FA Tutorial - W3

35

-

Upload

prachideedwania898 -

Category

Documents

-

view

571 -

download

78

Transcript of FA Tutorial - W3

Revenue recognition:

Benefit is Measurable and Revenue has been Earned

Expense recognition:

Incurred and Match with Revenue

Revenue earned but cash not yet received: Accrued Revenue (Assets)

Expense incurred but cash not yet paid: Accrued Expense (Liability)

Cash paid but expense not yet incurred: Prepaid Expense (Asset)

Cash received but goods not yet delivered: Unearned Revenue (Liability)

Key Concept: Accrual Accounting

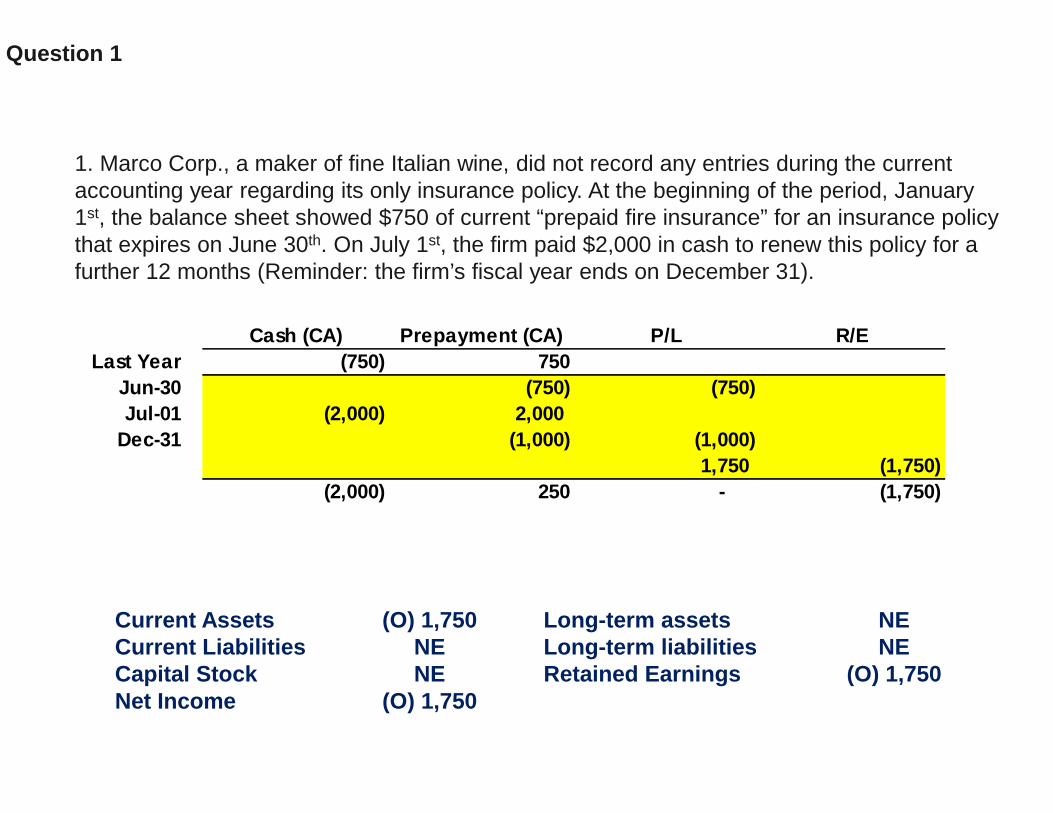

1. Marco Corp., a maker of fine Italian wine, did not record any entries during the current accounting year regarding its only insurance policy. At the beginning of the period, January 1st, the balance sheet showed $750 of current “prepaid fire insurance” for an insurance policy that expires on June 30th. On July 1st, the firm paid $2,000 in cash to renew this policy for a further 12 months (Reminder: the firm’s fiscal year ends on December 31).

Question 1

1. Marco Corp., a maker of fine Italian wine, did not record any entries during the current accounting year regarding its only insurance policy. At the beginning of the period, January 1st, the balance sheet showed $750 of current “prepaid fire insurance” for an insurance policy that expires on June 30th. On July 1st, the firm paid $2,000 in cash to renew this policy for a further 12 months (Reminder: the firm’s fiscal year ends on December 31).

