Fall Accounting Conference · 2016-06-18 · Banking and trust products and services are provided...

138

Fall Accounting Conference Oct. 27, 2011 • Tallahassee

Transcript of Fall Accounting Conference · 2016-06-18 · Banking and trust products and services are provided...

Fall Accounting ConferenceOct. 27, 2011 • Tallahassee

Jennifer B. Barineau, ChairBarbara S. Withers, Vice Chair

Dr. Rhoda C. Icerman, Faculty Liaison

Gregory L. MillerChief Economist and Senior Vice President / SunTrust BanksAtlanta

Vicki H. Meyer, CPAOf Counsel / Thomas Howell Ferguson P.A.Tallahassee

Jennifer B. Barineau, CPA, CISA, CISSPAudit Supervisor / State of Florida Auditor GeneralTallahassee

Jane Flowers, CPAAudit Manager / State of Florida Auditor GeneralTallahassee

Frank M. Ryll, JrDirector, Global Outreach / Florida Chamber of CommerceTallahassee

Kathleen E. BrothersJonathan W. Davis

Denise DickinsChristopher W. Falk

Scott L. Ingram

Keith L. JonesAlan Jowers

Coman C. Leonard IIIDavid C. MojaDavid C. Reid

Tiffany ParkerVice President-Marketing / Capital City BankTallahasseeandSkip SmithSenior Vice President-Business Banking / Capital City BankandRamsay SimsVice President-Institutional Banking / Capital City BankTallahassee

David C. Moja, CPANational Director of Not-for-Profit Tax Services / CapinCrouse LLPOrlandoandGregory B. Capin, CPAPartner / CapinCrouse LLPLawrenceville GA

Paul N. Brown, CPADirector of Technical Services / Florida Institute of CPAsTallahassee

Economic Update

Gregory L. Miller

Chief Economist & Senior Vice President SunTrust Banks, Inc.

Gregory Miller is Chief Economist with SunTrust Banks, Inc. He completed his graduate and undergraduate Economics degrees at Florida State University and has been a practicing economist, forecaster, and teacher for over 25 years.

As SunTrust’s Chief Economist, Mr. Miller forecasts the national economy, particularly its affect on interest rates. He advises corporate and bank boards of directors as well as SunTrust clients. He sits on committees charged with interest rate setting, corporate investment, and benefits policy. He is a policy advisor for Wealth and Investment Management and Corporate Investment Banking groups.

Mr. Miller represents SunTrust in business media, including CNBC, Bloomberg News, Reuters, USA Today, Wall Street Journal, the Financial Times, TheStreet.com and many local news media platforms.

Prior to joining SunTrust, Mr. Miller was on the faculty of the College of Business Administration at the University of South Florida in Tampa. Before joining USF, Mr. Miller served two Florida Governors in Florida State Economist’s Office in Tallahassee.

In addition to his regular SunTrust duties, Mr. Miller is active in the National Association for Business Economics and the Financial Roundtable.

Mr. Miller is also a member and past-chair of the Economic Advisory Committee of the American Bankers Association – a national group of economists who meet with the Federal Reserve Board of Governors to discuss the economy and monetary policy.

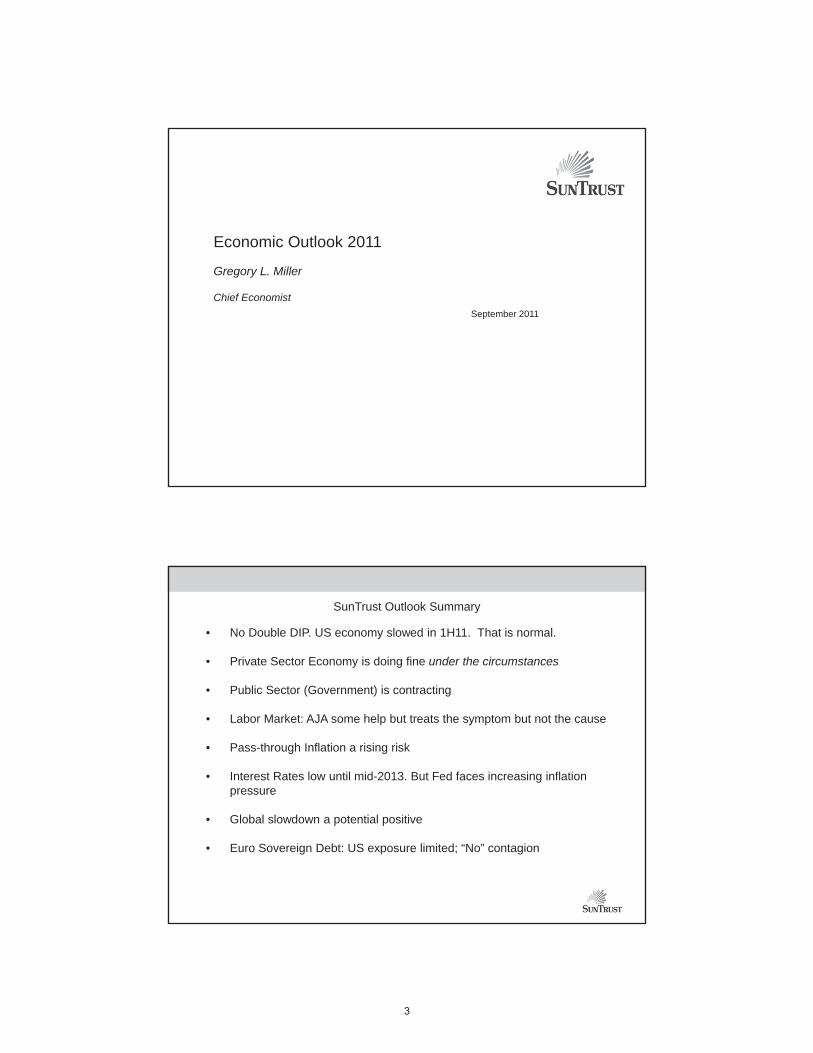

Economic Outlook 2011

Gregory L. Miller

Chief EconomistSeptember 2011

SunTrust Outlook Summary

• No Double DIP. US economy slowed in 1H11. That is normal.

• Private Sector Economy is doing fine under the circumstances

• Public Sector (Government) is contracting

• Labor Market: AJA some help but treats the symptom but not the cause

• Pass-through Inflation a rising risk

• Interest Rates low until mid-2013. But Fed faces increasing inflationpressure

• Global slowdown a potential positive

• Euro Sovereign Debt: US exposure limited; “No” contagion

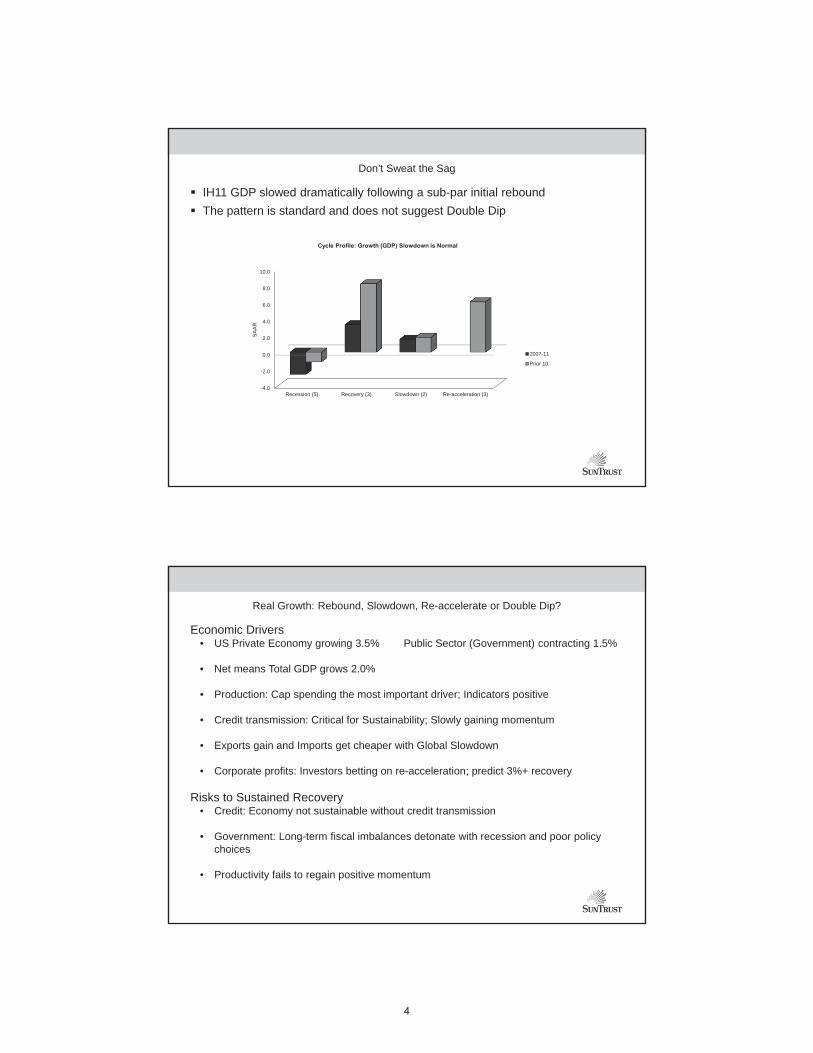

Don’t Sweat the Sag

IH11 GDP slowed dramatically following a sub-par initial reboundThe pattern is standard and does not suggest Double Dip

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

Recession (5) Recovery (3) Slowdown (2) Re-acceleration (3)

SA

AR

2007-11

Prior 10

Real Growth: Rebound, Slowdown, Re-accelerate or Double Dip?

Economic Drivers• US Private Economy growing 3.5% Public Sector (Government) contracting 1.5%

• Net means Total GDP grows 2.0%

• Production: Cap spending the most important driver; Indicators positive

• Credit transmission: Critical for Sustainability; Slowly gaining momentum

• Exports gain and Imports get cheaper with Global Slowdown

• Corporate profits: Investors betting on re-acceleration; predict 3%+ recovery

Risks to Sustained Recovery• Credit: Economy not sustainable without credit transmission

• Government: Long-term fiscal imbalances detonate with recession and poor policy choices

• Productivity fails to regain positive momentum

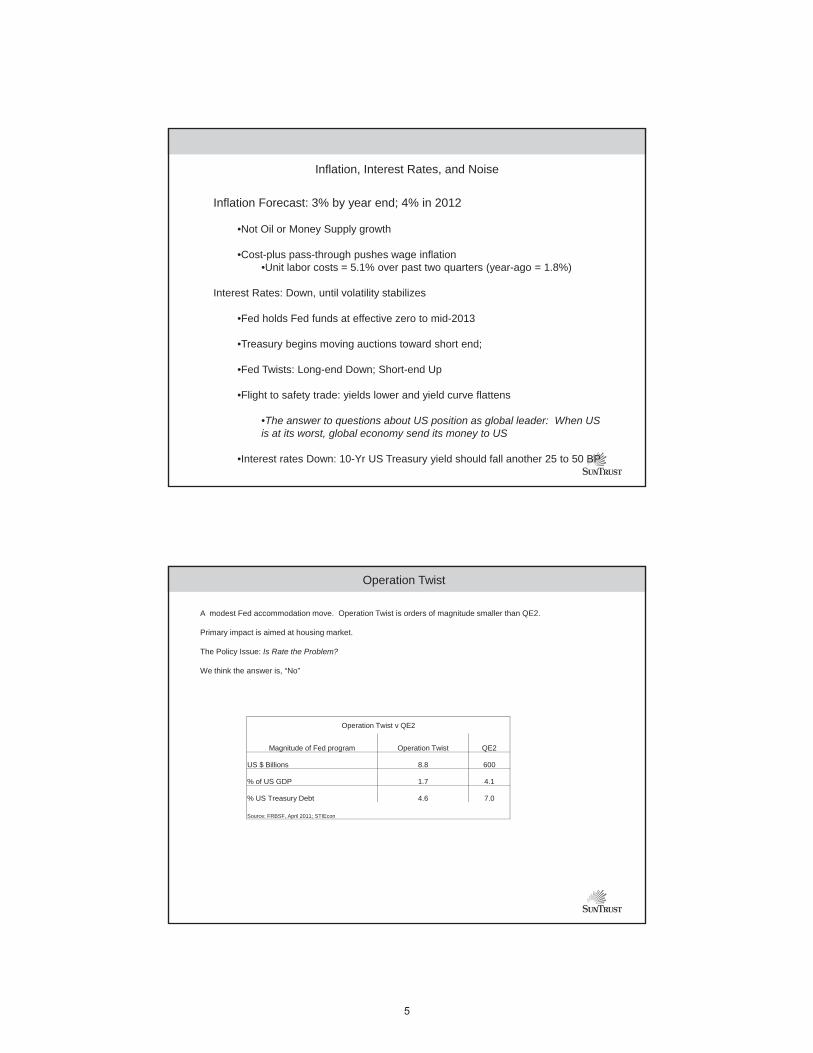

Inflation, Interest Rates, and Noise

Inflation Forecast: 3% by year end; 4% in 2012

•Not Oil or Money Supply growth

•Cost-plus pass-through pushes wage inflation •Unit labor costs = 5.1% over past two quarters (year-ago = 1.8%)

Interest Rates: Down, until volatility stabilizes

•Fed holds Fed funds at effective zero to mid-2013

•Treasury begins moving auctions toward short end;

•Fed Twists: Long-end Down; Short-end Up

•Flight to safety trade: yields lower and yield curve flattens

•The answer to questions about US position as global leader: When US is at its worst, global economy send its money to US

•Interest rates Down: 10-Yr US Treasury yield should fall another 25 to 50 BP

Operation Twist

A modest Fed accommodation move. Operation Twist is orders of magnitude smaller than QE2.

Primary impact is aimed at housing market.

The Policy Issue: Is Rate the Problem?

