Excise Tax Proclamation

15

* * fh.Tr-kl ~1-c.t-f\'£~/loht-f1.1'£ tT-ot\.h ~Yot.1A ., ;JtT ;JJtll] FEDERAL NEGARIT GAZETA OF THE FEDERAL DEMOCRATIC REPUBLIC OF ETHIOPIA "IO~~ ~oP:" eliTe t; "'-'t" "'OI1-';t"U..,P' f)'1+' IDf1~ 9rh Year No. 20 ADDIS ABABA-31 II December. 2002 Oh.:"V-k, 4..1..&-"«£ -'tlfOht-ft.'«£ &1".o"-h fiMHI "'IDt}V-~9"tIc 0."" ml1<t~""fIDII} tPf(J}«65J. "'''~ eII'I'Crf1/Iiif~~ ~.9" f",-hlt,.11:1"h""'''~ 11\ litIli CONTENTS Proclamation No. 307/2002 Excise Tax Proclamation Page 2011 "'''~ eII'I'Crf1/Iiif1~ f ",-h..,,e.1I :1"h" "'''~ foP''''P':''' 10. hIP/lt1..., O"",cc',(o f"'oPlffio lJ:I'''~ ",e. fIP/9"l:F IDQ.1. ""~ htt:A 1I''i f"'l.hLA f",-h..,,e.1I :1"h" oPlI}A "'I1Lf\1. If'i I1h"'1;1 ,e.O :1"h" '~'(P:" ~'-'to-r oPlPl:1"ce OoP(J''i''TtD- 9"h',:" f101 tt:I\o):1"T(J)o nIP/,e.+,,, ":I'''~ ",e. ~1-'tIl}A IP/~l'" "'10. oPlI')' "h:1"oP~n:"1 :1"h (to '..,l1l.,.(U1-1 m.'i" n"'l.""~ ~ 'i" fIP/.., n&-«£~..,C n"'l.f"h:"lt- ":I',,'f ",. oPlI}lt- "'m:l'+00-1 noP+~" l1~ "'".,." 1\" "h "'l.'i l tD-l nih1 oP1"'P'1: ""+1\ ~~ (li) ~'i" (Ili) oPlPl.,"" f"'l.h.,.htD- ;t"tD-~A II htt:A ""~ m~I\" li' "'~C c"" ,e.O "'''~ "f",-hlt"11 :1"h" "'''~ eII'I'C .,.111\- "-10+11 "~"AII I' :"C=\"I ':I'lt- "'11111 "''' :"C1-9" ~1-'tltmtD- t}I\"Lh1 n".,.+c nflO "'''~ CD-"'I'1 PROCLAMATION NO. 307/2002 EXCISE TAX PROCLAMATION WHEREAS, to improve government revenue it has become necessary to impose excise tax payable on selected goods; WHEREAS, it is believed that this tax should be imposed on luxury goods and basic goods which are demand inelastic; WHEREAS, it is believed that imposing the tax on goods that are hazardous to health and which are cause to social problems will reduce the consumption thereof; NOW, THEREFORE, in accordance with Article 55(1) and (11) of the Constitution, it is hereby proclaim~d as follows. SECTION 1 General 1. Short Tide rf1/Iiifj~" This Proclamation may be cited as the "Excise Tax Proclamation No. 307/2002." 2. Definitions In this Proclamation, unless the context otherwise requires: f1~ CP ;J U . t Pri 4.85 m ce ~,?t-r ,?H.II} ;r..".<Jl. it1f.li Negarit G.P.O.Box 80,001

Transcript of Excise Tax Proclamation

**fh.Tr-kl ~1-c.t-f\'£~/loht-f1.1'£ tT-ot\.h

~Yot.1A ., ;JtT ;JJtll]FEDERAL NEGARIT GAZETA

OF THE FEDERAL DEMOCRATIC REPUBLIC OF ETHIOPIA

"IO~~ ~oP:" eliTe t;"'-'t" "'OI1-';t"U..,P'f)'1+' IDf1~

9rhYear No. 20ADDIS ABABA-31 II December. 2002Oh.:"V-k, 4..1..&-"«£ -'tlfOht-ft.'«£ &1".o"-h

fiMHI "'IDt}V-~9"tIc 0."" ml1<t~""fIDII}

tPf(J}«65J.

"'''~ eII'I'Crf1/Iiif~~ ~.9"f",-hlt,.11:1"h""'''~ 11\ litIli

CONTENTS

Proclamation No. 307/2002Excise Tax Proclamation Page 2011

"'''~ eII'I'Crf1/Iiif1~f ",-h..,,e.1I :1"h" "'''~

foP''''P':''' 10. hIP/lt1..., O"",cc',(o f"'oPlffio lJ:I'''~",e. fIP/9"l:F IDQ.1.""~ htt:A 1I''i f"'l.hLA f",-h..,,e.1I :1"h"oPlI}A "'I1Lf\1. If'i I1h"'1;1

,e.O :1"h" '~'(P:" ~'-'to-r oPlPl:1"ce OoP(J''i''TtD-

9"h',:" f101 tt:I\o):1"T(J)onIP/,e.+,,, ":I'''~ ",e. ~1-'tIl}AIP/~l'" "'10. oPlI')' "h:1"oP~n:"1

:1"h(to '..,l1l.,.(U1-1 m.'i" n"'l.""~ ~ 'i" fIP/..,n &-«£~..,C

n"'l.f"h:"lt- ":I',,'f ",. oPlI}lt-"'m:l'+00-1 noP+~" l1~"'".,." 1\" "h "'l.'i l tD-l

nih1 oP1"'P'1: ""+1\ ~~ (li) ~'i" (Ili) oPlPl.,""

f"'l.h.,.htD- ;t"tD-~A II

htt:A ""~m~I\"

li' "'~C c"",e.O"'''~ "f",-hlt"11 :1"h" "'''~ eII'I'C.,.111\- "-10+11 "~"AII

I' :"C=\"I

':I'lt- "'11111"''' :"C1-9"~1-'tltmtD- t}I\"Lh1 n".,.+cnflO "'''~ CD-"'I'1

PROCLAMATION NO. 307/2002EXCISE TAX PROCLAMATION

WHEREAS, to improve government revenue it hasbecome necessary to impose excise tax payable on selectedgoods;

WHEREAS, it is believed that this tax should beimposed on luxury goods and basic goods which are demandinelastic;

WHEREAS, it is believed that imposing the tax ongoods that are hazardous to health and which are cause tosocial problems will reduce the consumption thereof;

NOW, THEREFORE, in accordance with Article 55(1)and (11) of the Constitution, it is hereby proclaim~d asfollows.

SECTION 1General

1. Short Tiderf1/Iiifj~" This Proclamation may be cited as the "Excise Tax

ProclamationNo. 307/2002."

2. DefinitionsIn this Proclamation, unless the context otherwiserequires:

f1~ CP;JU

.t Pri

4.85m ce

~,?t-r ,?H.II} ;r..".<Jl. it1f.liNegarit G.P.O.Box 80,001

1~ gitil J..1..t-A ~?~T ?ILtIJ 4:'1'C?)';1-,.,..,/" ?)'14" Iiln?; 'H".

c.

Ii' "(tm-" DIIi\T DIICj:fm-?" f1-~'J'C' (tm- OJf.?" fl:it"lf(tm-H' OD11T f1-(tmm- ~t}A ~m-;

I' "M1ODIJJ." DIIi\T flltU ~'P~ fh.tJPff.1I ;f"tJilf1-ll)i\I1:fm-'} /):1'9'":f OJf.~1C fDt!il111 (tm- ~m-;

C. "~C~T" DIIi\T '}"l~ JPt,. fDt!t}'l.~ DII'iTOJ.?"

h-11')! OJf.?" f1-ODH1fl f7iCtJCj DII'"rflC OJf.?"

hh-I1'}! OJf.?" h1'ODH1fl f7iCtJCj DII'"rflC ;1C

+tm"'''f.' flf~e; O(J)<o"1l'~1C :it"l ODlPl-r f1-**OD~C~T OJf.,tp' DIICj:fm-cr fOD'}"'JPT fADII-r JP~

~C~T W1-?" f1'}H11 ~C~-r c'1.1f,}: flm-"1I' ~1C

!i\'> ~t}A floOOJhA flh.Tf'A-! m-il'J'f,}"l~JP&.fDt!t}'l.f.m-'} OJh.A hCj O'}.y. flDtIP&.fl-r flh.-r

. f'k! cpf.,?";fl~I\ ~1C :it"l f1-ODlPl1- OJf.?" /)m-:"Cj!11 f1..1f'}9,"qf,.If,}?" h,}f. ~C~T fDt'}., ,.il'}f.,aJ.cr t,.IM .

§. "'}8-U }}AI1A" "7i\T 'J't,.-I: (to'/'}! .It"l~ OJf.?"

blLti rfli\m flf~ ~AI1A DIIi\-r ~m-;~. "~A,I1A" DIIAT~(I.~ ~Af1A ~m-;}. "f;f"tJil I1i\JPAll}'}" DIIi\T f&..Yot,.A ~1C ID-il'J'

1f1.. I1i\JPAll}'} 'PlJ ODjo.T hCj fl1-i\!~ f~1~i:tJlf:i\-":f f 1-**00- :"C'}fiJ, If: ~ j o.-Ai h,} .ltv--?"

tftJAlt- h~ fh1-DII ODil1-~~C'":f f1f1. (t11...f1.~t}I\T e;:fm-;

:L' "f/):1' OD;1H')" ""Ii\T f;f"tJ(}. I1i\JPAll}'} flD'J.~

:"f.m- ODlPl~ fDtmfl:"Cj ;f"tJil fA1-h~i\flT /):1'fDt "'OD'J'fl T 0. T OJf.?" P'If:&. ~m-;

:S. ~'fDII?"l:r .OJIJJ." DIIi\T i\?"CT 1-"lI1C fl.,.'J':1'fDtOJ.lt- 'J'&./):1'9'":fe;f,.AflT 'P;1: "''J'1-~ !AIf~"l11 Ct.y.":f OJQ;l. h Cj Mi C 't~ OJIJJ. c'1.1f,}: i\ ""/?" l:r

ODPf~!9'":f fD?;f"(tflaJ."} fhC~Cj :,.e;7i ~f.aJ..

?"C?"I'

U' ";f"tJil h4-f." DIIi\T fh.tJPff.1I :J'tJil h4-f. ~m-;!. "o'Ull-tC" hCj "Dt~il-rC" DIIi\T h'}f.:"f.?"

1-h+lt- . f1'}H11e; h.f1'fDt ADIIT Dt~il-l:C he;Dt~il-rC ~m-::

f~'P:( +~~Dt~Tf.,U ~'P~ 1-~,Dt fDt(f~m- hltU ~'P~ ;JC fl+!!Hm-lP'}mlY fl1-HlH~ /):1'9'":f I\f. ~m-::

tJlf:A V--i\T

fh.tJPff.1I;f"tJil DIIilh~ AtJ

fil"--I: ODlPlT: ~h4-~Afh.tJPff.,1I ;f"tJil DIIilh~! AtJ

hH.U MP~ PC fl1-!!Hm- lP'}mlY m-il'J' f1-HlH~T/):1'9'":f:-

.

U} hm-"1I' OJf.U1Cm-il'J' (t1f1':.i\) O~1C m-h'J' (tODl-l::

fl~Jml1f fl+ODi\h1-m- fDllilh~! AtJ ODlPl-rfh.hPff.1I :1'tJil f.h~AI1T'PA::

f h.tJ Pff.,11 :1'tJ il il ~-r OD IP l:'-

;f"tJ(}. fDt",I\ flT 'P;J i

Ii' I1h 1C m-il'J' i\ 1-ODl -I:-r /):1'9'":f fDII?"l:r OJlJ.1.t1"i

I' lDf.h1C m-il'J' i\Dt1f1' /):1'9'":fi f/):1'm- 'P;1:'~!,fOb~'"r,) ~l{1'} hCj fDII~~"" OJIJJ. «(t'~f.'h.If:)

f.1fe;A::

fh.tJPff.1I ;f"tJil~h4-~A

Ii' fh.tJPff.1I ;f"tJil:U) flh1C m-il'J' flDtODl-l: /):1'9'":f I\f. fl~?" &.~i

i\) OJf.~1C m-il'J' flDt1f1' /):1'9'":f I\f. fl~il

ODIJJ.m- flltU ~'}.,.?\ ,}(}oil ~'}.,.~ (I) fl1-OJ

fl~m- 1..", m-il'J' f.,h~I\A::

§.

li'

}.

Federal Negarit Gazeta- No. 20 31" December.2002-Page 2012

1) "person" means a physical or juridical person;

2) "Importer" means any person who imports goods

into the country;3) "Body" means any company, registered partnership,

entity formed under foreign law resembling a com-pany or registered partnership, or any public enter-

prise or public financical agency that carries out

business activities including body of persons cor-porate or unicorporated wh,ethercreated or recog-

nized under a law in force in Ethiopia, or elsewhere.and any foreign. body's business '~gent doing

business in Ethiopia on behaif of the pr~pcipal.4) "Pure Alcohol'~ me~ns Alcotlol of purity of 80

degrees or more;5) "Alcohol" means Ethyl Alc()hol;

6) "Tax Authority" means the Fed~ral Inland'Revenue

Authority and the tax authorities of the Regional

States and City Administrations;7) "Bonded Warehouse" means the building or place

destined for storage' of specified goods before the tax

is paid, secured in accordance .with requirements of

the Tax Authority;8) "Cost of Production" mean.s direct labour and raw

material cost incurred in the production process, cost

of indirect inputs and overhead costs, but does not

include depreciation costs of machineries;9) "Taxpay~r" means a person liable to pay Excise

Tax;10) "Ministry" and "Minister" means the Ministry

and Minister of Finance and Economic Develop-ment, respectively,;

3. ScopeThis Proclamation applies on goods listed in theScheduleattached to this Proclamation..

SECTJON 2

The Rate, Base and Payment of Excise Tax4. Rate of Excise Tax '

The Excise tax shall be paid on goods mentioned under

the Schedule attached to this Proclamation:(a) When imported;

(b) When produced locally at the rate prescribed in the

Schedule.

5. Base of Computation of Excise Tax1) in respect of goods produced locally, the cost of

production;2) in respect of goods imported, cost, insurance and

freight (C.LF.);

6. Payment of Excise Tax

1) The Excise tax shall be paid within the time

prescribed under Sub-Article (2) of this Article.(a) in respect of goods produced locally, by the

producer;(b) in respect of goods imported, by the importer.

