Executive Summary Training & Simulation Market- April 2013

33

Global Military Training and Simulation Market Assessment LVC is Key to Overcoming Tactical Challenges, Albeit in the Distant Future M8FB- 16 April 2013

-

Upload

frost-sullivan -

Category

Business

-

view

2.961 -

download

0

Transcript of Executive Summary Training & Simulation Market- April 2013

Global Military Training and Simulation Market Assessment

LVC is Key to Overcoming Tactical Challenges, Albeit in the Distant

Future

M8FB- 16

April 2013

2 M8FB-16

Research Team

Aman Pannu

Consultant—Europe, Aerospace, Defence &

Security

Alix Leboulanger

Research Analyst, Aerospace, Defence &

Security

Lead Analyst Contributing Analyst

Research Director

Steven Webb

Vice President, Aerospace, Defence & Security

Special Thanks

Lindsay Wooten

Associate Editor

Michael Blades

Senior Industry Analyst

Sabbir Ahmed

Consultant

3 M8FB-16

Contents

Section

Executive Summary

Market Overview

Total Market

• External Challenges: Drivers and Restraints

• Forecasts and Trends

• Competitive Analysis

• Macro Trends

Regional Analysis

North America

Latin America

Europe

Africa

Middle East

Central Asia

Asia-Pacific

4 M8FB-16

Contents (continued)

Section

Conclusion

The Last Word

Appendix

5 M8FB-16

List Of Figures

Figures

Forecast and Trends: Total Market

• Total Training and Simulation: Market Global Revenue Forecast

•Total Training and Simulation: Market Global Revenue Forecast by End-Users

•Total Training and Simulation: Market Global Revenue Forecast by Capabilities

•Total Training and Simulation: Market Global Revenue Forecast by Training Types

Regional Analysis

• Total Training and Simulation Market: Global Revenue Forecast by Regions

• Regional Market Attractiveness Map

Regional Breakdowns (for each region)

•Total Training and Simulation Market: Regional Revenue Forecast

•Total Training and Simulation Market: Regional Revenue Forecast by End-Users

•Total Training and Simulation Market: Regional Revenue Forecast by Capabilities

•Total Training and Simulation Market: Regional Revenue Forecast by Training Types

6 M8FB-16

List Of Figures (Continued)

Figures

Conclusion

•Global Market Attractiveness Map – Live Training

• Global Market Attractiveness Map – Virtual Training

• Global Market Attractiveness Map – Constructive Training

• Global Market Attractiveness Map – LVC Training

7 M890-16

Executive Summary

8 M8FB-16

Executive Summary

• Global economic downturns, global armed forces reorganisations, and troop withdrawals from Afghanistan

and Iraq could draw dark prospects over the training and simulation (T&S) market. However, several factors

are triggering strong dynamics across this market:

o Under-pressure defense budgets must choose cost-efficient training types, thus accenting innovative

training-type blends, such as synthetic and embedded training systems.

o New armed forces structures will need to enable each soldier to perform multiple tasks from procedural

to operational levels.

o Experience from Iraqi and Afghani theatres have highlighted the importance of new, reactive two-way

training simulators, especially comprising haptics technology, to better prepare and reinforce soldiers’

terrain expertise and how to deal with higher levels of stress, and to prepare muscle memory for platform

and systems reactions.

• Therefore, the global demand for training and simulation is expected to steadily grow at a compound annual

growth rate (CAGR) of 2.5 per cent between 2012 and 2021 and will represent up to $411.05 billion of

spending.

• The Asia-Pacific and Middle Eastern training markets are expected to increase at a CAGR of 4.3 per cent and

3.9 per cent, respectively, while other developing markets such as Central Asia and Latin America will grow at

slower pace, but will be driven by strong demands for immersive and system-based training. Despite a low

CAGR of 1.0 per cent, North America will still offer the largest market size for training opportunities, closely

followed by Asia-Pacific and Europe.

Source: Frost & Sullivan analysis.

9 M8FB-16

Executive Summary (continued)

• Globally, air forces will be the biggest users of training and simulation, representing a total market share of

50.5 per cent in 2021, driven by significant, complex combat platforms and new procurements in Asia-

Pacific, the Middle East, and Central Asia.

• Meanwhile, the land forces segment will represent the smallest market share, however, with a dynamic

demand for systems-based training, representing a total market size of at least $60.67 billion between 2012

and 2021.

