Y E EY E EY E EY E E YOUNGEUROPEANENTERPRISE. España España.

Upload

ezzedine-ghlamallahCategory

view

203download

0

World Islamic Banking Competitiveness Report 2014–15 Participation Banking 2.0

About MEGAMEGA is the leading international information

business results for

MEGA brands represents

WIBC is a MEGA Brand MEGA Brands. MEGA Clients. Market Leaders.

More than 20 Years of Market Leadership

Dear Banking and Finance Leader,

Yours sincerely,

David McLean Chief Executive

Contents

Abdulaziz Al-Sowailim

World Islamic Banking Competitiveness Report 2014–156

82%

Ashar Nazim

World Islamic Banking Competitiveness Report 2014–15 7

Robert Abboud Jan Bellens

World Islamic Banking Competitiveness Report 2014–158

World Islamic Banking Competitiveness Report 2014–15 9

Customers: is anyone listening?•

•

Growth•

•

Connectivity: key to sustainable growth •

•

•

World Islamic Banking Competitiveness Report 2014–1510

Going mainstream: Participation Banking 2.0•

•

Customers•

•

World Islamic Banking Competitiveness Report 2014–15 11

World Islamic Banking Competitiveness Report 2014–1512

Industry overview

World Islamic Banking Competitiveness Report 2014–15 13

International Participation banking assets* (US$b)

295

517

71

160

333

93

385

117

454

140

2009 2010 2011 2012 2013

GCC ASEAN Turkey and ROW South Asia

41

78

11 50

14 53

17 69

20

23

417

778

17%

Share of international Participation banking assets*

0% 20% 40% 60% 80% 100%

Turkey and ROW

South Asia

ASEAN

GCC

Islamic Conventional Malaysia

5%

12%

14%

33%

World Islamic Banking Competitiveness Report 2014–1514

Banking penetration and Participation assets market share

Malaysia

Saudi Arabia

UAE

Kuwait

Qatar

Turkey

Bahrain

Indonesia

Bangladesh

Egypt

PakistanJordan

0%

20%

40%

60%

0% 50% 100% 150% 200% 250%

Part

icip

atio

n ba

nkin

g m

arke

t sha

re

Banking penetration

Size of circle depicts Participation banking asset volumes

Growth rate of assets YOY 2013 (in local currency)

