Europäische Patent- European Patent Organisation ...European Patent Organisation Organisation...

123

Conseil d'administration Administrative Council Verwaltungsrat European Patent Organisation Organisation européenne des brevets Europäische Patent- organisation CA/20/15 CA/20/15 e Report of the Board of Auditors of the European Patent Organisation on the 2014 accounting period

Transcript of Europäische Patent- European Patent Organisation ...European Patent Organisation Organisation...

Conseil d'administrationAdministrative CouncilVerwaltungsrat

EuropeanPatentOrganisation

Organisation européenne des brevets

EuropäischePatent-organisation CA/20/15

CA/20/15 e

Report of the Board of Auditors of the European Patent Organisation on the 2014 accounting period

CA/20/15

Orig.: de, en, fr

Munich, 08.05.2015

SUBJECT: Board of Auditors' report on the 2014 accounting period Explanations and reasons supplied by the President of the Office

SUBMITTED BY: 1. Board of Auditors of the European Patent Organisation2. President of the European Patent Office

ADDRESSEES: 1. Supervisory Board of the RFPSS (for opinion, Article 80 FinRegs)2. Budget and Finance Committee (for opinion, Article 80 FinRegs)3. Administrative Council (for approval and discharge, Article 80

FinRegs and Article 49(3) and (4) EPC)

CA/20/15 e LT 0720/15 - 150560004

- - I

TABLE OF CONTENTS

Subject Page

I. SUMMARY.............................................................................................................. 1 A. Our task in Brief .................................................................................................... 1 B. OPINION ON THE ACCOUNTS ............................................................................. 1

1. accounting rules ...................................................................................................... 12. opinion .................................................................................................................... 1

C. Opinion on management ...................................................................................... 2 1. FINANCIAL SITUATION ......................................................................................... 2

1.1. Financial reporting ............................................................................................ 2 1.2. Balance-sheet figures ....................................................................................... 2 1.3. Economic situation, factoring in the present value of future national renewal

fees .................................................................................................................. 2 1.4. Income statement ............................................................................................. 3 1.5. Statement of cash flows ................................................................................... 3 1.6. Budget and forecasting accuracy ..................................................................... 4

2. Operations............................................................................................................... 42.1. Comments on the accounts .............................................................................. 4 2.2. Internal control system ..................................................................................... 5 2.3. Business administration ................................................................................... 6 2.4. IT ...................................................................................................................... 9 2.5. Buildings ......................................................................................................... 11

II. DETAILED REPORT ............................................................................................ 13A. Preliminary remarks ............................................................................................ 13 B. Audit opinion ....................................................................................................... 14 C. Comments on the accounts ............................................................................... 15

1. The organisation's Financial and economic position ............................................. 151.2. Introductory remarks ...................................................................................... 15 1.3. Financial-statement figures in brief ................................................................. 16

2. Specific Accounting Remarks................................................................................ 222.1. Post-employment benefit obligations .............................................................. 22 2.2. Repurchase value Caisse Nationale de Prévoyance (CNP) ........................... 31 2.3. IT Roadmap .................................................................................................... 32 2.4. Negative equity of the EPO ............................................................................ 33 2.5. Unitary Patent ("UNIP") .................................................................................. 34 2.6. Calculation of employee-related notes disclosures ........................................ 35

3. General comments on budget implementation ...................................................... 353.1. Forecast income statement ............................................................................ 35 3.2. Forecast balance-sheet figures ...................................................................... 36 3.3. Comparison of budget as adopted and as implemented ................................ 36

CA/20/15 e 150560004

- - II

D. Internal Control System ...................................................................................... 38 1. Internal auditing (Directorate 0.6.1) ....................................................................... 382. Governance of The RFPSS................................................................................... 39

2.1. Control system ............................................................................................... 39 2.2. Compliance system ........................................................................................ 39 2.3. Risk management/assurance and compliance management/assurance ........ 41 2.4. Management system and practice for Fund assets ........................................ 43 2.5. Update from past findings ............................................................................... 44

E. Reports on selected areas.................................................................................. 45 1. Review and Internal Appeals Procedure ............................................................... 45

1.1. Procedures ..................................................................................................... 45 1.2. Facts and figures ............................................................................................ 46 1.3. Recommendations ......................................................................................... 48

2. Patent grant process ............................................................................................. 482.1. Overview ........................................................................................................ 48 2.2. Processing time of the different steps ............................................................ 50 2.3. Backlog of products under Priority 1 ............................................................... 50 2.4. Findings and recommendations ..................................................................... 51

3. Tender procedures ................................................................................................ 533.1. Best practice comparison ............................................................................... 54 3.2. Findings and recommendations – general procurement process ................... 55 3.3. Findings and recommendations – IT procurement process ............................ 56

4. IT 584.1. IT Roadmap .................................................................................................... 58 4.2. IT security ....................................................................................................... 61

5. Building projects .................................................................................................... 635.1. New building project in The Hague ................................................................. 63 5.2. Other building activities .................................................................................. 65 5.3. Benchmarks for building cost ......................................................................... 66

III. STATUS OF FINDINGS FROM PREVIOUS YEARS ........................................... 67A. OFFICE'S FOLLOW-UP REPORT ON CA/20/14 (STATUS 31.01.2015), AND

AUDITORS' REACTION ..................................................................................... 67 B. OFFICE'S FOLLOW-UP REPORT ON CA/20/13 (STATUS 31.01.2015), AND

AUDITORS' REACTION ..................................................................................... 74 C. OFFICE'S FOLLOW-UP REPORT ON CA/20/12 (STATUS 31.01.2015), AND