• Live training will remain the most used training type, which is particularly significant across the naval

segment, with the projected market size reaching $84.83 billion over the forecast period, before shifting to

comprehensive and more realistic training-type blends, such as synthetic and Live, Virtual, and Constructive

(LVC) training.

• Virtual and constructive training will progressively gain end users’ preference as they allow complete,

immersive training in a shorter timeframe to enhance situational awareness and to improve joint decision-

making processes, at the right time and place, with reduced armed forces personnel having more

responsibilities. As a result, the use of virtual and constructive training are expected to raise at a CAGR of

2.1 per cent and 2.2 per cent respectively.

• Training is not only about simulators but also how to train efficiently in a simulated world and how to get the

most realistic, real-world conditions. Consequently, the training market is also impacted by end users’

growing interest for embedded training systems, which enables soldiers to train as they fight, for better

mission rehearsals and tactical awareness.

Source: Frost & Sullivan analysis.

10 M8FB-16

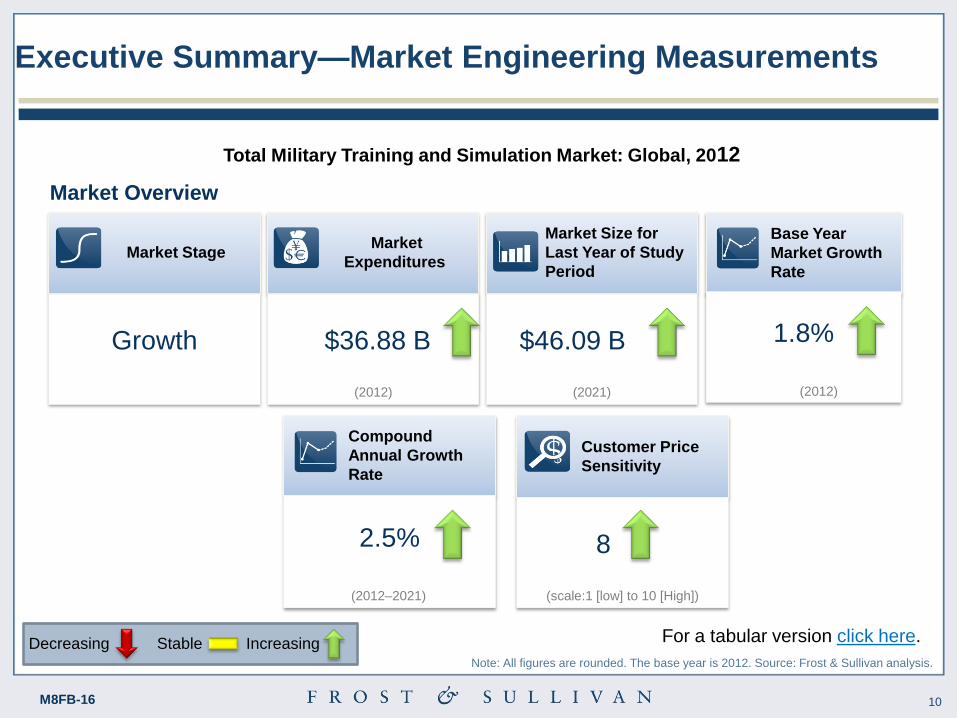

Executive Summary—Market Engineering Measurements

Market Stage

Growth

Market

Expenditures

$36.88 B

(2012)

Market Size for

Last Year of Study

Period

$46.09 B

(2021)

Compound

Annual Growth

Rate

2.5%

(2012–2021)

Customer Price

Sensitivity

8

(scale:1 [low] to 10 [High])

Total Military Training and Simulation Market: Global, 2012

Market Overview

For a tabular version click here. Stable Increasing Decreasing Note: All figures are rounded. The base year is 2012. Source: Frost & Sullivan analysis.

Base Year

Market Growth

Rate

(2012-2021)

1.8%

(2012)

11 M8FB-16

Executive Summary—CEO’s Perspective

2

Platform-based training will have the most

demanded training capability; however,

systems-based training will grow at a CAGR

of 2.0 per cent due to C4ISR capabilities.

3

While virtual training is preferred by Western

end users to optimise budget cuts, live

training remains the most popular training

type globally.

4

End users require cost-efficient training

solutions, enabling training in immersive,

seamless, and realistic environments,

enhanced by Augmented Reality technology.

