Event @ AICare Hub (30 March) - Manage your time and money as caregiver

18

1 Work Experience Dr Mary Tan has about 30 years of training experience. She has been actively involved in the Singapore government’s infrastructure planning, design and development. Currently, Dr Mary is with the LTA Academy and engages in a one-stop focal point for governments, organizations and professionals around the world to tap Singapore’s know-how and exchange best practices in management and development. She helps to design and conduct learning programmes, and organizes international conferences and seminars. Dr Mary also helps at the Singapore Polytechnic Business School and serves as a member of the Board of Examiners in BCA Academy with effect from 1 Aug 2012. She holds a full Advanced Certification in Training Assessment (ACTA) (6 units) certification. Besides her contribution in the civil service, Dr Mary uses her expertise wisely as a volunteer trainer at voluntary welfare organizations, educational institutions and religious organizations specializing in Financial Education and Successful Ageing. She was conferred a High Achiever Business Alumnus by the University of South Australia since 2008, and has been regularly interviewed by the local radio station Capital 95.8FM and featured in the local newspaper TODAY. Mobile: 92958169 Managing Your Dollars and $ense through Financial Planning by Dr Mary Tan

-

Upload

singapore-silver-pages -

Category

Healthcare

-

view

116 -

download

0

Transcript of Event @ AICare Hub (30 March) - Manage your time and money as caregiver

1

Work ExperienceDr Mary Tan has about 30 years of training experience. She has been actively

involved in the Singapore government’s infrastructure planning, design and

development. Currently, Dr Mary is with the LTA Academy and engages in a

one-stop focal point for governments, organizations and professionals around

the world to tap Singapore’s know-how and exchange best practices in

management and development. She helps to design and conduct learning

programmes, and organizes international conferences and seminars. Dr Mary

also helps at the Singapore Polytechnic Business School and serves as a

member of the Board of Examiners in BCA Academy with effect from 1 Aug

2012. She holds a full Advanced Certification in Training Assessment

(ACTA) (6 units) certification. Besides her contribution in the civil service, Dr

Mary uses her expertise wisely as a volunteer trainer at voluntary welfare

organizations, educational institutions and religious organizations specializing

in Financial Education and Successful Ageing. She was conferred a High

Achiever Business Alumnus by the University of South Australia since 2008,

and has been regularly interviewed by the local radio station Capital 95.8FM

and featured in the local newspaper TODAY.

Mobile: 92958169

Managing Your Dollars and $ensethrough Financial Planning

by Dr Mary Tan

What is Financial Planning?

• Financial Planning is a life-long commitment

to achieve financial security and success,

particularly for our care recipient’s financial

future.

If you fail to plan …

… you plan to fail!

A comprehensive financial plan includes:

EstatePlanning

InvestmentPlanning

RetirementPlanning

TaxPlanning

EducationPlanning

Making a Will

Saving for children’s education

Saving for retirement

Buying an appropriate

insurance plan

Choosing the right investment

product

•• Cash Management Cash Management –– Budget and Budget and Cash Flow PlanningCash Flow Planning

•• Risk Management Risk Management -- InsuranceInsurance

•• Estate PlanningEstate Planning

Basic Focus :Basic Focus :

Are you financially prepared?

• As a caregiver, are you prepared for:

� your own financial independence when you are retired?

� your care recipients’ medical and financial needs when you have no income or are gone, particularly in ensuring that they are able to maintain their standard of living including medical and care-giving expenses?

What is Net Worth?• A snapshot of your financial position at a specific point in time

• A calculation of your assets (WHAT YOU OWN) minus your liabilities (WHAT YOU OWE)

• Preparing a net worth statement will help you get a clearer understanding of your financial resources and make decisions about how best to manage them.

What is Net Worth?

Net worth = Assets – Liabilities

–Implies you have true wealth.

–Implies you are technically bankrupt.

Positive Amount = A Cash Surplus

Negative Amount = A Cash Deficit

Mdm. WongMr. Han

• Owns a 5-rm HDB flat worth $400,000. Fully-paid.

• Has savings of $30,000 in bank

• Current value of her shares is $20,000

• Owns a $1.2 million private condominium. Outstanding bank loan of $1 million.

• Has savings of $5,000 in bank

• Current value of his shares is $100,000

• Owns a $70,000 car but with outstanding loan of $50,000

Net worth$450,000

Net worth$325,000

Example: Who is Wealthier?

