Factor Analysis of The Creditworthiness of an Indonesian ...

16

Factor Analysis of The Creditworthiness of an Indonesian Peer-to- Peer Lending M Akhsanur Rofi1, Arghasa Rezaprasga1 1 PPM School of Management [email protected] Keywords: P2P lending; 5C credit model; creditworthiness. Abstract: The situation has been difficult for peer-to-peer lending to be widely accepted by the public if the risk for loan default is high. The paper will seek to explore what factors might influence loan creditworthiness in Indonesian P2P lending. It will examine the 5C credit model, regression analysis, business model canvas, industry analysis and how it pairs up with an unconventional financing method such as P2P lending. Primary research using interview and case study is conducted, with XYZ Indonesian lending platform as research focus. The result will be beneficial to develop P2P platform as well SMEs development in Indonesia. 1 INTRODUCTION Debt-based crowdfunding or peer-to-peer lending is byproduct of the information revolution that began over 20 years ago. The development of information technology has transformed the financial services industry and enable to created innovative business model. The rise of cloud-based computing has made it possible for peer-to-peer businesses such as Uber, Airbnb, and Go-jek to operate (Einav, Farronato, & Levin, 2016). Essentially, businesses have found a way to bring its consumers closer to the end product with minimal costs, as well as equity-based crowdfunding and peer-to-peer lending. Peer-to-peer lending refers to the practice where financial technology firms connect those who have money to invest with businesses who seek to raise its funds. P2P lending platforms act only as an intermediary between the investor and the borrower. This type of lending is traditionally only possible with banks (Baeck, Collins, & Zhang, 2014). Because it replaces banks as the intermediary, both investor & businesses reap the benefits. P2P lending offers a competitive Return on Investment for its investors, and it offers a competitive and convenient financing for its borrowers. The loan is processed through a website owned by the P2P lending firm. The investors are able to set the amount, a desired interest rate, length of loan, and where they’re lending their money to. Some P2P lending platforms diversify the investor’s portfolio automatically. As of January 2017, around 60 million of Indonesians possesses a bank account, while the registered investment account in the Indonesian Stock Exchange is around 1 million, or around 0.59% owns an investment account (KoinWorks, 2017). Compared to other leading ASEAN countries, Indonesia has the lowest investment participation, percentage-wise. Table 1: Percentage of population with an investment account (KoinWorks, 2017) Most of Indonesians tends to reluctant to invest their money, instead they prefer to deposit it in banks (Djumena, 2015). According to the Indonesian Financial Services Authority (OJK), most Indonesians are unwilling to take the risk of investing in stocks, mutual funds, and bonds (Djumena, 2015). This may be caused by three Country Adult Population (millions) Percentage of Population with an Investment Account Indonesia 171 0.59% Malaysia 63.3 1.17% Thailand 39.4 4.90% Phillipines 23 10.85% Singapore 5 31.81%

Transcript of Factor Analysis of The Creditworthiness of an Indonesian ...

Factor Analysis of The Creditworthiness of an Indonesian Peer-to-Peer Lending M Akhsanur Rofi1, Arghasa Rezaprasga1 1PPM School of Management [email protected] Keywords: P2P lending; 5C credit model; creditworthiness. Abstract: The situation has been difficult for peer-to-peer lending to be widely accepted by the public if the risk for loan default is high. The paper will seek to explore what factors might influence loan creditworthiness in Indonesian P2P lending. It will examine the 5C credit model, regression analysis, business model canvas, industry analysis and how it pairs up with an unconventional financing method such as P2P lending. Primary research using interview and case study is conducted, with XYZ Indonesian lending platform as research focus. The result will be beneficial to develop P2P platform as well SMEs development in Indonesia. 1 INTRODUCTION Debt-based crowdfunding or peer-to-peer lending is byproduct of the information revolution that began over 20 years ago. The development of information technology has transformed the financial services industry and enable to created innovative business model. The rise of cloud-based computing has made it possible for peer-to-peer businesses such as Uber, Airbnb, and Go-jek to operate (Einav, Farronato, & Levin, 2016). Essentially, businesses have found a way to bring its consumers closer to the end product with minimal costs, as well as equity-based crowdfunding and peer-to-peer lending. Peer-to-peer lending refers to the practice where financial technology firms connect those who have money to invest with businesses who seek to raise its funds. P2P lending platforms act only as an intermediary between the investor and the borrower. This type of lending is traditionally only possible with banks (Baeck, Collins, & Zhang, 2014). Because it replaces banks as the intermediary, both investor & businesses reap the benefits. P2P lending offers a competitive Return on Investment for its investors, and it offers a competitive and convenient financing for its borrowers. The loan is processed through a website owned by the P2P lending firm. The investors are able to set the amount, a desired interest rate, length of loan, and where they’re lending their money to. Some P2P lending platforms diversify the investor’s portfolio automatically. As of January 2017, around 60 million of Indonesians possesses a bank account, while the registered investment account in the Indonesian Stock Exchange is around 1 million, or around 0.59% owns an investment account (KoinWorks, 2017). Compared to other leading ASEAN countries, Indonesia has the lowest investment participation, percentage-wise. Table 1: Percentage of population with an investment account (KoinWorks, 2017) Most of Indonesians tends to reluctant to invest their money, instead they prefer to deposit it in banks (Djumena, 2015). According to the Indonesian Financial Services Authority (OJK), most Indonesians are unwilling to take the risk of investing in stocks, mutual funds, and bonds (Djumena, 2015). This may be caused by three Country Adult Population (millions) Percentage of Population with an Investment AccountIndonesia 171 0.59%Malaysia 63.3 1.17%Thailand 39.4 4.90%Phillipines 23 10.85%Singapore 5 31.81%