1 The military T&S market is expected to grow

at a CAGR of 2.5 per cent to gain $9.21

billion, mainly driven by air segment demand.

5

Current distribution channels must adapt to

meet budget constraints, requirements for

customisation, and cost visibility in after-

market support for LVC training capabilities. Source: Frost & Sullivan analysis.

12 M890-16

Market Overview

13 M8FB-16

Market Overview—Scope

Source: Frost & Sullivan analysis.

Air

Military Training and Simulation Market

End Users

Training

Types

Live

Capability

Types:

Training

Application

Support

Platforms

Land Naval

Live, Virtual,

Constructive (LVC)

Maintenance

Systems

Constructive

Virtual

Platforms

Maintenance

Systems

Platforms

Maintenance

Systems

Live

Live, Virtual,

Constructive (LVC)

Constructive

Virtual

Live

Live, Virtual,

Constructive (LVC)

Constructive

Virtual

14 M8FB-16

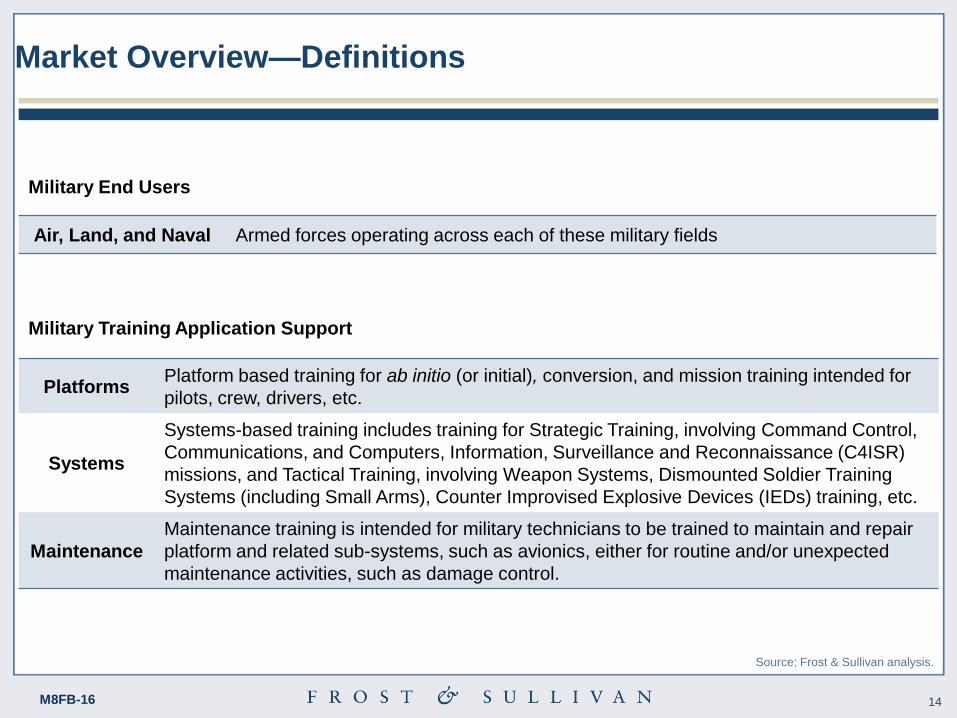

Market Overview—Definitions

Air, Land, and Naval Armed forces operating across each of these military fields

Military End Users

Military Training Application Support

Platforms Platform based training for ab initio (or initial), conversion, and mission training intended for

pilots, crew, drivers, etc.

Systems

Systems-based training includes training for Strategic Training, involving Command Control,

Communications, and Computers, Information, Surveillance and Reconnaissance (C4ISR)

missions, and Tactical Training, involving Weapon Systems, Dismounted Soldier Training

Systems (including Small Arms), Counter Improvised Explosive Devices (IEDs) training, etc.

Maintenance

Maintenance training is intended for military technicians to be trained to maintain and repair

platform and related sub-systems, such as avionics, either for routine and/or unexpected

maintenance activities, such as damage control.

Source: Frost & Sullivan analysis.