Source: MoneySENSE

Mdm Wong!!! Her net worth is higher!

How do I track my spending?

A good way to start taking control of your financial situation is to develop a savings and spending plan.

This is called a BUDGET.

Sources of Income Household Expenses Positive or Negative

=_

Salary, employer CPF, dividend, interest, rental income, public/ private financial assistance, etc.

Fixed payments e.g. rent, housing mortgage & maintenance, car loan & maintenance, insurance premiums, etc.

+

Variable payments e.g. food, personal care & use, utilities, medical, transport, recreation & social, savings & investments, education, pocket allowances for children, etc.

A Typical Family Budget

+

Care-recipient related expenses e.g. special diet, diapers, transport (day-care centre/ hospital), specialized treatment, maid/ caregiver, special assistive equipment, medical fees, etc.

What are the Spending Traps?

• Buying unnecessary things

• Expensive meals

• Cigarettes and drinks

• Gambling

• Keeping up with the others

How How much can it cost?much can it cost?

The Costs can Add Up…

Item MonthlyExpense

Amount when you are 85-yr-old*

Cigarettes($9.50/box, 3/week)

$114 $66,432

Beer($2.50/can, 3/week)

$30 $17,482

Gambling($10/week)

$40 $23,309

Assuming you are 45 years old. *Interest @ 3% p.a.

Some Money-Saving Ideas on Utility • Standby power can account for up to 10% of your

home electricity use. Switch off your home appliances from standby mode!

• Energy saving light uses up to 80% less electricity than light bulbs to produce the same amount of light, and they can last up to 10 times longer! Use an energy saving lamp (7W) instead of a bulb (40W)!

• A fan uses less than 10% of the electricity used by an air-conditioner! Use a fan instead of an air-conditioner to keep cool!

• Boil water only when needed or consider using a thermo-flask to keep hot water. Electric air-pots which keep water hot constantly can cost you about $180 a year in electricity! Source: www.e2singapore.gov.sg

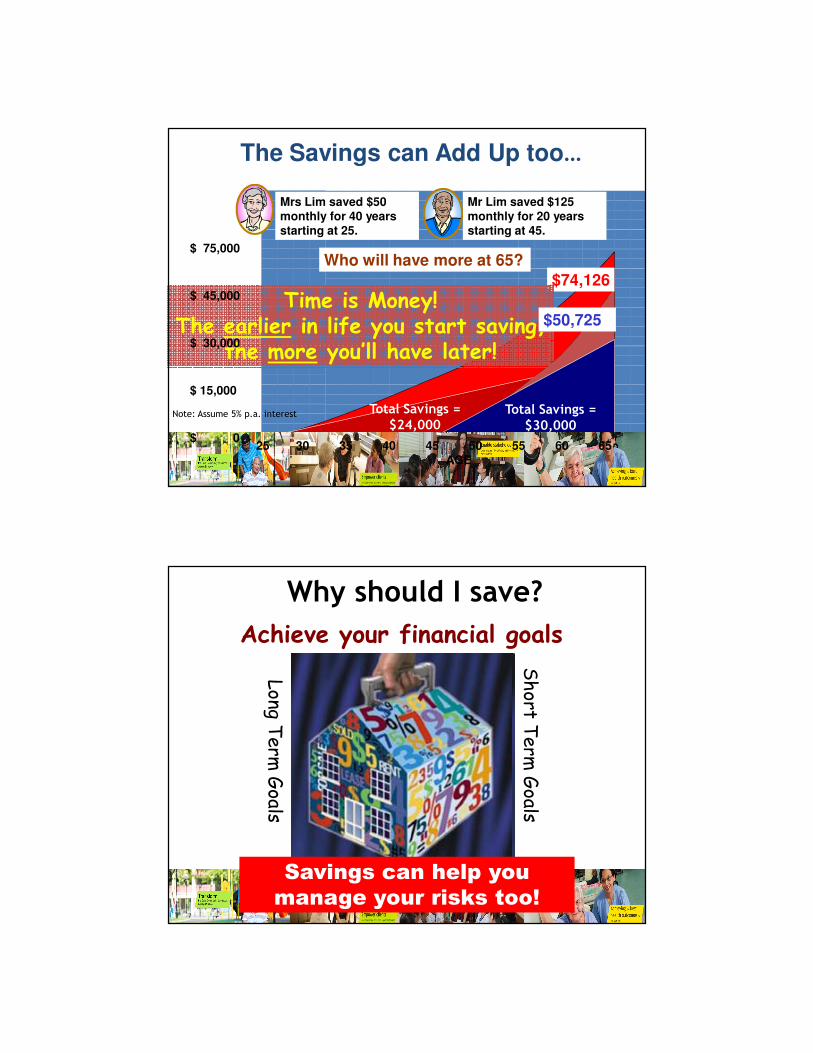

Mrs Lim saved $50 monthly for 40 years starting at 25.

