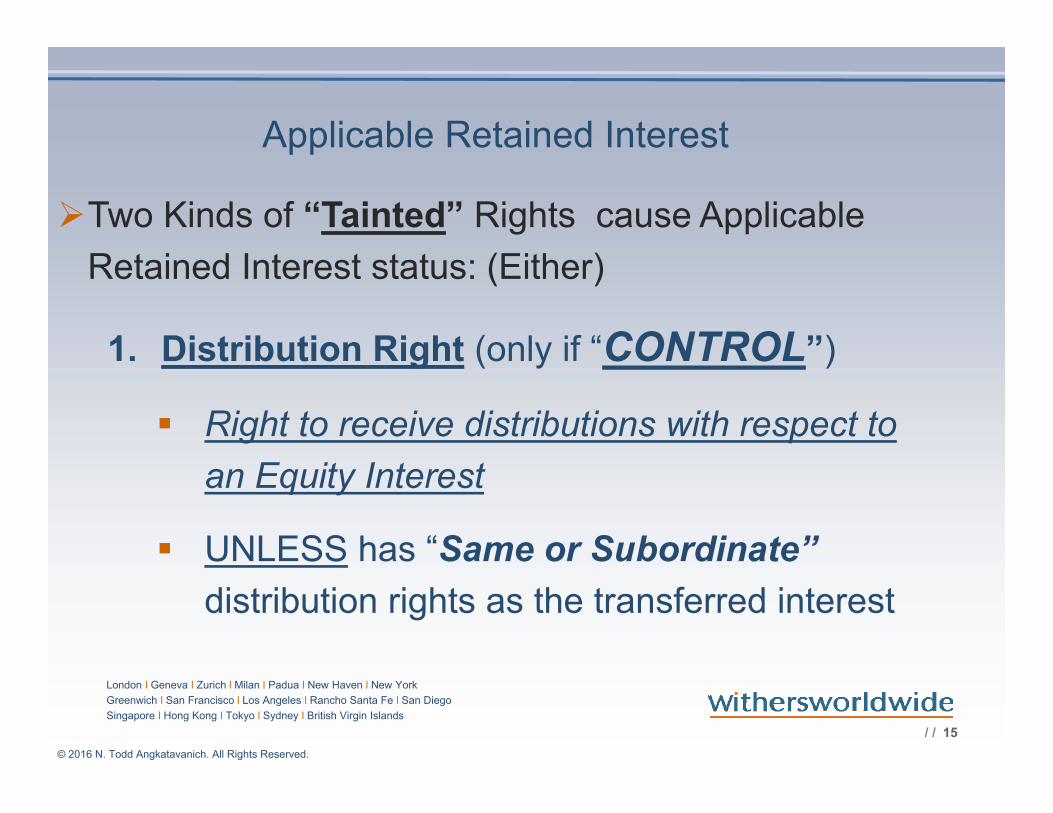

Applicable Retained Interest

Two Kinds of “Tainted” Rights cause Applicable

Retained Interest status: (Either)

1. Distribution Right (only if “CONTROL”)

Right to receive distributions with respect to

an Equity Interest

UNLESS has “Same or Subordinate”

distribution rights as the transferred interest

/ / 16

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

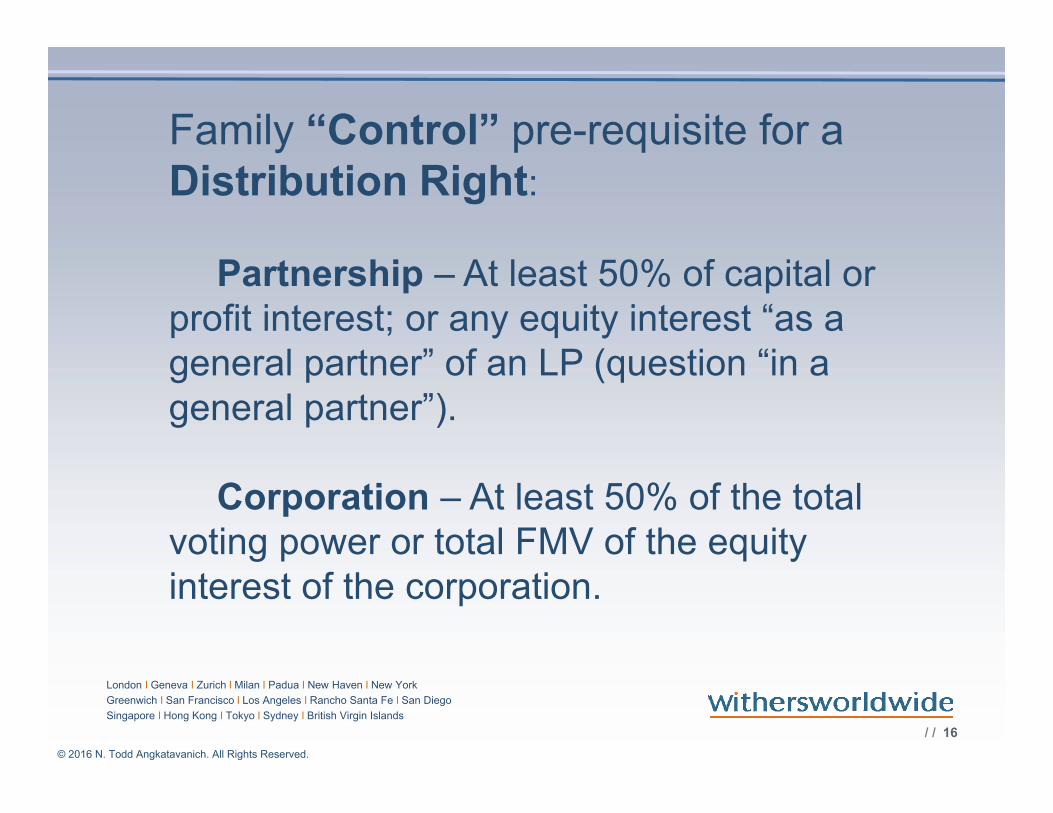

Family “Control” pre-requisite for a Distribution Right:

Partnership – At least 50% of capital or profit interest; or any equity interest “as a general partner” of an LP (question “in a general partner”).

Corporation – At least 50% of the total voting power or total FMV of the equity interest of the corporation.

/ / 17

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

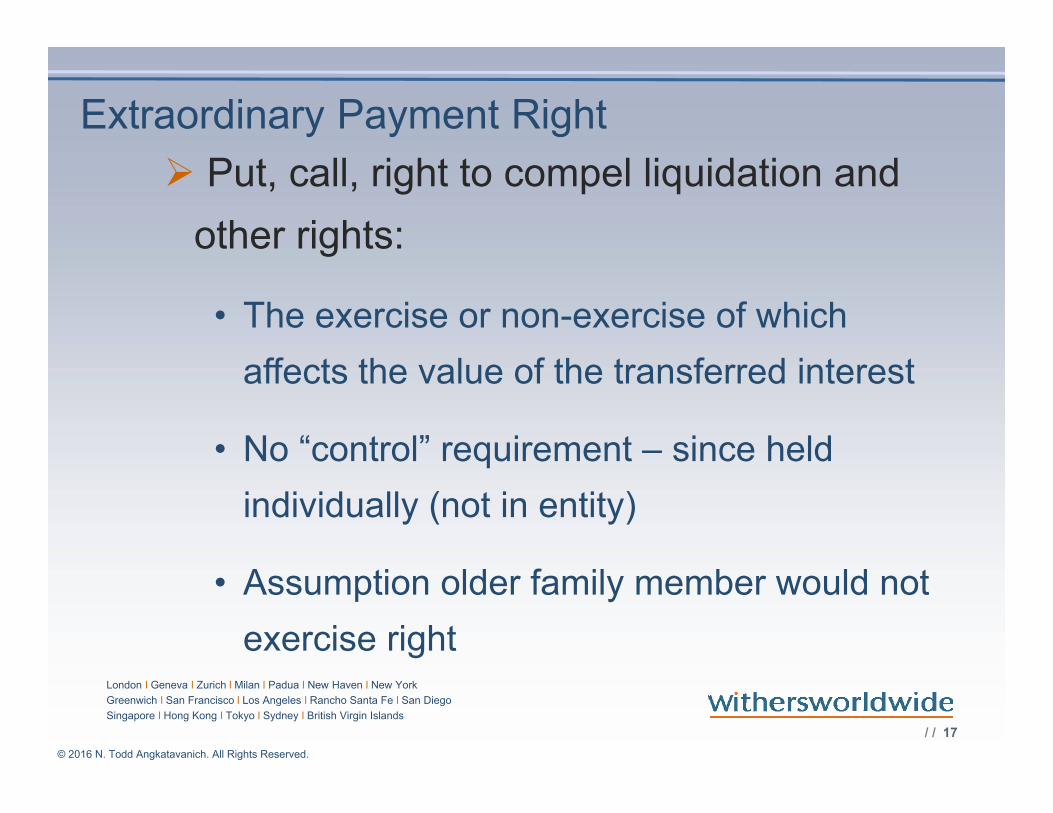

Extraordinary Payment Right

Put, call, right to compel liquidation and

other rights:

• The exercise or non-exercise of which

affects the value of the transferred interest

• No “control” requirement – since held

individually (not in entity)

• Assumption older family member would not

exercise right

/ / 18

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

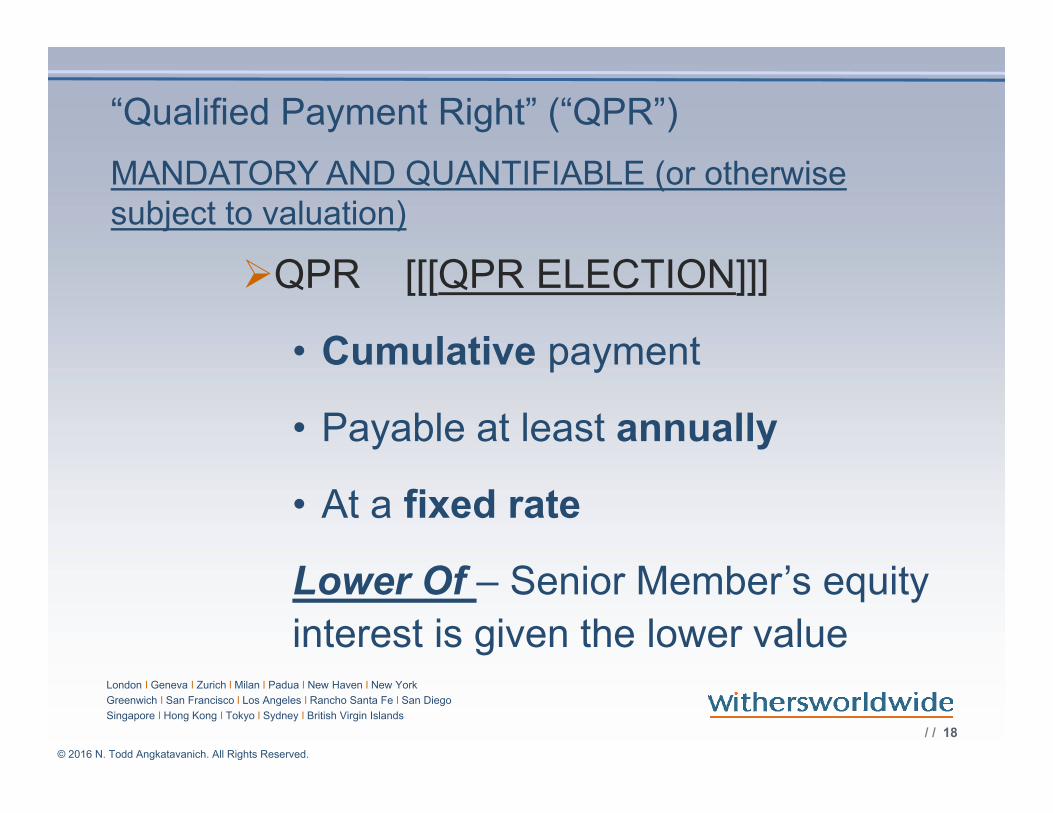

“Qualified Payment Right” (“QPR”)

MANDATORY AND QUANTIFIABLE (or otherwise subject to valuation)

QPR [[[QPR ELECTION]]]

• Cumulative payment

• Payable at least annually

• At a fixed rate

Lower Of – Senior Member’s equity

interest is given the lower value

/ / 19

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

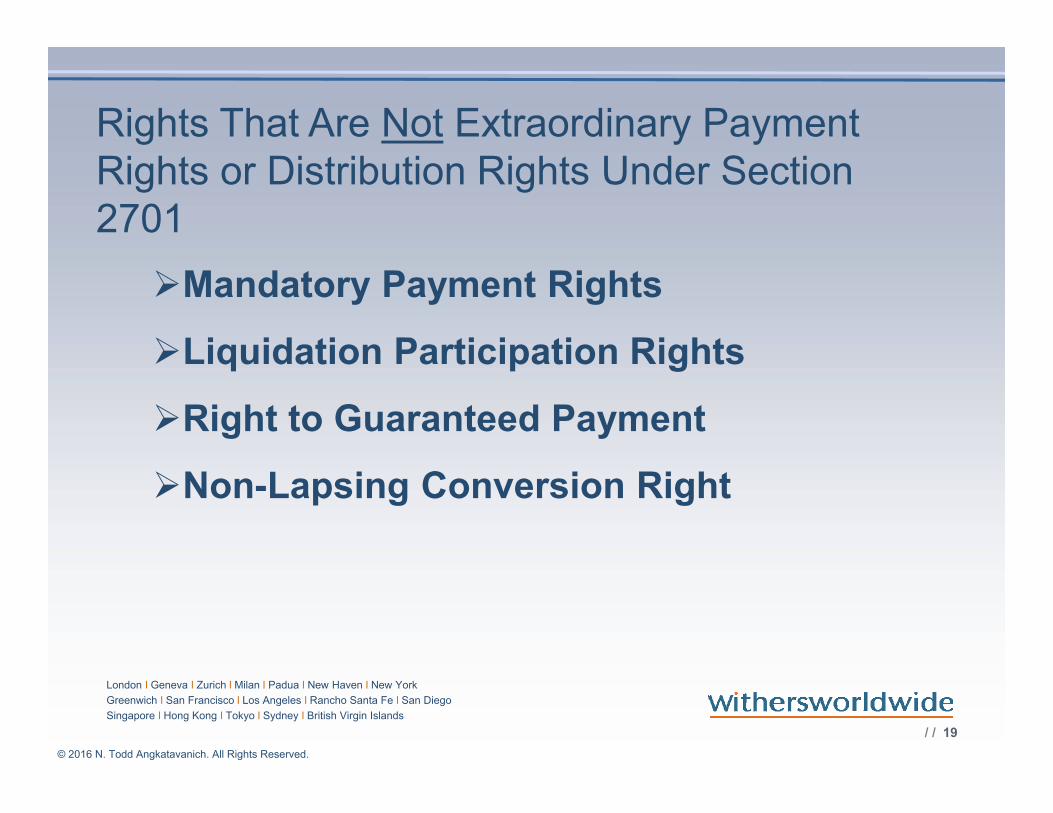

Rights That Are Not Extraordinary Payment Rights or Distribution Rights Under Section 2701

Mandatory Payment Rights

Liquidation Participation Rights

Right to Guaranteed Payment

Non-Lapsing Conversion Right

/ / 20

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

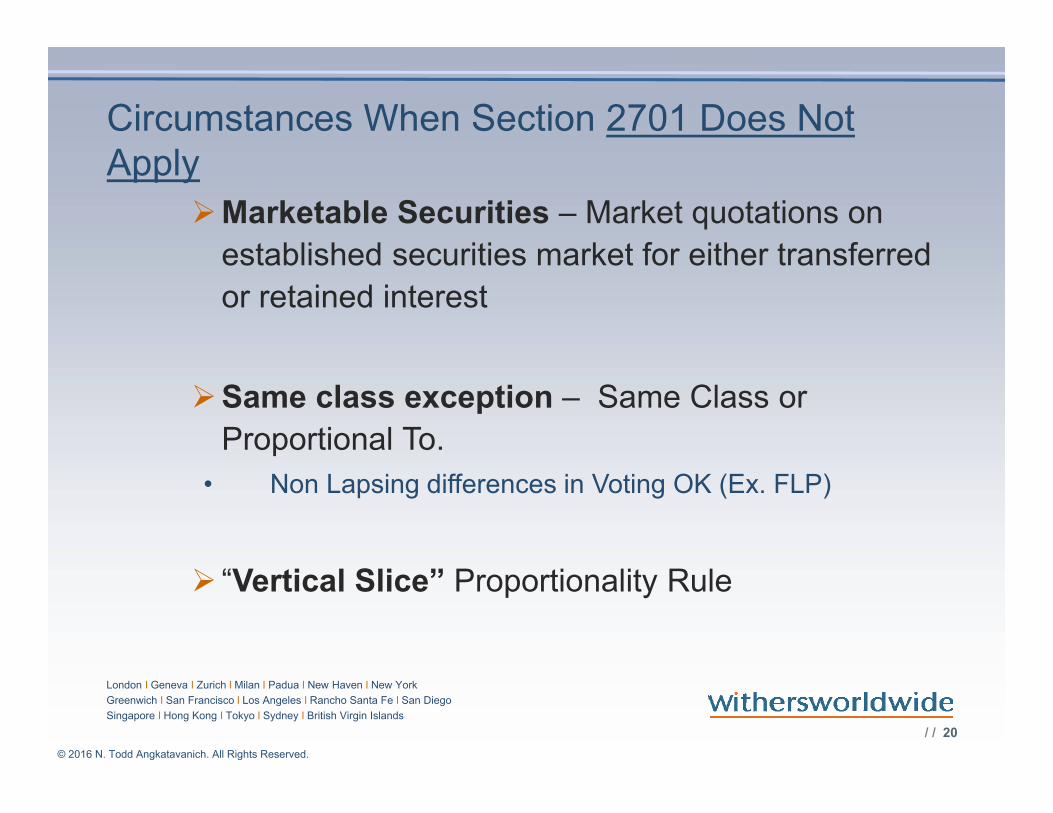

Circumstances When Section 2701 Does Not Apply

Marketable Securities – Market quotations on

established securities market for either transferred

or retained interest

Same class exception – Same Class or

Proportional To.

• Non Lapsing differences in Voting OK (Ex. FLP)

“Vertical Slice” Proportionality Rule

/ / 21

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

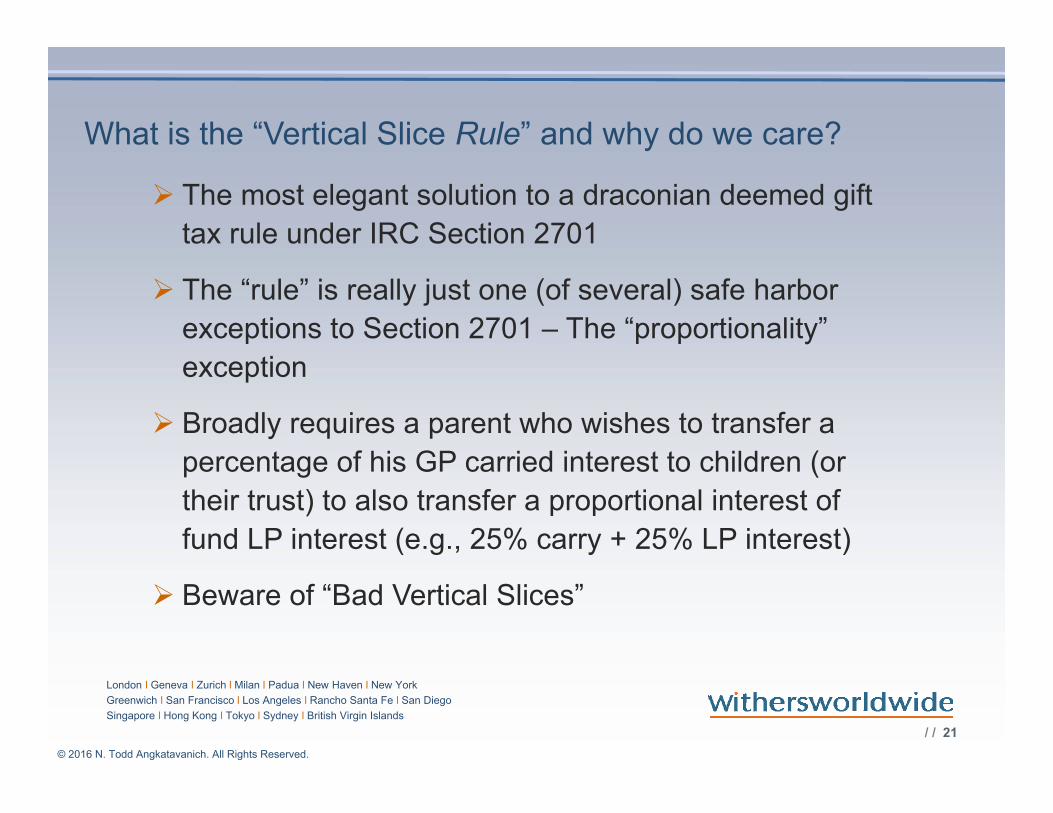

What is the “Vertical Slice Rule” and why do we care?