factors. First, they don’t feel the need to invest. Secondly, most Indonesians feel like they live paycheck-to-paycheck. After transit costs, groceries, rent, and installment payments, they don’t have enough money left to invest. Third, they don’t consider the difference between saving and investing. One of the safest methods of investment is government bonds. The risk of default is very low, so the returns are small. Nevertheless, some fintech-enabled investments are considerably more profitable. Peer-to-peer lending offers high return along with low volatility rate. In 2016, the ROI from the three highest P2P lending platforms in Indonesia (KoinWorks, Investree, and Modalku) ranges from 17% to 20%. Compared to the Indonesia Composite Index at 15.3% on the same year, P2P lending is considerably attractive than other investment (Haryono, 2017). Additionally, the 17%-20% figure is composed of A-grade investments, which possesses the lowest risk and return available on P2P lending platforms in Indonesia. Risk taker investors could potentially obtain up to 38% interest rates if they are willing to invest in E-grade investments. (Möllenkamp, 2016). One of factors why the public are disinterested in investing is because lack of capital to invest properly. A misconception as there are P2P lending offers investment options for as low as IDR100,000. To alleviate the knowledge problem, plenty of P2P lending platforms have auto-invest feature which allows investors with minimum finance education let the algorithm allocate their investment in the platform across multiple businesses that are in line with their preferences (Shierly, 2017). The low minimum amount of investment also means that plenty of the recipients of said funding are composed of a high amount of Small, Micro, and Medium Enterprises (SMEs). These are local businesses which employ local workers, who bought from local suppliers, and sells to local customers. SMEs are the lifeblood of any country. In 2017, OJK stated that P2P lending has funded over 2.5 trillion IDR across multiple SMEs in Indonesia, Singapore, and Malaysia (Basari, 2018). The Ministry of Cooperatives of Indonesia released a law on 2008 regarding SMEs, which states that the criteria for businesses to be considered SMEs are its asset about IDR 0 – IDR 10 billion and revenue about IDR 0 – 50 billion. In 2016, SMEs contributed over 60% of Indonesia’s national GDP. They also have the capability to increase the nation’s quality of life in general. The rise of SMEs plays a strategic role in the war against poverty and unemployment (Audriene, 2016). OJK (2018) explained that the threshold for NPL is around 8%. KoinWorks holds a 5% NPL across its platform and assures that “Because their businesses are slowing down, they’re late for their loan payments. We will contact them, and they will usually pay their loan eventually. It’s very rare for us to write-off the loan.” Modalku stated its NPL was 0.8%. In contrast, XYZ (anonym) has managed to maintain a 0% NPL across their platform. This outstanding performance is why XYZ is the P2P lending platform interviewed for this study. It’s been difficult for a new alternative financing method to be widely accepted by the public if the risk for loan default is high. Thus, this paper will seek to explore the research question: “What factors might influence loan creditworthiness in Indonesian P2P lending?” 2 LITERATURE REVIEW 2.1 Credit and Commercial Lending Credit is a type of contractual agreement where a buyer borrows money to make a purchase and agrees to pay back the loan over time. Credit can also refer to the amount of money available to be borrowed. Also. Credit is an accounting term, an act that would decrease asset and increase liability. Businesses that intend to expand but lack the means to do so are able to apply for a commercial loan. A commercial loan is an agreement between a business and a financial institution, in which they act as the borrower and lender, respectively. Commercial loans are typically used to fund capital expenditure and operational costs that would otherwise be unaffordable for the business. This process is called commercial lending. Commercial lending mutually benefits both borrower and lender. With the newly acquired capital, the borrower is now able to adequately fund their business and generate wealth. Meanwhile, the lender periodically gains interest payments by the borrower, as well as a principal payment at the end of the agreed upon period. The art of lending has been perfected over time, which had evolved to conventional banking as we

know it. Risk management techniques had reached a point where it is so comprehensive and thorough it ended up being overly complex and lengthy. This is an acceptable tradeoff, as the alternatives of loan default and foreclosures would be worse for both the lender and the borrower (Ruth, 1987). The worst-case scenario for a commercial lending is if the lender ends up unable to repay their loan. To mitigate this risk, banks conduct an investigative process to determine whether a potential lender is fit for a loan or not. This usually begins with a loan application by the borrower, which then will be reviewed by the banks to weed out some glaringly obvious unfit borrowers. The remaining prospective borrowers is then invited to an interview with the commercial lender, followed by credit inquiries, on-site visits, business plan evaluation, financial statement analysis, collateral evaluation, and a presentation to the lender. The initial interview allows the lender to figure out the prospective borrower’s character. The interviewer needs to be an expert in effective communication. Listening, observing subtle social cues, as well as appearing emphatic are essential to able to accurately ask the right questions and gain the necessary information regarding the prospective borrower’s character. Then, the loan underwriter reviews the potential borrower’s financial profile. The underwriting process consists of detailed financial profile analysis, using metrics such as financial statements, credit history, employment history, and credit rating. Then, the financial information used in the underwriting process is verified, approved, & closing paperwork is signed by both parties. Due diligence is applied to every step of the loan review process. A well-known guideline for facilitating the due diligence process is the five C’s of credit. This guideline helps the underwriter get a structured look to analyze whether the lender decide to approve the loan or not. Out of the five components, capacity, capital, and collateral focuses as a basis for quantitative analysis. While Characters and Conditions are considered qualitative interpretation (Baiden, 2011). 2.1.1 Character Character refers to the customer’s apparent willingness to fulfill its loan obligation. One of the most useful metrics for this component is the number of loan inquiries made by the borrower in the past 6 months. An inquiry happens when a prospective borrower applies for a loan. When processing the application, lenders take note of the very act of the loan application itself. The inquiry will be used in the future as an additional consideration in case the borrower’s loan is rejected or it applies for another loan. Lenders view a high number of inquiries as ‘credit seeking behavior’, which may hurt the prospective borrower’s credit score (Snitkof, 2013). A credit seeking behavior may indicate that the borrower is in desperate need for cash and has been declined by several other lenders for a valid reason. Lendingclub, a P2P lending platform based in the U.S. has a feature to filter loans based on this metric. Below is data from July 2009 onwards, comparing number of inquiries in the past 6 months to the loan’s default rate. Table 2: Number of inquiries compare to default rate, source: Lendingclub.com 2.1.2 Capacity Capacity measures a borrower’s ability to fulfill its loan obligation. This can be done by assessing the borrower’s debt-to-income ratio. The maximum debt-to-income ratio allowed by P2P Lending companies differs for each platform, while some P2P platform doesn’t consider debt-to-income ratio as a criterion for funding. Prosper requires its borrowers to have a debt-to-income ratio to be below 50%, while LendingClub’s maximum debt-to-income ratio for its borrowers are 30%. While Investree take debt-to-income ratio into consideration when approving a loan, they do not have a concrete rule regarding debt-to-income ratio limit. 2.1.3 Capital Also known as equity, represents the amount of retained earnings the company possesses that could provide as a safety net in case the company faces unexpected losses. A strong equity numbers would show the business owner’s dedication to its company, which would mitigate the risk of default. This component helps the lender understand what

to expect in regards to how much the borrower would contribute to its business’ own assets (Baiden, 2011). A good capital indicates the owner’s confidence in their business, which strengthens the trust between the lender and borrower. 2.1.4 Collateral Collateral functions to assure the lender that if the borrower’s loan defaults, the lender can repossess the collateral. This component is irrelevant to P2P Lending in Indonesia, because borrowers are not obligated to provide collateral when applying for a loan via a P2P lending platform. At its principle, P2P Lending in Indonesia is focused to increase the financial inclusion of its citizens, which is why conventional banking regulations such as collateral requirement is not needed. 2.1.5 Conditions Conditions refer to external factors that might affect the borrower’s business. Whether it is an industry-wide, regional, national, or global change, this component includes every factor that might directly or indirectly affects the performance of the borrower’s business (Baiden, 2011). The terms and conditions of the loan also influence the lender’s desire to finance the borrower. Lenders review internal and external conditions of the company, analyzing factors such as their strengths, weaknesses, Porter’s five forces, the overall economy, and the background industry of the company. Conditions also describe the intended purpose of the loan. Whether the loan would be used for capital expenditure, operational costs, or inventory would be a factor depending on the business’ surrounding economic condition. To assess conditions, quantitative metrics such as the loan’s interest rate, principal amount, and loan period can also be used. 2.2 Financial Technology Financial Technology, or fintech, is one of the side effects of the ever-developing technological progress in the world. Technology has become advanced enough to offer viable financial services to citizens all over the world, and it may replace and disrupt the activity of conventional financial institutions. Fintech is not necessarily a bad thing; however, it is growing, adapting, and changing rapidly. It is tough to regulate fintech companies because of its inherent ties with technology growth. Technology is moving faster than lawmakers’ ability to create laws. Some country handles fintech differently; some tried to treat fintech companies as conventional financial institutions, and some constructed a system where fintech companies may conduct their operations freely under supervision by the country’s financial regulation (Zetzsche et al, 2017) in the form of a regulatory sandbox. 2.3 Startup Startups refer to companies that just got out of the seed stage in the business life cycle (Jablonski, 2016). Startups are commonly funded through private funds of the founder and its team. Startups usually offer innovative products or services that are competitive, innovative, and ‘rare’ in a sense that it is not being offered by many firms in the market (Fontinelle, A. 2017). Startups and small businesses often struggle with funding; it could be too small for an angel investor, and borrowing from banks is often a hassle. Banks are highly regulated; thus, it makes getting a loan very complicated and the amount needed may be too much to finance on the entrepreneur’s credit card. On the other hand, P2P lending allows borrowers to fund its business at a low interest rate, zero collateral, and no paperwork except for a few online forms with your digital signature (Daisme, 2017). 2.4 Regulatory Sandbox Newly formed conventional financial institutions usually have to go through strict financial regulations and a large capital requirement, and start-ups tend to not have the capability to fulfill either. To alleviate this barrier of entry, Indonesia’s Financial Services authority has applied a regulatory sandbox system in which new fintech start-ups are given a special probationary period. When fintech startups in Indonesia first start operating, the regulatory sandbox allows them to bypass some conventional financial regulations which require a large amount of time and capital to be complied with. However, Indonesia is not the only country to apply this sort of method, there are UK, Thailand, Malaysia, Singapore, UAE, Hongkong, and Canada as well (Oswaldo, 2017). Different countries have different approaches in regards to how to regulate crowdfunding platforms. The US attempts to treat it as a normal

