Evolu’on!of!the!Auto!Industry!! in!Mexico -...

63

Evolu’on of the Auto Industry in Mexico Jorge Carrillo [email protected] h;p://colef.net/ApWpJCarrillo/presentacion 1 GERPISA Journée du Gerpisa 199 11 Jan 2013 14:00 – 17:00 La Défense, Tour Voltaire, Paris

-

Upload

vuongkhanh -

Category

Documents

-

view

216 -

download

0

Transcript of Evolu’on!of!the!Auto!Industry!! in!Mexico -...

Evolu'on of the Auto Industry in Mexico

Jorge Carrillo

h;p://colef.net/ApWp-‐JCarrillo/presentacion

1

GERPISA Journée du Gerpisa 199 11 Jan 2013 14:00 – 17:00

La Défense, Tour Voltaire, Paris

Content How important is the auto industry in Mexico? How the auto industry is structured in Mexico? How the industry is integrated in Mexico? What kind of employment relationships exists in Mexico?

1

How important is the auto

industry in Mexico?

Economy 13th place.

8th Worldwide Producer (2011) 3 LV out of 100 world wide are assembled in Mexico 1 out of 4 vehicles sales in USA are assembled in Mexico 28 Billion dlls US imports comes from Mexico (# 1) 25% of US auto industry purchases comes from Mexico (2011) 2nd USA Trade Partner

MEXICO AUTO INDUSTRY. SOME EVIDENCE

Source: Banxico, INA

2008 2009 2010 2011 2012* 2013* 2014* Real GDP (%) 1.2 -‐6.0 5.5 3.9 3.8 3.6 3.1

GDP per cápita

$10,070 $8,001 $9,221 $10,105 $10,172 $10,694 $10,965

NAFTA: Vehicle production (%)

Sources: Automotive News; Market Data Yearbook; Statistics Canada; AMIA, OICA, Mexico Now-

- PERIPHERICAL MODEL (GERPISA) BUT DYNAMIC

Year

U.S.A. CANADA MEXICO % Total

1970 9,663 85.7 12.3 2.0 100 1980 9,869 81.2 13.9 5.0 100 1990 12,551 77.9 15.5 6.5 100 2000 17,699 72.6 16.7 10.7 100 2011 20,164 72.4 14.6 13.0 100 2016 16,731 68.8 10.6 20.6 100

Coahuila

New geography, 2007-08

Sources; Banxico, INA

- 2.9 millions vehicles produced in 2012 - 17% of Mexico’s GDP manufacture (2011) - 20% of total Mexican manufacture exports (2010) - 34.5 Billions of dlls. of foreign exchange (2012) 29% higher than petroleum;

184% than tourism - FDI –OEMs : 15 billion US dlls (2006-2012)

- Exports to more than 100 countries - 90 of the Top Best 100 global players are located in Mexico

Auto Industry. Mexico´s General Impact

Mexico General View Auto Industry: Long tradi'on started in 1925. ISI period 60´s & 70s, 80’S huge restructuring. Export plaXorm –vehicles and parts-‐ North-‐South convergence process 1994 NAFTA 2001 & 2009 important crisis (rapid recovery) 53% SALES W/FINANCE (55% FROM DEALERS). 47% SALES CASH

(JanOct 2012) 2010 and on. Very Important increase:

12% growth of LV in 2011-‐2012 8

2

HOW THE AUTO INDUSTRY IS STRUCTURED IN MEXICO?

10

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

2000 2004 2009 2011 2012 (Jan-‐Oct)

67.7%

59.9%

67.0% 67.4%

63.2%

31.7%

39.9%

33.0% 32.6% 36.8%

Produc'on by segments (% of Total)

Automoviles Camiones Ligeros Camiones Pesados

Sources: Author elaboration based on AMIA data base

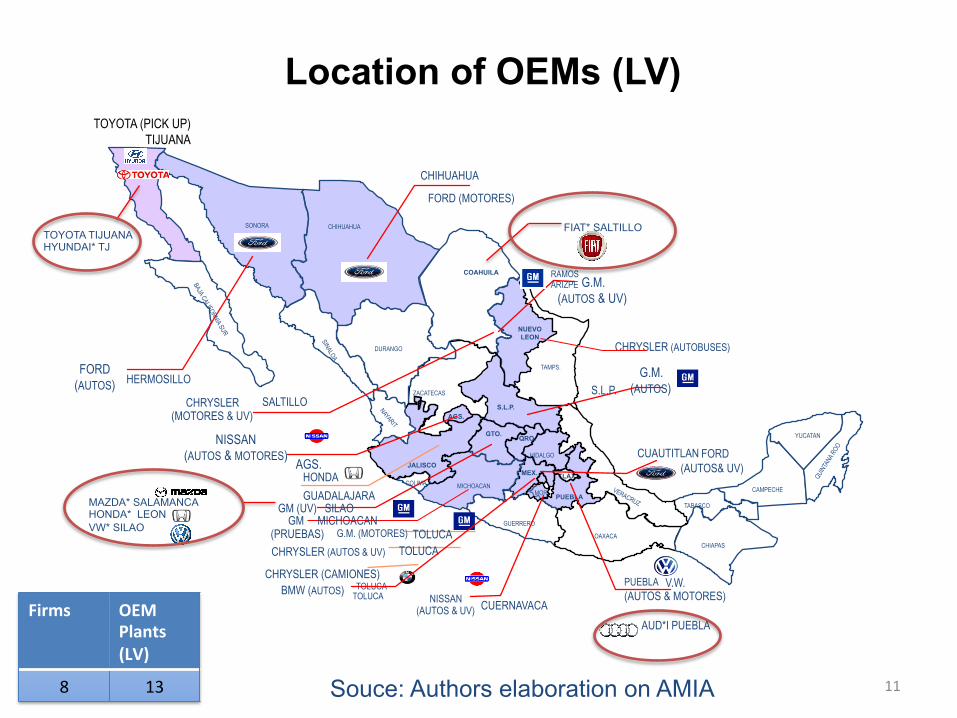

11

AGS.

TLAX. MEX.

PUEBLA

QRO.

COAHUILA

HERMOSILLO FORD

(AUTOS) SALTILLO CHRYSLER

(MOTORES & UV)

NISSAN (AUTOS & MOTORES)

GTO.

GM (UV)

CHRYSLER (CAMIONES)

SILAO

AGS.

V.W. (AUTOS & MOTORES)

AUD*I PUEBLA

PUEBLA

HONDA GUADALAJARA

SONORA

FORD (MOTORES)

CHIHUAHUA

MOR.

NISSAN (AUTOS & UV) CUERNAVACA

DURANGO

ZACATECAS

S.L.P.

TAMPS.

COLIMA MICHOACAN

GUERRERO

OAXACA CHIAPAS

TABASCO

CAMPECHE

YUCATAN

HIDALGO

NUEVO LEON

RAMOS ARIZPE G.M.

(AUTOS & UV)

TOLUCA G.M. (MOTORES) TOLUCA CHRYSLER (AUTOS & UV)

TOLUCA BMW (AUTOS)

CUAUTITLAN FORD (AUTOS& UV)

CHIHUAHUA

TOLUCA

S.L.P.

JALISCO

G.M. (AUTOS)

GM (PRUEBAS)

MICHOACAN

CHRYSLER (AUTOBUSES)

TOYOTA (PICK UP) TIJUANA

Location of OEMs (LV)

Souce: Authors elaboration on AMIA

FIAT* SALTILLO TOYOTA TIJUANA HYUNDAI* TJ

MAZDA* SALAMANCA HONDA* LEON VW* SILAO

Firms OEM Plants (LV)

8 13

AGS.

TLAX.

QRO.

COAHUILA

GTO.

SONORA CHIHUAHUA

MOR.

DURANGO

ZACATECAS S.L.P.

TAMPS.

COLIMA MICHOACAN

GUERRERO OAXACA

CHIAPAS

TABASCO CAMPECHE

YUCATAN HIDALGO

MEX.

