Evolution of Service Provider Markets in Europe - EITO · Communication Service Provider Markets in...

18

Communication Service Provider Markets in Europe Marta Munoz Research Director EMEA Telecommunications & Networking

Transcript of Evolution of Service Provider Markets in Europe - EITO · Communication Service Provider Markets in...

Communication Service Provider Markets in Europe

Marta Munoz

Research Director

EMEA Telecommunications & Networking

Agenda

The evolving ICT industry and Telcos

European telecom market realities

Evolution of the consumer

Helping the European enterprise

Essential guidance

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 2

The ICT Industry's 3rd Platform

© IDC Visit us at IDC.com and follow us on Twitter: @IDC Source: IDC

Every 20-25 years, ICT goes through a

period of “creative destruction” - the old

industry model is replaced with a new

platform for growth and innovation.

Last time around, the early 1990s,

Client/Server, Lans and the Web replaced

mainframes & dumb terminals as the

model.

This time around, the “3rd Platform” is the

new model. It’s built on the “Four Pillars”

(Mobility, Cloud services, Big

Data/analytics, and social technologies)

and on others including machine-to-

machine (M2M), aka the “Internet of things”

(IoT).

From 2013-2020, 90% of IT industry

growth and 40% of all revenue will be

driven by 3rd Platform technologies.

This will create a “mass extinction event”

that will wipe out many established

technologies, services and players - just

as Client/Server and the Web did in the

1990s.

Millions of Users Thousands of Apps

Hundreds of

Millions of Users

Tens of

Thousands of

Apps

Billions of Users Millions of Apps

IDC’s research revolves around what we

define as the 3rd platform for ICT industry

3

Evolving Telecom Ecosystem

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 4

West European Connectivity Markets

0

50

100

150

200

250

2012 2013 2014 2015 2016 2017

Spending on Connectivity Services (€B)

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 5

Legacy Source: IDC European Telecom

Services Database, 4Q2013

CAGR

12-17

3% Mobile Data

Mobile Voice

Fixed Data

Fixed Voice

-5%

-5%

1%

Overall CAGR 12-17 is -2%

Mobile Data: • Messaging (-6%)

• Data over Mobile (10%)

Mobile Voice covers spending and not Revenues

Fixed Data: • Legacy (-22%)

• Internet Access (2%)

• IP-VPN (-1%)

• Ethernet (11%)

Fixed Voice: • TDM (-10%)

• IP (10%)