We think the answer is, “No”

Operation Twist v QE2

Magnitude of Fed program Operation Twist QE2

US $ Billions 8.8 600

% of US GDP 1.7 4.1

% US Treasury Debt 4.6 7.0

Source: FRBSF, April 2011; STIEcon

Operation Twist

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

FF 3 Mo 6 Mo 1 Yr 3 Yr 5 Yr 10 Yr

%

Twist '61

Jan 1961 Feb 1962 Jan 1965

0.00.51.01.52.02.53.03.54.04.5

FF 3 Mo 6 Mo 1 Yr 3 Yr 5 Yr 10 Yr

%

Pre Twist 2011

Jan 2008 Dec 2008 Aug 2011

Twist ‘61: Gold Standard; Currencies pegged to dollar; normal Housing Recovery; normal Government production

Twist 2011: Floating Currencies; Exports Helping; No Housing; Negative Government

“If stupidity got us into this, Why can’t it get us out?” --Will Rogers

•Politics and the Press

•If we elected the President based on the honesty of campaign promises, Abe Lincoln would still be in office

•One “Ad” is worth 40 editorials

•Soft data and emotion winning shouting match with hard data, reason, and corporate profits

•In fairness: American Jobs Act will do about 0.3 percentage points of good

American Jobs ActRome fell because it had a Senate; We have a Senate and a House

-- Will Rogers

• AJA ($447 Bill) has potential to boost labor market more than ARRA ($816 Bill)• ARRA funneled to State and local governments: No Profit Motive• AJA directed toward Private Employers and Employees: Profit Motive

Total AJATotal = $447b

Tax Cuts

Infrastrusture and localaid

Unemployment

175

65

50

20

40

60

80

100

120

140

160

180

200

Employee Payroll Employer Payroll Extend 100%expensing

$Billion

s

Tax CutsTotal = $245B

The Debt Limit: Only the Worst of Fools

The Debt Ceiling is an historic relic that has never produced its intended result

US Sovereign Debt did not get downgraded because we were near the debt ceilingwith a massive budget deficit …

… the downgrade occurred because political leadership has NO CLUE about how totreat those symptoms

Passed in the Second Liberty Bond Act of 1917 to restrain Federal spendingHas never produced any restraint on Federal Spending and none on State andLocal spendingIncreased 70 times since passage

The Solution: Repeal.

2H11 remains in rebound territory

Tornados and floods, Japan’s tsunami, earthquake, and nuclear crisis, and $4.00 gasoline each displacedsome measure economic activity in 1Q and 2Q11

Not everything about a “slowdown” is bad; some data series needed to slow down to avoid inflation

Consumer show little sign of slowdown and Household wealth recovery continues

Job gains now total 1.2 million since recovery began vs. an average -715 million eight month gains followingthe last two recession.

Credit measures continue to improve

Previous potentially inflationary growth rates in retail sales and industrial production suggest that the soft patchmay have a silver lining

Cost pass-through remains a risk

Slowing productivity risks wage reversal

Crude oil prices dropped 25% from $114/bbl to $85/bbl. Gasoline reverses to $3.85/ gallon to $3.40/ gallon

QE2 completion by the end of June.

Operation Twist should be modestly effective – a “small step” Fed alternative

Global risk keeps US Treasury yields low, but history says higher rates would be a positive

10

Financial Resources for All Your Personal and Business Needs

11

12

SunTrust Private Wealth Management is a marketing name used by SunTrust Banks, Inc.. Banking and trust products and services are provided bySunTrust Bank. Securities, insurance (including annuities and certain life insurance products) and other investment products and services areoffered by SunTrust Investment Services, Inc., a SEC registered broker/dealer and a member of the FINRA and SIPC. Other insurance products andservices are offered by SunTrust Insurance Services, Inc., a licensed insurance agency. Investment advisory products and services are offered bySunTrust Investment Services, Inc. and GenSpring Family Offices, LLC (f/k/a Asset Management Advisors, L.L.C.), investment advisers registeredwith the SEC.

SunTrust Investment Services, Inc., SunTrust Bank, their affiliates, and the directors, officers, employees and agents of SunTrust InvestmentServices, Inc., SunTrust Bank and their affiliates (collectively, “SunTrust”) are not permitted to give legal or tax advice. While SunTrust can assistclients in the areas of estate and financial planning, only an attorney can draft legal documents and provide legal services and advice. Clients ofSunTrust Investment Services, Inc., SunTrust Bank and their affiliates should consult with their legal and tax advisors prior to entering into anyfinancial transaction or estate plan.

Securities and Insurance Products and Services:

• Are not FDIC or any other Government Agency Insured

• Are not Bank Guaranteed

• May Lose Value

13

Asset Allocation does not assure a profit or protect against loss in declining financial markets.

Emerging Markets: Investing in the securities of such companies and countries involves certain considerations not usually associated with investingin developed countries, including unstable political and economic conditions, adverse geopolitical developments, price volatility, lack of liquidity, andfluctuations in currency exchange rates.

Fixed Income Securities are subject to interest rate risk, credit risk, prepayment risk, market risk, and reinvestment risk. Fixed Income Securities, ifheld to maturity, may provide a fixed rate of return and a fixed principal value. Fixed Income Securities prices fluctuate and when redeemed, may beworth more or less than their original cost.

Hedge funds may involve a high degree of risk, often engage in leveraging and other speculative investment practices that may increase the risk ofinvestment loss, can be highly illiquid, are not required to provide periodic pricing or valuation information to investors, may involve complex taxstructures and delays in distributing important tax information, are not subject to the same regulatory requirements as mutual funds often chargehigh fees which may offset any trading profits, and in many cases the underlying investments are not transparent and are known only to theinvestment manager.

High Yield Fixed Income Investments, also known as junk bonds, are considered speculative, involve greater risk of default and tend to be morevolatile than investment grade fixed income securities.

International investing entails greater risk, as well as greater potential rewards compared to U.S. investing. These risks include potential economicuncertainties of foreign countries as well as the risk of currency fluctuations. These risks are magnified in emerging market countries, since thesecountries may have relatively unstable governments and less established markets and economies.

Investing in smaller companies involves greater risks not associated with investing in more established companies, such as business risk, significantstock price fluctuations, and illiquidity.

Managed Futures and commodity investing involve a high degree of risk and are not suitable for all investors. Investors could lose a substantialamount of money in a very short period of time. The amount you may lose is potentially unlimited and can exceed the amount you originally depositwith your broker. This is because trading security futures is highly leveraged, with a relatively small amount of money controlling assets having amuch greater value. Investors who are uncomfortable with this level of risk should not trade managed futures or commodities.

Real Estate Investments are subject to special risks, including interest rate and property value fluctuations, as well as risks related to generaleconomic conditions. Because of their narrow focus, sector investments tend to be more volatile than investments that diversify across many sectorsand companies.

Federal Tax Update

Vicki H. Meyer, CPA

Of Counsel Thomas Howell Ferguson, PA

Vicki is Of Counsel with Thomas Howell Ferguson, PA in Tallahassee, Florida where she brings over 30 years of experience in tax consulting, transactional analysis, and compliance as it pertains to corporations, partnerships and high net-worth individuals in a variety of industries.

Vicki is also the owner of Meyer Consulting, PLLC, which provides technical support and tax quality control for publicly traded corporations as well as other CPA firms throughout the state.

Vicki has authored several articles relating to tax practice and technical issues and frequently instructs continuing education courses.

Vicki is a Certified Public Accountant licensed in the State of Florida. She is a current member of the American Institute of Certified Public Accountants’ Partnership Technical Resource Panel, as well as a member of the Florida Institute’s Federal Taxation Committee, where she serves as the Chair of the Legislative Response Committee. She is also an AICPA ambassador for Financial Literacy.

J U L Y 2 0 1 0 – J U N E 2 0 1 1

Federal Tax Update

New Legislation

Education Jobs and Medicaid Assistance Act (H.R. 1586, P.L. 111-226,8/10/2010).Small Business Jobs Act of 2010 (“SBJA”) (Small Business Lending Funding Act, H.R. 5297, P.L. 111-240, 9/27/10).The Tax Relief Act of 2010 (The Tax Relief, Unemployment Insurance

Reauthorization and Job Creation Act of 2010, H.R. 4853, P.L. 111-312, 12/17/2010).1099 Act (Comprehensive1099 Taxpayer Protection and Repayment of Exchange Subsidy Overpayments Act of 2011, H.R. 4, P.L. 112-9, 4/14/2011).

Education Jobs and Medicaid Assistance Act

New code section 909(a), preventing splitting of foreign tax credits from income.Foreign tax credit denied in covered asset acquisitions.Separate application of FTC to items resourced under tax treaties.Limits on use of Code Sec 956 for FTC planning (“Hopscotch” Rule).E&P isn’t deemed distributed in certain redemptions by

foreign subsidiaries.Modification of affiliation rules for allocating interest expense.Repeal of 80/20 company rules.Suspension of 3-Year statute for failure to disclose or provide information returns.Advanced payment for EIC is eliminated after 2010.

Small Business Jobs Act of 2010

Increased Sec 179 expenses (500K wit 2M phase-out and qualified real property – 250K.Revived 50% bonus depreciation.Cell phones no longer listed.Increased start up to 10K, wit 60K phase out threshold.Credits can offset AMT. Health insurance for

taxpayer and is family are deductible for SE tax.Temporary reduction in S corporations built-in gain period.Information reporting requirement for rental income from realty.Increase information return penalties.New sourcing rules for guarantees.

The Tax Relief Act of 2010

Extends for two years the Bush-era tax cuts.Retains for two years favorable tax rates for long-term capital gains and qualified dividends.Provides significant estate and gift tax relief, and includes a two-year AMT “patch”.100% first-year write off of qualifying property placed in service after Sept. 8, 2010 and before Jan. 1,

2012.Payroll/self-employmenttax cut of two percentage points for 2011 for employees and self-employed individuals .Extends a host of expired and expiring tax breaks for businesses and individuals as well as a number of key disaster relief provisions.

1099 Act

Repeals expanded Form 1099 information reporting requirements mandated under health care legislation.Repeals Form 1099 reporting requirements, as enacted as part of the Small Business Jobs Act, on taxpayers who receive rental income.Did not repeal increased penalties for information reporting.

Individuals

Gates, 135 TC No 1Rebuilt home on existing land did not qualify for Code Sec. 121 Home Exclusion.Did not matter that land/property on which taxpayers' reconstructed home was situated had been site of their original residence or that original residence would have qualified for exclusion; rather, exclusion could only apply where home that is sold is itself principal residence

Rev. Rul. 2010-25, 2010-44 IRB Debt on home purchase can be home equity debt as well as acquisition debt.Home 1.5M, 300K down, original acquisition indebtedness 1.2M$1M is acquisition indebtedness.

Individuals

$100K is treated as home equity indebtedness.IRS will not follow TC which said home equity debt could not be acquisition debt.

Moss, 135 TC No 18"On call" time didn't count towards qualification as real estate professional under PAL rules .

Rev. Proc. 2011-34PALS – allows certain taxpayers to make late election to treat all interests in real estate activities as a single rental real estate activity by filing amended returns.

Individuals

Mayo Foundation for Medical Education and Research, et al. v. U.S. (S Ct 1/11/2011) 107 AFTR 2d ¶ 2011-312

Medical residents working full-time were employees for FICA purposes.Interpretive IRS regs are entitled to heightened deference (Chevron standard upheld).Legislative regs – code authorizes Treasury to write.Interpretive regs – under general grant of authority to provide guidance.Conclusion: IRS gets to “fill in the blanks” without legislative authority.

Individuals

Shao, TC Memo 2010-189 Inexperienced investor avoids substantial underpayment penalty for unreported disguised sale.

Hall, (2010) 135 TC No. 19 Tax Court once again invalidates reg placing time limit on request for equitable innocent spouse relief.

PLR 201043009 through PLR 201043014 Squeezed out shareholders qualify for ordinary loss treatment despite ongoing suit.

T.D. 9514, 2/4/11Election to treat self created musical work as exchange of capital asset.

Code Sections

§108 – Cancellation of DebtT.D. 9497, 08/11/2010

COD income – Corps.

T.D. 9498, 08/11/2010 § 108(i) deferral for partnership and S Corporations.

Prop. Reg. § 1.108-9 Proposed regs explain § 108 COD exclusion for grantor trusts and disregarded entities.

Code Sections

§162 – Trade or Business Expenses

Capitalization vs. Repairs Audit Technique Guide

New ATG focuses on capitalization-to-repair accounting method changes.

§199 – Domestic Manufacturing

Gibson & Associates, Inc. (2011), 136 TC No. 10

Taxpayer's infrastructure construction activities qualified for the DPAD.

Code Sections

§263(a) – Capitalized CostsRev. Proc. 2011-29, 2011-18 IRB

70% of success based fees deductible under new safe harbor election.

§263A - Unicap PLR 201030025

Packing material costs weren't from "pick and pack" activities and must be capitalized.

Rev. Proc. 2010-44, 2010-49 IRB IRS provided two new UNICAP safe harbors for motor vehicle dealerships.

Code Sections

§263A - Sales Based RoyaltiesAOD 2011-01,02/08/2011

IRS won't acquiesce in 2nd Circuit decision allowing deduction for trademark licensing costs (Robinson Knife) - consider costs Code Sec. 471 costs

LMSB -04-0910-026, Field Directive dated 3/1/2011

Vendor allowances are a purchase price adjustment under Code Sec. 471.

Prop. Reg. 149335-08, 12/16/2010Allocate sales based royalties and vendor allowances to property sold during year, not ending inventory

Code Sections

§460 – Percentage CompletionChief Counsel Advice 201046009

IRS explains calculation of look-back interest due the taxpayer under PCM method of accounting.

Chief Counsel Advice 201111006 IRS clarifies treatment of pre-contract R&E costs under the percentage of completion method.

SBJABonus depreciation in 2010 is not taken into account as a cost, avoids acceleration of income.

Accounting Methods

§446 – Change in Accounting MethodsBosamia, TC Memo 2010-218

Code Sec. 481 adjustment can be made for closed years.