PUEBLA

NUEVO LEON

JALISCO

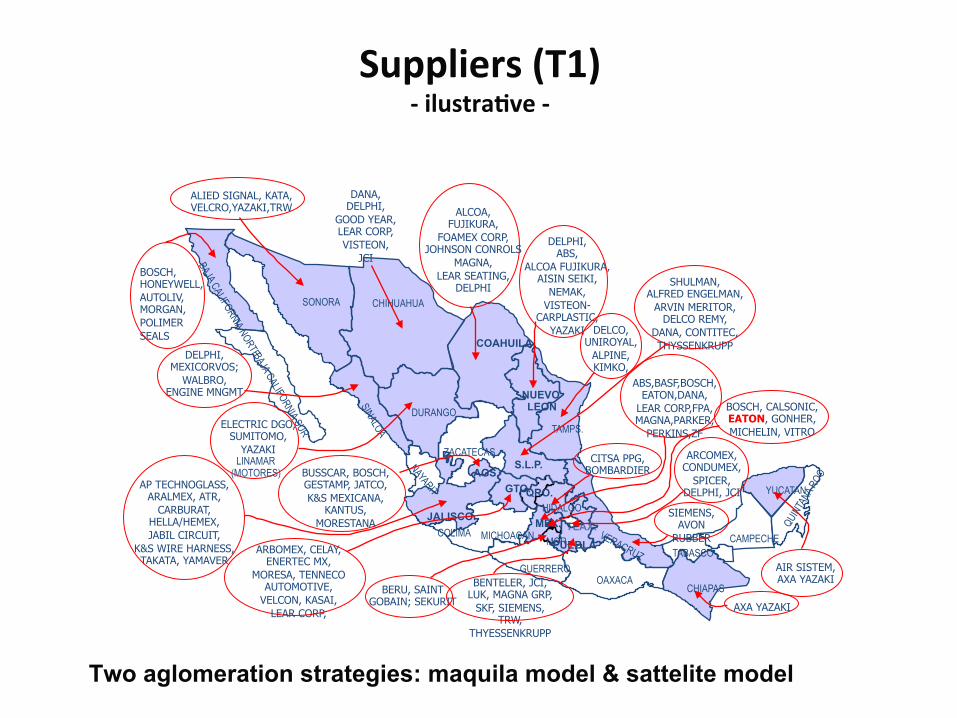

BOSCH, HONEYWELL, AUTOLIV, MORGAN, POLIMER SEALS

ALIED SIGNAL, KATA, VELCRO,YAZAKI,TRW

DANA, DELPHI,

GOOD YEAR, LEAR CORP, VISTEON,

JCI

ALCOA, FUJIKURA,

FOAMEX CORP, JOHNSON CONROLS

MAGNA, LEAR SEATING,

DELPHI

DELPHI, ABS,

ALCOA FUJIKURA, AISIN SEIKI,

NEMAK, VISTEON-

CARPLASTIC, YAZAKI DELCO,

UNIROYAL, ALPINE, KIMKO,

SIEMENS, AVON

RUBBER

AIR SISTEM, AXA YAZAKI

CITSA PPG, BOMBARDIER

DELPHI, MEXICORVOS;

WALBRO, ENGINE MNGMT

ELECTRIC DGO, SUMITOMO,

YAZAKI

BUSSCAR, BOSCH, GESTAMP, JATCO, K&S MEXICANA,

KANTUS, MORESTANA

SHULMAN, ALFRED ENGELMAN,

ARVIN MERITOR, DELCO REMY,

DANA, CONTITEC, THYSSENKRUPP

AP TECHNOGLASS, ARALMEX, ATR,

CARBURAT, HELLA/HEMEX, JABIL CIRCUIT,

K&S WIRE HARNESS, TAKATA, YAMAVER

ARBOMEX, CELAY, ENERTEC MX,

MORESA, TENNECO AUTOMOTIVE,

VELCON, KASAI, LEAR CORP,

ARCOMEX, CONDUMEX,

SPICER, DELPHI, JCI

BERU, SAINT GOBAIN; SEKURIT

BENTELER, JCI, LUK, MAGNA GRP,

SKF, SIEMENS, TRW,

THYESSENKRUPP

AXA YAZAKI

BOSCH, CALSONIC, EATON, GONHER, MICHELIN, VITRO

ABS,BASF,BOSCH, EATON,DANA,

LEAR CORP,FPA, MAGNA,PARKER,

PERKINS,ZF

LINAMAR (MOTORES)

Suppliers (T1) -‐ ilustra've -‐

Two aglomeration strategies: maquila model & sattelite model

1990 1995 2000 2006 2012

(Jan-Oct)

Policy Orientation

Export promotion

policy

NAFTA: Mexico

economic crisis

NAFTA: US

Recession

NAFTA: Mexican recovery Recovery

Production (millions of units) 0.83 0.93 1.9 2.0 2.7

% Domestic 34% 17% 25% 21% 17%

% Exports 66% 83% 75% 79% 83%

% Imports (of total sales) 0% 3% 46% 63%

54%

MEXICO: Vehicles

Sources: Author elaboration based on AMIA data base (several years)

1990 1995 2000 2006 2012

(Jan-Oct)

Policy Orientation

Export promotion

policy

NAFTA: Mexico

economic crisis

NAFTA: US

Recession

NAFTA: Mexican recovery Recovery

% LV (of total production) 75 67.1 69 62.6 67.6

% Big Three U.S. 62% 65% 58% 59% 45.5%

% Big Three European 21% 18% 25.3%

% Big Three Japanese 19% 23% 29.2% No. of Models 58 370 295 No. of Brands 8 28 29

MEXICO: Vehicles,

Sources: Author elaboration based on AMIA data base (several years)

Annual Average

1978-1982 1983-1987 1988-1994 1995-2000 2001-2005 2008-09 2011-‐2012

ISI Export Promotion NAFTA NAFTA 2 CRISIS BOOM

Production (000) 478 352 872 1,280 1,647 2,100 2,293

Domestic (000) 458 295 518 322 415 414 378.1

Export (000) 20 56 353 958 1,232 1,661 1,914.8

Vehicles (of total of production) 62% 67% 75% 67% 59% 66% 65%

Trucks (of total production) 38% 33% 25% 33% 40% 34% 34%

% Imports (of total retail sales)

0 0 3% 30% 76% 58% 52%

Export radio 4% 16% 40% 75% 76% 79% 81%

Exports to NAFTA nd nd nd nd 96% 85% 70%

Participation of “The American Big Three” 48% 55% 62% 65% 60% 55% 52%

Sources: Author elaboration based on AMIA data base (several years)

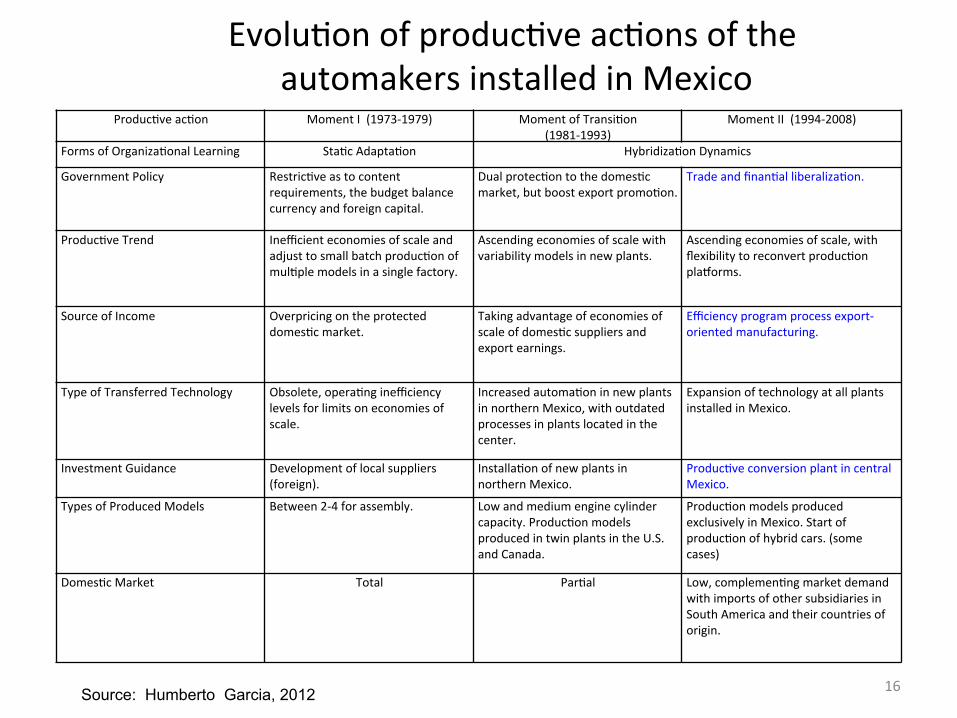

EvoluVon of producVve acVons of the automakers installed in Mexico

ProducVve acVon Moment I (1973-‐1979) Moment of TransiVon (1981-‐1993)

Moment II (1994-‐2008)

Forms of OrganizaVonal Learning StaVc AdaptaVon HybridizaVon Dynamics

Government Policy RestricVve as to content requirements, the budget balance currency and foreign capital.

Dual protecVon to the domesVc market, but boost export promoVon.

Trade and finanVal liberalizaVon.

ProducVve Trend Inefficient economies of scale and adjust to small batch producVon of mulVple models in a single factory.

Ascending economies of scale with variability models in new plants.

Ascending economies of scale, with flexibility to reconvert producVon plagorms.

Source of Income Overpricing on the protected domesVc market.

Taking advantage of economies of scale of domesVc suppliers and export earnings.

Efficiency program process export-‐oriented manufacturing.

Type of Transferred Technology Obsolete, operaVng inefficiency levels for limits on economies of scale.

Increased automaVon in new plants in northern Mexico, with outdated processes in plants located in the center.

Expansion of technology at all plants installed in Mexico.