financial firm and highly regulate it as they would normally regulate any banks or other financial institutions. But there are countries that are more lenient on regulating crowdfunding platforms, such as The UK (Freedman & Nutting, 2015). Home of one of the world’s largest crowdfunding platforms, CrowdCube, UK lawmakers actually apply little regulations for crowdfunding platforms and investors to engage in crowdfunding. Instead, policymakers in the UK allows fintech companies to almost freely operate under the condition that they agree to be placed in the government’s regulatory sandbox. Regulatory sandbox is a ‘safe space’ for startup fintech companies or incumbent financial institutions to develop and operate their innovative products in a real-world market, supervised by the financial regulator (Allen, 2017). 2.5 Crowdfunding History The core concept of crowdfunding is not a new thing. Pooling resources together as a community to reach a shared cause has been done in the past. However, the term ‘crowdfunding’ is relatively new. Before the term ‘crowdfunding’ existed, people refer to this type of fundraising method as ‘social lending’ (Hulme and Wright, 2006). Even though the act of social lending has always been there in the past, crowdfunding is still a force to be reckoned with. As is the case for most innovations, all financial technology is inherently disruptive. These innovations give people a way to bypass strict conventional banking criteria which would have inhibited their ability to apply for a loan or invest. Crowdfunding has the capability to reduce a country’s socio-economy gap, especially in developing countries (Buckingham et al, 2017). This is because crowdfunding allows people to spend a relatively small amount of capital to invest, which helps small-time investors and aspiring business owners. Previously, underserved and underbanked citizens would have a hard time raising funds to properly start a business. Crowdfunding increases the accessibility of investment and/or credit opportunities for underserved and underbanked citizens by offering them alternative financing methods such as peer-to-peer lending and equity-based crowdfunding (Buckingham et al, 2017). In 2012, JOBS Act (Jumpstart Our Business Startups) established in the US. The JOBS Act aims to help stimulate local businesses’ growth in an attempt to recuperate their weakened economy at the time. Title III of the JOBS Act essentially allows private participation of Title III crowdfunding portals by non-accredited as well as accredited investors (Moores, 2016). Back then, crowdfunding was a new concept that was relatively obscure. With the JOBS Act in place, citizens are allowed to spend their money directly to local businesses, which helps crowdfunding as a concept flourish in the US. Before the act, there are only around eight million accredited investors that are able to participate in angel investing. After the act, dozens of millions of citizens are able to be potential small-time investors, which helps local businesses as well as its investors (Freedman & Nutting, 2015). 2.6 Peer-to-Peer Lending Stakeholders Any crowdfunding project usually has three stakeholders; the business owner (borrower), the crowdfunding platform (website), and website visitors who are potential investors (Belleflamme et al., 2014). The three stakeholders are shown in the crowdfunding principle (Haas, Blohm, and Leimeister, 2014) below. Figure 1: Stakeholders in Crowdfunding (Source: Haas, Blohm, and Leimester (2014)) Capital-giving agents refer to institutions or ordinary people, who most likely would not have the means to invest using conventional methods. Capital-seeking agents refer to business owners who aim to raise its funds with crowdfunding. Crowdfunding intermediaries are the owner of the website.An underlying problem in P2P lending is information asymmetry, and how it causes the principal-agent problem between borrowers, lenders, and the platform. The borrower intends to maintain a good credit score to keep the interest rate as low as possible. Because of this, the

borrower may be inclined to hiding key information about their business that would lower their business’ perceived worth. On the other hand, lenders want to have as much information as possible to help them make an informed decision. Most P2P lending platforms publicly list the essential financial information of the borrowers’ business. Information such as income, expense, debt-to-income ratio (DTI), and overall credit score are accessible by the lenders— however, the credit score was determined by external rating agencies, who has access to a much more extensive personal data regarding the borrower (Bachmann, et al., 2011). 2.7 Crowdfunding Archetypes Crowdfunding can be categorized into four different categories; Donation-based crowdfunding, reward-based crowdfunding, debt-based crowdfunding, and equity-based crowdfunding (Cordova et al, 2015). Figure 2: Crowdfunding archetypes (Kirby & Worner, 2014) 2.7.1 Donation-based Crowdfunding In donation-based crowdfunding projects, campaign creators often seek funds to be put into a non-profit goal. Thus, financial backers of donation-based crowdfunding projects usually do not gain any tangible return for their money (Kunz et al. 2016). One of the largest donation-based crowdfunding projects in Indonesia is the Chiba Mosque project in Japan. In 2016, 3.2 billion IDR were raised in kitabisa.com for the Indonesian Muslim community in Chiba for them to buy a plot of land and construct a mosque. 2.7.2 Reward-based Crowdfunding The first crowdfunding site to gain mainstream attention was when Brian Camelio launched ArtistShare in 2003. Originally, it serves as a platform for musicians to obtain donations from their fan base to produce new music. The first crowdfunding project on the site sets a precedent on the tiered system that we still use in various platforms today. The project, “Concert in a Garden,” is a jazz album produced by Maria Schneider. The tiered reward system rewards its backers by giving them different benefits depending on how much they pledge. When an individual wants to raise funds for their project or company through crowdfunding, one must choose a crowdfunding platform to host their campaign. Before the campaign starts, the campaign creator lists in information regarding their project such as a funding target, campaign period, project type, etc. Once the campaign starts, visitors of the platform may choose to invest in the project if they are interested. If the campaign fulfilled 100% of the funding target within their campaign duration, the campaign is considered successful and gets funded by the platform. One of the largest crowdfunding platforms is Kickstarter.com. Total dollars pledged to Kickstarter projects amounts to $3.44 billion dollars, with 136,576 successfully funded projects and 42,628,199 pledges as of 2017. It adopts an “all-or-nothing” approach, in which projects that could not meet its target amount of funding will receive no funding at all. If the project fulfills its funding target, 95% of the raised funds are given to the creator of the project while Kickstarter takes a 5% fee. Oculus Rift, one of the most popular gadgets that pioneered a new age of Virtual Reality in the world were initially funded by a crowdfunding campaign in 2012. For a $275 contribution, for example, backers get an unassembled Rift prototype DIY kit for building the Rift from scratch. On a different tier, backers who pledged at least $500 gets a Rift developer kit, SDK, and engine integration docs which is targeted at an established or indie game developer interested in working with the Rift immediately. Seven backers who pledged $5000 were flied out to the Oculus lab in the US to spend a day with the Oculus Rift team itself, as well as a signed T-shirt, posters, etc, all signed by the entire Oculus Rift team in person, including all of the rewards from the previous tiers. The project proved successful, raising about $2.5 million from backers. Oculus Rift has grown massively since then, which caught the eye of Facebook, whom purchased Oculus for $2 billion in 2014.