The most elegant solution to a draconian deemed gift

tax rule under IRC Section 2701

The “rule” is really just one (of several) safe harbor

exceptions to Section 2701 – The “proportionality”

exception

Broadly requires a parent who wishes to transfer a

percentage of his GP carried interest to children (or

their trust) to also transfer a proportional interest of

fund LP interest (e.g., 25% carry + 25% LP interest)

Beware of “Bad Vertical Slices”

/ / 22

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Chief Counsel Advice 201442053 -Recapitalization

Mom contributed real estate to single class LLC and gifted interests to two sons and GCs; LLC had 20-year term.

LLC Recapitalized - sons allocated all profits and losses; ownership interests held by Mom and GCs were only capital interests with right to distributions based on capital account balances at recapitalization.

/ / 23

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

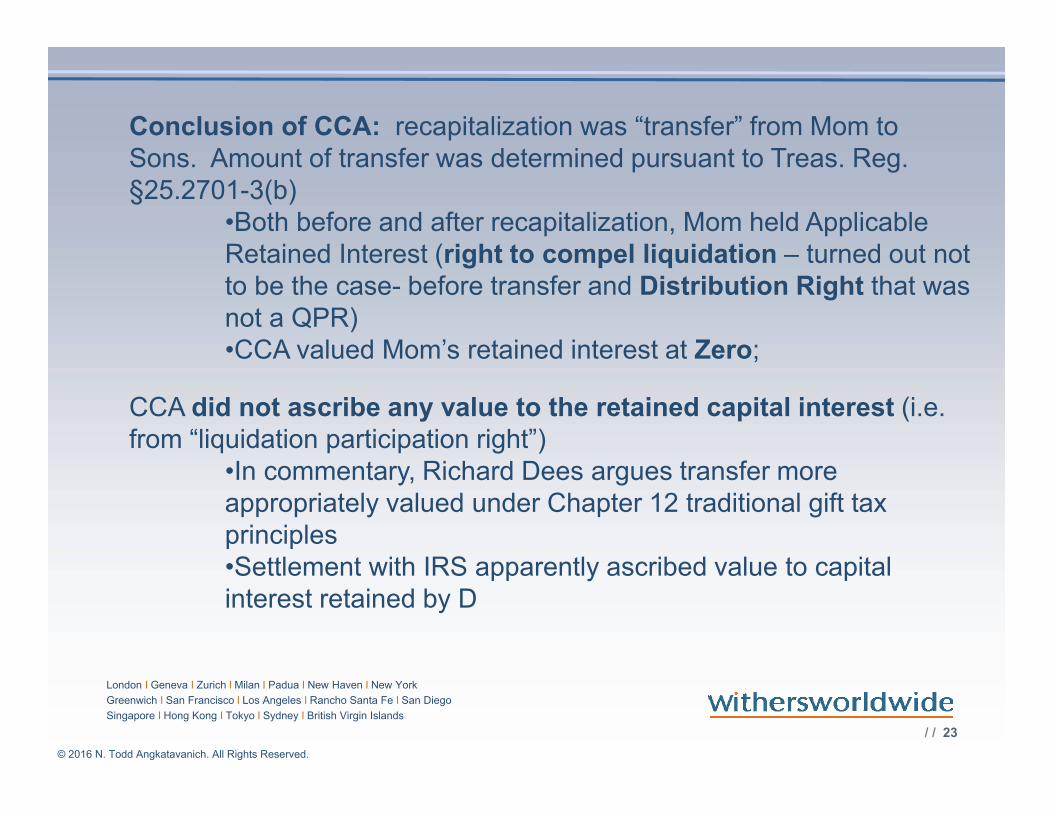

Conclusion of CCA: recapitalization was “transfer” from Mom to Sons. Amount of transfer was determined pursuant to Treas. Reg. §25.2701-3(b)

•Both before and after recapitalization, Mom held Applicable Retained Interest (right to compel liquidation – turned out not to be the case- before transfer and Distribution Right that was not a QPR)•CCA valued Mom’s retained interest at Zero;

CCA did not ascribe any value to the retained capital interest (i.e. from “liquidation participation right”)

•In commentary, Richard Dees argues transfer more appropriately valued under Chapter 12 traditional gift tax principles•Settlement with IRS apparently ascribed value to capital interest retained by D

/ / 24

© 2016 N. Todd Angkatavanich. All Rights Reserved.

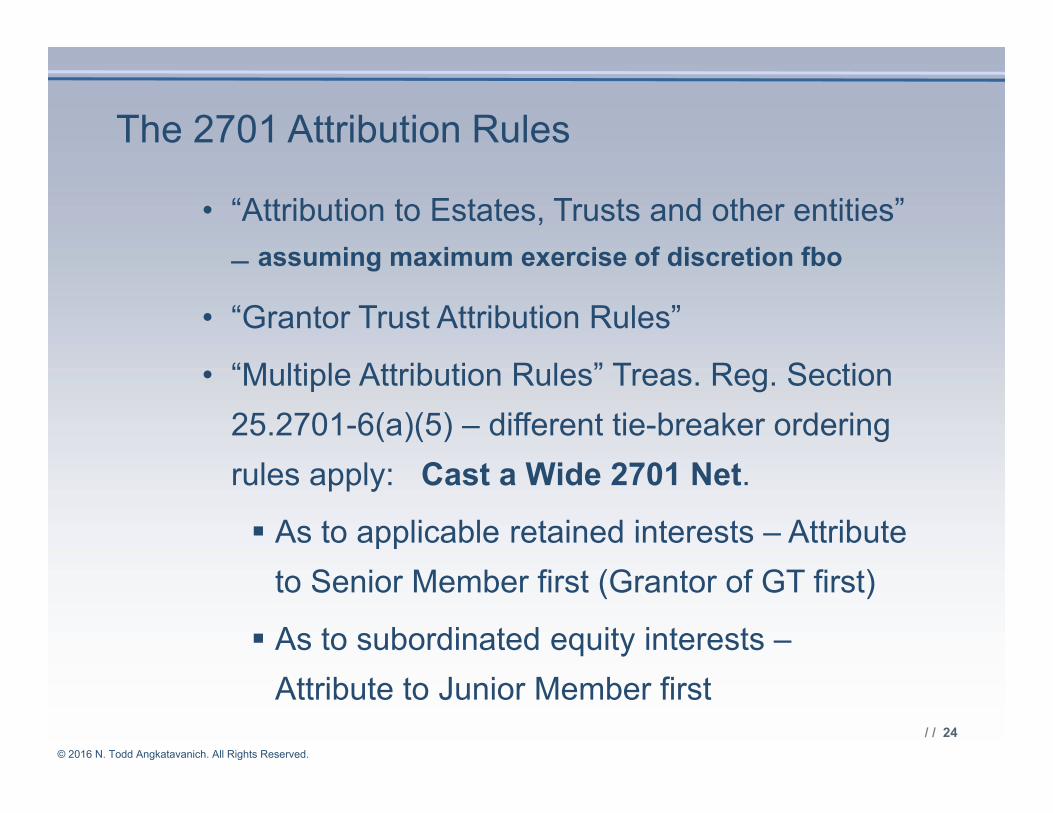

The 2701 Attribution Rules

• “Attribution to Estates, Trusts and other entities”

– assuming maximum exercise of discretion fbo

• “Grantor Trust Attribution Rules”

• “Multiple Attribution Rules” Treas. Reg. Section

25.2701-6(a)(5) – different tie-breaker ordering

rules apply: Cast a Wide 2701 Net.

As to applicable retained interests – Attribute

to Senior Member first (Grantor of GT first)

As to subordinated equity interests –

Attribute to Junior Member first

/ / 25

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

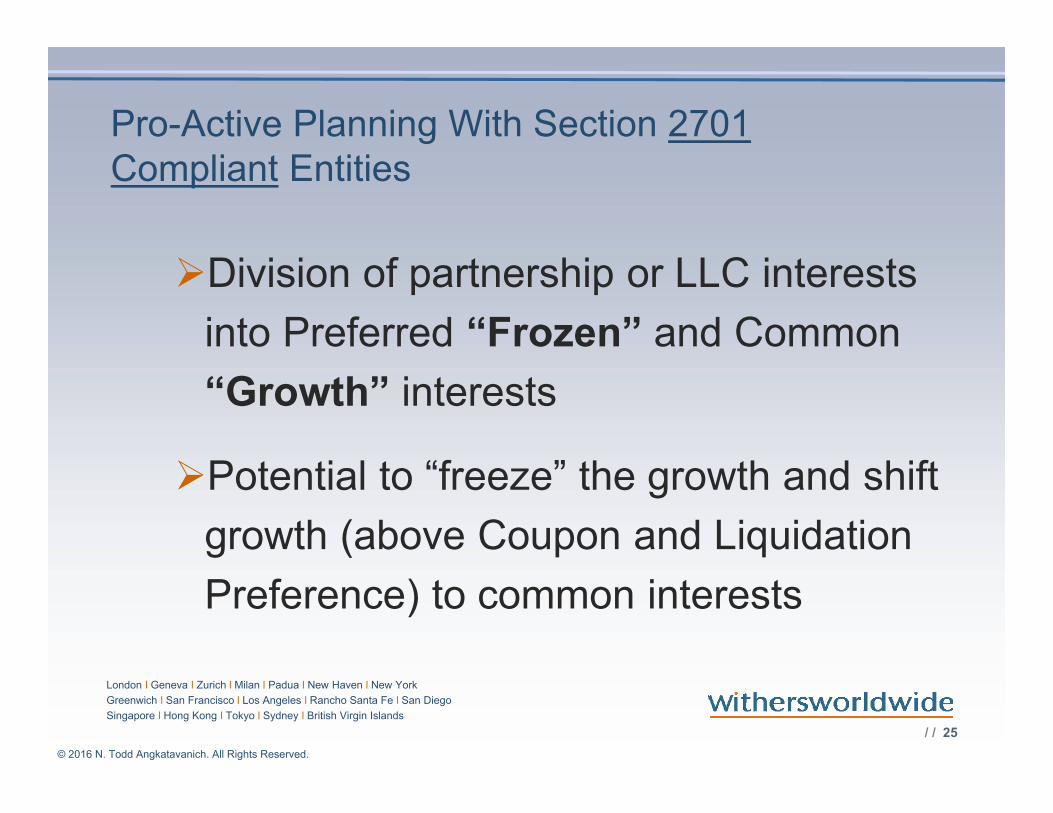

Pro-Active Planning With Section 2701 Compliant Entities

Division of partnership or LLC interests

into Preferred “Frozen” and Common

“Growth” interests

Potential to “freeze” the growth and shift

growth (above Coupon and Liquidation

Preference) to common interests

/ / 26

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Pro-active planning

* Shifting growth –“pop” in valueQTIP

GRAT

GST Non-Exempt

/ / 27

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

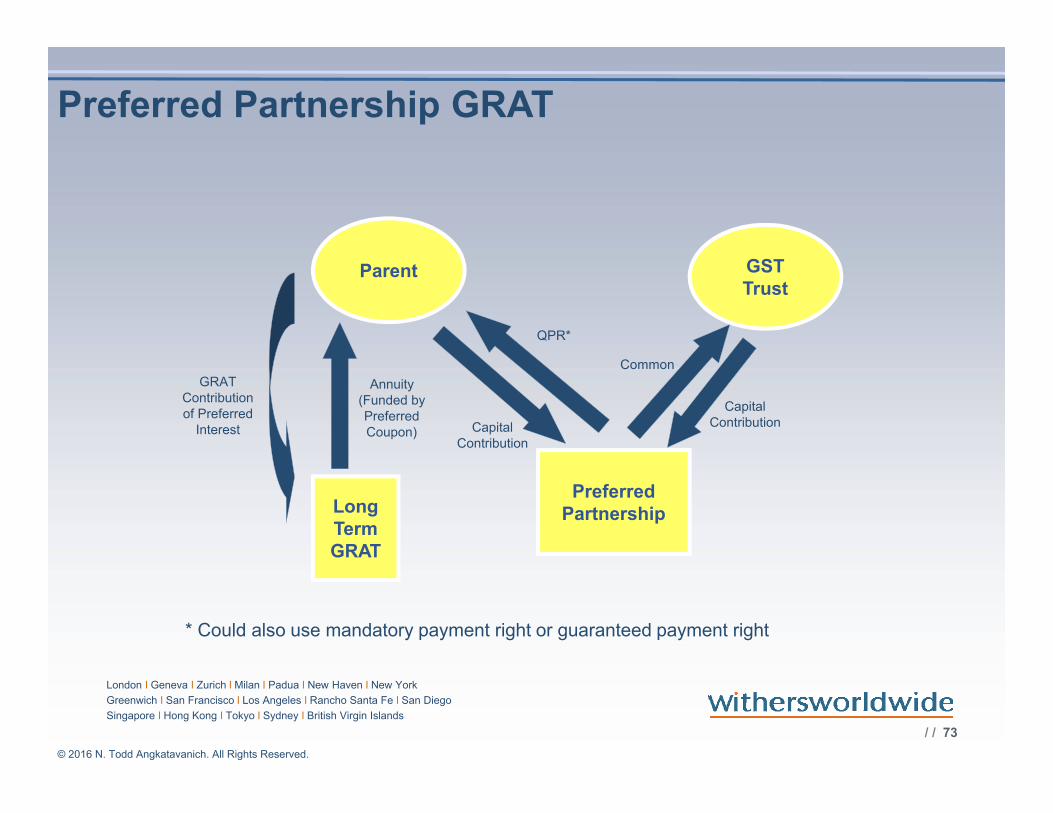

Preferred Partnership GRAT

GST Trust

Parent

Preferred Partnership

GRAT Contribution of Preferred

Interest

QPR*

Long Term GRAT

Annuity (Funded by Preferred Coupon)

Common

Capital ContributionCapital

Contribution

* Could also use mandatory payment right or guaranteed payment right

/ / 28

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

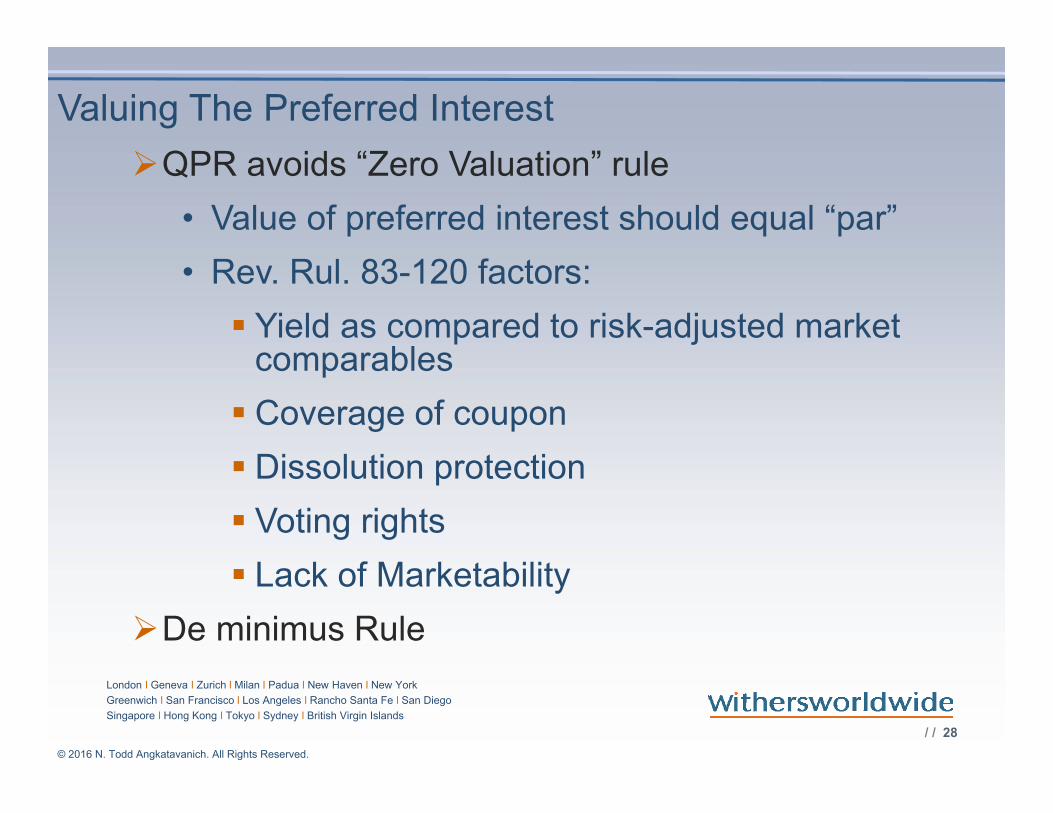

Valuing The Preferred Interest

QPR avoids “Zero Valuation” rule

• Value of preferred interest should equal “par”

• Rev. Rul. 83-120 factors:

Yield as compared to risk-adjusted market comparables

Coverage of coupon

Dissolution protection

Voting rights

Lack of Marketability

De minimus Rule

/ / 29

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

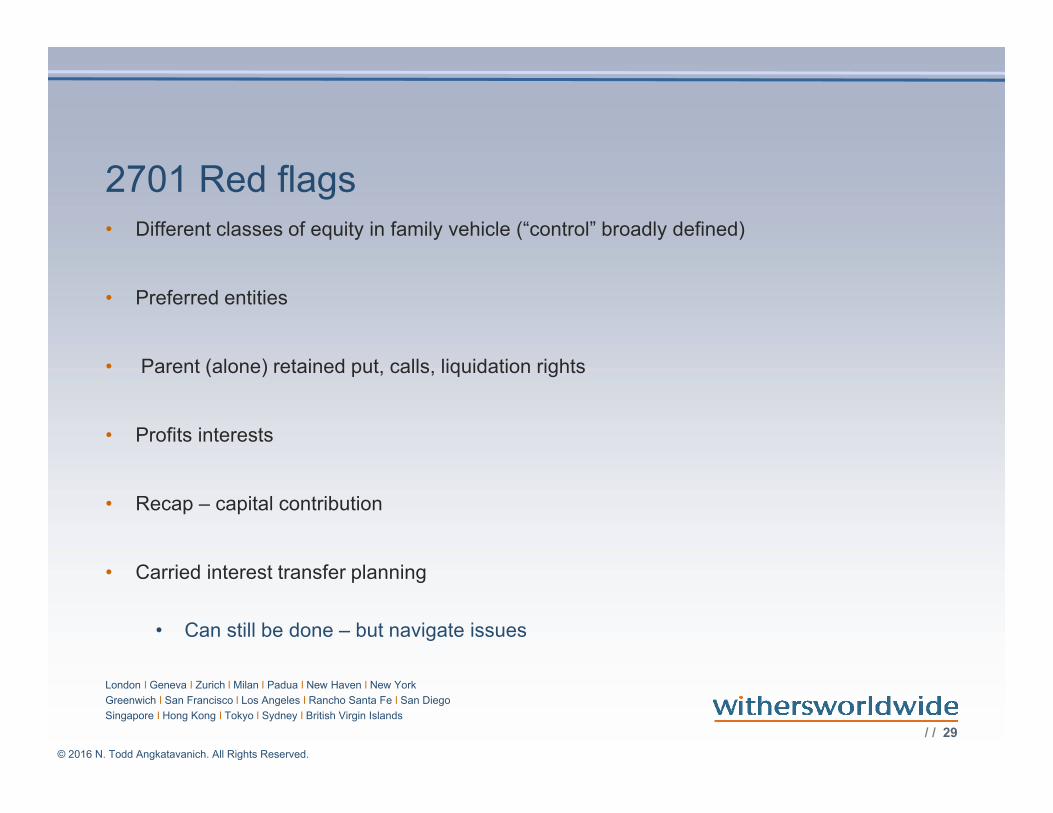

2701 Red flags• Different classes of equity in family vehicle (“control” broadly defined)

• Preferred entities

• Parent (alone) retained put, calls, liquidation rights

• Profits interests

• Recap – capital contribution

• Carried interest transfer planning

• Can still be done – but navigate issues

/ / 30

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

IRC SECTION 2704 (a) & (b)