1;r Ii'f.Ir t..1..t./A ";1&"" ;111.1IJck'l'C ?; :J-"I"IP' ?;I 4>1 IUn?; '}.9". Federal Negarit Gazeta - No. 20 31" December, 2002-Page 2013

l'

I' fh~!~ 1.H.1U) OH.tJ il1«1>7\1(Hl il1«1>7\ ~ (l\) 001Pl.:" f'I'M'

~"'1~ ilA-f'{)m Oil-f'«I>C (l1P1ml.1f f-f'ool\hi::" iJ:J>~'f1

ji' tDY.il1C f1.1n- ililoo6IJ.~ iJ:J>~~1h"9"~h hAA W''l.!tDllJO:''1.H.=

I' Oil1C ~il'r f1.00l.i: h-f'ool.i:(l:" «1>1

r.9"r: n~ «I>C;:"~()1' fn.hllff.11 ;rhilf.h~I\AII

l\) il9"t-.:r: f-f'001.i::"1 iJ:J>~'f f;J'hf1. 1ll\P'AllJ1 W''l.L''''Y.~ fiJ:J> 00;J111 ~il1' ;J'hilltf.h~A l\O'/il«l>oo1' ~:J>Y.' fmf«l> ~1f.If'1C;f;rhf1. 1ll\P'AllJ19" f.tJ1'" h~«I>Y. OILU Lr~;J'O-f'«I>oom:" iJ:J>~'f I\f. ;rh f1. iJ:J>~:r: h 00 ;J 111

~ 1 y'tDm tD-'l!~'" f.hl.I\A::ch) f;rhf1. 1ll\P'AllJ1 fil9"t-.:r: fp't-. ~1""il:J>~

fiJ:J> 00;JII1 fo<f.!il~A"~ If'i f1.!"1~

h1-'ltJ !l\~1 00;JII1 h1-'l!!I:<k9" f.~""Y:l\;rA:1 fiJ:J> 00 ;JII.,. P' t-.~1 fo<f.oot-.(l:"1Lr~;r9" Ooooot! f.tDilC;A:: ill\If'19" f;rhf1.1ll\~AllJ1 tDh.A 0P'~t-.~ ilA-f'''lC; ttA-f'~llJml. Oil-f'«I>C9"19" qf.1:" iJ:J> 000 ;JII1

~il'r 1\0'/il«l>oo1' (IJf.9" hoo;J "'" ~ 1-'l (IJllJ

l\ 0'/ Y: l. '"I J1.f.:F A9"::(0) il9"t-.:r: -f'''o. flf.,.:"1 f'LIIf-o 0011.,(l'fC;

iP'1,.'f ltf.1f f"'l. h1Y.1f'1 (IJf.9" ff(IJ~1f'L IIf-0 00'"1l\ 6liJ.! 1\«I>l.0 h 1 Y.1f'I (IJf.9" OILtJiltp~ O-f'(IJ{)'1~ 1.H. ~il1' ;rhf1.1 !Ah~l\

~ 1 Y.1f'I tDf.9" ! «I>l.(l~ f'L "'1-0 00'"1l\ 65J.09"Coot-. :"hhl\;;: If'i !A-f'''l ~11.1f'1;rhf1. hilh.h~A Y:l.il f;rhf1. 1ll\P'AllJ1

il 9" t-:r: 0'/1;;: ~19" iJ:J> hO'/9" l.:F ~ (l;f-(IJf.9" hiJ:J>~ 00 ;JII1 (J}4il1'~ 1~!(IJllJ l\oohAhA f.'fl\A:1

fn.hllff.1f ;rhil ilwlt{)1

b' f;f-hf1. 1ll\P'AllJ1 fil9"t-.:r: f'LIIf-o 001f1(l'fC;~1P'1Jlc'f Oo<f.11100 !tfT~1C; il9"t-.:r: OH.tJ il 'P~il1«1>7\ ~ (I\) O-f'OOl\h-f'~ 001Pl.:" fo<f.!«I>C(l~

fftD~ f'L"'111 oo'"ll\6liJ. :"hhA 001f.,.1 f1.«I>OA

0 'l.1If-o00'"1l\ 66J.~ 0-f'00 l\ h-f'~ 00 IP l.:" f -f'h~l\ ~

;rhil :"hhl\;;: If'i f.~mt-.A::

I' f;rhf1. fll\P'AllJ1 f;rhil h...~1 'Llt-o hool.ool.O~I\ ;rhil h...~ l\.h~A fo<f.1f1~1 ;rhil illt1(1!il;rtD«I> 001f.,.1 f1.l.{)O:" h11.11''1 -f'QJ.O'/t f;rhil~1If~ f.{)llJA::

[. f;rhf1. fll\P'AllJ1 f{)m~ f;rhil ~lt~ (lO'/il;r

tD<t! -f'tf;J~-f c\;f-hil h...~ f.I\ilA:: f~lt~ O'/il;f-OJ<t! fOOl\ h- il~~1.9" 010. '"I-oC il 'P~ (l-f'{)m

Y:1 ;J1.?J'f 001Pl.:" f.~1.O'/A::

§. f;f-hf1. fll\P'AllJ1 01o-il il1«1>7\ (I) 001Pl.:"

-f'QJ.O'/t f;rhil ~lt~ fc'tm ~C; f;f-hil ~lt~ O'/il;r

W<t! f1.l.{)~ ()~ O'/il;rw<t!~ 01.l.{)~ (l~ «1>1

~il'r h1-'lh~A f-f'mf«l>~1 -f'QJ.li7t ;f-hil!Ah~l\ Wf.9" O~lt~~ I\f. ""&.;r ill\~ Oil1«1>7\

I~ 001Pl.:" f.'"IfI~ !I\«I>l.O h11.1f'1 1' f';;: '1~::

~. OILtJ iltp~ il1«1>7\1; 001Pl.:" ;f-hil h...~ ;rhf1.1ilil;r~'" hhLl\O:" fOr.:,. qoo:,. 00aJ.l.i'f il1il-fO~ qoo:" 1.H. lD-il'r f;rh(\- 1ll\P'AllJ1 f;f-hf1.1Ah tDil'i «I>t 'Lltl1 00'i~1 ill\il;rOJ«I> f-f'h~l\~;f-hil O<t'i fooQJ,l.i'f f.1fC;A:: 1f'i9" ;rhil h...~.,0.~1 !I\il;f-OJ«I> tDf.9" f-f'~Ol.Ol. f10. O'/il;f-

tD<t! !«I>l.O h11.1f'1 f;f-hf1. 'fll\P'AllJ1 OO'/C;TlD-9" l\.I\ ih'"l f-f'1.'111~ f.C;J It!'"I1.~ ;rhf1.100'/c;:flD-9" 1.H. ootD{)1 f.'fl\A::

2) Time ofPayment:(a) Unless decided otherwise, as provided for

under Sub--Article 2(b) of this Article, theexcise tax on goods specified under theSchedule shall be payable.1) When imported at the time of clearing the

goods from Customs area;2) When produced locally, not later than 30

days from the date of production;

(b) Where the tax payer requests forpermission todeposit goods produced iu a bondedwarehouse without payment of tax and if therequest is approved by the Tax Authority thepayment of the tax on such goods so depositedshall be effectd at the time they are beingremoved from the Bonded warehouse;

(c) If the Tax Authority believes that the activityof the tax payer requires a Bonded Warehousemay give him permission to establish suchBonded Warehouse. The conditions underwhich the Bonded Warehouse operates shallalso be laid down by directive to be issued bythe Tax Authority. No goods shall therefore bedeposited in or removed from a BondedWarehouse except in the presence and underthe control of a representative of theAuthority;

(d) where a producer fails to keep proper accountsand records or fails to submit a monthlydeclaration or pay the tax within the time limitprescribed in this Proclamation or submits adeclaration which upon investigation is foundincorrect the Tax Authority shall be em-powered to forbid the producer to remove anygood from the place of production or BondedWarehouse.

7. Assessment of the Excise Tax1) If the Tax Authority accepts that the books and

records maintained by the producer are properlykept and that the monthly declaration submitted byhim, pursuant to Article 8(d) of this Proclamation iscorrect the tax paid in accordance with the monthlydeclaration shall be considered accurate.

2) If, after review by the Tax Authority, it appears thata person has understated his tax obligation, theAuthority shall issue an additional assessment.

3) The assessment made shall be prepared in anassessment notification and be delivered to the taxpayer. Delivery of the assessment notification shallbe made in accordance with the provisions ofIncome Tax Proclamation.

4) If the Authority makes an additional assessmentunder Sub-Artcle (2) and within 30 days of thenotice and demand, the person assessed does notpay the additional assessment or appeal the assess-ment as provided under Article 18, the person is indefault.

5) Ifthe Tax Authority fails to assess the tax and notifythe tax payer of the amount still due withn five yearsfrom the date of declaration and payment of the taxby the tax.payer in accordance with Article 6 of thisProclamation, the tax so paid shall be final andcoacisive. In case, where the taxpayer has notdeclared his income or has submitted a fraudulentdeclaration, nGtime limit provided in any other lawshall bar the assessment of the tax by the TaxAuthority.

1~ litI!! 1..1..~A. ~.??..,. .?JLIIJ4I1'C 1) ;t-'"rUfP' 1)~ +1 Iiinli q.9". Federal Negarit Gazeta - No. 20 31" December,2002-Page 2014

it.

htt:A Y'iI~

f;rhf\- J\(a'l(a-o J\-t~~9"

f;rhil h4.~ ~1o;r?J:f

OlUJ J\ 'P~ 01\.1\-:f ",+".:f h.,..m+ f\-~ ..,$',.;r?J:fO.,..Q;1.°IM",1i:flD-9" ;rhil h4.f. I

u) J\..,I1-o 'It\lD- f"£lt-o "ff1l FCI}~1i f ;rhil 'lI\FAll)). 0"7.-t:"~lD- I}f.'1"" f"£lt-o OOJ''''-o~11i ~;1k(a'1P.:f1 f.~IfA::

1\) O;rhil 'l1\, AII)). O"7.(amlD- :,.~ "f. ;rhf\-10"7.1'l t\oo(a-o(a-o J\iI-t"1. f"7.(nCD-1 ool)ff"7.fltf. 00..,t\65J,. IfPA..y. Ofc!) +). t\:rhil 'lI\FAll)). f+C'lA::

ch) OILU J\'P~ J\1+~ it 1o-il J\1+~ (r)OOJPl''''

f;rhil I1I\P'AII)). f"7.mf.+w.1 f.-t~"'A::(0) f;rhil 'It\P'AII)). CDh.A OFt. (l;rw. 00011 ~

ilt\;rhil J\(a'l(a-o t\"7.fS'.C1lD- ~'1"rC J\iI-t"1.

frf'1lD-1 IJcI\- J\ ":LA..y.f+C'lAulP) fP't.lD-1 I}f.'1""1i fP't.lD-1 J\~t.?j h1.ct1Jc9"

P't-lD-1 fI.~9"C CDWr fl.f!l:C1' 1Jc~;rlD-1 1\'lt\F

A 11)).m.ctflD-). f ltlD-fl' A II

l) P'6-lD-1 fl.f!l:C1' f"7.-tt\"'0~1 ;rhil Oon-I\-

P't.lD-1 l1!1:lm Oc!)+Ii~ w.il1' J\mli~ f.htt:"A::

f;rhf\- 'l1\P'AII)1 , A1I)1OILU J\'P~ t\.1\-:f J\1+".:f h""m+fa.~ 0""Q.1,111/~f ;rh fa. 11I\F A11)1 f"7. h.,..t\ lD- FA 11)1Ii ., , 'l Cf.'i l 'PAI

ii' f.tJ1 J\'P~ OFt- "f. f"''PA hli f"'iI-t~9" ;}"k'1~f;rhfa. 11t\P'AII)1 f.rfliA:1

I' ;rhil h4.~1 CDf.9"f"£lt-o 001l1(l:f1 hli (a'1P.:f1CDf.9"ool)f1 t\"'''''T f"7.:f1\lD-1 CDf.9"h'1H.U)'foomO:" ;}"k'1"" f""(amlD-'} ""~lD-'9" f;rhilh4.~1 ""+lI)t 0J\00=f f;rhfa. 'lI\FAII)1 fFt.(al}..y.:f hli O~/o.1: ",,":t;..y.t\"7.+Cn-t\"" I\"".c;~J\..,11-0 f":folD- 1'f-l: 9':f 00A iI h 1.ct(a1'1i f.,..'l I\-

""''/"' (a'1p':f h1..v+c-o t\"'~l"'f

r' U) f9"CT """''lC CDf.,/",f7if~ P't- ill\oot}Z.l;.CDf.,/", t\;rhfa. J\h4.-tA f"7.6c; ",ill)f

ilt\oo'i~ "-mt-mC CDf.'/"'f.U J\'P~ CDf.9"OJ\'P~ OOlPl"" f"7.CDm-T ~1(l:f hli oooo~f9'":(. 0"7.111 oohOt-:flD-1 t\",l;111' O:J:hil

h4.' IID~O~ fP't- (al}..y.:ff1\) f.U'} J\'P~ CDf.'/"'OJ\'P:( OOfPlT f"7.CDm-T1

~ 1 (1:f1iIIDIID~f9':f 000"""" tt: '1'4...,.f.,..-tRoot\OOrf)' fl.mt-mC 0""~lD-9" 1.H.fCD~;rhil h4.~ f P't- (l;r CDf.,/",f/Jfl' 00;1"'CDf.'/"' '/"'Cof: f.1:t; O;r A .,..-0 I\- CD~ "7.100""lD-",Ii :fm-'/"' , tt:t- f lID'"'l Tli 1Jc~;r?J:f1f"'II)t.Tf ool)f?J:f1 foo(a-o(aoO"""n.w.19"hC'/"')f fODlD-(a~

g. OILtJJ\'P~ ODlPlT t\.h-tA f"7.1'llD-1 ;r)1i1 t\;rhil

hof.' fP7i1;rCD:"I

~. ID~J\"C f"t.,n- ilfl'9':f1 O"7.ODt\hTIU) CDS'.OD1"'P'T f.,..'/"'~h hAA h.,n-OT +1

J\1il.,.hilh iI~"'T CDC~lil ;rhfa. t}A.,..h-tt\/Jfl' 9'=li1 f l1I\ifl' CDf.'/"' /Jfl'?J=Iif"7. 0" if. rf'ifI.f"~ 0",1i:flD-'/"' 1.11.h1.ct7i'm- fODCD(a1I

~.

SECTION 3Collection Enforcement

8. Obligations of the Tax Payer

In addition to the obligations specified in the otherprovisions of this Proclamation, every tax payershall :(a) maintain books of accounts and supporting.

documents in accordance with proper accoun-ting principles and in a manner acceptable to theTax Authority;

(b) submit every 30 days to the Tax Authority, in aform which shall be supplied by said Authority,a declaration containing such information asmay be necessary for proper collection of thetax.

(c) comply fully with requirements of the inspec-tion of his premises by the delegate of the TaxAuthority in accordance with Sub -Article 3 ofArticle 9 of this Proclamation.

(d) comply fully with the requirements of theinspection of his premises by the delegate of theTax Authority;

(e) immediately communicate to the T~x Authoritythe type and address as well as the commen-cement and termination date of his business;

(f) pay in full the tax due within 30 days from thedate of termination where such business isteIDlinated.