–20% 0% 20% 40% 60% 80% 100%

Pakistan

Bahrain

Indonesia

Turkey

Qatar

Kuwait

UAE

Malaysia

Saudi Arabia

Conventional Islamic

CAGR 2009–13

17%

19%

11%

11%

26%

19%

43%

2%

29%

Going mainstream

World Islamic Banking Competitiveness Report 2014–15 15

Global distribution of Participation banking assets*

•

•

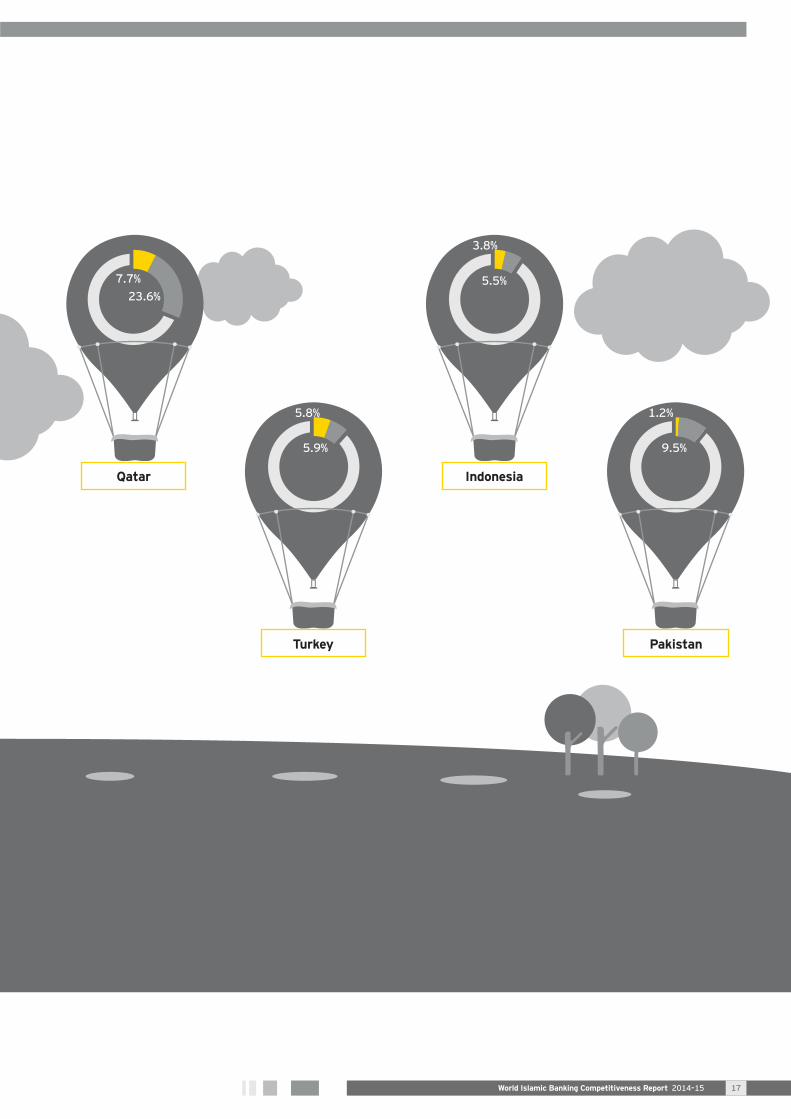

National market shares for Participation banking

•

•

Bahrain

31.7% 16.7%

48.9%20.7%

1.7%

27.7%

UAE

Saudi Arabia

Kuwait

Malaysia21.4% 44.6%

14.6%10.5%

World Islamic Banking Competitiveness Report 2014–1516

3.8%

5.5%

Turkey

IndonesiaQatar

23.6%

5.9%

7.7%

5.8%

Pakistan

9.5%

1.2%

World Islamic Banking Competitiveness Report 2014–15 17

Strengthening of capital base

•

•

Capitalization of top 20 banks

2010 2011–13

US$b

20%

CAR2013

17%

33%

18%

17%

19%

17%

21%

14%

15%

14%

19%

14%

13%

19%

14%

31%

16%

16%

14%

20%

CAR2012

13%

28%

17%

16%

19%

21%

17%

13%

16%

19%

19%

14%

15%

19%

14%

35%

16%

12%

14%

10 2 3 4 5 6 7 8 9 10 11

World Islamic Banking Competitiveness Report 2014–1518

•

•

Top 20 Participation banksAverage ROE 2009–2013Total assets 2013

0% 10% 20%020406080US$b

Average ROE

Average assets

Average growth 2009–13

Comparable

World Islamic Banking Competitiveness Report 2014–15 19

Future direction, opportunities and priorities for Participation banking

Initiatives to support implementation

• • • •

Opportunities ahead

• • •

• Contributing to the global dialogue

Challenges ahead

• •

•

Immediate sector priorities

• •

Impact of macro and environmental shifts

• • • • • •

World Islamic Banking Competitiveness Report 2014–1520

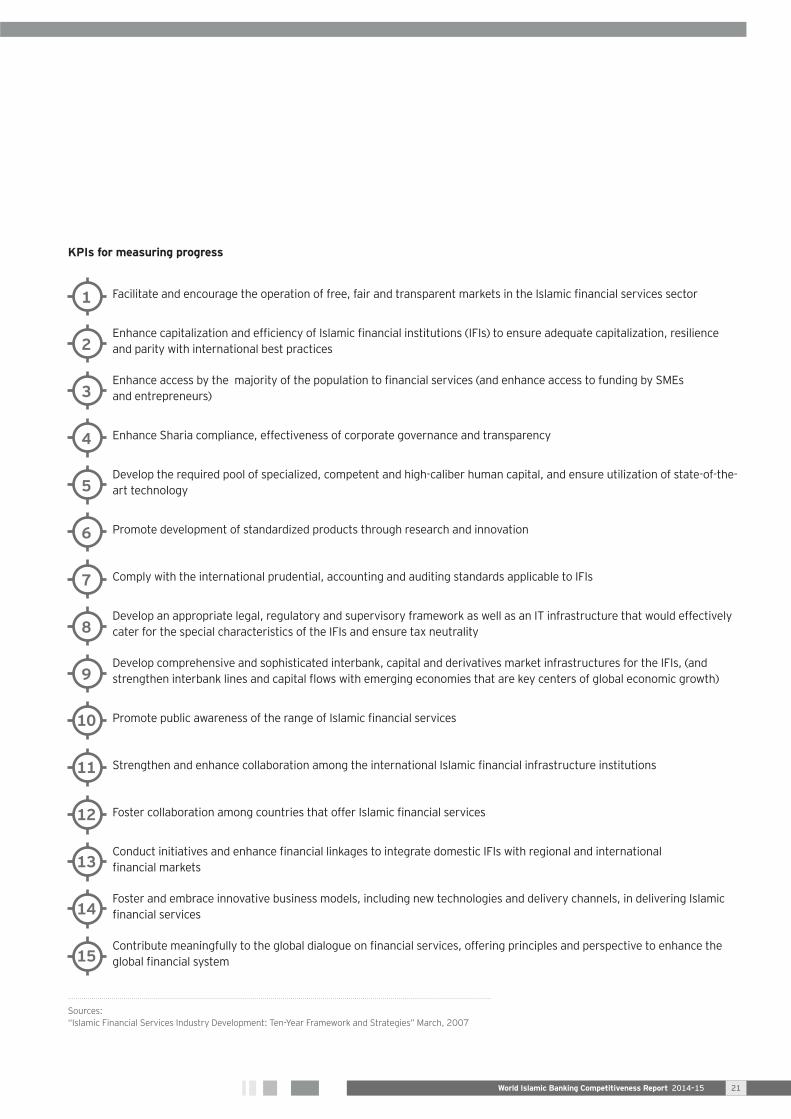

KPIs for measuring progress

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

World Islamic Banking Competitiveness Report 2014–15 21

Financial market infrastructure challenges Challenge scale*

Question marks remain on the state of the industry’s infrastructure

HighState of readiness

World Islamic Banking Competitiveness Report 2014–1522

World Islamic Banking Competitiveness Report 2014–15 23

World Islamic Banking Competitiveness Report 2014–1524

Performance outlook

World Islamic Banking Competitiveness Report 2014–15 25

0 100 200 300 400 500 600 700 800

2019f assets (US$b)2014e assets (US$b)

Pakistan

Bahrain

Indonesia

Turkey

Qatar

Kuwait

Malaysia

UAE

Saudi Arabia290

127

155

90

86

58

37

15

11

683

263

394

157

202

135

143

27

25

US$b

World Islamic Banking Competitiveness Report 2014–1526

US$10.2b in 2013

2013 2019

3x

Potential profit pool from business as usual

Potential incremental profit resulting fromtransformation improvements

0

5

10

15

20

25

30

35

40

World Islamic Banking Competitiveness Report 2014–15 27

Digitization

Impact banking

positioning itself as socially responsible

Customer engagement

Like Share

World Islamic Banking Competitiveness Report 2014–1528

World Islamic Banking Competitiveness Report 2014–15 29

World Islamic Banking Competitiveness Report 2014–1530

Your talking customers

World Islamic Banking Competitiveness Report 2014–15 31

World Islamic Banking Competitiveness Report 2014–1532

More than

2.25 million

Key message

Implications for future

Customers are increasingly active online and vocal about their experiences.

4 out of every 10 Participation banks are not “listening.”

World Islamic Banking Competitiveness Report 2014–15 33

Moment of truth

Malaysia

Relevant posts (000)

Indonesia

Bahrain

Kuwait

UAE

Qatar

Turkey

Oman

Saudi Arabia

375

22

184

44

25

905

47

212

523

Customer service

Branch experience

Online and phone

banking

Other general

sentiments

Products and services

Note: Bubble size represents size of comments in category for the country.Negative comments outnumber positive comments for category by more than 5%.Variance between positive and negative comments is less than 5%.Positive comments outnumber negative comments for category by more than 5%.

World Islamic Banking Competitiveness Report 2014–1534

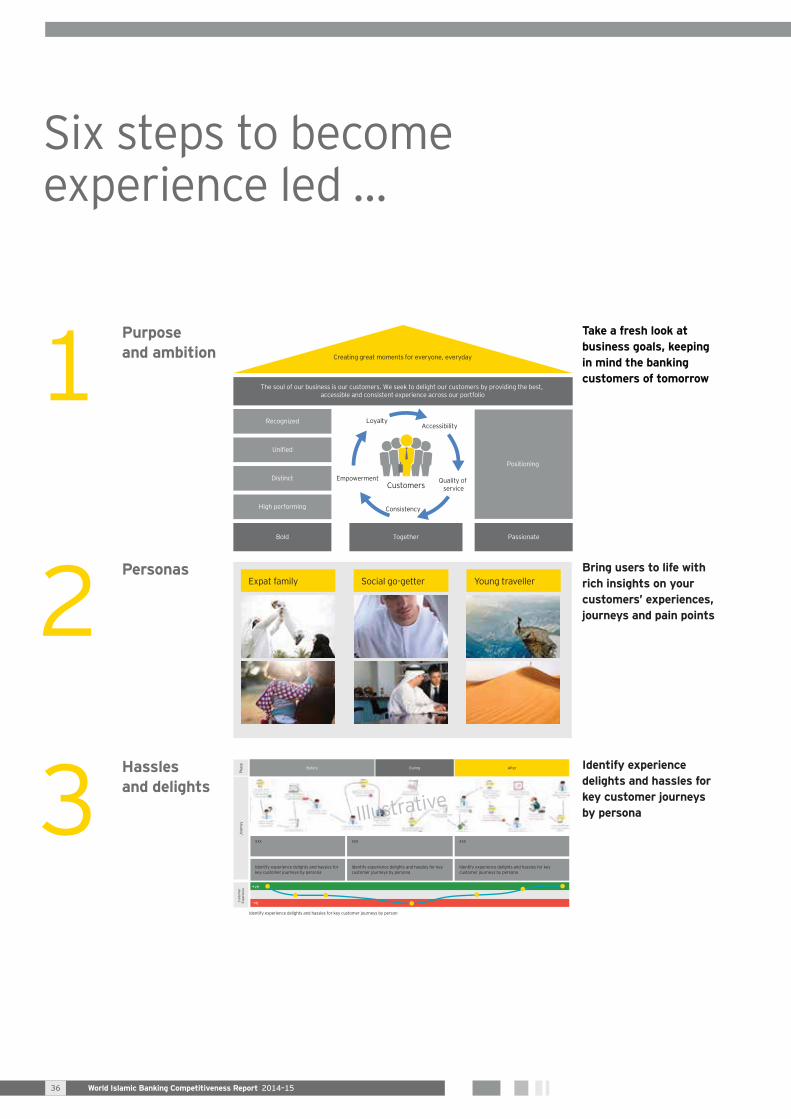

experience-led”