Question 1

Cash (CA) Prepayment (CA) P/L R/ELast Year (750) 750

Jun-30 (750) (750)Jul-01 (2,000) 2,000

Dec-31 (1,000) (1,000)1,750 (1,750)

(2,000) 250 - (1,750)

1. Marco Corp., a maker of fine Italian wine, did not record any entries during the current accounting year regarding its only insurance policy. At the beginning of the period, January 1st, the balance sheet showed $750 of current “prepaid fire insurance” for an insurance policy that expires on June 30th. On July 1st, the firm paid $2,000 in cash to renew this policy for a further 12 months (Reminder: the firm’s fiscal year ends on December 31).

Question 1

Current Assets (O) 1,750 Long-term assets NECurrent Liabilities NE Long-term liabilities NECapital Stock NE Retained Earnings (O) 1,750Net Income (O) 1,750

Cash (CA) Prepayment (CA) P/L R/ELast Year (750) 750

Jun-30 (750) (750)Jul-01 (2,000) 2,000

Dec-31 (1,000) (1,000)1,750 (1,750)

(2,000) 250 - (1,750)

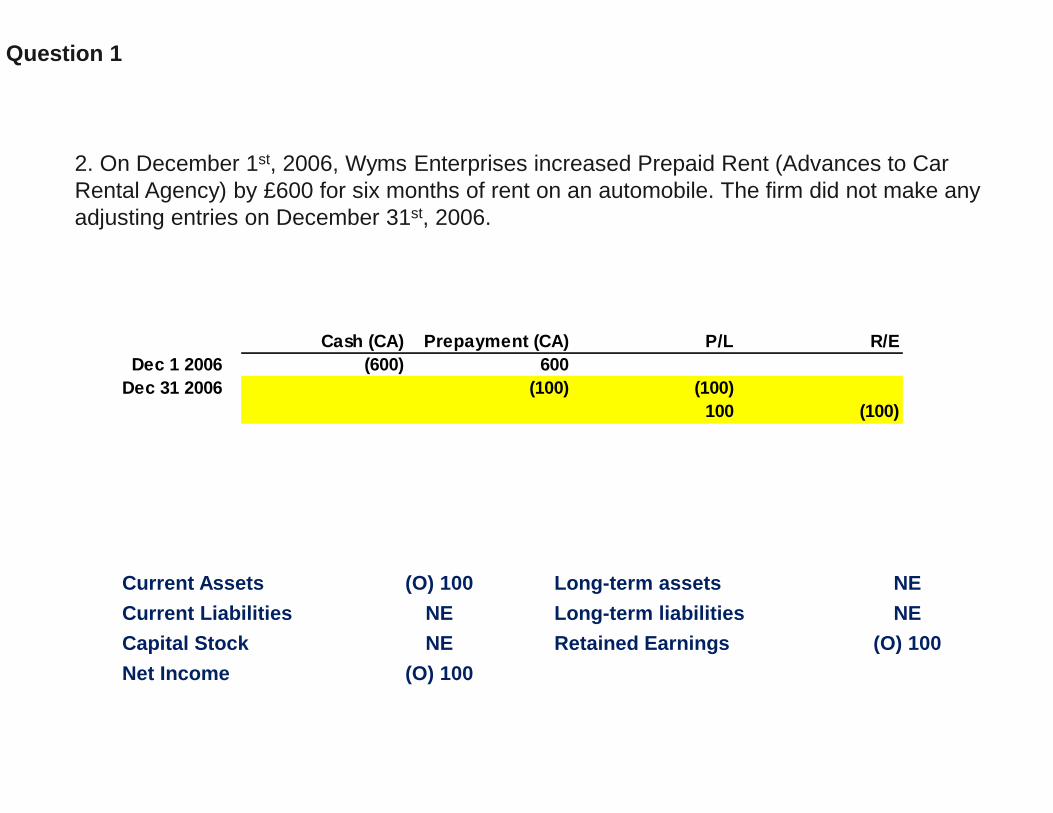

2. On December 1st, 2006, Wyms Enterprises increased Prepaid Rent (Advances to Car Rental Agency) by £600 for six months of rent on an automobile. The firm did not make any adjusting entries on December 31st, 2006.

Question 1

2. On December 1st, 2006, Wyms Enterprises increased Prepaid Rent (Advances to Car Rental Agency) by £600 for six months of rent on an automobile. The firm did not make any adjusting entries on December 31st, 2006.

Question 1

Cash (CA) Prepayment (CA) P/L R/EDec 1 2006 (600) 600

Dec 31 2006 (100) (100)100 (100)

2. On December 1st, 2006, Wyms Enterprises increased Prepaid Rent (Advances to Car Rental Agency) by £600 for six months of rent on an automobile. The firm did not make any adjusting entries on December 31st, 2006.