9. Power of the Tax Authority

In addition to the powers specified in the other provisionsof this Proclamation the Tax Authority shall have thefollowing powers and duties:1) The implementation and enforcement of this

Proclamationshall be the duty of the Tax Authority;2) Requiring the person or any employee who has

access to or custody of any information. records orbooks of account to produce the same and to attendduring normal office hours at any reasonablyconvenient tax office and answer any questionsrelating thereto;

3) Enter business premises or stores of the tax payer orto any place suspected to be storage of the products,inspect, collect information and take appropriatemeasures:(a) during the regular working hours of the tax

payer where it suspects that production or saleof goods is carried on or there is informationthat may be necessary for the prOper assessmentof the tax, and to ensure the observance of thisProclamation and Regulations issued for theimplementation of this Proclamation;

(b) at any time where it suspects that an offenseresulting from the violation of the provisions ofthis Proclamation or regulations issued for theimplementation of the Proclamation has beencommitted.

4) Notify the tax payer the additional tax to be paid inaccordance with this Proclamation;

5) as regards goods imported:(a) sell such goods where the tax in respect of them

is not paid within six months from the day ofdeposit within the premises of governmentwarehouse, or in the case of perishable goods,decide on their sale at any time it thinks fit;

1K" !{1LUi J..1..&-1A ";J~-r ;JUII)~'I'C 1j ;1'1VtP' 1j!{+, Iit£1G 'H". Federal -Negarit Gazeta - No. 20 31stDecember, 2002-Page 2015

t\) il. hLA fD? 1 11lD- ;t-h IIli t\.f\o";f lD(J;}JP";f

h"''''~f1- 0:\1\ "'t-k 11"11-1 t\oP"'OA oPlI-rf t\ lD- ()lD- iJ:J>lD- h.,. 11m 0"" .,.1 h 111.,. 0 ~~oP"" 1.H. lD-ll'l' 'I' f<l: Itf"'ClIli oPlI1:

Itl;J1'1' .,.t-klD- 11"11 t\f1t\oPlI1: h 1.1toPt\llt\-r fOlJf:l..,:

i. OIJ";J~ 0."" f:C~"" f4.f.li111 "'*9" lDf.9"

0IJ1~lD-9" f&..lot-A lDf.9" fhAA oP1..,F""oPF~f 0."" QJ.9"C' 0IJ1~lD-9" ()lD- llt\;t-hll h<t-~

fD?flD-"'lD-1 oPl~ lDf.9" f F t- h 1,pll:J>11.1'C"HCh1.1t1A~ t\OIJf:l.., f.";fl\A::

I. ;t-hllt\oP()lI()lIUlI-rllt\oPf"H

j;. 01o-11 h1"'~ (§) f'''f.~11lD- h1f."'m(H> I1'If

OIJliTlD-9" OH.U h'P~ f"'flJt\lD- ;t-hll fD?Lt\..,O-r()lD- Oh1"'~ 1: 1o-11 h1"'~ § lDf.9" Oh1"'~ It

1o-11 h1"'~ ({) 0"'f.~11lD- oPlPl-r 'I'<t-"'~ I1'If

f"'11 h1f.1f~ f;t-hf1- f1t\FAflJ1 ftlU1 ;t-hll

h4.f. UlI"" OoPf"H t\D?Lt\..,O"" ;t-hll hli 111l1:1t\ oP f"H f.,. f.l 1 lD-1 .,. QJ.OIJ~ lDlJJ. t\ oP 11 L 1h1.1tlD-At\OIJf:l..,~;J'f FAflJ1 f.lfl'PA::

I. t\H.U htt:A hL~~9" "oP f"H" OOlJliTlD-9" oP11f:oPf"H1 h1.1tu-9" fh.hUff."H ;t-hll fD?Lt\..,O:" ()lD-

flf~ 11"lIlDf.9" 111l"" Oh~ hD?1~ ()lD- ;t-hlloP()1I()1I1 f.QJ.9"t-A:: 01o-11 h1"'~ (E) hli (i)0"'~1llD- oPlPl"" I1AIf~ Oll.,..,.C oPf"H fD?:rt\lD-foP fn- ""iJtf"H O"'()mO-r 1.H. Of.tf;t- FC fD? 1~

111l"" hli foP fn- .,...,I1C 0D?hlilD10-r 1.H. tn.y.ft\ ..,1o;t-1 O"'oPt\h.,. 1I:r ~lD-:: f;t-h()' f1t\FAflJ1 f;t-hll h4.~1 UlI"" 0D?f."H0-r 1.H. fTil.ll

lPt-'f-r hl1A h1.1t1~ il.mf.,p f.";fl\A:: f1t\FAfIJ).hH.U Ol\f. O"'oPt\h"'lD- oPlPl-r UlI1:1 hf"O-r.,.1 h 111.,. hD?~mC hI .,.li"" 1.H. 0:\1\ Otht- ~lDf.9" OI1t\FAfIJ). O.,.L"'f. OOlJliTlD-9" t\.1\ "10ff"lD-1 111l"" oP1I'I' f.";fl\A:: Iflf9" 111l1:fD?Ol\(i hlf~ f111l1:1 I1UCf. h"'9"-r lD-ll'l'00lJil1 11"" "'1 n. oP IIf\o 0 D?;t- f lD- 1.H. il. 11 mlD-f.";fl\A::

E. OIJliTlD-9" f.,. f" 111l"" t\oP fn- 9"h1 f"" flf~lD-1f;t-hll iJ.I; t\oP1IL1 oct "f.1f1 f"'l h1f.1f~:f;t-hf1- I1t\FAflJ1 h;t-hll h<t-~ I\f. fD?Lt\1lD-f;t-hll iJ.I; hli hH.U ;JC f"'ffn- A~ A~ lDlJJ.sP";f.,.htt:t\lD- hllhD?mli"'~ f:lll f;t-hll iJ.I;lD-fD?Lt\

..,0""1 ()lD- t\.f\o";f UlI.,.";f oPf"H f.";fl\A==§. hH.U Ol\f. 01o-11 h1"'~ (j;) O.,.f. ~11lD- oPlPl""

I1A"'hLt\ f;t-hll iJ.I; 9"h1f"" 111l-r oP;"HfD?:rt\lD- f;t-hf1- I1t\FAflJ1 UlI1:1 foP f"H U"lIh1.1;t\lD- hll.,.f:IJP t\;t-hll h4.~ O~m.tt: 1111;t-lD"'lD-0:\1\ f.lfliA:: OH.U ~f.~"" fD?()mlD- OIJll;t-lDctfUlI1: hoP fn- he!) .,.1 Ok"" t\;t-hll h<t-~ il.f.C()lD-f.1I1A::

~. f;t-hf1- I1t\FAflJ1 f;t-hf1-1 h()f1()l1 fD?ff.li,ptt:J-~;t- oPlf';'1 f"'l.l; h1f.1f~ 01o-11 h1"'~ (j;)

f"'oPt\h"'lD- fc!J .,.1 f1.H. 1f.1I hli 01o-11 h1"'~(§) f"'oPt\h"'lD- fc!J .,.1 f1.H. 1f.1I "f.mO,p ;t-h()'lD.ltflD-). h1.1thLA t\OIJf:l.., 'l'f<l: h"'lOli ;t-hll

h<t-~ t\oPhLA Uf.~ I1AIf~ 111l""1 OoPf"H;t-hll foP()lI()11- hL~~9" ~;J'f f.lfliA::

i. OIJliTlD-9" 111l"" f"'f" lDf.9" h1JLf"H f;t-()O

hlf~ llt\H.u-111l"" OIJlll~ fD?1f1lDf.9" oP..,t\65j.

ff" ()~f: lD~"" oP"H111 Oh~ fD?1~ lDf.9"O~'I''I'';' FC fA OIJliTOJ-9"()lD-O;t-hf1- I1AFAtlJ1'I' f<l: It "'C-nt\:" ()~~ 1 lDf.9" oP"H111-1 AOIJIII

~~..,. 0IJ,p l-a "'''0""::

(b) transfer to the Government treasury thebalance, if any, remaining after the deduction ofthe tax and other expenses, provided, however,that it shall pay the same person entitled theretowhere he claims it within five years from thedate of the sale and where his claims areprovided.

6) Requiring any person including a municipality,body, financial institution, department or agency ofFederal or Regional Government to disclose par-ticulars of any information or transactions.

10. Seizure ofProperty to Collect Tax

1) Subject to Sub-Article (4), if any person liable to payany tax imposed by this Proclamation is in defaultunder Article 7, Sub-Article (4) or Article 18,Sub-Article (2), it shall be lawful for the Authority tocollect such tax (and such further amount as shall besufficient to cover the expenses of the seizure) byseizing any property belonging to such person.

2) For purposes of this Section, the term "seizure"includes seizure by any means, as well as collectionfrom a person who owes money or property to theperson liable for VAT. Except as provided inSub-Articles (3) and (6), a seizure shal extend onlyto property possessed and obligations existing at thetime the seizure is made. The Authority may requesta police officer to be present during the seizure.Where the Authority seizes any property as providedhereinabove, it shall have the right to sell the seizedgods at public auction or in any other mannerapproved by the Authority not less than 10 days afterthe seizure, except that when the goods seized areperishable, the Authority can sell the goods after anyreasonable period having regard to the nature of thegoods.

3) Whenever any property on which iieizure had beenmade is not sufficient to satisfy the claim for whichseizure is made, the Authority may, thereafter and asmay be necessary, proceed to seize other propertyliable to seizure of the person against whom theclaim exists until the amount due from such person,together with all expenses, is fully paid.

4) Seizure may be made under Sub-Article (1) onproperty of any person in default with respect to anyunpaid tax only after the Authority has notified suchperson in writing of the intention to make suchseizure. The notice shall be delivered not less thanthirty (30) days before the day of the seizure.

5) If the Authority makes a finding that the collection ofthe tax is in jeopardy, demand for immediatepayment of such tax may be made by the Authorityand, on failure or refusal to pay the tax, collectionthereof by seizure shall be lawful without regard tothe 3O-day period provided in Sub-Article (1) andthe 3O-day provided in Sub-Article (4).

6) If a seizure has been made or is about to be made onany property, any person having custody or controlof any books or records containing evidence orstatements relating to the property subject to seizureshall, on demand of the Authority, exhibit suchbooks or records to the Authority.

n' ~i'i.n; &"J'..MiI. ";J/'-} ;J/J.nJ <I:'I'C ?! ;J'..,..,r ?!~ .,,-) :OH~i?;'HI".

:z.

Federal Negarit Gazeta - No. 20 31,IDecember, 2002-Page 2016

O~Cf.; (t-)- :'-01'1' f-HHllWJ.'.9u Oh.{,~~~ IIJ.'.YI\WJ.'.~ OCPfl:'-lJ'f-f-YII ilAln Ofl-f-</,C u'llJ':':W-~O;J-hfl ~h,}Y:'- fi-YH '}-nl-} nh~: fU'J_1~ lDJ.'.9uI\;J-hfl h4.f- u'llJ':t:W-9u ..,!!o;J- Yl\tH- (}W- f:J-h()'IMP' A II}'} (}.mJ.'.<f'w- f YtlW-') u-tH- I\;J-h ()- tll\P'All}'} fU'Jfllh-n lDJ.'.9u Yl\tH--} "'Yo;J' fOV6_~9u;')116.'t-)- hl\tH-::

u'l~':':W-9u (}m- f:J-h()' tll\P'Ann (}_mJ.'.'l'co-h')Y.;'} f-'-YtI '}-nl-} l\U'JflLh-O 6_:J>Y,7,:".elf'}f</'l h'}f.tf't O-f-YtlW- '}-nl-)- ovm'} n..,A -hn_r'~J.'.tflJ'A:: tflj~ i-mytH; I\'}-nli: OVY1' 9utJ1Y-}htf'tw- f;J-hfl o~ ovm'} (n;J-h()' o~ IIJ.'. fU'J_;J-(}nm-'} W{J;1.hlJ' wI\Y: lJJ,~C') I\.YA~ hJ.'.-;'j-A9u::

n'}trfl h'}</'''' (t) h-f-ovl\h-f-m- f..,A -t-tnYt't-)-ni-lJJ,U'J6 '}.nl-f:'} fYtlm- (}w- ')-nl-f:,} l\U'Jfllh-n.{,:t'Y-~ YAtf'tm- Yl\nt ~h'}Y-)- htf't n'}o-fl

h'}</'''' (:I:) ODlPl:'- fU'J_'{'1\1W-'} f1'}IHl ODm'} IiTC(}'}-)- (H-lJJ,U'J6 h,})).h~A J.'.Y-l;JA::

..

ntw h'}</'''' ODlPl:" nJ.'.I':}-m- P'C Yl\w-1 '}-nL-)-Yfllhn wJ.'.~ n:t"hfl h4.V- fU'J..{,I\..,n-)-1 1'}tI-nh;J-h(}' I1I\P'AII}'} n-f-mf</'m- ODlPl:,. 1fl. _rY,l1U'JlJ'rw-~ (}m- ilfllhnm- ').ol-} WJ.'.~ 1 fl. tlf.l1m-1'} 11.0 ;JC n-f'Y YII f:t"h fl ..,!!o;J'm-'} tl A-"lDlI}m-;t'hfl h4.J.'. Wf-~ U'JlJ':t:m-~ 1\.11(}m- hU'J.6_I\..,n-)o~ WJ.'.~ ill\n:" ..,!!o;J- 't., J.'.tflJ'A::

II!- OU.o-} IIJ.'.fU'J.</'c-n f</'f.~:"":'- OD-n:,. 'l'Y<I:I!- tpflT~- f"'(}lI}rm- f I\.I\"~ hn~69'~ fq. Y:U'J.Y

OD.o:" h'}f."'mn</, tflj ntw htp~ ODlPl:" ;J'hfl-t-h4.J.'. hU'J.tf'}OT </''} h'}fl-Y. -Hl~I\" hflhhl\</'O:" 'lit. ~lfl ;J-hfl fODh'{'A ..,!!o:}- tll\tH-(}m- U.o T IIJ.'. f:t"h (). 111\P'A II}') f</'y-~-)-.,:"OD.oT J.'.ljltpA::

!:- U'JlJ'rm-~ (}m- ;J-hfl fODh'{'A "'!!o:t"m-') I1I\ODWII}T 'l'4.-t-~ tflj f-t-17 h'}f.tf't f:}-tJ(}. IMp'All}'} n'l'4.T ~h'}Y:" YA-t-h'{'I\m-'} ;t-hfl hlJ';J-h{}.'} l\U'Jflh'{'A fU'J.Y-l1m- h'}q.fl:J>ib fU'J_YflhTI\m-'} WlJ.1.U'Jflh6_A h'})).:FA f:t"hfl h~ fU'J.'{'1\..,OT (}m- U.oT ntpfl:"lJ' i'J.'." h'})).~J.'. ')-nl-f:,}I\ODH1nm- hilA f6J1.~ TOII1' fU'J.(}'I' ODtf't-,}fU'J.1A'" U'Jflm'}</'tY I\+ODtl1nm- (}m- J.'.(}II}A::

E- n'}trfl h'}</'''' (ID f+1I\Om- U'Jflm'}</'tY fY,l(}m-:J-hfl h4.J.'. U'Jflm'}</'tym- nY,l(}m- ncn </'') m-fl'l';J-h{}',} YAh'{'l\ h'}f.tf't f;J-h{}' "tll\P'AII}'}1\'}.olT OD1I;Jf1.m- I1I\P'AII}'} f"'ODII1nm- (}m-U.oT I1A+h.{,l\m- f;J-hfl o~ ODm') Otpfl:"lJ' +J.'."h'})).~J.'. TO'l1l J.'.(}II}A::

Q- n'}trfl h1</'''' (E)ODlPlT f;J'h{}'I1I\P'AII}'} ;J-hflfU'J..{,I\..,nT (}m- U.o:" OtpflTlJ' +J.'." h1)).~J.'.TO'l1l f(}m (}.tf1: OD1I;Jf1.m- I1I\P'AII}')' U'JlJ':t:m-1~ h~Y "J.'.mJ.'.q. 1.ol-l: OtpflTlJ' h1)).Y1Iff.l(}m- TO'l1l h1f.U'JlJ'rm-cr nu.o-l: IIJ.'. h1~1\fODY"'- (}'1~ J.'.ODH..,I1A: </'f.cr (}.A f-t-(}mfODY"'- OD.oT h1f."'mn</, tflj ftpfl:"lJ'm- '1"1'111fU'J..{,1\1m-1 :J-hfl l\U'Jflh'{'A nU'JlJ'rm-cr ODAh-n:lt.., h 1f. +() m ODY"'- WJ.'.cr h 1f. U'JlJ'rm-cr 1\.11o~ WJ.'.~ h~Y tflj J.'.~mt-A::

H- :J-hfl h4.V- fll\l\m- 'l'n:t'ntlU htp~ h~A E ODlPlT f+YH U'JlJ'rm-cr '}{Jl:"fU'J.YHm-: fU'J.mn</'m-: hlJ' fU'J.ODH1nm- n:J-h{}. 111\P'A1I}1.o:F J.'.(],lJ'A::U'JlJ'rm-cr 1\.1\fOD1..,P':" hilA nILuh~A ODlPlT f+ YHm-1 1.olT U'JlJ'rm-'}cr 1\.11~h1Y:" ODIPI.T OU'J~I.'" h1)).(}mm- wJ.'.~ h'})).-'-III\~I\T ODmfq. hJ.'."fA~:: f+YH 1.01.:" f+lim h'}Y,tf'th7iyaa: h+17m- 11H.o m-fl'l' :J-hfl h4.V- hU'J..{,I\..,n:,.o~ nl\J.'. ftf'1m- 11H.o 1\1.01.-1: 111\0.:" w)).ym-'t-J.'.ODl\ftA::

r;'

j!'