World Islamic Banking Competitiveness Report 2014–15 35

Purpose and ambition Creating great moments for everyone, everyday

The soul of our business is our customers. We seek to delight our customers by providing the best, accessible and consistent experience across our portfolio

Recognized

Unified

Distinct

High performing

Positioning

Bold Together Passionate

Customers

Accessibility

Quality of service

Consistency

Empowerment

Loyalty

Take a fresh look at business goals, keeping in mind the banking customers of tomorrow

Personas Bring users to life with rich insights on your customers’ experiences, journeys and pain points

Hassles and delights

Before During After

Phas

eJo

urne

y

+ve

Cust

omer

Ex

perie

nce

Identify experience delights and hassles for key customer journeys by person

Identify experience delights and hassles for key customer journeys by persona

xxx

Identify experience delights and hassles for key customer journeys by persona

xxx

Identify experience delights and hassles for key customer journeys by persona

xxx

Illustrative

–ve

Identify experience delights and hassles for key customer journeys by persona

World Islamic Banking Competitiveness Report 2014–1536

Intentional journey maps

48 hours

Journey maps

Stage 1: Enter branch Stage 2: Customer contact Stage 3: Phone reg. Stage 4: Issue

Xxx Xxx

Xxx Xxx Xxx

Xxx

Xxx

Xxx

Xxx

Xxx

Create journey maps to communicate future experience and identify areas for improvement

Capability needs and gaps

Customer Interations

Life cycle stages

People Process Technology Data

See

Aware

Buy

Deposit

Post Exp

Training1. 2. 3.4.

Activity1. 2. 3.4.

Tech1. Applications

cannot currentlygather secondarycutomer information

Data1. Data collected only for

the primary customer2. Birth date and previous

historical transactionscannot be identified

ILLUSTRATIVE

1. ..................................

2. ..................................

3. ..................................

4. ..................................

5. ..................................

6. ..................................

7. ..................................

8. ..................................

9. ..................................

10. Customer walks-in

11. .................................

12. .................................

13. .................................

14. .................................

15. .................................

16. .................................

P1 P2 Px R1 R2 Rx T1 T2 Tx D1 D2 Dx

Experiences prioritized based on importance and complexity

Experiences aligned to work-stream and sub-groups

Ownership assigned for gaps

Build future-state, multichannel customer experience across talent, process, data, tools and technology

Experience calculator and road map

Impa

ct

High

Act Now

Act Now

Act Now Act Now

Medium

Long-term

Long-term

Long-term

Low

Aware Aware

Low Medium High

Complexity

Initiatives

123

123

123

123

123

123

123

123

123

12332

32

32

32

32

32

32

32

32

32

32

32

32

3232

32

32

32

Type 1Type 2Type 3Type 4Type 5Type 6Type 7Type 8

Prioritize initiatives on the basis of their value to customer and complexity to implement

World Islamic Banking Competitiveness Report 2014–15 37

Bahrain

30,397sentiments monitored

Total post and relevant post — daily volume

0

50

100

150

200

250

300

350

400

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

Irrelevant Volume Relevant Volume

posts on this

termination of

Positive and negative (Total)

General

Products and services

Customer service

Branch experience

Online and mobile banking

Neutral: general neutral

42%45%

5%12%

2%16%

17%4%

7%13%

10%1%

13%

Positive Negative Neutral

Topic wheel highlighting key negative opinions*

General

Topic wheel highlighting key positive opinions*

Positive and negative opinion breakdown

Bank B

Bank

B

Bank B

World Islamic Banking Competitiveness Report 2014–1538

World Islamic Banking Competitiveness Report 2014–15 39

Call to action

Changing the status quo

Abid Shakeel

Total post and relevant post — daily volume

0

2000

4000

6000

8000

10000

12000

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

Irrelevant Posts Relevant Posts

Positive and negative (Total)

General

Products and services

Customer service

Branch experience

Online and mobile banking

Neutral: general neutral

63%26%

6%3%

3%1%

29%4%

7%7%

17%10%

11%

Positive Negative Neutral

Topic wheel highlighting key negative opinions*

General

Topic wheel highlighting key positive opinions*

Positive and negative opinion breakdown

Interest generated from

340,441sentiments monitored

World Islamic Banking Competitiveness Report 2014–1540

World Islamic Banking Competitiveness Report 2014–15 41

Call to action

Mohd Husin

Saudi Arabia

Total post and relevant post — daily volume

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

Irrelevant Posts Relevant Posts

Topic wheel highlighting key negative opinions*

General

Topic wheel highlighting key positive opinions*

Positive and negative opinion breakdown

567,071sentiments monitored

Positive and negative (Total)

General

Products and services

Customer service

Branch experience

Online and mobile banking

Neutral: general neutral

67%29%

7%14%

16%7%

7%3%

20%4%

17%1%

5%

Positive Negative Neutral

More than

posts related to an online and

Saudi Arabia

World Islamic Banking Competitiveness Report 2014–1542

World Islamic Banking Competitiveness Report 2014–15 43

Ashar Nazim

Call to action

55,884sentiments monitored

Total post and relevant post — daily volume

0

200

400

600

800

1000

1200

1400

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

Irrelevant Posts Relevant Posts

Topic wheel highlighting key negative opinions*

General

Topic wheel highlighting key positive opinions*

Positive and negative opinion breakdown

Positive and negative (Total)

General

Products and services

Customer service

Branch experience

Online and mobile banking

Neutral: general neutral

58%30%

11%4%

5%17%

29%1%

11%7%

2%1%

12%

Positive Negative Neutral

posts on this

sentiments

Bank B

World Islamic Banking Competitiveness Report 2014–1544

World Islamic Banking Competitiveness Report 2014–15 45

Call to action

Karan RanaManager

Total post and relevant post — daily volume

0

100

200

300

400

500

600

700

800

900

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

Irrelevant Posts Relevant Posts

posts related

partnership

a leading

Qatar

Topic wheel highlighting key negative opinions*

General

Topic wheel highlighting key positive opinions*

Positive and negative opinion breakdown

Positive and negative (Total)

General

Products and services

Customer service

Branch experience

Online and mobile banking

Neutral: general neutral

30%33%

7%2%

8%6%

2%1%

5%20%

8%4%

38%

Positive Negative Neutral

29,718sentiments monitored

Qat

ar

Bank B

Feedback

FeedbackSpeed

Qatar Bankin

g

Customer request

Product 1Marke

ting

World Islamic Banking Competitiveness Report 2014–1546

World Islamic Banking Competitiveness Report 2014–15 47

Call to action

Houssam Itani

199,415sentiments monitored

Total post and relevant post — daily volume

0

1000

2000

3000

4000

5000

6000

7000

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

Irrelevant Posts Relevant Posts

Topic wheel highlighting key negative opinions*

General

Topic wheel highlighting key positive opinions*

Positive and negative opinion breakdown

Positive and negative (Total)

General

Products and services

Customer service

Branch experience

Online and mobile banking

Neutral: general neutral

58%27%

4%15%

39%7%

2%2%

8%2%

4%1%

16%

Positive Negative Neutral

World Islamic Banking Competitiveness Report 2014–1548

Call to action

Challenge the status quo

Maged FanousPartner

World Islamic Banking Competitiveness Report 2014–15 49

71,130sentiments monitored

Total post and relevant post — daily volume

0

500

1000

1500

2000

2500

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

Irrelevant Posts Relevant Posts

Topic wheel highlighting key negative opinions*

General

Topic wheel highlighting key positive opinions*

Positive and negative opinion breakdown

Positive and negative (Total)

