FACTORY OVERHEAD - blogs.unpad.ac.idblogs.unpad.ac.id/ratnakomara11/files/2012/02/AKBI-5.pdf ·...

24

FACTORY OVERHEAD FACTORY BURDEN, PRODUCTION OVERHEAD, MANUFACTURING EXPENSE, MANUFACTURING OVERHEAD, FACTORY EXPENSE & INDIRECT MANUFACTURING /PRODUCTION COST

Transcript of FACTORY OVERHEAD - blogs.unpad.ac.idblogs.unpad.ac.id/ratnakomara11/files/2012/02/AKBI-5.pdf ·...

FACTORY OVERHEAD

FACTORY BURDEN, PRODUCTION OVERHEAD,

MANUFACTURING EXPENSE, MANUFACTURING

OVERHEAD, FACTORY EXPENSE & INDIRECT

MANUFACTURING /PRODUCTION COST

Factory Overhead is generally defined as

indirect materials, indirect labor, and all

other factory costs that cannot be

conveniently identified with or charged

directly to specific jobs, lots, products, or

final cost objectives.

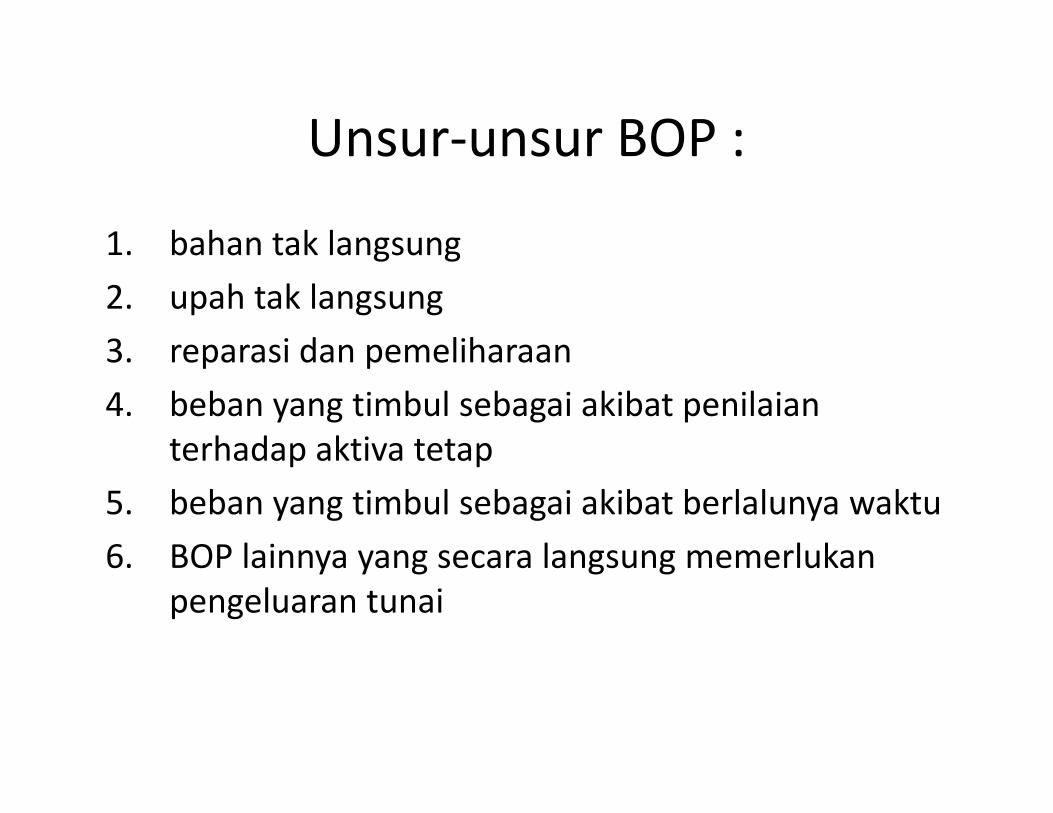

Unsur-unsur BOP :

1. bahan tak langsung

2. upah tak langsung

3. reparasi dan pemeliharaan

4. beban yang timbul sebagai akibat penilaian 4. beban yang timbul sebagai akibat penilaian

terhadap aktiva tetap

5. beban yang timbul sebagai akibat berlalunya waktu

6. BOP lainnya yang secara langsung memerlukan

pengeluaran tunai

Klasifikasi BOP:

1. bila dikaitkan dengan volume produksi, maka BOP dapat dibagi ke dalam :BOP variabel, BOP tetap dan BOP semivariabel.

