EY Biotechnology Report 2017: Beyond borders - Staying the course

30

Biotechnology Industry Report 2017 Staying the course Beyond borders

Transcript of EY Biotechnology Report 2017: Beyond borders - Staying the course

Biotechnology Industry Report 2017

Staying the course

Beyond borders

Page 1 Biotechnology Industry Report 2017 | Beyond borders

Beyond borders 2017Key trends and implications

Page 2 Biotechnology Industry Report 2017 | Beyond borders

Despite multiple uncertainties, the biotech industry stays the course in 2016

Industry financing dips 27%, but …

… is third highest total in 31 years

Decline in IPOs and follow-ons, but …

… robust early stage VC investment

Deal milestones more common, but …

… M&A total second highest in history

Market cap falls below US$1t, but …

… rebounded in 2017

Net income drops 52%, but …

… R&D spending hits new record

FDA approvals drop sharply, but …

… FDA remains science and access focused

Ongoing drug pricing pressure, but …

… industry adapting to value-based payments

Page 3 Biotechnology Industry Report 2017 | Beyond borders

In the dynamic biotech landscape, the only certainty is uncertainty

“I can’t think of a period that has been characterized by so much uncertainty as the past six to nine months. … The uncertainty is a factor that comes up in every board meeting I attend.”

– Alan Mendelson, Partner

Latham and Watkins

Successful companies have “learned to filter that [uncertainty] out and focus on the things that are right for the company. There may be tax reform. There may be repatriation. But you can’t count on it – and you can’t wait for it either.”

– John Milligan, CEO

Gilead Sciences

Page 4 Biotechnology Industry Report 2017 | Beyond borders

Key performance metrics for US and EU biotechs (US$b)

Numbers may appear inconsistent because of rounding.

Commercial leaders are companies with revenues in excess of US$500m.

Sources: EY; S&P Capital IQ and company financial statement data.

Page 5 Biotechnology Industry Report 2017 | Beyond borders

Financial performance of US biotechnology commercial leaders and other companies (US$b)

US biotechnology: commercial leaders and other companies (US$b)

2016 2015 US$ change % change

Commercial leaders

Revenues 98.8 93.7 5.1 5%

R&D expense 21.9 18.8 3.1 16%

Net income (loss) 29.1 32.0 (2.9) (9)%

Market capitalization 522.0 660.3 (138.3) (21)%

Number of employees 87,930 77,823 10,107 13%

Other companies

Revenues 13.4 13.7 (0.3) (2)%

R&D expense 16.9 15.2 1.8 12%

Net income (loss) (19.9) (16.6) (3.2) 19%

Market capitalization 176.7 231.0 (54.3) (24)%

Number of employees 47,846 52,316 (4,470) (9)%

Numbers may appear inconsistent because of rounding.

Commercial leaders are companies with revenues in excess of US$500m.

Sources: EY; S&P Capital IQ and company financial statement data.

Page 6 Biotechnology Industry Report 2017 | Beyond borders

Financial performance of European biotechnology companies (US$b)

European biotechnology: commercial leaders and other companies (US$b)

2016 2015 US$ change % change

Commercial leaders

Revenues 23.6 19 4 23%

R&D expense 3.5 3.8 (0) (8)%

Net income (loss) 2.0 3.0 (1) (32)%

Market capitalization 120.9 43.3 78 179%

Number of employees 48,233 31,893 16,340 51%

Other companies

Revenues 3.7 3.6 0 3%

R&D expense 3.4 2.9 0 16%

Net income (loss) (3.3) (2.0) (1) 66%

Market capitalization 43.2 132.3 (89) (67)%

Number of employees 19,405 16,721 2,684 16%

Source: EY, S&P Capital IQ and company financial statement data.

Page 7 Biotechnology Industry Report 2017 | Beyond borders

FinancingInvestors downshift in 2016

Page 8 Biotechnology Industry Report 2017 | Beyond borders

2016 was another strong year for “innovation capital” in the US and Europe

Sources: EY; S&P Capital IQ and VentureSource.

Page 9 Biotechnology Industry Report 2017 | Beyond borders

VC investment in early stage US- and EU-based biotechs is a reason for optimism

Sources: EY; S&P Capital IQ and VentureSource.

Page 10 Biotechnology Industry Report 2017 | Beyond borders

US and European venture investment by round

Sources: EY; S&P Capital IQ; VentureSource.

Page 11 Biotechnology Industry Report 2017 | Beyond borders

New sources of capital are emerging, especially in Asia

Size of bubbles shows number of financings per regionInnovation capital is the amount of equity capital raised by companies with revenues of less than US$500 million.

Sources: EY; S&P Captial IQ and VentureSource.