AUDITORS' REACTION ..................................................................................... 81 D. OFFICE'S FOLLOW-UP REPORT ON CA/20/11 (STATUS 31.01.2015), AND

AUDITORS' REACTION ..................................................................................... 87 E. SUMMARY AND PRIORITY OF OUR RECOMMENDATIONS ............................ 89

IV. EPO PRESIDENT ADDITIONAL EXPLANATIONS AND REASONS ................ 102

CA/20/15 e 150560004

- - III

V. ANNEXES ........................................................................................................... 103ANNEX I Year-on-year comparison, balance sheet and income and expenditure account

(in EUR '000s) ............................................................................................... 104 Annex I/1 Income statement ................................................................................... 104 Annex I/2 Balance sheet ......................................................................................... 105 Annex I/3 Statement of cash flows ......................................................................... 106

ANNEX II Comparison of budgeted and actual income and expenditure (in EUR '000s)107

Annex II/1 Income .................................................................................................... 107 Annex II/2 Expenditure ............................................................................................ 108 Annex II/3 Implementation of the budget of the Pension and Social Security Schemes

............................................................................................................... 109 Annex II/4 Comparison between original and amended budgets............................. 111

ANNEX III Financial forecast and actual income and expenditure.................................. 113 Annex III/1 Income .................................................................................................... 113 Annex III/2 Balance sheet ......................................................................................... 114

ANNEX IV Audit expenditure .......................................................................................... 115 ANNEX V List of abbreviations ...................................................................................... 116

CA/20/15 e 150560004

I. SUMMARY

A. OUR TASK IN BRIEF

1) The Board of Auditors performs its tasks in accordance with Articles 49 and 50 EPC,its rules of procedure and professional audit principles.

2) Under Article 50 EPC in conjunction with Article 79 FinRegs, our report contains inparticular:

• an audit opinion on the accounts

• the results of our audit carried out to ascertain whether the financialmanagement of the Office is sound

• whatever observations we consider necessary as to the appropriateness of theexisting budgetary and financial arrangements.

B. OPINION ON THE ACCOUNTS

1. ACCOUNTING RULES

3) In 2005, the EPO introduced IFRS, albeit subject to an exception in Article 1(3)FinRegs enabling it to net out its social-security liabilities against RFPSS assets.

4) In view of the revision of IFRS 9 (financial instruments) and IFRS 19 (employeebenefits), the EPO did away with the Article 1(3) FinRegs exception with effect from1 January 2011 (CA/D 5/11).

2. OPINION

5) We have been able to give an audit opinion without any reservations on the 2014accounts.

CA/20/15 e 1/118 150560004

6) The notes to the financial statements shed further light on specific aspects of the balance sheet.

C. OPINION ON MANAGEMENT

7) Our audit included not only the annual accounts but also management audits concerning in particular the financial situation, operations and the RFPSS. These have given rise to the following main findings.

1. FINANCIAL SITUATION

1.1. Financial reporting

8) The EPO revised its financial reporting procedure with effect from 1 January 2011, doing away with the exception under Article 1(3) FinRegs. As a result, its accounts as from 2011 are comparable under IFRS. As set out in CA/84/11, discontinuing the corridor approach and not netting out social-security assets and liabilities in the balance sheet mean that the annual result is subject to greater volatility.

1.2. Balance-sheet figures

9) As at 31 December 2014, non-current assets were approx. EUR 8 016m. Of the EUR 991m increase, EUR 855m came from RFPSS net assets and EUR 137m from bonds.

10) As at 31 December 2014, non-current liabilities amounted to some EUR 20 536m, including EUR 19 741m for defined benefit liabilities (for pensions and similar obligations). They were up EUR 8 721m on 2013, with defined benefit liabilities rising by EUR 8 667m.

11) Current assets fell by EUR 5m, while current liabilities went up by EUR 20m.

1.3. Economic situation, factoring in the present value of future national renewal fees

12) The present value of future national renewal fees cannot be shown under IFRS because there is no legal obligation to pay them.

CA/20/15 e 2/118 150560004

13) With no eligible future income to set against the EPO's long-term liabilities from its future business, its balance sheet looks rather lopsided. To counteract that, the present value of future national renewal fees needs to be borne in mind. The figures are taken from CA/60/15.

14) Each year up to 2011, net business assets and pension liabilities were in balance. The imputed shortfall is now EUR 9.8bn, reduced 2014 discount rates alone leading to a EUR 8.4bn increase in liabilities.

15) For a long-term view, see the actuarial valuation as at 31 December 2012 (CA/61/13) and the Office's comments on it (CA/62/13). An updated valuation is expected for 2015.

1.4. Income statement

16) At EUR -5m, the operating result is slightly negative but up EUR 36m on the 2013 figure. The main reason for this year's figure is that, while revenue rose by EUR 81m, employee benefit expenses increased by EUR 40m.

17) The financial result was EUR 156m, i.e. EUR 41m higher than in 2013.

18) The loss of EUR 7 907m under other comprehensive income can be attributed almost exclusively to the reduced discount rates (e.g. the discount rate for pension obligations fell from 3.89% to 1.61%).

1.5. Statement of cash flows

19) The inflow from operating activities is EUR 447m, the outflow from investing activities EUR 410m. Taking into account the EUR 6m outflow from financing activities, there has been a net increase of EUR 31m in cash and cash equivalents, i.e. up EUR 93m on the 2013 figure.

CA/20/15 e 3/118 150560004

1.6. Budget and forecasting accuracy

20) In CA/D 1/13, the AC adopted an authorisation budget within the meaning of Article 25(1)(a) FinRegs totalling EUR 2 079m. The actual outturn was EUR 2 048m, i.e. just 1.5% lower than the forecast value.