2. bila dikaitkan dengan departemen yang ada, 2. bila dikaitkan dengan departemen yang ada, maka BOP dibagi ke dalam: BOP langsung departemen/direct dept overhead dan BOP tak langsung departemen/indirect dept overhead.

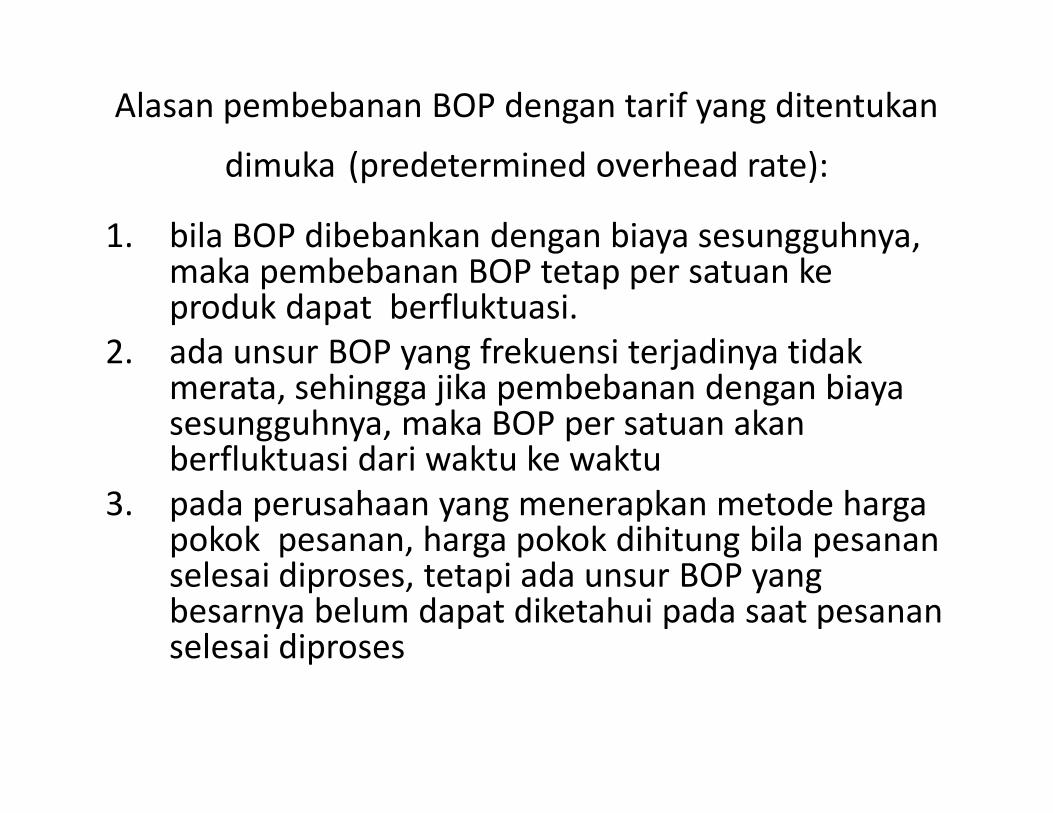

Alasan pembebanan BOP dengan tarif yang ditentukan

dimuka (predetermined overhead rate):

1. bila BOP dibebankan dengan biaya sesungguhnya, maka pembebanan BOP tetap per satuan ke produk dapat berfluktuasi.