Investment Guidance Development of local suppliers (foreign).

InstallaVon of new plants in northern Mexico.

ProducVve conversion plant in central Mexico.

Types of Produced Models Between 2-‐4 for assembly. Low and medium engine cylinder capacity. ProducVon models produced in twin plants in the U.S. and Canada.

ProducVon models produced exclusively in Mexico. Start of producVon of hybrid cars. (some cases)

DomesVc Market Total ParVal Low, complemenVng market demand with imports of other subsidiaries in South America and their countries of origin.

16 Source: Humberto Garcia, 2012

Source: Author elaboraVon based on Secretaría de Economía with informaVon from AMIA.

MEXICO: PRODUCTION, EXPORTS AND IMPORTS OF LV

(000s units)

0

500

1,000

1,500

2,000

2,500

3,000

2000 2001 2002 2003 2004 2005 2009 2010 2011 2012 (JAN-‐OCT)

ProducVon

Exports

Imports

43%

16% 4%

6% 1% 0% 0%

30%

MEXICO: Imports by country of origin, 2012 (Jan-‐Oct)

US

Germany

Spain

France

England

Italy

Switzerland

Japan

Source: Author elaboraVon based on Secretaría de Economía with informaVon from AMIA.

19

-‐ Export facts Export Ratio: 83% (2012) (of total production)

- 63% to US (22,000 dlls avg. per unit in 2010) - 14% of exports goes to Latin America (101% annual growth

2009-2011)

12 times Exports Growths (1980-2005)

Import facts

Import Ratio 54% (2012) (of total sales) (9,000 dlls avg. per unit in 2010) – Brands 300% growth – Models 700% growth

Source: AMIA, Banxico.

20

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

CHYSLER FORD GM HONDA NISSAN TOYOTA VW FIAT

LV Produc'on by firm (Porcenteges of Total)

2000 2004 2009 2011 2012 (Jan-‐Oct)

Source: Author elaboraVon based on AMIA data base.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008

2010

2012 (Jan-‐Oct)

2009

2011

2008

2010

2012 (Jan-‐Oct)

2009

2011

2008

2010

2012 (Jan-‐Oct)

2009

2011

2008

2010

2012 (Jan-‐Oct)

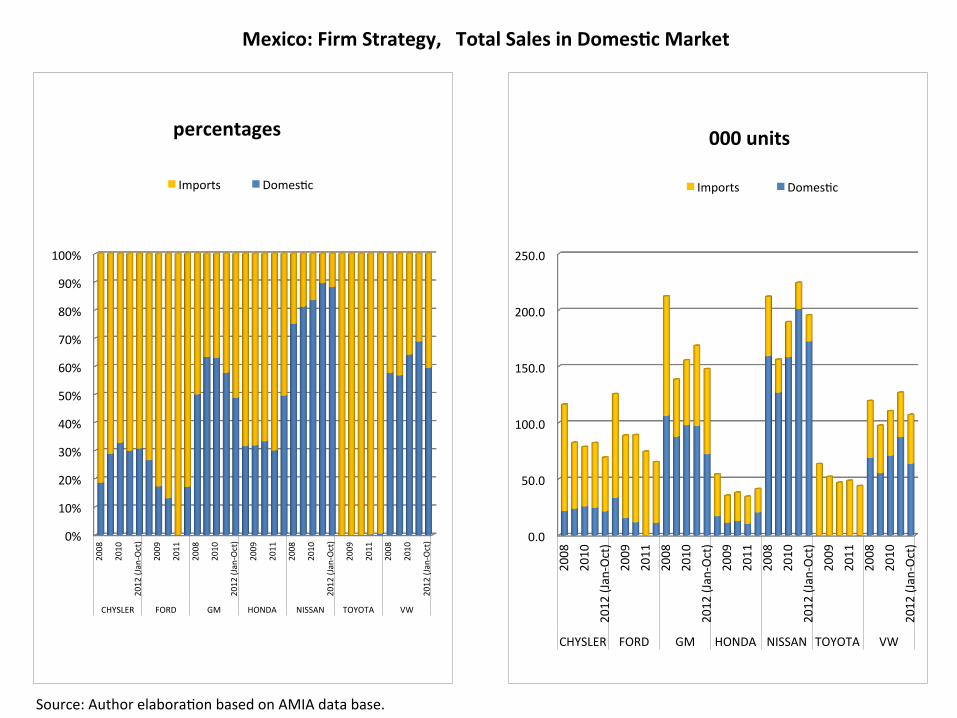

CHYSLER FORD GM HONDA NISSAN TOYOTA VW

Percentages

DomésVco Exportación

Mexico: Firm Strategy: Domes'c Produc'on and Exports

0

100

200

300

400

500

600

700

2008

2010

2012 (Jan-‐Oct)

2009

2011

2008

2010

2012 (Jan-‐Oct)

2009

2011

2008

2010

2012 (Jan-‐Oct)

2009

2011

2008

2010

2012 (Jan-‐Oct)

CHYSLER FORD GM HONDA NISSAN TOYOTA VW

000 units DomésVco

Exportación

Source: Author elaboraVon based on AMIA data base.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008

2010

2012 (Jan-‐Oct)

2009

2011

2008

2010

2012 (Jan-‐Oct)

2009

2011

2008

2010

2012 (Jan-‐Oct)

2009

2011

2008

2010

2012 (Jan-‐Oct)

CHYSLER FORD GM HONDA NISSAN TOYOTA VW

percentages

Imports DomesVc

0.0

50.0

100.0

150.0

200.0

250.0

2008

2010

2012 (Jan-‐Oct)

2009

2011

2008

2010

2012 (Jan-‐Oct)

2009

2011

2008

2010

2012 (Jan-‐Oct)

2009

2011

2008

2010

2012 (Jan-‐Oct)

CHYSLER FORD GM HONDA NISSAN TOYOTA VW

000 units

Imports DomesVc

Mexico: Firm Strategy, Total Sales in Domes'c Market

Source: Author elaboraVon based on AMIA data base.

Firms, plants and models (IlustraVve) Firm Plant Model

Kenworth Mexicali Heavy trucks

Ford Chihuahua Engines

Hermosillo LV

CuauVtlán LV, Precision tools

GM Ramos Arizpe, Coahuila LV, Engines

Silao, Guanajuato LV, engines

San Luis Potosí Trucks

Toluca Trucks

Chrysler Ramos Arizpe, Coahuila LV, engines

SalVllo, Coahuila. Pick-‐up Trucks

Toluca, Edo. México LV, engines

Source: AMIA.

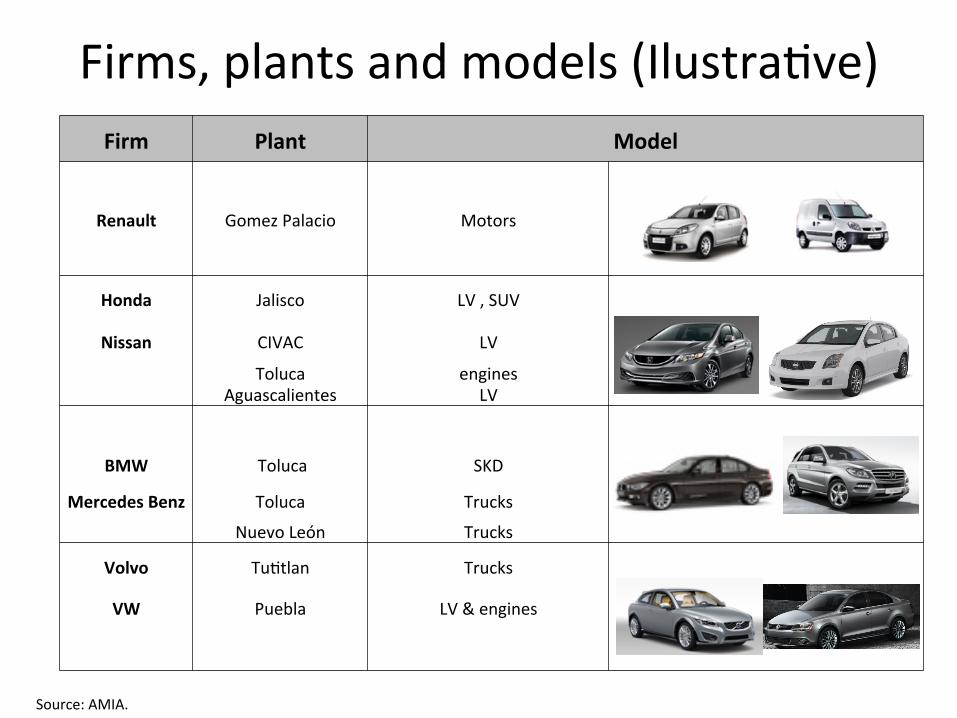

Firms, plants and models (IlustraVve) Firm Plant Model

Renault Gomez Palacio Motors

Honda Jalisco LV , SUV

Nissan CIVAC LV

Toluca Aguascalientes

engines LV

BMW Toluca SKD

Mercedes Benz Toluca Trucks

Nuevo León Trucks

Volvo TuVtlan Trucks

VW Puebla LV & engines

Source: AMIA.