Question 1

Current Assets (O) 100 Long-term assets NE

Current Liabilities NE Long-term liabilities NE

Capital Stock NE Retained Earnings (O) 100

Net Income (O) 100

Cash (CA) Prepayment (CA) P/L R/EDec 1 2006 (600) 600

Dec 31 2006 (100) (100)100 (100)

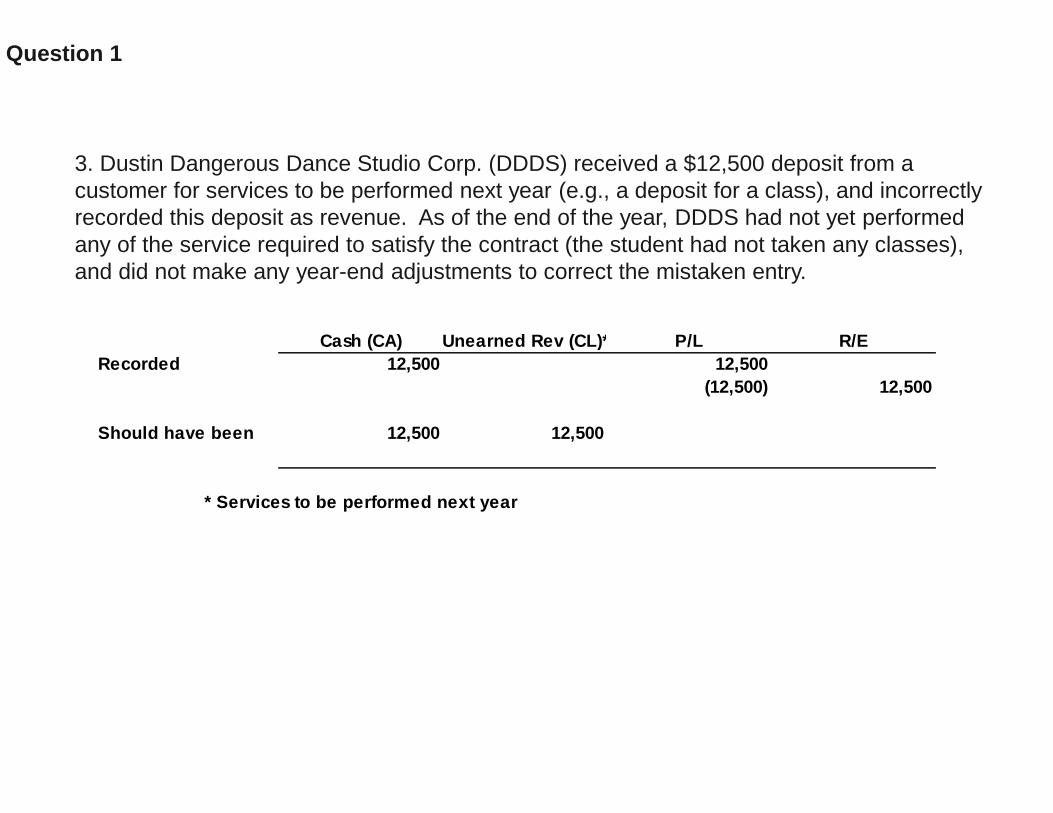

3. Dustin Dangerous Dance Studio Corp. (DDDS) received a $12,500 deposit from a customer for services to be performed next year (e.g., a deposit for a class), and incorrectly recorded this deposit as revenue. As of the end of the year, DDDS had not yet performed any of the service required to satisfy the contract (the student had not taken any classes), and did not make any year-end adjustments to correct the mistaken entry.

Question 1

3. Dustin Dangerous Dance Studio Corp. (DDDS) received a $12,500 deposit from a customer for services to be performed next year (e.g., a deposit for a class), and incorrectly recorded this deposit as revenue. As of the end of the year, DDDS had not yet performed any of the service required to satisfy the contract (the student had not taken any classes), and did not make any year-end adjustments to correct the mistaken entry.

Question 1

Cash (CA) Unearned Rev (CL)* P/L R/ERecorded 12,500 12,500

(12,500) 12,500

Should have been 12,500 12,500

* Services to be performed next year

3. Dustin Dangerous Dance Studio Corp. (DDDS) received a $12,500 deposit from a customer for services to be performed next year (e.g., a deposit for a class), and incorrectly recorded this deposit as revenue. As of the end of the year, DDDS had not yet performed any of the service required to satisfy the contract (the student had not taken any classes), and did not make any year-end adjustments to correct the mistaken entry.