I-

7) Any person in possession of (or obligated withrespect to) property subject to seizure on which aseizure has been made shall, on the demand of theAuthority, surrender such property (or dischargesuch obligation) to the Authority, except such part ofthe property as is, at the time of such demand, subjectto a prior secured claim of creditors and subject to anattachment or execution under any judicial process.

8) Any person who fails or refuses to surrender anyproperty subject to seizure, on demand of theAuthority, shall be personally liabk. to the govern-ment in a sum equal to the value of the property notso surrendered, but not exceeding the amount of taxfor the collection of which seizure has been made(together with costs and interest on such sum)

9) In addition to the personal liability imposed bySub-Article (8), if the failure or refusal to surrenderis without reasonable cause, such person shall beliable for an additional charge equal to fifty percent(50%) of the amount recoverable under Sub-Article(8)

10) Any person in possession of property who surren-ders or makes payment in accordance with thisArticle shall be discharged from any obligation orliability to the delinquent person or to any otherperson arising from such surrender or payment.

11. Preferential Claim to Assets

1) From the date on which tax becomes due and payableunder this Proclamation, subject to the prior securedclaims of credtiors, the Authority has a preferentialclaim upon the assets of the person liable to pay thetax until the tax is paid.

2) Where a person is in default of paying tax, theAuthority may, by notice in writing, inform thatperson of the Authority's intention to apply to theRegistering Authority to register a security interest inany asset, which is owned, by that person, to coverany unpaid tax in default, together with any expenseincurred in recovery proceedings.

3) If the person on whom a notice has been served underSub-Article (2) fails to pay the amount specified inthe notice within 30 days after the date of service ofthe notice, the Authority may, by notice in writing,direct the Registering Authority that the asset, to theextent of the defaulter's interest therein, shall be thesubject of security for the total amount of unpaid tax.

4) Where the Authority has served a notice on theRegistering Authority under Sub-Article (3), theRegistering Authortity shall without fee, register thenotice of security as if the notice were an instrumentof mortgage over or charge on, as the case may be,such asset, and such registration shall, subject to anyprior mortgage or charge, operate while it subsists inall respects as a legal mortgage over or charge on theasset to secure the amount due.

12. Taxpayer SafeguardsAny property seized under Section 3 ofthis Proclamationshall be seized, held, and accounted for only by theAuthority. No other agency of the govermment mayrequire the property seized under this Section to betransferred or given over to it for any cause whatsoever. Ifany property seized under this Section is sold, anyportion of the proceeds in excess of the persons liabilitiesshall be returned promptly to the owner of the property.

1~ litI1 ~1..t-l\ ~:M"" ,;Ju,1IJ~'I'C 1) ;1'''1''1''' n"',} Iitfj~ 'H".-

IE' f1'~ttn. "'~;rIi' OtlU h1"'1\ OJ-il'l' "1'~ttn." cry/\:,. 01\.'}r-A'f

OJ-il'l' fDll..1~1 f;rtJil h4.~1 Ull:" Oi'oP/\hi':u) fh-q1f 111~:" hllJ~ Iflj fi-(}foP:/\) h~C~ o..} OJ-tJ.1.mf.9" O~C.r.' 0.:" f-Hi (/IJ

1'~ttn.tch) 011."'It- OJ-il'l' fDll..1~ ~C~.} q/\hf.t-:OD) ODf"" Of.tI;rOJ- FC,fDll..1~:

11') f'JP1'1 (}OJ-111~.}' fDll..fil1''&;~C mf.9"~) o~.., i-/\-;r fl\.AOJ-1 (}OJ- f1"'~ Fir fDll..f

tt,£~j

cry'iTOJ-9" (}OJ- ~OJ-::

~. 01\..}r-kf OJ-il'l' fA 111~.} 1'~ttn. Iflj f1'j'iOD

mf.9" 111~.} Of.tI;rOJ- FC f1'f.~1 1'~ttn. hi-j'iODO.} mf.9" 111~i: Of.tI;rOJ- FC h1'f.~10:"

ho-/\i: h.,.f.ODOJ- .,., "f.9"r: OIQ .,., 1./1. OJ-il'l'f1'j'iOD mf.9" 111~:" Of.tI;rOJ- FC f/\ ODIf't-1

A;rtJl'1- qAFAllJ1 cryil;rm:t> h/\O:"::

E' f;rtJl'1- q/\FAllJ1111~-I: 01'~ttn.OJ- f.tI;r FC f/\(}OJ-fDll..LA..,0:"1 f;rtJil ().&;/\ODIiL 1 fDll..filLA

1OJ-1 f11"11 ODm1 /\1'~ttn.OJ- 0K"m.~ fil;rOJ-:J>A::

Q' 1'~ttn.OJ-:u) 01o-il

h"''''(E) ODIP~.} O;rtJil qAFAllJ't-

f1'1AOOJ-1'f11"11 ODm1 mf.9" hcryil;rm<tfOJ- 0:\1\ Oil9"9"~.} f1'f.~(}0:"1 1\.1\f11"'0ODm1 h111~i: 7if6fJ> I\f. ""(1 /\11:rOJ- fll.,.9"llJA::

A) 1'''''(1 /\11:rOJ- 01''''ODmOJ- f11"11 ODm1 AtJ

f1'~hOOJ- 111~.} q/\o..} hlf~OJ- (}OJ- /\cry.LA1OJ-f;rtJil ().&;1'mf<t f.1f'iAII

ch) OtlU h1"'1\ f1'ODAh1'OJ- n.ljC9" h;J-tJll

"'f.9":"~'} fAOJ-1 cry'iTOJ-19" ().&; /\.h~A

f.i-I\A::

~. 1'~ttn.OJ- 01o-il h1"'1\ (E) f1'm"'(}OJ-1 ;I.tlll

01'ODAh1' 01o-il h1"'1\ (Q) ODIP~:" 1'''''(1/\1I:rOJ- h1..ct.,.OD'I' f1'f.~1OJ-1 f11t111 ODm1 O'LU

h1"'1\ /\1'm"'(}OJ- ;rtlil ttl\CP/\ .,.""(1 /\11:r Oi-'"ODmOJ-11"11 AtJ O..,A 1'mf<t f.1f'iA::

IQ' /\OJ-{I1i-1 ilAcryil;rm:t>

cry'iTOJ-9" ;rtJil h4.f.:-

Ii' iloo-: h~t-"liOJ- f1"'~ Ft-OJ- (1;r: hf.~~"f..t::

mf.9" ;rtJil fDll..hLAO:"1 CP1-;;:OJ-f1"'~ Fir

h 1:t>il:J>11.mf.9" fDll..fh'iOJ-'iTOJ- 1'..,qlr.} flf.~.}.:~. ;rtJil fD7..hLAO.} f1"'~ Fir h 1:t>il:J>11.fDll..h'im

10:" h~t-"li mf.9" il9":

f"'f~ h1Y.11'~ f.U1't- A;rhl'1- q/\FAllJ1 O~ "''i:'' 1./1.

OJ-il'l' cryil;r m:t>h /\ O.} II

tJ~A ht-.}

f.'" q~ fDll...,.C11O.} F C fl.}

I~' fho.i:;r hllJ~ I"tDll..i;ifho.i:;r hllJ~ I"tDll..i;hql\.} O;rhil q/\FAllJ't- ~I\&.h:t>t-n.~.} h1f.h..,ql1~i: 01n.sPi- DIl..~il.}C mf.9"h..,qq qAOJ-fhAA qAFAllJ1 f.(}fcryfrll

Ii' f h o.i:;r h llJ~ I"tDll..i; il/\ DIl..lj~OJ- FA llJ1'i 1''''q c:

Ii' I"tDll..i;OJ- 1'm~ ~-I: /\;rh(}' qAFAllJ11flj:U) O;rtJil h4.\"i- oP"'65J.h 1..ct~...: m/\~ .,.~ h 1.';.

f.~'" mf.9" f;rtJil ..,Y..;r h1..ct"li"liA fDll...,.CO'cryODAh:rsPi-1 AODODCODC'i OJ-"'I~ /\ODilm:":

Fe.deral Negarit Gazeta - No. 20 31" December, 2002-Page 2017

13. Duties of Recei vers1) In this Article, "receiver" means a person who, with

respect to an asset in Ethiopia of a taxpayer, is:(a) a liquidator of a company;(b) a receiver appointed out of court or by a court;(c) a trustee for an unrehabilitated insolvent;(d) a mortgage in possession;(e) an executor of a deceased estate; or(f) any other person conducting a business on

behalf of a person legally incapacitated.2) A receiver shall, in writing, notify the Authority

within 14 days after being appointed to the positionor taking possession of an asset in Ethiopia,whichever first occurs.

3) The Authority may, in writing, notify a receiver, ofthe amount which appears to the Authority to besufficient to provide for tax which is or will becomepayable by the person whose assets are in thepossession of the receiver.

4) A recei ver:(a) shall set aside, out of the proceeds of sale of an

asset, the amount specified by the Authorityunder Sub-Article (3), or such lesser amount asis subsequently agreed on by the Authority;

(b) is liable to the extent of the amount set aside forthe tax of the person who owned the asset; and

(c) may pay any debt that has priority over the taxreferred to in this Article notwithstanding anyprovision of this Article.

5) A receiver is personally liable to the extent of anyamount required to be set aside under Sub-Article (4)for the tax referred to in Sub-Article (3) if, and to theextent that, the receiver fails to comply with therequirements of this Article.

14. Notification of ChangesEvery taxpayer shall notify the Authority, in writing, of;1) any change in the name, address, place of business,

constitution, or nature of the principal taxableactivity or the activities of the person; and

2) any change of address from which, or name in which,a taxable activity is carried on by the taxpayer,

within 5 days of the change occurring.

Section 4Appeal procedure

15. Review CommitteeMembers of the Review Committee shall be appointed bythe Minister of Revenue or the competent authority of theregional government, as appropriate, upon the recom-mendation of the head of the Authroity.

16. Powers and Duties of the Review Committee1) The Review Committee shall be accountable to the

head of the Authority and shall have the followingduties:(a) to examine and decide on all applications

submitted by tax payers for compromise ofpenalty and interest and on the tax assessed;

1~ !li'f.!~ t..F..t.t\ 'i;J&-r ;lUll) ~'I'C tt ;J-..,..,P' ttl .po')Iif2~ 't.,.. Federal Negarit Gazeta - No. 20 .31" December, 2002-Page 2018

1\) h+lo-:" M1.-J::1'9»~ ;1C ..,')j..,+ l1\r""')lP/ljr""')9" f~,h.C;: lP/ll~:4'9»~ID"'" 0II~:4'9»~OD (} -0 ('111 II

th) 09"CODt. It,. fOl/.11""') .,..c;,. OOl/.OIII\h+

l11; "'C(l fOl/.mf"'''''') 1'14: h'),tlODAllh;1'h(}. hlDlt(}') ;1C 0+1':1' ID"'" +1':1'

f1A(f" "'')j.''+ 11\",.') lP/,)~""')'" (}",.fOD1't."":

OD) f :1'h (}. f1I\P' AIl)') f (}m"" f :1'h II ",.", ~

:"hhl\~: f+".7." hlj ,.U')') h'P~ m-o~

f+(}m 0110'),') f"7~;111': P'AIl)') ,.If ~

'PAIlf M1.-J::1' 1101/.1:h:1'h II h4.f"~ fOl/..,.C 0 m-') M1.-J::1'1\.1,. fOl/.~I\"" :1'hll h4.~ f:1'hll ",.lt~"7ll:1'ID't1Of.l (}",. 0 I +'1''''' ",.ll1' M1.-J::1''''',) t}+ ~ 0 .,""11f :1'h (}. f1I\P' A Il)')

~"k fI101/.1:""') f",.", ~ Olt-o1\.101;:" 1D"9" o",.",~ Olto- t}A+ll"7"7 ".h')I-J:')0 OD'"1\~ .,..c;~ h ') f. 1 'I' h,),tl:1' ,. 1\1101/.-J;",.

I\.ODA(}"" ,.~" A II

I%' OD"'6l>J.'}lll\lP/')lt:"fMl.-J::1' hll)~ 1101/.1:h'}f.h..,f1-o.,-J: f1n.9»~ OI/.tll+C

OJ"9" h.., f1-o 11\",. fh AA f1I\P' A Il)') OD7.f1D1l)""

ODOD~1 ODLPl"" O:1'hll h...~ It,. f+Il)I\",. hll+.c;f.t.'fOD+6l>J.Ooo-(\- lDf,9" OhkA h'),tl.,lt "71;~.., f,~I\AII

It. f,..,cftli' O:1'h(}' f11\P'AIl)'} f+"I\4C.""') f+~"7~ :1'hll

",.", ~ f OI/.:l'lD9" "7'1'r""9" :1'h II h...,. f:1'h II ,,,.It ~lP/ll:1'lD't1 hf.~ (}",. IDf,9" 0 M1.-J::1' h Il)~ 1101/.-J;",.", ~ h + (}m 0+ +') "f.9" c: 0 cD (LP" It) +'1'+ ",.ll1'Of11\P'AIl)). f+lD(}"""') +~"7~ :1'hll 2% (V9"ltOOD"') f11\P'AIl)). "')1; O"7ll111 I\..,-oc f,"'f1~ (}OI/.