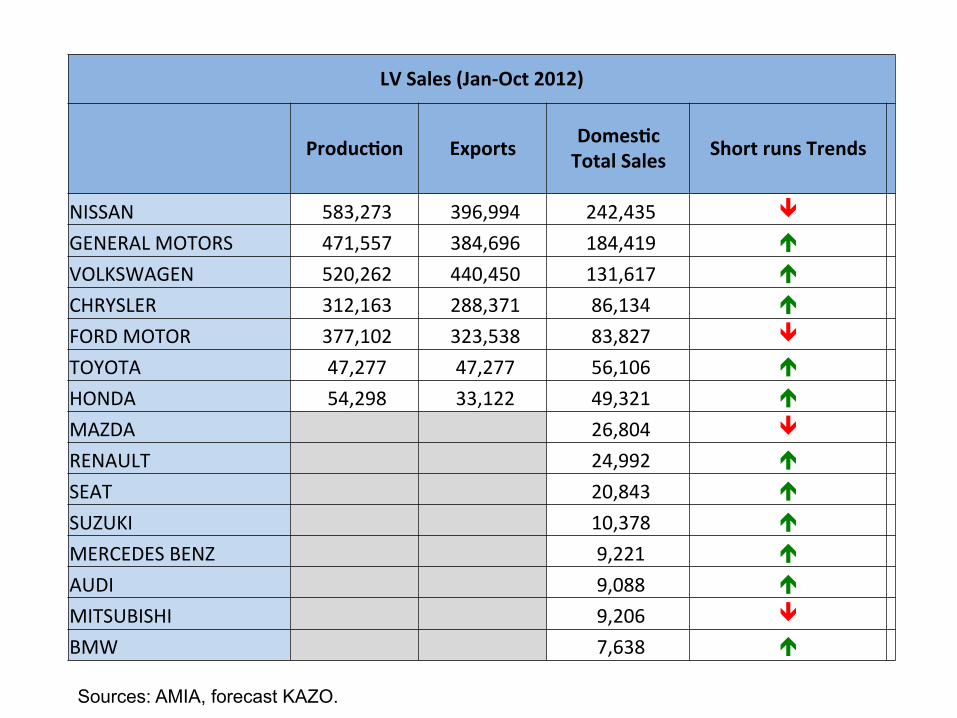

LV Sales (Jan-‐Oct 2012)

Produc'on Exports Domes'c Total Sales Short runs Trends

NISSAN 583,273 396,994 242,435 ê

GENERAL MOTORS 471,557 384,696 184,419 é

VOLKSWAGEN 520,262 440,450 131,617 é

CHRYSLER 312,163 288,371 86,134 é

FORD MOTOR 377,102 323,538 83,827 ê

TOYOTA 47,277 47,277 56,106 é

HONDA 54,298 33,122 49,321 é

MAZDA 26,804 ê

RENAULT 24,992 é

SEAT 20,843 é

SUZUKI 10,378 é

MERCEDES BENZ 9,221 é

AUDI 9,088 é

MITSUBISHI 9,206 ê

BMW 7,638 é

Sources: AMIA, forecast KAZO.

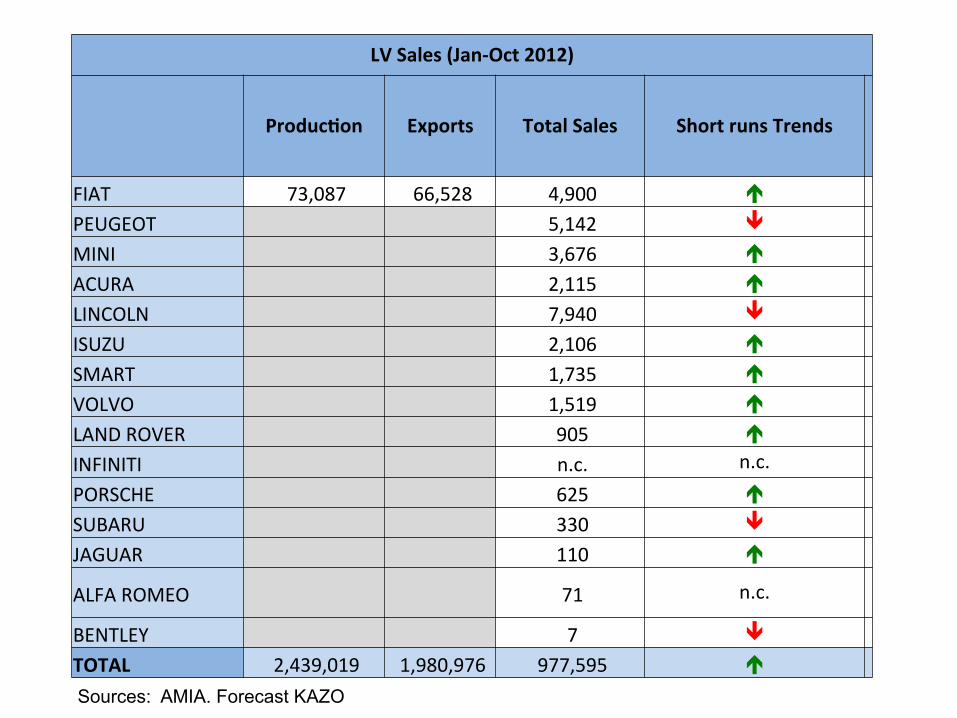

LV Sales (Jan-‐Oct 2012)

Produc'on Exports Total Sales Short runs Trends

FIAT 73,087 66,528 4,900 é

PEUGEOT 5,142 ê

MINI 3,676 é

ACURA 2,115 é

LINCOLN 7,940 ê

ISUZU 2,106 é

SMART 1,735 é

VOLVO 1,519 é

LAND ROVER 905 é

INFINITI n.c. n.c. PORSCHE 625 é

SUBARU 330 ê

JAGUAR 110 é

ALFA ROMEO 71 n.c.

BENTLEY 7 ê

TOTAL 2,439,019 1,980,976 977,595 é

Sources: AMIA. Forecast KAZO

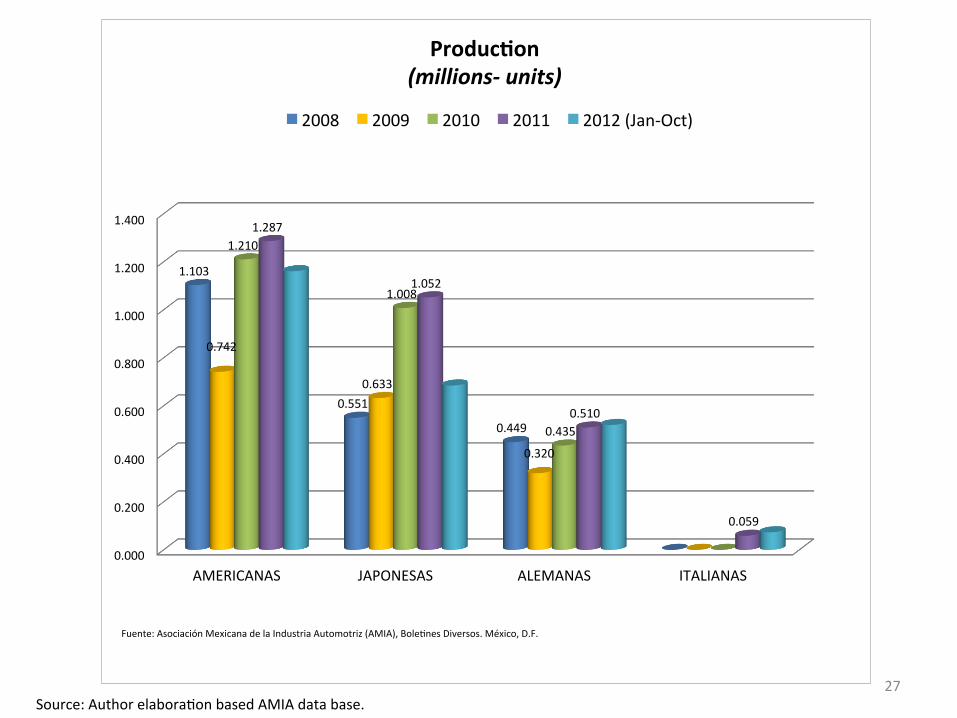

27

0.000

0.200

0.400

0.600

0.800

1.000

1.200

1.400

AMERICANAS JAPONESAS ALEMANAS ITALIANAS

1.103

0.551

0.449

0.742

0.633

0.320

1.210

1.008

0.435

1.287

1.052

0.510

0.059

Produc'on (millions-‐ units)

2008 2009 2010 2011 2012 (Jan-‐Oct)

Fuente: Asociación Mexicana de la Industria Automotriz (AMIA), BoleVnes Diversos. México, D.F.