Who will have more at 65?

$74,126

The Savings can Add Up too…

Mr Lim saved $125 monthly for 20 years starting at 45.

Time is Money!The earlier in life you start saving,

the more you’ll have later!

Note: Assume 5% p.a. interest

25 30 35 40 45 50 55 60 65AGE

$50,725

$ 75,000

$ 45,000

$ 30,000

$ 15,000

$ 0

Total Savings =$24,000

Total Savings =$30,000

Why should I save?

Achieve your financial goals

Long T

erm

Goals

Short T

erm

Goals

Savings can help you

manage your risks too!

Tips for Maintaining a Budget• Spend on your Needs, Save

from your Wants• Exercise will-power and

self-control• Develop a good record-

keeping system• Review your budget regularly• Educate yourself in money

matters

Basic Insurance Basic Insurance

Schemes Schemes To To

Protect Protect

Caregivers Caregivers & &

Their Elderly Their Elderly

Loved Ones Loved Ones

Insure Your “Largest” Assets• YOUR HEALTH

• YOUR HOME

• YOUR INCOME

What is Insurance?Protection against large-scale financial loss in exchange for a small charge (premium). In other words, in the event that something unexpected were to occur, it is one way to AVOID risk, MINIMIZE risk, or to pass on or TRANSFER risk.

� Life Insurance

• Gives you and your family financial protection against the financial loss that can happen after your death or if you suffer a total and permanent disability.

• Can also give you a retirement income or act as a financial back-up in emergencies and protect you against health-care costs.

Insuring your Income

Types of Life Insurance Products

Traditional Policy

Whole Life • policy will pay out the sum insured and any bonuses you have built up (if any) when you die or become totally and permanently disabled

Term Life • pays the sum insured only if you die or become totally and permanently disabled during the covered period.

Endowment • pays the sum insured and any bonuses you have built up at the end of the set period of time (maturity date), when you die or become totally and permanently disabled if it happens during this period.

Source: MoneySENSE, “Your Guide to Life Insurance”

Mortgage Reducing Term Assurance Plan (MRTA)

• provides for a sum of money to cover the housing loan balance if the insured person dies

• the sum insured is reduced over the loan duration in tandem with the decrease in the housing loan amount

Insuring your Home

Home Protection Scheme (HPS)

• For borrowers who use CPF savings to pay instalments on HDB, HUDC….

• CPF will settle the housing loan if the insured dies or meets any incident that incapacitates their ability to earn income

Insuring your Home

Insuring your Health

� Health Insurance

• Prevents you and your familyfrom suffering a financial loss asa result of an accident, illness ordisability

• Provide an income while you aredisabled or in hospital, or coverthe cost of your medical ornursing care