15 M8FB-16

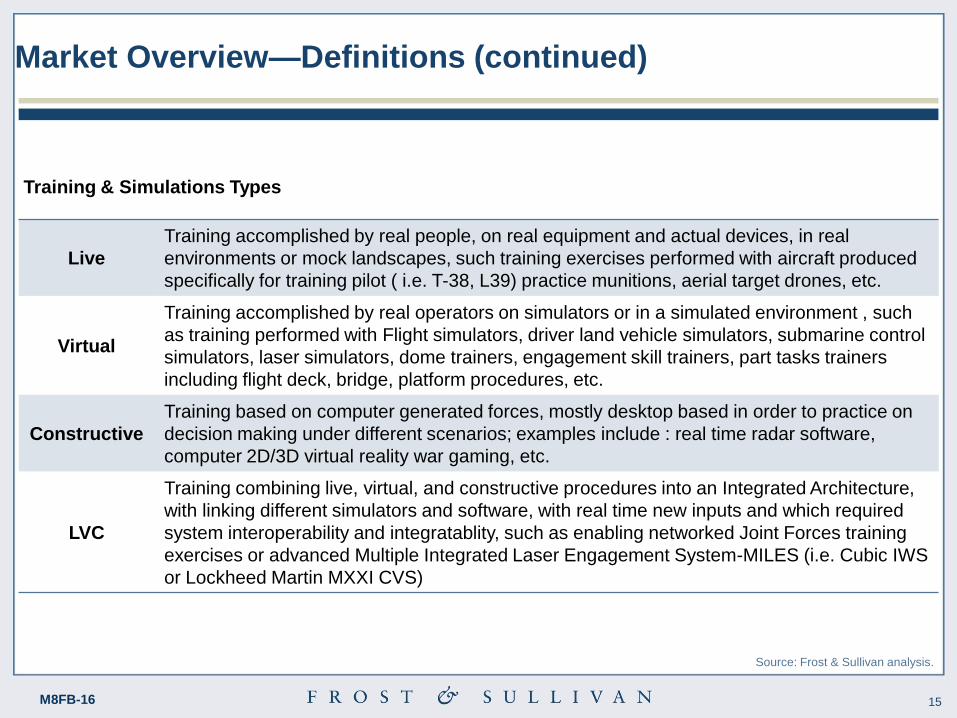

Market Overview—Definitions (continued)

Training & Simulations Types

Live

Training accomplished by real people, on real equipment and actual devices, in real

environments or mock landscapes, such training exercises performed with aircraft produced

specifically for training pilot ( i.e. T-38, L39) practice munitions, aerial target drones, etc.

Virtual

Training accomplished by real operators on simulators or in a simulated environment , such

as training performed with Flight simulators, driver land vehicle simulators, submarine control

simulators, laser simulators, dome trainers, engagement skill trainers, part tasks trainers

including flight deck, bridge, platform procedures, etc.

Constructive

Training based on computer generated forces, mostly desktop based in order to practice on

decision making under different scenarios; examples include : real time radar software,

computer 2D/3D virtual reality war gaming, etc.

LVC

Training combining live, virtual, and constructive procedures into an Integrated Architecture,

with linking different simulators and software, with real time new inputs and which required

system interoperability and integratablity, such as enabling networked Joint Forces training

exercises or advanced Multiple Integrated Laser Engagement System-MILES (i.e. Cubic IWS

or Lockheed Martin MXXI CVS)

Source: Frost & Sullivan analysis.

16 M8FB-16

Please kindly note this study does not include:

These following capabilities:

• Homeland Security and Police training

• Space-based C4ISR systems training

• Unmanned, Underwater, and Ground Vehicles (UUVs and UGVs) training

• Chemical, Biological, Radiological, and Nuclear (CBRN) training

The following aspects:

• Educational training, such as accessions, basic training, military academies, advanced degrees,

teaching certifications and other commissioning sources

• Private military companies providing training services

• Operational costs (such as fuel, training ammunitions, etc.)

Market Overview—Definitions (continued)

Source: Frost & Sullivan analysis.

17 M8FB-16

Forecast Assumptions

• Market Size: The market size is the representation of total forecast military spending across platforms,

systems, and platform maintenance capabilities for training purposes.