2.7.3 Peer-to-Peer Lending Entrepreneurs or business owners create a campaign where they ask for funds to start their business. The campaign creator is expected to pay back a certain amount with interest within a certain period to its investors. Equity-based and donation-based are the most popular types of crowdfunding in Indonesia. This is because the OJK has authorized some peer-to-peer lending platforms to operate under their jurisdiction, which gives these platforms a sense of security and legitimacy on the eyes of investors. 2.7.4 Equity-based Crowdfunding Equity-based crowdfunding is similar to peer-to-peer lending in a way that the projects of these types of crowdfunding are for-profit. Instead of interest and principle, backers who pledged money in a successful equity-based crowdfunding project will receive a part of the company’s profits. Equity-based crowdfunding are perfect for growing businesses that are unable to fulfill the criteria of conventional fundraising methods like bank credit, angel investors, or venture capitalists. 2.8 Firm Life Cycle Following the rise of technology, crowdfunding in all its forms has grown as an alternative source of finance for numerous types of different projects, charities, and companies. A firm’s funding type is often tied to its current life cycle stage; from inception, pre-seed, seed, maturity, and decline. (Lukkarinen et al, 2015) Figure 3: A firm's funding source tied with its life cycle stage (World Bank, 2013) At the inception stage, most firms and projects are funded through personal funds, family, and friends. Venture capitalists and business angels often invest on after a firm had entered the seed stage; firms may be defined has having entered the seed stage after it had actually launched with a maximum revenue of $5,000 per month (Bulan and Subramanian, 2009). Firms at its maturity have plenty of funding options, from institutional investors to new market issues. Firms at its decline may engage in a takeover or liquidation to gain funding. This leaves the pre-seed stage void of funding methods, until reward and/or donation-based crowdfunding rose in popularity. The pre-seed stage is defined when the firm’s revenue is still zero as the firm has yet to release a product. However, unlike the Inception stage, the firm should have a prototype and personal cash flow ready at its disposal. At the pre-seed stage, companies often struggle with finding a suitable conventional investor. Risk-averse investors tend to stick to more mature firms, because it is difficult to gauge the viability and profitability of start-ups with no revenue. However, with reward-based crowdfunding, it is possible for firms to create a project without a conventional investor, bypassing the conventional fundraising method entirely. According to a study done by World Bank in 2013, crowdfunding may fill the pre-seed funding gap that many firms struggle with. 2.9 P2P Lending Risks & Fraud Prevention P2P lending is regulated through Financial Services Authority Regulation No. 77/POJK.01/2016 regarding IT-based lending services. The regulation is issued to enable the growth of the LPMUBTI industry (Layanan Pinjam Meminjam Uang Berbasis Teknologi Informasi). Imansyah, OJK Deputy Commissioner of Strategic Management 1A, explained that the LPMUBTI industry provides an alternative financing source for communities that couldn’t optimally make use of conventional financial services industries such as banks, capital market, financing companies, and venture capital firms. To anticipate for the rapid growth of the LPMUBTI industry, measures need to be taken by the government. Funds and data security, national interests, money laundering, terrorism funding, and overall stability of the financial system of the country are prone to risk. As mentioned above, Indonesia has adopted the regulatory sandbox in terms of fintech firms. Fintech firms are required to register under OJK before they can apply for licenses.

Under the regulatory sandbox, firms that have registered but haven’t obtained their license are allowed to conduct their business under supervision of the OJK. The probationary period has a time limit of one year after their registration, before the firm is obligated to apply for a license. To protect consumer interests, firms are required to open escrow accounts and virtual accounts at conventional banks and set up data centers in Indonesia. To maintain the financial stability of the country, LPMUBTI firms are only allowed to offer up to 2 billion IDR per borrower. There are two institutions that manage credit information in Indonesia, PT Kredit Biro Indonesia Jaya, and PT Pefindo Biro Kredit (PBK). P2P lending platforms use those credit reporting agencies’ services to rate loans submitted on their website. 3 METHODOLOGY This study gathers data through desk research from previously conducted research, thesis, journals, news, and textbooks regarding factors that might determine the creditworthiness of a P2P lending loan. Desk research, or secondary data analysis, is an analysis of data that was collected by another researcher for a different primary purpose (Johnston, 2013). This study also utilizes data gathered from interviews. Interviews are useful for getting an in-depth information around the topic. Interviews are particularly useful for getting the complete story that may be overlooked when only looking at the data from an outsider’s perspective (McNamara, 1999). Qualitative data are gathered by researchers through interviews or surveys. Compared to surveys, interviews allow the experts behind the data to explain their thought process and opinions regarding the subject in a greater depth (Kvale, 1996). 3.1 Influential Factors Identification Through desk research analysis, multiple possible factors that could influence the creditworthiness of a P2P lending loan are found. This study will examine the 5 C credit model, and how it pairs up with an unconventional financing method such as P2P lending. 3.2 Case Study Case study is used to investigate fields that have not been extensively researched (Dul and Hak, 2008). The case study approach is used to obtain an in-depth knowledge on the issue in a real-life context. This point is especially crucial, because there is a lot of data regarding P2P lending in Indonesia that is not made available to the public. Qualitative and quantitative analysis are used to investigate whether findings that are made in other countries would also apply in Indonesia. A regression analysis is made to prove the relationship between possible variables on the Five C’s of Credit and the possibility of loan default; number of credit inquiries in the last 6 months, debt-to-income, and background industry or loan purpose. After the literature review and research were conducted and thoroughly analyzed, the researcher identified which variable possesses the largest impact on the creditworthiness of the loan. Then, the implications of each variable are reviewed with the help of data gathered from the interview. After the implications of each variable had been analyzed, the researcher will attempt to conclude which factors are influential in determining the creditworthiness of a P2P lending loan. 3.2 Data Collection Because the P2P lending industry in Indonesia is relatively new, there are few studies publicly available regarding the topic that originates from Indonesia. This study uses desk research to gather data from previous studies such as Möllenkamp (2016), Buckingham (2017), and Baiden (2011) to be used as the foundation for P2P lending background and history. This study also utilizes interview as a method to gain in-depth knowledge regarding the topic in Indonesia. For this study, the researcher interviewed XYZ Director. The interview consists of open-ended questions to let the interviewee explain his though process and point of view. The P2P lending industry in Indonesia is not as transparent about its data compared to the U.S. (where detailed historical data regarding its clients are publicly available on the internet). As a follow-up to the interview, the researcher of this study also obtained a sample data of 70 successfully disbursed P2P lending loan projects from XYZ, all of which was completed in 2018.