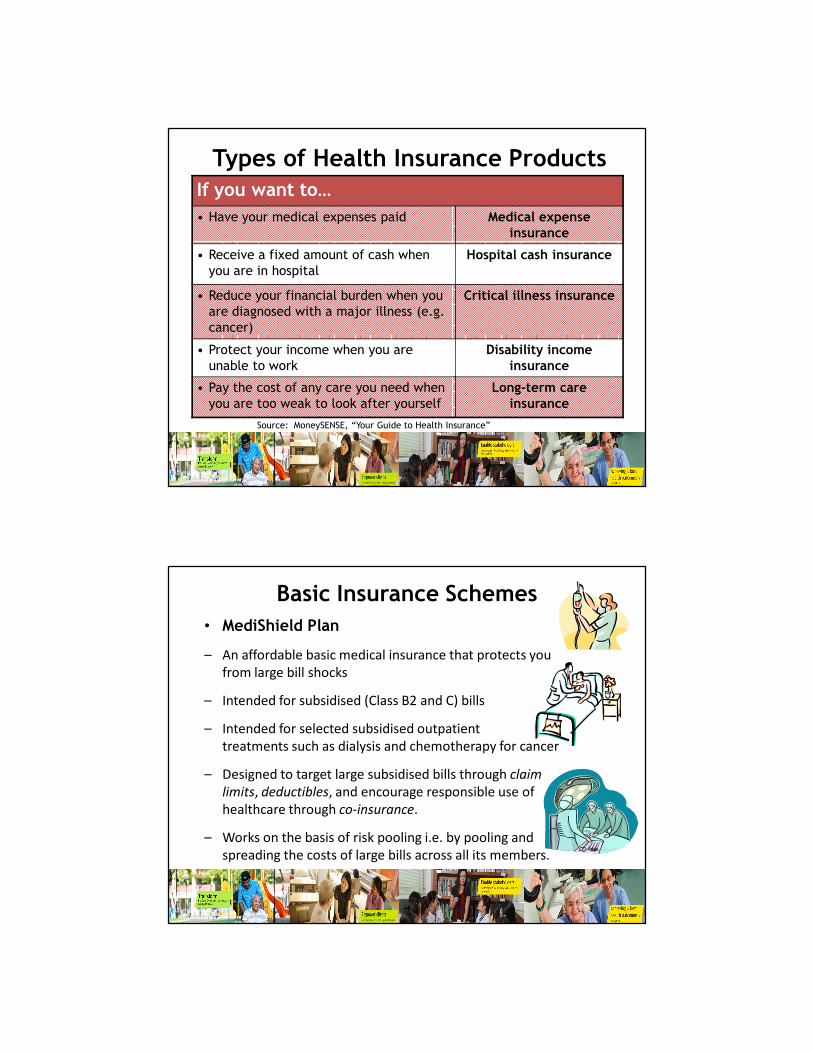

Types of Health Insurance ProductsIf you want to…

• Have your medical expenses paid Medical expense insurance

• Receive a fixed amount of cash when you are in hospital

Hospital cash insurance

• Reduce your financial burden when you are diagnosed with a major illness (e.g. cancer)

Critical illness insurance

• Protect your income when you are unable to work

Disability income insurance

• Pay the cost of any care you need when you are too weak to look after yourself

Long-term care insurance

Source: MoneySENSE, “Your Guide to Health Insurance”

• MediShield Plan

– An affordable basic medical insurance that protects you

from large bill shocks

– Intended for subsidised (Class B2 and C) bills

– Intended for selected subsidised outpatient

treatments such as dialysis and chemotherapy for cancer

– Designed to target large subsidised bills through claim

limits, deductibles, and encourage responsible use of

healthcare through co-insurance.

– Works on the basis of risk pooling i.e. by pooling and

spreading the costs of large bills across all its members.