PLR 201035016 Recharacterization of activity from nonpassive to passive wasn’t accounting method change.

Rev. Proc. 2011-14Successor to Rev. Proc. 2008-52. There are significant changes.

Modified Debt Instruments

T.D. 9513, Reg. § 1.1001-3, 01/06/2011 Clarify effect of issuer's worsened fiscal condition on a

modified debt instrument’s recharacterization as an instrument or a property right that is not debt.

New regs state that financial condition is not taken into account unless there is a substitution of a new obligor or the addition or deletion of a co-obligor.

§1031 Like Kind Exchanges

Ralph E. Crandall, Jr. and Dene E. Dulin, TC Summary Opinion 2011-14

Failure to use qualified escrow account resulted in taxable gain.Escrow account with bank did not restrict taxpayer’s access to and use of the funds.

Ocmulgee Fields, Inc., (CA 11 8/13/2010) 106 AFTR 2d ¶2010-5198

The Eleventh Circuit affirms Tax Court decision.Cannot avoid the Code Sec. 1031(f) like-kind-exchange related-party rule by interposing a qualified intermediary (QI).Courts continue to disallow basis shifts between related parties.

Statute of Limitations – Judicial Deference to Temporary Regs

§6501 – Basis OverstatementTC rules, in Bakersfield Energy Partners, LP,based on a Supreme Court decision in Colony,

that basis overstatement was not an ”omission of income” for purposes of extending the 3 statute to 6 years under Code Sec. 6501.

IRS responds with temporary regs (T.D. 9511, 12/14/2010)

Basis overstatement IS an omission of income and temporary regulations can be retroactively applied to closed years (up to 6 year limitation period).

Tax Court – IS NOT AN OMISSION OF INCOME Carpenter Family Investments, LLC, (2011) 136 TC No. 17.

Statute of Limitations – Judicial Deference to Temporary Regs

Circuit Courts of Appeal – IS TOO

Seventh Circuit: Beard v. Comm., (CA 7 01/26/2011) 107 AFTR 2d ¶ 2011-372. Grapevine Imports LT.D.. v. U.S., (CA FC 03/11/2011) 107 AFTR 2d ¶ 2011-564.

Circuit Courts of Appeal – IS NOT

Fifth Circuit: Daniel S. Burks, Tax Matters Partner v. U.S.,(CA 5 2/9/2011) 107 AFTR 2d ¶ 2011-447.Fourth Circuit: Home Concrete & Supply, LLC v. U.S., (CA 4 2/7/2011) 107 AFTR 2d ¶ 2011-425.Tenth Circuit: Salman Ranch, LT.D.; Frances Koenig, Tax Matters Partner, (CA 10 05/31/2011) 107 AFTR 2d ¶ 2011-886.

Statute of Limitations

Issue is Judicial Deference to Temporary Regs

Chief Counsel Advice 201118020 Amended return showing “corrected income” will not avoid 6-year assessment period. IRS will look to original returns.

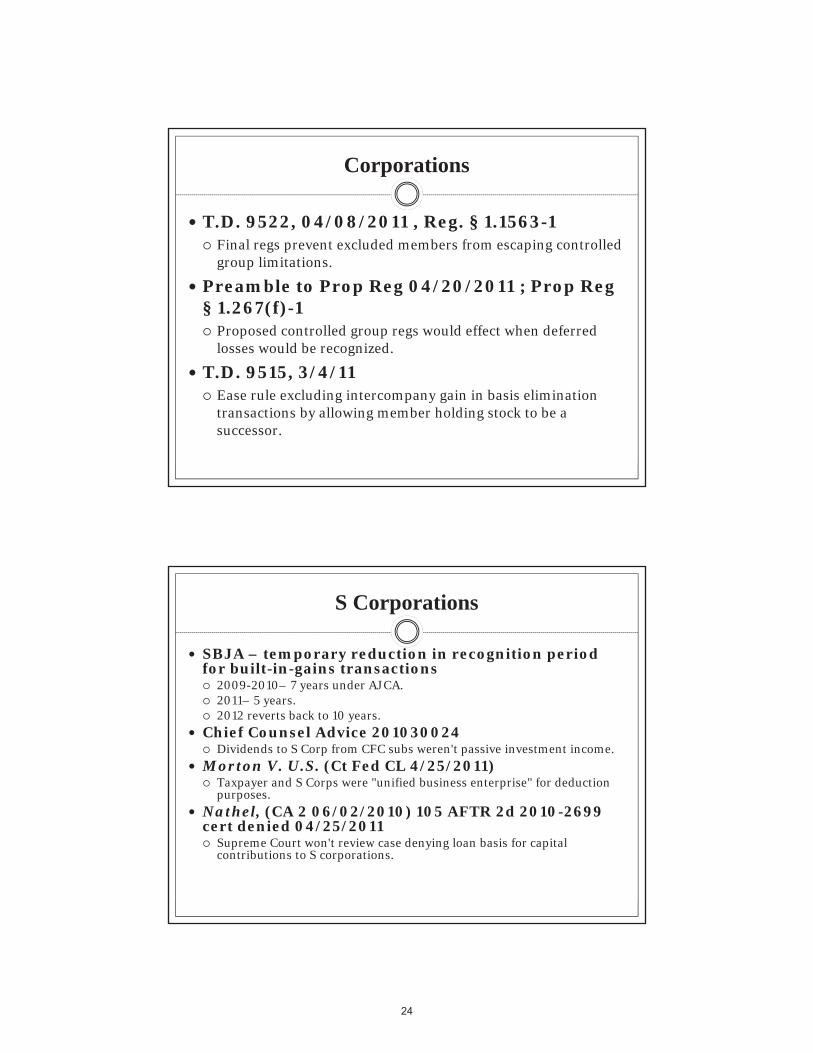

Corporations

Ann. 2010-75, 2010-41 IRB, Final Schedule UTP

Includes five-year phase in of the reporting requirements based on a corporation’s asset size.No reporting of: maximum tax adjustment, concise description of the position, or administrative practice positions.

Media Space, Inc., 135 TC No 21Partial taxpayer win for corporation’s payment to preferred shareholders to forebear redemption.To extent not capitalized, deductable under Code Sec. 162.

Corporations

Notice 2010-58, 2010-37 IRB Longer NOL carryback options.

Notice 2011-18Corporations won't file information returns for organizational actions before 2012.

PLR 201027035 Discount prepayment of corporation's contingent obligation didn't result in COD income.

Corporations

PLR 201113003Transactions to divide corp.’s business among feuding shareholders upheld as tax free (divisive D).

Rev. Proc. 2011-35Procedures that an acquiring corporation may use to establish its basis in stock of another corporation (target) when it acquires the target stock in a transferred basis transaction.

T.D. 9510, 12/13/2010Final regs under Code Sec. 6012 for uncertain tax positions.

Corporations

T.D. 9522, 04/08/2011 , Reg. § 1.1563-1 Final regs prevent excluded members from escaping controlled group limitations.

Preamble to Prop Reg 04/20/2011 ; Prop Reg § 1.267(f)-1

Proposed controlled group regs would effect when deferred losses would be recognized.

T.D. 9515, 3/4/11Ease rule excluding intercompany gain in basis elimination transactions by allowing member holding stock to be a successor.

S Corporations

SBJA – temporary reduction in recognition period for built-in-gains transactions

2009-2010– 7 years under AJCA.2011– 5 years.2012 reverts back to 10 years.

Chief Counsel Advice 201030024 Dividends to S Corp from CFC subs weren't passive investment income.

Morton V. U.S. (Ct Fed CL 4/25/2011)Taxpayer and S Corps were "unified business enterprise" for deduction purposes.

Nathel, (CA 2 06/02/2010) 105 AFTR 2d 2010-2699 cert denied 04/25/2011

Supreme Court won't review case denying loan basis for capital contributions to S corporations.

S Corporations

Nestle Purina Petcare Co. v. Comm. (CA 8 2/9/2010), 105 AFTR 2d 2010-912 , cert denied 10/4/2010

Supreme Court won’t review holding that ESOP redemption payments are nondeductible.

PLR 201115016S corporation's sale of certain assets structured as type F reorganization upheld.

Ralph's Grocery Co. and Subsidiaries, TC Memo 2011-25

Bankrupt parent's and holding company's Code Sec. 338(h)(10) election upheld as valid.

Partnerships

Canal Corp., 135 TC No. 9, 8/4/2010First case litigating anti-abuse rule of Code Sec. 752.TC ruled that risk of loss was so limited that arrangement only gave the appearance of economic risk of loss, when in substance, such risk was lacking, no debt basis existed.Therefore exception to disguised sales rules for debt financed distributions did not apply, some or all of the distribution to be recasted as a taxable sale of assets.KICKER – Taxpayer assessed Code Sec. 6662(b)(2) accuracy related penalty. Could not rely on PWC tax opinion since PWC was not independent (they were also taxpayer’s auditors, and financially tied to taxpayer).

Partnerships

(REG-119921-09, 9/14/10) - Proposed regs on the treatment of Series LLCs

Example:LLC is a series organization that has 3 members, (1,2,and 3).LLC establishes 2 series (A and B) pursuant to a series state statute.Under general tax principles, member 1 and 2 are the owners of series A, and member 3 is the owner of series B. Series A and B are treated as an entity formed under local law.Series A is a partnership (2 members).Series B is a disregarded entity.

Partnerships – State Tax Credits

Historic Boardwalk Hall, LLC, (2011) 136 TC No. 1

Rehab credits had economic substance.

Tempel, 136 TC No 15Transferable state tax credits on conservation easement property were capital assets, not contract rights generating ordinary income.Taxpayer could not use land as basis for a state tax credit..

Virginia Historic Tax Credit Fund 2001 LP, (CA 4 03/29/2011) 107 AFTR 2d ¶ 2011-633

Partnership contributions for allocations of state tax credits were disguised sales.

Partnerships

PLR 201028016 Partnership can use full netting approach for aggregating built-in gains & losses when making reverse allocations .

Renkemeyer, Campbell, and Weaver, LLP, et al. v. Commissioner, 136 T.C. No. 7 (2011).

What constitutes a limited partner entitled to the exception to the self-employment tax provided under Section 1402(a)(13)? Limited partners are akin to passive investors in that they lack management powers and their distributive shares arise as a return on invested capital and constitute investment-type earnings.In contrast, the three law partners of the LLP enjoyed limited

liability protection, had management powers and performed services that generated the LLP's income. Accordingly, the court concluded that the investment partners of the LLP were not the same as limited partners.

International

IRM 8.11.5, International Penalties, 08/27/2010IRS allows Appeals to review assessed international penalties before taxpayer is required to pay.

IRS Memorandum dated 3/1/2011IRS details penalty framework for the second offshore voluntary disclosure initiative (OVDI).Runs through 8/31/2011.In a new frequently asked question (FAQ) released June 2, IRS indicated that deadline is postponed for up to 90 days after the Aug. 31, 2011, deadline. Higher penalties (25%), longer reporting required (8 vs. 6 years).

International

Notice 2010-41Upcoming regs will classify certain domestic partnerships as foreign solely for purpose of identifying which U.S. shareholder is required to include amounts in gross income under Code Sec. 951(a).Regs will treat domestic partnership as foreign under certain narrow conditions.The regulations to be issued will provide similar results in the case of tiered-partnership structures.

International

Notice 2010-60Withholdable payments to foreign financial institutions - preliminary guidance.

Notice 2010-92, 2010-52 IRB Guidance on new law preventing splitting of foreign tax credits from income, specifically for pre-2011 taxes.

Notice 2011-31Information with respect to foreign financial assets - guidance for 2010 returns.For returns filed on or after March 28, a taxpayer should reference only the new final regs.

Notice 2011-34, 2011-19 IRBIRS releases ne FATCA guidance for foreign financial institutions and other foreign entities.

International

AOD 2010-005IRS won't acquiesce in Veritas transfer pricing decision.Veritas used comparable uncontrolled transaction (CUT) method of pricing for a buy-in from foreign sub for pre-existing intangibles.Service wants “all-in” intangibles, including R&D, marketing,distribution channels, customer lists, etc.

FCEN 31 CFR Part 1010 RIN 1506-AB08Final rules clarifying FBAR reporting requirements.

International

Rev. Proc. 2010-32Foreign entity classification - "check-the-box" election relief -incorrect number of owners.

T.D. 9521, 04/06/2011Final regs reflect AJCA's reduction of foreign tax credit limitation categories.

T.D. 9526, 05/17/2011 , Reg. § 1.367(a)-3 , Reg. § 1.367(b)0

Final regs curb abuses in triangular reorganizations involving foreign corporations “Killer Bs”, largely adopting 2008 proposed regs.

Estates and Trusts

Baccei, 107 AFTR 2d 2011-898 (CA-9, 2011)

Incomplete extension request resulted in late payment penalty and interest to taxpayer.CPA failed to complete Part III, which asked for the extension date and whether an extension of time to pay was requested.

Estate of Axel O. Adler,TC Memo 2011-28

Estate not entitled to fractional interest discount for land divided among children.

Estate of Erma V. Jorgensen, (CA 9 5/4/2011) 107 AFTR 2d ¶ 2011-793

Ninth Circuit upholds inclusion of securities transferred to FLP in decedent's estate.

Estate of Gertrude Saunders, (2011) 136 TC No. 18

Estate couldn't deduct pending litigation claim for malpractice.

Estates and Trusts

Estate of Louise Blyth Timken v. U.S., (CA 6 04/02/2010) 105 AFTR 2d ¶ 2010-702 cert denied 1/10/2011.

Supreme Court won't review decision that trust transfers weren't grandfathered from GST tax.

IR 2011-33New deadline for electing modified carryover basis rules for 2010 decedents.

Notice 2011-37, 2011-20 IRB Bundled fiduciary fees are fully deductible until final regs are issued.