/ / 31

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

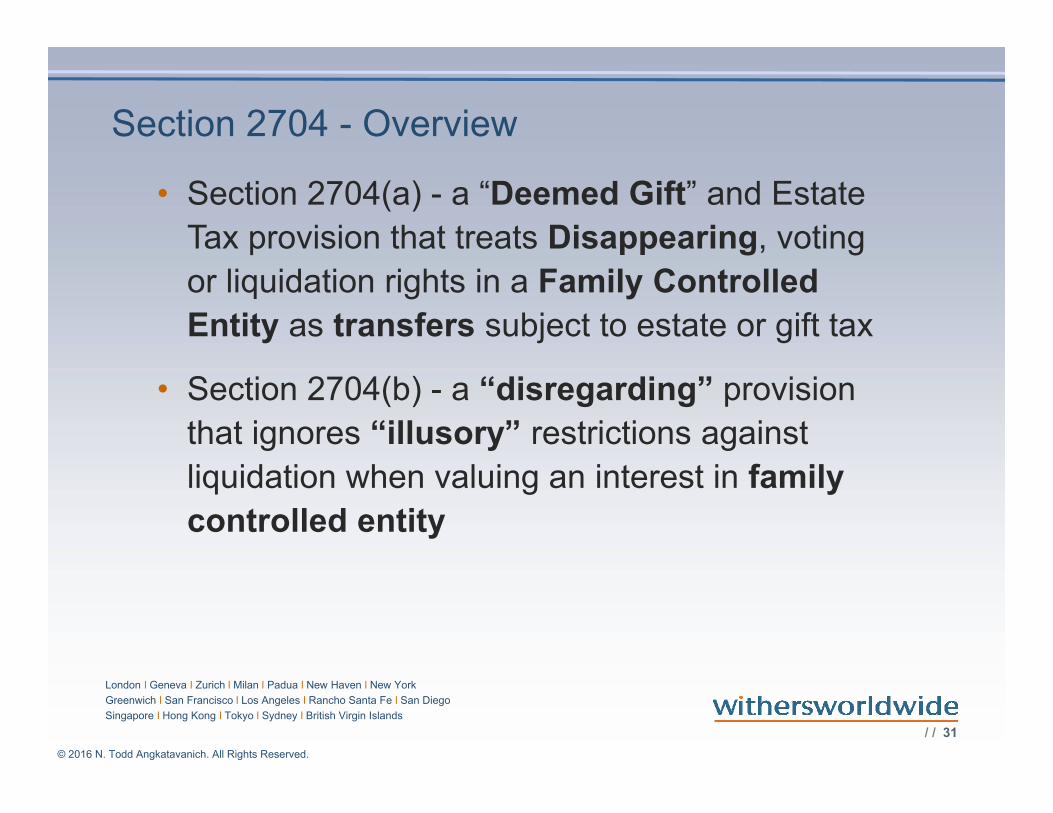

Section 2704 - Overview

• Section 2704(a) - a “Deemed Gift” and Estate

Tax provision that treats Disappearing, voting

or liquidation rights in a Family Controlled

Entity as transfers subject to estate or gift tax

• Section 2704(b) - a “disregarding” provision

that ignores “illusory” restrictions against

liquidation when valuing an interest in family

controlled entity

/ / 32

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

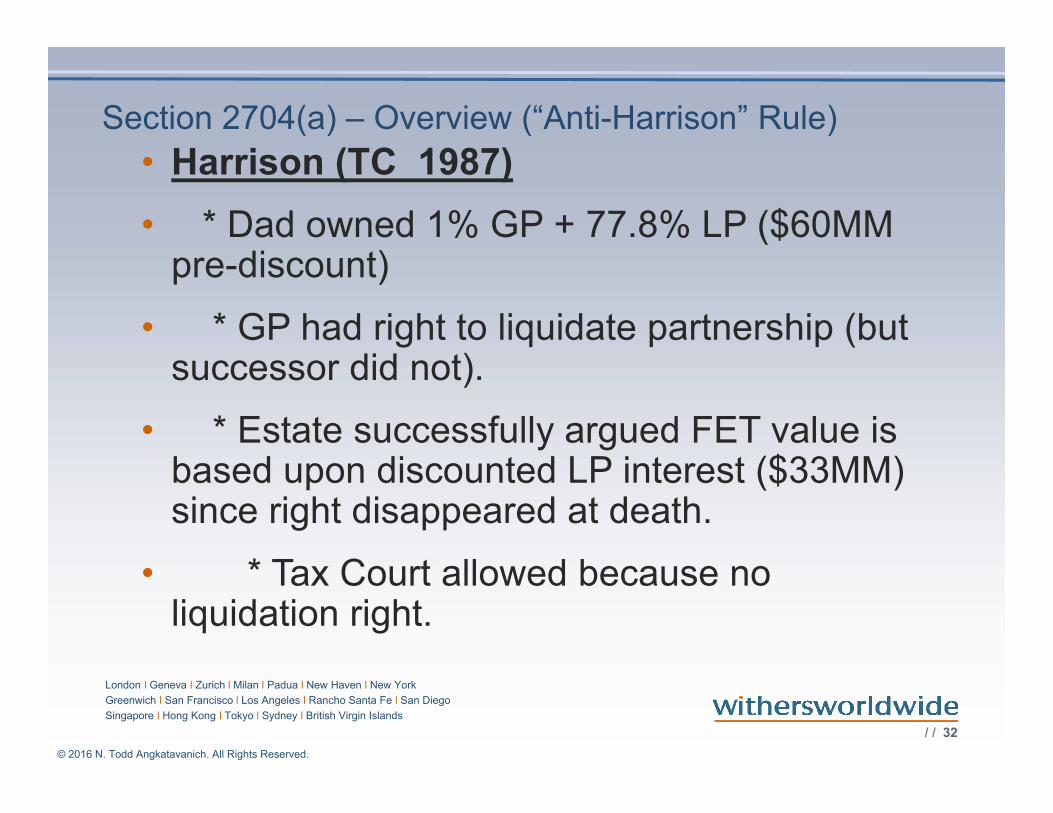

Section 2704(a) – Overview (“Anti-Harrison” Rule)

• Harrison (TC 1987)

• * Dad owned 1% GP + 77.8% LP ($60MM pre-discount)

• * GP had right to liquidate partnership (but successor did not).

• * Estate successfully argued FET value is based upon discounted LP interest ($33MM) since right disappeared at death.

• * Tax Court allowed because no liquidation right.

/ / 33

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

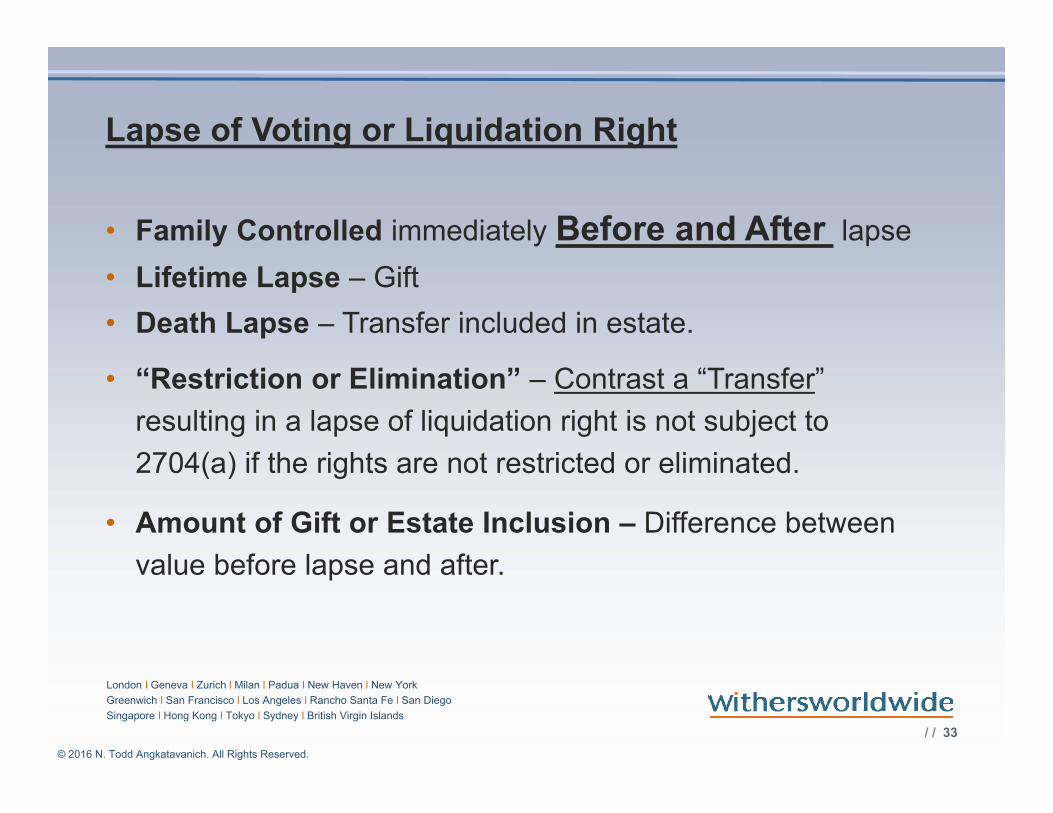

Lapse of Voting or Liquidation Right

• Family Controlled immediately Before and After lapse

• Lifetime Lapse – Gift

• Death Lapse – Transfer included in estate.

• “Restriction or Elimination” – Contrast a “Transfer”

resulting in a lapse of liquidation right is not subject to

2704(a) if the rights are not restricted or eliminated.

• Amount of Gift or Estate Inclusion – Difference between

value before lapse and after.

/ / 34

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

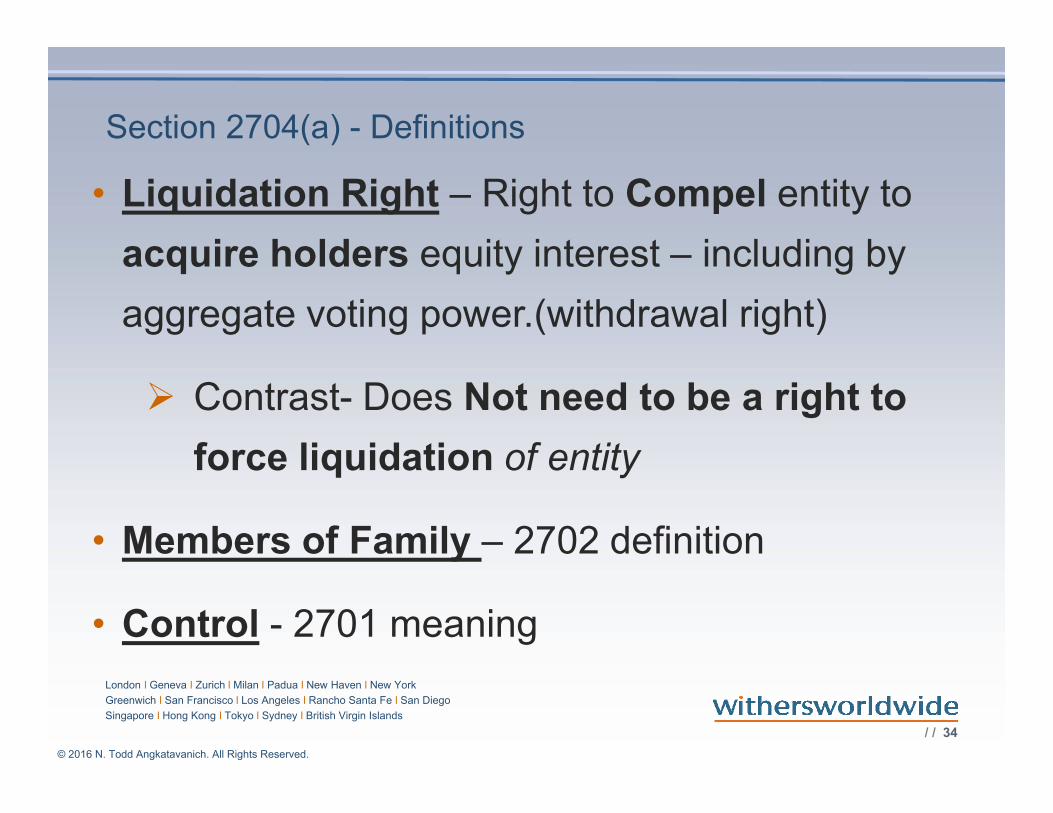

Section 2704(a) - Definitions

• Liquidation Right – Right to Compel entity to

acquire holders equity interest – including by

aggregate voting power.(withdrawal right)

Contrast- Does Not need to be a right to

force liquidation of entity

• Members of Family – 2702 definition

• Control - 2701 meaning

/ / 35

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

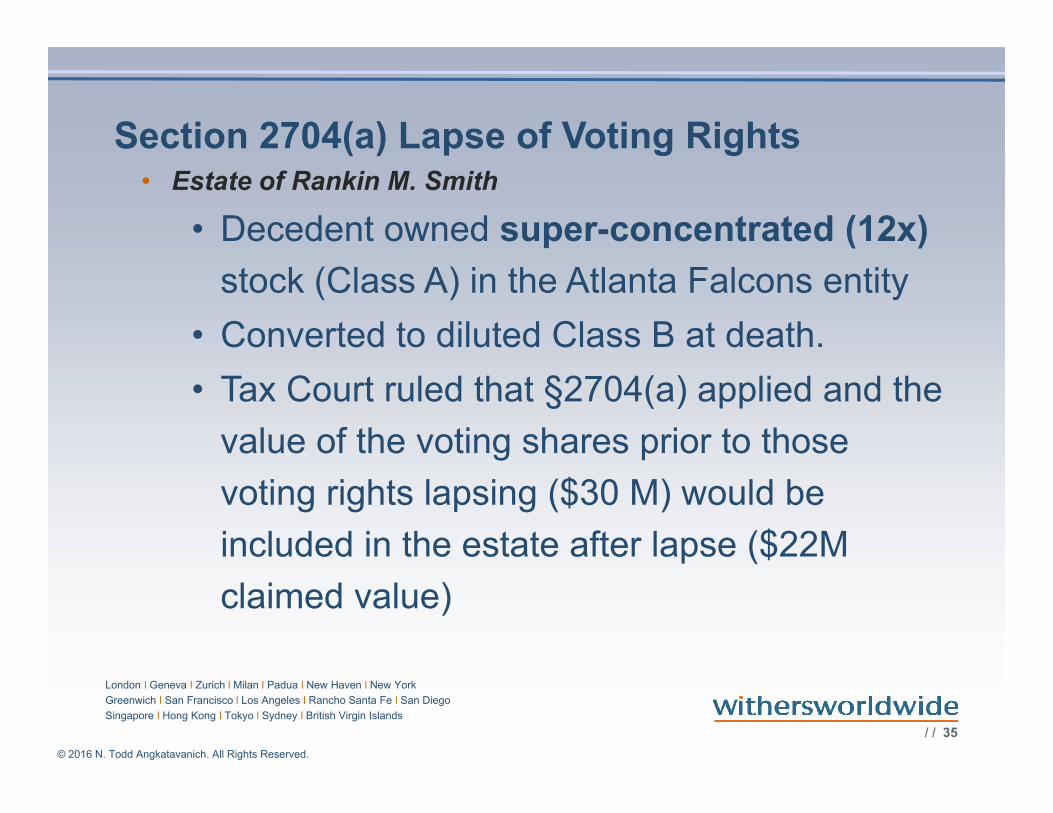

Section 2704(a) Lapse of Voting Rights• Estate of Rankin M. Smith

• Decedent owned super-concentrated (12x)

stock (Class A) in the Atlanta Falcons entity

• Converted to diluted Class B at death.