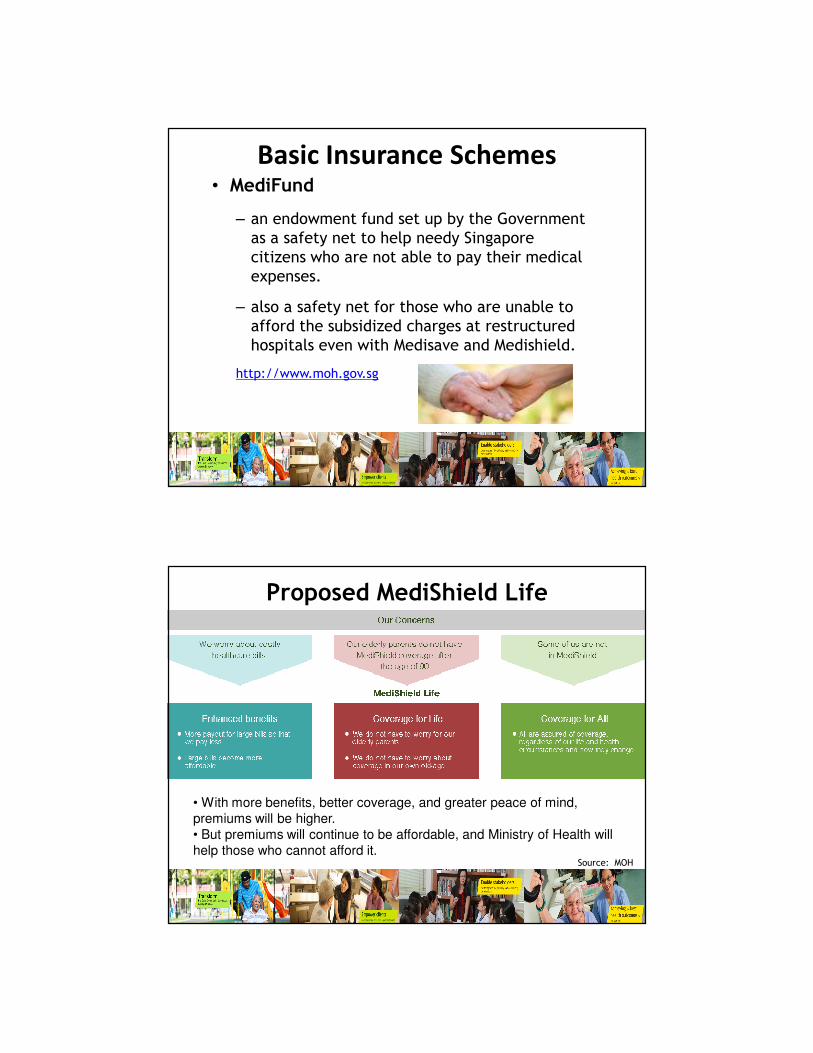

Basic Insurance Schemes

• MediFund

– an endowment fund set up by the Government as a safety net to help needy Singapore citizens who are not able to pay their medical expenses.

– also a safety net for those who are unable to afford the subsidized charges at restructured hospitals even with Medisave and Medishield.

http://www.moh.gov.sg

Basic Insurance Schemes

Proposed MediShield Life

Source: MOH

• With more benefits, better coverage, and greater peace of mind,

premiums will be higher.

• But premiums will continue to be affordable, and Ministry of Health will

help those who cannot afford it.

Estate PlanningEstate Planning

“Basic” Estate Planning• Mental Capacity Act

– allows you to appoint guardians to make decisions on your behalf should you lose your mind to illness or accident

• Will & Trust

– deals with disposition of property at death

• Trust & Revocable Nomination

– with use during lifetime and at death

• Advance Medical Directive (AMD)

– allows you to set forth your wishes regarding extraordinary life-saving measures

Mental Capacity Act• New law passed in Sept 2008

• Allows you to:

1. Choose someone you trust beforehand to make decisions for your welfare and finances when you can’t do so yourself some day.

2. Ask the court to appoint a decision-maker for your loved ones when you are no longer able to do so.

Avoiding Intestacy

If you die without leaving a valid Will, you are said to die Intestate.Surviving Relatives Entitlement

1. Spouse (no children, no parents) Spouse takes all

2. Spouse & children Spouse takes half, Children share balance equally

3. Spouse & parents (no children) Spouse takes half, Parents share balance equally

4. Parents (no spouse, no children) Parents share equally

5. Siblings (no spouse, no children or parents)

Siblings share equally

6. Grandparents (no spouse, children, parents or siblings)

Grandparents share equally

7. Uncles & aunts (no spouse, children, parents, siblings or grandparents)

Uncles & aunts share equally

8. In the absence of any of the above mentioned relatives

Government takes all

Why have a Will?• To ensure that it is YOU who decides how your estate is distributed upon your death.

• To be assured that your loved ones (who are ultimately the Beneficiaries of your Will) are provided for in accordance with your wishes.

• To avoid Intestacy and having the public trustee decide who receives your property

– To appoint an Executor whom you trust– To appoint a Guardian for your loved ones– To appoint a Guardian or Trustee to administer property for your loved ones

Resources and Assistance Schemes for Patients and Caregivers

•Advance Care Planning

•Aged Care TransitION (ACTION) Project

•AICare Hub

•Caregivers Training Grant

•Community Health Assist Scheme (CHAS)

•Foreign Domestic Worker Grant

•Foreign Domestic Worker Levy Concession for Persons with Disabilities

•HOlistic care for MEdically advanced patients (HOME) Programme

•NEXTSTEP

•Public Education and Community Engagement

•Seniors' Mobility and Enabling Fund

•Singapore Programme for Integrated Care for the Elderly (SPICE)

•Singapore Silver Pages

Source: NCSS - Assistance Schemes for Individuals

& Families in Social and Financial Needs

Please check AIC website at www.aic.sg for more details

Q & A

Thank you!Thank you!