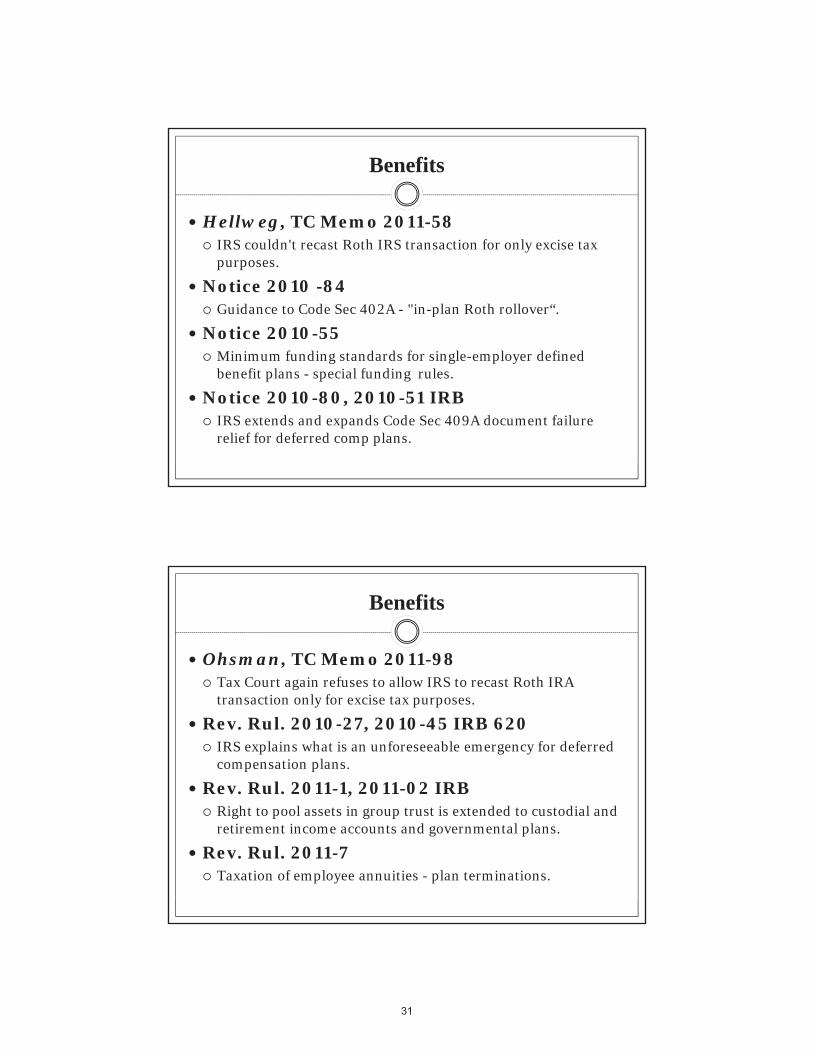

Benefits

Hellweg, TC Memo 2011-58 IRS couldn't recast Roth IRS transaction for only excise tax purposes.

Notice 2010 -84Guidance to Code Sec 402A - "in-plan Roth rollover“.

Notice 2010-55Minimum funding standards for single-employer defined benefit plans - special funding rules.

Notice 2010-80, 2010-51 IRB IRS extends and expands Code Sec 409A document failure relief for deferred comp plans.

Benefits

Ohsman, TC Memo 2011-98 Tax Court again refuses to allow IRS to recast Roth IRA transaction only for excise tax purposes.

Rev. Rul. 2010-27, 2010-45 IRB 620 IRS explains what is an unforeseeable emergency for deferred compensation plans.

Rev. Rul. 2011-1, 2011-02 IRB Right to pool assets in group trust is extended to custodial and retirement income accounts and governmental plans.

Rev. Rul. 2011-7Taxation of employee annuities - plan terminations.

Health Care

Notice 2010-59Contributions by employer to accident and health plans -reimbursements restricted to prescribed drugs and insulin.

Notice 2010-69, 2010-44 IRB , IR 2010-103 Employer's reporting of health insurance coverage on Forms W-2 is optional for 2011.

Notice 2010-82Additional guidance on health insurance credit under Code Sec. 45R.

Health Care

T.D. 9506, 11/15/2010; Reg. §54.9815-1251T

Amended regs allow health plans to change insurers without losing "grandfathered" status.

Notice 2011-5, 2011-3 IRB ; IR 2010-128

IRS modifies early guidance on FSA and HRA debit cards for OTC drugs.

Notice 2011-28, 2011-16 IRB ; IR 2011-31

IRS further delays health insurance coverage information reporting for small employers.

Notice 2011-59Contributions by employer to accident and health plans - reimbursements restricted to prescribed drugs and insulin.

Not For Profit

Ocean Pines Association, 135 TC No. 13 UBTI - beach club and parking lot operations are not substantially related to association’s exempt purpose.

Excise Tax

James Zadroga 9/11 Health and Compensation Act of 2010” (the Zadroga Act), new Code Sec. 5000C

New excise tax on foreign procurement payments on certain foreign persons providing goods and services to the federal government.

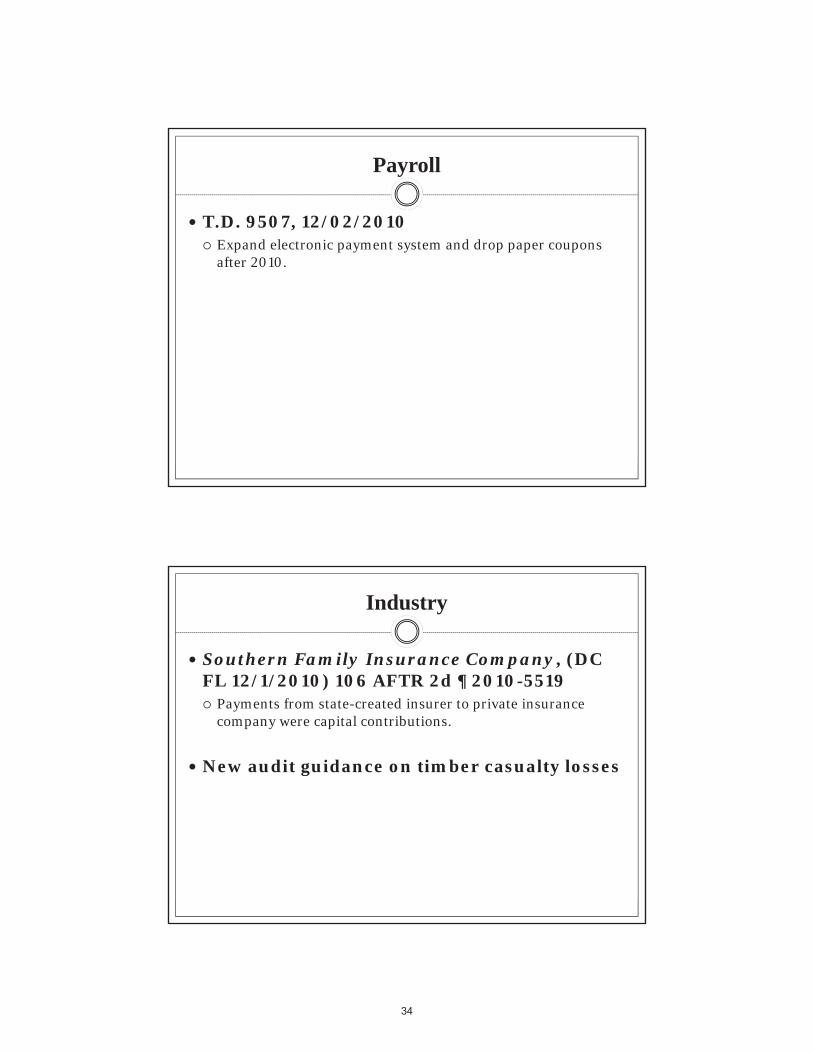

Payroll

T.D. 9507, 12/02/2010 Expand electronic payment system and drop paper coupons after 2010.

Industry

Southern Family Insurance Company, (DC FL 12/1/2010) 106 AFTR 2d ¶ 2010-5519

Payments from state-created insurer to private insurance company were capital contributions.

New audit guidance on timber casualty losses

IRS

IR-2010-88Service announces realignment of LMSB to LBI (Large Business & International).

Ann. 2011-5, 2011-4 IRB Fast Track Settlement extended to SB/SE.

IR-2011-32Compliance Assurance Program for large corporate taxpayers isexpanded and made permanent.

Notice 2011-38Pilot program - truncation of payee numbers by information return filers.

Revenue Exams -Quickbooks Soft File

More years than exam periodContains others information that could be considered private, confidential and beyond what is pertinent to the audit.

Circular 230

T.D. 9527, 5/31/2011, Final regs

Codifies registered tax return preparer (RTRP) rules.

Modifies standards for all practitioners to be consistent with the civil penaltystandards under Code Sec. 6694 for tax return preparers.

RTRPs cannot use the term “certified”.

Ads promoting RTRP designation must state “The IRS does not endorse any particular individual tax return preparer. For more information…”

Tax preparers cannot use a standard less than REASONABLE BASIS when signing returns or claims for refund (can no longer use non-frivolous with disclosure).

Expands definition of disreputable conduct to include practicing without a PTIN or not filing electronically where required.

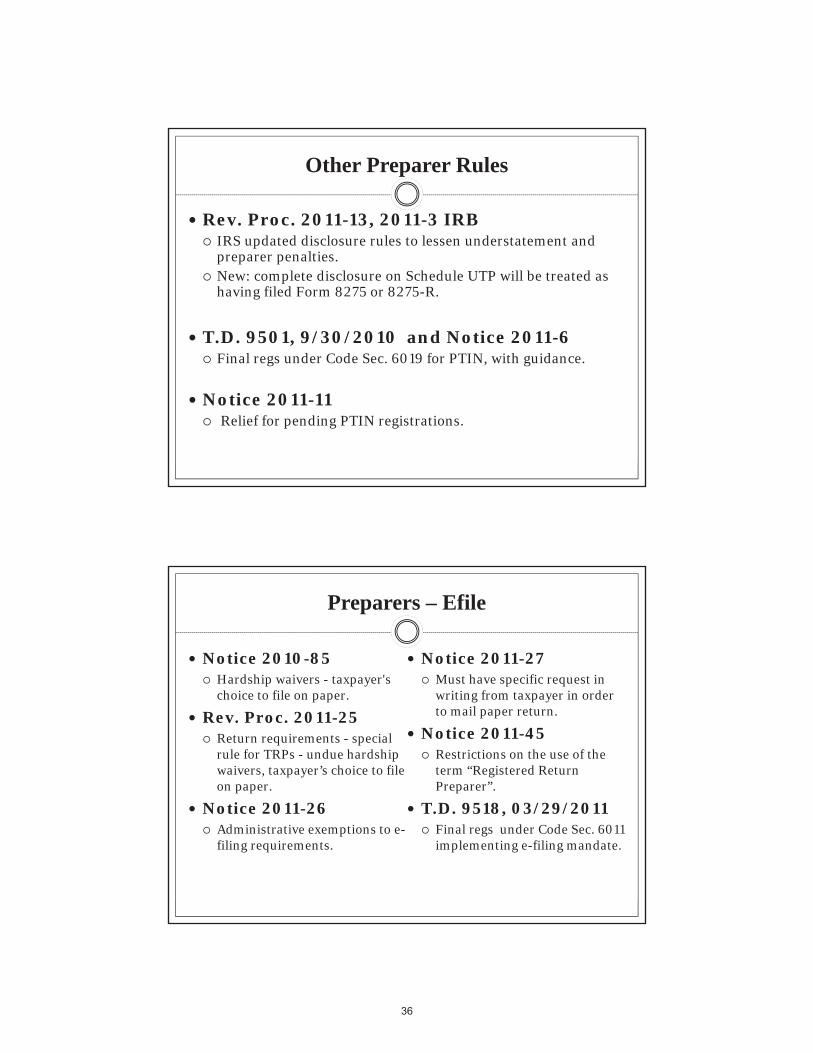

Other Preparer Rules

Rev. Proc. 2011-13, 2011-3 IRB IRS updated disclosure rules to lessen understatement and preparer penalties.New: complete disclosure on Schedule UTP will be treated as having filed Form 8275 or 8275-R.

T.D. 9501, 9/30/2010 and Notice 2011-6Final regs under Code Sec. 6019 for PTIN, with guidance.

Notice 2011-11Relief for pending PTIN registrations.

Preparers – Efile

Notice 2010-85Hardship waivers - taxpayer's choice to file on paper.

Rev. Proc. 2011-25Return requirements - special rule for TRPs - undue hardship waivers, taxpayer’s choice to file on paper.

Notice 2011-26Administrative exemptions to e-filing requirements.

Notice 2011-27Must have specific request in writing from taxpayer in order to mail paper return.

Notice 2011-45Restrictions on the use of the term “Registered Return Preparer”.

T.D. 9518, 03/29/2011Final regs under Code Sec. 6011 implementing e-filing mandate.

Taxpayer Errors

Chief Counsel Advice 201052003 Sec 7502's “timely-mailed is timely filed rule” inapplicable to amended return showing increased tax due. Must be received by statute due date.

Deutsche Bank Ag v. U.S., Ct Fed Cl, 106 AFTR 2d 2010-6922

IRS denied interest income (over $2M) on overpayment due to Taxpayer’s failure to attach Form 8805 and 1042-S to Form 1120-F, when filed. Tax return deemed non-processible under Code Sec. 6611.

Weekend Warriors Trailers, Inc., et al, TC Memo 2011-105

Court denied deduction for unsubstantiated "management fees" paid to related entity.

Other

FedEx Ground Package System, Inc., (DC IN 12/13/2010)

FedEx drivers seeking employee status (for benefits) lose in multidistrict litigation.They are held to be independent contractors.

JCX-55-10 (December 10, 2010

JCT sheds light on what is considered qualified retail improvement property.Must be a store retailer under NAICS sub-sectors 441-453. Professional services and entertainment property do not qualify.

Notice 2010-62, 2010-40 IRB

Interim guidance on codification of economic substance doctrine. IRS will continue to rely on relevant case law and apply in the same fashion as it did before enactment of Code Sec. 7701(o).