Page 12 Biotechnology Industry Report 2017 | Beyond borders

DealmakingDealmaking remains active, though not as lucrative, for biotechs

Page 13 Biotechnology Industry Report 2017 | Beyond borders

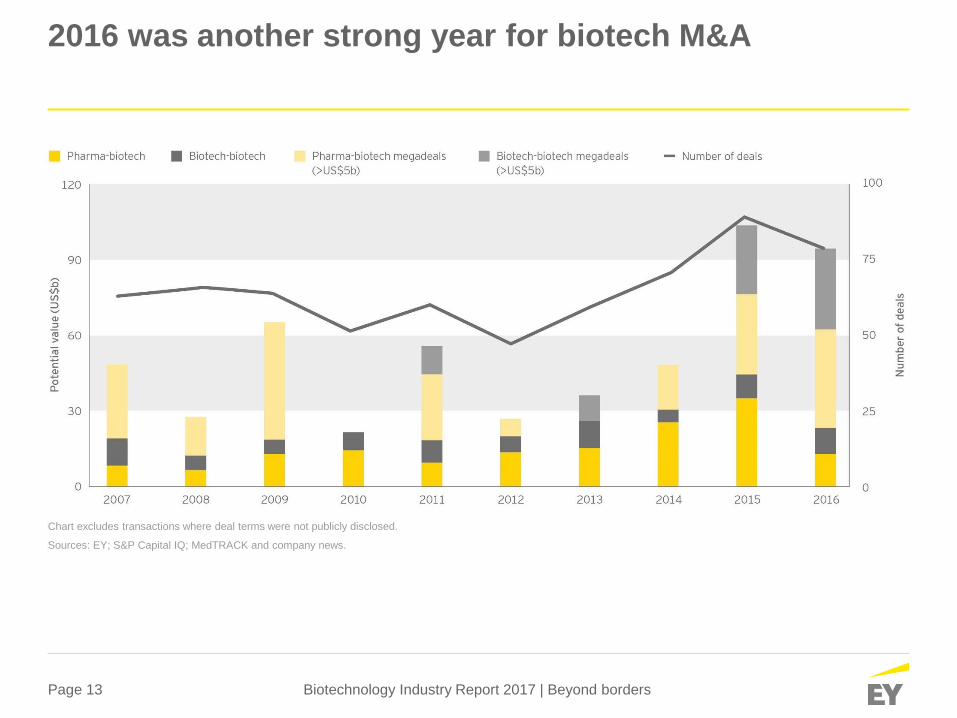

2016 was another strong year for biotech M&A

Chart excludes transactions where deal terms were not publicly disclosed.

Sources: EY; S&P Capital IQ; MedTRACK and company news.

Page 14 Biotechnology Industry Report 2017 | Beyond borders

US M&As (2007–16)

Chart excludes transactions where deal terms were not publicly disclosed.

Sources: EY; S&P Capital IQ; MedTRACK and company news.

Page 15 Biotechnology Industry Report 2017 | Beyond borders

European M&As (2007–16)

Chart excludes transactions where deal terms were not publicly disclosed.

Sources: EY; S&P Capital IQ; MedTRACK and company news.

Page 16 Biotechnology Industry Report 2017 | Beyond borders

Top biotechnology IPOs by region (2016)

Sources: EY; BioCentury; S&P Capital IQ and VentureSource.

Page 17 Biotechnology Industry Report 2017 | Beyond borders

Navigating complexity: key issues for biotechs

Page 18 Biotechnology Industry Report 2017 | Beyond borders

Continued success requires the ability to navigate complexity on multiple fronts

1Product

reimbursement

2R&D

efficiency

3Digital

strategy

4Deal-

making

How can

biotechs

accelerate

value-based

payment

models?

How can biotechs

improve the ROI for

their R&D spend?

What deal structures

and partners give

companies the most

optionality?

What technologies

should companies

invest in today?

5Financing

volatility

What sources of

financing are most

relevant?

Page 19 Biotechnology Industry Report 2017 | Beyond borders

Complexity: product reimbursementAs conversations shift from price to value, what steps do biotechs need to take?

► As emphasis on demonstrating value grows, biotechs should consider:

► Investing in real-world evidence to capture patient-centric data during

development

► Using biomarkers to segment populations to demonstrate improved efficacy

► Incorporating stakeholders’ definition of value into pricing decisions

► Around-the-product services that will enable better outcomes

► Proactive pay-for-performance deals with payers (depending on therapeutic area)

Future strategiesTraditional strategies Emerging strategies

Rebates

and

discounts

Patient

assistance

Indication-

specific pricing

Financial-

based risk

sharing

Performance-

based risk

sharing

Annuity

models

Capitation

1

Page 20 Biotechnology Industry Report 2017 | Beyond borders

Complexity: R&D efficiencyHow can companies improve efficiency via new technologies and capabilities?

► Right drug to right

patient at right time

► Highest use in

oncology

► Shortened

development time

► Increased probability

of success

► Increase probability

of success

► Reduce capital

invested

► Shortened

development time

► Increased sales

► Using technology to

monitor trials

remotely

► Increased regulatory

compliance

► Shortened

development time

► Use social, mobile

and big data

► Develop disease

models and

advanced

therapy solutions

► Targeted clinical

recruitment

► Real world efficacy

and safety

Precision medicine

Biopharmas must overcome challenges to transform the R&D process.