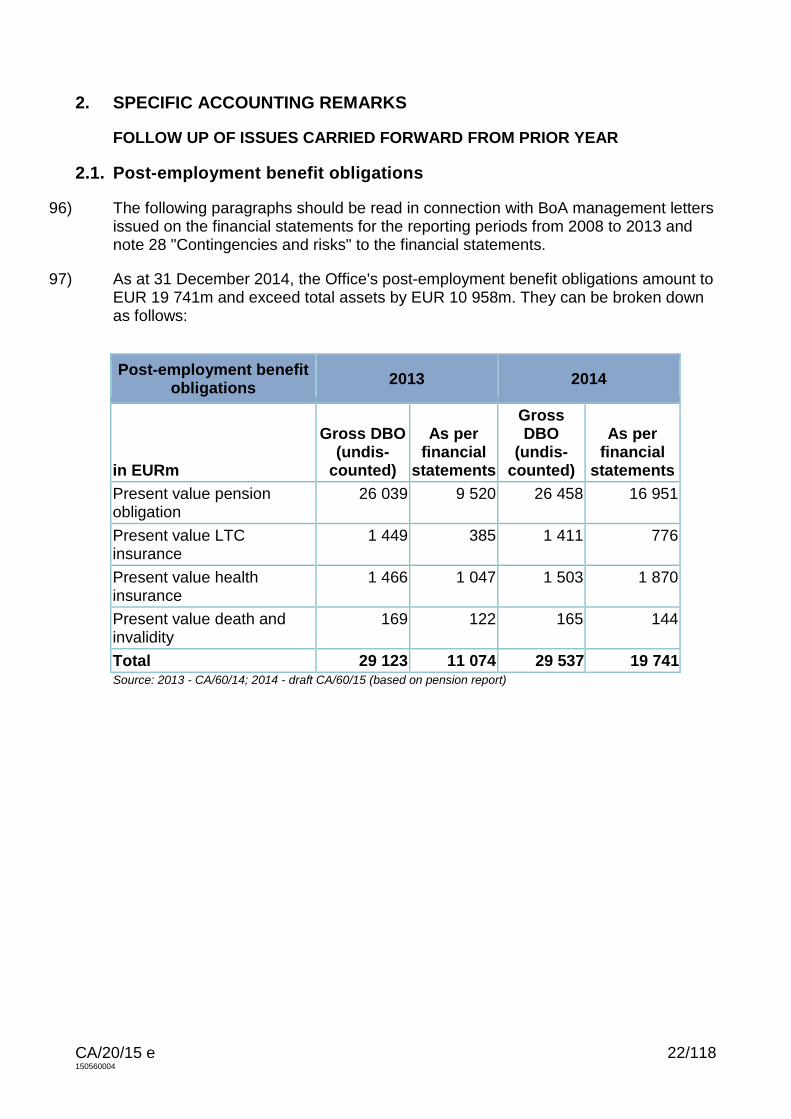

21) For the RFPSS, income is EUR 26m (7.9%) and expenditure EUR 21m (10.2%) under plan. The transfer to the RFPSS is nearly EUR 5m (3.9%) below the budgeted figure.

2. OPERATIONS

2.1. Comments on the accounts

22) The changes in schemes (return to tax adjustment, new career scheme, invalidity allowance) come into force after 2014 and so have no actual impact on the 2014 financial statements for accounting purposes.

23) Although the EPO is not a party to the legal proceedings, it is providing legal support to pensioners who have been approached by national tax authorities claiming taxes on partial compensation. In total, it knows of and is providing support in 361 cases (out of 1 149 recipients of partial compensation).

By re-introducing the former tax adjustment scheme, the Office has limited its risk exposure for future years.

24) In 2011, the IT Roadmap project was initiated to develop and implement improvements in the patent-granting process through integrated IT tools. The capitalised costs are EUR 33m (EUR 16.5m for IT systems and EUR 16.6m for construction in progress).

25) UNIP: the Office's costs at the current stage mainly comprise costs for IT set-up and administrative costs. These are accounted for in line with the Office's general accounting policies on capitalisation of development costs.

CA/20/15 e 4/118 150560004

The total costs of IT set-up for administration of requests and renewal fees, Micado adjustment and IT development for the unitary patent procedure are estimated to amount to EUR 2 533k. All other costs relating to process set-up, administration of the Select Committee and any other costs incurred by the Office are considered to be part of its ordinary business within its tasks under the EPC and are currently not separately measured by the Office.

26) To derive accurate and precise values for employee-related accruals, certain automated standard procedures and documentation should be in place. The information underlying related party disclosures should be documented in a consistent, reliable and auditable way.

2.2. Internal control system

(a) Internal Auditing

27) Internal Auditing (D 0.6.1) was the subject of an external quality assessment exercise, carried out by the German Institut für Interne Revision (internal audit institute - DIIR), which found that, in the main, its activities meet the standards laid down in the International Professional Practices Framework (IPPF) developed by the Institute of Internal Auditors (IIA).

(b) Governance of the RFPSS

28) On 23 December, a data import failure resulted in the Fund not becoming aware of a downgrade of a specific bond and thus in a passive breach. No procedures were in place to detect the consequence of the failure. Due to the failure on the 23 December, followed by the Office's closure over the Christmas holidays and on local public holidays, the portfolio managers only became aware of the downgrade and the passive breach on 7 January.

29) All other passive breaches during the year were minor and corrected in accordance with the relevant rule in the Code of Procedure.

30) Two years after introduction of the new governance framework, the roles of risk management and compliance management within the RFPSS Fund Administration and the Risk Assurance Officer / Compliance Assurance Officer are still evolving.