General

Products and services

Customer service

Branch experience

Online and mobile banking

Neutral: general neutral

55%15%

16%3%

9%1%

8%2%

4%5%

18%4%

30%

Positive Negative Neutral

World Islamic Banking Competitiveness Report 2014–1550

Call to action

Noman MubashirManager

World Islamic Banking Competitiveness Report 2014–15 51

918,565sentiments monitored

Total post and relevant post — daily volume

0

20000

40000

60000

80000

100000

120000

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

Irrelevant Posts Relevant Posts

Topic wheel highlighting key negative opinions*

General

Topic wheel highlighting key positive opinions*

Positive and negative opinion breakdown

Positive and negative (Total)

General

Products and services

Customer service

Branch experience

Online and mobile banking

Neutral: general neutral

45%38%

20%34%

10%1%

1%1%

1%2%

12%1%

18%

Positive Negative Neutral

about a

World Islamic Banking Competitiveness Report 2014–1552

World Islamic Banking Competitiveness Report 2014–15 53

Call to action

Murat Hatipoglu

Indonesia

374,400sentiments monitored

Total post and relevant post — daily volume

0

2000

4000

6000

8000

10000

12000

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

Irrelevant Posts Relevant Posts

Topic wheel highlighting key negative opinions*

General

Topic wheel highlighting key positive opinions*

Positive and negative opinion breakdown

General

Products and services

Customer service

Branch experience

Online and mobile banking

Neutral: general neutral

Positive and negative (Total) 11%88%

2%3%

1%6%

7%18%

1%53%

1%9%

2%

Positive NeutralNegative

World Islamic Banking Competitiveness Report 2014–1554

sentiments relate to disappointing

World Islamic Banking Competitiveness Report 2014–15 55

Call to action

Yasir YasirPartner

World Islamic Banking Competitiveness Report 2014–1556

Country outlook

World Islamic Banking Competitiveness Report 2014–15 57

•

•

•

Participation banking penetration in Bahrain

Total banking assets**

US$

b

2009 2010 2011 2012 2013

13

35

29% 28%

0

10

20

30

40

US$

b

2009 2010 2011 2012 2013

12

22

31% 35%

0

10

20

30

40

Total deposits**

30% 33%

0

10

20

30

40

2009 2010 2011 2012 2013

11

23

US$

b

Assets** YoY growth 2% 4%

5%

2010 2011 2012 2013

–1%

–10%

0%

10%

20%

Financing** YoY growth 2% -2%

2010 2011 2012 2013

7%

–10%–10%

0%

10%

20%

Deposits** YoY growth 4% 1%

7%

–15%

–5%

5%

15%

2010 2011 2012 2013

0%

Bahrain

World Islamic Banking Competitiveness Report 2014–1558

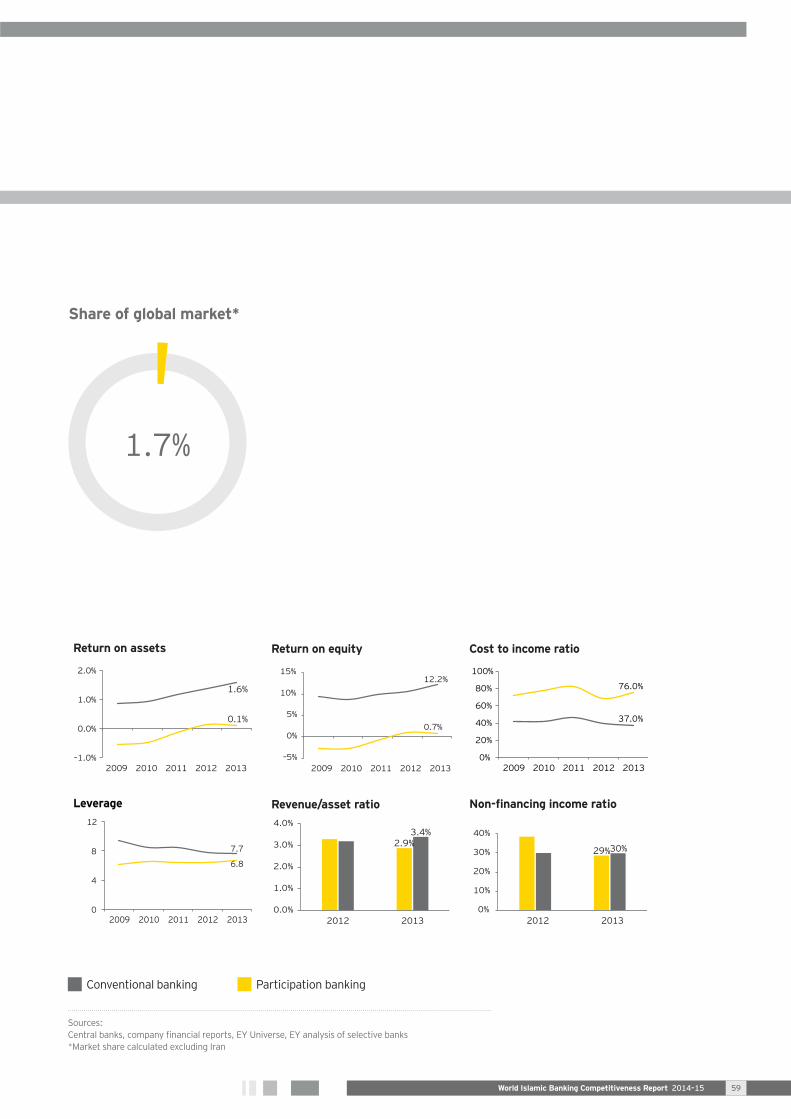

Share of global market*

Return on assets

–1.0%

0.0%

1.0%

2.0%

2009 2010 2011 2012 2013

1.6%

0.1%

Return on equity

2009 2010 2011 2012 2013

12.2%

0.7%

–5%

0%

5%

10%

15%

Cost to income ratio

2009 2010 2011 2012 2013

76.0%

37.0%

0%

20%

40%

60%

80%

100%

Leverage

2009 2010 2011 2012 2013

7.7

6.8

0