• Tax Court ruled that §2704(a) applied and the

value of the voting shares prior to those

voting rights lapsing ($30 M) would be

included in the estate after lapse ($22M

claimed value)

/ / 36

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

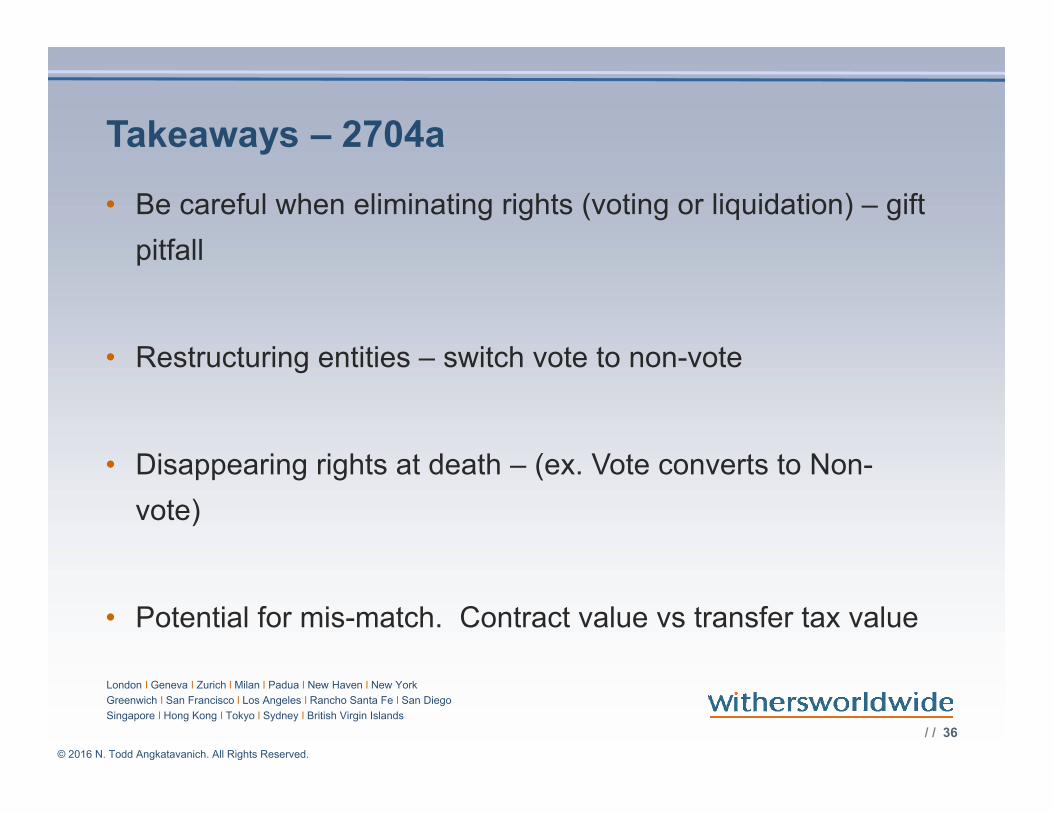

Takeaways – 2704a

• Be careful when eliminating rights (voting or liquidation) – gift

pitfall

• Restructuring entities – switch vote to non-vote

• Disappearing rights at death – (ex. Vote converts to Non-

vote)

• Potential for mis-match. Contract value vs transfer tax value

/ / 37

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

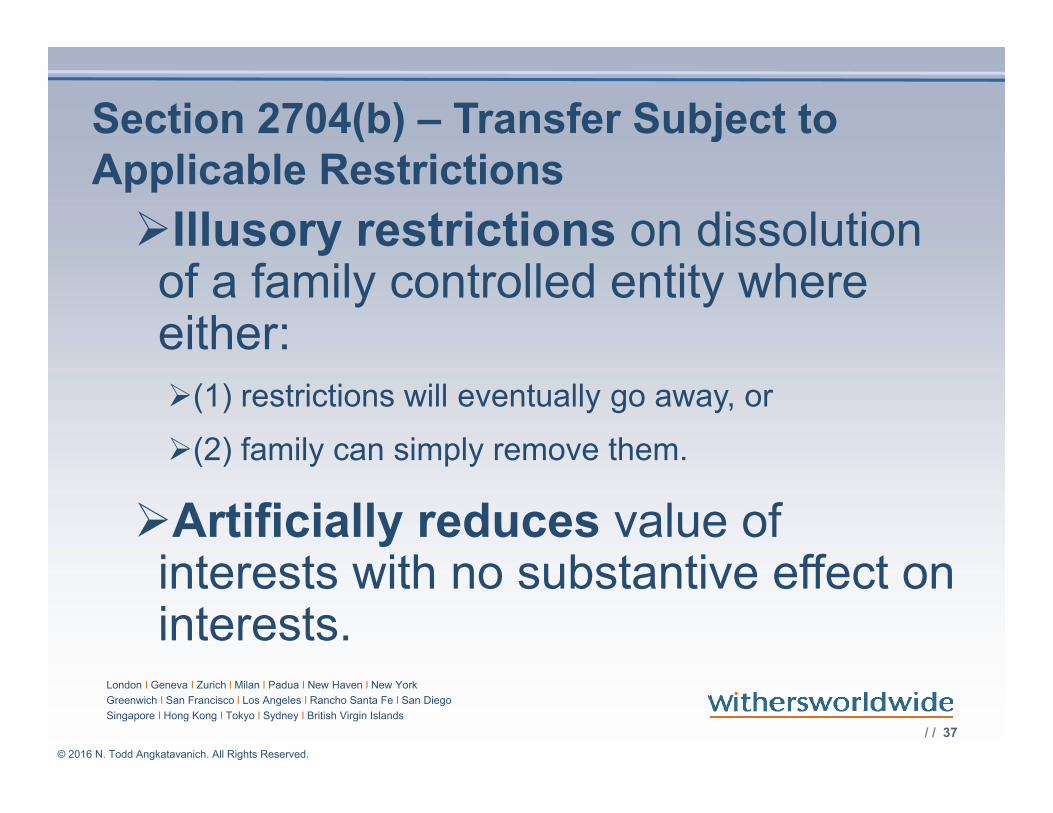

Section 2704(b) – Transfer Subject to Applicable Restrictions

Illusory restrictions on dissolution of a family controlled entity where either: (1) restrictions will eventually go away, or

(2) family can simply remove them.

Artificially reduces value of interests with no substantive effect on interests.

/ / 38

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

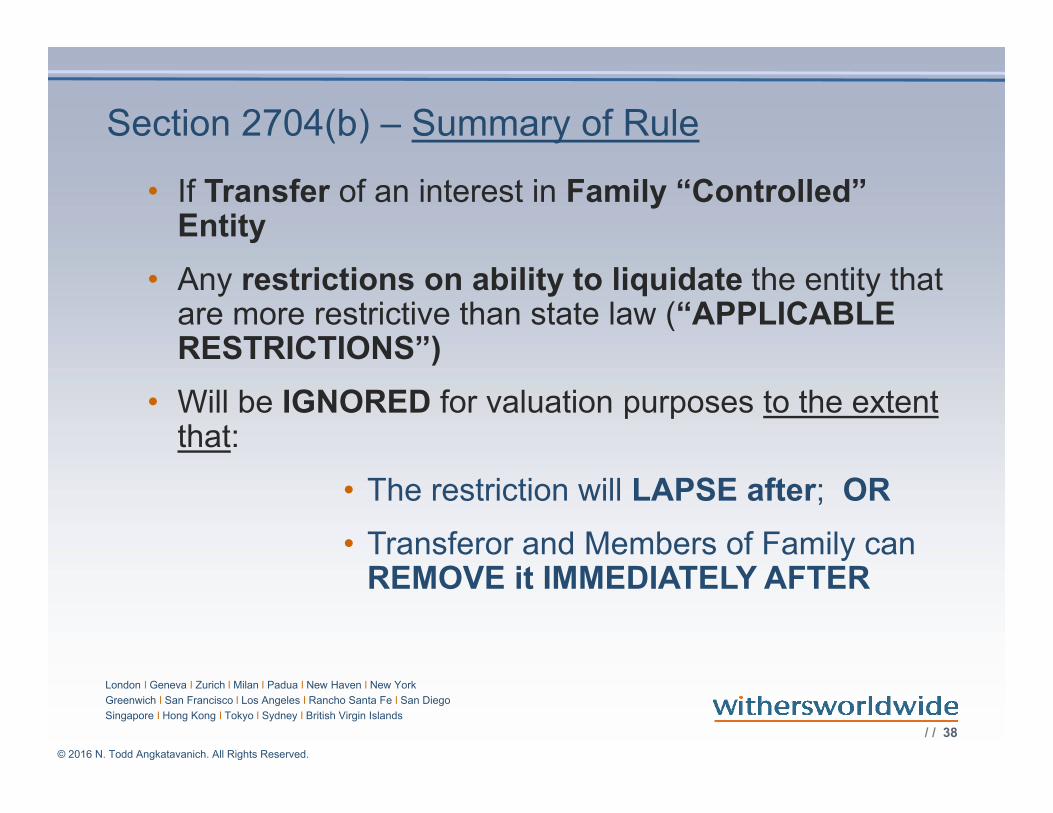

Section 2704(b) – Summary of Rule

• If Transfer of an interest in Family “Controlled” Entity

• Any restrictions on ability to liquidate the entity that are more restrictive than state law (“APPLICABLE RESTRICTIONS”)

• Will be IGNORED for valuation purposes to the extent that:

• The restriction will LAPSE after; OR

• Transferor and Members of Family can REMOVE it IMMEDIATELY AFTER

/ / 39

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Elements of 2704(b)

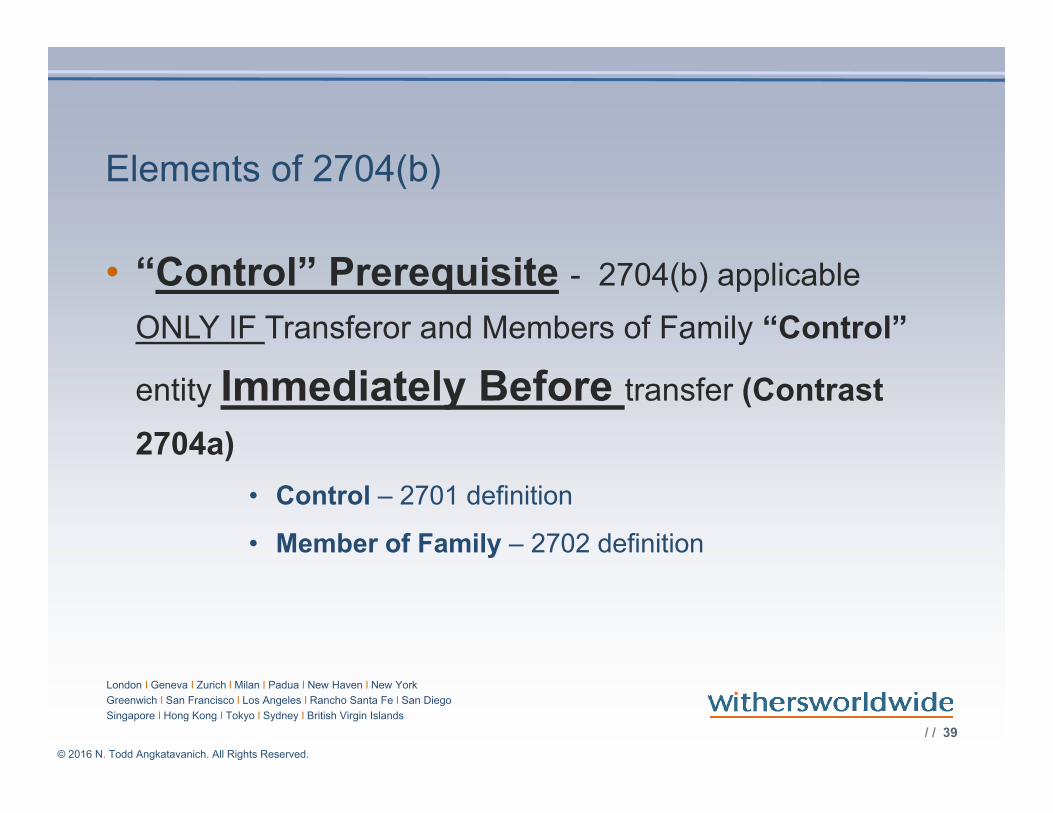

• “Control” Prerequisite - 2704(b) applicable

ONLY IF Transferor and Members of Family “Control”

entity Immediately Before transfer (Contrast

2704a)

• Control – 2701 definition

• Member of Family – 2702 definition

/ / 40

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Section 2704(b) – Example

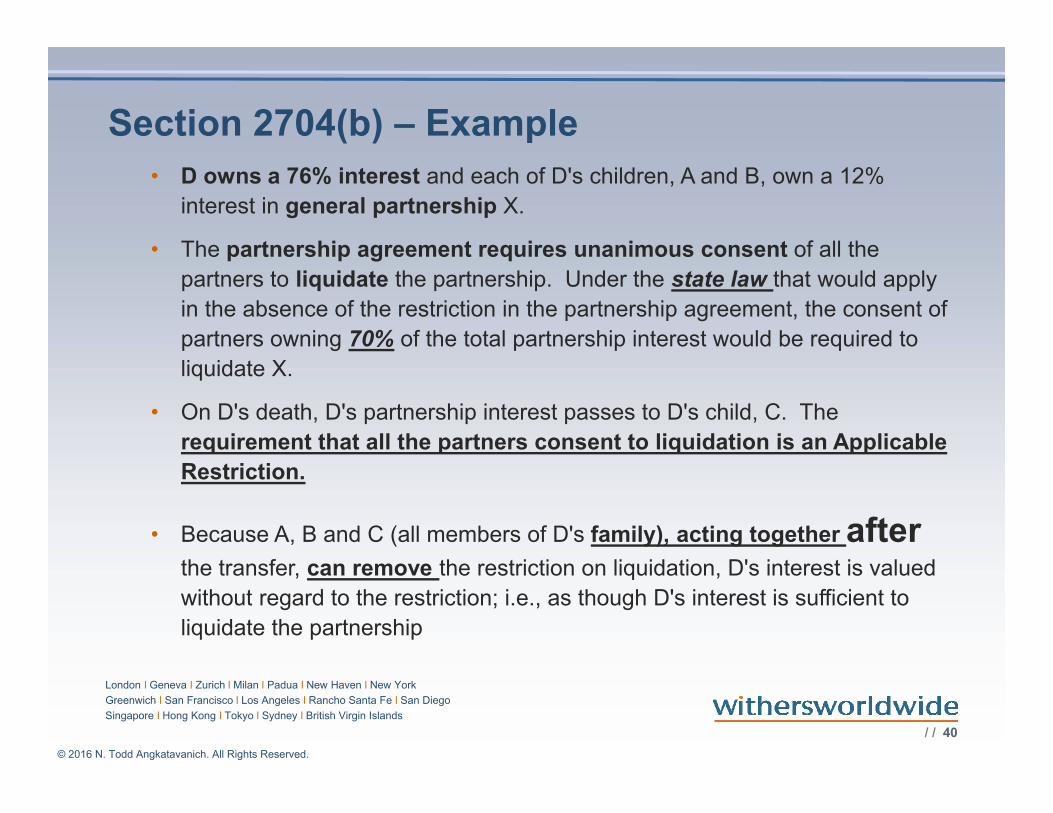

• D owns a 76% interest and each of D's children, A and B, own a 12%

interest in general partnership X.

• The partnership agreement requires unanimous consent of all the

partners to liquidate the partnership. Under the state law that would apply

in the absence of the restriction in the partnership agreement, the consent of

partners owning 70% of the total partnership interest would be required to

liquidate X.

• On D's death, D's partnership interest passes to D's child, C. The

requirement that all the partners consent to liquidation is an Applicable

Restriction.

• Because A, B and C (all members of D's family), acting together afterthe transfer, can remove the restriction on liquidation, D's interest is valued

without regard to the restriction; i.e., as though D's interest is sufficient to

liquidate the partnership

/ / 41

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

2704(b) and Kerr

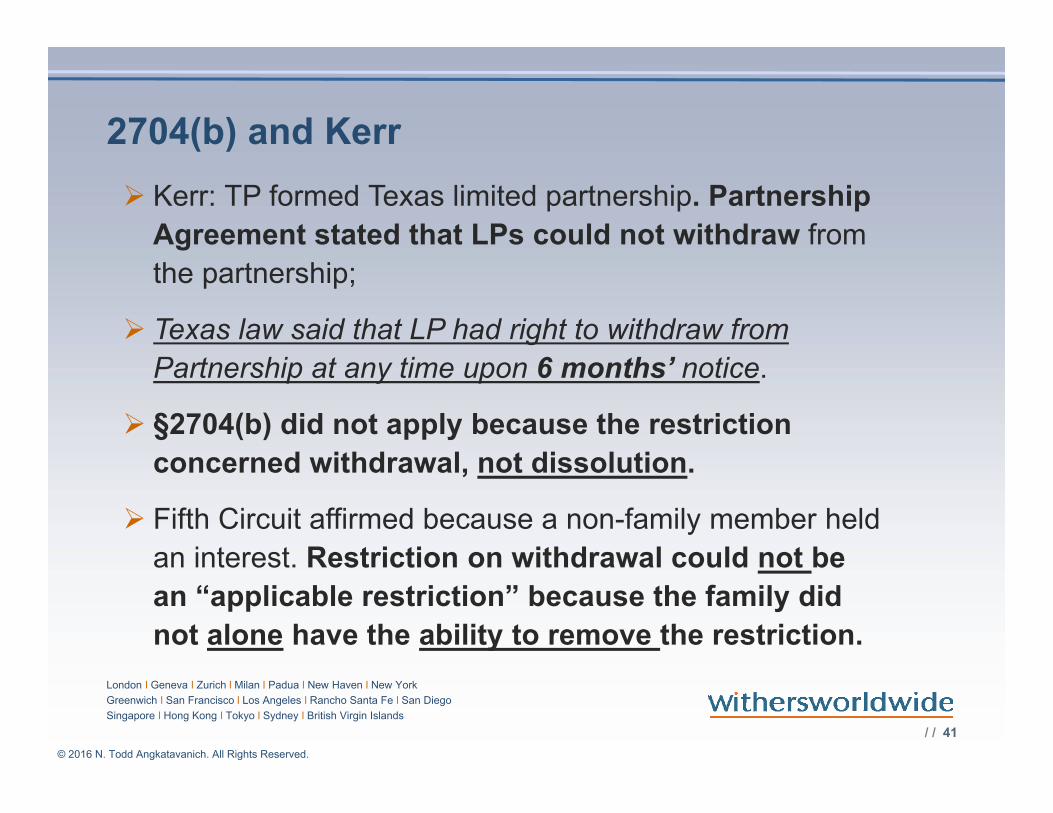

Kerr: TP formed Texas limited partnership. Partnership

Agreement stated that LPs could not withdraw from

the partnership;

Texas law said that LP had right to withdraw from

Partnership at any time upon 6 months’ notice.

§2704(b) did not apply because the restriction

concerned withdrawal, not dissolution.

Fifth Circuit affirmed because a non-family member held

an interest. Restriction on withdrawal could not be

an “applicable restriction” because the family did

not alone have the ability to remove the restriction.

/ / 42

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Possible Expansion of § 2704(b)

Under § 2704(b)(4):• The Secretary may by the regulations provide that other restrictions

shall be disregarded in determining the value of the transfer of any interest in a corporation or partnership to a member of the Transferor’s family if such restriction has the effect of reducing the value of the transferred interest for purposes of this subtitle but does not ultimately reduce the value of such interest to the transferee.

Proposed Expansion:

• Proposals for the expansion Obama Administration’s Greenbook for fiscal years 2010-2013.

• Congress has not adopted - but Treasury Dept. previously indicated that it has working on draft proposed regulations that presumably are similar to those in the Greenbook. More recently indicated that the draft would not be based on the Greenbook, but rather upon the statute.

/ / 43

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

The Greenbook proposals expand 2704(b) by:

Create Additional Category of restrictions (known as “Disregarded Restrictions”) that would be

IGNORED:

(i) limitations on a holder’s right to liquidate that holder’s interest (i.e., restrictions on Withdrawal Right), that are more restrictive than Default standards set in the Regulations, and

(ii) limitations on a Transferee’s Ability to be Admitted as a full partner or to hold an equity interest in the entity.

/ / 44

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Disregarded Restrictions would include:

Enumerated default assumptions would replace the Disregarded Restrictions

(Contrast: currently Applicable Restrictions default to State Law)

/ / 45

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Default Assumptions (if Disregarded Restrictions are ignored):

• Greenbook proposals would also treat interests held by charities and non-family members of the Transferor as held by the Transferor’s family for purposes of determining if the restriction can be removed by Members of Family.

• Marital and Charitable Deduction Mismatch - The Greenbook proposals promise to make “conforming clarifications” with regard to the interaction with the transfer tax marital and charitable deductions.

/ / 46

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Safe Harbors

Greenbook proposals envision regulatory safe harborswhich will provide standards for allowable restrictions.

Other Predictions – Operating Business Exception

Some commentators have suggested that the proposed regulations may include a carve-out for active or “genuine” family-owned businesses.[1]

[1] Ronald D. Aucutt, ACTEC Capital Letter No. 38: Anticipated Valuation Discount Regulations(Jul. 20, 2015).

/ / 47

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Questions Regarding Validity

Richard Dees argues that, absent Congressional action, regulations based on the Greenbook proposal would be invalid.[3] Dees argues that:

(i) Legislative history under Chapter 14 intended to protect traditional valuation discounts and to prohibit family attribution in valuing business interests; and

(ii) Treasury’s authority under § 2704(b)(4) does not extend to the creation of new categories of disregarded restrictions, new regulatory defaults, or redefining “Members of a Family” to include charities and others.

[3] See Richard L. Dees, Possible New Regulations under Internal Revenue Code Section 2704(b), TAX NOTES (August 31, 2015).