Notice 2010-91, 2010-52 IRB

3% withholding on government payments by payment card delayed until after 2012.

Other

PLR 201034004 LIFO and non-LIFO financial statement disclosures don't violate LIFO conformity rule.

PLR 201111004Disaster-affected business allowed to defer gain on involuntary converted inventory. Although inventory is not held for productive use in a trade or business, there is no explicit exclusion of inventory under Code Sec. 1033(h)(2).

Rev. Rul. 2011-9Exception to loss of interest deduction on insurance with inside buildup doesn’t carry over in an tax-free exchange.

Other

Ross B. Thomann, TC Memo 2010-241

Taxpayers couldn't expense leased assets due to failure to prove terms of oral leases.

T.D. 9524, 05/06/2011Final regs defer effective date of 3% governmental withholding requirement.

T.D. 9504, 10/12/2010Address basis and character reporting rules for securities acquired after 2010.

U.S. v. Mark Richey,(CA 9 1/21/2011) 107 AFTR 2d ¶2011-376

Appellate court refuses to quash IRS summons for appraiser's work files.

Boltar LLC, (2011) 136 TC No. 14

Legal standards for appraisal experts.

The New Yellow Book: SameColor, Revised Standards

Jennifer B. Barineau, CPA, CISA, CISSP

Quality Control Audit Supervisor Florida Auditor General’s Office

Jennifer has been with the Florida Auditor General’s Office for over 15 years, and has been in the quality control area for 5 years. She served on the board of the FICPA local chapter from 2004-2011 and is Chair of this year’s FSU Accounting Conferences. She serves on the Peer Review Committee for the National State Auditor’s Association. She oversees the Quality Assessment Reviews of the State Agency Inspectors General and has participated in External Peer Reviews in New York, California, Utah, and Georgia. She also develops and provides training courses related to auditing standards and other relevant topics for Auditor General staff.

THE NEW YELLOW BOOK:

SAME COLOR

REVISED STANDARDS

2011 GovernmentAuditing Standards

2011 Version

Internet version issued inAugust 2011; still awaitingfinal version.

2011 GovernmentAuditing Standards

Effective Dates

Financial Audits andAttestation Engagements –Periods ending on or afterDecember 15, 2012

Performance Audits –Beginning on or afterDecember 15, 2011

Early implementation is NOTpermitted.

2011 GovernmentAuditing StandardsRelationship of YB with OtherStandards

• AICPA field work andreporting standards areincorporated by referencefor financial audits

• PCAOB and IAASBstandards can be used inconjunction with GAGASfor financial statementaudits

2011 GovernmentAuditing StandardsRelationship of YB with OtherStandards

SUMMARY OF MAJOR CHANGES:

• Conceptual Framework forIndependence Added

• Requirements GoverningNonaudit Services Established

• Nonaudit Services GuidanceRevised

• Documentation Requirementsfor Independence Added

• SAS/SSAE RequirementsRemoved

• Attestation EngagementCategories Discussion Added

• Reporting Requirement forFraud Further Defined

2011 GovernmentAuditing Standards Changes to the Overall

Format• Chapters 1 and 2 have beenrealigned

• All financial audit standardsare now in Chapter 4

• Use of footnotes is moreconsistent

2011 GovernmentAuditing Standards

Chapter 1 Changes• Clarified/Added Definitions• Clarified the auditfunction’s structurallocation relative to theaudited entity

2011 GovernmentAuditing Standards

Chapter 2 Changes• Changes in terminology forconsistency

• Clarified citing compliancewith GAGAS

2011 GovernmentAuditing Standards

Chapter 3 Changes –IndependenceConceptual frameworkrequires that auditors:• Identify threats toindependence;

• Evaluate the significance ofthe threats identified; and

• Apply safeguards, whennecessary to eliminate thethreats or reduce them toan acceptable level.

Government AuditingStandards

2011 Revision

Independence:

Threats to independence arecircumstances that couldimpair independence.

Safeguards are controls thateliminate or reduce to anacceptable level a threat’spotential to impairindependence.

Government AuditingStandards

2011 Revision

Conceptual Framework Steps:

1. Identify Threats2. Evaluate Significance3. Apply Safeguards4. Determine Threat Level is

Acceptable

2011 GovernmentAuditing Standards

2011 Revision

Independence: SevenCategories of Threats

1. Self interest threat2. Self review threat3. Bias threat4. Familiarity threat5. Undue influence threat6. Management participationthreat7. Structural threat

2011 GovernmentAuditing Standards

2011 Revision Compared/Contrasted to2007 overarching ethicalprinciples and three areas ofpotential independenceimpairments:• Personal• External• Organizational

2011 GovernmentAuditing Standards

Independence – Safeguards

Include safeguards created bythe profession, legislation, orregulation, as well assafeguards in the workenvironment

2011 GovernmentAuditing Standards

Other Changes:

• Competence• Continuing ProfessionalEducation

• Systems of Quality Control• Peer Reviews

2011 GovernmentAuditing Standards

Changes Related to FinancialAudits:

• Early Communication• Deleted Paragraphs toEliminate Redundancy

2011 GovernmentAuditing Standards

Changes Related toAttestation Engagements:

• Three Categories• Fraud Reporting Thresholdfor Examinations

• Additional Considerations• Fieldwork Requirements forInternal Control Removed

2011 GovernmentAuditing Standards

Changes Related toPerformance Audits:

• Validity Discussion Revised• Sufficiency andAppropriateness ofComputer ProcessedInformation Revised

• Fraud ReportingRequirement Revised

• Other Misc

2011 GovernmentAuditing Standards

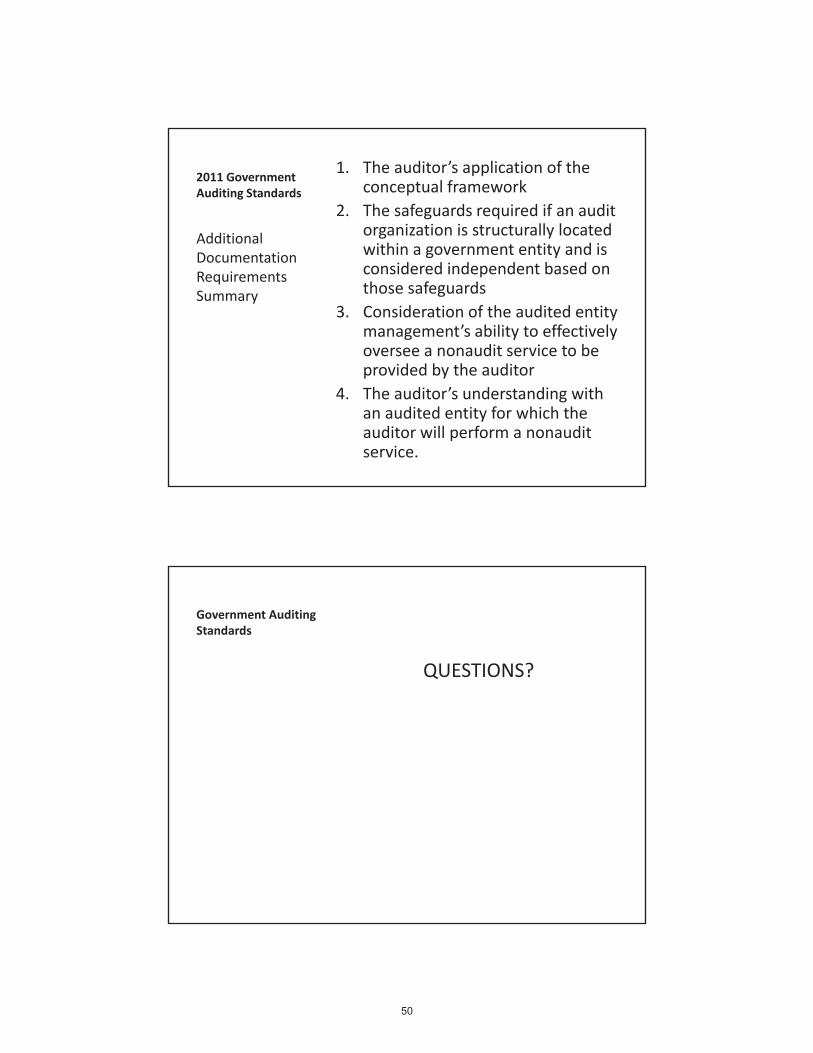

AdditionalDocumentationRequirementsSummary

1. The auditor’s application of theconceptual framework

2. The safeguards required if an auditorganization is structurally locatedwithin a government entity and isconsidered independent based onthose safeguards

3. Consideration of the audited entitymanagement’s ability to effectivelyoversee a nonaudit service to beprovided by the auditor

4. The auditor’s understanding withan audited entity for which theauditor will perform a nonauditservice.

Government AuditingStandards

QUESTIONS?

Health Care Fraud in Florida

Jane Flowers, CPA

Audit Manager Florida Auditor General

Jane has been with the Auditor General’s office for 29 years and an Audit Manager since January 2005. She manages operational audits of State Government agencies with the majority related to Health and Human Services including audits of the Medicaid Program. Jane is agraduate of Troy University and also a member of the AICPA.

OCTOBER 27, 2011

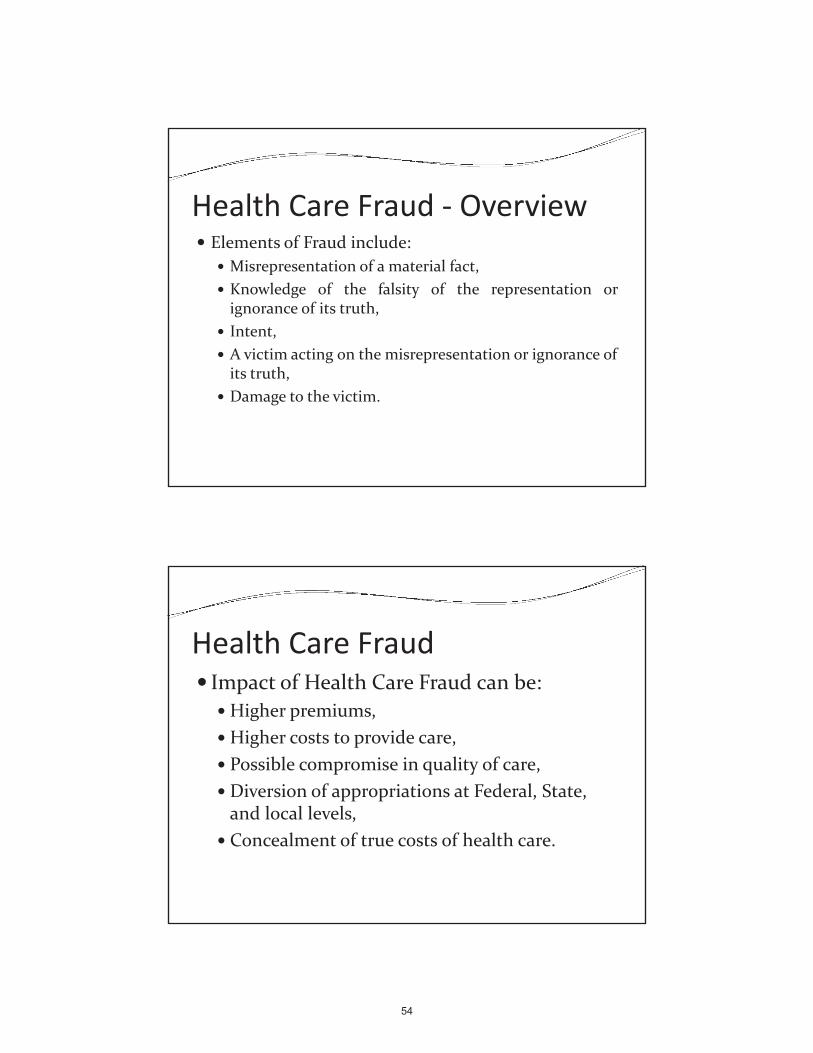

Growing nationwide crime with significant effecton health care payment system.Health Care Fraud in Florida occurs in Medicare,Medicaid, and private insurance programs.Fraud can be defined as an intentional deception ormisrepresentation that is made by an individual whoknows it to be false and knows the deception couldresult in some unauthorized benefit from that action.

Health Care Fraud Overview

Health Care Fraud OverviewElements of Fraud include:

Misrepresentation of a material fact,Knowledge of the falsity of the representation orignorance of its truth,Intent,A victim acting on the misrepresentation or ignorance ofits truth,Damage to the victim.

Health Care FraudImpact of Health Care Fraud can be:

Higher premiums,Higher costs to provide care,Possible compromise in quality of care,Diversion of appropriations at Federal, State,and local levels,Concealment of true costs of health care.