4

8

12

Revenue/asset ratio

0.0%

1.0%

2.0%

3.0%

4.0%

2012 2013

2.9%3.4%

0%

10%

20%

30%

40%

2012 2013

29%30%

World Islamic Banking Competitiveness Report 2014–15 59

Saudi Arabia

• Participation banking penetration in the Saudi Arabia

Total banking assets

0

100

200

300

400

2009 2010 2011 2012 2013

247258

US$

b

36% 49%

2009 2010 2011 2012 2013

207174

0

100

200

300

400

US$

b

47% 54%

Total deposits*

0

100

200

300

400

2010 2011 2012 2013

374

US$

b

2009

Assets YoY growth 17% 2%

0%

10%

20%

30%

40%

2010 2011 2012 2013

14%

5%

Financing YoY growth 15% 7%

–10%

0%

10%

20%

30%

40%

2010 2011 2012 2013

16%12%

Deposits YoY growth* 10%

–10%

0%

10%

20%

30%

40%

2010 2011 2012 2013

11%

World Islamic Banking Competitiveness Report 2014–1560

Share of global market*

Return on assets

0.0%

1.0%

2.0%

3.0%

2009 2010 2011 2012 2013

1.9%

2.3%

Return on equity

0%

5%

10%

15%

20%

2009 2010 2011 2012 2013

15%

14%

Cost to income ratio

25%

30%

35%

40%

2009 2010 2011 2012 2013

36%

35%

Leverage

2009 2010 2011 2012 2013

7.2

6.7

0

5

10

Revenue/asset ratio

2012 2013

4.6%

3.6%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

0%

10%

20%

30%

40%

2012 2013

32%34%

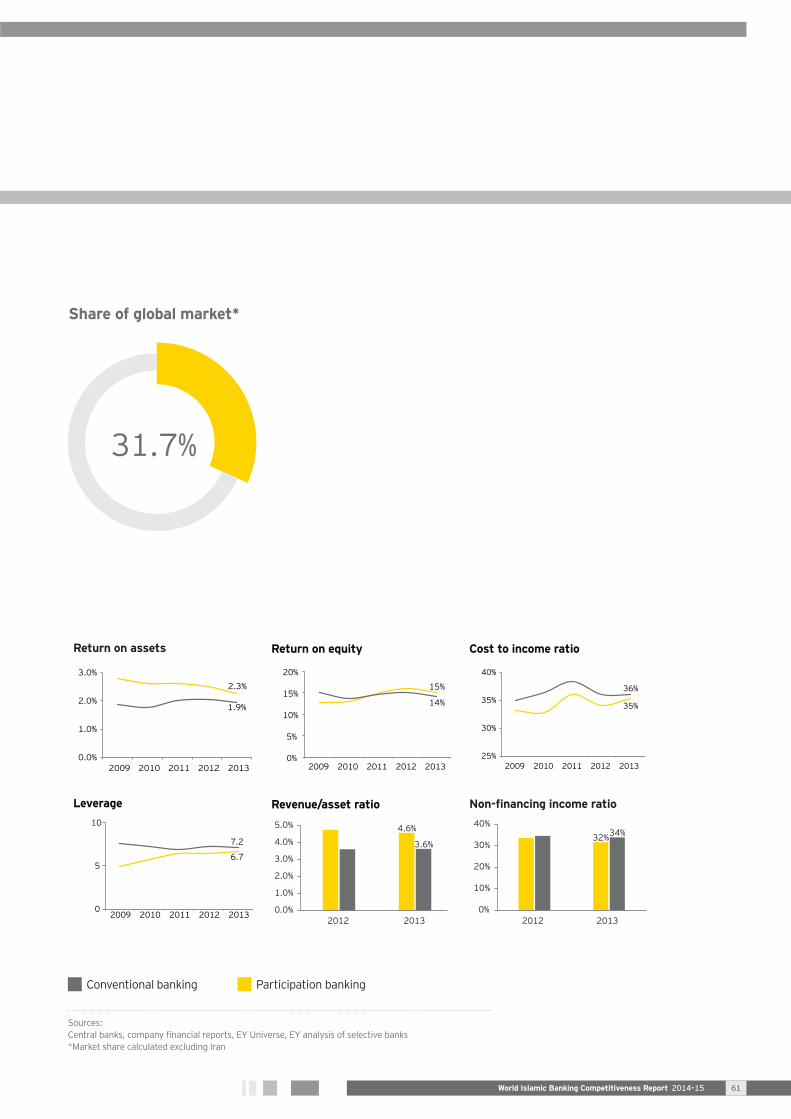

World Islamic Banking Competitiveness Report 2014–15 61

Total banking assets

US$

b

16% 21%

0

200

400

600

2009 2010 2011 2012 2013

498

130

US$

b

0

200

100

300

500

400

2009 2010 2011 2012 2013

85

282

17% 23%

Total deposits

0

200

100

300

500

400

2009 2010 2011 2012 2013

106

360

US$

b

17% 23%

Assets YoY growth 19% 10%

0%

10%

20%

30%

40%

2010 2011 2012 2013

1%

8%16%

Financing YoY growth 23% 11%

0%

10%

20%

30%

40%

2010 2011 2012 2013

14%

1%

22%

Deposits YoY growth 19% 9%

–10%

0%

10%

20%

30%

2010 2011 2012 2013

–1%

15%

7%

Participation banking penetration in Malaysia•

•

World Islamic Banking Competitiveness Report 2014–1562

Return on assets

0.0%

1.0%

2.0%

2009 2010 2011 2012 2013

0.9%

0.8%

Return on equity

0%

5%

10%

15%

20%

2009 2010 2011 2012 2013

11%

10%

Cost to income ratio

30%

40%

50%

60%

2009 2010 2011 2012 2013

48%

41%

Leverage

2009 2010 2011 2012 2013

12.2

12.1

11

12

13

14

Revenue/asset ratio

0%

1%

2%

3%

4%

5%

2012 2013

2.6%3.3%

2012 2013

34%33%

0%

10%

20%

30%

50%

40%

Share of global market*

World Islamic Banking Competitiveness Report 2014–15 63

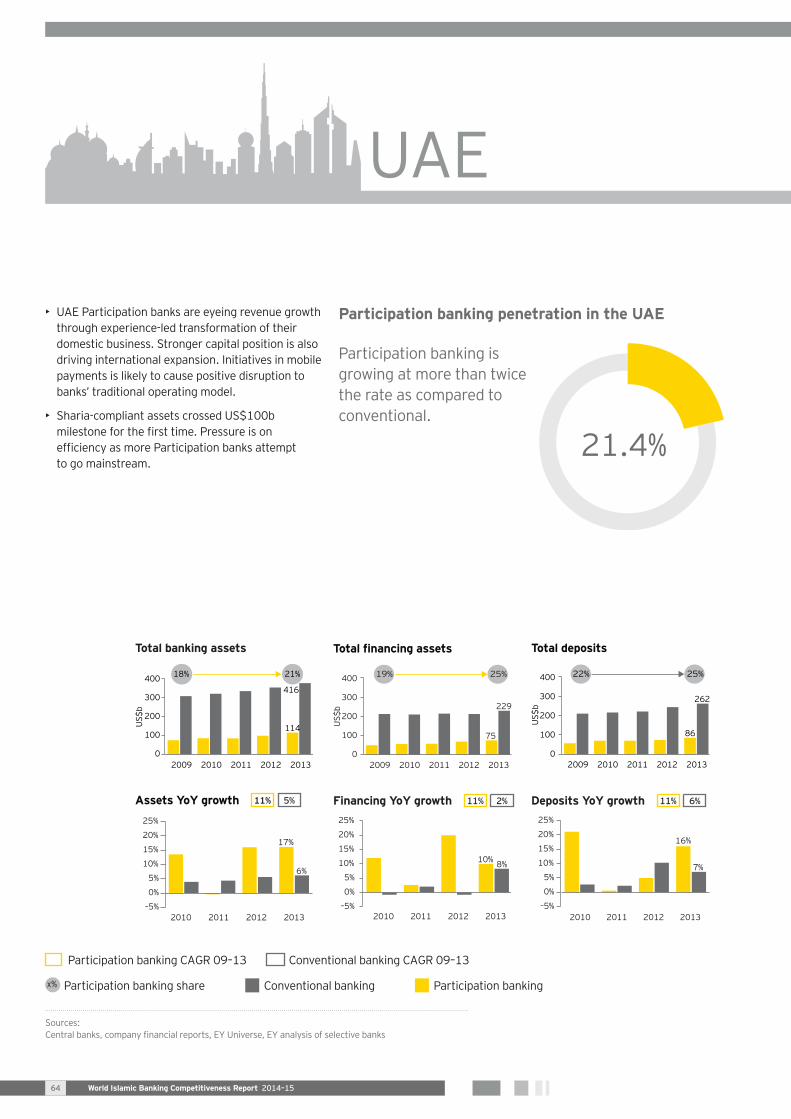

•

•

Participation banking penetration in the UAE

Total banking assets

0

100

200

300

400

2009 2010 2011 2012 2013

US$

b

18% 21%

416

114

2009 2010 2011 2012 2013

75

229

US$

b

19% 25%

0

100

200

300

400

Total deposits

2009 2010 2011 2012 2013

86

262

US$

b

22% 25%

0

100

200

300

400

Assets YoY growth 11% 5%

–5%

0%

5%

10%

15%

20%

25%

2010 2011 2012 2013

17%

6%

Financing YoY growth 11% 2%