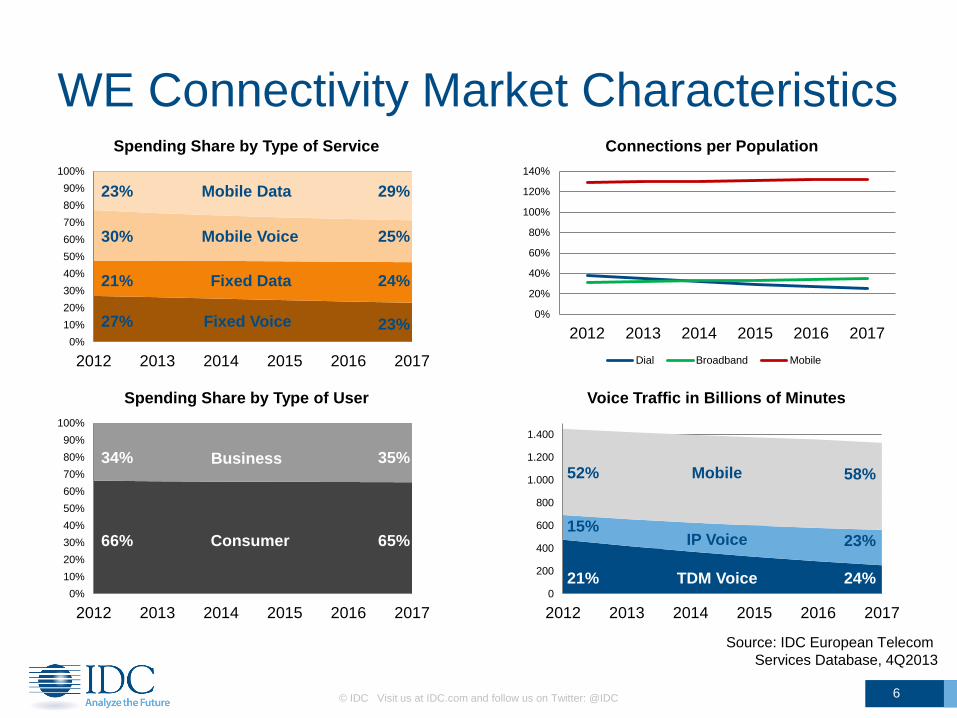

WE Connectivity Market Characteristics

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 2015 2016 2017

Spending Share by Type of Service

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 6

0%

20%

40%

60%

80%

100%

120%

140%

2012 2013 2014 2015 2016 2017

Connections per Population

Dial Broadband Mobile

Legacy

Growth

Source: IDC European Telecom

Services Database, 4Q2013

Mobile Data

Mobile Voice

Fixed Data

Fixed Voice 27%

29% 23%

25% 30%

24% 21%

23%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 2015 2016 2017

Spending Share by Type of User

Business

Consumer

35% 34%

65% 66%

0

200

400

600

800

1.000

1.200

1.400

2012 2013 2014 2015 2016 2017

Voice Traffic in Billions of Minutes

TDM Voice 24% 21%

IP Voice 23% 15%

Mobile 58% 52%

WE Telco Portfolio Evolution

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 7

Legacy

Growth

Unified

Communications

Conferencing

Solutions &

Services Network

Infrastructure

Network Lifecycle

Services

Datacenter &

Cloud Services

Security Services

Mobility Software

Enterprise

Mobility Services

Internet of Things Consumer

Content

Telcos

Expanding

Into

Associated

Markets

Fixed and Mobile Broadband Penetration in WE in 2013

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 8

DE

FR

GB

IT

ES

NL

CH

BE

GR

PT

AT

SE

DK

NO

FI

Fix

ed

Bro

ad

ba

nd

Pe

netr

ati

on

Mobile Broadband Penetration

Average for WE is 32%

Average for WE is 62% Source: IDC European Telecom Services Database, 4Q2013

Size of

bubble

represents

total FBB

and MBB

users

Fixed and Mobile Broadband Penetration in WE in 2017

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 9

DE

FR

GB

IT

ES

NL

CH

BE

GR

PT

AT

SE

DK

NO

FI

Fix

ed

Bro

ad

ba

nd

Pe

netr

ati

on

Mobile Broadband Penetration

Average for WE is 35%

Average for WE is 81% Source: IDC European Telecom Services Database, 4Q2013

Size of

bubble

represents

total FBB

and MBB

users

Some Key Industry Themes (1)

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 10

Tension between operators and regulators remains a prominent

theme.

Operators want:

"investment-friendly" policies

on consolidation, network

sharing, net neutrality, and

regulated prices

Regulators want:

cheaper prices, better

networks, unrestricted use of

the Internet, and a single

European market

Some Key Industry Themes (2)

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 11

Operators look to reduce network and device costs.

The trend toward network

sharing continues during

2012 and 2013.

Operators try to move away

from handset subsidy and

bundling.

IPTV providers investigate

move to cloud-based STB

functionality.

Some Key Industry Themes (3)

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 12

M&A gathers pace: some

consolidation, some

diversification.

France Telecom/Sonaecom

Telefónica/Hispasat

Liberty Global/Virgin Media, Ziggo,

and Telenet

Sky/O2 U.K. Broadband

Deutsche Telekom/MetroPCS

Hutchison/O2 Ireland

Vodafone/Kabel Deutschland

Telecom Italia fixed-line spinoff

European Enterprises want QoS

13

n=1,822 (all companies)

Q42. When selecting a network service provider, which are the most important

factors in making a decision?