/ / 48

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

IRC SECTION 2703

/ / 49

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Introduction: §2703 – why you should care

Presumption that any:

• Option, Agreement or Right to Acquire or Use

Property (at less than fair market value)

OR

• Restriction on the right to sell or use property

Is DISREGARDED for transfer tax purposes

Overcoming the presumption very difficult

/ / 50

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

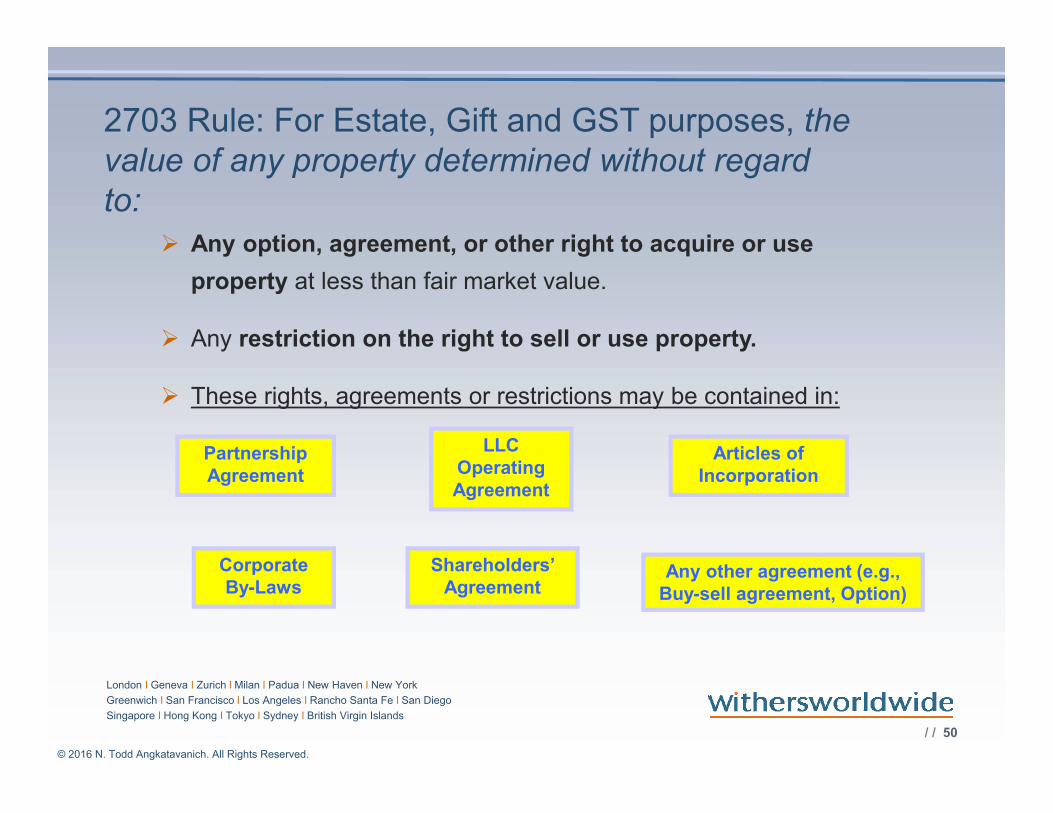

2703 Rule: For Estate, Gift and GST purposes, the value of any property determined without regard to:

Any option, agreement, or other right to acquire or use

property at less than fair market value.

Any restriction on the right to sell or use property.

These rights, agreements or restrictions may be contained in:

Partnership Agreement

LLC Operating Agreement

Articles of Incorporation

Corporate By-Laws

Shareholders’ Agreement

Any other agreement (e.g., Buy-sell agreement, Option)

/ / 51

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

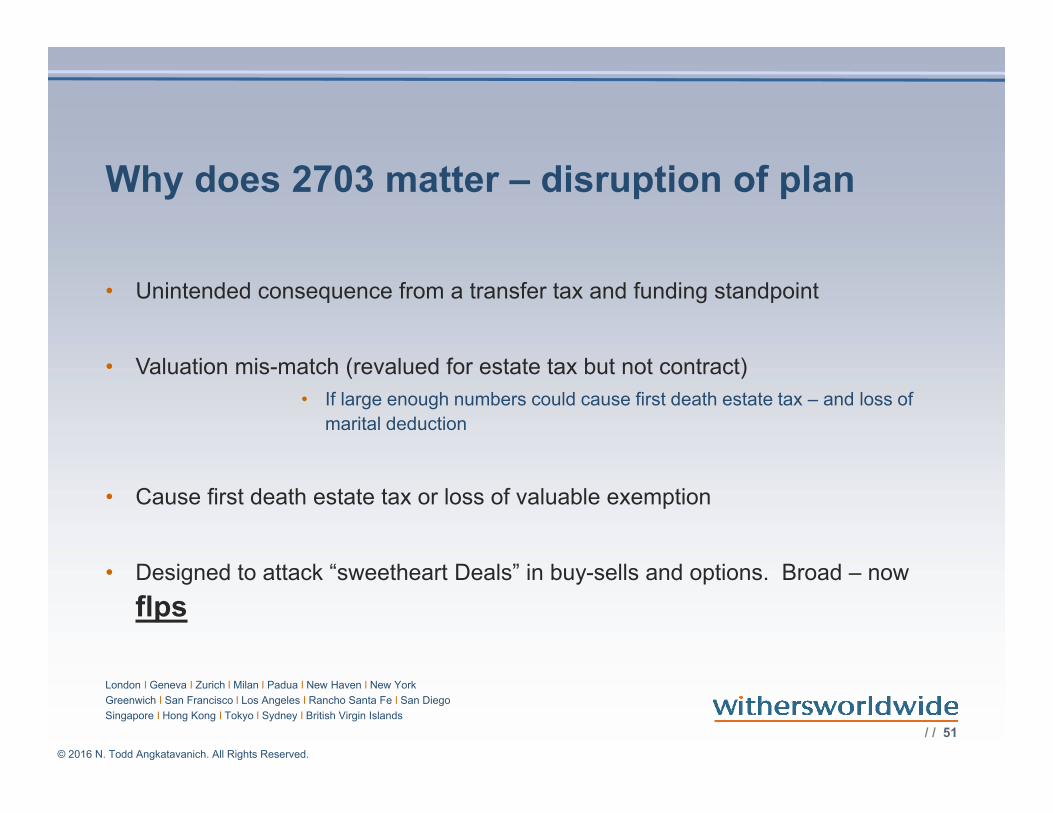

Why does 2703 matter – disruption of plan

• Unintended consequence from a transfer tax and funding standpoint

• Valuation mis-match (revalued for estate tax but not contract)

• If large enough numbers could cause first death estate tax – and loss of

marital deduction

• Cause first death estate tax or loss of valuable exemption

• Designed to attack “sweetheart Deals” in buy-sells and options. Broad – now

flps

/ / 52

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Effective date of §2703

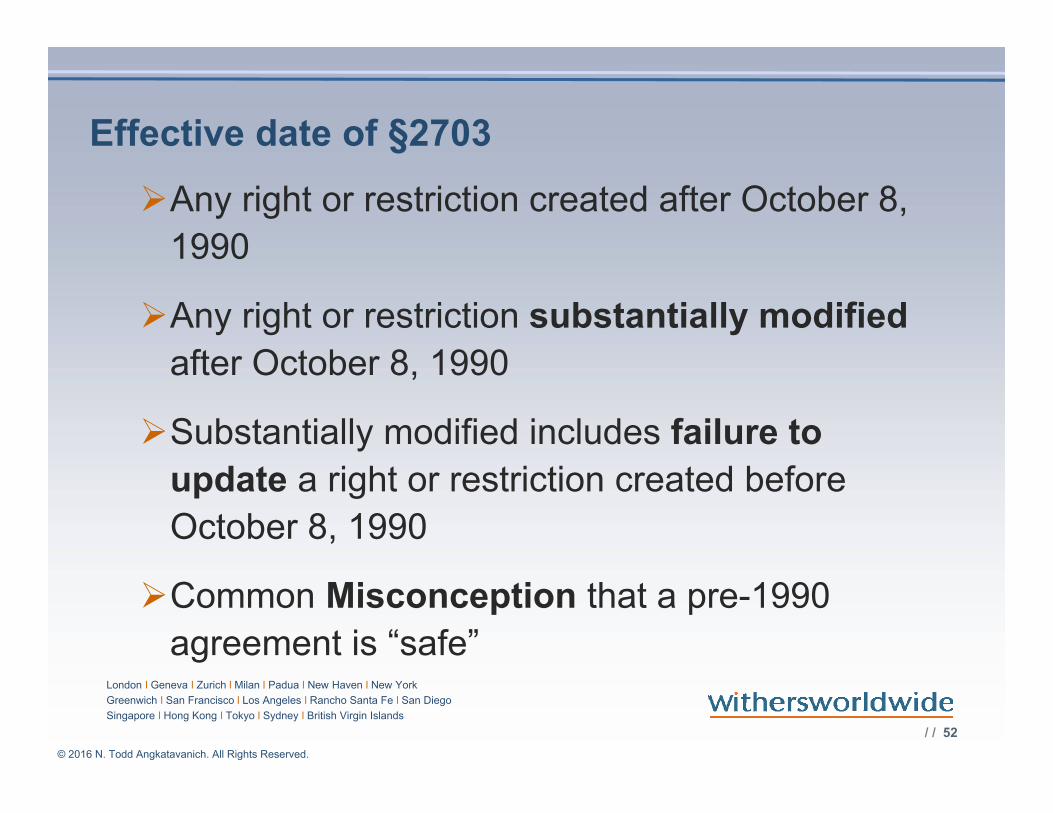

Any right or restriction created after October 8,

1990

Any right or restriction substantially modified

after October 8, 1990

Substantially modified includes failure to

update a right or restriction created before

October 8, 1990

Common Misconception that a pre-1990

agreement is “safe”

/ / 53

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

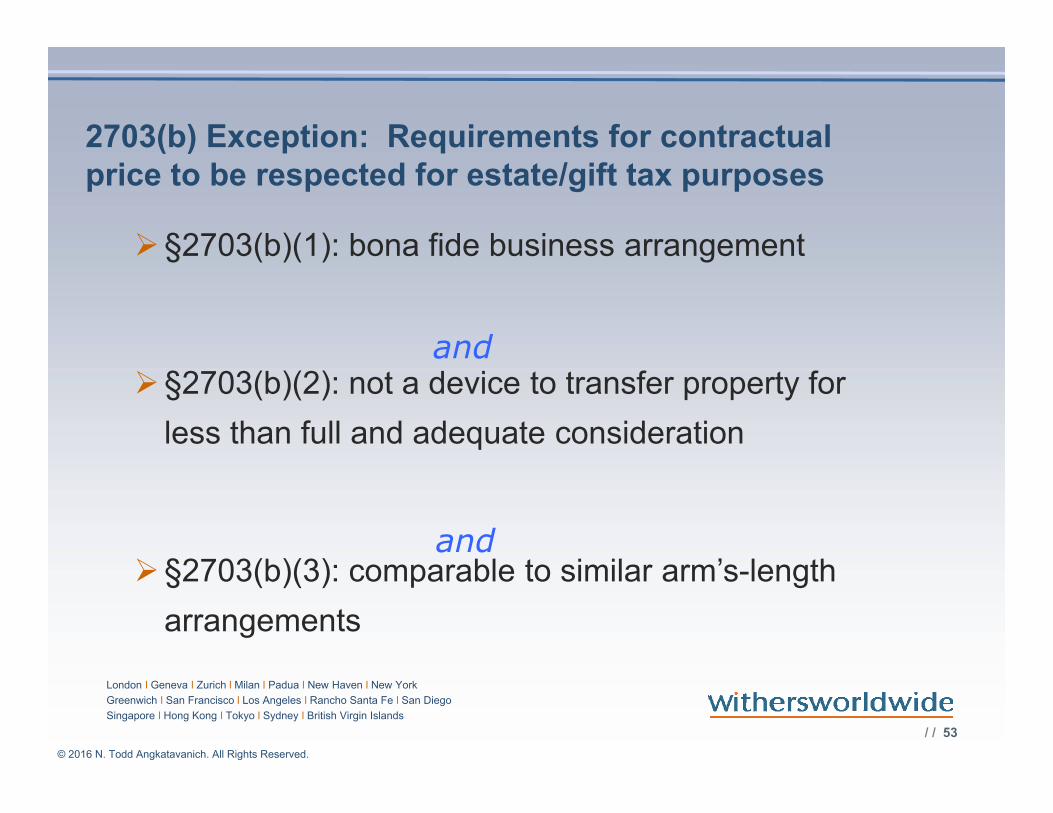

2703(b) Exception: Requirements for contractual price to be respected for estate/gift tax purposes

§2703(b)(1): bona fide business arrangement

§2703(b)(2): not a device to transfer property for

less than full and adequate consideration

§2703(b)(3): comparable to similar arm’s-length

arrangements

and

and

/ / 54

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

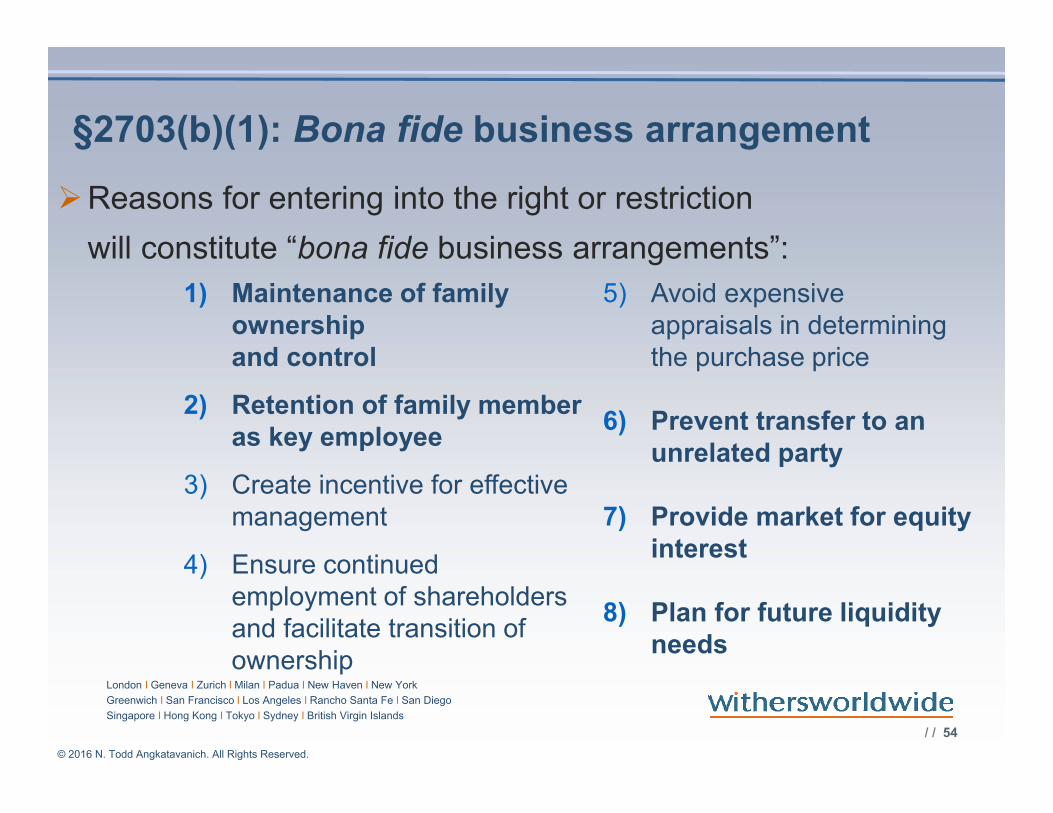

§2703(b)(1): Bona fide business arrangement

Reasons for entering into the right or restriction

will constitute “bona fide business arrangements”:

1) Maintenance of family ownership and control

2) Retention of family member as key employee

3) Create incentive for effective management

4) Ensure continued employment of shareholders and facilitate transition of ownership

5) Avoid expensive appraisals in determining the purchase price

6) Prevent transfer to an unrelated party

7) Provide market for equity interest

8) Plan for future liquidity needs

/ / 55

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

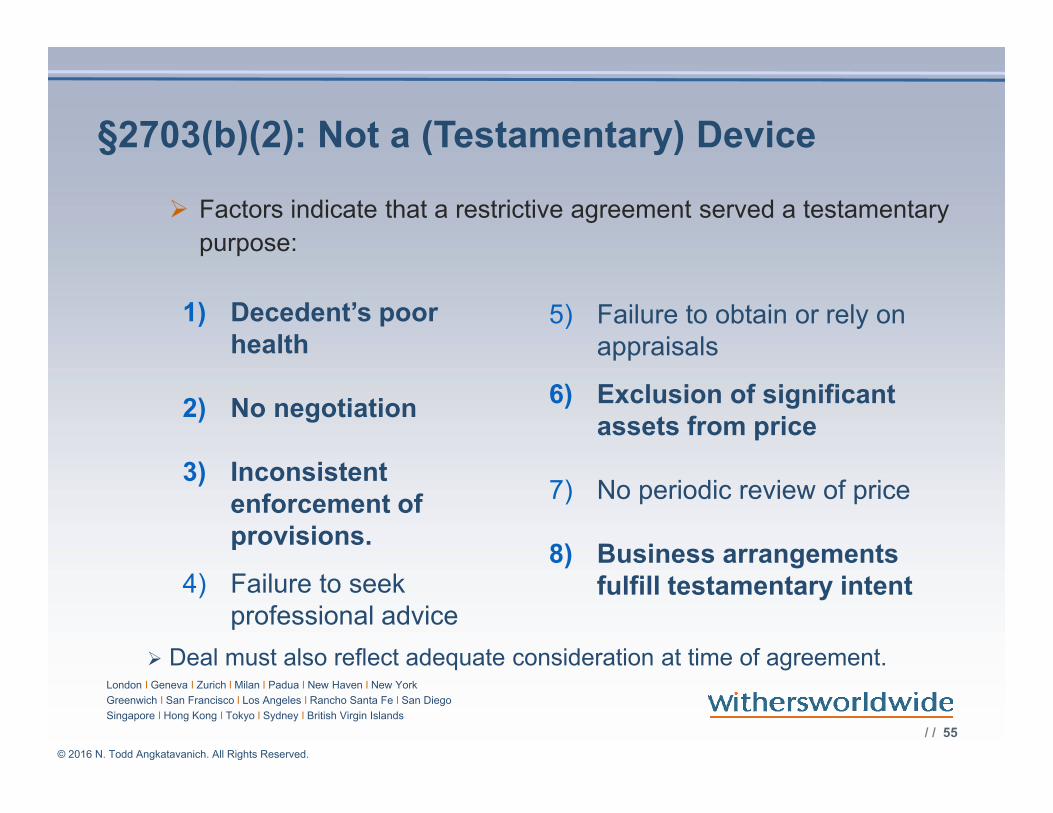

§2703(b)(2): Not a (Testamentary) Device

Factors indicate that a restrictive agreement served a testamentary

purpose:

1) Decedent’s poor health

2) No negotiation

3) Inconsistent enforcement of provisions.

4) Failure to seek professional advice

5) Failure to obtain or rely on appraisals

6) Exclusion of significant assets from price

7) No periodic review of price

8) Business arrangements fulfill testamentary intent

Deal must also reflect adequate consideration at time of agreement.