–5%

0%

5%

10%

15%

20%

25%

2010 2011 2012 2013

10% 8%

Deposits YoY growth 11% 6%

–5%

0%

5%

10%

15%

20%

25%

2010 2011 2012 2013

16%

7%

World Islamic Banking Competitiveness Report 2014–1564

Share of global market*

Return on assets

0.0%

1.0%

2.0%

3.0%

2009 2010 2011 2012 2013

1.6%

1.3%

Return on equity

0%

5%

10%

15%

20%

2009 2010 2011 2012 2013

12%

10%

Cost to income ratio

20%

30%

40%

50%

2009 2010 2011 2012 2013

46%

31%

Leverage

7

8

9

2009 2010 2011 2012 2013

7.9

7.8

Revenue/asset ratio

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

2012 2013

3.6%3.7%

0%

10%

20%

30%

40%

2012 2013

30%25%

World Islamic Banking Competitiveness Report 2014–15 65

Participation banking penetration in Kuwait

more than three times their

•

•

Total banking assets

020

406080

100

120

2009 2010 2011 2012 2013

82101

US$

b

38% 45%

020

406080

100

120

2009 2010 2011 2012 2013

5647U

S$b

41% 54%

Total deposits

020

406080

100

120

2009 2010 2011 2012 2013

6168

US$b

44% 47%

Assets YoY growth 11% 3%

–15%

–5%

5%

15%

25%

2010 2011 2012 2013

12%7%

Financing YoY growth 11% –3%

–15%

–5%

5%

15%

25%

2010 2011 2012 2013

0%

16%

Deposits YoY growth 9% 5%

–15%

–5%

5%

15%

25%

2010 2011 2012 2013

10%7%

World Islamic Banking Competitiveness Report 2014–1566

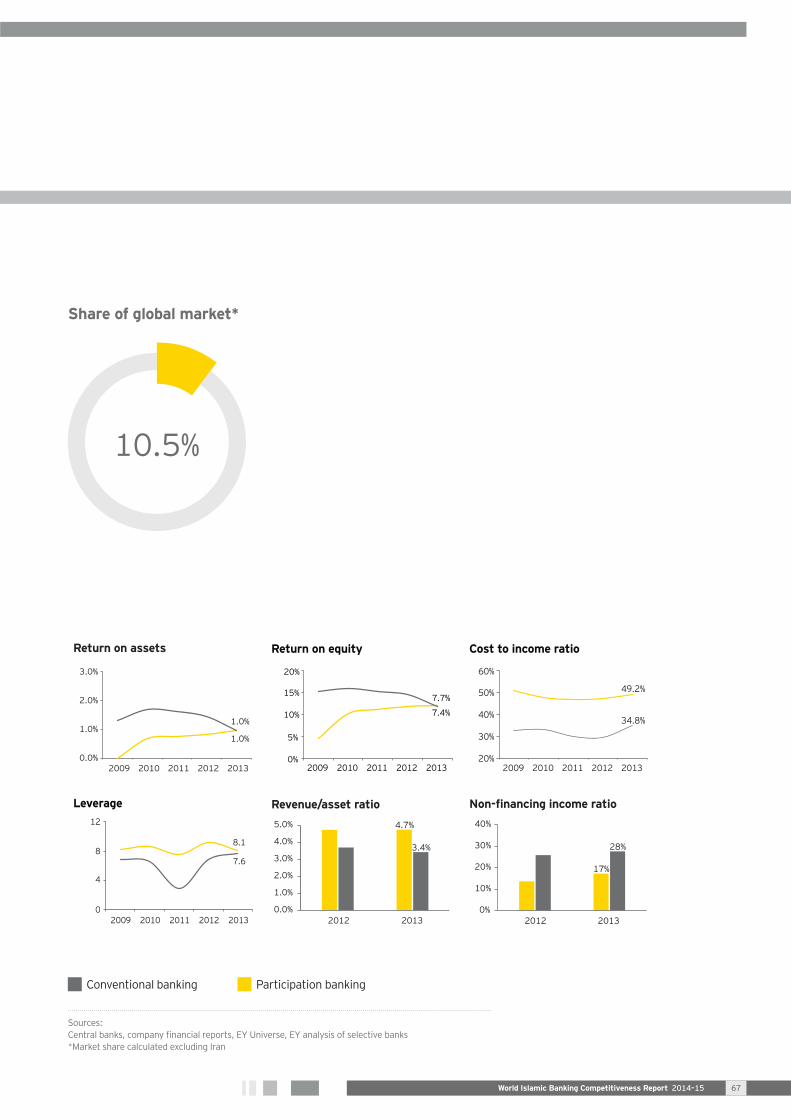

Share of global market*

Return on assets

0.0%

1.0%

2.0%

3.0%

2009 2010 2011 2012 2013

1.0%

1.0%

Return on equity

0%

5%

10%

15%

20%

2009 2010 2011 2012 2013

7.4%

7.7%

Cost to income ratio

20%

30%

40%

50%

60%

2009 2010 2011 2012 2013

49.2%

34.8%

Leverage

0

4

8

12

2009 2010 2011 2012 2013

8.1

7.6

Revenue/asset ratio

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

2012 2013

4.7%

3.4%

0%

10%

20%

30%

40%

2012 2013

17%

28%

World Islamic Banking Competitiveness Report 2014–15 67

Qatar

Participation banking penetration in Qatar•

•

Total banking assets

0

50

100

150

200

250

2009 2010 2011 2012 2013

60

US$b

18% 24%

193

0

50

100

150

200

250

2009 2010 2011 2012 2013

38

121

US$

b

21% 24%

Total deposits

0

50

100

150

200

250

2009 2010 2011 2012 2013

39

111

US$

b

16% 26%

Assets YoY growth 26% 16%

0%

20%

40%

80%

60%

2010 2011 2012 2013

11%12%

Financing YoY growth 25% 20%

0%

20%

40%

80%

60%

2010 2011 2012 2013

13%14%

Deposits YoY growth 38% 18%

0%

20%

40%

80%

60%

2010 2011 2012 2013

16%20%

World Islamic Banking Competitiveness Report 2014–1568

Share of global market*

Return on assets

0.0%

1.0%

2.0%

3.0%

4.0%

2009 2010 2011 2012 2013

2.1%2.1%

Return on equity

0%

5%

10%

15%

20%

25%

2009 2010 2011 2012 2013

13%

16%

Cost to income ratio

0%

10%

20%

30%

40%

2009 2010 2011 2012 2013

28%

25%

Leverage

0

5

10

2009 2010 2011 2012 2013

7.7

6.0

Revenue/asset ratio

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