Question 1

Current Assets NE Long-term assets NECurrent Liabilities (U) 12,500 Long-term liabilities NECapital Stock NE Retained Earnings (O) 12,500Net Income (O) 12,500

Cash (CA) Unearned Rev (CL)* P/L R/ERecorded 12,500 12,500

(12,500) 12,500

Should have been 12,500 12,500

* Services to be performed next year

1. What is the effect on the basic accounting equation of an entry recording the cash payment of salaries that were previously accrued?

(a) Decrease liabilities, decrease assets.

Question 2

When salaries accrued previously:

Accrued expense/liability P&L

XXX (XXX)

When salaries paid:

Cash Accrued expense/liability

(XXX) (XXX)

2. Which of the following circumstances would result in a decrease in income under accrual-based accounting but not under cash-based accounting?

(a) Purchase of inventory on account.(b) Payment of two months’ rent in advance.(c) The use of prepaid rent.(d) The return of defective inventory purchased on account, where full credit was given.(e) The payment of the current period's utility bill.

Question 2

Cash Inventory Prepayment A/P P&L

a) XX XX

b) (XX) XX

c) (XX) (XX)

d) (XX) (XX)

e) (XX) (XX)

Expense based on cash-accounting Expense based on accrual accounting

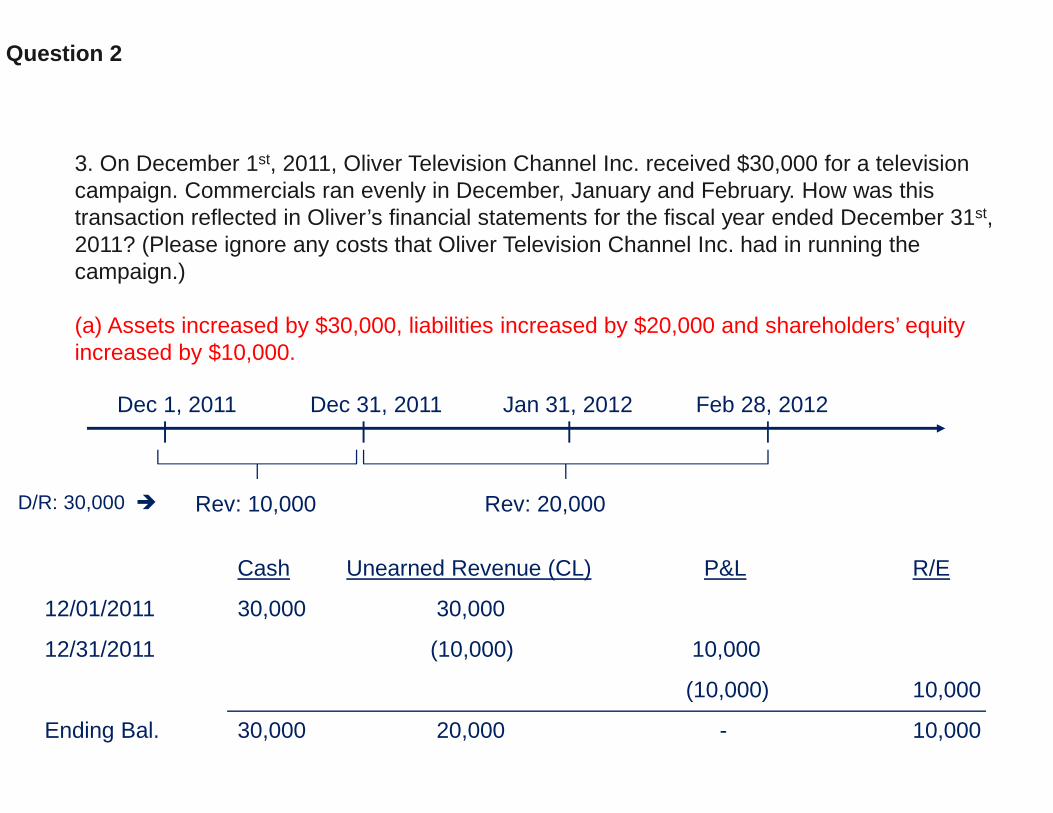

3. On December 1st, 2011, Oliver Television Channel Inc. received $30,000 for a television campaign. Commercials ran evenly in December, January and February. How was this transaction reflected in Oliver’s financial statements for the fiscal year ended December 31st, 2011? (Please ignore any costs that Oliver Television Channel Inc. had in running the campaign.)

(a) Assets increased by $30,000, liabilities increased by $20,000 and shareholders’ equity increased by $10,000.