.,.f1't f,"'f1~ f"7:"l-o OD-o+ hl\",.11~. O')o-ll h,}"'~ (li) ODLP~:" ff,"'f1~ M1.-J::1' +C(l

f..,-oC ""'f1~ .,.f1't :1'hll h4.~ O+~"7~ f+lD(}'1o:,.') :1'hit Ooo-(\- 1Df,9" OhkA fODh4C.A ..,1..:1'

h ') ~ 1\n + ",." ~ h (}m 0+ +') h,) ll.,. 0 cD +') 1..tL

",.ll1' :1'hll h...~ fOl/.4C.I\..,n+') +~"7~ :1'hllt}Ah.tl\ 1''''+~ """11

[. nH.U h,)+~ ')o-ll h,)+~ (li) O+ODI\h+"" l..tL

""ll1' ,..., f1~ t}A .,.~ 0 0 f1I\P' All)). f +lD (}'1",.

+~"7~ :1'hll ""hhl\~lj fOD~~if (flf 1D,tl1"").+h...f, f,(flj All

2' fH.U h,}+~ ')o-ll h,)+~ (li) 1;');11. h')f.+mO.,.(flj 01n. ..,-oC h'P~ lll\f,"'f1~ f+f..,.,.,.+ h,)+Y.~h'}f.h..,f1-o":1'r"" OH.U h'P~ OIILP~+ f+lD(}).:1'h"~,) nOl/.ODI\h+ I\OI/.+CO-f,"'f1~~ +4C.~0I/.f,(flj (\-11

Ii!' flP/ll~~:" ~"k 'l:"f +lD(}'1OJ- ..,-0C 01l:f;A IDf,9" f :1'h (}. f11\P'A Il)')f(}m"" ",.",~ +hhA hf,f.I\9" nOl/.A OOl/.+C-ohChcf"7ll~.c;-J: ~"k"+ f+ID(}"""') :1'hll 1Df,9" ff11\P'AIl)).'} ",.lt~ fOl/.:l'lDOD",. (}",. f,l1'ljAII

tJti:A h 9" ll+

h II+.c;f.t.'f :"Il)"'~

"7it;1'ID'tI') 01..tL",. f11\"7:"~-o lll\OI/.4C.09"

~.

[.

?}. f:1'hll:"Il)+

li' OH.U h'P~ 0"-" h';».:\,) h'),tl4C.R9" h+ID(}"""

Oll++C: n + ID(}.,,,,. 1..tL ",.ll1' f:1'h II "7 it:1' ID:"

"'1..:1'''''') IA+1D1l) :1'hll h...,. I\""fn+ I\hl')~'}~ lDC 1D"9" flD~ hkA 1\11''''''' l..tL: IA+h4C.1\",.') :1'hll ~% (h9"ll+ OOD"') 1)~% (VI h9"ll+

nOD"') hit h. qu" 1;~ll OD+6l>J.f,hC;:"A::

(b) to gather any written evidence or information

relevant to the matter submitted;(c) to summon any person who directly or indirectly

has dealt with the assessment, to appear before itfor questioning him about the case under itsinvestigation; and

(d) to review determinations made by the Authority

for accuracy, completeness, and compliancewith this Proclamation.

2) The Committee shall only review applicat!Clnssub-mitted to it within 10 days of receipt of taxassessment notification.

3) The Head of the Tax Authority may approve the

recommendations or remand the case, with hisobservations, to the committee for further review.

17. Waiver of PenaltyThe Review Committee may waive administrative penal-ties in accordeance with the directivies issued by theMinsiter of Revenue or the competent authority of theregional government, as apprporiate.

18. Appeal1) Any person who object to an additional assessment

made by the Authority has the right to appeal, within30 days from the receipt of that assessmentnotification, or from the date of decision of theReview Committee to the Tax Appeal Commissionby depositing in cash with the Authority an amountequal to 50% of the additional tax assessed.

2) If a person appeals in accordance with Sub-Article(1) and the Tax Appeal Commission determines his

tax liability, that person is in default unless he paysthe additional assessment determined by the TaxAppeal commission within thirty (30) days of thedecision of the Commission.

3) If no appeal is made within the period prescribed inSub-Article (1) of this Article, the Additional assess-ment of the tax made by the Authority shall bedeemed to be correct and final and shall be im-mediately payable.

4) Without prejudice to Sub-Article (1) of this Article,the provisions of the Income Tax Proclamation,concerning appeals shall, mutatis mutandis, apply toappeals regarding taxes imposed by thisProclamation.

19. Burden of Proof

The burden of proving that an assessment is excessive orthat a decision of the Authority is wrong is on the personobjecting to the assessment or decision.

Section 5Administrative Penalties

20. Penalties for Late Filing

1) Except as otherwise provided in this Proclamation, aperson who fails to file a timely return is liable for apenalty equal to 5 percent of the amount of taxunderpayment for each month (or portion thereof)during which the failure continues, up to 25 per centof such amount.

'A" 11tll1 U.~A ~;J~:" ;JILtli ofI'I'Cr ;f-"''''P' r. !1ff16,.,..

I' f;l-h" .,";l-ID-I:l -:"l-fl I1AO+ mc ID~" flD~h4l.A Oll'~. 1.", f:J"h" "''':J"m-l:l1I\ottO ft.Olt.U ""+A" "0-" "..otlt (Ii) 1:";11. oPlPt""

f"th~A"" -+... h-flC !l 1f. (VfO/t 1f..,) "1-0A'I'fOll

r. Alt.., "..ot X"".I. 98fO 1 A .,.h.l.A ;l-h" ~(Dof",,,,,,(Do

O;l-h" "''';l-ID-I:ll\'' oP;l-f"" 0 ~OtO"" '-Ii :1"hi't-

-hLA 11A0"" ot.. O.,.ht.AlJJo ;l-h"oP"'hA lAlJJo

A \t~"" ~lJJoll

i' O",Ii:flJJofO .,.1.;1- f"71'.A(Do :"tIJ"" +'I'fto h"'oPA

h-t:"" hll:""'~.'~i't "1-1I'1fOIu) -flCI1f.A) O;l-h" "''';l-m-l:l 1\" --Ah"" h~OlO""

f:1"hh -m" f OoP'" (,,'}.(' oP'" TCi't'}"")

ri' "1M O.,.hLA ;l-h" 1\1-"A"7.;l-ft1l mA.('

i' -hLA O~OtO"" IDC I\A.,.hLA ;l-h'" -h.l.Ah~OlO"" +'} '-"h.,.h.l.AO""+'} I1AlJJo1.", lJJo"'I';l-h" h4-\t mA.(' f-h.l.A ..,,.;1- "AO"":I

I, 0lt.1J" '}+It .. 0-" "'}+It Ii - II't"" f"7.h.l.A (Do

IDA.(' fG'I"hL! Ah I1ALlJJof~1I 'oP"" o'}..,.('

11 1- pI~ 1\" OCPAlJJoh~"'~. MO~~IIDA.('O8tlJ1. 1\" rlJ OoP'" (VI "fO""" 0-.,.) ;l-hftoO""

"lI'liAII

htt:A ".('"..,.

fID"~A :"tIJ"'~

f"'7..I.O"'" ID'}~fto~ "A"7.-~O"" ~~rl' O;l-h" ""~C,..,.Olt.U htt:A f"'"t"~"" O;l-h" 1\" f"'7.LOIJDolD'}lfto~

fID'}lA" 08:"" ;"1-'} O-.,.I\Att: f"'7.LfJIJDoO-II'~hi't- f"7.08lPt"""'f f"t;l-f. '-Ii ""'11~ f"7.+COlJJoOID'}lA" -:".. ;,.", ~~ ~C,..,. oPlPt"" "l1'liAII

reo ;,...,.. O-tlJ" ;l-h" "I\AoPh.l.A;".." O-tlJ" fi'tOi'tOlJJo'};l-h" 11\";l-m+ m1-fO f"7..I.A..,O""'} ;l-h" lAh.l.A "'liTlJJofO i'tlJJom,}~A '-'}~Ua08 Um&-AII "AII'~fO Olt.U "CP~ htt:A lJ -11"""

h"'7.tlJAO""-+Mii 0"'t;Q."'~ 'I'4-"'~ -11'~ Ott:C.(' 0.""i't.l;J"'I' h~ ,-..,. 0",,,,, ~~&-..,.1-+tlJAII

ri' fdti't"" ID"" ,,/t/t~ oDl~ "A",:"l1l

i' "'IliTlJJofO;l-h" h4-1-1u) A;l-hc\-I1A~AtIJ'}11'&-"'''"..~ ~'I'1I0.,.-

Ah.,.fUi't""ID"fO"

~ -l~ lottO' lD1-fOA) A;l-h i't- q A~ A tIJ'} II'&-.,.~ t\. otC1I h"7." I1lJJo

-..,A.. ."'1' -..,A<Ai(Do'}"

~ t\.1~C'"0"7.~A ,,\\:\ '} oP"'''''''' f"7. .,qTlJJo'} ~'I'(1:f

'''+l '-1~II'~f fm"1:A h" 1--lPl""O;l-AIII' f., /t.,. -.., A<Aif .,.ftmlJJoID1-fOoP1}"''''' f"7." 11(Do

~'I'-fI f"''''IDlJJo lAO-l: fOh'}''''' fl1'~ '-,}~11'~'u) foP"'AMiilJJo""hhA~ ,A-II''} t\.~l"O""

IA-rit' t\.h.l.A f"7..,l1lJJo;l-h" h1lC Ii if.O",,.OA'I' ,,'}(\ '-1Jlh.l.A f"7.'~C'" hll'~;l-h" h4-\t h-oC I if. 0""'" '-Ii h1lC r if.0"7"OA 'I' '1"'"11 -+<Ai '-Ii h" ,.(' 'oP""0",,,,, '-Ii hi: ,-..,. 0",1-0A'I' '-~&-..,.,.ottIJAII

A) ,,'}(\ '-'JlhLA f~l"lJJo :1"h" h1lC Ii if.f"7.0A'I' hll'~ h-oC S if. O""'}" ~Ii h1lC f if.

0"'1-0A'I' f.,,"-o -+<Ai '-Ii h",,"" 'oP""0"7"" '-Ii h""""" 'tIP"" O","OA'I' '-P'&-""UtIJAI1

e. f dti't"" -.., A<Aif.,.i't m lJJoID1-fO ,...,. f"7." 11lJJo~'I'-fI '-'}Jl"'''':'' IA"'~l1lJJo II',} .,.1Ifto ID"fOOhl1.(' :fA"'~~"" fll'~ '-,}~II'~f

Pederal Negarit Gazeta No. 20 31- December,2002 Page 2019

2) The penalty under Sub-Article (1) of this Article islimitedto ~O,OOO Birr for the flfStmonth (or portionthereot) in which no return is filed.

3) For purposesof this Article, an underpayment of taxis the difference between the tax required to beshown on the return and the amount of tax paid bythe due date.

4) In any event the penalty may not be less than thesmallerof theMo amounts:(a) 10,000,Birr;(b) lOOpercent of the amount of tax required to be

shown on the return.

21. Late Payment Interest1) If any amount of tax is not paid by the due date, the

person liable is obliged to pay interest on suchamount for the period from the due date to the datethe tax is paid.

2) The interest rate under Sub-Article (1) of this Articleis set at 2~% (twenty five per cent) over and abovethe highest commercial lending interest rate thatprevailed during the preceding quarter.

Section 6Criminal Offen~es

22. Procedurein Tax Offence CasesA tax offence under this Section is a violation of thecriminal law of Ethiopia and shall be charged,prosecuted, and appealed in acc.ordancewith EthiopiaCriminal Procedure Code of Ethiopia.

23. Tax EvasionA person who evades the declaration or payment of tax,commitS an offence and, in addition to any penalty underSection 5, may be prosecuted and, on conviction, besubject to a term of imprisonment of not less than five (5)years. .

24. Making False OTMisleading Statements1) A taxpayer who,

(a) makes a statement to a tax officer of theAuthority that is false or misleading in amaterial particular, or

(b) omits frOni a statement made to an officer of theAuthority any matter or thing without which thestatement is misleading in a material particui:::r.

commits an offence and is liable on convcition..2) Where the statement or omission is made "',lthout

reasonable excuse,(a) and if the inaccuracy of the statement were

undetected may result in an underpayrnent oftax by an amount not exceeding 1,000 Birr, lO afine of not less.than 10,000 Birr and not morethan 20,000 Birr, and imprisonment for a ternlof not less than One (1) year and not more thanthree (3) years, and

(b) if the underpayment of tax is in an amountexceeding 1,000 Birr to a fine of not le~s than20,000 Birr and not more than IOOO,OC'O Birrand imprisonment for a term of not k~;s thanthree (3) years and not more than five (5) years,

3) Where thestateplent or omission is made knowinglyor recklessly,

110 17(.~~1..t-A ~;Jt-r ;JtLtiJ<liTe~ ;MulP' ~I"" Iilf1~,.,... Federal Negarit Gazeta- No. 20 31" December.200r"-' Page'2020 -

v) fou..,A6liLlD--rhhA2i' lAou", l\.~l"OTlAouiF/r l\.h~1\ f"t11)lD- ;t-h" h-flC Ii itO"7"OA1' h1(\ h'JLh~A f"7.1~C'" h"~'+h" h'i-~ h11C !l it O"7nn h'i h11C f itO"7"OA1' f1")n11 ~+6IiL h'i hh"'''T 'iOUTO"7f")" h'i hhp'C 'iOUT O"7"OA1' hP'&-TI

A) h,,)(\ h")-'lh4C.~ f~l1lD- '+h" h11C Ii itf"triA1' hlnh11C <:T;it O"7n" h'i h11C Ifit O"7"OA1' f.,")n11 ou+6IiL h'i hI 'iOUTO"7f")" h'i hIt 'iOUT O"7"OA1' hP'&-T"+tfJAII

?;T;' f.+h,,"") I)AP'AtfJ") P'&- "A"7(aCjhA6' "7'i:flD-'" (alD-1 . .~

V) OrltJ h'P~ OUlPlT P'&-lD-") O"7h'i(l)")""fA").f.+h" I)AP'AtfJ,,) 1P&-"'2i'.,...,I)C f(a'ihA

(I)"'" A"7(a'itlA f'l"hl. f f1I"'"A) fh'P)t.") h4C.'IO'" O"7'iTlD-~

"""h\to:\")

f(a'ihA (1)"9" A"7(a'ihA f'l"hl h")~ln fm")1:A OU4C.Oao-.,.l;l"'tn f It.~l~OT h11C

liit O"7f")" h'i h11C fit O...,"OA1' f1")n11OU+6IiLh'i Oo-AT 'iOOT hP'&-T 1A"tfJA II

I' f"th.,./rT h'ih~.un foota(a/r A.l\-T "''''I)C'Tf.+h,,"") I)AP'AtfJ") P'&- f"7(a'ihA "''''I)&-T1f~lD- "m(a~/r ;

v) f;t-h" h'i-~") 10. h"1"£ fP'&- h,:"":J>f\9'T")f"tOUAhi: (a~p..~1 I ~;r.c"'T' (I)"'" h.~T"7'iTlD-")9" OUl1f9'T ADDOIJCDDCf;t-h,," I)AP'AtfJ") It.m'':''.U~2i' 1ft;" lA0D1;+ i

A) f'+h,," I)AP'AtfJ,,) "1'14: h1-'l+C11 It.111~:J>~?/ 1ft;" fAOD1YT i

tit) f'+h,," I)AP'AtfJ") 1P&-"'2i' (I)~;t-h" h'i-~f,,)"'~ pi&- (1'+ ""...,1)+ lAlD-1 OOoOTOD1~11 II

fIi' AlD-1" fA"7"'+(I):"h'+Jt Ii O"7.1nlD- ODlPlT' 0o-1;t-9'T "I. f"'~l'"AlD-tnT' A;t-h,," I)AP'AIIJ' '''it;t-(I)+ "7'iTlD-~ (alD-

1''i-'''2i' ODIf). Ott:C~ o.T It.l;l11' IV) 1''i-i: f.,.4C.OOD(J)o1M .,.00 (I)"'" Ohl)~ TA.,.