/ / 56

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

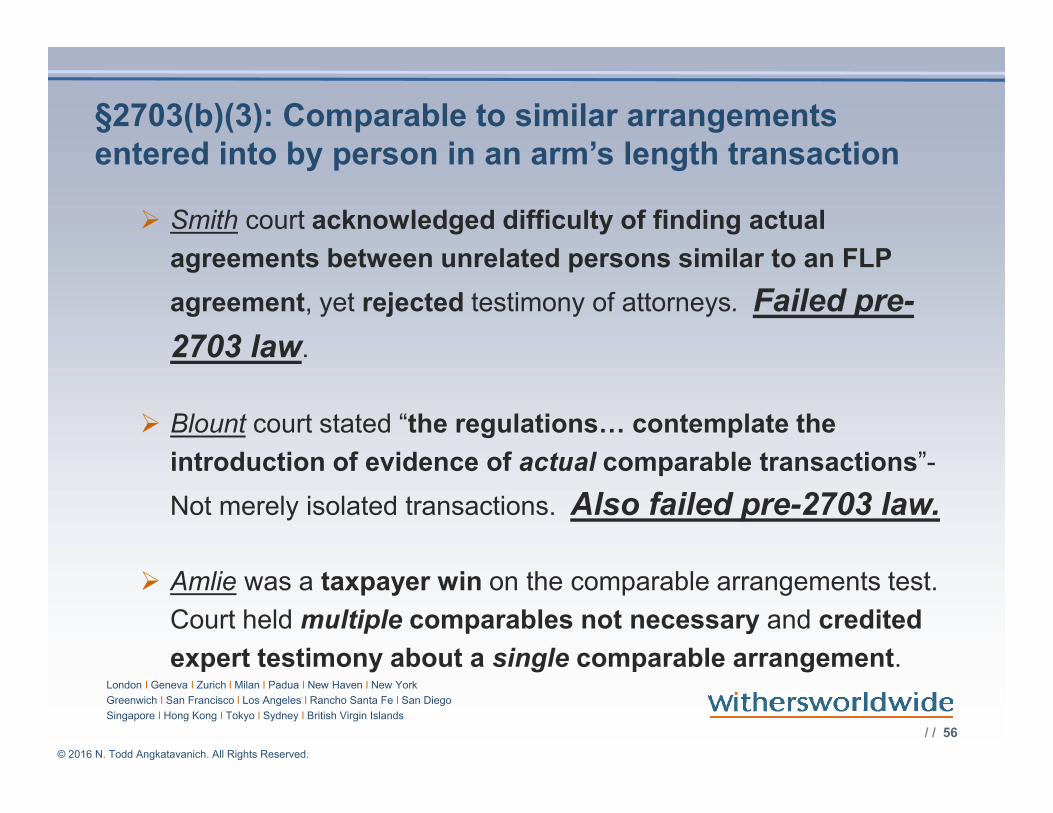

§2703(b)(3): Comparable to similar arrangements entered into by person in an arm’s length transaction

Smith court acknowledged difficulty of finding actual

agreements between unrelated persons similar to an FLP

agreement, yet rejected testimony of attorneys. Failed pre-

2703 law.

Blount court stated “the regulations… contemplate the

introduction of evidence of actual comparable transactions”-

Not merely isolated transactions. Also failed pre-2703 law.

Amlie was a taxpayer win on the comparable arrangements test.

Court held multiple comparables not necessary and credited

expert testimony about a single comparable arrangement.

/ / 57

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

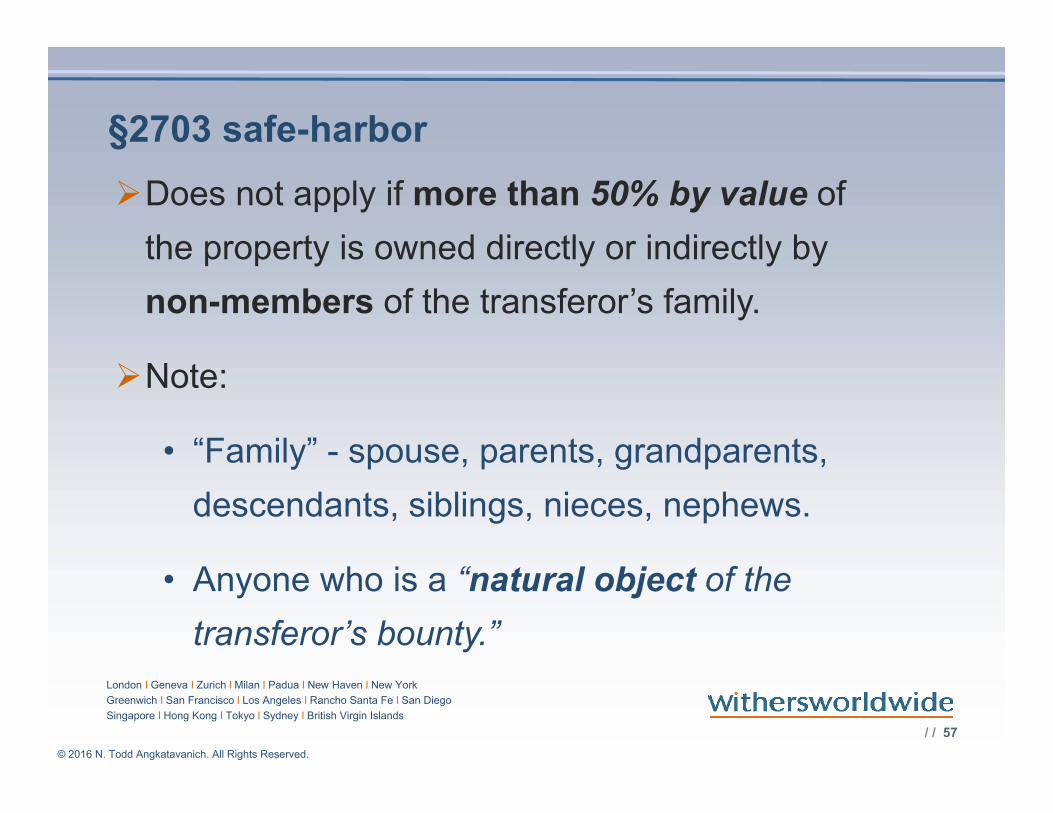

§2703 safe-harbor

Does not apply if more than 50% by value of

the property is owned directly or indirectly by

non-members of the transferor’s family.

Note:

• “Family” - spouse, parents, grandparents,

descendants, siblings, nieces, nephews.

• Anyone who is a “natural object of the

transferor’s bounty.”

/ / 58

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Section 2703 and FLPS

Old Argument: 2703 Disregard of Entire Partnership

2 IRS Arguments

• “Property” refers to the underlying assets

owned by the partnership

• “Restrictions” refers to the partnership entity

itself – “LOOK THROUGH”

• IRS Lost both:

• Church v. U.S.

• Strangi v. Comm’r

/ / 59

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Section 2703 and FLPS Current Arguments: 2703 and Holman

GIFT TAX CASE

TP received a substantial amount of Dell

Computer Corp. stock options.

TP formed partnership for the following purposes,

and funded it with Dell stock:

• Long-term Growth

• Asset Preservation

• Asset Protection

• Education

/ / 60

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Held: Restrictive provisions (“ROFR”) ignored

under 2703

NOT Bona fide Business Purpose –

Personal Goals of TP.

Restriction was DEVICE - GP could re-acquire

partners’ interest at a discount attempted

transfer

Section 2703 and FLPS

Current Arguments: 2703 and Holman

/ / 61

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

2703 on your radar

• Buys-sell agreements (pre and post 2703)

• Options

• FLP

• Mismatch consequences – unexpected disruption

• Remember pre-2703 law – “substantial modification”

/ / 62

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

IRC SECTION 2702

/ / 63

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

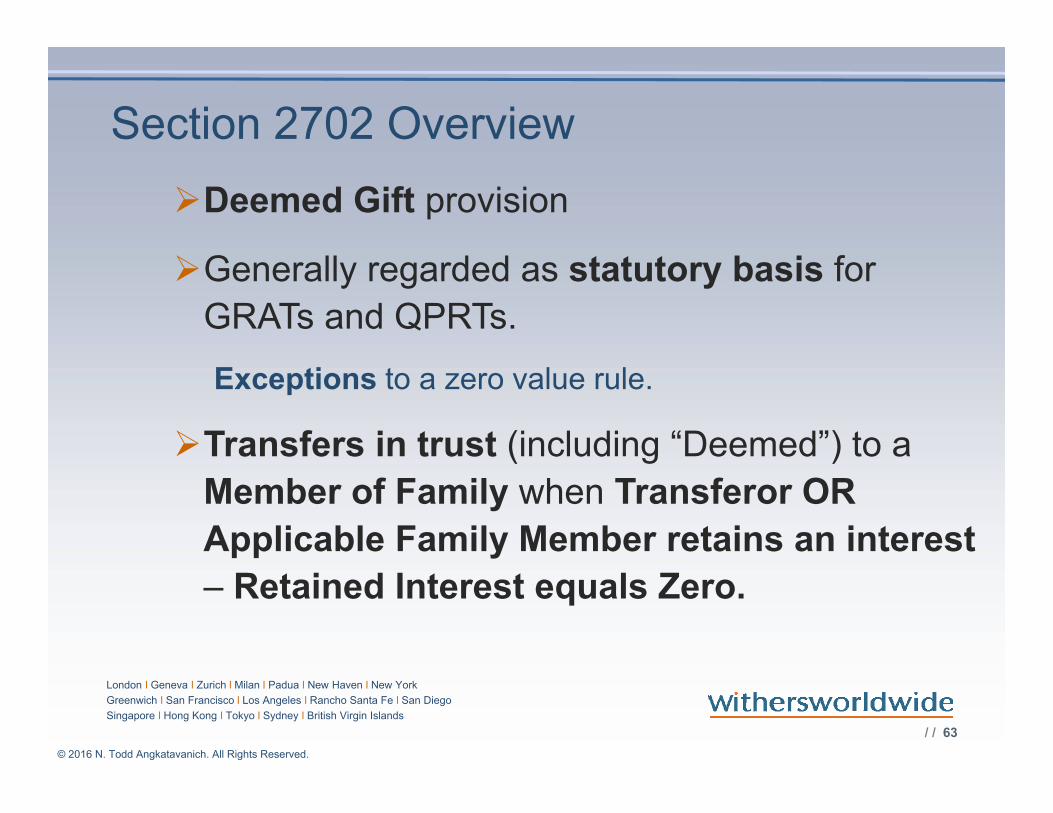

Section 2702 Overview

Deemed Gift provision

Generally regarded as statutory basis for

GRATs and QPRTs.

Exceptions to a zero value rule.

Transfers in trust (including “Deemed”) to a

Member of Family when Transferor OR

Applicable Family Member retains an interest

– Retained Interest equals Zero.

/ / 64

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

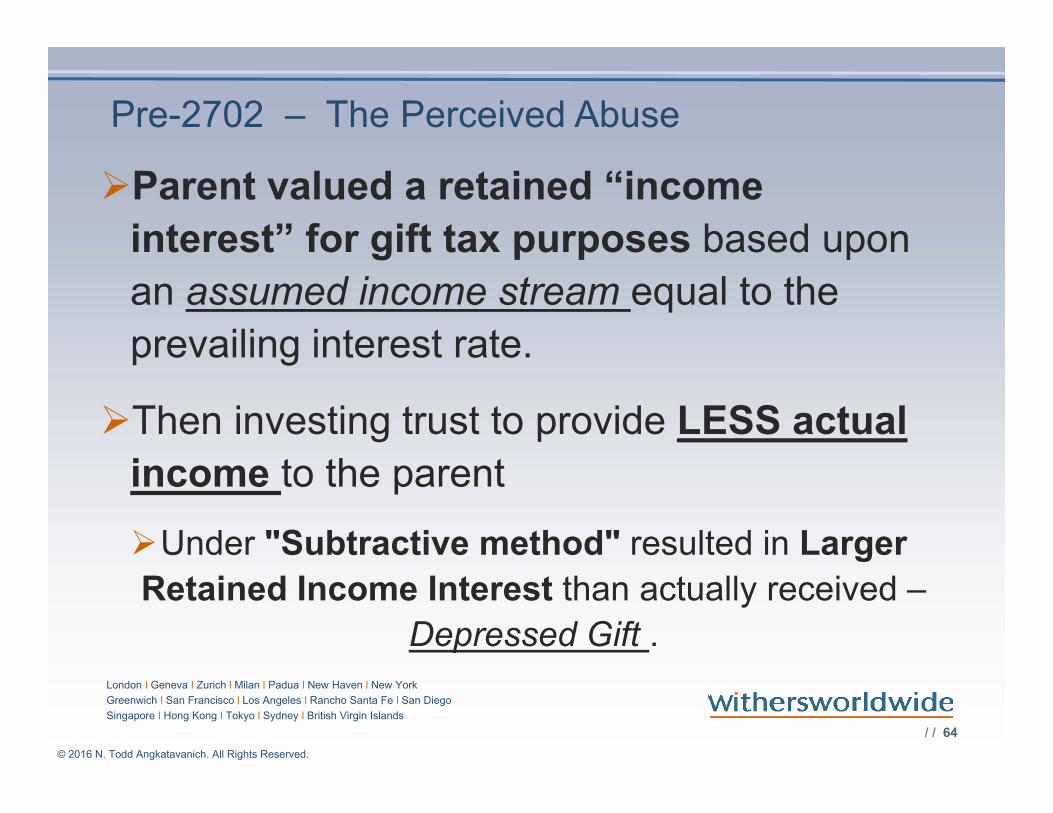

Pre-2702 – The Perceived Abuse

Parent valued a retained “income

interest” for gift tax purposes based upon

an assumed income stream equal to the

prevailing interest rate.

Then investing trust to provide LESS actual

income to the parent

Under "Subtractive method" resulted in Larger

Retained Income Interest than actually received –

Depressed Gift .

/ / 65

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

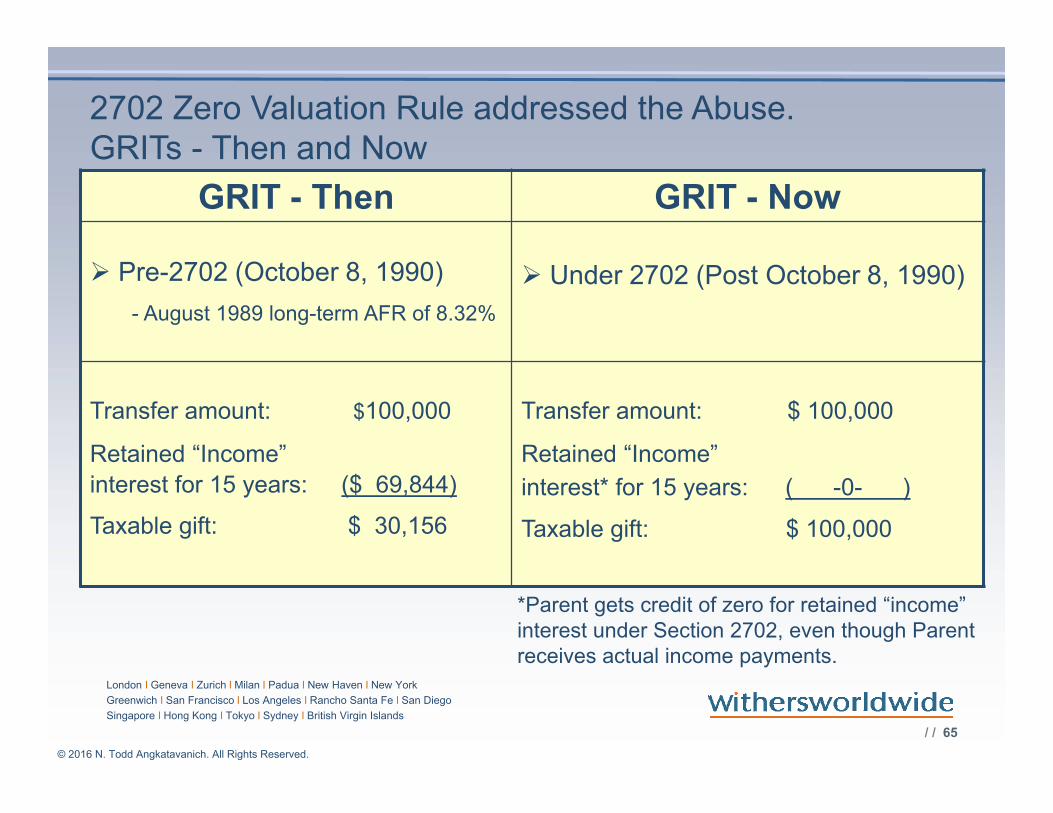

2702 Zero Valuation Rule addressed the Abuse.GRITs - Then and Now

GRIT - Then GRIT - Now

Pre-2702 (October 8, 1990)

- August 1989 long-term AFR of 8.32%

Under 2702 (Post October 8, 1990)

Transfer amount: $100,000

Retained “Income”

interest for 15 years: ($ 69,844)

Taxable gift: $ 30,156

Transfer amount: $ 100,000

Retained “Income”

interest* for 15 years: ( -0- )

Taxable gift: $ 100,000

*Parent gets credit of zero for retained “income” interest under Section 2702, even though Parent receives actual income payments.

/ / 66

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

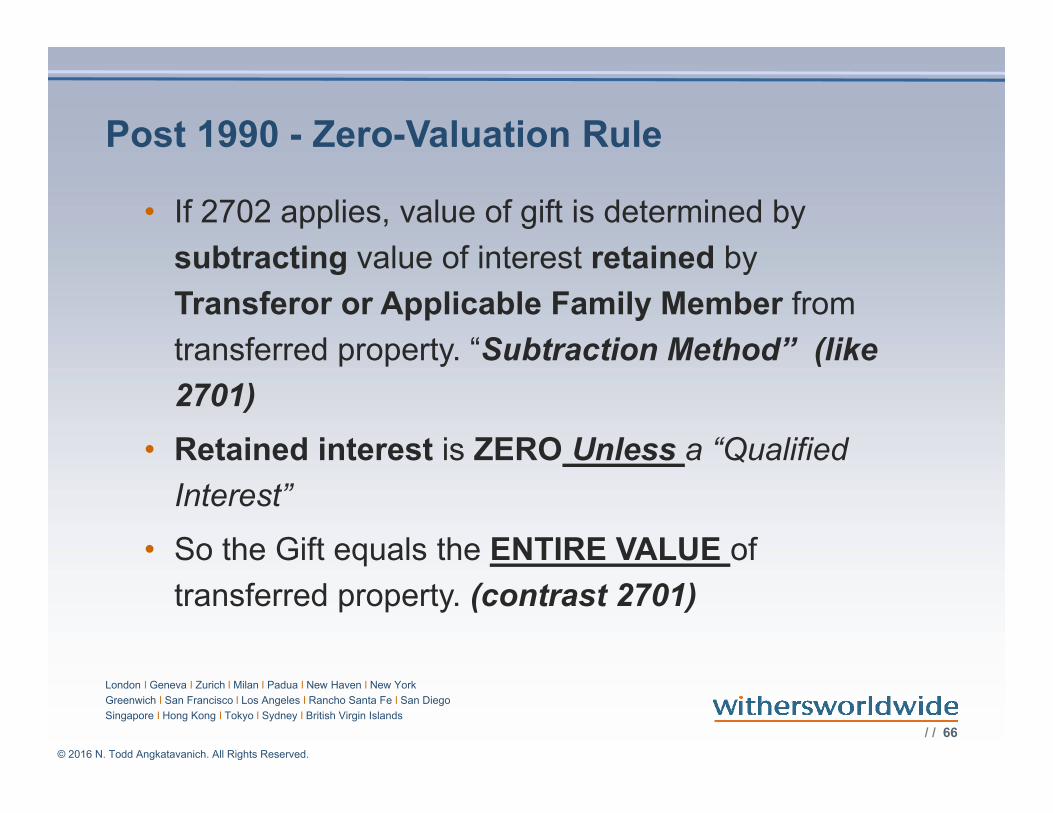

Post 1990 - Zero-Valuation Rule

• If 2702 applies, value of gift is determined by

subtracting value of interest retained by

Transferor or Applicable Family Member from

transferred property. “Subtraction Method” (like

2701)

• Retained interest is ZERO Unless a “Qualified

Interest”

• So the Gift equals the ENTIRE VALUE of

transferred property. (contrast 2701)

/ / 67

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

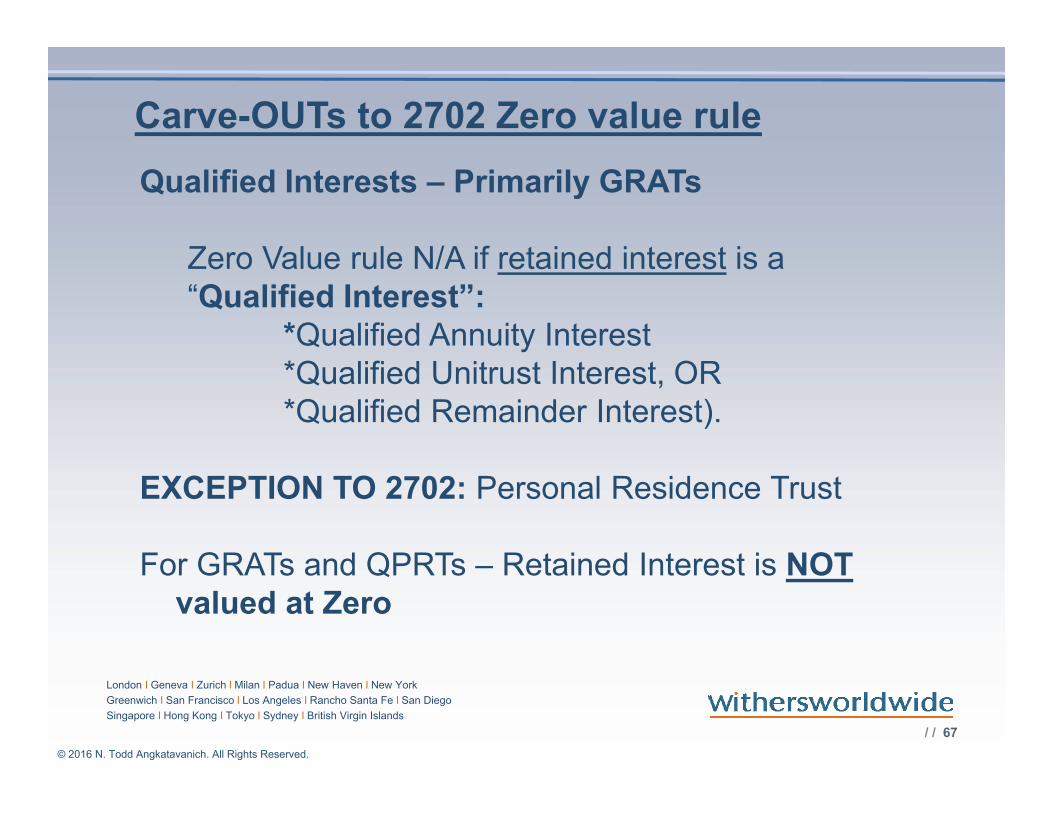

Carve-OUTs to 2702 Zero value rule

Qualified Interests – Primarily GRATs

Zero Value rule N/A if retained interest is a “Qualified Interest”:

*Qualified Annuity Interest*Qualified Unitrust Interest, OR*Qualified Remainder Interest).