Source: Author elaboraVon based AMIA data base.

28

931.7

788.3

646.7

1,149.0

1,069.1

161.3

149.6

307.7

494.4 593.6

340.1

163.7

272.1

429.3

684.8

0.0

200.0

400.0

600.0

800.0

1,000.0

1,200.0

1,400.0

2000 2004 2009 2011 2012 (Jan-‐Oct)

Export Produc'on (000 units)

AMERICANS JAPANESE

GERMANS

Source: AMIA 0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

2000 2004 2009 2011 2012 (Jan-‐Oct)

55.3%

49.0%

41.0%

37.2%

35.9%

23.1% 25.1%

31.2%

34.5%

40.8%

20.9% 19.0% 17.2% 18.6%

18.7%

% Domes'c Market

AMERICANAS JAPONESAS ALEMANAS Source: Author elaboraVon based AMIA data base.

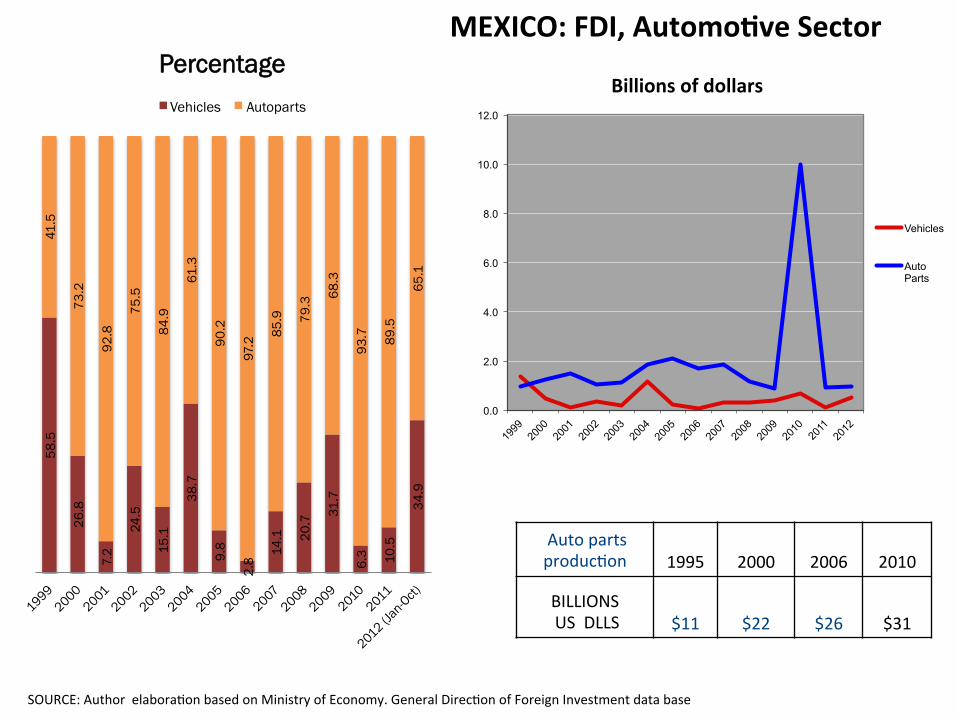

2.1 SUPPLIERS

MEXICO: FDI, Automo've Sector

Auto parts producVon 1995 2000 2006 2010

BILLIONS US DLLS $11 $22 $26 $31

58.5

26.8

7.2

24.5

15.1

38.7

9.8

2.8

14.1

20.7

31.7

6.3 10

.5

34.9

41.5

73.2

92.8

75.5

84.9

61.3

90.2

97.2

85.9

79.3

68.3

93.7

89.5

65.1

Percentage Vehicles Autoparts

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Billions of dollars

Vehicles

Auto Parts

SOURCE: Author elaboraVon based on Ministry of Economy. General DirecVon of Foreign Investment data base

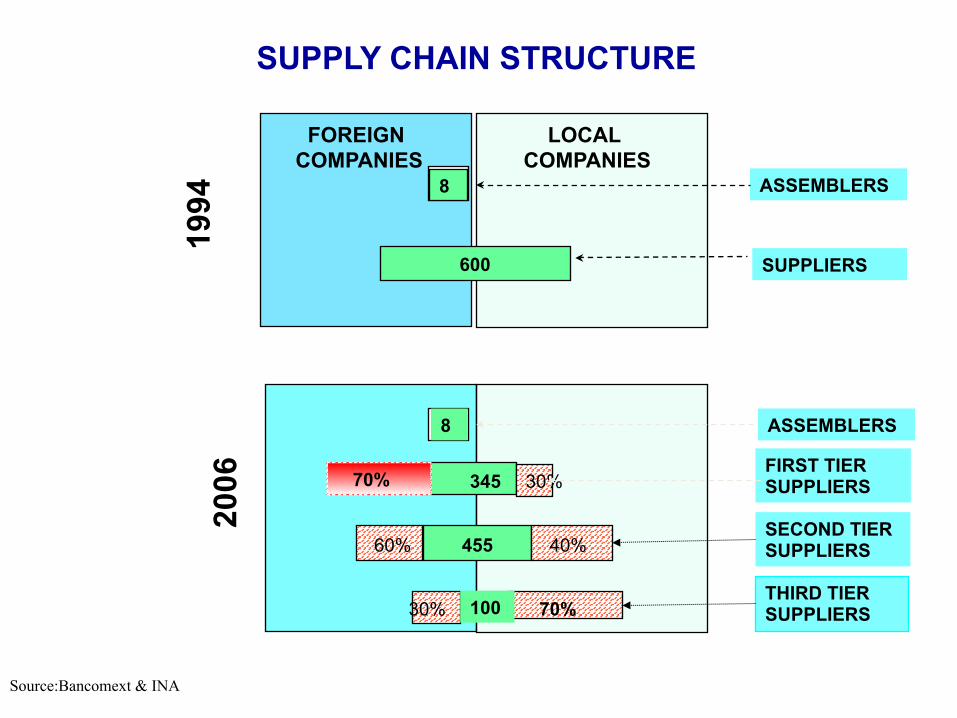

FOREIGN COMPANIES

LOCAL COMPANIES

ASSEMBLERS

FIRST TIER SUPPLIERS

SECOND TIER SUPPLIERS

THIRD TIER SUPPLIERS

8

600

ASSEMBLERS

SUPPLIERS

1994

20

06

8

345 30%

40% 60%

100 30% 70%

455

SUPPLY CHAIN STRUCTURE

Source:Bancomext & INA

70%

Auto Parts Facts Has become the hub for NAFTA: • 2,000 plants, aprox. in 2012 (1,100 in 2006; 650 in 1994) (Source: INA)

– 45% OES; 55% SMEs (2009) (Source: INA)

– 70% foreign 30% Mexicans (2009) (Source: INA)

• 80% of value goes to USA/Canada (2009) (Source: INA)

Spin-‐offs seen from the MNC MNC Ex-Managers that created their own company AUTO industry

38 (sample)

Average. New firms created

Total companies created AUTOS IND. 56 1.5

Became MNCs suppliers AUTO IND. 40%

Source:Bancomext & INA

Source: Contreras and Carrillo 2012

Source: Author elaboration based on CIEMEX-WEFA, 1991, 1997, 2004 y 2005.

MEXICO: Maquila Strategy? Maquila & IMMEX. Selected industries

1981-1989

27%

58%

15%

37%

43%

20% Garment

Electronics

Autoparts

2007-2010 (IMMEX) Plants

14%

62%

24%

23%

46%

31%

Employment % of Total Plants

1981 65 1991 50 2001 57 2006 54 2010 50

% Total Employ

80 68 74 72 70

3

HOW THE AUTO INDUSTRY IS

INTEGRATED IN MEXICO?

35

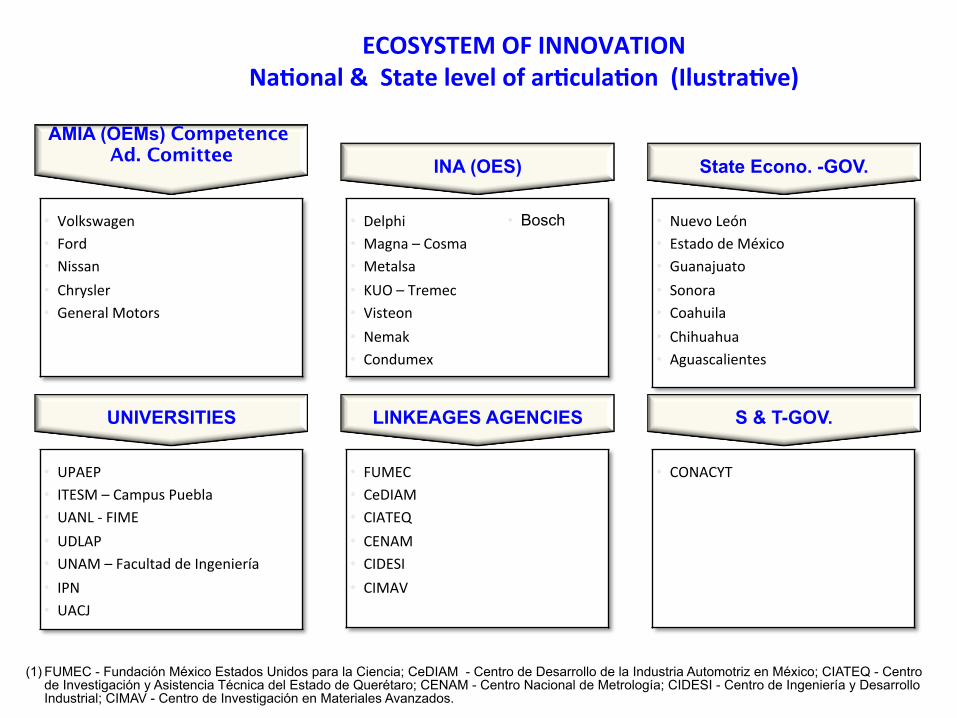

ECOSYSTEM OF INNOVATION Na'onal & State level of ar'cula'on (Ilustra've)

• Volkswagen • Ford • Nissan • Chrysler • General Motors

AMIA (OEMs) Competence Ad. Comittee

INA (OES) State Econo. -GOV.