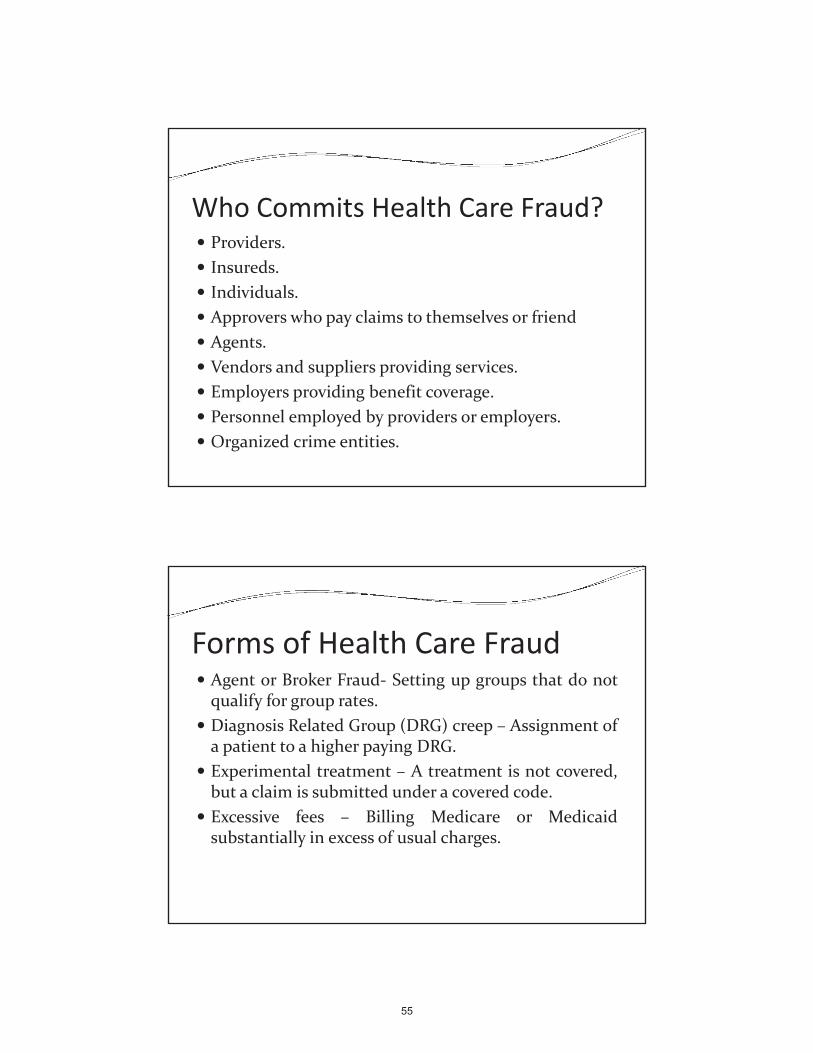

Who Commits Health Care Fraud?Providers.Insureds.Individuals.Approvers who pay claims to themselves or friendAgents.Vendors and suppliers providing services.Employers providing benefit coverage.Personnel employed by providers or employers.Organized crime entities.

Forms of Health Care FraudAgent or Broker Fraud Setting up groups that do notqualify for group rates.Diagnosis Related Group (DRG) creep – Assignment ofa patient to a higher paying DRG.Experimental treatment – A treatment is not covered,but a claim is submitted under a covered code.Excessive fees – Billing Medicare or Medicaidsubstantially in excess of usual charges.

Forms of Health Care FraudFalse billing Providers or insured individuals bill forservices not rendered or claim representatives withinpayer systems generate false billings.False cost reports – Cost reports with false orfraudulent information. Examples include reportingcosts of noncovered services and improperlymanipulating statistics such as patient census andsquare footage information.Improper modifiers – Codes that reflect an alterationof the basic code to create higher reimbursements.

Forms of Health Care FraudKickbacks – Payments to another individual in orderto receive a referral or to undergo treatment.Medical necessity – Billing for services and items notmedically necessary. Especially becoming prevalentrelated to Durable Medical Equipment.Membership fraud – Billing for noncovereddependents or nonexistent dependents.

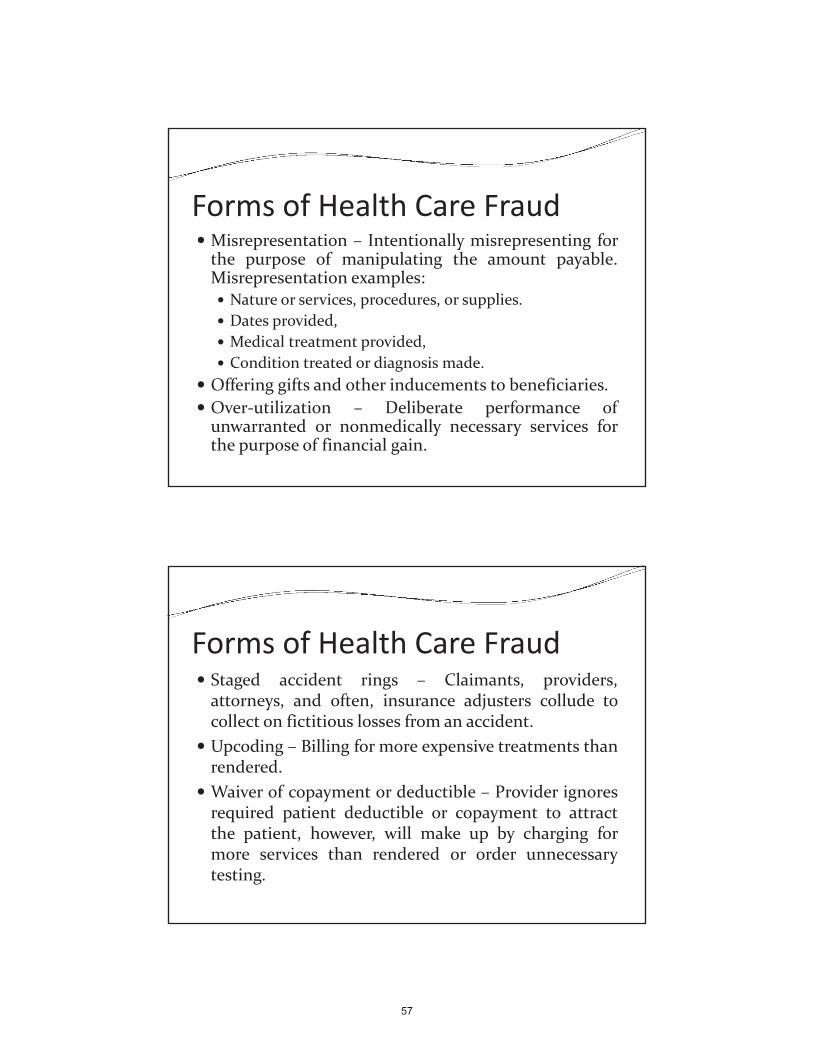

Forms of Health Care FraudMisrepresentation – Intentionally misrepresenting forthe purpose of manipulating the amount payable.Misrepresentation examples:

Nature or services, procedures, or supplies.Dates provided,Medical treatment provided,Condition treated or diagnosis made.

Offering gifts and other inducements to beneficiaries.Over utilization – Deliberate performance ofunwarranted or nonmedically necessary services forthe purpose of financial gain.

Forms of Health Care FraudStaged accident rings – Claimants, providers,attorneys, and often, insurance adjusters collude tocollect on fictitious losses from an accident.Upcoding – Billing for more expensive treatments thanrendered.Waiver of copayment or deductible – Provider ignoresrequired patient deductible or copayment to attractthe patient, however, will make up by charging formore services than rendered or order unnecessarytesting.

Forms of Health Care FraudAdvertisements for free screenings or other servicescould be a red flag for collecting health information tobill for services not provided.Using high pressure marketing practices to coercebeneficiaries to order unneeded equipment.

Forms of Health Care FraudRecently, scammers have focused on home healthcareagencies, mental health services, and physical therapy.“Phantom Pharmacy” scams are occurring, usually:

Criminals use a legitimate address to establish a fakepharmacy business.Use stolen or otherwise obtained doctor ID and patientinsurance ID numbers, write fraudulent prescriptionsfor expensive drugs that were never actually prescribedor dispensed.Then submit to insurers, Medicare, or Medicaid.

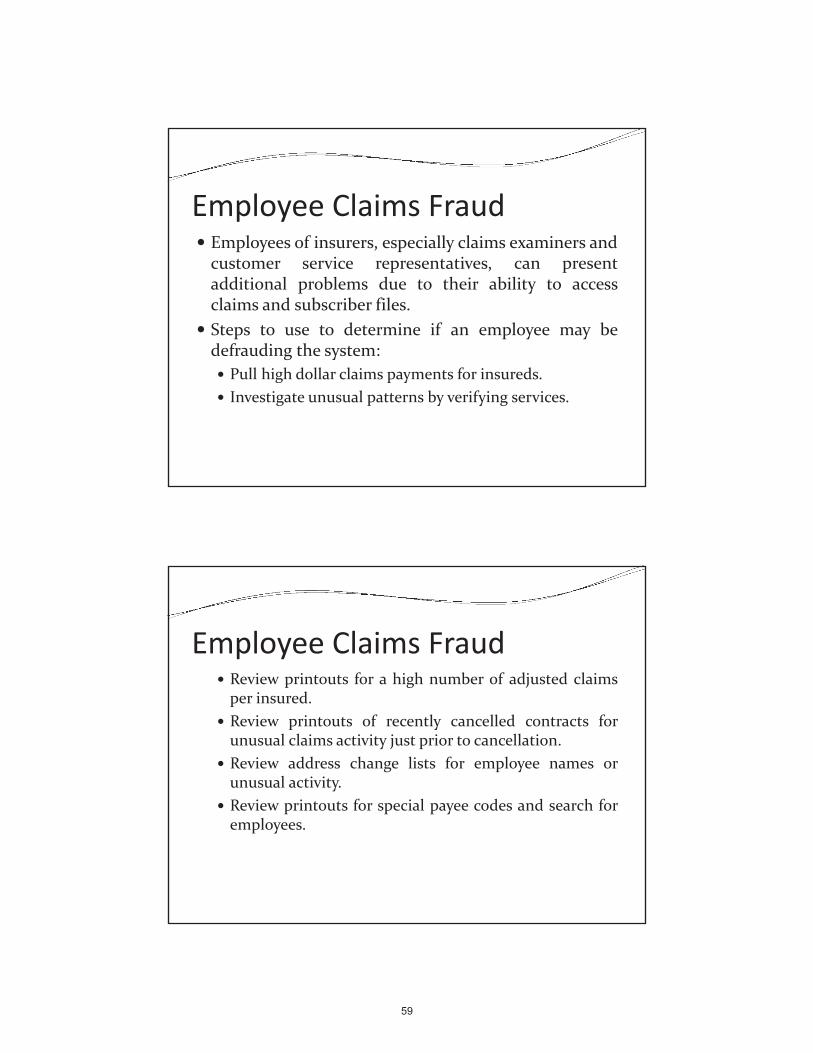

Employee Claims FraudEmployees of insurers, especially claims examiners andcustomer service representatives, can presentadditional problems due to their ability to accessclaims and subscriber files.Steps to use to determine if an employee may bedefrauding the system:

Pull high dollar claims payments for insureds.Investigate unusual patterns by verifying services.

Employee Claims FraudReview printouts for a high number of adjusted claimsper insured.Review printouts of recently cancelled contracts forunusual claims activity just prior to cancellation.Review address change lists for employee names orunusual activity.Review printouts for special payee codes and search foremployees.

Employee Claims FraudPreventive steps to avoid employee claims fraud:

Separate area to handle employee claims.Limit access to employee claims information.Include edits in the claims system that will generateexception reports for high dollar claim payments andmultiple adjusted claims.Make it known to employees that audits are regularlyconducted.

Employee Health Insurance Billing ScamRecently Miami Dade Schools police uncovered anemployees’ health insurance billing scam.

School detective went undercover to a clinic.Received EKG and had blood drawn. Discreetly received$400 in cash.Clinic billed for pelvic ultrasound, heart sonogram andchest x ray $5,490 in medical procedures.Scam was uncovered when administrators noticedstrange financial transactions involving certain clinics.

Employee Health Insurance Billing ScamClinics billed never performed procedures for about100 school employees, mostly bus drivers.Estimate of about $1 million in bogus claims.According to police, clinics paid $400 in kickbacks toeach client per visit and another $50 for referrals.School police worked their way into the ring through aschool bus driver.Reports indicate another $2 million in bogusprocedures may have been billed to private insurers.

Medicare Fraud SchemesIn Florida two entities participated in a scheme todefraud Medicare by submitting false claims fortherapy and home health services.Kickbacks were paid to patient recruiters, nurses, andemployees in exchange for delivery of patients to itsfacilities.Patient files were falsified by including descriptions ofnonexistent medical conditions in order to create thefalse impression that the patients were unable to selfinject medication and were homebound, which wouldqualify for Medicare home health care benefits.

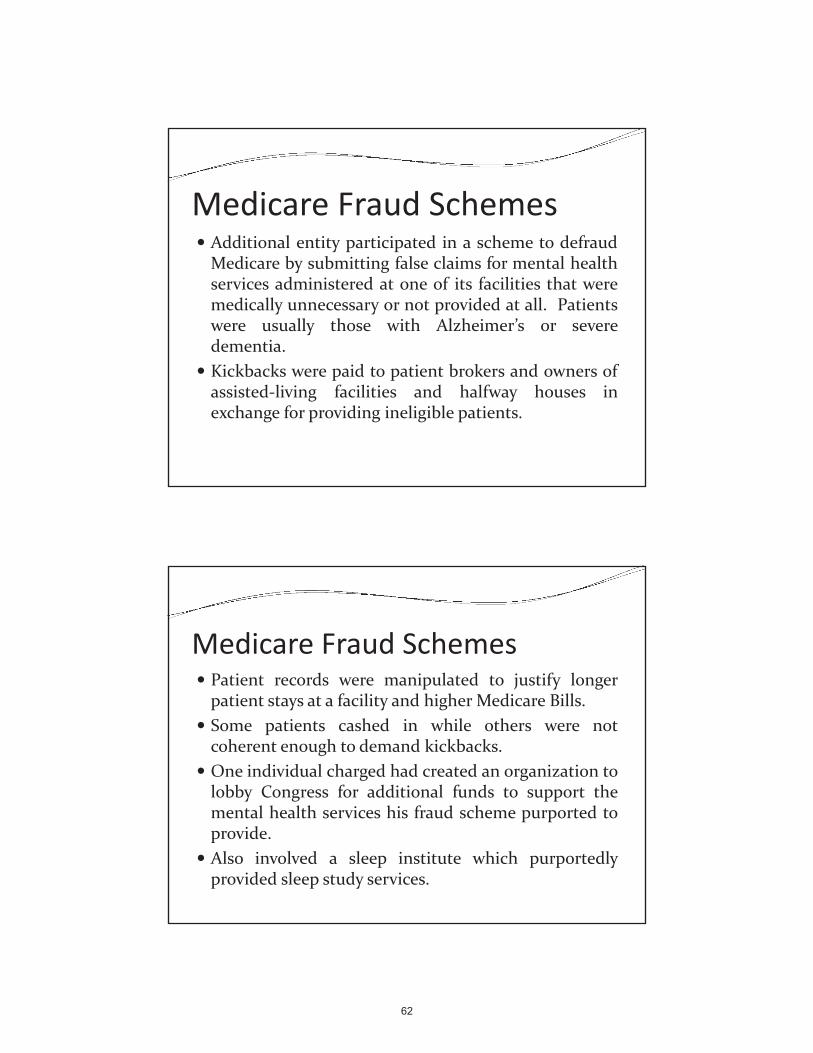

Medicare Fraud SchemesAdditional entity participated in a scheme to defraudMedicare by submitting false claims for mental healthservices administered at one of its facilities that weremedically unnecessary or not provided at all. Patientswere usually those with Alzheimer’s or severedementia.Kickbacks were paid to patient brokers and owners ofassisted living facilities and halfway houses inexchange for providing ineligible patients.