Question 2

Dec 1, 2011 Dec 31, 2011 Jan 31, 2012 Feb 28, 2012

Cash Unearned Revenue (CL) P&L R/E

12/01/2011 30,000 30,000

12/31/2011 (10,000) 10,000

(10,000) 10,000

Ending Bal. 30,000 20,000 - 10,000

Rev: 10,000 Rev: 20,000D/R: 30,000 �

4. Puck Ltd started the fiscal year 2012 with a balance of $15,000 of prepaid rent. This prepayment covers the fiscal year of 2012 and the first 6 months of fiscal year 2013. Puck Ltd did not record any transactions related to this rent during fiscal year 2012. As a result:

(b) Assets are overstated by $10,000 and shareholders’ equity is overstated by $10,000.

Cash Prepaid Rent P&L R/E

FY2011 (15,000) 15,000

FY2012 (10,000) (10,000)

10,000 (10,000)

Question 2

FY 2012 FY2013

$15,000 prepaid rent pertains to 1.5 years.

$10,000 $ 5,000

5. On July 1st, 2009, Allen Company obtained a $50,000, one-year, bank loan at a 10% interest rate. At the due date, June 30, 2010, the principal and interest will be paid. Interest expense should be reported on the income statement for the year ended December 31, 2009 as

(b) $2,500.

Total interest for one year = 5,000 (50,000 x 10%) payable at June 30, 2010 with Principal.

2,500 2,500

Interest expense on Dec 31, 2009 P&L (Jul – Dec interest) = $2,500.

Question 2

Jul 1, 2009 Dec 31, 2009 Jun 30, 2010

Problem Set 1: Part II: Introduction to accrual accounting

Question 1: Locke Ltda. Locke Ltd has a year-end of December 31st. On August 31st, 2013, it paid (in cash) £27,000 of rent for the six months ending on February 28th, 2014. What amount should appear in the 2013 profit and loss account? What amount should appear on the closing balance sheet for 2013? Record these transactions in a transaction worksheet.

Problem Set 1: Part II: Introduction to accrual accounting

Question 1: Locke Ltda. Locke Ltd has a year-end of December 31st. On August 31st, 2013, it paid (in cash) £27,000 of rent for the six months ending on February 28th, 2014. What amount should appear in the 2013 profit and loss account? What amount should appear on the closing balance sheet for 2013? Record these transactions in a transaction worksheet.

Aug 31, 2013 Dec 31, 2013 Feb 28, 2014

Prepayment: 27,000

Expense: 27,000 * (4/6) = 18,000 Expense: 27,000 – 18,000 = 9,000

4 Mo. 2 Mo.

Problem Set 1: Part II: Introduction to accrual accounting

P&L Expense = 27,000 * (4/6) = 18,000

Prepayment = 27,000 - 18,000 = 9,000

ASSETS Shareholders’ Equity Date Cash Prepaid Rent P&L Retained Earn. Payment (27,000) 27,000 Rent Sep1- Dec31 (18,000) (18,000) Transfer to R/E 18,000 (18,000) Closing Balance (27,000) 9,000 - (18,000)

Question 1: Locke Ltda. Locke Ltd has a year-end of December 31st. On August 31st, 2013, it paid (in cash) £27,000 of rent for the six months ending on February 28th, 2014. What amount should appear in the 2013 profit and loss account? What amount should appear on the closing balance sheet for 2013? Record these transactions in a transaction worksheet.

Aug 31, 2013 Dec 31, 2013 Feb 28, 2014

Prepayment: 27,000

Expense: 27,000 * (4/6) = 18,000 Expense: 27,000 – 18,000 = 9,000

4 Mo. 2 Mo.

Problem Set 1: Part II: Introduction to accrual accounting

b. Now suppose that the next two semi-annual rent payments are:February 28th, 2014 £30,000August 31st, 2014 £36,000What amount should appear in the 2014 profit and loss account? What amount should appear on the closing balance sheet for 2014? Record these transactions in a transaction worksheet.

Problem Set 1: Part II: Introduction to accrual accounting

b. Now suppose that the next two semi-annual rent payments are:February 28th, 2014 £30,000August 31st, 2014 £36,000What amount should appear in the 2014 profit and loss account? What amount should appear on the closing balance sheet for 2014? Record these transactions in a transaction worksheet.