31) The strategic asset allocation including setting benchmarks gives a framework but also contributes to stability and long-term thinking. The maximum tracking error (as compared to the benchmark) is restricted by the Fund Administrator by asset class and is not often changed.

CA/20/15 e 5/118 150560004

2.3. Business administration

Review and internal appeals procedures

32) The Administrative Council asked the Board of Auditors to audit the Office's review and internal appeal procedures and how these had been implemented up to now.

33) The findings and recommendations are summarised in this report (CA/20/15). Report CA/21/15 gives more detailed information.

34) In 2013 and 2014 (until 24 November 2014) 535 cases with 3 777 requesters were registered for management review. 55% of the cases and 92% of the requesters are focused on regulations and/or policies.

The Appeals Committee registered 186 cases with 492 appellants in 2013 and 142 cases with 438 appellants in 2014 (until 24 November 2014). The list of registered cases includes 369 appellants in 2011 and 617 in 2012.

In 2013-2014 (up to 24 November 2014), final decisions taken by the President covered 170 cases and 573 requesters. 94% of the cases were rejected.

In 2013-2014 (up to 24 November 2014) 133 cases with 200 appellants were submitted to the ILOAT.

35) The average time between the start of an internal appeal and the final decision is 46 months for decisions taken in 2013 and 44 months for decisions taken in 2014.

36) The backlog of pending appeals as at 20 November 2014 covers 759 cases with 5 761 requesters. Most of the pending cases (356 cases with 1 542 requesters) are waiting for the position paper.

CA/20/15 e 6/118 150560004

37) The complexity of the system leads to duplicate work through registration in the Conflict Resolution Unit and in the Administrative Council.

There is no common tool and so a lack of interface with other units and a lack of harmonised categories.

There is a considerable backlog of internal appeals, as it takes a long time to draft the position paper.

The reasons for most requests and appeals concern policy decisions and regulations. The EPO's complaints management process was created for individual cases, not for mass requests / appeals. We recommend having separate procedures for individual cases for cases relating to policy decisions or regulations.

Patent grant process

38) The result of the "Early Certainty from Search" procedure, implemented on 1 July 2014, was a change in product prioritisation for DG 1. The key element of the procedure is that search files need to be processed in time (Priority 1 files).

There is a downward trend in the backlog of products under priority 1 files, even if not all clusters had met the backlog-reduction target by the end of 2014.

39) In most areas, the number of new requests is greater than the number of examiner products.

40) The average patent grant time of the different clusters cannot be easily compared due to individual problems, complexity and sector-related differences that have to be taken into account.

41) The examiners receive different PAX points for the different products. These points are required in order to meet individual targets. Search files obtain a value of 0.6 points while examination files receive 0.4 points, which promotes the reduction of the backlog for search files.

However examination files are needed in order to meet the target of the Office, which is measured in publications.

CA/20/15 e 7/118 150560004

Since many examination files need more time and also bring fewer points for the examiners than search files, the search files may be preferred.

42) The quality dashboard is well suited as a management system for promoting positive development of the key performance indicators (KPIs) as the transparency is given.

43) Furthermore, a new performance management system is planned. Currently there is no linkage between the new performance system and the KPIs. It should be considered whether files with a long processing time should receive more points.

Tender procedures

44) The best practice comparison shows that EPO procurement is mainly focused on the "how" (the process) and not on the "what". The EPO procurement organisation (CP) is mainly focused on the selection and contracting process while limited attention is paid to the more strategic processes of the Strategic Sourcing Cycle. The contract management function is scattered throughout the organisation without the support of clear KPIs and relevant systems.

45) There is no standardised process for approvals or a workflow procedure which states what approvals are needed and what kind of documents have to be used.

46) Currently, a strategic supplier performance management process to manage the risk, quality and performance of the suppliers is only partially in place.

47) There is no common system used for purchasing. Co-ordination between the business units and procurement takes place through various systems.

IT procurement

48) The EPO is in the process of professionalising its procurement function. Currently the procurement function is partially decentralised in terms of categories (e.g. IT, buildings, HR, etc.).

CA/20/15 e 8/118 150560004

Currently, a strategic supplier performance management process to manage the risk, quality and performance of the suppliers is only partially in place.

Supplier risk evaluation is performed during the tender only, and Finance is not involved in this evaluation.

Responsibility for licence management lies with PD Service Operations but seems to be scattered throughout the organisation.

49) There is a realistic possibility that the current supplier base does not offer the most effective solutions for the EPO (mismatch of the current supplier base) for the following reasons.

• There is limited alignment between the EPO's business, procurement and IT strategies

• Central Procurement has a limited focus on strategic sourcing processes such as performing supply market analyses, developing category strategies, etc., in order to create the best fit with the supplier base.

• The complex and rigid selection processes and the rigid terms and conditions seem to deter some potentially suitable suppliers because the risks and the cost of sales are too high in comparison with the value that can be generated from the projects. This could lead to a narrow selection of potential suppliers and a mismatch of the current supplier base.

2.4. IT

(a) IT Roadmap

50) The IT Roadmap 2011-2015 (CA/46/11) was presented at the Administrative Council's June 2011 meeting and set out the strategic directions for IT at the EPO.

In addition to achieving efficiency gains, the IT roadmap objectives include provision of services to external users and a reduction in the running and maintenance costs of IT. As a result, (further) implementation of the new case management (CMS) system to facilitate the re-engineered patent grant process is a key element. Compared with the original schedule in the IT roadmap, CMS implementation is facing a delay of approximately 18 to 24 months. At this point, further delay will start to jeopardise the scheduled completion date of late 2017.