2012 2013

3.4%3.3%

0%

10%

5%

15%

20%

25%

2012 2013

11%

23%

World Islamic Banking Competitiveness Report 2014–15 69

Participation banking penetration in Turkey•

•

Total banking assets

US$

b

4% 6%

0

200

400

600

800

2009 2010 2011 2012 2013

45

726

US$

b

7% 6%

0

200

400

600

800

2009 2010 2011 2012 2013

30

447

Total deposits

US$

b

6% 7%

0

200

400

600

800

2009 2010 2011 2012 2013

29

410

Assets YoY growth 19% 10%

0%

10%

20%

30%

40%

2010 2011 2012 2013

14%5%

37%

Financing YoY growth 18% 21%

–10%0%

10%20%30%40%50%60%

2010 2011 2012 2013

8% 11%30%

Deposits YoY growth 12% 8%

–10%0%

10%20%30%40%50%60%

2010 2011 2012 2013

3% 7%24%

World Islamic Banking Competitiveness Report 2014–1570

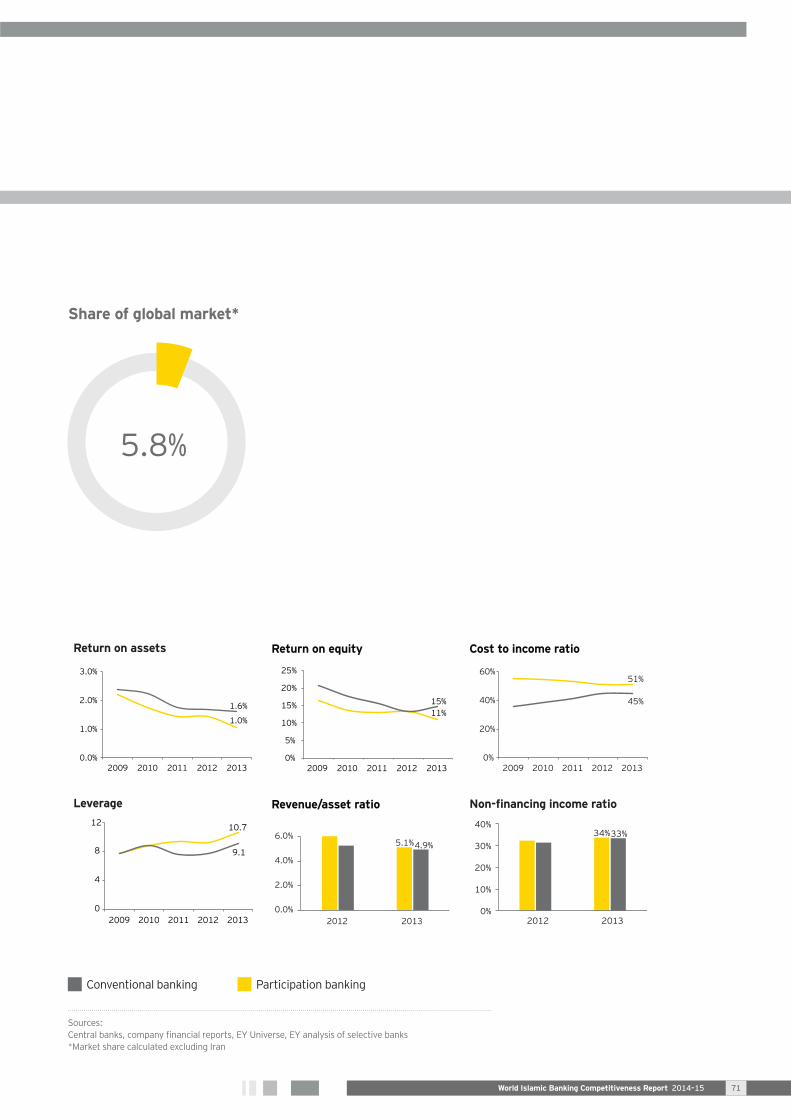

Share of global market*

Return on assets

0.0%

1.0%

2.0%

3.0%

2009 2010 2011 2012 2013

1.6%

1.0%

Return on equity

0%

5%

10%

15%

20%

25%

2009 2010 2011 2012 2013

15%11%

Cost to income ratio

0%

20%

40%

60%

2009 2010 2011 2012 2013

51%

45%

Leverage

0

4

8

12

2009 2010 2011 2012 2013

10.7

9.1

Revenue/asset ratio

0.0%

2.0%

4.0%

6.0%

2012 2013

5.1%4.9%

0%

10%

20%

30%

40%

2012 2013

34%33%

World Islamic Banking Competitiveness Report 2014–15 71

•

•

•

Participation banking penetration in Indonesia

Total banking assets

US$

b

2% 6%

0

200

400

600

2009 2010 2011 2012 2013

510

30

US$

b

2% 4%

0

200

400

600

2009 2010 2011 2012 2013

15

356

Total deposits

US$

b

2% 4%

0

200

400

600

2009 2010 2011 2012 2013

15

398

Assets YoY growth 43% 12%

–20%

0%

20%

40%

60%

80%

2010 2011 2012 2013

46%

–11%

85%

Financing YoY growth 32% 15%

–20%

0%

20%

40%

60%

80%

2010 2011 2012 2013

–1%–3%

25%

Deposits YoY growth 28% 9%

–20%

0%

20%

40%

60%

80%

2010 2011 2012 2013

–1%–10%

24%

Indonesia

World Islamic Banking Competitiveness Report 2014–1572

Share of global market*

Return on assets

0.0%

1.0%

2.0%

3.0%

2009 2010 2011 2012 2013

2.7%

1.3%

Return on equity

0%

5%

10%

15%

20%

25%

2009 2010 2011 2012 2013

22%

15%

Cost to income ratio

0%

20%

40%

60%

80%

2009 2010 2011 2012 2013

64%

37%

Leverage

0

5

10

15

20

2009 2010 2011 2012 2013

11.8

8.0

Revenue/asset ratio

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2012 2013

6.8%

8.8%

0%

5%

10%

15%

20%

25%

2012 2013

17%20%

World Islamic Banking Competitiveness Report 2014–15 73

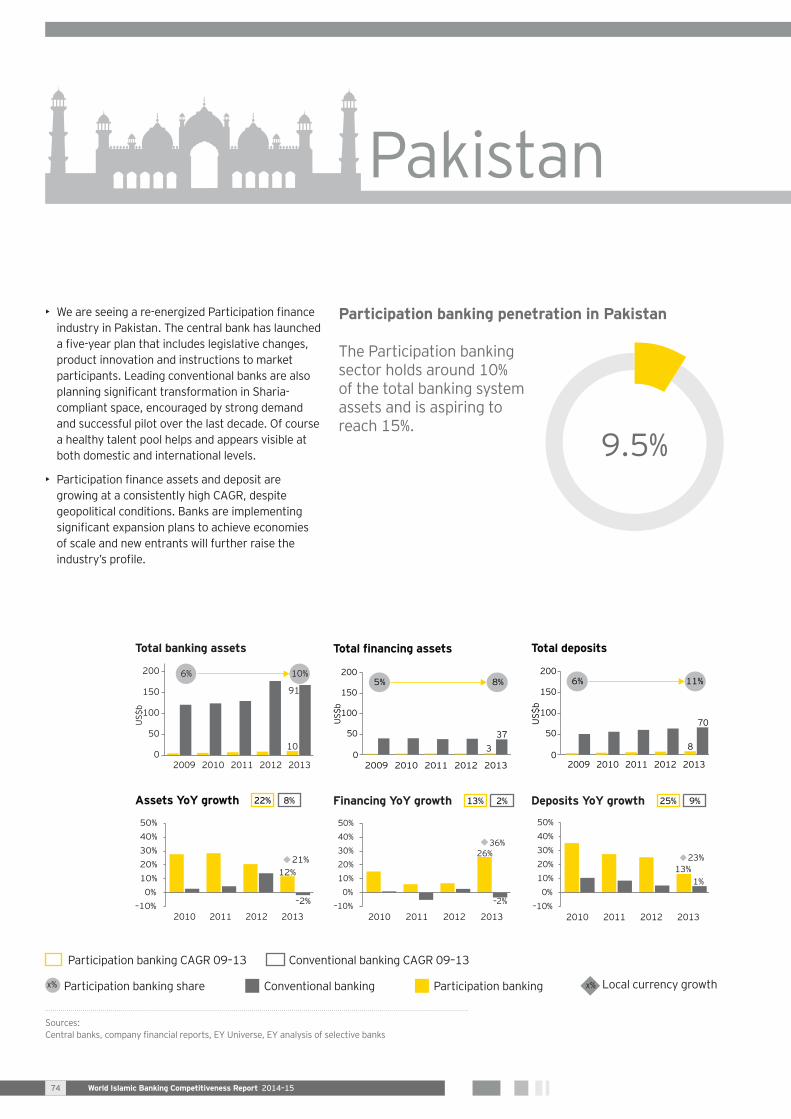

Participation banking penetration in Pakistan

assets and is aspiring to

Total banking assets

2009 2010 2011 2012 2013

10

US$

b

6% 10%

0

50

100

150

200

91

02009 2010 2011 2012 2013

337

US$

b

5% 8%

50

100

150

200

Total deposits

02009 2010 2011 2012 2013

8

70US$

b

6% 11%

50

100

150

200

Assets YoY growth 22% 8%

–10%0%

10%20%30%40%50%

2010 2011 2012 2013

12%

–2%

21%

Financing YoY growth 13% 2%

–10%0%

10%20%30%40%50%