Aug 31, 2013 Dec 31, 2013 Feb 28, 2014 Aug 31, 2014 Dec 31, 2014 Feb 28, 2015

Prepayment:27,000

18,000 9,000 30,000

Prepayment:30,000

Prepayment:36,000

4 Mo.

Expenses:

4 Mo.6 Mo.2 Mo.

36,000 * (4/6) = 24,000 36,000 * (2/6) = 12,000

2 Mo.

Problem Set 1: Part II: Introduction to accrual accounting

P&L Expense = 9,000+30,000+24,000 = 63,000Prepayment= 36,000 * (2/6)= 12,000

ASSETS Shareholders’ Equity Cash Prepaid Rent P&L Retained Earn. Beginning Balance (27,000) 9,000 - (18,000) Rent Jan-Feb (9,000) (9,000) Payment (Feb) (30,000) 30,000 Rent Mar-Aug (30,000) (30,000) Payment (Aug) (36,000) 36,000 Rent Sep-Dec (24,000) (24,000) Transfer to R/E 63,000 (63,000) Closing balance (93,000) 12,000 - (81,000)

b. Now suppose that the next two semi-annual rent payments are:February 28th, 2014 £30,000August 31st, 2014 £36,000What amount should appear in the 2014 profit and loss account? What amount should appear on the closing balance sheet for 2014? Record these transactions in a transaction worksheet.

Aug 31, 2013 Dec 31, 2013 Feb 28, 2014 Aug 31, 2014 Dec 31, 2014 Feb 28, 2015

Prepayment:27,000

18,000 9,000 30,000

Prepayment:30,000

Prepayment:36,000

4 Mo.

Expenses:

4 Mo.6 Mo.2 Mo.

36,000 * (4/6) = 24,000 36,000 * (2/6) = 12,000

2 Mo.

Problem Set 1: Part II: Introduction to accrual accounting

Question 2: Descartes PlcOn December 31st, 2013, Descartes plc (which has a December 31st year-end) received and paid a telephone bill of £24,000 comprising:

Calls for the three months ended on December 31st, 2013 £18,000Rental for the six months ending on March 31st, 2014 £6,000

What amounts should appear in the 2013 profit and loss account and on the closing 2013 balance sheet in respect of this bill? Record these transactions in a transaction worksheet.

Problem Set 1: Part II: Introduction to accrual accounting

Question 2: Descartes PlcOn December 31st, 2013, Descartes plc (which has a December 31st year-end) received and paid a telephone bill of £24,000 comprising:

Calls for the three months ended on December 31st, 2013 £18,000Rental for the six months ending on March 31st, 2014 £6,000

What amounts should appear in the 2013 profit and loss account and on the closing 2013 balance sheet in respect of this bill? Record these transactions in a transaction worksheet.

Oct 1, 2013 Dec 31, 2013 Mar 31, 2014

Call expense = 18,000

3 Mo.

Rental expense = 6,000 * (3/6) = 3,000Rental expense = 3,000Prepaid rent = 6,000 for 6 Mo.

Problem Set 1: Part II: Introduction to accrual accounting

Question 2: Descartes PlcOn December 31st, 2013, Descartes plc (which has a December 31st year-end) received and paid a telephone bill of £24,000 comprising:

Calls for the three months ended on December 31st, 2013 £18,000Rental for the six months ending on March 31st, 2014 £6,000

What amounts should appear in the 2013 profit and loss account and on the closing 2013 balance sheet in respect of this bill? Record these transactions in a transaction worksheet.

P&L expense = 18,000 + 6,000 * (1/2) = 21,000Prepaid rent = 6,000 * (1/2) =3,000

ASSETS Shareholders’ Equity Cash Prepaid Rent P&L Retained Earn. Calls Oct-Dec (18,000) (18,000) Rental Jan-Mar (6,000) 3,000 (3,000) Transfer to R/E 21,000 (21,000) Ending Balance (24,000) 3,000 (21,000)

Oct 1, 2013 Dec 31, 2013 Mar 31, 2014

Call expense = 18,000

3 Mo.

Rental expense = 6,000 * (3/6) = 3,000Rental expense = 3,000Prepaid rent = 6,000 for 6 Mo.

Problem Set 1: Part III: General Concepts

1. On December 31st , 2012, Bingo Corp. borrowed $50,000 from a bank. Half of the loanwas to be repaid in 2013, and the other half in 2014. This entry was never recorded. The effect of this error in the financial statements for the fiscal year end 2012 was:

Should have recorded:

Cash (CA) Borrowing (Liab.)

50,000 25,000 � CL

25,000 � LTL

CA: (U) 50,000

CL: (U) 25,000

LTL: (U) 25,000

Problem Set 1: Part III: General Concepts

2. On December 31st, Plato Inc. bought inventory for $1,000, which was paid in cash. This entry was never recorded.

Should have recorded:

Cash (CA) Inventory (CA)

(1,000) 1,000

No Effect

Problem Set 1: Part III: General Concepts

3. On December 31st, Spyros Alarm Clocks Corp. borrowed $50,000 from a bank. This amount has to be repaid in 6 months. It used this money, along with $40,000 of its own money, to purchase a piece of machinery for its factory for $90,000. It forgot to record any entries for either of these transactions.