• Delphi • Magna – Cosma • Metalsa • KUO – Tremec • Visteon • Nemak • Condumex

• Nuevo León • Estado de México • Guanajuato • Sonora • Coahuila • Chihuahua • Aguascalientes

• UPAEP • ITESM – Campus Puebla • UANL -‐ FIME • UDLAP • UNAM – Facultad de Ingeniería • IPN • UACJ

UNIVERSITIES LINKEAGES AGENCIES S & T-GOV.

• FUMEC • CeDIAM • CIATEQ • CENAM • CIDESI • CIMAV

• CONACYT

(1) FUMEC - Fundación México Estados Unidos para la Ciencia; CeDIAM - Centro de Desarrollo de la Industria Automotriz en México; CIATEQ - Centro de Investigación y Asistencia Técnica del Estado de Querétaro; CENAM - Centro Nacional de Metrología; CIDESI - Centro de Ingeniería y Desarrollo Industrial; CIMAV - Centro de Investigación en Materiales Avanzados.

• Bosch

Higher

Lower Lower

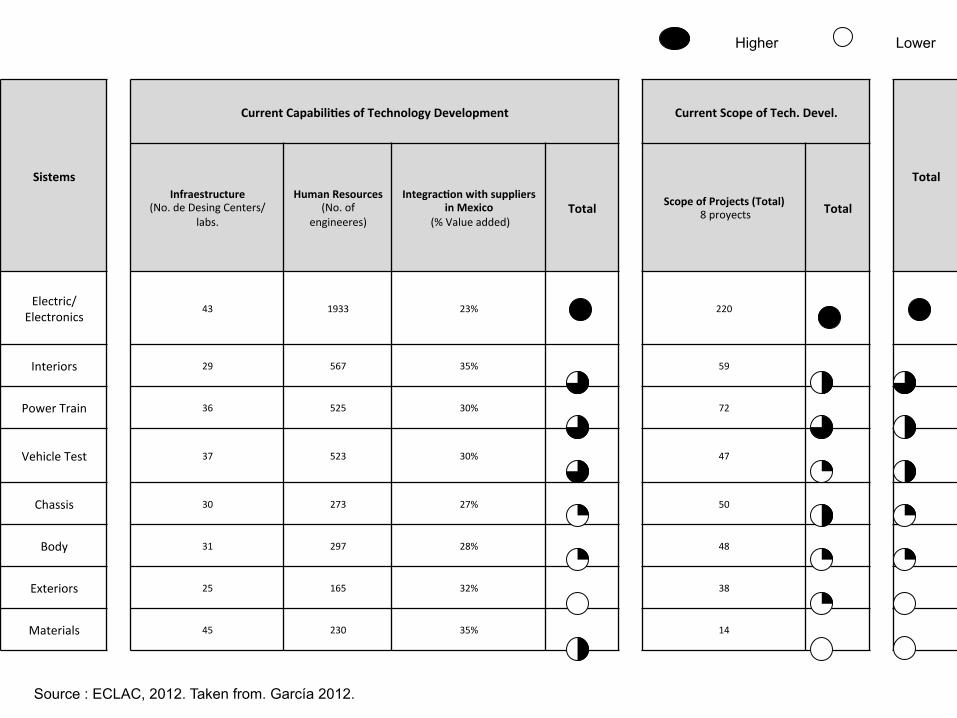

Technological development in Mexico

Higher

Capacities of Tech development Infraestructure − Design Centers − Test Labs.

• Human Resources − Concentration of

engineers by system

− Capabilities − Integration with

suppliers in Mexico

Current scope of tech. development • Value and number of projects-companies • Value and number of colaborative projects industry- universities • Value and number of projects with goverment funding

Power Train Vehicle Test

Materials

Exteriors

Interiors

Electric Electronic

Body

Chasis

Sample of firms & institutions interviewed, 2011

Source : ECLAC, 2012. Taken from. García 2012.

Sistems

Current Capabili'es of Technology Development Current Scope of Tech. Devel.

Total Infraestructure

(No. de Desing Centers/ labs.

Human Resources (No. of

engineeres)

Integrac'on with suppliers in Mexico

(% Value added) Total Scope of Projects (Total)

8 proyects Total

Electric/ Electronics

43 1933 23% 220

Interiors 29 567 35% 59

Power Train 36 525 30% 72

Vehicle Test 37 523 30% 47

Chassis 30 273 27% 50

Body 31 297 28% 48

Exteriors 25 165 32% 38

Materials 45 230 35% 14

Higher Lower

Source : ECLAC, 2012. Taken from. García 2012.

Design Centers (sample)

9

7

6

7

6

7

5

5

12

13

10

8

9

7

8

7

Electric-Electronics 21

Interiors 15

Power Train 16

Materials 20

Exteriors 12

Body 13

Chassis 14

Vehicle Test 15

Companies Universities

No of Design Centers = 28

Areas/ systems inside Design Centers

Universities / Research Centers = 14 Companies = 14

Source : ECLAC, 2012. Taken from. García 2012.

5 OEMS HAVE TEST CENTERS

Comments

• OEMS have their own test centers • At these sites, there are different types of tests, for

example: • Performance (acceleration, braking, Consumption,

Noise, A / C, Emissions) • Durability (life of the vehicle and its components) • Many tests are sent to Mexico to save costs • "It's cheaper testing in Mexico and is greatly

facilitated by the proximity to the U.S." - Director of OEM Engineering

• Almost all vehicle testing infrastructure works to less than 50% capacity.

• Some companies rent their facilities to third parties to perform tests. However this is not a common practice

Vehicle Test Centers in Mexico

Estado de México – 3 D.F. - 2

Puebla - 1

Aguascalientes - 1

Colima - 1

Vehicles Test Centers Centros = 9

Capacidad de desarrollo tecnológico - Infraestructura

Michoacán - 1

Source : ECLAC, 2012. Taken from. García 2012.

Sector opinions: "The work they do not require our engineers graduate" –

OEM Director of Engineering "To hire engineers by area there is no preference for

area of specialization, this is because no one meets the required specific profile" – OEM Director of Engineering

Human Resources. Engineers

The technological development of the sample is carried out mostly with undergraduate alumni

The system with the highest number of engineers in the sample is the Electric / Electronic

No. Of Engineers by system (Sample = 4,512)

Goverment opinions:

• En México se gradúan casi 100,000 ingenieros por año altamente calificados y compeVVvos

165230273297

523525567

1933

Vehcile Test

Power Train

Interiors

Electric /Electronic

Exteriors

Materials

Body

Chassis

PhD

2%

Master 11%

BA

87%

Source : ECLAC, 2012. Taken from. García 2012.

In Mexico, nearly 100,000 engineers graduating per year highly qualified and competitive

Research Projects, Sample

Technological Development Projects

• Electrical and Electronics • Thermal Resistance, electronic systems, embedded

systems, MEMS • Vehicle Testing • Vibration prototypes, improved noise, vibration and

roughness vehicle test stands, sensors, instrumentation, test methodology, emissions

• powertrain • Prediction of vibration, design new transmissions, motors

alternative energy • chassis • Lightweight structures, suspension, steering, axles • materials • Eco-friendly materials, light, efficient, strong • interiors • Validation interior plastic parts, interior design parts • Bodywork • Redesign of parts

Vehicle Test 9%

Exteriors 7%

Materials 3%

Power Train 13%

Chassis 9%

Interiors 11%

Electric/ Electronic 40%

Body 9%

Total = 548 projects

Distribu'on of Projects by System Examples

Source : ECLAC, 2012. Taken from. García 2012.