2010 2011 2012 2013

26%

–2%

36%

Deposits YoY growth 25% 9%

–10%0%

10%20%30%40%50%

2010 2011 2012 2013

13%1%

23%

•

•

World Islamic Banking Competitiveness Report 2014–1574

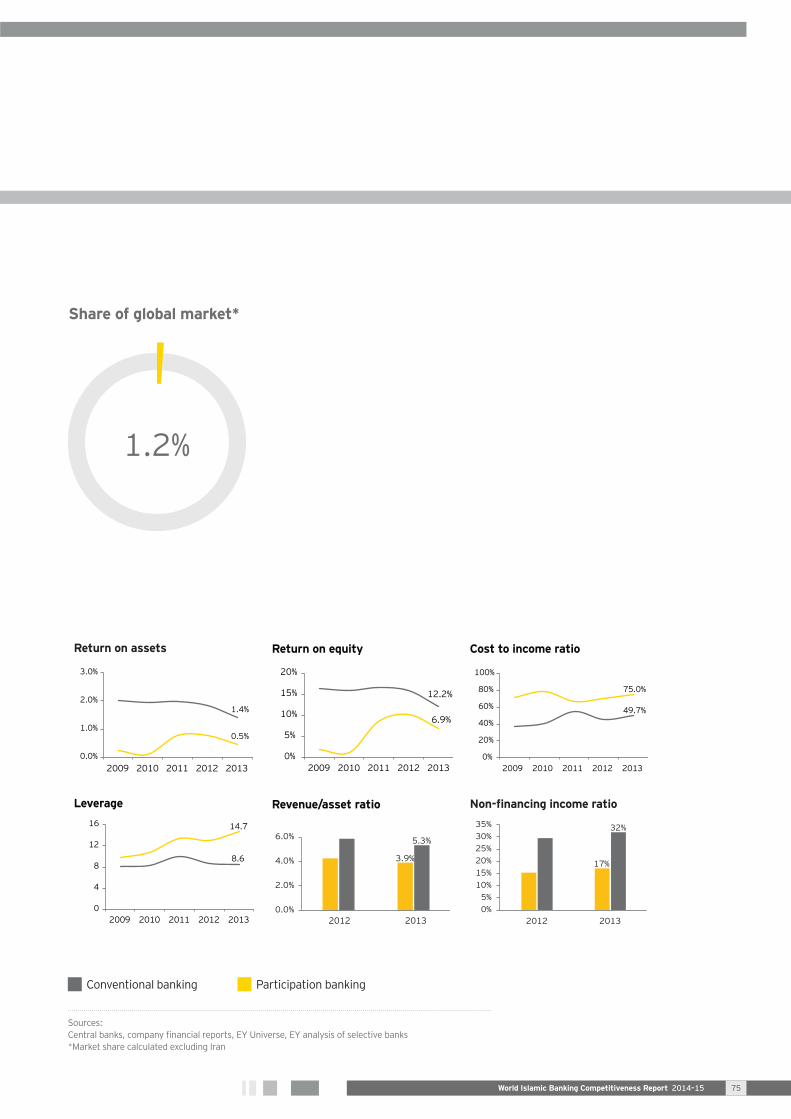

Share of global market*

Return on assets

0.0%

1.0%

2.0%

3.0%

2009 2010 2011 2012 2013

1.4%

0.5%

Return on equity

0%

5%

10%

15%

20%

2009 2010 2011 2012 2013

12.2%

6.9%

Cost to income ratio

0%

20%

40%

60%

80%

100%

2009 2010 2011 2012 2013

75.0%

49.7%

Leverage

0

4

8

12

16

2009 2010 2011 2012 2013

14.7

8.6

Revenue/asset ratio

0.0%

2.0%

4.0%

6.0%

2012 2013

3.9%

5.3%

0%5%

10%15%20%25%30%35%

2012 2013

17%

32%

World Islamic Banking Competitiveness Report 2014–15 75

Our industry awards

Best Islamic Advisory Firm,

2014

Euromoney Islamic Banking Award

Best Takaful Advisory Firm,

2011/2009

3rd International Takaful Summit,

London

WIBC Leading Islamic Financial

Services Provider,2008

World Islamic Banking Awards, Bahrain

Best Islamic Finance

Advisory Firm, 2009/2008/

2007

World Islamic Banking Awards, Bahrain

Best Islamic Advisory Firm,

2014

8th International Takaful Summit 2014

Thought Leadership

Award, 2013

20th Annual World Islamic Banking

Conference Awards, Bahrain

ADIB — Appreciation Award, 2013

1st Annual Global Islamic Economy Summit, Dubai

10th international Real Estate Finance Summit Awards —

London

Best Islamic Advisory Firm, 2013/2011/ 2010/2009

World Islamic Banking Competitiveness Report 2014–1576

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

World Islamic Banking Competitiveness Report 2014–15 77

Ashar Nazim

Gordon Bennie

Robert Abboud

World Islamic Banking Competitiveness Report 2014–1578

Wajih Ahmed(Bahrain)

Nader Rahimi(Bahrain)

Muzammil Kasbati(Bahrain)

Sarvesh Ramachandran(Dubai)

Imitiaz Ibrahim(Qatar)

Abid Shakeel(Saudi Arabia)

Karan Rana(Dubai)

Nida Raza(Dubai)

Adnan Setaih(Bahrain)

Noman Mubashir(Bahrain)

Umair Yousaf(Bahrain)

Houssam Itani(Qatar)

Ashar Nazim

Noman Mubashir

Murat Hatipoglu (Turkey)

Mohd Husin (Malaysia)

Ken Eglinton (UK)

Merisha Kassie (South Africa)

Yasir Yasir (Indonesia)

World Islamic Banking Competitiveness Report 2014–15 79

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

The MENA practice of EY has been operating in the region since 1923. For over 90 years, we have grown to over 5,000 people united across 20 offices and 15 countries, sharing the same values and an unwavering commitment to quality. As an organization, we continue to develop outstanding leaders who deliver exceptional services to our clients and who contribute to our communities. We are proud of our accomplishments over the years, reaffirming our position as the largest and most established professional services organization in the region.

© 2014 EYGM Limited. All Rights Reserved.

EYG no. EK0339

ED 0115

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com/mena