Should have recorded:

Cash (CA) Machinery (PPE) (LTA) Borrowing (CL)

50,000 50,000

(90,000) 90,000

(40,000) 90,000 50,000

CA: (O) 40,000

LTA: (U) 90,000

CL: (U) 50,000

Problem Set 1: Part III: General Concepts

4. Porter Wine Bar Inc. neglected to record any entries to recognize the issuance of common stock. The firm sold 100 shares on the open market and received $27 per share.

Should have recorded:

Cash (CA) Capital/Common Stock (Equity)

2,700 2,700

CA: (U) 2,700

C/S: (U) 2,700

Problem Set 1: Part III: General Concepts

5. A firm neglected to record any entries related to the sale of an item to a customer on credit. The item was in inventory at a cost of $4,000 at the time of sale and was sold for $5,000.

Should have recorded:

A/R (CA) Inventory (CA) P&L R/E

5,000 5,000

(4,000) (4,000)

(1,000) 1,000

CA: (U) 1,000

Income: (U) 1,000

R/E: (U) 1,000

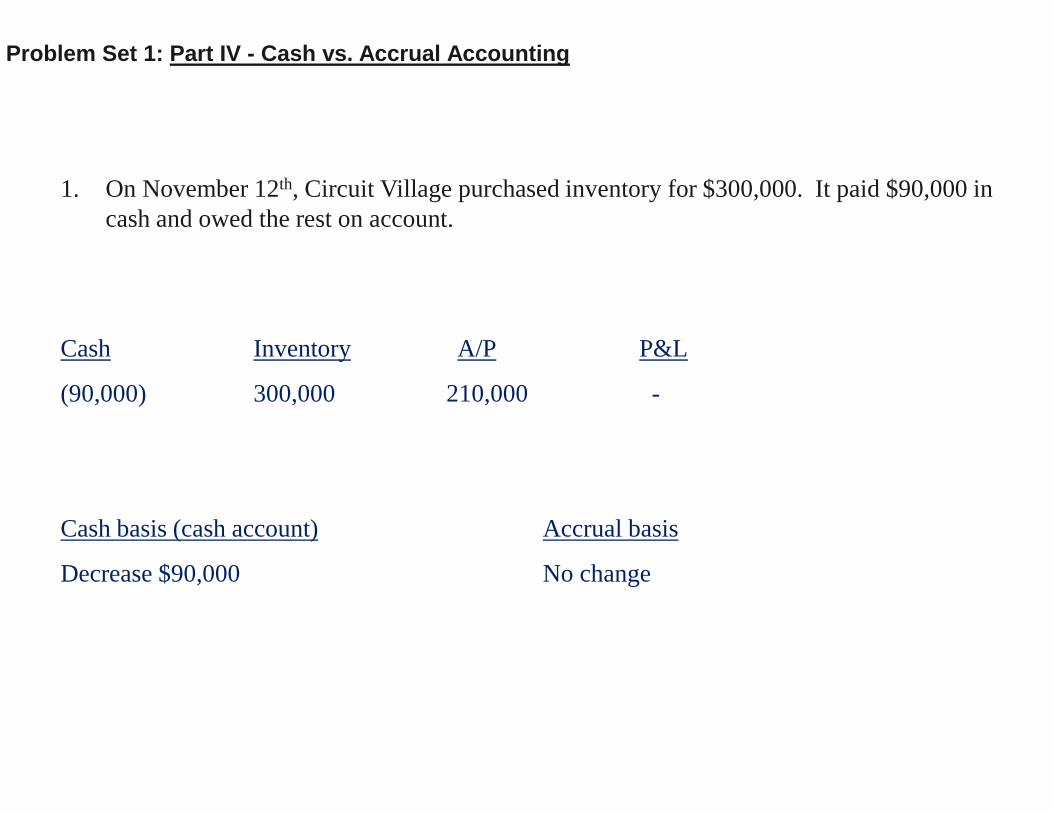

Problem Set 1: Part IV - Cash vs. Accrual Accounting

1. On November 12th, Circuit Village purchased inventory for $300,000. It paid $90,000 in cash and owed the rest on account.

Cash Inventory A/P P&L

(90,000) 300,000 210,000 -

Cash basis (cash account) Accrual basis

Decrease $90,000 No change

Problem Set 1: Part IV - Cash vs. Accrual Accounting

2. Circuit Village paid employees $15,000 in wages for work done during the year. An additional $1,000 for 2014 wages will be paid in January 2015.