• Forecast Methodology: Quantifying the total market size first involves evaluating for each country’s different

parameters at the macro level: country tiers, defence budget assessments, national strategic intents, threat

assessments, combat status, and local industry evaluations. From there, depending on capabilities, other

parameters are assessed to determine training market spending for each segment, such as the level of

training customization, mission readiness requirements, local facilities and MoDs’ outsourcing trends.

o Platforms-based training forecasts include: active units, their lifespan assessment depending on end-

user segments, scheduled retirements, new platforms being procured, and platform-pricing factors

depending on end-users types.

o Systems-based training forecasts include: end users’ spending intensity evaluation, commitment to

interoperability, evidence or intent of C4ISR investment over the study period, and MoD's capability to

adopt hi-tech systems, project value, and life cycle.

o Maintenance training forecasts are only based on platforms, lifespan assessment, their level of

complexity, evaluation of local industry, and country outsourcing trends.

Note: For a detailed outlook on forecast modelling tools, please click here. Source: Frost & Sullivan analysis.

18 M8FB-16

• Market Size Segmentation: The total market size is provided at the global level and regional levels, by

end users, by capabilities, and by training-type levels, in order to present a full analysis on the dynamics

and challenges across this market.

o Education is included in the market size and it is understood as training accomplished in a

classroom setting or online courses received from specific Universities (i.e. Defense Acquisition

University), Service War Colleges and courseware developed to support training, is included in the

market size. However, Education exists across all training segments (live, Virtual and Constructive),

and for the purpose of this report not sub-segmented in the market size.

o Program Assessment: any specific programs, such as for operator training, have been segmented

for the purposes of the market size across Live, Virtual and Constructive training types. For example

the Warfighter FOCUS Program in the US comprises each type of training depending on end-users

fighting requirements.

• Country Scope: This forecast assesses training and simulation spending across 105 countries until

2021.

Forecast Assumptions (continued)

Source: Frost & Sullivan analysis.

19 M8FB-16

• Time Frame: The time frames for the forecast period are indicated in the table below.

• Training Customisation Level: Based on the country’s strategic intent, combat status, and planned

procurements, this parameter assesses the degree of customisation required by end users, from very

low, such as in training products available commercially off-the-shelve (COTS), up to very high, such as

tailored and personalised software.

• Training Types Assessment: Platform, system, and maintenance training calculations depend on end-

user types, a capability’s age and respective lifespan (based on their operating sectors), existing training

programmes, and a country’s budget forecast, combat status, and threat assessment.

Short Term Year 1–2 2013–2014

Medium Term Year 3–4 2015–2016

Long Term Year 5–9 2017–2021

Forecast Assumptions (continued)

Source: Frost & Sullivan analysis.

20 M8FB-16

Market Overview—Covered Regions and Countries

North America

Latin America

Europe

Africa

Middle East

Central Asia

Asia-Pacific

21 M8FB-16

Market Overview—Key Questions This Study Will Answer

What is the market potential for military training and simulation despite global budget

constraints?

Which segments and sub-segments hold the most prospect for growth and why?

Which countries and regions are showing the most promising rates of growth and what

is the future for these markets over the forecast period?

How will new technologies available to the industry revolutionize the military training

and simulation market?

Is there a real shift from Live training towards total Virtual training ?

Are the available distribution channels appropriate enough to meet end users’ needs?

Source: Frost & Sullivan analysis.

22 M8FB-16

Market Overview—Military Training and Simulation

Distribution Channels

Total Military Training and Simulation Market: Distribution Channel Analysis, Global, 2012

*Key: COTS- commercially off-the-shelf .

Source: Frost & Sullivan analysis.

Key Takeaway: There are many available distribution channels, but these are not

adequate to meet end users’ training requirements.