~hT flf~ h,,)~If~ h11C lit 0"71")" f1,noOOD+6IiLh'i Oh,,)~ 'iODT hP'&-T i

A) O,,"""T o-1;J-9'T hoOC T;it O"7n" f1")n11ou+6IiLh'i 0'; mc hP'&-T ~+tI)A II

f)1. O;t-h" I)AP'AtfJ)' IP&-"'~T f"tUlao-1'~T

Ii' f.un h'P~ ~");l1.9'~ Aoyit~,9" O:t'h" I)AP'AtfJ). f"'+ml IP&-"'~ (I)"'" 1'+~'l" "'+tfJ~f~Ol;

V) Oih.., ODlPlT l\.11;lD- h"7.11) htt:l (I)"'"7iA"7T lD-QJ"h~+mlOT .,...,I)C ;lC 0""1nO+1';t- (I)"'" +1'.,.1jI I)AIf~ OD'1~ f1")n11

(I)"'"""" 'i"~T htt:l (I)"'" "tn;t- h")-'l~l

..,AT fmf+ (I)"'" 1'.,.+01\ f Ahtt:llD- (I)"'"A"tn;t-t& ",,,4<0(I)"" -'V fmf+ m"".f.,.+OA (I)"'" i

A) h;t-h" 0"t1ilD- 10.""

"7~OCOC m"".htlU h'P~ ~';11;9'T ;lC (I)"'" h"'(amlD-~"d.~T OUAI1"'h~'"'' ;lC f"'U"l,,) .,...,I)CAou~O'" i "71:l.., f"t11)lD-") h"7~l'"Aou;t-+oOI "'10. lA.If~,,) ~1C AODtt:+~ i

O;t-h"""

fDtUJ'" f"7~OCOC .,...,I)CAou~O:" (I)"'" O"tn1'C AOD"''''OC t&A "11)(I)"'" O"t 1 I)lD- "7'iTlD-'" lD-A lD-"1' OtlU.,...,I)C ou"'I)O~ ") fOUta" ""''''~T f(am f

1''i-'''~ oulf)' Ott:C~ I1.T It.l;l11' h11C !litf"7"OA1' f1,noO -~ h'i hI 'iODTO"7f'" h?; 'iOOT ft.,"OA1' hP'&-T"+tfJAII

(a) and if the inaccuracy of the statment wereundetected may result in an underpayment oftax by an amount not exceeding 1,000 Birr, to afine of not less than 50,000 Birr and not morethan 100,000 Birr, or imprisonment for a termof not less than five (5) years and no~more thanten (10) years; and

(b) If the underpayment of tax is in an amountexceeding 1,000 Birr, to a fine of not less than75,000 Birr and not more than 200,000 Birr orimprisonment for a term of not less than ten(10) years and not more than fifteen (15) years.

25. Obstruction of Tax Administration1) A person who,

(a) obstructs or attempts to obstruct an officer ofthe Authority in the performance of dutiesunder this Proclamation, or

(b) otherwise impedes or attempts to impede theadministration of the Proclamation,

commits an offence and is liable on conviction to afine of not less than 1,000 Birr and not more than100,000 Birr, and imprisonment for a term of two(2) years,

2) For purposes of Sub-Article (1), the following andsimilar other actions are considered to constituteobstruction;

'(a) refusal to satisfy a request of the Authority forinspection of documents, reports, or other infor-mation related to a taxpayer's income-producing activities;

(b) noncompliance with an authority request toreport for an interview;

(c) interference with a taxation officer's right toenter the taxpayer's business premises.

26. Failure to NotifyA person who fails to notify the Authority of a change asrequired by Article 14 commits an offence and is liable onconviction

(a) where the failure was made knowingly orrecklessly, to a fine of not less than 10,000 Birrand to imprisonment for one year; or

.

(b) in any other case, to a fine of not less than 5,000Birr and to imprisonment for six months.

27. Offences by Tax Officer1) Any tax officer or former taxation officer employed

in carrying out the provisions of this Proclamationwho:

.(a) directly or indirectly asks for, or receives in

connection with any of the taxation officer'sduties, a payment or reward, whether pecuniaryor otherwise, or promise or security for thatpayment or reward, not bieng a payment orreward which the officer is lawfully entitled toreceive, or

(b) enters into or acquiesces in an agreement to door to abstain from doing, permit, conceal, orconnive at any act or thing whereby the taxrevenue is or may be defrauded or which iscontrary to the provisions of this Proclamationor to the proper execution of the taxationofficer's duty,

1A' 11(11 1.1.("A ~;J&T ?UII} <t1'C ~ ;J-"'~I'"'~1"'1 Iiin?i ,.,.. Federal Negarit Gazeta- NQ. 20 31" P'.< ;;.'<' "..:f--2,02 ~

~,Ili""""'~"'..,""~,., :.,, ....

...-."

,., ,.,,' ",."..-

I. f;J-hh tll\P'AtJ)). 1Pt.-t-~ f"~ mf.r f~Ol 'he;fH.U') h'P~ 1:') ;J1.9'"f I\"'ilLIJr f-t-"'ml :01\.-1'f-k 1 ')..,1: :It.., 0')'" 1: :Jtl.tJ) ;J-+1fP'h').Il mtJ)h;J-HHeD-~f.~+ ool)f Oil-t-"'C :

u) ;J-hil,) O"'ilLIJr l11: tlt\eD- P'AtJ)') mf.r..,f..;J- rh') 1:" 1 m"'eD-') f 1\." (leD-"'t;TeD-')rool)f I\"'t;TeD-r 1\." (leD- mf.r fH.1 (leD-mh.A t\ln (leD-hltA£ f(lm :

1\) OH.U h'P~ oolPl-1' ;J-hil,) O"'ilLIJSf" l11:1 t\eD-') P' A tJ)') t\ 00 m"'9" mf.r fP' t. ..,f..:r')I\oomtJ)-1''h')"l1il"fA O;J-tlil tll\P'AtJ)). H')1:f°"l.:fYeD-') "'t;TeD-')r ool)f O~C1: 0.+-1',).,11 I1AIf~ Oil.,..,.C I\V'il-t-~ m1') hltAl::fflm 'h,)1.If~ :

'I'4--t-~ oolf)' O~C1: 0.:"l\l.71'1' h11C In. 0""1ilf1')tl11 00"'65j. 'ht; ho-t\-1' ~oo+ O"",)il hhSf"il+~00-1' O"'f.OA'1' 'hP't.:" f."'tJ)A II

c. fH.U h')"'''' 1:').7"1. f:rhil tlt\P'AlI}). 1Pt."'~ :u) "'t;TeD-')r (I~1: mf.r ool)f:-

(i) t\H.U h'P~ mf.r t\"'t;TeD-Sf" 11tHI ~tI

h'P~ hL'IJSf" hilL"1. Olf~ 1.H. :(ii) O:lt.., f-t-(lmeD-') .,...,tlce; ;}"k~-r

I\OPmll}+ hilL"1. 1\1f,): I\'Pt;eD-

1>Jl-t-C:(iii) ool)f t\ool\'Pm'1': -t-1.t.t.f1. ..,11C') t\'"

il"'l+ h,:,.r-k1 hl\.t\"1- h1~1- .7Ctl1.l11-eD- ilrr~+ oolPl."f' h..,tl11

""TeD- fl\.ft<>1-h1~1- tll\P'AlI}Cf1-:(iv) O:lt.., f-t-flmeD-') -t-..,tlct; ;}"cC.~:,.

I\oolDlI}:" hilL"1. 1\1f'): t\P'~ r..,l1ct;

t\ IJl 00-il t; f1"7.7i'):

(v) hH.U O"f. "A"'11\~ I\"'t;TeD-C}" :It..,hitL~"7. 00/0.+ ..,f..:reD-1 I\OOL~rf"7.1h 1-t\eD- ool)f 'h')"lflmeD- h111.9'1-"7.~il1:C O"',h.~ I\:rH1H

1\) ;}".c.~:rTeD-') ~oomll}:" hilLf\1. 'hilhlf~ 1:lilh,) 1:') fleD- I\f.-t-eD- f'" f.m:"

{}. 00 l)f 9'1-')

1\",e; TeD-C}" 0 00')'" P';" 1 11. P't. "f. t\ "7.11

1\'"A 'he; I\it;J--1'l\ 1:tI it 00/0. + IPt."'~~oo itm -r h1'" 1.eD-C}"::

tI~. "f.L.,.1: :rtlil itt\(JDfl11fl11

",e;TeD-C}" (leD- OH.U h'P~ oolPl."f' ltf.L.,.1:t\+ :rtlillDf.C}" 'h')1.:rhit f"7.:rf. 1\." tI~1 f(lO(lO mf.C}"I\oofl11fl11 flfPhl m,)~A fL~oo IfCf: '1'4-"'~ oolf)'

O~C1: 0.:" I\l.'l1'1' h11C !in. 0""1 it f11 H11 00"'65j.'he; h~ ~00-1' O"'f,)il hI ~00-1' O"'f.OA'I' 'hP't.+,..,. tlJA II

tilt. ooc~-1' lDf.r "'Ol:r;J--1'"''iTeD-r "eD- fH.U h'P~ 1:1.7"1.9'1- 'h1"ltIJ{}. f l.';:10l:r:rf 1~ltlt: mf.r O"7.it'1'C f-t-110l 'h') 1.1f~'h,)1.'P')~eD- 'I'4--t-~ fH.U') h'P~ 1:1;J1.fP1- oooll}h

'1'4-:" f.L'GOOJAI: hH.U O"f. f-t-tlltl~""') fL~OO (1m.

'I'4--t-~ 001Y). O~C1: 0.:" I\l;J1'1' ')C.';;J-eD-1 mf.Sf"."f'1111~') t\flmO:" '1'4-:" h-t-mfl~eD- f1')H11 'ht;f'hP't.:" :"lI}-r tlAOl\m 01')tl11 'ht; O'hP'&.+f."'lI}AII

0. 01:C~"'1- f"7.L~r '1'4-:"

li. o')o-it h,)"'1\ (c) f-t-1.~11m. 'h')1."'mO.,. IfCf:h')1: 1:C~-r f.U')') h'P~ Ooo-t-"I\~ '1'4-+ fL~OO"'')1..,., '1'4-1: O""J.~OO1.H.f1:C~1: P't. hith.1~fl1'~ "''i:feD-1}'' flCD-01:C~1: f-t-L~(1Dm-1 '1'4-+'h,)1.L~oo -t-"''1'~: OH.U h'P~ f-t-lI}t\m- :"lI}+.,.1..'''7. f.1f') O;J-A::

commits an offence and is liable on convctiOn to afine of not less than 50.000 birr and to imprisonmentfor a termof not less than teo ( !

"~':'n ,one! '~utmorethan twenty (20) years,

2) A tax officer or former (;"" . ,yed incarrying out the provisions or thisP; \ ,'; Jdmatian.

except such information is requir~d th C')mmer-cial Code of Ethiopia to be putJ1ishcJ in the Ti.1deGazette, who,(a) discloses to any person or that person's

representative, any matter in respect of anotherperson, that may, in the exercise of the t.:.xationofficer's powers or the performance of thetaxation officer's dUIit's under the saidprovisions, come to the taxation officer'sknowledge; or

(b) permits any other person to have access torecor~s in the possession or custody of theAuthority, except in the exercise of the taxatIonofficer's powers or the performance of theofficer's duties under this Proclamation or byorder of a court;

Commits an offence and is liable on conviction to afine of not less than 10,000 Birr and to imprisonmentfor a term of not less than two (2) years and not morethan five (5) years.

3) Nothing in this Article shali prevent a taxationofficer from disclosing,(a) any document or information to:

(i) any person where the disclosure ISneces-sary for the purposes of this Proclamationor any other fiscal law;

(ii) the Auditor-General where the dis-closure is necessary for the perform.wceof duties entrusted to it by law.

(iii) the competent authority (If the govern-ment of another <.,it!!1!', ""!lh whIchEthiopia has ente.red i 'j "i,J<:(,[i'!nt

for the avoidancc uf duubie ta:.,atll . ,n

for the exchange of infonn;u1un. tu lll':.',extent permitted under the agn:cmcJ1I,

(iv) the Ethics and Antl-CCHTUptlc.n (\:;-0-mission where the disclosure IS nc~:cs-sary for the performance of dulic'; en.trusted to it bv law.

(v) a law enforcement agency no! '.kscrit)'~dabove where the Minister of RCVCIIUI:issues written authorizationto make disclosures necessary for the enforccmC'!i! ofthe laws under the agency's autholity: '.'1'

(b) Information which does not identify a spc,ifi<person to any person in the service of the :;takin a revenue or statistical departrnent \vhercsuch disclosure is necessary for the petrOlmance ofthe person's official dutie:;

28. Unauthorized Tax CollectionAny person not authorized to collect tax undC' thl"Proclamation who collects or attempts to collect l,lX Wan amount the person describes as tax comm;ls a"offence and is liable on convjeticn tn :) 11C ;c':'than 50,000 Birr and to imprisonrnent iUl a [CII,nnt j:()less than five (5) years and not more than ten (j OJ >~:ar'

29. Aiding or Abet(ingA person who aids, abets, iJwites, or conspire, v, i1',another person to commit a violation of this Pf(X:!;)!i;;J,)also commits a violation of this Proclamation. n'~.,perspn may be subject to prosecution and is hat..:;, (!'conviction, to a fine and imprisonment, not in cxu~ss ~the amount of fine or period of imprisonment pn ':id.::for the offence aided or abetted.

30. Qffences by EntitiesI)Subject to Sub-Article (3), where g, :.:('r1ir;"~ i

offence, every person who is iJ !k ::;n;' t:, .

that time is treated as also having COJTJmn\!;1;,.:~i',ani',offence and is liable to a fine and irnpnSUi:';.::d I,""this Proclamation.