3.3 Data Analysis In conventional financing, creditworthiness is often determined by a borrower’s FICO score. FICO score is a metric used by major credit agencies to rate a borrower’s creditworthiness. Since the Fair Isaac Company was founded in 1956, it has sold over 100 billion credit scores. The FICO score system is so widely used in the conventional credit scoring industry. Fair Isaacs issued 120 patents to secure its intellectual property, but other countries had its own forms of credit scoring method. In Indonesia, whenever a borrower is looking for a loan such as Kredit Tanpa Agunan (KTA), Kredit Pemilikan Rumah (KPR), or a Kredit Kendaraan Bermotor (KKB), a Sistem Layanan Informasi Keuangan (SLIK OJK) check is conducted. However, P2P lending platforms in Indonesia such as Modalku, Investree, and KoinWorks do not use conventional credit score as a metric in their loan list. Instead, most P2P lending platforms in Indonesia utilize a letter-based grading system. There are two major credit rating agencies responsible for the rating; PT Kredit Biro Indonesia Jaya, and PT Pefindo Biro Kredit. This study will attempt to analyze which factors are taken into consideration, and what are the implications of said factors in regards to the overall creditworthiness of a P2P lending loan. 4 RESULT 4.1 P2P Lending Business Model Canvas 4.1.1 Key Partners The three main stakeholders in P2P lending platforms are its investors, borrowers, and the government agency bodies responsible for the law regarding P2P lending. Because P2P lending platforms only act as an intermediary, those three forces are what allow P2P lending platforms to conduct its activities. 4.1.2 Key Activities P2P lending platforms need to maintain its website constantly, as it is where the marketplace is located. Borrowers who had their loan approved are placed on the website listing, and investors looking to invest their money browse the website listing. In-house credit assessment may be done by the platform to ensure the credit grades given to their loan applications are accurately portraying the risk and quality of the loan. The website maintenance and R&D of a P2P lending is essential to the company, which places more responsibility to their IT department. 4.1.3 Key Resources To properly conduct their activities, P2P lending platforms must possess a high-end IT backend code. This prevents fraud, as well as enhancing the customer experience at their website. Officially registering the platform under OJK also increases customer trust in the company. A strong core staff & management team is also important to make sure the platform is competitive compared to other P2P lending platforms. 4.1.4 Value Proposition P2P lending platforms offer low loan rates for borrowers, and high returns for investors. This is made possible by the fact that most of the process is digitalized with no paperwork, so P2P lending platforms enjoy a reduced overhead cost compared to a bank. P2P lending platforms also allow small-time investors and borrowers to invest and borrow from their website, which leads to an increase in overall economic activity and health of the country. 4.1.5 Customer Relationships P2P lending platforms openly state their terms and conditions for applying for a loan; there are no hidden costs. Borrowers are free to choose the terms of their loan. The process is purely online— it is quick, convenient, and efficient. Because 4.1.6 Customer Segments Borrower-wise, P2P lending allows people to set up their business with more convenience and flexibility. Borrowers without access to conventional financing methods could raise their funds through P2P lending. Investor-wise, people with limited amount of money can choose to invest their money via P2P lending. However, large investors or institutional investors looking to diversify their investments could also invest their money across multiple P2P lending loans.

4.1.7 Channels P2P lending platforms mainly centralize their communication in their website as a one-stop destination. The website is the lifeblood of any P2P lending platform, so it contains all the necessary information for the company. Some P2P lending platforms such as Investree, Modalku, and KoinWorks also have its own application available to be downloaded in the Google and Apple app store. They also have their own dedicated team to handle customer support and social media accounts, where users can inquire about the company. 4.1.8 Cost Structure Because the lending and investing process is completely online, the company does not incur as many expenses compared to a conventional bank. While P2P lending platforms serve people living on rural areas in Indonesia such as farmers, they do not need to come to a branch of the company to apply for a loan. Thus, the costs of rent, salaries and wages, and other numerous overheads are not incurred by the company. A substantial amount of the cost goes towards the IT backend infrastructure and R&D costs. They also need to pay for partner & legal fees, staff salaries, office rent, and taxes. 4.1.9 Revenue Streams P2P lending platforms receive a fee of every loan that gets funded, from 1% up to 5%. The amount of fees depends on the credit rating of the loan. Additionally, P2P lending platforms receive a 1% annual service fee from its investors. Baiden (2011) stated the five C’s of credit must be used comprehensively by lenders to stay competitive, because they are related to shareholders value and risk mitigation. Zhou et al, (2018) concluded the credit rating of the borrower has the strongest negative impact on the probability of loan default. Debt-to-income ratio and number of defaults within two years has a positive correlation on the probability of loan default. Then, Lust (2017) found that the more number of hard inquiries that have been made on the credit file of the borrower has a positive correlation to the probability of loan default. While Debt-to-income ratio has a positive correlation to the probability of loan default 4.2 P2P Lending Development in Indonesia The financial technology sector of Indonesia experienced a rise in popularity after OJK officially instated a rule that directly affects financial technology products in POJK no.77/POJK.01/2016. The shared opinion of both Bank Indonesia and Otoritas Jasa Keuangan is supportive of new and disruptive financial technology products. The total government support can be seen in the formation of PADG No. 19/14/PADG/2017 regarding Ruang Uji Coba Terbatas, or Regulatory Sandbox. Thie sandbox is in favor of new financial technology companies, where they are exempt in the same rules that apply to conventional institutions. These rule exemptions allow financial technology companies to freely innovate on their product, and not let the government slow them down with strict rules that require time to form. In 2016, Indonesia had one of the highest rates of alternative market growth in the Asia Pacific Region. The total market size of Indonesia in 2015 amounts to $2.26 million arose to $35.35m in 2016 (Buckingham et al, 2017). This growth in activity is due to increased public interest. Figure 4 Indonesia's total alternative finance market size 2013-2016 in million USD (Buckingham, 2017)

While the increase seemed very high, Indonesia’s alternative finance industry still has a long way to go in comparison to other countries of the Asia Pacific region. In 2016, the top three leading countries in the Asia Pacific region are Australia, Japan, and Korea, with $609.6m, $398.45m, and $376.31m, respectively (Buckingham et al, 2017). Figure 5: Total alternative finance market volume by country, in 2016 (Buckingham et al, 2017) Across the Asia Pacific region, P2P lending was the largest alternative finance model, with a total market share of 24% in 2016. It was followed by equity-based crowdfunding with 5%, reward-based crowdfunding with 3.04%, and donation-based crowdfunding at 2.75% (Buckingham, 2017). Figure 6: Composition of Asia Pacific alternative finance market, rounded up (2016) Both P2P lending and equity-based crowdfunding are classified as ‘for-profit crowdfunding’, which attracts investors and businesses with a high amount of capital. Meanwhile, reward-based crowdfunding and donation-based crowdfunding projects usually has a set amount of goal in terms of money. This leads to the market volume gap between those two types. Even so, equity-based crowdfunding’s market volume is still disproportionately small compared to P2P lending’s. This is due to the legal and regulatory ambiguities of equity-based crowdfunding (Pyburn, 2014). As previously mentioned in the paper, the U.S. has the JOBS Act, which actively promotes equity, debt, and reward-based crowdfunding. Without a similar act in the Asia Pacific region, equity-based crowdfunding is struggling legally. This phenomenon adversely affects the total market volume of equity-based crowdfunding in the Asia Pacific region. 4.3 XYZ’s P2P Lending Loan System XYZ is a fintech startup that offers P2P lending services since 2015. Operating under the special fintech law of POJK no.77/POJK.01/2016, XYZ is officially registered and supervised by OJK by the registration number S-2492/NB.111/2017. Naturally, when people conduct their transaction via P2P lending, there is no face-to-face activity involved. This may cause distrust and hesitation when people use these kinds of services. XYZ hope that OJK’s supervision will foster trust and cooperation amongst our borrowers, lenders, and stakeholders of our platform.” As stated in POJK no.77/POJK.01/2016, XYZ only serves as an intermediary platform. The company provides, maintains, and manages the website. Another takeaway from the terms and conditions is that lenders incur the risk of loan default on their own. Non-performing loans are not reimbursed by XYZ or any other government institution. To apply a loan through XYZ, borrowers will be required to provide personal details such as ID Card (KTP), Taxpayer Registration Number (NPWP), Certificate of Employment, and a valid pay stub. After the loan application is assessed and approved, the loan will be displayed on the XYZ marketplace. Compared to conventional financial institutions, the whole process is immensely more convenient, with no paperwork and flexible funding fees. The whole loan application process is online, so there is no paperwork involved— excluding the checklists on terms and services agreement pages.