CA/20/15 e 9/118 150560004

51) The quality of the IT Roadmap is periodically assessed and reported on by "Project Services". The QA report of October 2014 shows that the projects within stream I are facing challenges, with 7 out of 10 assessed projects reported to have quality issues or be outside tolerance. Additionally, 5 out of 10 projects are beyond their planned stage end date.

We noted that executive reports on the status of the individual projects are being issued every two weeks. Detailed project status reports are applied for most projects (and especially for projects running in exception), but not for all projects within the IT roadmap.

52) It is indicated that the IT Roadmap programme is an effective and efficient structure for developing and managing enhancements from a business perspective. However, the goals set within IT roadmap ("leading edge" technology) may limit the ability to determine a fixed end goal.

Current financial figures do not include all costs incurred during the transition phase (as clearly highlighted in CA/46/14).

The forecasts and expenditures are budgeted and accounted for in the yearly budget cycle and agreed within the Council. As a result, the financial expenditure is principally managed from a "year-to-year" perspective rather than a "program" perspective.

(b) IT security

53) Escalation rules and clear guidelines on responsibilities are not formally defined. Drafted documentation of the current IT security project may address the deficiency.

The risk assessment process is only applied to newly initiated projects, thus not considering security requirements for the existing systems and information unless they are further developed or replaced within a project.

Inconsistencies and uncertainties in terms of classification exist between the policies and the completed risk assessment templates.

CA/20/15 e 10/118 150560004

54) The EPO has no complete documented overview of information assets and the logical (e.g. applications) and physical assets (e.g. servers) containing / dealing with the information assets. Thus, related risks may not have been identified to their full extent.

2.5. Buildings

(c) Building investments in The Hague

55) Project Organisation

• The President has delegated the chair of the Steering Committee to VP 4 and will only participate when important aspects arise.

• The project is regularly audited by an external Quality Assurance. The complex process for obtaining EPO-internal authorisation for a variation order (11 working days) is going to be simplified for minor cases.

56) Progress of project and time schedule

57) There is a delay of approx. four months due to asbestos and a late delivery of planning. The building is expected to be completed in August 2017 (or even earlier) and the project is expected to be completed in May 2019.

58) Project risks

• Project risks have been identified and documented in the risk log, which is updated regularly. Responsibilities are defined and mitigation actions are assigned.

(d) Other building activities

59) Vienna

• The planned completion date is April 2015 for interior work and May 2015 for work outside the building. The expected costs are line with the amounts in the contracts (EUR 2.3m).

CA/20/15 e 11/118 150560004

60) Berlin

• Interior renovation and improvements concerning room climate, security and the entrance area are necessary (see building roadmap, CA/73/11). Most of the costs will be paid by the Federal Republic of Germany. The costs for the EPO are limited to EUR 6m (excluding VAT).

61) Other

• No major projects. Surveys of the roof of the Isar building and the underground car park in the PschorrHöfe are planned. The lease contract for the Capitellum building in Munich was terminated in 2015.

(e) Benchmarking building cost

62) The expenses for offices used by the EPO are in line with previous years, and no new material information was obtained as a result of the audit. As the approach used was identical to the approach in 2012, we have chosen not to include the full report this year.

CA/20/15 e 12/118 150560004

II. DETAILED REPORT

A. PRELIMINARY REMARKS

63) The Board of Auditors of the European Patent Organisation (hereinafter "the Board") reports herewith under Article 79 of the Financial Regulations (FinRegs) on the 2014 accounting period.

64) The accounts reached us in good time before 31 March 2015, in compliance with Article 70 FinRegs.

65) Under Article 75 FinRegs and following a public invitation to tender the Board also commissioned certain work from the following audit firms:

• KPMG Deutsche Treuhand-Gesellschaft Aktiengesellschaft Wirtschaftsprüfungsgesellschaft, D - Munich (for audit of EPO accounts, business administration and IT)

• BDO AG Wirtschaftsprüfungsgesellschaft, D - Hamburg (for buildings and RFPSS)

66) Pursuant to Article 76(2) FinRegs the checks were intended in particular to establish whether:

• the terms of the budget and other budgetary provisions were adhered to • the annual accounts as defined in Article 69 FinRegs were properly

substantiated and all transactions properly recorded • securities and cash on deposit and in hand accorded with the amounts in the

cash accounts • procedures were efficient and economical and whether work could be

performed more efficiently with fewer staff or other resources, or in other ways.

67) Pursuant to Article 7(1)(c) of the Regulations for the Reserve Funds for Pensions and Social Security (RFPSS), we recommend that the Fund Administrator be discharged in respect of the 2014 accounting period. For our comments on the RFPSS, see Section I.C.2.1 in the Executive Summary and Section II.D.2 in the detailed report below.

68) In accordance with Article 76 FinRegs, the Board or the above firms carried out checks on the EPO premises in Munich, The Hague, Berlin and Vienna. Petty cash at all sites was closed before 1 January 2014.

69) We would like to take the opportunity to thank the President and the EPO staff consulted for their help and constructive co-operation.

CA/20/15 e 13/118 150560004

B. AUDIT OPINION

We have audited the financial statements, comprising the statement of financial position, statement of comprehensive income, statement of changes in equity, statement of cash flows and notes (Article 69(1)(a) of the Financial Regulations), together with the bookkeeping system of the European Patent Organisation (EPO), Munich, for the accounting period 1 January to 31 December 2014 – as disclosed in CA/60/15. Responsibility for maintaining books and records and preparing the financial statements in accordance with Article 50(g) of the European Patent Convention (EPC) and the Financial Regulations (FinRegs), as described in Section 2.1 of CA/60/15 ("Basis of Preparation"), lies with the President of the Office. Under Article 1(3) FinRegs, the EPO's generally accepted accounting principles are the International Financial Reporting Standards (IFRS) as promulgated by the International Accounting Standards Board (IASB).