Joint

Ventures

and Public or

Private

Partnerships

Government

to

Government

(G2G) and

Foreign

Military Sales

Training

Centre

leases and

Direct Sales,

like COTS*

Government

to Business

(G2B) and

Private

Finance

Initiatives

End Users

23 M8FB-16

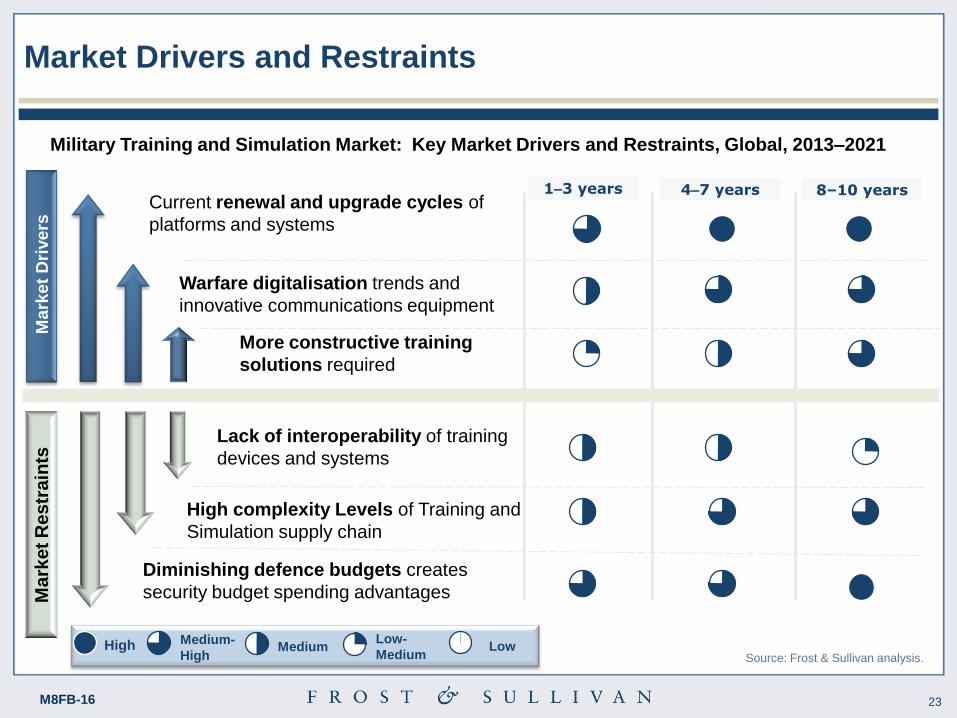

Market Drivers and Restraints M

ark

et

Dri

vers

M

ark

et

Re

str

ain

ts

1–3 years 4–7 years 8–10 years Current renewal and upgrade cycles of

platforms and systems

Source: Frost & Sullivan analysis. High Medium-

High Medium Low

Military Training and Simulation Market: Key Market Drivers and Restraints, Global, 2013–2021

Warfare digitalisation trends and

innovative communications equipment

Diminishing defence budgets creates

security budget spending advantages

High complexity Levels of Training and

Simulation supply chain

Low-

Medium

More constructive training

solutions required

Lack of interoperability of training

devices and systems

24 M8FB-16

Military Training Demand

(Market Size)

Market

Growth

(CAGR)

Low

0-3% Low

<10 $Billion

High

>150 $Billion

Latin

America

Europe

Middle

East High

Attractiveness

Low

Attractiveness

High

3-5% Asia-

Pacific

North

America

Africa

Regional Market Attractiveness Map

Source: Frost & Sullivan analysis.

Region CAGR

Africa 0.03%

Asia-Pacific 4.36%

Central Asia 3.58%

Europe 1.86%

Latin America 3.07%

Middle East 3.92%

North America 1.05%

The table represents regional consolidated expenditures and compound annual growth rates across the

period 2012–2021.

Central

Asia

Military Training and Simulation: Market Attractiveness Map

Global, 2012–2021

25 M890-16

Appendix

26 M8FB-16

Legal Disclaimer

Frost & Sullivan takes no responsibility for the incorrect information supplied to us by

manufacturers or users. Quantitative market information is based primarily on interviews

and therefore is subject to fluctuation. Frost & Sullivan research services are limited

publications containing valuable market information provided to a select group of

customers. Our customers acknowledge, when ordering or downloading, that Frost &

Sullivan Research Services are for customers’ internal use and not for general publication

or disclosure to third parties. No part of this Research Service may be given, lent, resold or

disclosed to noncustomers without written permission. Furthermore, no part may be

reproduced, stored in a retrieval system, or transmitted in any form or by any means,

electronic, mechanical, photocopying, recording or otherwise, without the permission of the

publisher.