EXCEPTION TO 2702: Personal Residence Trust

For GRATs and QPRTs – Retained Interest is NOTvalued at Zero

/ / 68

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

GRATs and QPRTs - Rationale

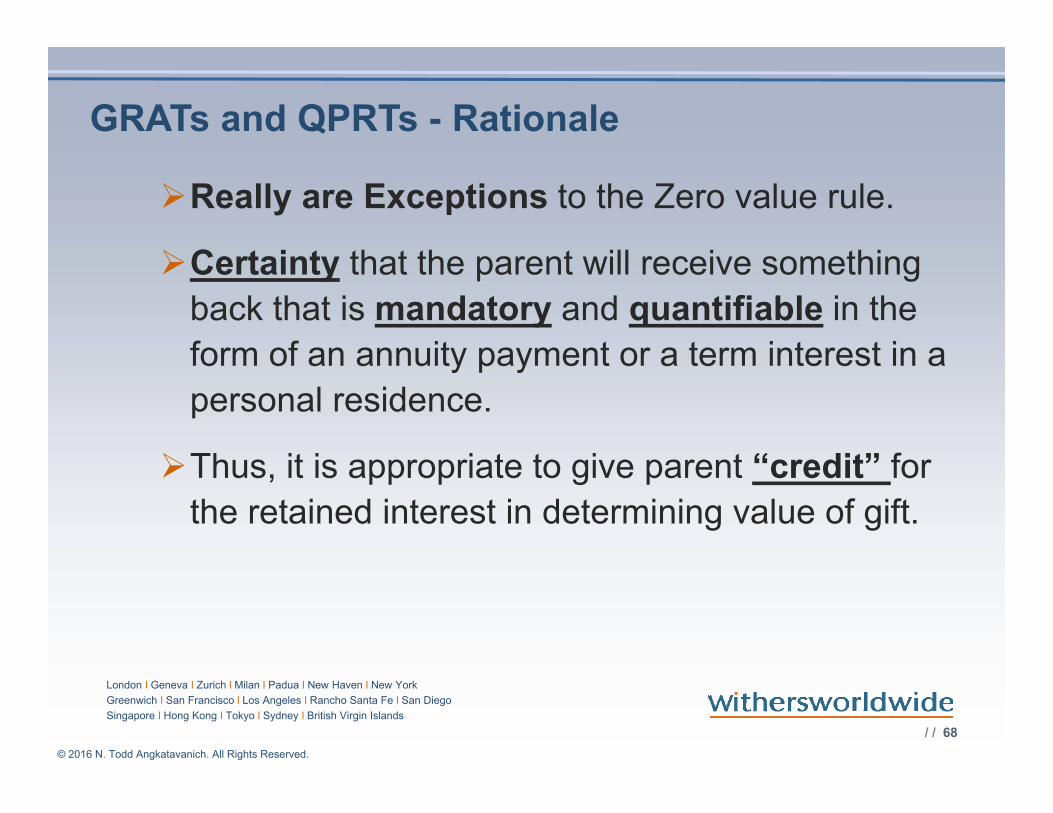

Really are Exceptions to the Zero value rule.

Certainty that the parent will receive something

back that is mandatory and quantifiable in the

form of an annuity payment or a term interest in a

personal residence.

Thus, it is appropriate to give parent “credit” for

the retained interest in determining value of gift.

/ / 69

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

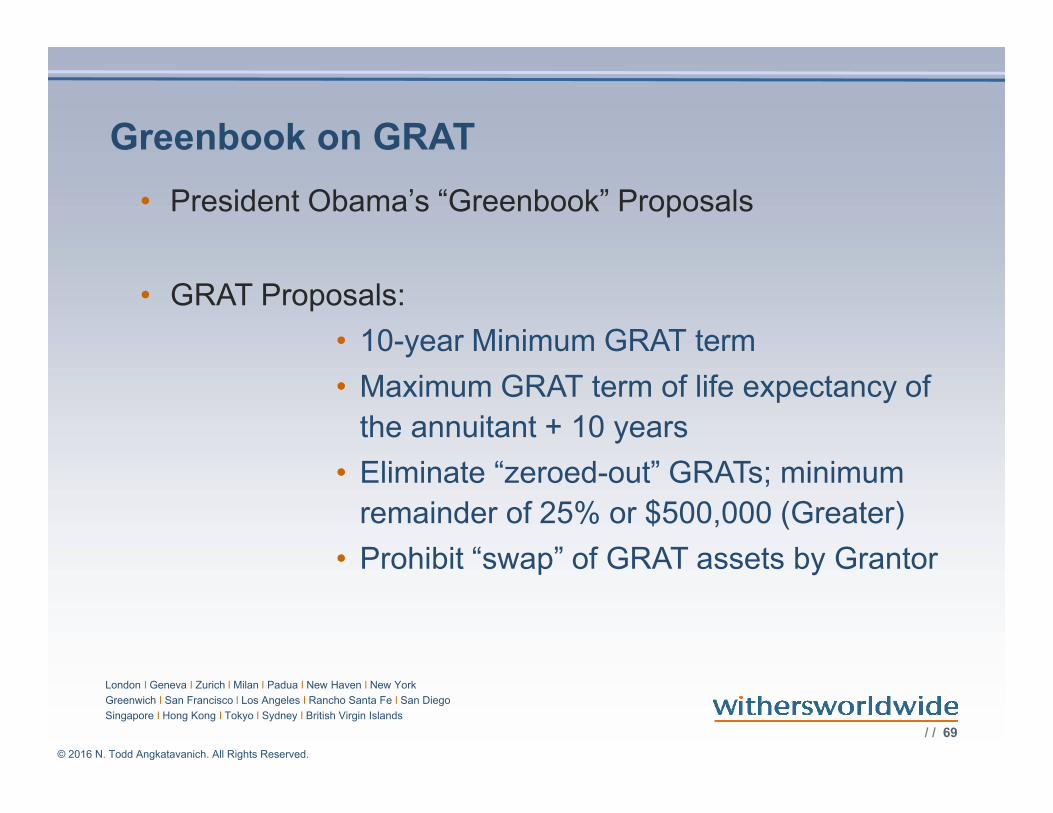

Greenbook on GRAT

• President Obama’s “Greenbook” Proposals

• GRAT Proposals:

• 10-year Minimum GRAT term

• Maximum GRAT term of life expectancy of

the annuitant + 10 years

• Eliminate “zeroed-out” GRATs; minimum

remainder of 25% or $500,000 (Greater)

• Prohibit “swap” of GRAT assets by Grantor

/ / 70

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

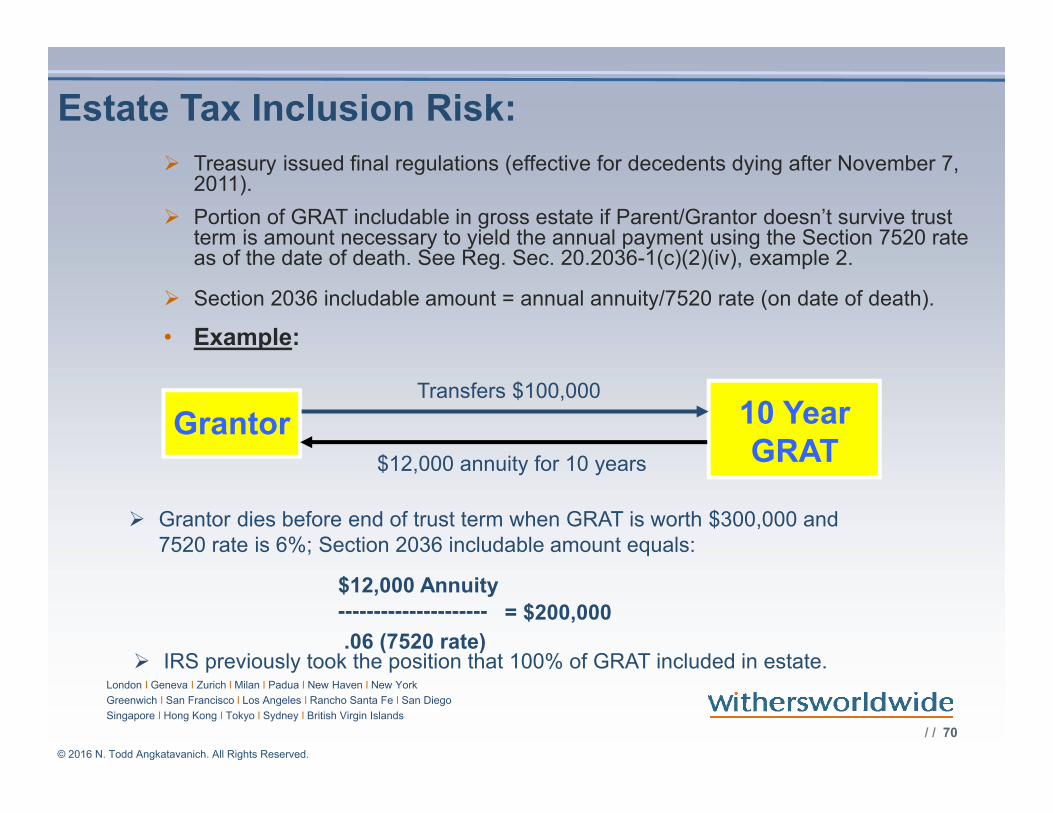

Estate Tax Inclusion Risk:

Treasury issued final regulations (effective for decedents dying after November 7, 2011).

Portion of GRAT includable in gross estate if Parent/Grantor doesn’t survive trust term is amount necessary to yield the annual payment using the Section 7520 rate as of the date of death. See Reg. Sec. 20.2036-1(c)(2)(iv), example 2.

Section 2036 includable amount = annual annuity/7520 rate (on date of death).

• Example:

Grantor dies before end of trust term when GRAT is worth $300,000 and 7520 rate is 6%; Section 2036 includable amount equals:

IRS previously took the position that 100% of GRAT included in estate.

Transfers $100,000

$12,000 annuity for 10 years

$12,000 Annuity---------------------

.06 (7520 rate)

= $200,000

Grantor 10 Year GRAT

/ / 71

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Generation Skipping Tax / ETIP Issue

ETIP inclusion under 2036

Cannot allocate GST exemption until end of

trust term (ETIP)

To maximize GST you want to allocate to

assets before assets appreciate

GST automatic allocation to indirect transfers

to deemed “GST Trusts”

Preferred Partnership GRAT idea

/ / 72

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Generation Skipping Tax / ETIP Issue (Cont’d)

Cannot allocate GST exemption until end of trust term (ETIP)

To maximize use of GST exemption, want to allocate to assets before

assets appreciate. GRATs are therefore less effective for GST planning

than other techniques (such as gift/sale transactions).

GST automatic allocation to indirect transfers to deemed “GST Trusts.”

Consider “election out” of GST automatic allocation rules at

end of trust term/ETIP

Example:

GRAT value at end of trust-formed ETIP - $10,000,000

Grantor’s remaining GST exemption = $2,000,000

If don’t elect out, results in GST inclusion ratio of .8 (80% subject

to GST tax)

/ / 73

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Preferred Partnership GRAT

GST Trust

Parent

Preferred Partnership

GRAT Contribution of Preferred

Interest

QPR*

Long Term GRAT

Annuity (Funded by Preferred Coupon)

Common

Capital ContributionCapital

Contribution

* Could also use mandatory payment right or guaranteed payment right

/ / 74

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

GRATs

Zeroed-out GRATs

Increasing Volatility and

Capturing the Upside (Rolling

GRATs; Series GRATS)

Estate tax inclusion risk

/ / 75

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

GRAT Technical Requirements

Fixed amount

Annuity amount may be increased up to 20% each year

GRAT adjusts for incorrect valuations

Cannot be payment of a debt obligation option

No additional contributions to GRAT permitted

No pre-payment

105 day rule

/ / 76

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Section 2702 and Karmazin (and now Woebling)

IRS argued - sale of the LP interest by

the TP in exchange for note constituted

a “transfer in trust” under §2702

Under §2702, a retained interest has no

value unless it is a “qualified interest”

/ / 77

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

The sold LP interest should be recharacterized as a gift to the IDGT, in exchange for a retained interest valued at zero, resulting in a taxable gift of all LP interests sold

Woelbing - Tax Court scheduled trial for February 29, 2016. Ultimately settled.

Section 2702 and Karmazin (and now Woelbing)

/ / 78

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

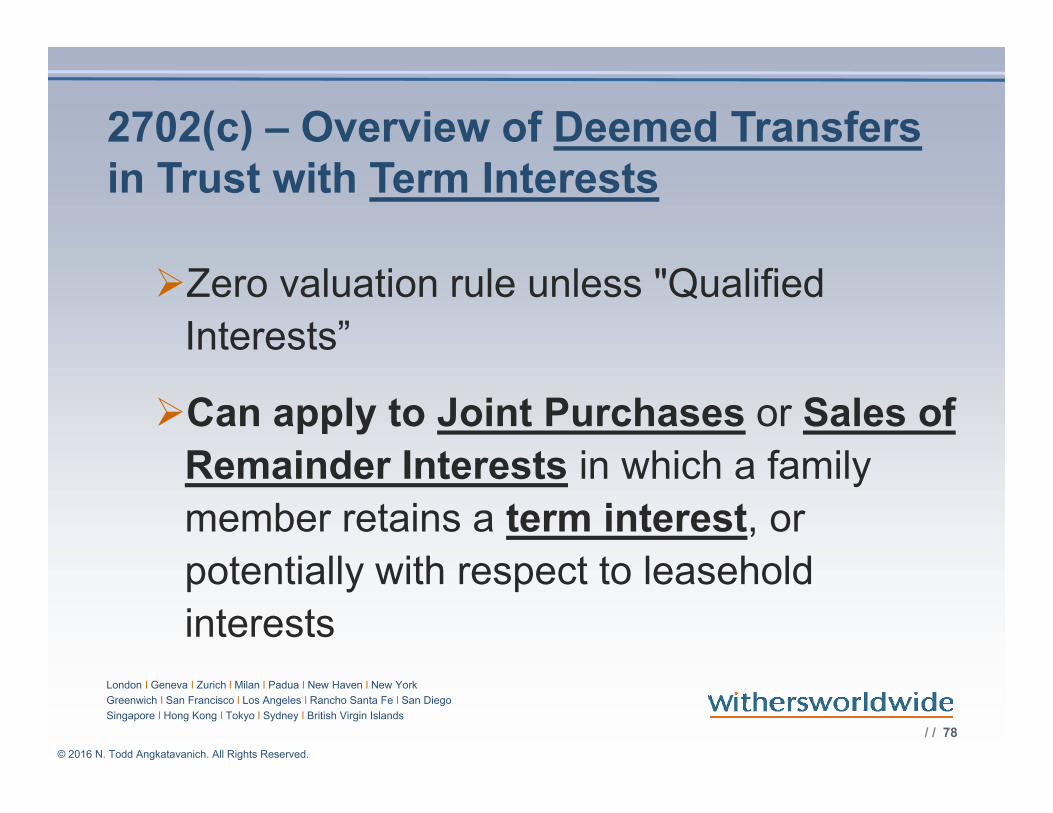

2702(c) – Overview of Deemed Transfers in Trust with Term Interests

Zero valuation rule unless "Qualified

Interests”

Can apply to Joint Purchases or Sales of

Remainder Interests in which a family

member retains a term interest, or

potentially with respect to leasehold

interests

/ / 79

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

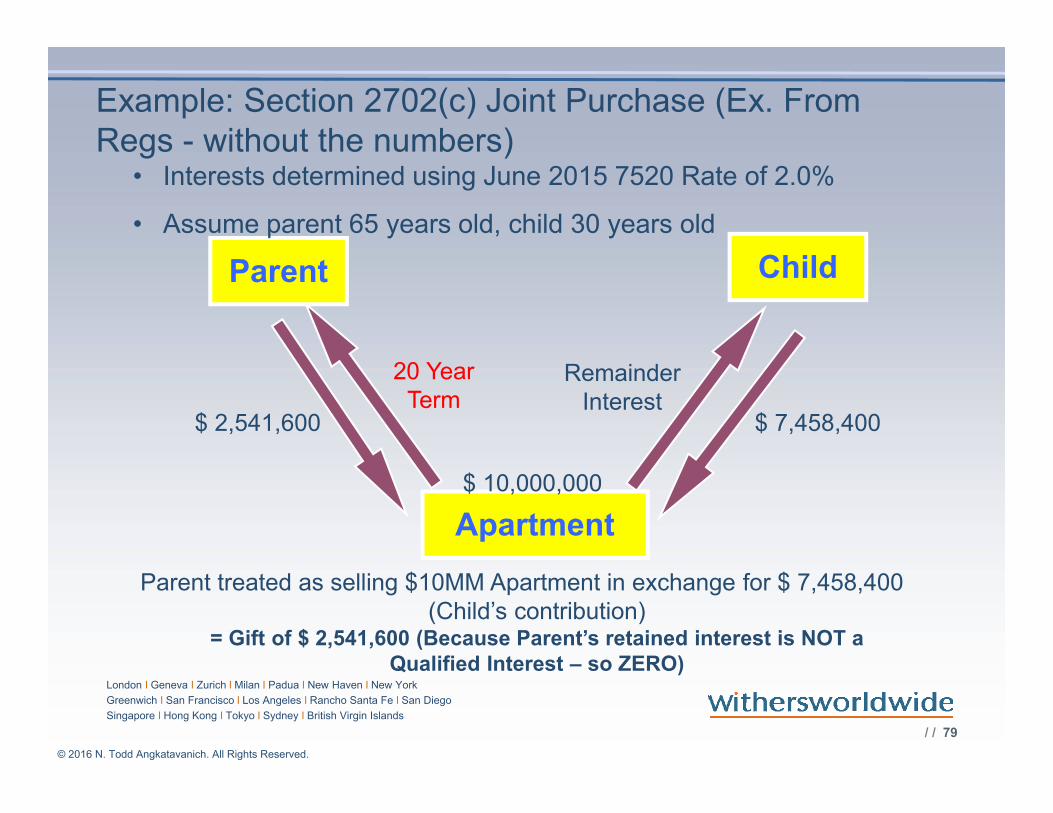

Example: Section 2702(c) Joint Purchase (Ex. From Regs - without the numbers)