We conducted our audit of the financial statements in accordance with Article 49 EPC and the appropriate regulations of the FinRegs – especially Article 79 FinRegs – and drawing on the audit principles adopted by Germany's Institut der Wirtschaftsprüfer (= institute of auditors). Those standards require that we plan and perform the audit such that misstatements materially affecting the presentation of the net assets, financial position and results of operations in the financial statements in accordance with the applicable accounting provisions of the FinRegs are detected with reasonable assurance. Knowledge of the business activities and the economic and legal environment of the EPO and expectations as to possible misstatements are taken into account in the determination of audit procedures. The effectiveness of the accounting-related internal control system and the evidence supporting the disclosures in the books and financial statements are examined primarily on the basis of sample checks within the framework of the audit. The audit includes assessing the accounting principles used and significant estimates made by the President of the EPO, as well as evaluating the overall presentation of the annual financial statements. We believe that our audit provides a reasonable basis for our opinion.

Our audit has not led to any reservations.

In our opinion, based on the findings of our audit, the financial statements comply with IFRS as promulgated by the IASB and give a true and fair view of the net assets, financial position and results of operations of the EPO in accordance with these standards.

Munich, 20 April 2015

The Board of Auditors

H. Schuh O. Hollum F. Angermann

CA/20/15 e 14/118 150560004

C. COMMENTS ON THE ACCOUNTS

1. THE ORGANISATION'S FINANCIAL AND ECONOMIC POSITION

1.2. Introductory remarks

70) Every BoA report analyses the EPO's financial situation. Our task under Article 79 FinRegs of ascertaining whether its financial management is sound involves not only verifying compliance with the "three Es" (efficiency, effectiveness and economy) but also scrutinising the EPO's specific self-financing model. The EPO has to manage its resources in such a way that it does not need to call on the member states' guarantee.

71) In CA/D 5/11 the Administrative Council did away with the Article 1(3) FinRegs exception, with retroactive effect from 1 January 2011. So the EPO now has to apply in their entirety the accounting principles issued by the International Accounting Standards Board.

72) This change in its financial-reporting procedure has two major effects: (a) the RFPSS assets (now valued according to IFRS 9) are shown as assets and the DBO as a liability, which leads to significantly higher total assets and liabilities; (b) the "corridor" approach, used when accounting for financial and actuarial fluctuations in the liabilities and assets of the social-security schemes, has been discontinued, making the annual accounts much more volatile.

A third change relates to the valuation of some of the Office's assets under IFRS 9, but this has had little impact on the accounts.

73) In order to show, nevertheless, the long-term trend in the EPO's financial position, we have based our report on restated (and therefore unaudited) annual accounts for 2005-2009 provided by the Office. This takes account of discontinuing the corridor approach and no longer offsetting the DBO against RFPSS assets, but not of revaluations of the Office's assets under IFRS 9.

CA/20/15 e 15/118 150560004

74) The 2014 estimates and figures are based on CA/60/15 (financial statements) and CA/10/15 (budget implementation statement).

75) For the detailed balance-sheet and income-statement figures, see Annexes I/1 and I/2 taken from CA/60/15. Annex III compares the budget estimates as adopted in 2012 and subsequently restated ("IFRS forecast") with actual income and expenditure as per CA/10/15.

1.3. Financial-statement figures in brief

(a) Balance sheet

-25.000.000

-20.000.000

-15.000.000

-10.000.000

-5.000.000

0

5.000.000

10.000.000

15.000.000

EQUITY ASSETS LIABILITIES

(EUR '000) 2010 2011 2012 2013 2014Non-current assets 5.262.222 5.427.877 6.256.840 7.024.503 8.015.868Current assets 546.811 577.364 673.345 772.878 767.374Assets 5.809.033 6.005.241 6.930.185 7.797.381 8.783.242Non-current liabilities -7.220.781 -7.447.778 -11.513.459 -11.814.884 -20.535.860Current liabilities -570.070 -547.745 -559.382 -567.353 -587.538Liabilities -7.790.851 -7.995.523 -12.072.841 -12.382.237 -21.123.398Equity -1.981.818 -1.990.282 -5.142.656 -4.584.856 -12.340.156

CA/20/15 e 16/118 150560004

76) Non-current assets rose by EUR 991m from 2013 to 2014. RFPSS net assets accounted for EUR 855m, bonds for another EUR 137m.

77) Non-current liabilities were up by EUR 8 721m, an exceptionally large increase over the 2013 figure, with defined benefit liabilities (for pensions and similar obligations) rising by EUR 8 667m.

78) Current assets fell by EUR 5.5m, financial assets going down by EUR 35m and cash assets up by EUR 30m.

79) Current liabilities were up by EUR 20m.

80) The combined effect of these changes is that negative equity increased by EUR 7 755m, from EUR -4 549m to EUR -12 340m.

Non-current liabilities

81) As at 31 December 2014, non-current liabilities amounted to some EUR 20 536m, including EUR 19 741 for defined benefit liabilities.

82) The latter can be shown as follows:

(EUR '000) Active staffStaff entitled to deferred pension Pensioners Total

Pension liability 12.976.454 59.057 3.915.240 16.950.751LTC insurance 540.746 4.724 230.150 775.620Health insurance 1.363.917 506.641 1.870.558Death and invalidity 144.027 144.027Total 15.025.144 63.781 4.652.031 19.740.956

CA/20/15 e 17/118 150560004

83) The pension liability (EUR 16 951m) breaks down as follows:

84) The considerable increase in defined benefit liabilities is almost entirely attributable to heavily reduced discount rates.