For information regarding permission, write to:

Frost & Sullivan

331 E. Evelyn Ave. Suite 100

Mountain View, CA 94041

Source: Frost & Sullivan analysis

27 M8FB-16

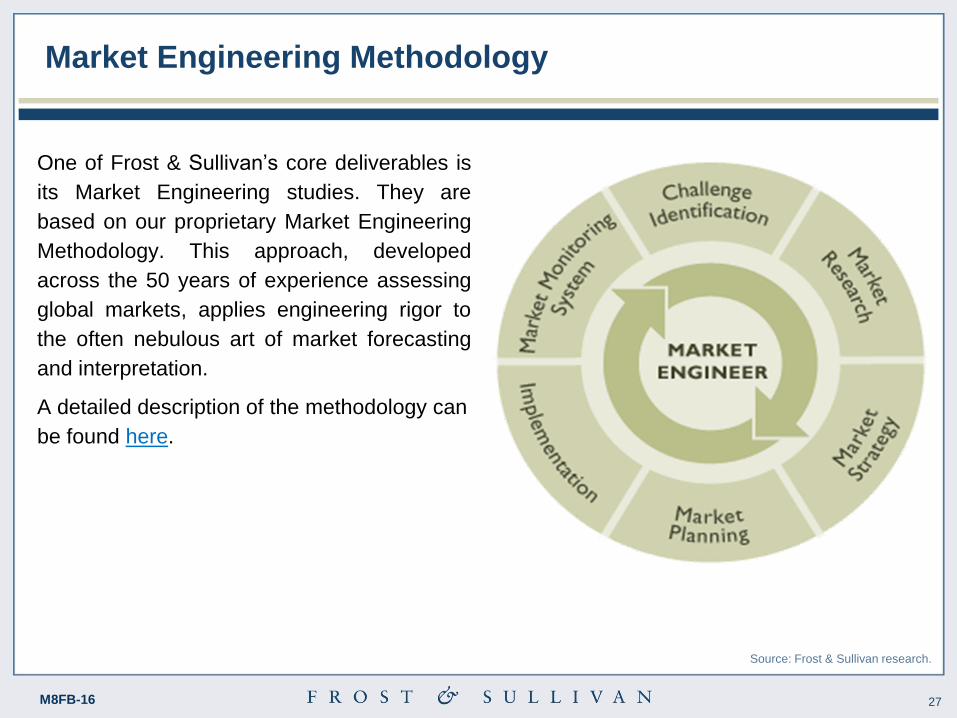

Market Engineering Methodology

One of Frost & Sullivan’s core deliverables is

its Market Engineering studies. They are

based on our proprietary Market Engineering

Methodology. This approach, developed

across the 50 years of experience assessing

global markets, applies engineering rigor to

the often nebulous art of market forecasting

and interpretation.

A detailed description of the methodology can

be found here.

Source: Frost & Sullivan research.

28 M8FB-16

F&S Quantitative Modelling

•Scenario-based Market simulation, deploying market-tested assumptions to translate qualitative data (key factors impacting defence segments, for example) into quantitative data.

• Price matrix • Weightening metrics • Market share statistics • Time-based probabilities

F&S Database

•Use of extensive, bottom-up databases (in-house and outsourced) listing the raw data necessary in the first step of a market forecast exercise:

• Existing Military capabilities • Planned programmes •Anticipated programmes

•Engage industry experts, end users, and industry in constructive discussions to ensure that data is up to market standards and has been thoroughly updated

F&S Analysis (Key Factors and Parameters) •Analyse key factors to filter and select the core factors relevant for each Defence market segment, Product Line, service and/or technology, based on F&S expertise from ongoing secondary and primary research. •Create an industry matrix to ascertain the supply and demand trend within specific markets.

Military Customer: Strategic Intent, Budgets, Replacement, Operations, Infrastructure Technology: R&D, New Products & Technologies, Lifecycle, Substitutes, Obsolescence

Economic Factors: Global & National Economy, Customer Spending

Global Military Trends: Markets, Cultural Factors, In-Country Industrialisation, Skills Competitive Environment: Competition, New Entrants, New Markets, First Mover Advantage

F&S Database

(platforms, systems)

F&S Analysis

(Key Factors and Parameters)