1}\' ~;r$~ ~f..MA ~.7t"" .7ff.1IJ ~TC ~ :M..,P' ~I"',} Iiln~ ,.9'".

~.

Federal Negarit Gazeta - No. 20 31" December.2002-Page 2022""'~.,-

y~_;e','.Z~-. -~ ... ',-.,,~.~-,

OH.U h,}"'1\ '}(HI h,}"'1\ (C) f.,.1.'1""CD- 'h,}1..,.

mO.,. If'i: O'/CjTCD-ijUf:C~:" OH.U hfJ'~ 001P1.:"

lLht.A fOl/..,qCD-') (JJf.ijU hfJ'~ 'h'}1.;rtJil fOl/.4'>'1'I.CD-') 0'/ CjTCD-'}ijU 't'" tJ lJ:f ., 0. Itf 1.C<? f.,.1.'h'}1.If '1 '1'~-I: O.,.t.KooO:" 1.tL (JJf.ijU'1'~-I: h.,.t.K000:" 'UJ. hil.,. f:1fP 0'10~:" itf:il:" (JJto:" CD-il'1'ff:C~-I: P'to hilh.f~ f'10~ (),-:f hf:C~-I: 'h'iht\.l\CD- ()CD-;1C Oh'}f:'1:"'i" O"'CjmA f;rtJ,," ql\P'All)'} l\OI/.t.A.,CD- ;rtJit 'hCj A.tto:f tJlJ:f,-:f "'mfctf.IfCj f\cII

O'}tJ.il h,}"'1\ (Ii) 'h'i" (I) f+1.'1""':":U) '1'~-I: f.,. t.o 00 CD-<?l\ (){}-Itf CD-:J>(JJf.ijU Itf. ilO'/

0'/0:" hlf'1:l\) h,}~' '1.,t::f'} 0'1''}.4>-I: fOl/.ff. ()CD-O.,.ooltltf.

V-1;r CD-it'1'f'1'~-I:,) ooUijU l\ooha\hA f.(JJil.';TfJ' A .,.-0 tto fOl/..,00-1: '1''}.4>-I:,-:f'}: .,.., 0.CD-'}:";1:" 'hCj fhlPtoC '1'0-0 f.,.IfPa\O:" 'hCijUjf<?l\ () {}- (JJil P. f.,.., 1 'h,}1.1f'I: .,.t. , 01/.hf.If'l-O:"ijU::

l\'}tJ.il h,}"'~ (Ii) 'hCj (I) ht.,OijU "P'to hilh.f~"0'/ l\ :,.;

u) f'liCtJ'i O'/"'OC'} OOl/.ool\h:" f'liCtJ'i"CD-O'/"'OChqA (JJf.ijU fO'/"'O~ P'to hith.f~ (JJf.ijUhv-l\-I: ~a\'(''1''':f Oh,)~ 'h'}1.OI/.lPto If'i

fOl/.:rf.:l\) h-q'} f'} OOl/.OOl\h:" fh-q'} fCD- f P' to oo~:

P'to hil h.f~ (JJf.ijUO'/'i"TCD-ijUA.a\ if.ijU (JJf.ijU

h'h'1H.U ~a\'(''1''':f Oh,)~ 'h'}1.OI/.lPto If'ifOl/.;r f.:

tit) f()~:f'} ..,-01.:" OOl/.OOl\h:" f..,-ol.-I: P'to

hith.f~ (JJf.ijUOH.V- ~a\'(''1:'' 'h'}1.OI/.lPto If'ifOl/.;rf. '1CD-::

i!H;' O"'I.\1o.~:f fOl/.t.OijU '1'~:"

ii- O'/'i"TCD-ijU()CD-Oh,}"'1\ Ic '}tJ.it h,}"'~ (!l) 0.,.1.'1.,., CD- 00 IP I.:" 1tf.t.~ijU f.,.1. 'h') 1.If '1: '1'~'" ~ '1-1:OlJ:C.(- 0.:" l1.1.;1.,'1' -oc ~if.u f.,'}H-o 00"'65i. 'h'i"

Oh'} f: '}oo:" 'hP'to:" f."'lI)A::~. O'/'i"TCD-ijU()CD-Oh,}"'1\ Ic '}tJ.il h,}"'1\ (!l) 001P1.:"

l\;rtJit tJlJ:f fOl/.CD-l\CD-').,'}H-o l\M ql\O'/il.,.onm-ijUtJ'}f:" O'}tJ.it h,}"'~ (Ii) 001P1.:" '1'~"'~ If'if"'''1 'h,}1.If'1 lJ:Cf: 0.-1: h.,'}H-oCj 'hP'to:"00"'65i.CD- 0"'Q;1,0'/~ l\M fa\it",oomCD-'} f.,'}H-ooom'} l\;rtJ"" ql\P'AlI)'} .,0. 'h,}.Jl!1.C<? lLf1lf.:fa\AII

@!.. f<M..,.~:f'} itijU O;1tLlI) h:"1fP itl\O'/CD-lI):"

Ii' f;rtJ,," ql\P'AlI)'} OH.tJ hfJ'~ hh,}"'1\ ttt-r!J1i

f.,.1.'1"",:"'} f(JJ'}1:A '1'~"':f Ooot.KijU f.,.t.I.1.qTCD- (),-:f itijU 1IC1IC Of1.tLCD- O~l\;r'f ;1tL(O:f;r:"1fP 'h'}-'l(JJlI) f1.C;1A::

~. OH.U h,}"'1\ '}tJ.il h,}"'1\ (Ii) 001P1.:" ;r:"""fOl/.aJlI)CD-1IC1IC:-

v) ff:C~-I:,} aJf.ijU f<?l\(){}-,} ilijU 'h'i" hf:toif:l\) ql\P'AlI)'I- "'.,0. '1CD--Otto fO?fijU'}O:"'}

f(JJ'}1:f\c'} ht. 'OijU 1IC1IC:ch) '1'~-I: f.,.t.OooO:"'} f<?-oc Hoo'} (JJf.ijU

Hoo'i:f:00) ltf.ht.A f.,.I.CD-'} <?-oC oom'}:

IP) 0"'Q;1,0'/~ 'h'}-'lh~A f"'(JJ()'10:" <?-oC \1l\f.U'} '1-:

~

2) Subject to Sub-Article (3), where an entity commits

an offence by failing to pay an amount of tax,including an amount treated by this Proclamation asthough it were tax, every person who was a managerof that entity at that time or was a manager within six(6) months prior to the date of commission is jointly

and severally liable with that entity and that otherperson to the Authority for the amount.

3) Sub-Articles (1) and (2) do not apply where(a) the offence is committed without that person's

knowledge or consent; and(b) that person has exercised the degree of care,

diligence and skill that a reasonably prudentperson would have exercised in comparable

circumstances to prevent the commission of theoffence.

4) In Sub-Articles (1) and (2), "manager" means.(a) in the case of a partnership, a partner or manager

of the partnership or a person purporting to actin either of those capacities;

(b) in the case of a company, a director, manager, or

officer of the company or a person purporting toact in any of those capacities; and

(c) in the case of an association of persons, a

manager or a person purporting to act in thatcapacity.

31. Offences by Receivers1) A person who fails to comply with the requirements

of Article 13, Sub-Article (4) commits an offenceand is liable on conviction to a fine of 5,000 Birr andto imprisonment for one (1) year.

2) Where a person is convicted of an offence under

Sub-Article (1) for failing to set aside an amount asrequired under Article 13, Sub-Article (4), the courtmay, in addition to imposing a fine and prison

sentence, order the convicted person to pay to theAuthority, amount not exceeding the amount whichthe person failed t9 set aside.

32. Publication of Names1) The Authority shall from time to time publish by

notice in the Gazette a list of persons who have beenconvicted of offences under any of Articles 22 to 31.

2) Every list published in terms of Sub-Article (1) shall

specify:(a) the name, address, and principal enterprise of

the person;(b) such particulars of the offence as the Authority

may think fit;(c) the tax period or tax periods in which the

offence occurred;(d) the amount or estimated amount of the tax

evaded; and(e) the amount, if any, of the additional tax im-

posed.

1~ gn:1)!: J..1..t./:\ "?~T ?t1tIJ ~1'C 1) :M"'~ 1)1"" liiU?; ,.9".

hif:A flfl:"

A ~ A ~ 1:') ;J1.sP"f

t!}C- fao"'fI OC dlf-o:1"

b- ~u') ~1'~ OP't. ,,~ /\0'/1'/.\ f&..f-ot./.\ 'hCJ'fh/.\A

ao,)"'P':1":r- fI/\P'AIlJ~"f hCJ' mh."";f-Tm. 01'Q;l,

O'/t9" ~'C~"'"f: f<l>O/\. aol\.,-.';~.C':r,: O'/..,Ot.:"lJw~ h:1"h fl. fI/\P' A fl}') ;J C f ao1'fI 0 C ..,f-o:1"~/\flTm.::

I- u) O~"'ll~ <l>mC',,~ I1AIf~ m~lJ" f:1"hfl. 11/\p'Afl}') f"'t.tlao f :1"hl\ aoht.f'UL I1A(}mOl\.,.<I>C: ;l'hl\ h4.~ f"'1.t."..,O:"') ..,-nC

om:"-I: fht./\ l\/\aolf~ m~lJ" ~.ltl\ :1"hl\h4.~') O"'1.ao/\h:" f:1"hl\ h4.~ ao/\f ~1'C

11""'~O Ol\.,.<I>Ct.:f'1: fla\ "'1.~l\'I;C: O'/tI;J'Jf

fl.:": f&..f-ot.A mf.'r fhAA ooP'tf fl.+~.ltl\ f,).., 1: P't. t.:f'1: ao l\m + m~lJ" O'/1.l\~~"fA9"::

/\) f:1"hfl. fI/\P'Afl}') :1"hit h4.~ f/\O:r-') ..,1..:1"l\/\aot.~ap. flJ"l\hc m~<I>+ fO'/~fl1' f1.1f'):

l\/\rtlJw f/\m.1 lJ"h')f:r- OaotlCtlC fl~mtt:/\ mf cf:m. ~fl fl}A II

m) flJ"l\hC m~<I>+~Afl1'9" /\0'//\-1: m~lJ" f1..,1:

P't. t.:f' 1: /\aolP~H- f:1"hf1.fI/\P'Afl}')Oflfl}:fm. lJ"h') f.,."f :"C f 1"fll 0'/');;:m.lJ":1"hl\ h4.~ :"t.:1"m.') /\~fl}t 1'10'/.<1;/\.f<l>C-n~"f"A:I

@i - f"'1. ~ l\ +~ P' A fl}')

0rt U ~ l' ~ /\.fto"f ~ ') <I>"."f h"'1 /\~m. O"'Q;l,O'/ t

"'1.),l\:r-~ /\h. 1'1~ "'1.: /\0'/'"10 t. If m~lJ" /\~ l\1''«;1.ClJ"h') f.,."f m~9" 01fl. ..,-nC ~1'~ ~1'C ~fif?;/j§~,)<I>~ ~I(/\) O"'tI~tI~+ lJ"h')f.,."f flrttJ ~1'~h.,.IlJ/\m. :1"hlahtt:f Ooo-~ m~9" OhkA ~, fO'/1:~'"

P' Afl}') .,. fl1'''' :1"A II.

t!}~- aoaotfsP"f

f1fl.sP"f "'1.~l\:r-C /\rtU ~1'~ ht.,OlJ" f"'1.~~ ODODtfsP"f') /\O'/m.fl}:r- ~"f"AII

t!}?;- fOD"{i;J1tf 1:');J1.f.U ~1'~ hOD{)CJ'-I:.Ok:r- "'~ht.A f<l>~ fh.h"'~1f:1"hl\ 07if"l!"IJ h.h"'~1f :1"hit h1'~ O+1.~11m.ODIP ~:r- f "'1.fl 0 fl-n ~If CJ'A II

t!}~- la/\OD?tC

~U ~tp~ OP't. ,,~ h1'/\O+ 'UL r.lJ"C' f7if"l!"CJ'h.h"'~1f :1"hl\ ~1'~ ~1'C ~:s/IUfif~ /h')f..,.7i7i/\j.,. fl C fl.A II

t!}:s - ~ 1':( f"'1.0CJ'fl:r- 'Lli..

~tJ ~1'~ h:1""''''p'' 3'1 <1>') I!in~ q-lJ" r.lJ"C' fOCJ'

~1fCJ'AI:

~.ltl\ ~Ofl :1"1UfP' 3'1<1>')Iun~ q-lJ"

"'e"? m/1.f"C1.l\

fh.:r-f"kf L1..t-"'C ~""ht.f1.flf tT-n/\.h,.t.rt~'):r-

Federal Negarit Gazeta - No. 20 31SI December, 2002-Page 2023

SECTION 7Miscellaneous Provisions

33. Duty to Cooperate1) All Federal and Regional Government Authorties

and their Agencies. Bodies, Kebele Administrationsand Associations shall have the duty to cooperatewith the Tax Authority in the enforcement QfthisProclamation.

2) (a) no Ministry, Municipality, Department or Of-fice of Federal or Regional Government shallissue or renew any license ~any taxpayerunless the applicant produces a certificate fromthe Tax Authority to the effect that tax due inrespect of the preceding year or years, havebeen paid or where the taxpayer is seekinglicense for the first time taxpayer identificationnumber (TIN) issued by the Tax Authorityunless appeal is pending, or time for payment isextended by the Tax Authority,

(b) If the Tax Authority refuses to issue a ce'rtificateit shall, on demand by the applicant for thelicense, provide him or it with a writtenstatement of its reasons therefore.

(c) Any applicant who is aggrieved by the reasonsstated by the Tax Authority for refusing to issuea certificate or by the revocation of his or itslicense may appeal in writing to the ReviewCommitte.

34. Powers of the MinisterThe Minister may wai ve in whole or in part, the tax leviedunder this Proclamation for Economic, Social or ad-ministrative reasons or for reasons specified underArticrle 42 (b) of the Income Tax Proclamation No. 286/2002.

35. DirectivesThe Minister of Revenue may issue directives for theproper implementation ofthis Proclamation.

36. Transitory ProvisionsAI) Excise Tax due prior to the coming inFo force of thisProclamation shall be paid in accordance .with the Salesand Excise Tax Proclamation. .

37. RepealsThe Sales and Excise Tax Proclamation No. 68/1993 (asamended) shall be rescinded as from the day on whichthis Proclamation becomes effective.

38. Effective DateThis Proclamation shall enter into for.ce as of the 31" dayof December, 2002. .

Done at Addis Ababa, this 31s1day of December, 2002.