The minimum principal loan value that XYZ will facilitate is IDR 5,000,000 and a maximum period of 12 months. This is designed to enable micro businesses to raise their funds through P2P lending. Interest rates will depend on the specific profile of each loan case-by-case, assessed by the team at XYZ. The process of assessment, selection, and approval by XYZ will take three working days at the most, provided that every required document has been completed. After that, the loan will immediately be put into the XYZ marketplace along with other loan applications for 14 days. If enough lenders fund the loan completely before 14 days, the funds can be immediately disbursed into the borrower’s account. However, if the pledged amount is below 60% of the target during the offering period, the borrower could either cancel or extend the loan application period. The policy is designed in such a way to mitigate risk for the platform, while making sure the platform is convenient enough for the user. 4.4 Case Study Result The study done by Baiden (2011) proves that a creditworthiness of a loan can be measured by the five C’s of credit. Mistakes in determining the creditworthiness of a loan may result in a loan default, or an increase in non-performing loan. As mentioned above, KoinWorks holds a 5% NPL across its platform. In the same period, Modalku’s NPL was 0.8%. So far, XYZ has been the only P2P lending platform in Indonesia that is free of NPL across their platform. To investigate which factors might contribute to the creditworthiness of a loan in P2P lending, the five C’s of credit model will be used as the main reference. Studies done by Serrano (2015), Lust (2017), and Zhou et al, (2018) all pinpoints to the same shared finding. In regards to the probability of loan default, credit rating is the single variable that possesses the highest predictive capability. Because XYZ does not have a statistically meaningful number of NPL, this study uses credit rating as a measure on the probability of loan default. 4.4.1 Character Character represents the borrower’s willingness to fulfill its loan obligation. This component is typically measured by the number of credit inquiries made in the last 6 months (Serrano, 2015). A study done by Serrano (2015) and Lust (2017) proved that there is a clear relationship between the number of inquiries made in the last 6 months and the probability of loan default. It is proven that the number of inquiries made in the last 6 months has a positive correlation in regards to the probability of loan default. Borrowers who rent their house have the highest probability of defaulting on his loan, while borrowers who own their own house have the lowest probability of default (Lust, 2017). Borrowers from XYZ have varied number of credit inquiries made in the last 6 months. Among 70 companies, the number of credit inquiries made in the last 6 months ranges from 0 to 12. XYZ assigns its borrowers to a grade-based credit rating, where the values range from A1++, A1+, A1, A2, A3, B1, B2, B3, C1, C2, and C3. In order to calculate the relationship between these two, credit grade is assigned into numerical values, from 11 to 1 (the higher, the better). If the theory is correct, companies with a low number of credit inquiries made in the last 6 months should possess a low numerical credit grade. To test this theory, regression analysis was used. Below is the summary output of the relationship between inquiries in the last 6 months and credit rating: Judging from the multiple R, the linear relationship of inquiries in the last 6 months is considered weak. The R square explains that the number of credit inquiries made little to no effect on credit rating. This result is contrarian to the results of previous studies done in different countries. This may be caused by the fact that out of 70 companies, there are 32 companies with 0 inquiries made in the last 6 months, skewing the data pool (as shown below). SUMMARY OUTPUTRegression StatisticsMultiple R 0.08143939R Square 0.006632374Adjusted R Square -0.007975973Standard Error 2.124563642Observations 70ANOVA df SS MS F Significance FRegression 1 2.049308903 2.049308903 0.454012633 0.502719559Residual 68 306.9364054 4.513770667Total 69 308.9857143Coefficients Standard Error t Stat P-value Lower 95% Upper 95% Lower 95.0% Upper 95.0%Intercept 5.690036309 0.297411034 19.13189378 4.46271E-29 5.096561831 6.283510787 5.096561831 6.283510787X Variable 1 -0.061885946 0.091845539 -0.673804595 0.502719559 -0.245160866 0.121388973 -0.245160866 0.121388973