F&S Quantitative

Modelling

F&S Interactive

Forecast Model

Forecast Modelling Tools for our Defence Programmes

Frost & Sullivan’s Approach to Quantitative Analysis

29 M8FB-16

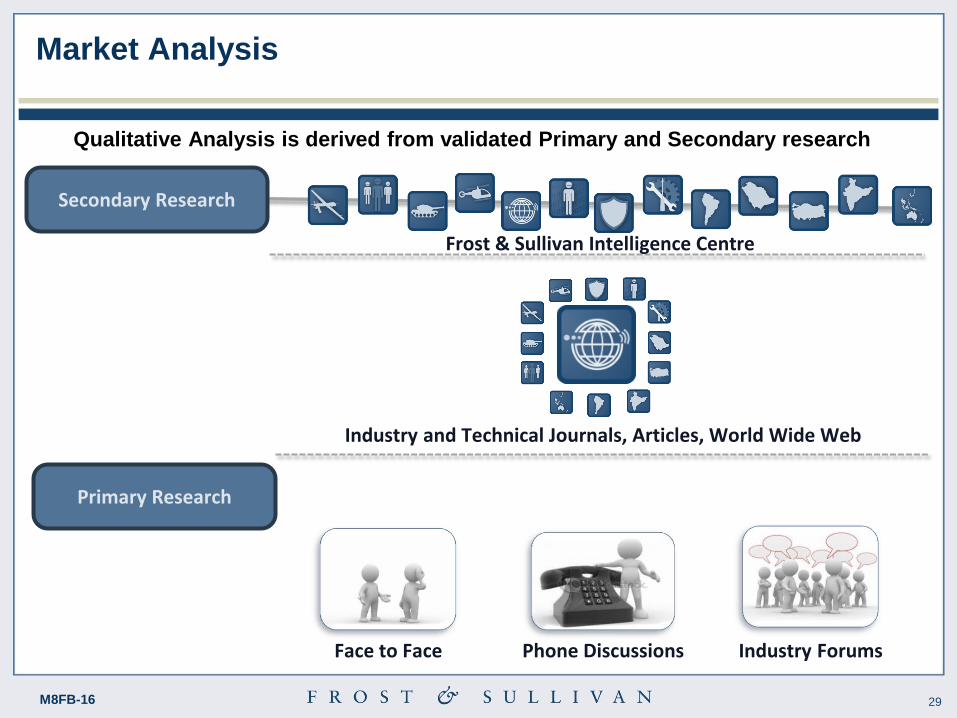

Market Analysis

Frost & Sullivan Intelligence Centre

Secondary Research

Industry and Technical Journals, Articles, World Wide Web

Primary Research

Industry Forums Phone Discussions Face to Face

Qualitative Analysis is derived from validated Primary and Secondary research

30 M8FB-16

Learn More—Next Steps

• Talk to an analyst

• Take our DNA Survey

• Arrange a Growth Workshop

• Explore the Growth Excellence Matrix 2.0

• Attend a relevant live or virtual event

31 M8FB-16

Table of Acronyms Used

C4ISR Command Control Communications and Computers, Information, Surveillance, and

Reconnaissance

C4ISTAR Command, Control, Communications, Computers, Intelligence, Surveillance, Target Acquisition,

and Reconnaissance

C5ISTAR Command, Control, Communications, Computers, Combat Systems, Intelligence, Surveillance,

Target Acquisition, and Reconnaissance

CAGR Compound Annual Growth Rate

CfA Contracting for Availability

CPAF Cost plus award fee

CPFF Cost plus fixed fee

G2B Government to Business

G2G Government to Government

IDIQ Indefinite Delivery and Indefinite Quantity

IEDs Improvised Explosive Devices

JV Joint Venture

LVC Live Virtual Constructive

OEM Original Equipment Manufacturer

MILES Multiple Integrated Laser System

32 M8FB-16

Table of Acronyms Used- (continued)

MoD Ministry of Defence

MOOTW Military Operations Other Than Wars

MRO Maintenance, Repair, and Overhaul

PPP Public Private Partnership

PBL Performance-Based Logistics

PFI Private Funding Initiative

SIS Support in Service

TCO Total Cost of Ownership

TLM Through-Life Management

TSS Total Service Solution

TSP Training Service Provider

UAV Unmanned Aerial Vehicle

UGV Unmanned Ground Vehicle

UUV Unmanned Underwater Vehicle

33 M8FB-16

Frost & Sullivan 4, Grosvenor Gardens London SW1W 0DH United Kingdom

www.frost.com

Alexander Woods Director, Strategic Accounts Aerospace, Defence & Security

+44 (0) 20 7343 8309

+44 (0) 7811357516

Contact Information

![Food security and nutrition: building a global narrative ... · EXECUTIVE SUMMARY EXECUTIVE SUMMARY EXECUTIVE SUMMARY EXECUTIVE SUMMAR Y [ 2 ] This document contains the Summary and](https://static.fdocuments.net/doc/165x107/5ff5433612d22125fb06e6b5/food-security-and-nutrition-building-a-global-narrative-executive-summary-executive.jpg)