85) The calculations in CA/60/15 (section 20.1) show that a 1% increase in the discount rate would reduce defined benefit liabilities by EUR 4 451m, whereas a 1% reduction would increase them by EUR 6 277m.

86) Despite heavily reduced discount rates, the following parameters were the same as in 2013, except that for medical costs, which increased only very slightly:

(EUR '000) 2010 2011 2012 2013 2014Pensions 4.402.511 4.611.919 7.371.651 7.415.948 13.344.298Tax adjustment / partial compensation 971.533 1.006.295 1.598.686 1.602.267 2.851.942Invalidity allowances 237.574 202.042 281.424 270.498 389.299Familiy allowances 150.925 159.310 231.978 230.877 365.211Total 5.762.543 5.979.566 9.483.739 9.519.590 16.950.750

Discount rate 2010 2011 2012 2013 2014Pension liability 5,33% 5,38% 3,57% 3,89% 1,61%LTC insurance 5,44% 5,55% 3,77% 4,10% 1,75%Health insurance 5,34% 5,51% 3,55% 3,90% 1,61%Death and invalidity 4,75% 4,56% 2,89% 3,17% 1,32%

(EUR '000) Liability 1% increase 1% decreasePensions 16.950.751 13.219.586 22.198.320LTC insurance 775.620 568.800 1.082.339Health insurance 1.870.558 1.370.893 2.577.539Death and invalidity 144.027 130.714 159.591Total 19.740.956 15.289.993 26.017.789

Difference 0 -4.450.963 6.276.833

Inflation 2010 2011 2012 2013 2014Future salary increases 2,50% 2,50% 2,50% 2,50% 2,50%Future pension increases 2,50% 2,50% 2,50% 2,50% 2,50%Medical costs 3,20% 3,10% 3,10% 3,20% 3,10%

CA/20/15 e 18/118 150560004

(b) Economic situation, factoring in the present value of future national renewal fees

87) The present value of future national renewal fees cannot be shown under IFRS, because there is no legal obligation to pay them.

88) With no future income to set against long-term liabilities from future business, the balance sheet looks rather lopsided. To counteract that, the present value of future national renewal fees needs to be borne in mind. The figures below are from CA/60/15.

89) Until 2011, net business assets and pension liabilities were more or less in balance. The shortfall, which was between EUR 2 and 3bn in 2012 and 2013, increased in 2014 to almost EUR 10bn.

0,00%

1,00%

2,00%

3,00%

4,00%

5,00%

6,00%

Pension liability Future salary increases

(EUR '000) 2010 2011 2012 2013 2014RFPSS net assets 3.978.966 3.934.618 4.622.017 5.229.485 6.084.859Present value of future national renewal fees 2.839.901 3.142.273 3.490.544 3.647.126 3.876.977Net business assets 6.818.867 7.076.891 8.112.561 8.876.611 9.961.836Defined benefit liabilities -6.625.315 -6.808.831 -10.825.416 -11.074.231 -19.740.956Balance 193.552 268.060 -2.712.855 -2.197.620 -9.779.120

CA/20/15 e 19/118 150560004

90) Compare the present value of future national renewal fees with equity, and a similar picture emerges:

91) For a long-term view, see (as in the 2013 report) the joint report of the Actuarial Advisory Group to the EPO President - actuarial valuation as at 31 December 2012 (CA/61/13) and the Office's comments on it (CA 62/13). Estimates based on actuarial studies have shown that net payments from the RFPSS to pensioners are not expected before 2023. These studies are expected to be updated in 2015.

(c) Income statement

(EUR '000) 2010 2011 2012 2013 2014Equity -1.981.818 -1.990.282 -5.142.656 -4.584.856 -12.340.156Present value of future national renewal fees 2.839.901 3.142.273 3.490.544 3.647.126 3.876.977

858.083 1.151.991 -1.652.112 -937.730 -8.463.179

-2.000.000

-1.500.000

-1.000.000

-500.000

0

500.000

1.000.000

Profit / loss Operating result Financial result

CA/20/15 e 20/118 150560004

92) The 2014 operating result, whilst remaining slightly negative, is up by EUR 37m on the 2013 figure, with income increasing by EUR 83m and expenditure by EUR 46m.

93) The positive financial result of EUR 156m is around EUR 41m higher than the 2013 figure, with revenue increasing by around EUR 87m and expenses by around EUR 46m.

94) The loss of EUR 7 906m under other comprehensive income is down to heavy reductions in discount rates for valuation of DBOs and can be broken down as follows:

(d) Statement of cash flows

95) The inflow from operating activities is EUR 447m, the outflow from investing activities EUR 410m. Taking into account the EUR 6m outflow from financing activities, there has been a net increase of EUR 31m in cash and cash equivalents, i.e. up EUR 93m on the 2013 figure.

(EUR '000) 2010 2011 2012 2013 2014Operating result 89.788 89.232 110.824 -42.028 -5.180Financial result 57.370 -463.905 215.762 115.479 156.247Profit / loss for year 147.158 -374.673 326.586 73.451 151.067Other comprehensive income -295.630 366.209 -3.478.960 484.349 -7.906.367Total comprehensive income -148.472 -8.464 -3.152.374 557.800 -7.755.300

(EUR'000)

Revised financial assumptions

Revised demographic assumptions

TotalPension obligation -7.050.830 262.493 -6.788.337LTC insurance -387.702 25.866 -361.836Sickness insurance -943.939 197.769 -746.170Death and invalidity -23.155 13.131 -10.024Total -8.405.626 499.259 -7.906.367

2011 2012 2013 2014Cash flows from operating activities 379.269 407.370 376.721 446.953Cash flows from investing activities (299.867) (401.558) (436.117) (410.439)Cash flows from financing activities (13.272) (9.824) (3.344) (5.964)NET INCREASE/DECREASE IN CASH AND CASH EQUIVALENTS 66.130 (4.012) (62.740) 30.550

CA/20/15 e 21/118 150560004

2. SPECIFIC ACCOUNTING REMARKS

FOLLOW UP OF ISSUES CARRIED FORWARD FROM PRIOR YEAR

2.1. Post-employment benefit obligations

96) The following paragraphs should be read in connection with BoA management letters issued on the financial statements for the reporting periods from 2008 to 2013 and note 28 "Contingencies and risks" to the financial statements.