43

City with Delphi plants City with Delphi plants in joint venture City of Delphi plants and co-investment

Mexico Presence: 34 years in Mexico Present in 22 cities

More than 52,000 employees 46 Delphi plants

Three engineering centers 17 plants in joint venture

Over 100 customers Destination of products

90% to the U.S. and Canada

Source : Delphi presentation, 2012

Juárez Mexico Technical Center

44

Delphi Technical Centers

Querétaro Queretaro Techical Center in

co-investment Saltillo Tool Technical Center

§ More than 2,000 engineers

§ 284 patents § 3 Engineering Centers

CIATEQ, UACJ, ITESM

2011

Source : Delphi presentation, 2012

45

Mexican Technical Center (Juarez). Some Facts

• Mexico Technical Center is the largest Delphi technical center globally • Unique technical center with all divisions represented. • Opened in 1995 and expanded in 1997 • The "Launch Center" was annexed to the complex in 1999

Tests carried out in laboratories

• Materials analysis • calibraVon • ElectromagneVc CompaVbility • VibraVons and InstrumentaVon • Rapid prototyping • Substances care

– dimensional – durability – corrosion – Packaging Validation – analytical engineering

Source : Delphi presentation, 2012

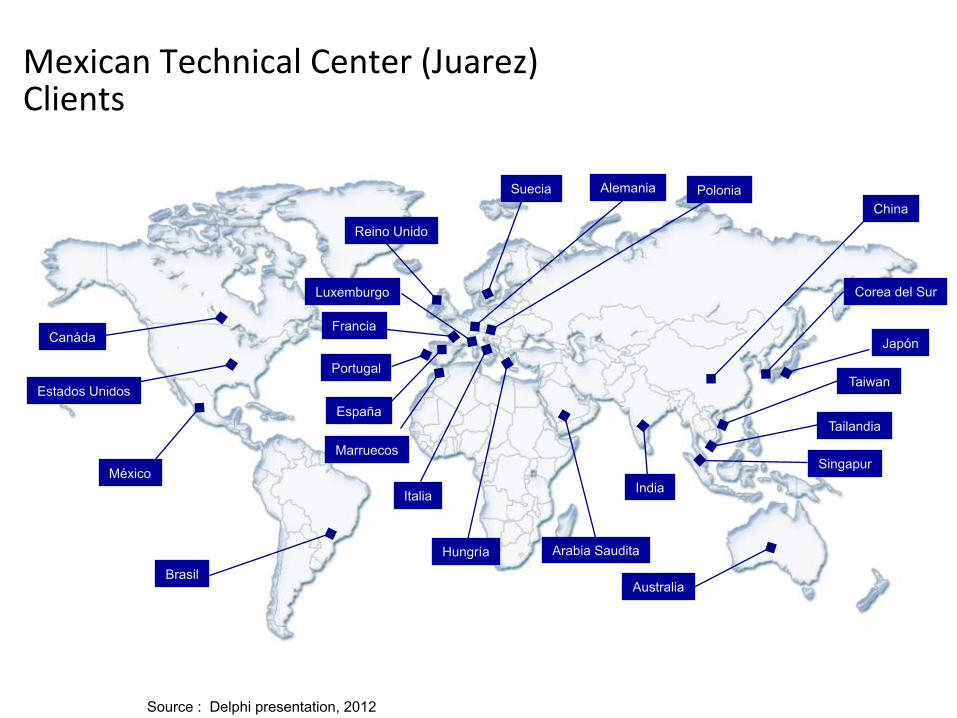

Mexican Technical Center (Juarez) Clients

Canáda

Estados Unidos

México

Brasil

España

Francia

Reino Unido

Suecia Alemania Polonia

Corea del Sur

Arabia Saudita Hungría

Italia

Luxemburgo

Singapur

Tailandia

Taiwan

China

India

Australia

Portugal

Japón

Marruecos

Source : Delphi presentation, 2012

4

WHAT TYPE OF EMPLOYMENT RELATIONS EXIST?

Index of the cost of manufacturing auto parts (Index 100=USA)

82.1

85.1

87

87.6

94.6

95

96.6

96.9

97

100

100.1

107.4

0 20 40 60 80 100 120

China

India

Mexico

Rusia

Brazil

UK

France

Canada

Italy

USA

Germany

Japan

Source: KASO & Asociados based on data from KPMG. Guide to international business location, 2012.

4.1 Employment

1997 2005 2012 500,000 (aprox.)

1’051,193

n.d.

CANADA + 500,000 US 3,500,000

5% OEMs 40% Auto Parts 8% Vehicle Dealers 16% Auto. Parts Stores 31% Auto. Repair Shops

50,000 OEMs 550,000 parts

49 Source: Author elaboration based on INEGI, AMIA, Secretará de Economía, INA

Par'cipa'on in the Global Value Chain

Ac'vi'es Par'cipa'on of Employment Automo've Manufacture

I. Pre Manufacture 2.19 2.90 II. Manufacture 69.80 67.30 III. Post Manufacture 28.01 29.70

100.0 100.0

Employment in the Global Value Chain (%)

Work areas Autos Manufacture R&D 2.2 3.0 ProducVon 69.8 67.3

MarkeVng & Sales 1.8 12.0

Customer Service 2.1 5.0

Accountancy & Management 8.4 9.1 Other AcVviVes 15.6 3.6 100 100

Mexico auto sector: GVC employment (Ilustrative)

Source: Carrillo, Contreras y Gomis, 2012. Multinational Survey in Mexico. Project COLEF-CONACYT # 55108, "Multinational Firms in Mexico: A study on organizational structure, innovation and employment practices", 2010

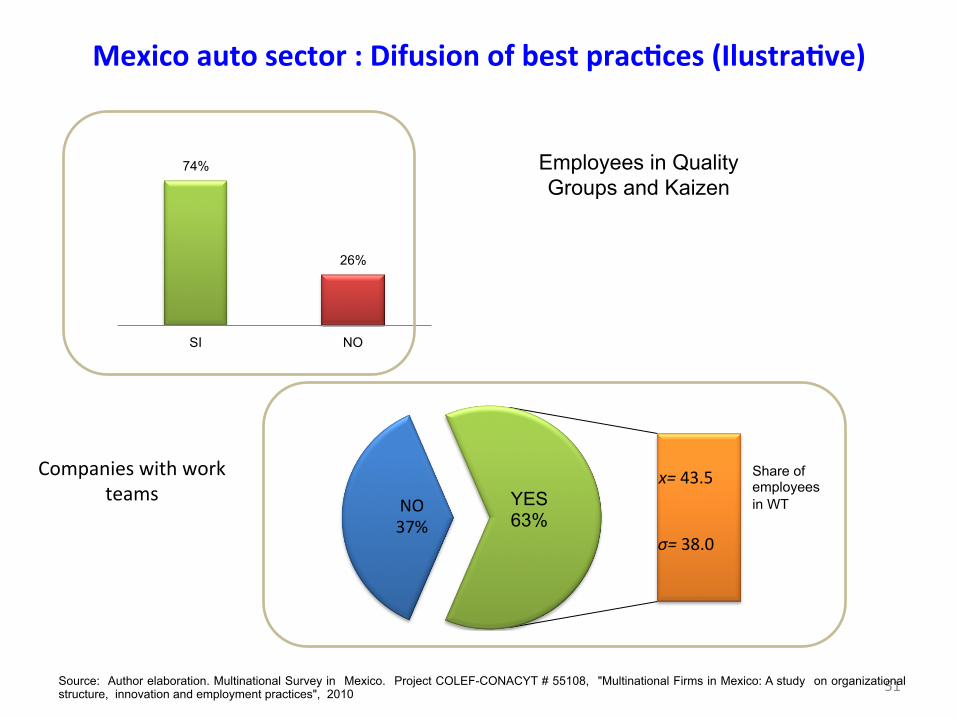

Mexico auto sector : Difusion of best prac'ces (Ilustra've)

74%

26%

SI NO

NO 37%

x= 43.5

σ= 38.0

YES 63%

Share of employees in WT

Companies with work teams

51

Employees in Quality Groups and Kaizen

Source: Author elaboration. Multinational Survey in Mexico. Project COLEF-CONACYT # 55108, "Multinational Firms in Mexico: A study on organizational structure, innovation and employment practices", 2010

4.2 Industrial RelaVons • Mexico’s automoVve supply base has developed into mature clusters of auto parts & OEMs satellite model, but...

• The compeVVveness and industrial upgrading of the automoVve sector is not reflected in salary levels of their workers.