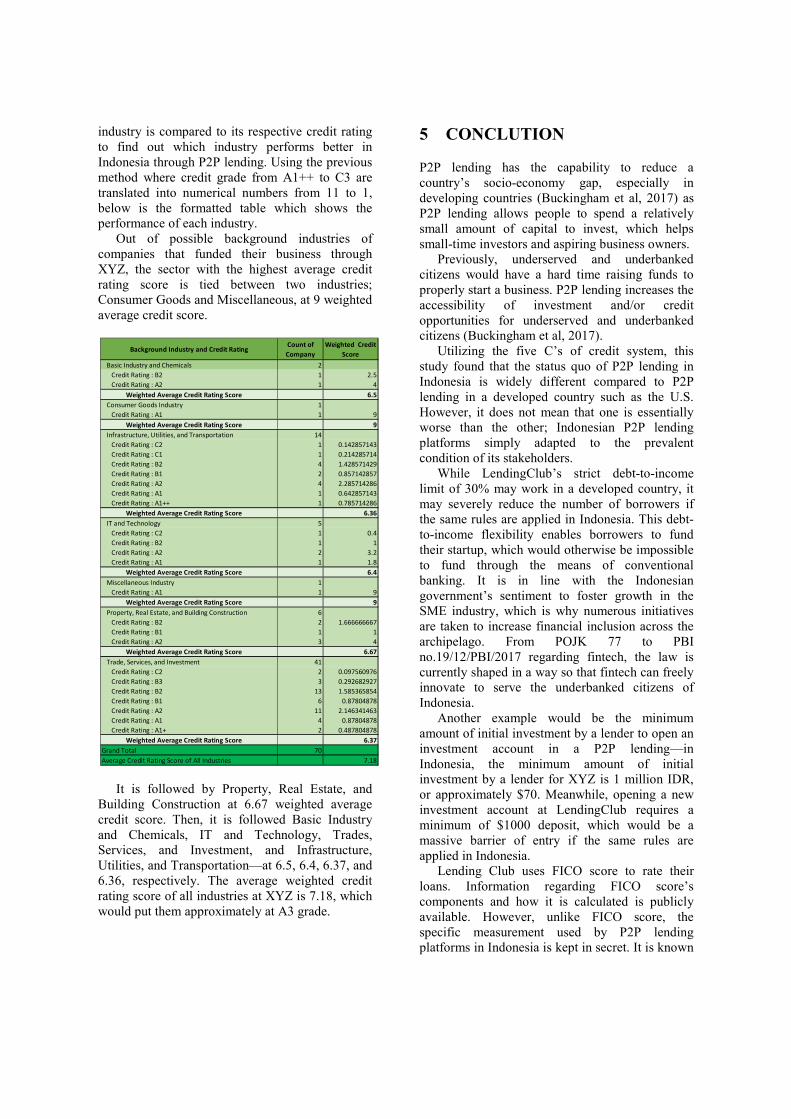

Figure 8 Composition of Asia Pacific alternative finance market, rounded up (2016) Thus, it can be considered that credit inquiries in the last 6 months is an insignificant factor in the creditworthiness of a P2P lending loan in Indonesia. 4.4.2 Capacity Capacity measures a borrower’s ability to fulfill its loan obligation. This can be done by assessing the borrower’s debt-to-income ratio. While XYZ take debt-to-income ratio into consideration when approving a loan, they do not have a concrete rule regarding debt-to-income ratio limit. This is shown in the data, where some companies have an estimate debt-to-income as high as 350%. This is also contrarian to Zhou’s (2018) findings where debt-to-income ratio mildly affects the probability of loan default in borrowers from LendingClub. LendingClub places a strict rule regarding debt-to-income ratio of its borrowers, where companies are required to keep their debt-to-income ratio below 30% if they were to apply for a loan in LendingClub. Below is a detailed look at companies, their debt-to-income ratio, and their background sector: Note that the debt-to-income ratio is a nearest approximation. Out of 70 companies, only 41 companies’ debt-to-income ratio is shown. While most of those companies hold a 75% debt-to-income ratio, this table shows that XYZ’s credit assessors allow companies with a much higher debt-to-income ratio. This difference to previous studies’ findings may be due to the fact that XYZ’s motto is “We facilitate digital financial inclusion.” In Indonesia, P2P lending caters to startup micro businesses which are often considered unbankable. Thus, debt-to-income ratio can be considered as an insignificant factor in the creditworthiness of P2P lending in Indonesia. 4.4.3 Capital A strong equity numbers would show the business owner’s dedication to its company, which would mitigate the risk of default. This component helps the lender understand what to expect in regards to how much the borrower would contribute to its business’ own assets (Baiden, 2011). However, data regarding each company’s equity on XYZ is confidential, so this study is unable to test the relationship between the company’s debt-to-equity ratios to its credit rating. 4.4.4 Collateral Collateral functions to assure the lender that if the borrower’s loan defaults, the lender can repossess the collateral. This component is irrelevant to P2P Lending in Indonesia, because borrowers are not obligated to provide collateral when applying for a loan via a P2P lending platform. At its principle, P2P Lending in Indonesia is focused to increase the financial inclusion of its citizens, which is why conventional banking regulations such as collateral requirement are not needed. Borrowers are only required to provide their personal details such as ID Card (KTP), Taxpayer Registration Number (NPWP), Certificate of Employment, and a valid pay stub. 4.4.5 Conditions Conditions refer to external factors that might affect the borrower’s business. Whether it is an industry-wide, regional, national, or global change, this component includes every factor that might directly or indirectly affects the performance of the borrower’s business (Baiden, 2011). To measure this component, each company’s background Credit Inquiries Count of Companies0 321 152 83 44 55 17 18 212 115 1Grand Total 70

industry is compared to its respective credit rating to find out which industry performs better in Indonesia through P2P lending. Using the previous method where credit grade from A1++ to C3 are translated into numerical numbers from 11 to 1, below is the formatted table which shows the performance of each industry. Out of possible background industries of companies that funded their business through XYZ, the sector with the highest average credit rating score is tied between two industries; Consumer Goods and Miscellaneous, at 9 weighted average credit score. It is followed by Property, Real Estate, and Building Construction at 6.67 weighted average credit score. Then, it is followed Basic Industry and Chemicals, IT and Technology, Trades, Services, and Investment, and Infrastructure, Utilities, and Transportation—at 6.5, 6.4, 6.37, and 6.36, respectively. The average weighted credit rating score of all industries at XYZ is 7.18, which would put them approximately at A3 grade. 5 CONCLUTION P2P lending has the capability to reduce a country’s socio-economy gap, especially in developing countries (Buckingham et al, 2017) as P2P lending allows people to spend a relatively small amount of capital to invest, which helps small-time investors and aspiring business owners. Previously, underserved and underbanked citizens would have a hard time raising funds to properly start a business. P2P lending increases the accessibility of investment and/or credit opportunities for underserved and underbanked citizens (Buckingham et al, 2017). Utilizing the five C’s of credit system, this study found that the status quo of P2P lending in Indonesia is widely different compared to P2P lending in a developed country such as the U.S. However, it does not mean that one is essentially worse than the other; Indonesian P2P lending platforms simply adapted to the prevalent condition of its stakeholders. While LendingClub’s strict debt-to-income limit of 30% may work in a developed country, it may severely reduce the number of borrowers if the same rules are applied in Indonesia. This debt-to-income flexibility enables borrowers to fund their startup, which would otherwise be impossible to fund through the means of conventional banking. It is in line with the Indonesian government’s sentiment to foster growth in the SME industry, which is why numerous initiatives are taken to increase financial inclusion across the archipelago. From POJK 77 to PBI no.19/12/PBI/2017 regarding fintech, the law is currently shaped in a way so that fintech can freely innovate to serve the underbanked citizens of Indonesia. Another example would be the minimum amount of initial investment by a lender to open an investment account in a P2P lending—in Indonesia, the minimum amount of initial investment by a lender for XYZ is 1 million IDR, or approximately $70. Meanwhile, opening a new investment account at LendingClub requires a minimum of $1000 deposit, which would be a massive barrier of entry if the same rules are applied in Indonesia. Lending Club uses FICO score to rate their loans. Information regarding FICO score’s components and how it is calculated is publicly available. However, unlike FICO score, the specific measurement used by P2P lending platforms in Indonesia is kept in secret. It is known Background Industry and Credit Rating Count of Company Weighted Credit ScoreBasic Industry and Chemicals 2Credit Rating : B2 1 2.5Credit Rating : A2 1 4Weighted Average Credit Rating Score 6.5Consumer Goods Industry 1Credit Rating : A1 1 9Weighted Average Credit Rating Score 9Infrastructure, Utilities, and Transportation 14Credit Rating : C2 1 0.142857143Credit Rating : C1 1 0.214285714Credit Rating : B2 4 1.428571429Credit Rating : B1 2 0.857142857Credit Rating : A2 4 2.285714286Credit Rating : A1 1 0.642857143Credit Rating : A1++ 1 0.785714286Weighted Average Credit Rating Score 6.36IT and Technology 5Credit Rating : C2 1 0.4Credit Rating : B2 1 1Credit Rating : A2 2 3.2Credit Rating : A1 1 1.8Weighted Average Credit Rating Score 6.4Miscellaneous Industry 1Credit Rating : A1 1 9Weighted Average Credit Rating Score 9Property, Real Estate, and Building Construction 6Credit Rating : B2 2 1.666666667Credit Rating : B1 1 1Credit Rating : A2 3 4Weighted Average Credit Rating Score 6.67Trade, Services, and Investment 41Credit Rating : C2 2 0.097560976Credit Rating : B3 3 0.292682927Credit Rating : B2 13 1.585365854Credit Rating : B1 6 0.87804878Credit Rating : A2 11 2.146341463Credit Rating : A1 4 0.87804878Credit Rating : A1+ 2 0.487804878Weighted Average Credit Rating Score 6.37Grand Total 70Average Credit Rating Score of All Industries 7.18