Medicare Fraud SchemesPatient records were manipulated to justify longerpatient stays at a facility and higher Medicare Bills.Some patients cashed in while others were notcoherent enough to demand kickbacks.One individual charged had created an organization tolobby Congress for additional funds to support themental health services his fraud scheme purported toprovide.Also involved a sleep institute which purportedlyprovided sleep study services.

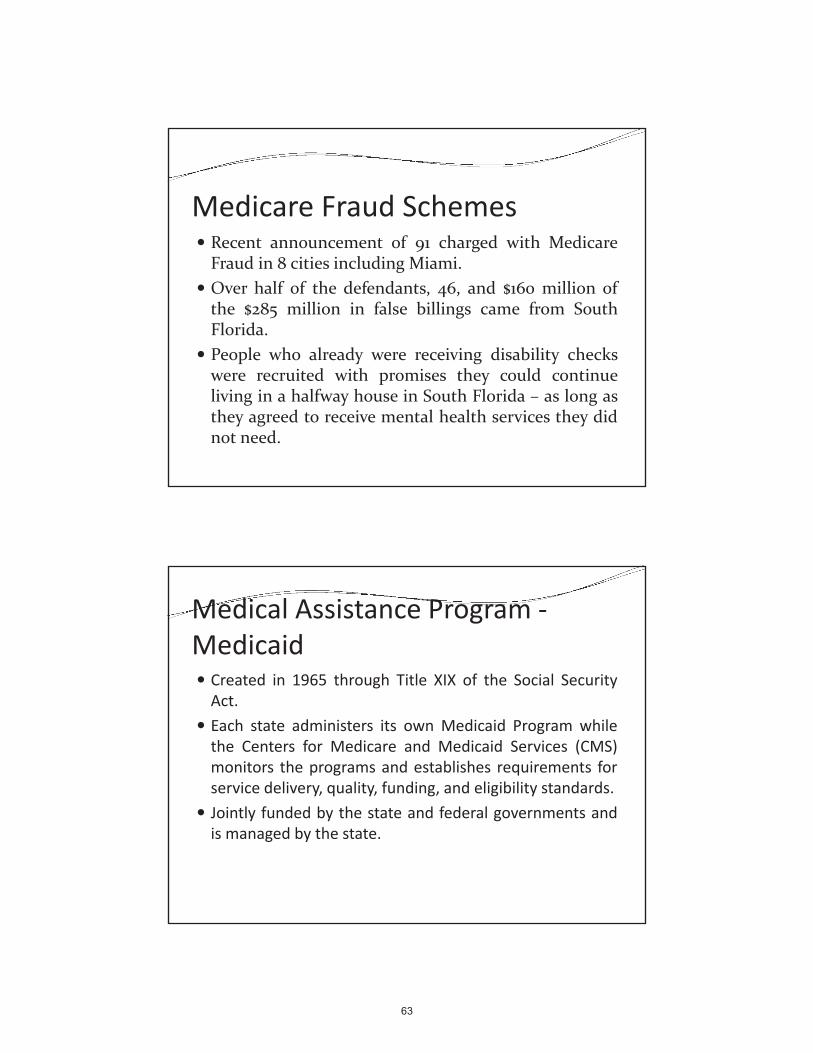

Medicare Fraud SchemesRecent announcement of 91 charged with MedicareFraud in 8 cities including Miami.Over half of the defendants, 46, and $160 million ofthe $285 million in false billings came from SouthFlorida.People who already were receiving disability checkswere recruited with promises they could continueliving in a halfway house in South Florida – as long asthey agreed to receive mental health services they didnot need.

Medical Assistance ProgramMedicaid

Created in 1965 through Title XIX of the Social SecurityAct.Each state administers its own Medicaid Program whilethe Centers for Medicare and Medicaid Services (CMS)monitors the programs and establishes requirements forservice delivery, quality, funding, and eligibility standards.Jointly funded by the state and federal governments andis managed by the state.

Common Medicaid Fraud SchemesWatch for the following:

Payments (in cash or in kind) in return for Medicaidnumbers,Every patient in a group setting receiving the same typeof service on the same day,Every patient in a group setting receiving the same typeof medical equipment, and services listed on themedical summary that recipient does not rememberreceiving or didn’t need.

Common Medicaid Fraud SchemesBilling for “phantom patients” who did not really receiveservices.Billing for medical services or goods that were notprovided.Billing for old items as if they were new.Billing for more hours than there are in a day.Billing for tests that the patient did not need.Paying a “kickback” in exchange for a referral formedical services or goods.

Common Medicaid Fraud SchemesCharging Medicaid for personal expenses that havenothing to do with caring for a Medicaid client.Overcharging for health care services or goods that wereprovided.Concealing ownership in a related company.Using false credentials.Double billing for health care services or goods thatwere provided.

Challenges in Preventing FraudStaying a step ahead of the fraudsters.Maintaining a careful balance:

Majority of providers are honest,Paying claims on time vs. conducting additional review,Preventing and detecting fraud and brokering goodpartnerships.

Preventing fraud through effective internal controls.

Internal ControlsStrong internal controls by medical providers and thepaying agent decrease the opportunity for fraud byincreasing the risk of detection.Internal controls can enable health care services to beprovided more efficiently and effectively.For Medicare and Medicaid, controls are especiallycritical due to the programs’ complexity and size.

Internal ControlsDue to volume of medical claims, process needs to beautomated. Technology can play an important role indetecting fraud and abuse, and can help pave the waytoward prevention. Technology cannot eliminate thefraud problem; however, it can significantly minimizefraud and abuse and result in reduced health carefraud losses.In Medicaid, as state and federal laws apply, statelegislatures often modify the program which mayallow opportunities for fraud to not be detected timely.

Florida MedicaidFor fiscal year 2010 2011, in Florida, Medicaid wasappropriated $20.8 Billion.Agency for Health Care Administration (AHCA) isdesignated as the state agency responsible foradministering the Florida Medicaid Program.Recipients enrolled in Medicaid generally either enrollin a managed care plan or receive their servicesthrough a fee for service payment structure.

Florida MedicaidAHCA has a contract with HP Enterprise Services (HP)to serve as the state’s fiscal agent. Bureau of MedicaidContract Management supervises the contract.Functions include enrolling non institutionalproviders, processing Medicaid claims, serving as theenrollment broker for Medicaid recipients, anddistributing Medicaid forms and publications.Bureau manages the information interface withvarious entities and the Florida Medicaid ManagementInformation System (FMMIS).

Florida MedicaidFMMIS allows the use of electronic edits and audits toensure each claim is from a valid provider, for a validrecipient, and for a valid service.Electronic audits are also to ensure that the claimsubmitted does not exceed Medicaid programlimitations.Edits and audits in FMMIS are essential to ensureclaims are paid appropriately.

Florida Medicaid Fraud and AbuseAHCA and the Medicaid Fraud Control Unit (MFCU) of theAttorney General’s Office are by law responsible forpreventing, reducing, and mitigating health care fraud,waste, and abuse.AHCA and MFCU collaborate with each other as well asother partners including, Department of Health,Department of Law Enforcement, Department of Children& Families (DCF), Agency for Persons with Disabilities, andthe Federal Centers for Medicare and Medicaid Services(CMS).

UtilizationAHCA maintains contracts with vendors and internallyperforms utilization management functions which includeonsite and desk reviews of quality of care and claimsmonitoring for various provider types.Utilization management processes help AHCA monitorthe use of services and prevent unnecessary, excessive,duplicative, or otherwise inappropriate expenditures.

Prevention ActivitiesAHCA’s Medicaid Program Integrity (MPI) activitiesinclude the following:

Use of prepayment reviews to identify improper claims anddeny payment.Recommendation for termination of providers suspected ofmisusing the Medicaid Program.Denial of reimbursement for prescription drugs prescribedby terminated providers.Site visits to certain Medicaid providers in specifiedgeographic areas.Application of administrative sanctions, as appropriate.

Special Projects and Pilots – TelephonicHome Health DMV Program

AHCA has contracted with a vendor to implement theTelephonic Home Health Service Delivery Monitoring andVerification (DMV) Program. The Program is to addressaberrant billing practices, potential fraud, and the qualityof recipient care in home health care.Requires providers to submit claims for home health visitselectronically through the vendor’s system.Home health visits are verified by telephone using atechnology called “voice biometrics.”Vendors system maintains databases for each homehealth agency in the pilot area (Miami Dade County).

Special Projects and Pilots – TelephonicHome Health DMV Program

Databases contain information on home health agencystaff, recipients, service authorizations, visit schedules,visit verification, and billing activity.Each home health agency logs in to the vendor’ssystem to access the health agency’s database.Provides AHCA with more tools to detect theappropriateness of service provision and to hold homehealth agencies accountable for providing onlyauthorized services.Should allow AHCA to better track quality of service toensure correct population obtains the services needed.

Special Projects and Pilots – TelephonicHome Health DMV Program

Vendor receives data feeds from the Florida MedicaidManagement Information System (FMMIS) that contain priorauthorization information for home health visits granted tohome health agencies in Miami Dade County. When nurse oraide arrives and leaves the recipient’s residence, they will call anumber assigned to the home health agency, enter a unique staffID number, and completes a speaker verification process.Voice is matched to a pre recorded voice print to verify that theassigned staff is providing a home health visit to a specificrecipient.When a home health visit has occurred and the verificationprocess is complete, the vendor’s system generates the claimsfile. Each provider is responsible for reviewing the claims in thevendor’s database and giving approval for the vendor toelectronically transmit the claims to AHCA for payment.

Special Projects and Pilots – TelephonicHome Health DMV Program

Findings from report by AHCA, dated February 1, 2011,indicated:

Visit exceptions are occurring when required elementsto verify a home health visit do not align.Three issues that generated the largest number ofexceptions were:

Visits not being scheduled in the vendor’s systemIncorrect recipient phone numbers in FMMISLength of visit was more or less than scheduled time.

Special Projects and Pilots – TelephonicHome Health DMV Program

AHCA’s initial evaluation of this system indicated thatthe incorporation of a Web based system that includesrecipient, provider, service authorization, andscheduling information, combined with the use ofvoice biometrics, not only supplements physicaldocumentation of delivery and utilization of homehealth visits but also provides AHCA with tools tomore effectively monitor the provision of home healthvisits.

Special Projects and Pilots ComprehensiveCare Management

AHCA amended its contract with a vendor, who wasresponsible for utilization management for homehealth visits, private duty nursing, personal careservices and inpatient medical and surgical services inFY 2009 10 to include a On Site Care ManagementProject in Miami Dade County for home health visits.Purpose was to identify potential overutilization andfraud or abuse of Medicaid services by ensuring thatthe level of services provided matches the needs of therecipients.

Special Projects and PilotsIn first three months of these projects, AHCAterminated two large home health agencies.Has assisted AHCA in identifying trends whenreviewing ordering physician information and AHCAhas been furnished a list of physicians who aresuspected of potentially fraudulent activity.Recipients and Providers are becoming bettereducated about what is reimbursable through theFlorida Medicaid home health program.

Special Projects and PilotsAfter one year of operation of these two pilots , AHCAhas indicated a decrease of 50% in claims paid forhome health visits and a reduction of 51% in homehealth care visits.Plan to expand the pilots to other selected counties.

Special Projects and PilotsAHCA and DCF have been conducting pilot projectsusing link analysis.AHCA is performing link analysis on individuals indatabases including providers in FMMIS to gatherinformation from other sources including criminaldatabases and other state’s exclusion list.During the first quarter of this fiscal year, 120providers have been identified with various actionsincluding termination from the Medicaid program.

Special Projects and PilotsDCF has worked using technology to perform linkanalyses between information in databases. Pilotdemonstrated the capacity to aid in the verification ofapplicant identities.Incorporating this technology into the current DCFACCESS system could prevent identity fraud at theentry point for eligibility determination.

AHCA Field Initiatives Case StudyMPI investigated the billings of twelve DME providersin Miami Date and Broward Counties. Some providershad failed to conduct or document home visits, hadbilled for equipment not delivered or not needed, hadfailed to obtain required medical information, had notposted required “Oxygen in Use” signs or had engagedin other violations of Medicaid Policy. One providerbilled for services for a recipient who was deceased.Two providers were referred to MFCU. Action ispending for another. Only one of the twelve had noadverse findings.

AHCA Case StudiesFocused on physicians operating outside scope of theirpractice.Physicians such as ophthalmologists were writing largenumbers of prescriptions for controlled substancesnormally associated with pain management.Evidence revealed some Medicaid recipients paid up to$250 for office visits and received prescriptions for painmedications. Some were filled using Medicaid andsome in cash.

AHCA Case StudiesMedicaid provider had a high volume of prescriptions foratypical anti psychotic medications.Reimbursed by Medicaid for a relatively low dollar amountfor his office visits.Claims review indicated more than $7 Million inprescription claims written by this physician betweenJanuary 2008 and June 2009.Medical records were reviewed and Medicaid recipientsinterviewed. Majority of recipients could not producemedications that were recently prescribed.Provider was terminated and investigation is continuing.