Cost of Labor in Mexico in Automo've Mul'na'onals

MNC's Average Income Cost of labor a % 2007 of total cost

Employment Less than 500 2.72 32.5 More than 500 2.71 26.8 Total 2.71 28.3

Origin Mexico 3.73 28 United States 2.56 28.3 Rest of the World 2.72 28.4

Total 2.71 28.3

Cost of Labor in Mexico in Automo've Mul'na'onals

MNC's Minimum Wages < 5 mw > 5 mw

Employment Less than 500 63.10 36.40 More than 500 61.30 38.70

Origin Mexico 0.00 100.00 United States 75.00 25.00 Rest of the World 60.90 39.10

Total 61.90 38.10

Contrary to what is a common believe, the Mexican MNCs pays 45% more than MNC’s from the US and 37%

more than MNC’s from the rest of the

world

2012 Hour Wages averge (US dlls) OEMs 5-6 SUPPLIERS: 3-4

Source: Bensusán and,Carrillo, 2010. Multinational Survey in Mexico. Project COLEF-CONACYT # 55108, ‘Multinational Firms in Mexico: A study on organizational structure, innovation and employment practices’, 2010

Source: Besusán and Carrillo, 2010. Multinational Survey in Mexico. Project COLEF-CONACYT # 55108, ‘Multinational Firms in Mexico: A study on organizational structure, innovation and employment practices’, 2010

Level of employee representaVon (IlustraVve)

Yes

No

UNION

Union density 86% (19% EAP; 60% MNCs)

86%

14%

Annual average wages according level of employment representaVon

Source: Bensusán and Carrillo, 2010. Multinational Survey in Mexico. Project COLEF-CONACYT # 55108, ‘Multinational Firms in Mexico: A study on organizational structure, innovation and employment practices’, 2010

Capacity of individual business units to recognize unions

in Automotive Multinationals, 2008

MNC's Capacity (%) Nule Medium Total

Employment Less than 500 25.00 50.00 25.00 More than 500 24.00 56.00 20.00

Origin Mexico 0.00 100.00 0.00 United States 40.00 40.00 20.00 Rest of the World

12.00 65.00 24.00

Total 24.00 55.00 21.00

Managers Opinion: The company monitors the enforcement of labor rights of workers in supplier

companies or in each part of the processes outsourced

MNC's Capacity (%) Disagree No opinion In Accordance

Employment Less than 500 20.0 20.0 60.0 More than 500 6.9 13.8 79.3

Origin Mexico 0.0 33.3 66.7 United States 20.0 6.7 73.3 Rest of the World

4.8 19.0 76.2

Total 10.3 15.4 74.4

Managers opinion: The union representatives are cooperating to solve problems and achieve business

objectives

MNC's Capacity (%) Disagree No opinion In Accordance

Employment Less than 500 11.1 0.0 88.9 More than 500 7.4 11.1 81.5

Origin Mexico 0.0 0.0 100.0 United States 16.7 16.7 66.7 Rest of the World

4.8 4.8 90.5

Total 8.3 8.3 83.3

There is a correlation between medium recognition of Union and the level of wages…

Source: Bensusán and Carrillo, 2010. Multinational Survey in Mexico. Project COLEF-CONACYT # 55108, ‘Multinational Firms in Mexico: A study on organizational structure, innovation and employment practices’, 2010

5

CONCLUSIONS

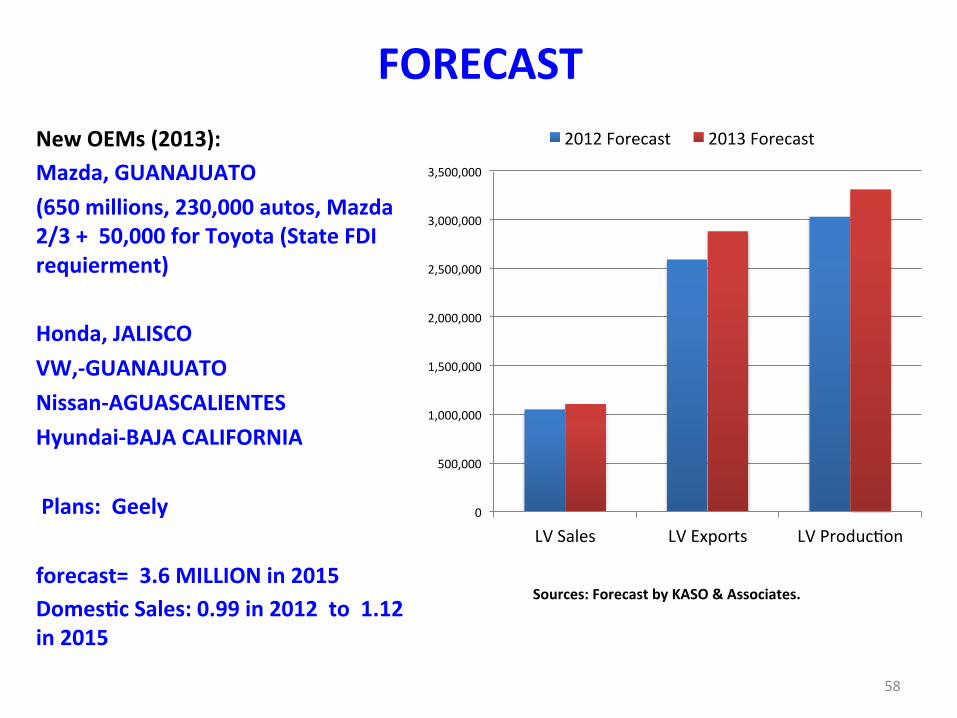

FORECAST New OEMs (2013): Mazda, GUANAJUATO (650 millions, 230,000 autos, Mazda 2/3 + 50,000 for Toyota (State FDI requierment) Honda, JALISCO VW,-‐GUANAJUATO Nissan-‐AGUASCALIENTES Hyundai-‐BAJA CALIFORNIA Plans: Geely forecast= 3.6 MILLION in 2015 Domes'c Sales: 0.99 in 2012 to 1.12 in 2015

58

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

LV Sales LV Exports LV ProducVon

2012 Forecast 2013 Forecast

Sources: Forecast by KASO & Associates.

2001 2008 2015* NAFTA 35 30 27 W.Europe 30 26 22 Japan 10 9 8 Subtotal 75 65 57 China 4 10 13 Rest of Asia 8 11 14 E. Europe 4 6 6 L. America 4 4 5 Other Markets 5 4 5 Subtotal 25 35 43

Light Vehicle Sales (%)

Sources: Automotive News; Global Insight; OICA;

• Path dependence

• Evolutive trajectory (Industrial Upgrading, intra-firm & inter-firm).

• Dynamism: Limited and slow. Need more enigneering design, research and development. More fiscal incentives

• Structural Heterogeneity. (Firm strategy; OEMs vs. suppliers; tiers 1, 2, 3; Regions; Ind. Relations enviroment)

Final thoughts (1)

Final thoughts (2)

• Overview from the data, mainly fro auto parts sector:

– High integraVon in the intra corporate global value chain

– Low-‐status posiVon in these strings: mandates specific producVve, highly specialized producVon, standardized products

– Guidance to external markets, but regional at global level

– Import of R &D rather than local made

Final thoughts (3) • This suggests that the GVC to which most auto firms are built in Mexico, are of a hierarchical type

• Dynamics associated with innovaVon are mainly outside Mexico

• But, learning process and upgrading local capabiliVes occurred (adaptaVve innovaVon –Ford/VW, etc.) Especially in 1st. Tier suppliers. Some tech. leaders such as Delphi.

References AMIA, Asociación de la Industria Automotriz Mexicana, México, data Base and Bulletins. www.amia.com.mx

Automotive News, (several months) www.autonews.com Bancomext, Banco Nacional de Comercio Exterior, México (several presentations) www.bancomext.com Banxico, Banco Nacional de Mexico (internal documents) www.banxico.com Graciela Bensusan, Jorge Carrillo and Ismael Plascencia, 2010, "Social Responsibility and Multinationals" XVIII International Gerpisa Coloquium, Berlin, June 9-11, Jorge Carrillo, Oscar Contreras and Gomis, 2012, “ Investment Strategies and Global Value Chain in the Automotive Industry", Paper presented at XX International Gerpisa Coloquium, Krakow, May 30-June1 Oscar Contreras, Jorge Carrillo y Jorge Alonso “Local Entrepreneurship within Global Value Chains: A case study in the Mexican Automotive Industry” World Development, Vol. 40, no. 5, pp.1013-1023, 2012 CIEMEX-WEFA, (several years) Forecasting company Delphi, Mexican Technical Center, Juarez (internal document), 2012 Eclac, Inversión Extranjera en América Latina, Comisión Económica para América Ltina, Santiago, 2012 www.eclac.org/ Global Insight (several years) www.ihs.com/products/global-insight INA, Instituto Nacional de Autopartes (bulletins and presentations) www.ina.org.mx KAZO & Asociados, Diagnóstico y perspectivas económicas de la indusria automotriz de México, Presentación parala Reunión de Evaluación de la Industria Automotriz RESA-INA, November 9, 2012. Mexico Now, Revista Bimensula de Maquiladoras y Negocios en Mexico, Chihuhua (several numbers) www.mexico-now.com Multinational Survey in Mexico. Project COLEF-CONACYT # 55108, "Multinational Firms in Mexico: A study on organizational structure, innovation and employment practices", 2010 OICA (several years) www.oica.net Secretaria de Economia, Goberino de Mexico, Mexico (data base) www.economia.gov.mx

63