2. ada unsur BOP yang frekuensi terjadinya tidak merata, sehingga jika pembebanan dengan biaya sesungguhnya, maka BOP per satuan akan sesungguhnya, maka BOP per satuan akan berfluktuasi dari waktu ke waktu

3. pada perusahaan yang menerapkan metode harga pokok pesanan, harga pokok dihitung bila pesanan selesai diproses, tetapi ada unsur BOP yang besarnya belum dapat diketahui pada saat pesanan selesai diproses

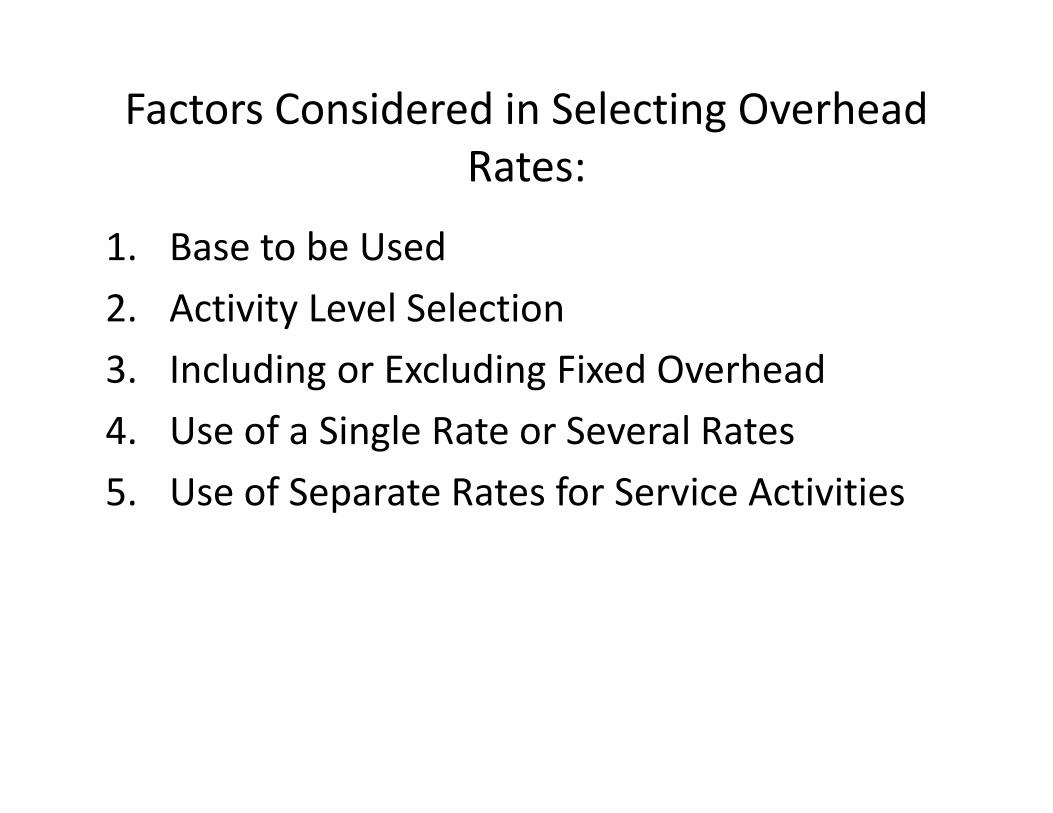

Factors Considered in Selecting Overhead

Rates:

1. Base to be Used

2. Activity Level Selection

3. Including or Excluding Fixed Overhead

4. Use of a Single Rate or Several Rates4. Use of a Single Rate or Several Rates

5. Use of Separate Rates for Service Activities

Base to be used

The factor measured in the denominator of an

overhead rate is called the overhead rate base, the

overhead allocation base, or simply the base.