GIRMA W/GIORGIS

PRESIDENT OF THE FEDERALDEMOCRATIC REPUBLIC OF ETHIOPIA

.,,,. Iif.~r (0) IJ.6-A ~:JtT ?tLlIJ 4t'l'C~ :M"I'" ~I +'J Iif7~ '}.\I". Federal Negarit Gazeta - No. 20 31"December,2002-Page 2023(A)

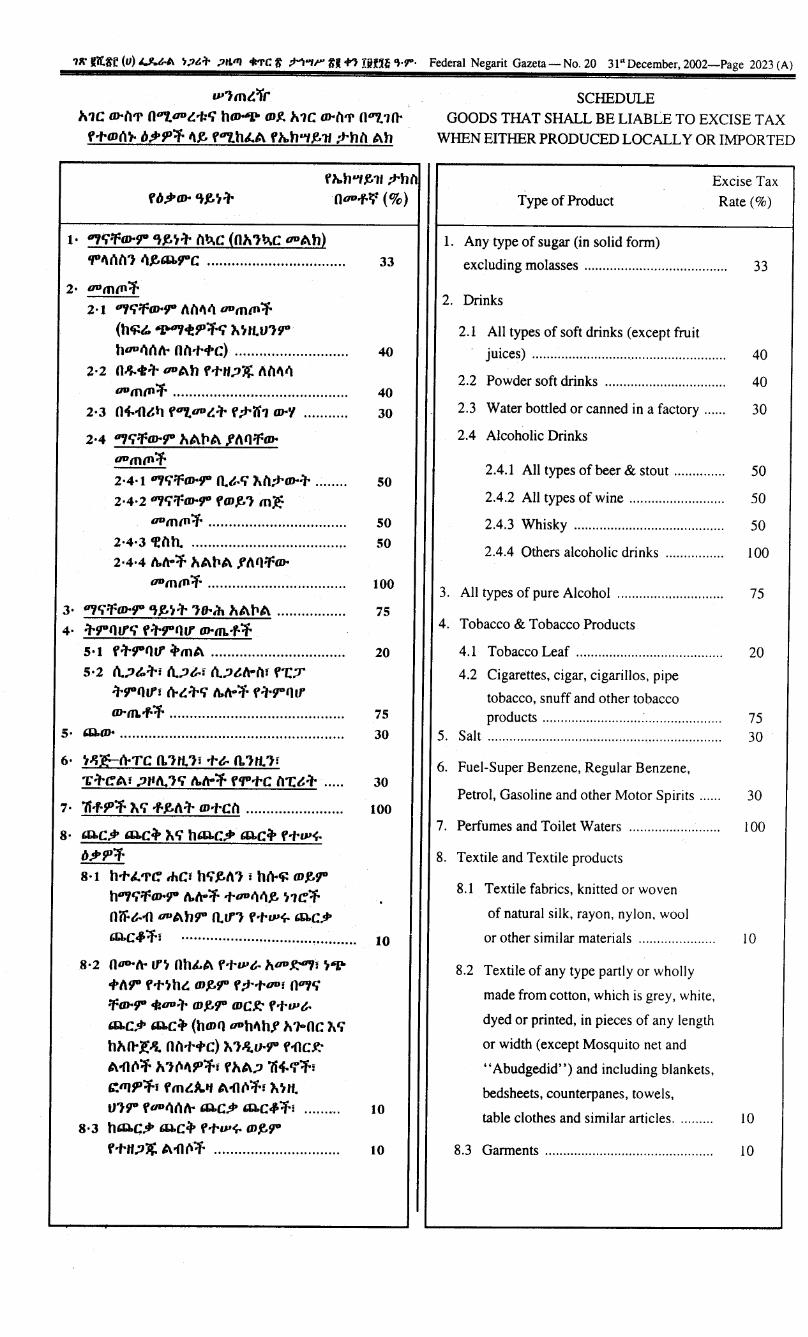

lP'mtv

"1C lD-it1' 0"7.00~i:CJ' h~ mY. "1C lD-it1' 0D?1l1-f.,.m",)' iJ:J'91'f ,,1. f"7.h~A fA.h"~lI ;l'hit Ah

fiJ:J'lD-,1.H',A. tJ., .f, 11 :J'tJ it

Ooo.,.~ (%)

l' "'I'itflD-1}"'~~T itl).C (O"'I).C ooAh~",,,...it, ".e,t;Q.I}"C..................................

2. oomtn'f

2' 1 "'ICJ'tflD-1}"" it""

00 m tn 'f

(hft:&. "f.W'7<t9''fCJ' h ~If. 0'1}"

hoo"",,,, Oit.,..,.C) ............................

2'2 O~ctT ooAh f.,.n;Jjf. "it""00 mtn 'f ...........................................

2'3 04-1MtJ ,oy"oo~T ';l'if1lD-'/ ...........

2.4 "'ICJ'TlD-1}""At'1A '''t}tflD-

oomtn'f

2.4'1 "'ICJ'tflD-1}"0.&.CJ'hit;l'lD-T ........

2'4.2 "'ICJ'tflD-1}"'OJ~' m~oomtn'f ......................

2 ,4, 3 If it h. ......................................

2.4.4 lbfro'f "At'1A '''t}:flD-oomtn'f ..................................

3, "'ICJ'tflD-I}'" ~ ~T ,,,. ih "A t'1A .. .. .. . .. .. ..4. Tl}"t}lJ'CJ'fTl}"t}lI" lD-m."''f

5'1 'Tl}"t}lI" :"mA .................................5.2 f1.;J&'T: f1.;J&.= f1.;J~froit: f1;;T

Tl}"t}lI":~~TCJ'~fro'f'Tl}"t}lI"

lD-m."''f ...........................................5. t;Q.lD ......................................

6, ~.c;~~TC 0.'If. ,: .,.&.0.")If.,:1:T~A: ;JJfA.'CJ' lbfro'f ,"''''c it1;~T .....

7. 1i.f9''f hCJ'"'1."T m.,.Cit ........................

8. t;Q.C:J' t;Q.C:" hCJ'ht;Q.c:J' t;Q.C:" f"'lP~

iJ:J'9''f

8'1 h"'~1'C" thC: hCJ'.e,,,, : h~ft: m~1}"h"'lCJ'tflD-1}"~fro'f .,.oo,,"~ ~1~'f

0if.&.11 OUAhl}" 0.11"")''''IP~ t;Q.C:J't;Q.c~ 'f:

"""""'''''''''''''''' "........

8.2 000-'" II"~ OhkA ''''IP&' "ooY:"'l: ~~.,." I}" ,.,. ~h ~ OJ~I}" ';l''''oo: O"'le.'tflD-1}" cflooT m~1}" mc!: ''''IP&'t;Q.C:J' t;Q.C:" (hmt) ooh"hl ".,..OC 'he.'

h"l1-;()lOit.,..,.C) 'h"))lV-1}" '11C!:

A11(e'f "'(e"91'f: f"A;J 1i4-tj'f:

C:tlJ91'fi fm~A.1f A11(e'f: h~lf.

0'1}" foo,,"'''' t;Q.C:J' t;Q.C~'fi ,..8,3 ht;Q.c:J' t;Q.C:" ''''IP~ m.f,1}"

f.,.n;Jjf. A11(e'f ...............................

33

40

40

30

50

50

50

100

75

20

75

30

30

100

10

10

10

SCHEDULE

GOODS THAT SHALL BE LIABLE TO EXCISE TAX

WHEN EITHER PRODUCED LOCALLY OR IMPORTED

Type of ProductExcise Tax

Rate (%)

1. Any type of sugar (in solid form)

excluding molasses .....

2. Drinks

2.1 All types of soft drinks (except fruit

juices) , """"""'" """"""'"

2.2 Powder soft drinks .................................

2.3 Water bottled or canned in a factory......

2.4 Alcoholic Drinks

2.4.1 All types of beer & stout ..............

2.4.2 All types of wine ...~......................

2.4.3 Whisky ......................

2.4.4 Others alcoholic drinks ................

3. All types of pure Alcohol.............................

4. Tobacco & Tobacco Products

4.1 Tobacco Leaf ........................................

4.2 Cigarettes, cigar, cigarillos, pipe

tobacco, snuff and other tobacco

products """"'" ....

5. Salt """"''''''''''''''''''''''''''''''''''''''''''''''''

6. Fuel-Super Benzene, Regular Benzene,

Petrol, Gasoline and other Motor Spirits ......

7. Perfumes and Toilet Waters .........................

8. Textile and Textile products

8.1 Textilefabrics, knitted or woven

of natural silk, rayon, nylon, wool

or other similar materials .....................

8.2 Textile of any type partly or wholly

made from cotton, which is grey, white,

dyed or printed, in pieces of any length

or width (except Mosquito net and

"Abudgedid") and including blankets,

bedsheets, counterpanes, towels,

table clothes and similar articles. .........

8.3 Garments """"''''''''''''''''''''''''''''''

33

40

40

30

50

50

50

100

75

20

7530

30

100

10

10

10

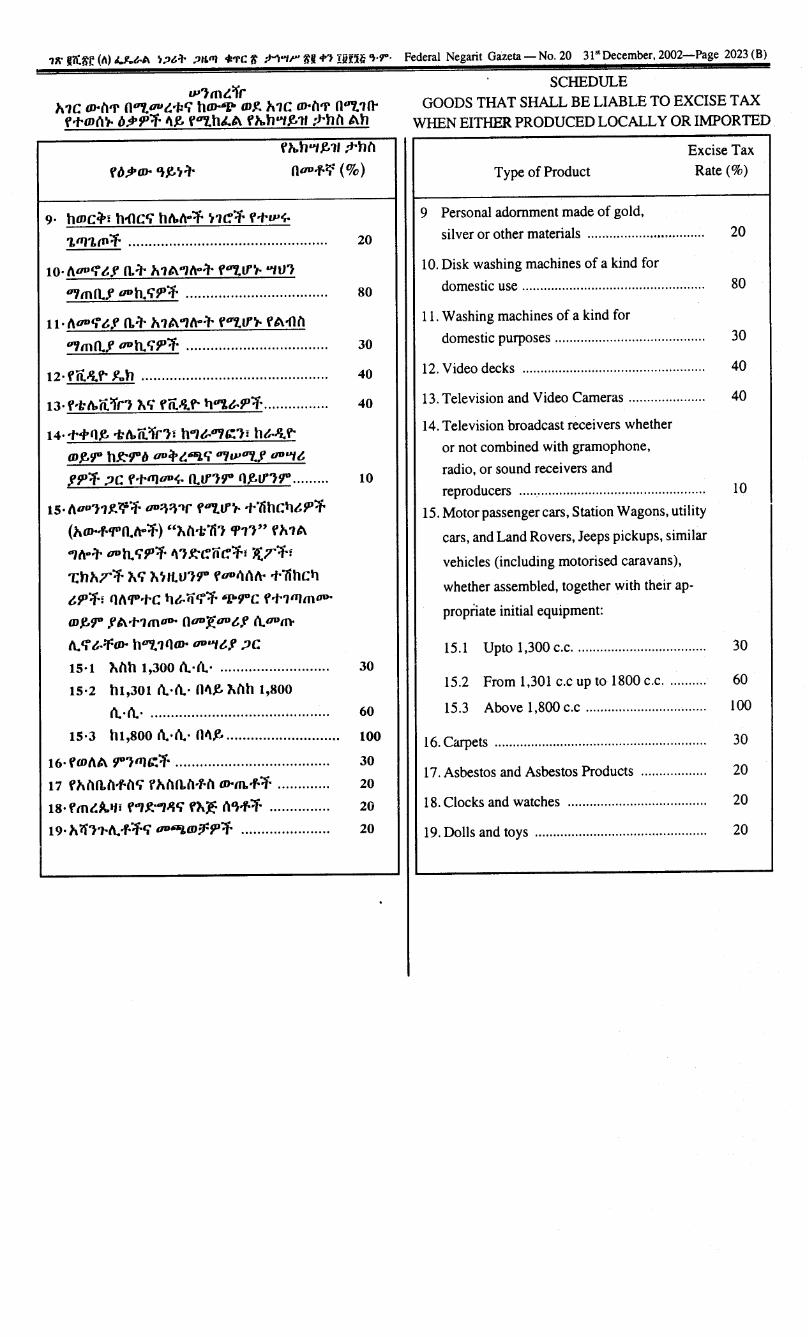

1Jt !lif.1)~ (1\) .u..t.~ ~:>t:" :>/1,11)4I1'C 1) ;M"tP' 1)1 4") Xitl]?; 'H'" Federal Negarit Gazeta - No.20 31It December, 2002-Page 2023 (8)

1P11O~1rh 1C CD-il'l' 0117.{/II~ -f:'i" hCD-"1'"mY. h 1C CD-il'l' 0117.10-

fTml't.,. b:l',,"f I\y. fDthLA f11.h"'Y.lI :J"hil Ah

fh.h..,Y.lI :J"hil

ooo.y.~ (%)f b:l' CD- ~ Y.., ..,.

9, hmc:": h1lC'i" hlt./r'"f ""C-"f fTIP<;'

1.lfJ1.(1\"f .................................................

10. "ootj ~f 0."" h1A..,/r''''' fDtIf.,. ..,01

OI/mo.f ooh. 'i",,"f ...................................

11. "ootj ~f 0."" h 1A.., /r''''' fD7..lf.,. fA 11il

01/ mo.f 00 h. 'i",,"f ...................................

12.fiiJlf" ~h ..............................................

13. f*l:lt.ii1f1 "h'i"fiiJlf" t}1P1t.,,"f................

14. T'"qy. *I:It.ii1r1: h.., t.0I/ G:1: h t-Jl f"

my.1}" h.('l}",) 00:"~65L'i" OI/IPDtf oo..,~

f,,"f ;JC fTlfJoo<;, 0.11'19" qY.1f19".........

15. "oo11Y.?f'"f 00=\=\"'- fDtIf.,. T1ihCt}~""f

(hCD-.y.'l"o./r'"f) ""hil-t1i1 '1'11" fh1A

..,,, ,. ooh.'i",,"f 1\1.('c-iic-"f: j{T"f:

1:hhT"f "h'i""h"IL019" fool}l'tft- .,.1ihCt}

~ ,,"f: q" 'l" TC t}t. Ii tj"f "1'"9"C f T.,lfJ m 00-

my.9" fAT.,moo- ooo]!oo~f fLoom

l\.tj t.TCD- hOlJ..1 q CD-00'" ~f ;JC

15'1 "hilh 1,300 fl ......................

15.2 hl,301 fL.fL. Ol\y. "hilh 1,800

fl. fl. ............................................

15. 3 h 1,800 fl. fl. Ol\y... .............

16' f(JJ"A 9"1lfJG:"f ......................................

17 fhilll.il.y.il'i" fhilll.il.,.il CD-m..y."f .............

18. fm~A.If: f"'.(''''~'i'' f"h~ I't~.y."f ...............

19. h i'f11-l\. .y."f'i" ooftl,tD;F,,"f ......................

20

80

30

40

40

10

30

60

100

30

20

20

20

SCHEDULE

GOODS THAT SHALL BE LIABLE TO EXCISE TAX

WHEN EITHER PRODUCED LOCALLY OR IMPORTED

Type of Product

9 Personal adornment made of gold,

silver or other materials ,..........

10. Disk washing machines of a kind for

domestic use..................................................

11. Washing machines of a kind for

domestic purposes.. .......................................

12. Video decks ..................................................

13. Television and Video Cameras .....................

14. Television broadcast receivers whether

or not combined with gramophone,

radio, or sound receivers and

reproducers , .

15. Motor passenger cars, Station Wagons, utility

cars, and Land Rovers, Jeeps pickups, similar

vehicles (including motorised caravans),

whether assembled, together with their ap-

propnate initial equipment:

15.1 Upto 1,300 C.c. ...................................