that PT Kredit Biro Indonesia Jaya and PT Pefindo Biro Kredit (PBK) are involved in the loan grade assessment of major P2P lending platforms in Indonesia, some platforms have their own private credit assessor in-house. One of the reasons XYZ is able to keep its default risk so low is because of their in-house credit assessor. XYZ still work with third-party credit rating agencies, however they take also take their in-house credit assessor’s opinion into consideration. REFERENCE Allen, H. (2017). A US Regulatory Sandbox Audriene, D. (2016). Kontribusi UMKM Terhadap PDB Tembus Lebih Dari 60 Persen. Retrieved from https://www.cnnindonesia.com/ekonomi/20161121122525-92-174080/kontribusi-umkm-terhadap-pdb-tembus-lebih-dari-60-persen Bachmann, A., Becker, A., Buerckner, D., Hilker, M., Kock, F., Lehmann, M., et al. (2011). Online Peer-to-Peer Lending – A Literature Review. Baeck, P., Collins, L., & Zhang, B. (2014). Understanding Alternative Finance. Baiden, J. (2011). The 5C's of Credit in the Lending industry. Basari, T. (2018). Modalku Jadi P2P Lending Pertama Penerima Sertifikasi ISO 27001. Retrieved from http://kalimantan.bisnis.com/read/20180308/105/747639/modalku-jadi-p2p-lending-pertama-penerima-sertifikasi-iso-27001 Belleflamme, P., Lambert, T., & Schwienbacher, A. (2013). Crowdfunding: Tapping the Right Crowd. Brüntje, D., & Gajda, O. (2016). Crowdfunding in Europe: State of the Art in Theory and Practice. Buckingham, E., Garvey, K., Chen, H.-Y., Zhang, B., Ralston, D., Katiforis, Y., et al. (2017). Cultivating Growth: The 2nd Asia Pacific Region Alternative Finance Industry Report. Bulan, L., & Subramanian, N. (2009). The Firm Life Cycle Theory and Dividends. Cabral, L. (2012). Reputation on the Internet. Cordova, A., Dolci, J., & Gianfrate, G. (n.d.). 2015. The Determinants of Crowdfunding Success: Evidence From Technology Projects. Cresswell, J. (2009). Research Design: Qualitative, Quantitative, and Mixed Methods Approaches. Daisme, P. (2017). Using Peer-to-Peer Lending As A Method For Startup Growth. Retrieved from https://www.forbes.com/sites/theyec/2017/07/26/using-peer-to-peer-lending-as-a-method-for-startup-growth/#5754f72f50f3 Djumena, E. (2015). Masyarakat Indonesia Masih Takut Investasi di Pasar Modal. Retrieved from Kompas: http://bisniskeuangan.kompas.com/read/2015/06/10/150500126/Masyarakat.Indonesia.Masih.Takut.Investasi.di.Pasar.Modal Dul, J., & Hak, T. (2008). Case Study Methodology in Business Research. Einav, L., Farronato, C., & Levin, J. (2016). Peer-to-Peer Markets. Fontinelle, A. (2017). Retrieved from https://www.investopedia.com/ask/answers/12/what-is-a-startup.asp Freedman, D., & Nutting, M. (2015). A Brief History of Crowdfunding. Gelderblom, O., & Joost, J. (2004). Completing a Financial Revolution: The Finance of the Dutch East India Trade and the Rise of the Amsterdam Capital Market, 1595-1612. Griffin, Z. (n.d.). 2012. Crowdfunding: Fleecing the American Masses. Haas, P., Blohm, I., & Leimister, J. (n.d.). 2012. An Empirical Taxonomy of Crowdfunding Intermediaries. Haryono, B. (2017). Meningkatkan Minat Investasi Melalui Peer-to-Peer Lending. Retrieved from https://fintech.id/Idea%20PDF/FinTech%20Talk%20-%20Opinion%20Editorial%2019%20-%20Meningkatkan%20Minat%20Investasi%20-%20Benedicto%20Haryono%20-%204%20April%202017.pdf Hulme, K., & Wright, C. (n.d.). 2006. Internet Based Social Lending. Jabłoński, A., & Jabłoński, M. (2016). Research on Business Models in their Life Cycle. Johnston, M. (2013). Secondary Data Analysis: A Method of which the Time Has Come. Kirby, E., & Worner, S. (2014). Crowd-funding: An Infant Industry Growing Fast. Kunz, M., Englisch, O., Beck, Jan, Bretschneider, & Ulrich. (2016). Sometimes You Win, Sometimes You Learn- Succcess Factors in Reward-Based Crowdfunding. Kvale, S. (1996). Interviews: An Introduction to Qualitative Research Interviewing. . Lukkarinen, A., Teich, J., Wallenius, H., & Wallenius, J. (2015). Success Drivers of Online Equity Crowdfunding Campaigns.

Lust, D. (2017). Analysis of Scoring in Peer-to-Peer Lending. Mcnamara, C. (1999). Conducting Interviews. Molick, E. (2013). Dynamics of Crowdfunding: An Exploratory Study. Möllenkamp, N. (2016). Determinants of Loan Performance in P2P Lending. Moores, C. (2015). Kickstart My Lawsuit: Fraud and Justice in Rewards-Based Crowdfunding. Neuman, L. (2013). Social Research Methods: Qualitative and Quantitative Approaches. Paakkarinen, P. (2016). Success Factors in Reward based and Equity based Crowdfunding in Finland. Popper, B. (2015, 6 11). FTC announces it will go after scummy Kickstarter projects that steal backers’ money. Retrieved from https://www.theverge.com/2015/6/11/8765557/ftc-kickstarter-deceptive-fraud-doom-that-came-atlantic-city Pyburn, G. (2014). Crowdfunding (Equity-Based) in Asia-Pacific: Legal and Regulatory Ambiguities without an analogous US JOBS Act Exemption. Quinn, M. (2002). A Guide to Using Qualititative Research Methodology. Ruth, G. (1987). Commercial Lending. Schumacher, E. (1973). Small is Beautiful. Retrieved from http://www.daastol.com/books/Schumacher%20(1973)%20Small%20is%20Beautiful.pdf Serrano, C. (2015). Determinants of Default in P2P Lending. Shierly. (2017). Alasan Investasi P2P Lending yang Membuat Anda Sulit Menolak Berinvestasi. Retrieved from https://www.finansialku.com/5-alasan-investasi-p2p-lending/ Snitkof, D. (2013). Credit Variables Explained: Inquiries in the Last 6 Months. Steinberg, S. (2012). The Crowdfunding Bible: How to Raise Money For Any Startup, Video Game, or Project. Sue, V., & Lois, R. (2012). Conducting Online Surveys. Ungureanu, C. (2006). The Lisbon Strategy. Retrieved from http://www.ipe.ro/rjef/rjef1_06/rjef1_06_6.pdf Wu, J., Siegel, M., & Manion, J. (1999). Online Trading: An Internet Revolution. Zetsche, D., Buckley, R., Arner, D., & Barberis, J. (2017). Regulating a Revolution: From Regulatory Sandboxes to Smart Regulation