a. Physical output

b. Direct materials

c. Direct labor

d. Direct labor hours

e. Machine hours

f. Transaction or activities

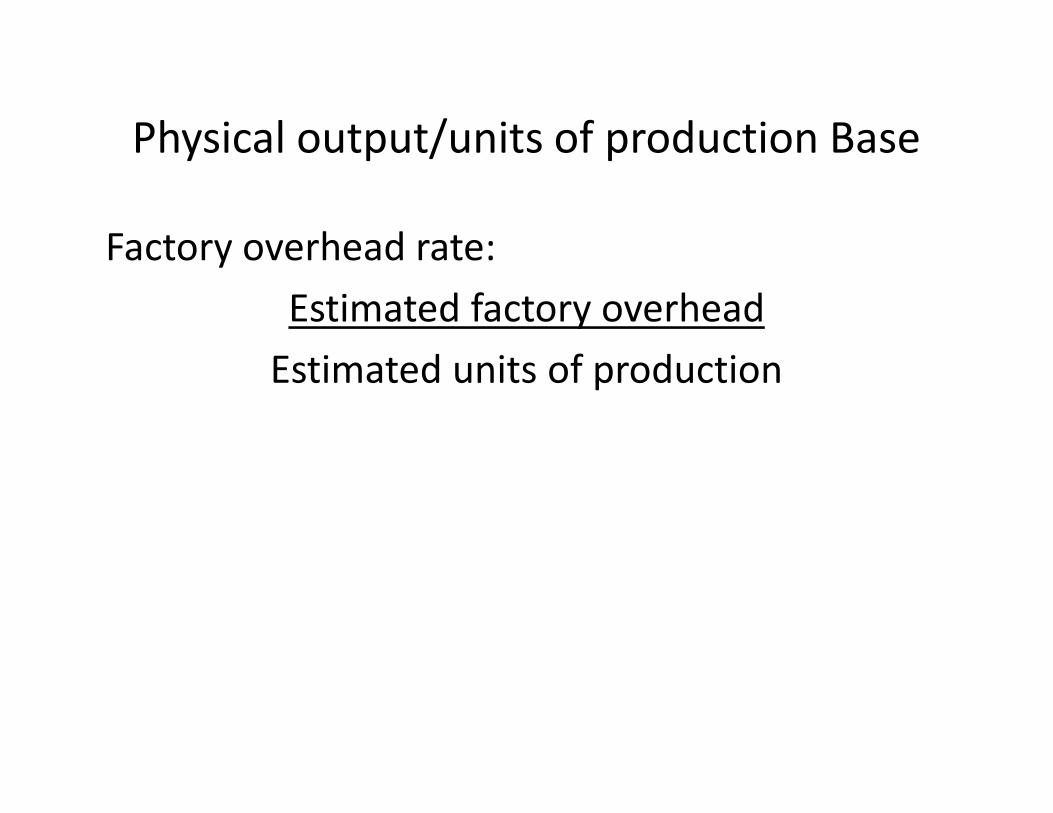

Physical output/units of production Base

Factory overhead rate:

Estimated factory overhead

Estimated units of production

Direct materials Base

Factory overhead rate:

Estimated factory overhead x 100%

Estimated direct materials

Direct labor Base

Factory overhead rate:

Estimated factory overhead x 100%

Estimated direct labor

Direct labor hour Base

Factory overhead rate:

Estimated factory overhead

Estimated direct labor hours

Machine hour Base

Factory overhead rate:

Estimated factory overhead

Estimated machine hours

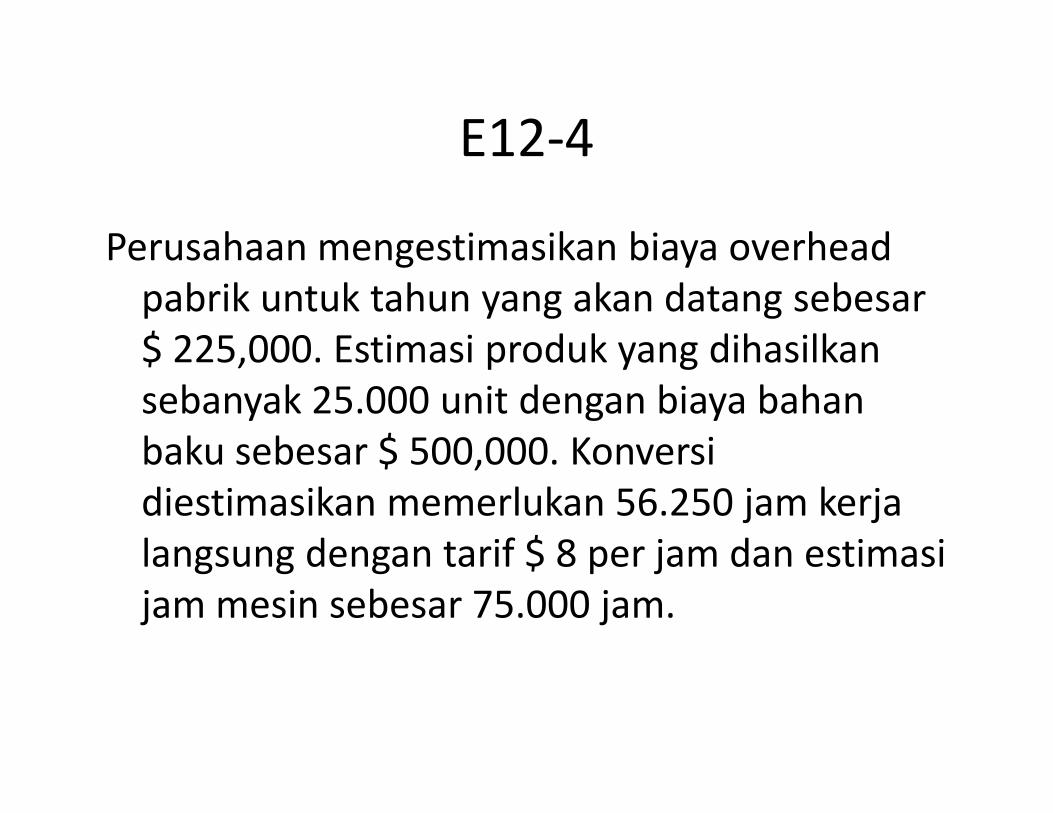

E12-4

Perusahaan mengestimasikan biaya overhead

pabrik untuk tahun yang akan datang sebesar

$ 225,000. Estimasi produk yang dihasilkan

sebanyak 25.000 unit dengan biaya bahan sebanyak 25.000 unit dengan biaya bahan

baku sebesar $ 500,000. Konversi

diestimasikan memerlukan 56.250 jam kerja

langsung dengan tarif $ 8 per jam dan estimasi

jam mesin sebesar 75.000 jam.

Tarif BOP yang ditentukan dimuka:

Berdasarkan,

(1) Units of production

(2) Materials cost

(3) Direct labor hours(3) Direct labor hours

(4) Direct labor cost

(5) Machine hours

• Ordinarily the Base should be closely related to

functions represented by the overhead cost

being applied.

