Evolving Private Label Strategies, Consumer Choices and ... · by Morrisons, Walmart,Tesco, Ahold,...

4

© Copyright Canadean, 2013 This product is licensed and is not to be photocopied Evolving Private Label Strategies, Consumer Choices and the future impact on Food Brands & Private Labels – Sample Pages Reference Code: CS0595IS Publication Date: October 2013

Transcript of Evolving Private Label Strategies, Consumer Choices and ... · by Morrisons, Walmart,Tesco, Ahold,...

© Copyright Canadean, 2013 This product is licensed and is not to be photocopied

Evolving Private Label Strategies, Consumer Choices and the

future impact on Food Brands & Private Labels – Sample Pages

Reference Code: CS0595IS

Publication Date: October 2013

© Copyright Canadean, 2013 This product is licensed and is not to be photocopied 2

Canadean has identified fifteen countries that can be classified as “hot-spots”

for future overall private label growth

Future hotspots – key countries where private labels are underdeveloped in penetration and/or sophistication and where

multinational retailer interest will drive growth

Source: Canadean, 2013

Europe: increased

penetration in

Eastern Europe, and

more sophisticated

and diversified PL

Asia: promoting

added value,

building retailer

equity, and moving

consumers away

from the brands

they continue to

trust

Latin America:

Casino, Carrefour,

Walmart, and

Cencosud fight for

leadership, which

will see a key focus

on price credentials

Future hotspots:

Europe: Poland, Hungary, Romania, Bulgaria,

Czech Republic, Russia, Turkey, Ukraine

Asia: India, China, Thailand, Malaysia, South

Korea

Latin America: Argentina, Brazil

© Copyright Canadean, 2013 This product is licensed and is not to be photocopied 3

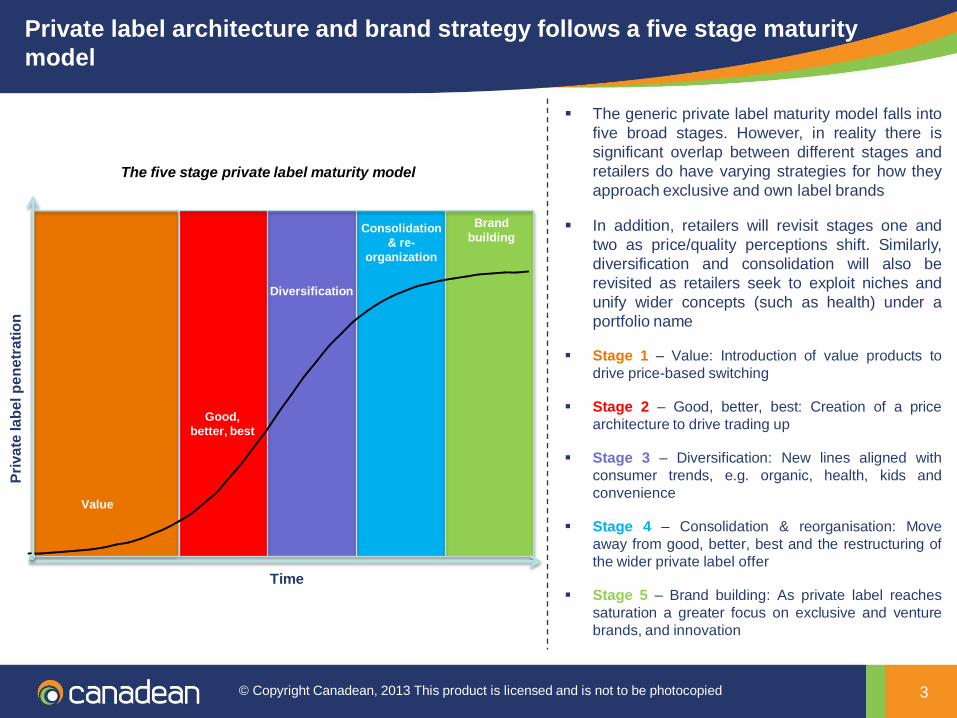

Private label architecture and brand strategy follows a five stage maturity

model

The five stage private label maturity model

Value

Good,

better, best

Diversification

Consolidation

& re-

organization

Brand

building

Time

Pri

va

te la

be

l p

en

etr

ati

on

The generic private label maturity model falls into

five broad stages. However, in reality there is

significant overlap between different stages and

retailers do have varying strategies for how they

approach exclusive and own label brands

In addition, retailers will revisit stages one and

two as price/quality perceptions shift. Similarly,

diversification and consolidation will also be

revisited as retailers seek to exploit niches and

unify wider concepts (such as health) under a

portfolio name

Stage 1 – Value: Introduction of value products to

drive price-based switching

Stage 2 – Good, better, best: Creation of a price

architecture to drive trading up

Stage 3 – Diversification: New lines aligned with

consumer trends, e.g. organic, health, kids and

convenience

Stage 4 – Consolidation & reorganisation: Move

away from good, better, best and the restructuring of

the wider private label offer

Stage 5 – Brand building: As private label reaches

saturation a greater focus on exclusive and venture

brands, and innovation

© Copyright Canadean, 2013 This product is licensed and is not to be photocopied 4

A growing trend among a large number of retailers

in developed countries is to revisit the brand image

of products right across the price spectrum.

One of the best examples is Morrisons’ redesign

and rebranding of its ‘Value’ range to ‘M Savers’ in

December 2011.

At the premium end of private label, most retailers

have followed the lead set by Tesco’s ‘Finest’ and

opted for muted colors, and small or minimal use of

the retail brand.

Sweden’s ICA is the retailer taking the boldest

moves in giving each of its private label ranges a

distinct brand identity. Its core range is designed

for simplicity rather than a specific brand

personality – in contrast to the approaches taken

by Morrisons, Walmart, Tesco, Ahold, and others.

However, its ‘I ❤ Eco’, ‘Skona’, ‘Selection’, and

‘Gott Liv’ ranges have all been designed to convey

a sense of fun and brand personality that is unique

to the retailer. The ICA approach is still relatively

unusual within private labels – most retailers still

prefer the approach of keeping branding quite

conservative outside their core and best ranges.

ICA is essentially selling ‘natural’ ‘environmentally

friendly’, ‘high quality’, and ‘healthy’ as

complementary lifestyles – an interesting

approach.

Morrisons – redesign of its ‘Value’ range in the rebranding to ‘M

Savers’

ICA –attractive brand identities for its natural (I ❤ Eco), environmentally

friendly (Skona), best (Selection) and healthy (Gott Liv) ranges

Private label growth: value can be added by developing a cross-category

private label brand image