Cash Accrued Exp (CL) P&L

(15,000) (15,000)

1,000 (1,000)

Cash basis (cash account) Accrual basis

Decrease $15,000 Decrease $16,000

Problem Set 1: Part IV - Cash vs. Accrual Accounting

3. On December 15th, Circuit Village paid $24,000 for a twelve month fire insurance policy that runs from December 16th, 2014 to December 15th, 2015. Include the effect of any adjusting entry necessary on December 31st.

Cash Prepayment (CA) P&L

(24,000) 24,000

(1,000)* (1,000)

* Monthly insurance premium = 24,000 / 12 = 2,000

Insurance expense from Dec 16, 2014 to Dec 31, 2014 = 2,000/2 = 1,000

Cash basis (cash account) Accrual basis

Decrease $ 24,000 Decrease $1,000

Problem Set 1: Part IV - Cash vs. Accrual Accounting

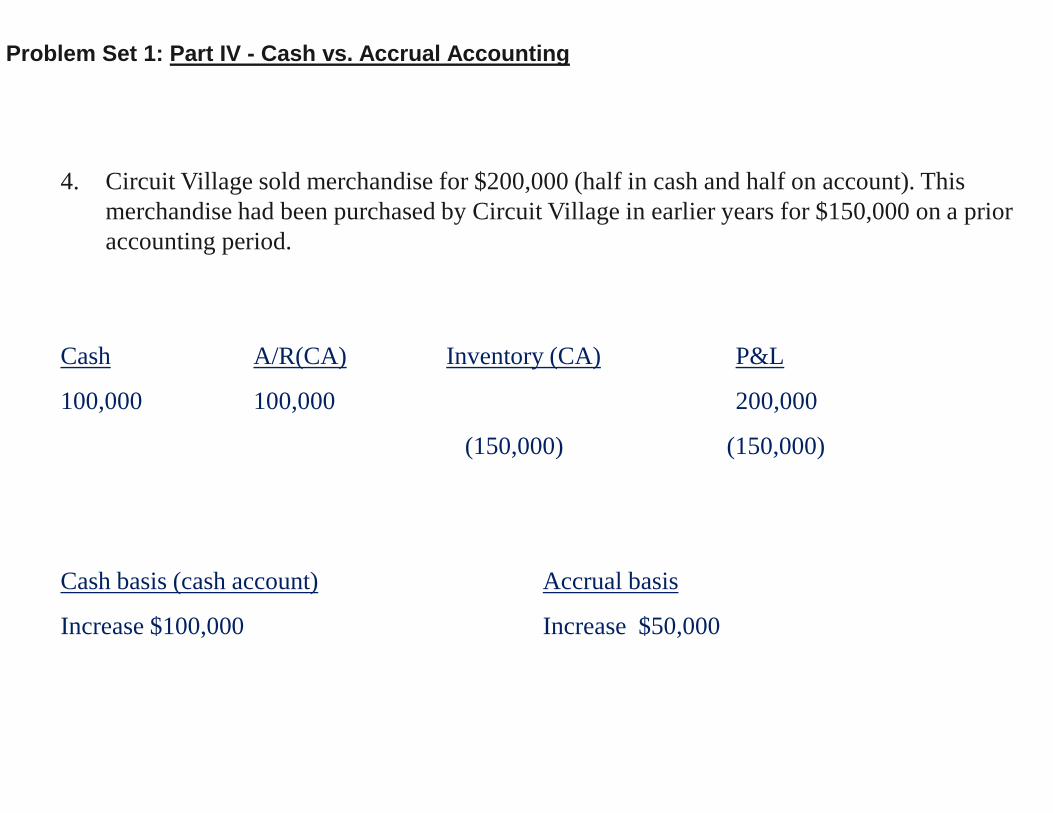

4. Circuit Village sold merchandise for $200,000 (half in cash and half on account). This merchandise had been purchased by Circuit Village in earlier years for $150,000 on a prior accounting period.

Cash A/R(CA) Inventory (CA) P&L

100,000 100,000 200,000

(150,000) (150,000)

Cash basis (cash account) Accrual basis

Increase $100,000 Increase $50,000

Problem Set 1: Part IV - Cash vs. Accrual Accounting

5. On December 20th, Circuit Village made $14,000 cash sales of gift certificates, which can be used to purchase merchandise at the store. None of the gift certificates were redeemed by December 31st.

Cash Deferred Revenue (CL) P&L

14,000 14,000 -

Cash basis (cash account) Accrual basis

Increase $14,000 No effect