• Based to be Used � Physical Output, Direct

Materials Cost, Direct Labor Cost, Direct Labor

Hours, Machine Hours

Activity Level Selection

• Theoretical Capacity

• Practical Capacity

• Expected Actual Capacity

• Normal Capacity• Normal Capacity

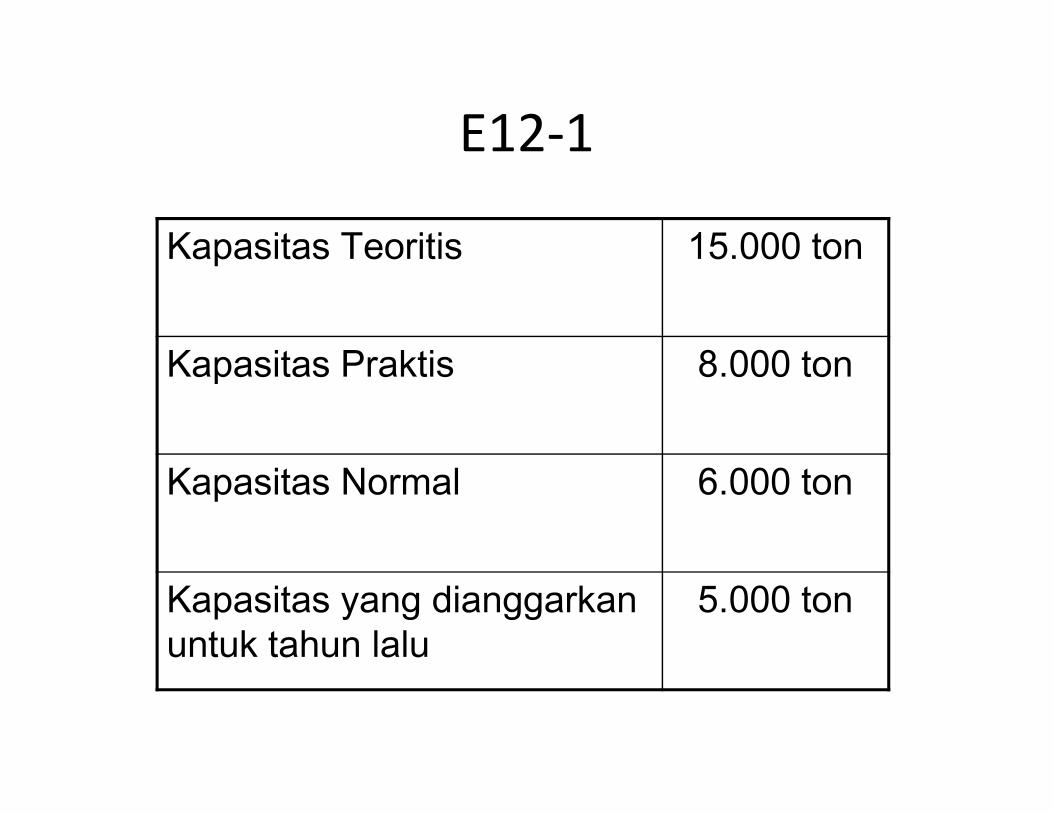

E12-1

Kapasitas Teoritis 15.000 ton

Kapasitas Praktis 8.000 ton

Kapasitas Normal 6.000 ton

Kapasitas yang dianggarkan untuk tahun lalu

5.000 ton

• Anggaran BOP pada kapasitas sesungguhnya

yang diharapkan sebesar $ 5,350,000.

• Anggaran BOP pada kapasitas normal sebesar

$ 6,070,000$ 6,070,000

Tentukan tarif BOP pada setiap kapasitas!