Significant increase in

importance of quality

compared to previous year.

Price remains important factor

Core service attributes are

key decision factors

Source: IDC EMEA WAN Manager Survey, 2013

1%

21%

31%

33%

35%

39%

44%

45%

64%

66%

-25% 0% 25% 50% 75%

Other(Please Specify)

Cloud service strategy

Vertical/ industry expertise

A broad service portfolio

The ability to provide mobile and…

Geographical coverage

Contract flexibility

Technology innovation

Pricing

Quality of service and support

Enterprise Data Services

Competitive landscape

14

target company size

Domestic incumbents e.g. DT, BT, Orange,Telefónica

Domestic challengers e.g. SFR, VM B, Vodafone DE

Mass market

players e.g. cable ops

Domestic

Business SPs e.g. Completel, QSC

Global Carriers e.g. BT GS, VES,

AT&T, etc.

Regional operators e.g. Colt, Easynet, Interoute

bre

ad

th o

f p

ort

folio

• Landscape can be very different per

segment or country

• Markets typically dominated by

domestic incumbent

• Many operators aim to be provider of

“solutions” instead of just connectivity

• Operators expand target markets, e.g.: • Cable operators try to address beyond

very small business

• VES addresses sizes below its

traditional market

• C&W acquisition has substantially

strengthened Vodafone’s position in the

BNS space

Global carriers (e.g., OBS, AT&T, BTGS,

Verizon)

Equipment vendors

(e.g., Cisco, Avaya, Microsoft, Broadsoft)

Target company size

Domestic incumbents (e.g., DT, BT, Orange,Telefónica)

Regional operators (e.g., Colt, Level3)

Domestic challengers (e.g., SFR, Vodafone DE,

VoiceFlex)

Bre

adth

of port

folio

Enterprise Voice Services

Competitive Landscape

15

Landscape can be very different per segment or

country.

Markets are typically dominated by domestic

incumbent.

Many operators aim to be providers of "solutions"

instead of just services.

Operators expand target markets, for example Cable operators try to address beyond very

small business

Global carriers address sizes below their

traditional market

VoIP

TDM

2011/12 “Consumerization”

2013+ “Mobile First”?

iOS + Blackberry Silos

Executive Jewellery

BYO Device

Experimental Apps

(mainly B2C)

IT Night Job

Risk Management

Point Solutions

Fluid, Multi-OS

>50% of employees

BYO Tools

Widespread Apps

(B2E/B + 2nd Gen B2C)

Dedicated Mobile IT & CoEs

Business Enablement

Platform Architecture

Source: IDC Mobile Enterprise Strategies

Firms Now Entering Next Phase of

Enterprise Mobility

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 16

IT Players Targeting the MEM Opportunity

17

Through which channel would you consider purchasing a

mobile enterprise solution as a trusted partner?

Source: IDC Enterprise Mobility Survey, July 2013 | N = 375

0% 10% 20% 30% 40% 50%

Mobility Implementation Specialist

Mobility Software vendor

IT Value Added Reseller (VAR)

ICT Carrier or Fixed Telecom Provider

Mobile operator

Systems Integrator

#1 choice for

the first time in

the Summer

2013 survey

Essential Guidance

© IDC Visit us at IDC.com and follow us on Twitter: @IDC 18

In the mass market Telcos need to:

Invest in NGA and ensure it pays

off

Leverage the power of the

bundle

Position to exploit the mass-

market megatrends

Adapt to the bigger and more

diverse competitive landscape

In the enterprise market Telcos must

Help clients with cost

optimisation and innovation

Focus on service quality

Move more aggressively in

offering VoIP solutions

Become more technology

agnostic around the WAN

Sell solutions but don’t neglect

the connectivity element

The Telecom Market is

still a large and

dynamic market