Emerging

understanding of

disease

Data security and

governance issue

Partnering with new

players

Lack of FDA

guidance-

regulatory fears

Lack of resources

(talent and funds)

2

New trial designsRisk-based

monitoringData analytics

Page 21 Biotechnology Industry Report 2017 | Beyond borders

Complexity: digital strategyTechnological advances will change biotech value chain

Smart and connected

Sensors

Device miniaturization

Artificial intelligence

Cheaper sequencing technology

Block chain

3-D printing

Cloud computing

Robotics

Memory processing

More data has been created in the past

two years than in the entire previous

history of the human race.

Empowered by data

Data-focused companies are disrupting

the retail, entertainment and

transportation industries.

Data generation + new technology will

disrupt traditional biotech R&D and

commercial activities.

3

Page 22 Biotechnology Industry Report 2017 | Beyond borders

Complexity: dealmakingWhat deal structure give biotechs the greatest optionality?

► A significant portion of biotechs will be acquired at some point:

► From 2012-16, 10 of 37 commercial leaders (US and EU) were acquired

► How can companies be more strategic to realize full value from portfolio?

M&A

optionality

Option to buy

LLC model

Single asset co Sell minority stake

Divest business

Spin out assets

Biogen/Bioverativ

JNJ buys Actelion; spins out

Idorsia

Lonza sells peptide biz

to PolyPeptide

Roche/Genentech

Gilead/Nimbus Apollo

program in NASH

Takeda/Maverick

Therapeutics

Medicxi funds Kymo

Therapeutics through POC

4

Page 23 Biotechnology Industry Report 2017 | Beyond borders

Complexity: financing volatilitySharp decline in US and EU IPOs underscores financial volatility

5

Sources: EY; S&P Capital IQ and VentureSource.

Page 24 Biotechnology Industry Report 2017 | Beyond borders

Complexity: financing volatilityHow can biotechs build access to multiple pools of capital?

► Ongoing market volatility driving financial volatility:

► IPO window didn’t slam shut in 2016-17, but for many, it’s not open

► Tougher climate for follow-ons

► Private companies tapping a more diverse set of investors (by type

and geography):

► Traditional venture vs. corporate venture/biopharma business

development

► Foundations/family endowments vs. growth investors

► Life sciences vs. technology

► US vs. Europe vs. China/Asia-Pacific

► Long time cycles and cash required to bring products to market still

bias to public listings

5

Page 25 Biotechnology Industry Report 2017 | Beyond borders

EY survival index for US and EU biotechs (2015–16)

Chart shows percentage of biotech companies with each level of cash. Numbers may appear inconsistent because of rounding.

Sources: EY; S&P Capital IQ and company financial statement data.

Page 26 Biotechnology Industry Report 2017 | Beyond borders

Beyond borders 2017: key findings

Payers’ cost containment efforts result in slowing top-line

growth for biotechs.Product reimbursement1

R&D investment increased but FDA approvals dropped;

improving R&D efficiency is an ongoing area of focus.R&D efficiency2

Partnering with new technology entrants to access new

digital capabilities is a key topic.Technological change3

Capital markets pull back significantly in 2016; biotechs

must take advantage of a broader investment pool.Financing4

M&A activity remains strong, but up-front commitments for

alliances decline as biotech valuations fall.Dealmaking5

Page 27 Biotechnology Industry Report 2017 | Beyond borders

When the only

certainty is

uncertainty, is

staying the course

your best bet?

Page 28 Biotechnology Industry Report 2017 | Beyond borders

Additional resources

Contact an EY advisor:

► Glen Giovannetti

EY Global Biotechnology Leader

► Jürg Zürcher

EY Biotechnology Leader,

Germany/Switzerland/Austria

► Ellen Licking

EY Global Life Sciences Senior Analyst

Also:

► Download the report:

ey.com/beyondborders

► Explore/subscribe for new content:

ey.com/VitalSigns

► Follow us on Twitter:

@EY_LifeSciences

EY | Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transaction and advisory

services. The insights and quality services we deliver help build trust

and confidence in the capital markets and in economies the world

over. We develop outstanding leaders who team to deliver on our

promises to all of our stakeholders. In so doing, we play a critical role

in building a better working world for our people, for our clients and

for our communities.

EY refers to the global organization, and may refer to one

or more, of the member firms of Ernst & Young Global Limited, each

of which is a separate legal entity. Ernst & Young

Global Limited, a UK company limited by guarantee, does not

provide services to clients. For more information about our

organization, please visit ey.com.

Ernst & Young LLP is a client-serving member firm of

Ernst & Young Global Limited operating in the US.

© 2017 Ernst & Young LLP.

All Rights Reserved.

EYG no. 04481-174Gbl

CSG no. 1706-2348176

ED None

This material has been prepared for general informational purposes

only and is not intended to be relied upon as accounting, tax or other

professional advice. Please refer to your advisors for specific advice.

The views of third parties set out in this publication are not necessarily the views of the

global EY organization or its member firms. Moreover, they should be seen in the context of

the time they were made.

ey.com/lifesciences

ey.com/vitalsigns