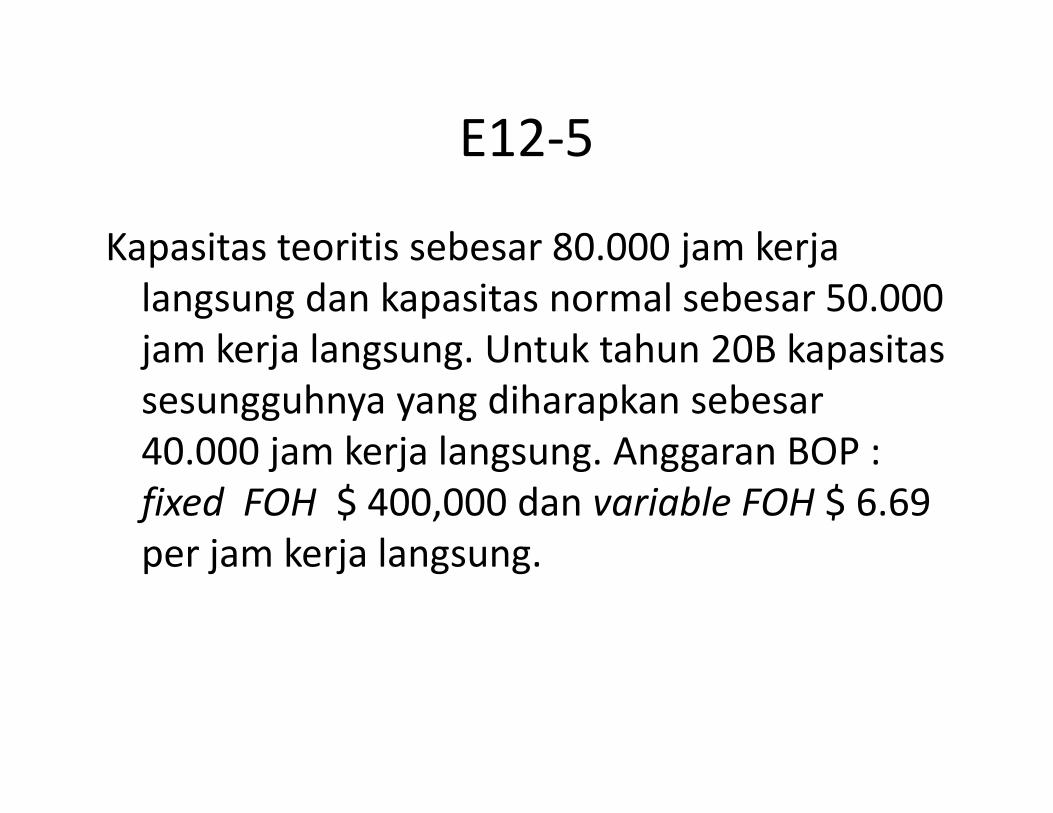

E12-5

Kapasitas teoritis sebesar 80.000 jam kerja

langsung dan kapasitas normal sebesar 50.000

jam kerja langsung. Untuk tahun 20B kapasitas

sesungguhnya yang diharapkan sebesar sesungguhnya yang diharapkan sebesar

40.000 jam kerja langsung. Anggaran BOP :

fixed FOH $ 400,000 dan variable FOH $ 6.69

per jam kerja langsung.

Accounting for Overhead

• Actual costs will almost never equal budgeted

costs. Accordingly, an imbalance situation

exists between the two overhead accounts

– If Overhead Control > Overhead Allocated, this is – If Overhead Control > Overhead Allocated, this is

called Underallocated Overhead

– If Overhead Control < Overhead Allocated, this is

called Overallocated Overhead

Over/Under applied FOH

• Actual FOH is the amount of indirect production cost incurred.

• Applied FOH is the amount of indirect production cost allocated to output.

FOH controlFOH control

Various credits

Work In Process

Applied FOH

Applied FOH

FOH control

Income Summary/Cost of Goods Sold

FOH control

• This difference will be eliminated in the end-

of-period adjusting entry process, using one of

three possible methods

• The choice of method should be based on • The choice of method should be based on

such issues as materiality, consistency, and

industry practice

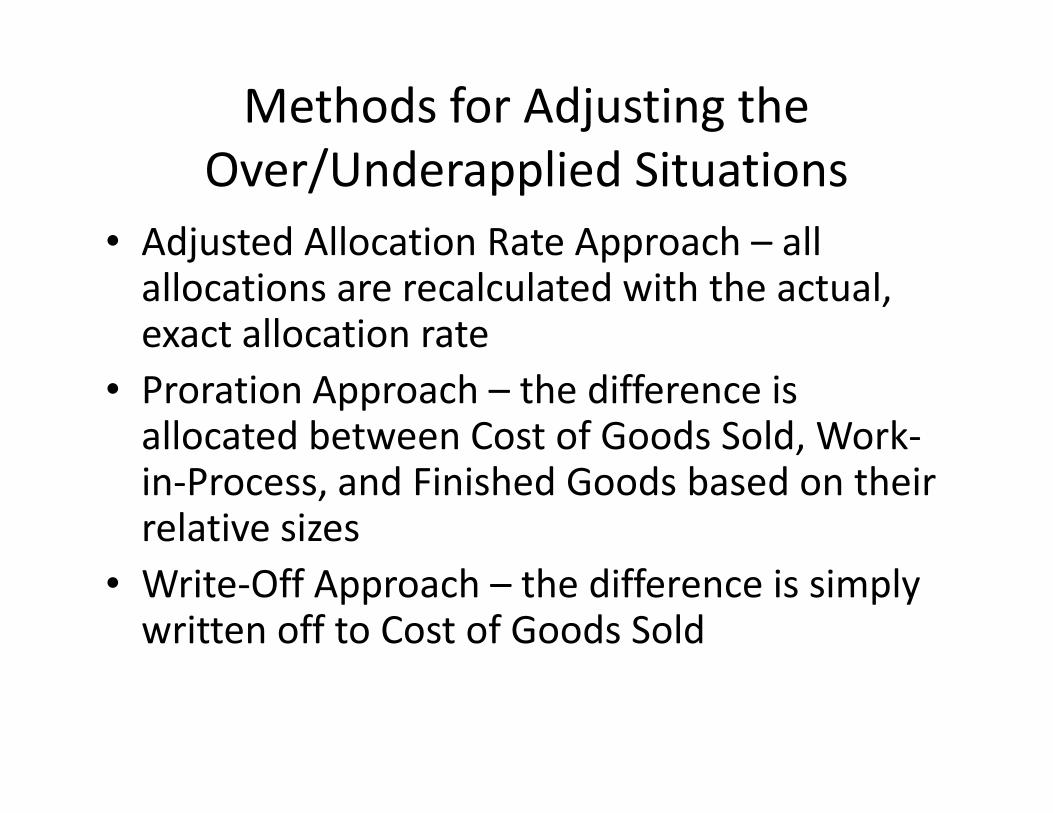

Methods for Adjusting the

Over/Underapplied Situations

• Adjusted Allocation Rate Approach – all allocations are recalculated with the actual, exact allocation rate