Remainder Interest

$ 2,541,600

20 YearTerm

Parent Child

Apartment

Parent treated as selling $10MM Apartment in exchange for $ 7,458,400 (Child’s contribution)

= Gift of $ 2,541,600 (Because Parent’s retained interest is NOT a Qualified Interest – so ZERO)

$ 10,000,000

$ 7,458,400

• Interests determined using June 2015 7520 Rate of 2.0%

• Assume parent 65 years old, child 30 years old

/ / 80

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Example: Section 2702(c) Joint Purchases (Cont’d)

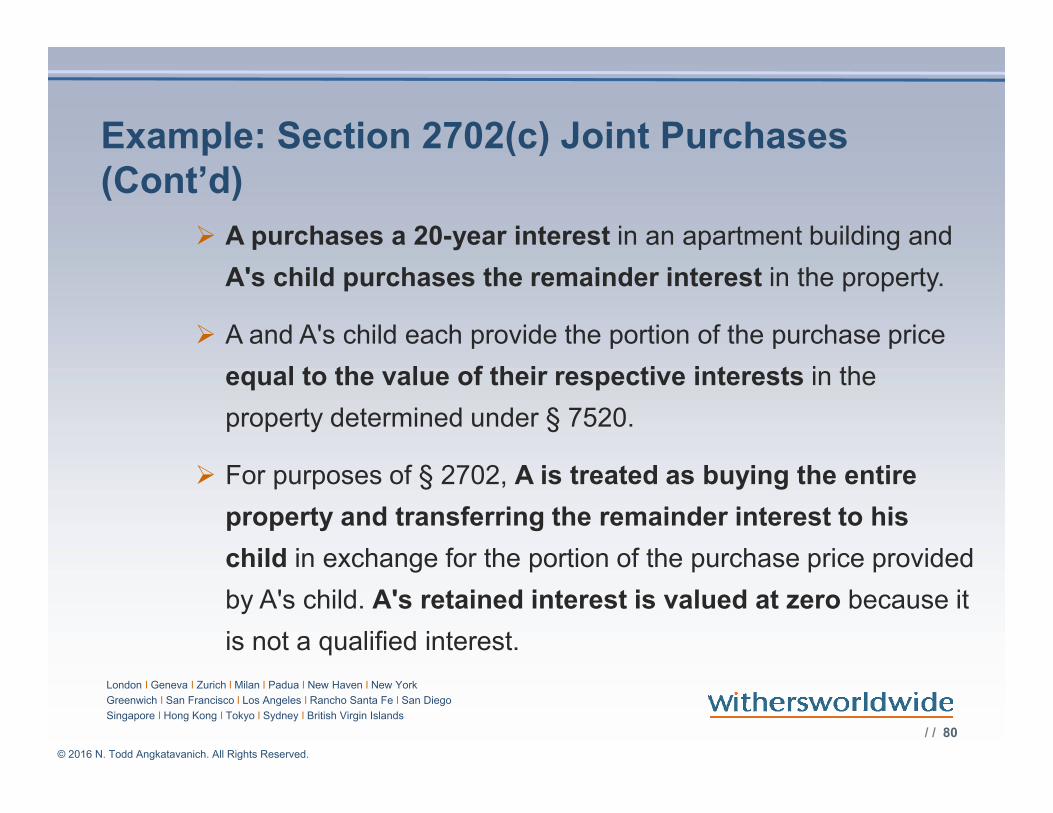

A purchases a 20-year interest in an apartment building and

A's child purchases the remainder interest in the property.

A and A's child each provide the portion of the purchase price

equal to the value of their respective interests in the

property determined under § 7520.

For purposes of § 2702, A is treated as buying the entire

property and transferring the remainder interest to his

child in exchange for the portion of the purchase price provided

by A's child. A's retained interest is valued at zero because it

is not a qualified interest.

/ / 81

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

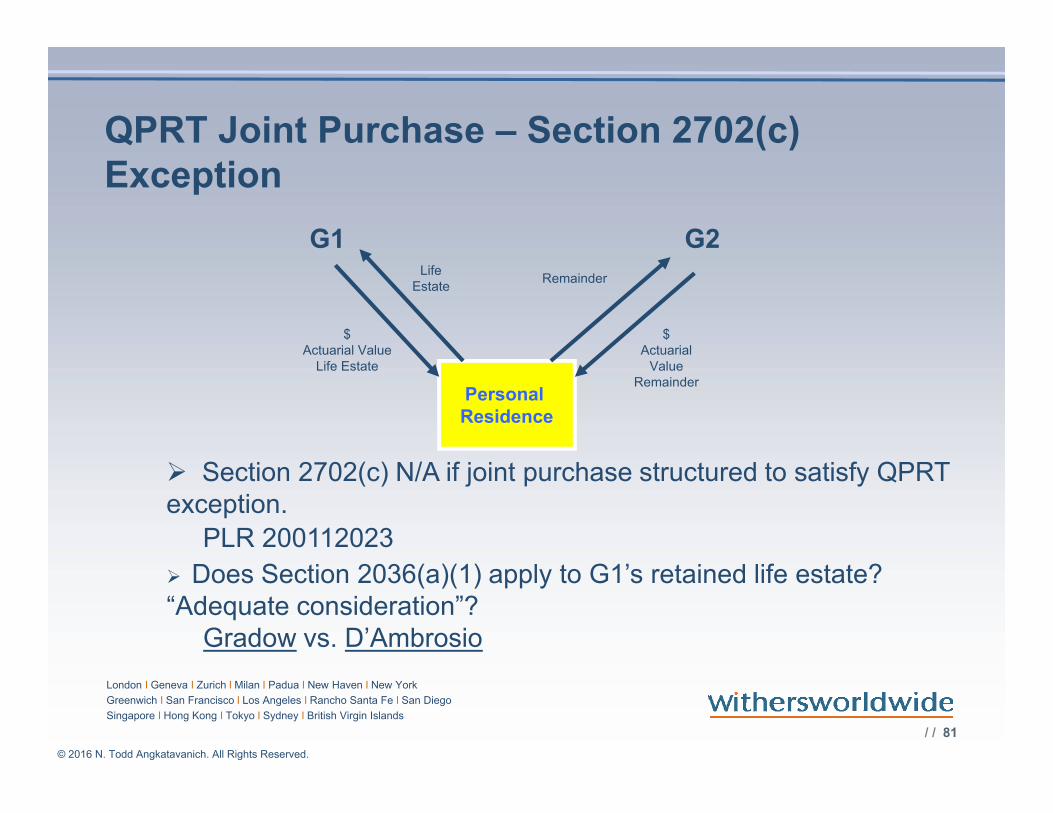

QPRT Joint Purchase – Section 2702(c) Exception

Personal Residence

G1 G2Life

Estate

$ Actuarial Value

Life Estate

Remainder

$Actuarial

Value Remainder

Section 2702(c) N/A if joint purchase structured to satisfy QPRT exception.

PLR 200112023

Does Section 2036(a)(1) apply to G1’s retained life estate? “Adequate consideration”?

Gradow vs. D’Ambrosio

/ / 82

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

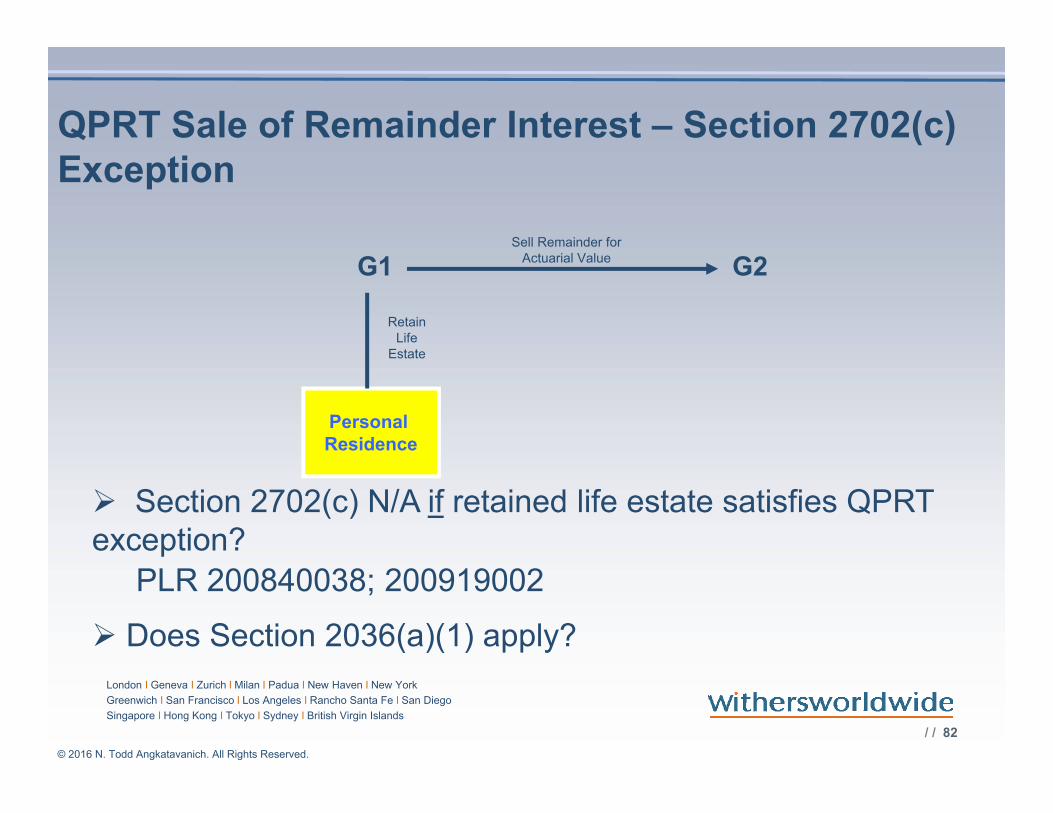

QPRT Sale of Remainder Interest – Section 2702(c) Exception

Personal Residence

G1 G2

RetainLife

Estate

Sell Remainder for Actuarial Value

Section 2702(c) N/A if retained life estate satisfies QPRT exception?

PLR 200840038; 200919002

Does Section 2036(a)(1) apply?

/ / 83

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Section 2702(c) Exceptions

Leasehold Interest – If full and adequate consideration (good faith facts and circ.)

Property Interests which are NOT treated as term interests:

• Tenants-in-Common

• Tenants by the Entireties

• Tenants with Rights of Survivorship

/ / 84

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Qualified Personal Residence Trust

“Subtraction method” of valuation

is applied.

Retained use of the house is valued

based on the 7520 rate for the month

of the gift

/ / 85

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

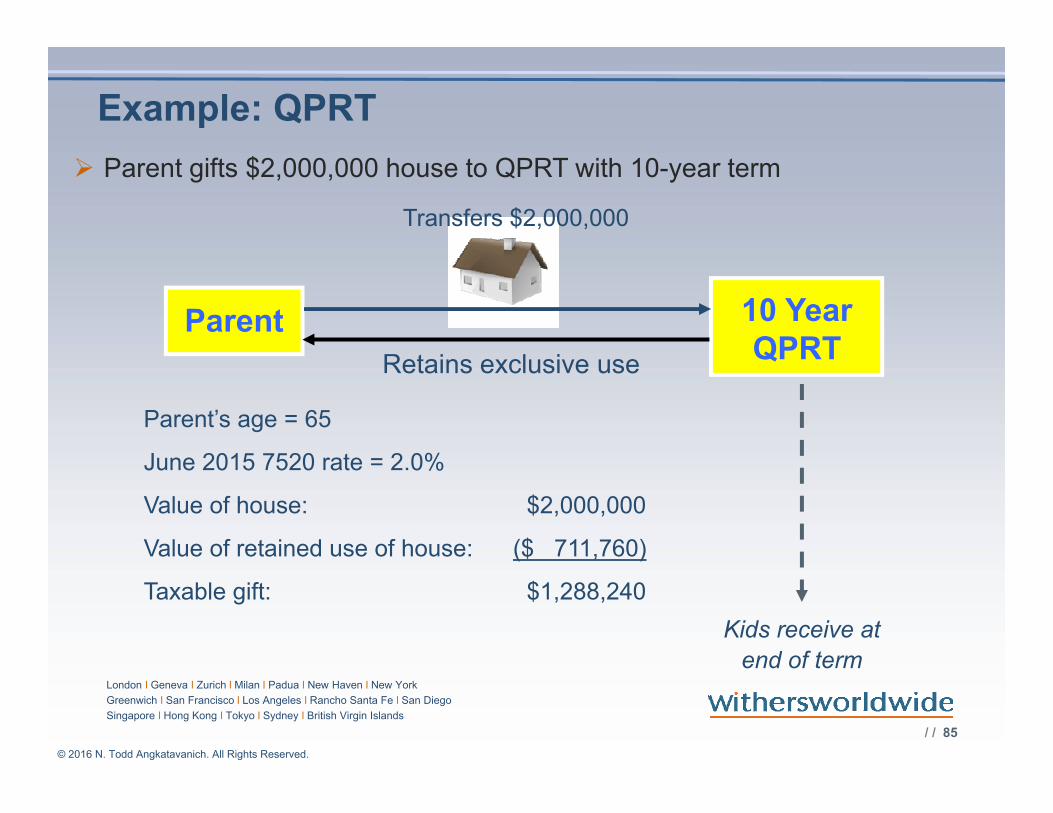

Example: QPRT

Parent gifts $2,000,000 house to QPRT with 10-year term

Parent’s age = 65

June 2015 7520 rate = 2.0%

Value of house: $2,000,000

Value of retained use of house: ($ 711,760)

Taxable gift: $1,288,240

Transfers $2,000,000

Parent 10 Year QPRT

Retains exclusive use

Kids receive at

end of term

/ / 86

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Continuing Trust After QPRT Terms:

Parent/Grantor may occupy

Must pay fair market rent to avoid

inclusion under Section 2036.

GST/ETIP issues must be considered if

continuation trust structured.

• Consider “electing out” of GST automatic

allocation

/ / 87

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

QPRT Technical Requirements:

Only one personal residence

Two QPRTs permitted at a time

“Personal residence” as defined in Section 121

Mortgage issue – additional gift

Sale by QPRT – QPRT must purchase replacement

residence within 2 years

Contribution of cash to purchase property through QPRT

permitted- must purchase within 3 months.

Prohibition against selling or transferring residence back

to the grantor or grantor’s spouse

/ / 88

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

QPRT Technical Requirements (cont’d):

Cash for improvements allowed if reasonably expected

Income distributed to term holder at least annually

May hold appurtenant structures and adjacent land

reasonably appropriate for residential purposes

Insurance proceeds can be held and reinvested in a new

personal residence within 2 years of receipt

No pre-payment permitted

More advantageous in high interest rate environments

/ / 89

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

N. Todd Angkatavanich is a partner at Withers Bergman, LLP, in the firm’s Greenwich, New Haven and New York offices. He serves as Regional Practice Group Co-Leader of the firm’s US Trust, Estate and Charities Practice Group. Todd is a Fellow of the American College of Trust and Estate Counsel and is a member of the Society of Trusts & Estates Practitioners. Todd has published articles in publications such as Trusts & Estates, ACTEC Law Journal, Estate Planning, BNA Tax Management, Probate & Property and other publications. He serves as Co-Chair of the Estate Planning & Taxation Committee of the Editorial Advisory Board of Trusts & Estates magazine, as well as a member of the Advisory Board for BNA/Tax Management Estates, Gifts and Trusts Journal. Todd is co-author of the pending BNA/Tax Management Portfolio No. 875, entitled “Wealth Planning with Hedge Fund and Private Equity Fund Interests.” A frequent speaker, Todd has given presentations for a number of organizations including the Heckerling Institute on Estate Planning, the Federal Tax Institute of New England, the Notre Dame Tax and Estate Planning Institute, the Washington State Bar Association Annual Estate Planning Seminar, the ABA Real Property, Trusts and Estates Section (Spring Symposia, Fall Joint Meetings and the joint ABA/New York Law School Skills Training Programs), BNA/Tax Management, as well as numerous estate planning councils, CPA societies and family office groups. Todd has been quoted in articles that have appeared in Barron's, Bloomberg Businessweek, The Boston Globe, The Philadelphia Inquirer, The Chicago Tribune, The Miami Herald, Forbes, MSN Money and other publications. Todd is Co-Chair of the ABA/RPTE Business Planning Group – Business Investment Entities, Partnerships, LLC’s and Corporations Committee and serves as a member of the ABA/RPTE Diversity Committee. He is a member of the Executive Committee of the Connecticut Bar Association, Estates and Probate Section, and on behalf of the Section also serves on the Planning Committee for the Federal Tax Institute of New England. He is the 2012 recipient of the award for “Private Client Lawyer of the Year” from Family Office Review. Todd has been included in The Best Lawyers in America® (for New York City, Greenwich and New Haven, Connecticut) and is also the recipient of the Best Lawyers® 2015 Trusts & Estates “Lawyer of the Year” award for New Haven, Connecticut. He has been rated AV Preeminent® by Martindale-Hubbell® Peer Review Ratings™ and has been listed in Who's Who Legal: Private Client. Todd received his B.A., in Economics, magna cum laude, from Fairleigh Dickinson University, his J.D., Tax Law Honors, from Rutgers University School of Law, Camden, his M.B.A. from Rutgers University Graduate School of Management, and his LL.M, in Taxation, from New York University School of Law.

Speaker BiographyN. Todd Angkatavanich, Esq., Withers Bergman LLP

/ / 90

© 2016 N. Todd Angkatavanich. All Rights Reserved.

London l Geneva l Zurich l Milan l Padua l New Haven l New York

Greenwich l San Francisco l Los Angeles l Rancho Santa Fe l San Diego

Singapore l Hong Kong l Tokyo l Sydney l British Virgin Islands

Marissa Dungey is an attorney at Withers Bergman, LLP, based in the firm’s Greenwich, Connecticut office. Her practice focuses on transfer tax planning, estate planning and trust structuring for wealthy individuals and their families. Marissa works with individuals and their advisors to develop and implement sophisticated planning strategies designed to minimize gift, estate and generation-skipping transfer taxes with trust planning optimized to achieve the individual's tax and non-tax goals, including creditor protection, charitable giving and income tax efficiency. Marissa regularly advises on planning with complex assets including interests in hedge funds, private equity funds and family businesses. She also advises on estate and trust administration matters, including adapting existing trusts to improve their tax efficiency and utility.Marissa frequently speaks to national audiences on a breadth of topics within wealth planning, including transfer taxes, income taxation of trusts, planning with fund interests and the gift and estate tax implications of Chapter 14 relevant to business interests.

Marissa earned her B.A. degree, cum laude, from New York University and her J.D. degree, magna cum laude, from Boston College Law School. Ms. Dungey is admitted to practice in Connecticut and New York. She is a member of the Connecticut Bar Association, Greenwich Bar Association, New York State Bar Association and American Bar Association. She serves on the Executive Committee of the Estates & Probate Section and the Pro Bono Committee of the Connecticut Bar Association and was named as a Trusts & Estates Fellow for the Real Property, Trust & Estate Law Section of the American Bar Association for 2014-2016 and an ACTEC Young Leader for 2016-2018.

Speaker BiographyMarissa Dungey, Esq., Withers Bergman LLP

4728130.1