AHCA Case StudiesDentist billed Medicaid for services not performed.Received over $1 million in calendar year 2009.Onsite visit conducted along with interviews of theprovider, staff, and recipients.Provider was paying non Medicaid enrolled dentist adaily fee to perform dental work from two locations.Second location was not enrolled in Medicaid.Provider was terminated and case has been referred tolaw enforcement.

Medicaid Fraud Control UnitThe MFCU investigates and prosecutes fraud involvingproviders that intentionally defraud the MedicaidProgramPer Annual Report of fraud by AHCA and AttorneyGeneral, dated December 2010, top 5 Medicaid Fraudby Provider type in FY 2009 10 were:

Home and Community Based ServicePharmaceutical ManufacturerPhysician (MD)Medical Supplies/Durable Medical EquipmentCommunity Alcohol/Drug/Mental Health

Medicaid Fraud Control UnitReport also indicates case investigations will focus ontypes of fraud, types of subjects/targets and types ofproviders having a widespread impact on the Medicaidprogram or involving public safety. Emphasis placedon case investigations/prosecutions that have adeterrent effect.Emphasis is placed on developing and fostering keypartnerships with agencies such as AHCA,Department of Health, and the Agency for Personswith Disabilities.

Medicaid Fraud Control UnitLast year, MFCU was granted a waiver that will allowMFCU to “mine” FMMIS data to identify cases ofpotential Medicaid fraud.Will allow MFCU to sort electronic claims through theuse of statistical models and technologies to uncoverpatterns and relationships.Before MFCU was prohibited from using federalMedicaid matching funds to detect potential fraudthrough routine claims review procedures. Instead,MFCU generally relied on referrals from AHCA.

Medicaid Fraud Control UnitWaiver should allow MFCU to use federal matchingfunds to apply sophisticated electronic data miningtools that are beyond the scope normally performed byAHCA.CMS is to monitor the progress of the waiver.

MFCU Case StudiesProvider was billing for respiratory therapy servicesdid not have medical authorization to provide.Falsified service logs were submitted related to homeand community based services.Medicaid billed for unsupervised occupational andphysical therapy. For five years provider billedMedicaid .Provider billed for unallowable speech therapy.

Department of Children andFamilies (DCF)

Medicaid eligibility is determined either by DCF or theSocial Security Administration for SupplementalSecurity Income (SSI) recipients.The ACCESS Florida Program, as the service deliverymodel for economic self sufficiency services, isresponsible for public assistance eligibilitydetermination and ongoing case management forFood Assistance, Temporary Cash Assistance, andMedicaid.

Division of Public Assistance Fraud(DPAF)

Investigative unit dedicated to fraud detection inpublic assistance programs including Medicaid,related to recipient fraud.Is located within the Department of FinancialServices.

Additional Legislative Tools to Prevent andDetect Medicaid Fraud

Senate Bill 1986 (CH 2009 223, Laws of Florida) amendedsections of law to address systemic health care fraud.Increases the Medicaid program’s authority to addressfraud, particularly as it relates to home health services.Health care facility and health care practitioner licensingstandards are increased. Also, increases administrativepenalties for committing Medicaid fraud.Designated Miami Dade County as a health care fraudarea of concern.

Additional Legislative Tools to Preventand Detect Medicaid Fraud cont.

Senate Bill 1484 (Chapter 2010 144, Laws of Florida) createdthe Medicaid and Public Assistance Fraud Strike Force (StrikeForce) within the Department of Financial Services (DFS) todevelop a statewide strategy and coordinate state and localefforts and resources to prevent, investigate and prosecuteMedicaid and public assistance fraud.Strike Force consists of 11 members with the Chief FinancialOfficer (CFO) serving as chair and the Attorney General servingas vice chair. The Strike Force shall provide advice and makerecommendations, as necessary, to the CFO.

Additional Legislative Tools to Preventand Detect Medicaid Fraud cont.

Strike Force may advise the CFO on initiatives that include,but are not limited to:

Conducting a census of local, state, and federal efforts toaddress Medicaid and public assistance fraud, including frauddetection, prevention, and prosecution, in order to discernoverlapping missions, maximize existing resources, andstrengthen current programs.Developing a strategic plan for coordinating and targetingstate and local resources for preventing and prosecutingMedicaid and public assistance fraud. The plan must identifymethods to enhance multi agency efforts that contribute toachieving the state’s goal of eliminating Medicaid and publicassistance fraud.

Additional Legislative Tools to Preventand Detect Medicaid Fraud cont.

Identifying methods to implement innovativetechnology and data sharing in order to detect andanalyze Medicaid and public assistance fraud with speedand efficiency.Establishing a program to provide grants to state andlocal agencies that develop and implement effectiveMedicaid and public assistance fraud prevention,detection and investigation programs, which areevaluated by the Strike Force and ranked by theirpotential to contribute to achieving the state’s goal ofeliminating Medicaid and public assistance fraud.

Additional Legislative Tools to Preventand Detect Medicaid Fraud cont.

Developing and promoting crime prevention servicesand educational programs that serve the public,including, but not limited to, a well publicized rewardsprogram for the apprehension and conviction ofcriminals who perpetrate Medicaid and public assistancefraud.

Additional Legislative Tools to Preventand Detect Medicaid Fraud cont.

Providing grants, contingent upon appropriation, for multiagency or state and local Medicaid and public assistance fraudefforts which include, but are not limited to:

Providing for a Medicaid and public assistance fraudprosecutor in the Office of the Statewide Prosecutor.Providing assistance to state attorneys for support services orequipment, or for the hiring of assistant state attorneys, asneeded, to prosecute Medicaid and public assistance fraudcases.Providing assistance to judges for support services or for thehiring of senior judges, as needed, so that Medicaid and publicassistance fraud cases can be heard expeditiously.

Additional Legislative Tools to Preventand Detect Medicaid Fraud cont.

Strike Force shall receive periodic reports fromstate agencies, law enforcement officers,investigators, prosecutors, and coordinating teamsregarding Medicaid and public assistance criminaland civil investigations.Strike Force shall annually prepare and submit areport on its activities and recommendations byOctober 1.

Additional Legislative Tools to Prevent andDetect Medicaid Fraud cont.

Report included increased emphasis on preventionincluding changes to statutes and improvements ineligibility determinations.Also need to make better use of available data andincrease leveraging of resources.Report indicates currently technology is not in placethat connects all databases that contain health carefraud and related data.Eight recommendations were made to the Legislature.

Additional Legislative Tools to Preventand Detect Medicaid Fraud cont.

Law also requires the Auditor General and the Officeor Program Policy Analysis and GovernmentAccountability (OPPAGA) to review and evaluate theAHCA’s Medicaid fraud and abuse systems andrequires a report by December 1, 2011.

Additional Legislative Tools to Preventand Detect Medicaid Fraud cont.

Review is to include but is not limited to:An evaluation of current Medicaid policies and theMedicaid fiscal agent;An analysis of the Medicaid fraud and abuse preventionand detection processes, including agency contracts,Medicaid databases, and internal control risk assessments;A comprehensive evaluation of the effectiveness of thecurrent laws, rules and contractual requirements thatgovern Medicaid managed care entities;An evaluation of the agency’s (AHCA) Medicaid managedcare oversight processes;

Additional Legislative Tools to Prevent andDetect Medicaid Fraud cont.

Recommendations to improve the Medicaid claimsadjudication process, to increase the overallefficiency of the Medicaid Program, and to reduceMedicaid overpayments; andOperational and legislative recommendations toimprove the prevention and detection of fraud andabuse in the Medicaid managed care program.Auditor General Reports are included on Web sitehttp://www.myflorida.com/audgen/index.htm.

Lunch Presentation: Why Focuson International Trade

Frank M. Ryll, Jr.

Sources: AWI, Mortgage Bankers Association, FDCF, FDOE, FOEDR

$5

$10

$15

$20

$25

1995 2000 2005 2010 2015 2020 2025 2030 2035

Trill

ion

U. S

. 200

0 D

olla

rs

Real Gross Domestic Product

Real Value of Imports and Exports

Source: Global Insight, Inc. April 2009.

Source: European Communities, 2008

Source: America 2050

Source: U.S. Bureau of Economic Analysis, 2010

Trade and Logistics Industry Percent of Total Employment

20091999

FloridaGeorgia Texas LouisianaNorth

Carolina Alabama MississippiSouth

CarolinaUnitedStates

8.9%

8.2%

7.2%7.1% 7.0%

6.6 % 6.5%

6.3%6.3%5.9%

Florida Origin Exports

Source: U.S. Census Bureau/WISER Trade, 2010.

(billions of 2010 dollars)

20102008200620042002200019981996

3.3%

$28.8

$32.7

$33.6 $29.7

$33.5

$41.7

$54.9

$55.2Value of FloridaOrigin Exports

Florida Share of USTrade Export Value 4.3%

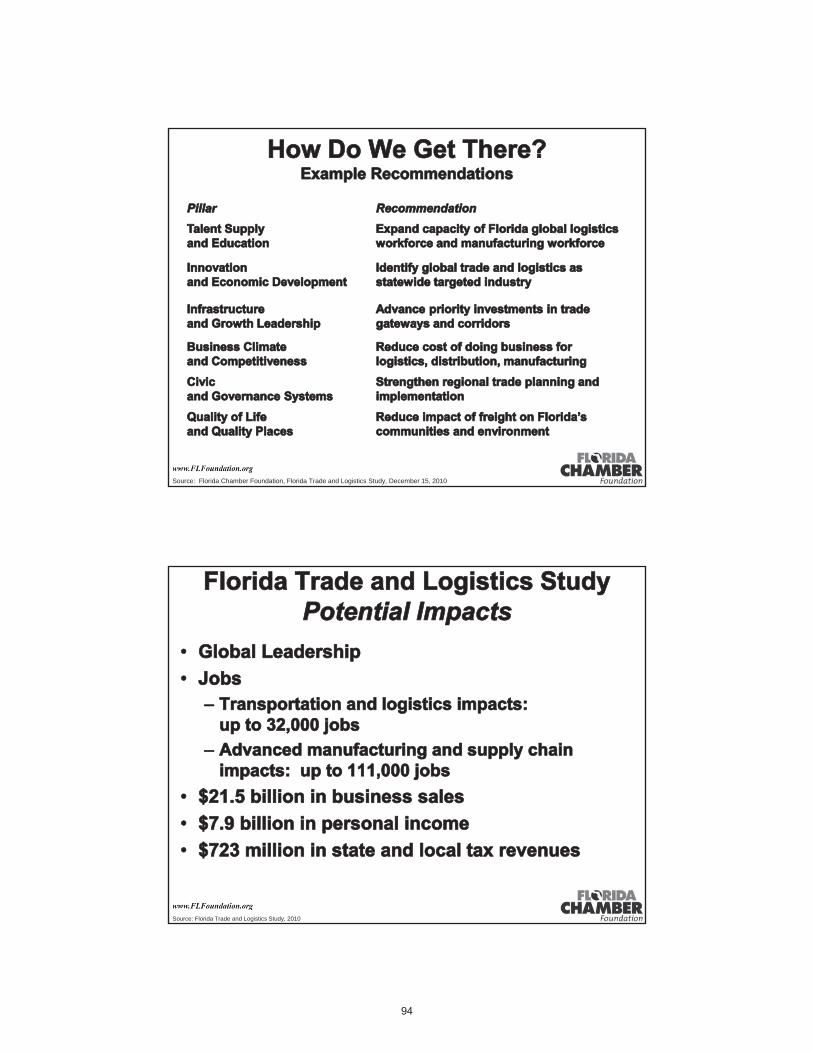

Source: Florida Chamber Foundation, Florida Trade and Logistics Study, December 15, 2010

Source: Florida Trade and Logistics Study, 2010

Bank Panel

Tiffany Parker Skip Smith

Ramsay Sims

Market Leader III/Leon County Market

Tiffany Parker began her career with Capital City Bank in 2001 in Macon, Georgia. Tiffany has held several positions with Capital CityBank in our retail division, and four years ago moved to Tallahassee to further her career with Capital City. Tiffany currently manages the Metropolitan Office, and oversees nine of the fifteen Leon County retail offices in Tallahassee.

Skip Smith is Senior Vice President and Manager of the Business Banking Group at Capital City Bank (NASDAQ: CCBG) in Tallahassee, Florida. He and his team are responsible for delivering loan, deposit and fee based products to small and mid sized businesses and business owners. He has been with Capital City Bank since 1998.

Prior to this, he spent 14 years at Barnett Bank in several roles including Business Banking Manager, manager of the Small Business Lending Unit, Corporate Relationship Manager and Director of Barnett People for Better Government, the governmental relations arm of the bank.

Skip holds a bachelors degree from the Florida State University School of Business and has attended numerous banking and finance schoolsin his 27 year career. He is active in the community and currently serves on several civic and non profit boards including the Committee of 99, the Tallahassee Marine Institute and the Alpha Tau Omega fraternity Board of Trustees.

Mr. Sims leads Capital City Bank’s Institutional Banking Group where he specializes in banking and lending for governments and non-profitorganizations. Mr. Sims has 18 years of experience serving governments and non-profit organizations in the financial sector. Prior to joining Capital City Bank, Mr. Sims spent 5 years in Public Finance with Merrill Lynch, 3 years in Corporate Tax-Exempt Finance with Banc of America Securities, and 6 years in Government Finance with GE Capital. Mr. Sims earned his Bachelors degree in Economics from the University of the South (Sewanee) and his M.B.A. from Florida State University.

FASB Not-for-Profit Advisory Committee Update

David C. Moja, CPA Gregory B. Capin, CPA

Principal, National Director of Not-for-Profit Tax ServicesCapinCrouse, LLP

Dave is on the firm’s leadership team for not-for-profit tax services. His goal is to provide our clients with the highest quality tax services so they can focus on advancing their mission. He is an expert on emerging issues such as the new Form 990, Unrelated Business Income issues, Board Governance, and tax credits and incentives.