• Proration Approach – the difference is • Proration Approach – the difference is allocated between Cost of Goods Sold, Work-in-Process, and Finished Goods based on their relative sizes

• Write-Off Approach – the difference is simply written off to Cost of Goods Sold

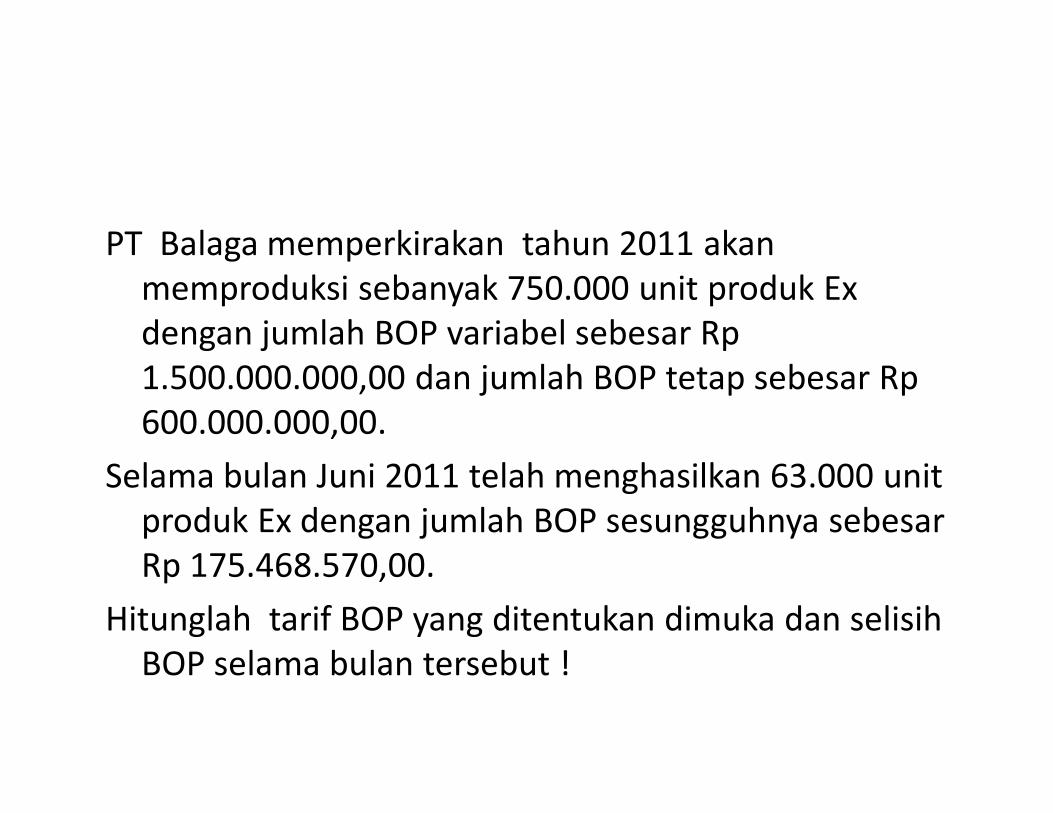

PT Balaga memperkirakan tahun 2011 akan

memproduksi sebanyak 750.000 unit produk Ex

dengan jumlah BOP variabel sebesar Rp

1.500.000.000,00 dan jumlah BOP tetap sebesar Rp

600.000.000,00. 600.000.000,00.

Selama bulan Juni 2011 telah menghasilkan 63.000 unit

produk Ex dengan jumlah BOP sesungguhnya sebesar

Rp 175.468.570,00.

Hitunglah tarif BOP yang ditentukan dimuka dan selisih

BOP selama bulan tersebut !