97) As at 31 December 2014, the Office's post-employment benefit obligations amount to EUR 19 741m and exceed total assets by EUR 10 958m. They can be broken down as follows:

Source: 2013 - CA/60/14; 2014 - draft CA/60/15 (based on pension report)

Post-employment benefit obligations 2013 2014

in EURm

Gross DBO (undis-

counted)

As per financial

statements

Gross DBO

(undis-counted)

As per financial

statements Present value pension obligation

26 039 9 520 26 458 16 951

Present value LTC insurance

1 449 385 1 411 776

Present value health insurance

1 466 1 047 1 503 1 870

Present value death and invalidity

169 122 165 144

Total 29 123 11 074 29 537 19 741

CA/20/15 e 22/118 150560004

98) We draw attention to the following major assumptions and uncertainties:

(a) Decrease in interest rate

99) According to IAS 19, the interest rate used for discounting the defined benefit obligations ("DBO") is determined by reference to market yields at the end of the reporting period. In the case of the Office, it is based on the "iBoXX EURO Corporates AA" index and therefore subject to general market fluctuations. The determination of the discount rate applied by the Office is in line with the requirements of IAS 19.

100) The discount rate used as of 31 December 2014 amounts to 1.61% for pension obligations and has decreased from 3.89% in 2013. This net decrease is the main reason for the actuarial losses / remeasurements of EUR 7.906m that have caused a further decline in equity. We consider the discount rate used by the Office appropriate. The method used for determining the rate has been applied consistently. Nonetheless it is at the lower end of the range of acceptable rates. Benchmark studies of the discount rates used by listed companies in Germany as at 31 December 2014 indicate a range between 1.6% and 2.4%.

101) These movements in equity are triggered by market parameters outside the EPO's control (accounting "mechanics"). Since 2013, it has no longer been possible to choose how to recognise actuarial losses for accounting purposes, i.e. these have to be recognised in the comprehensive income ("below net income") and, consequently, in equity.

(b) Increase of service costs 2015

102) The decrease in the discount rate does not have any impact on the 2014 operating result. However, due to the mechanics of IAS 19, in 2015 current service costs are projected to increase by EUR 416m to EUR 845m, which might lead to a negative operating result under IFRS for 2015. Obviously, the low discount rate will have a positive impact on the 2015 financial result as the interest costs are projected to decrease from EUR 367m to EUR 272m.

CA/20/15 e 23/118 150560004

(c) Update of mortality tables

103) The Office's actuary, SIRP, has drawn up updated mortality tables based on actual mortality rates of twelve international organisations located in Europe during the observation period 2008 – 2012 as well as mortality tables for four European countries. These updated tables have been used by the Office to determine its pension obligation at the end of 2014. The 2014 actuarial gain of EUR 499m from changes in demographic assumptions mainly relates to this update in the mortality tables. In line with the requirements of IAS 19, the change in mortality tables has been treated as actuarial gain / loss presented as "remeasurement of defined benefit obligations" in the statement of comprehensive income.

(d) Medical cost inflation

104) Medical cost inflation has to be included in the calculation of health insurance. Based on the actuarial report, there has been a change in the estimate of long-term medical cost expectations. The overall impact of the change in estimate is not material. However, the Office could improve the documentation on development and trend of medical cost inflation.

2013 2014

in EURm

As per financial

statements

One month increase in

life expectancy

As per financial

statements

One month increase in life

expectancy Present value pension obligation

9 520 9 555 16 951 16 963

Present value LTC insurance

385 387 776 777

Present value health insurance

1 047 1 049 1 870 1 873

Present value death and invalidity

122 - 131 -

Total 11 074 10 991 19 741 19 613

CA/20/15 e 24/118 150560004

(e) Impact from changes in schemes

(i) Return to tax adjustment

105) The Office proposed the replacement of the partial compensation scheme by the former tax adjustment (CA/95/14 Rev. 1) in place until 31 December 2008. The proposal was approved by the BFC and Administrative Council at their meetings in November and December 2014, respectively. It will apply from 1 January 2015 onwards to all pensioners who took up active service before 1 January 2009. There has no impact on the financial statements as, for accounting purposes, the Office had treated the partial compensation in accordance with the former tax adjustment rules (in place until 31 December 2008).

106) We concur with the accounting treatment applied by the Office and draw attention to the disclosures in note 28 describing the contingent liability and uncertainties. Moreover, we highlight that the matter is primarily a legal and political issue.

107) Regarding the measurement of the tax adjustment, please refer to paragraph (f) below.

(ii) New career scheme

108) In CA D/10/14, the Administrative Council decided to amend the Service Regulations on remuneration. The new scheme will apply from 1 January 2015 onwards and is relevant for financial reporting in the following respects:

• The actuarial calculation of the DBO includes an estimate of future salary increases (estimating the salary of the employee upon retirement) which takes account of promotions, as these are considered "regular" at the EPO. Under the proposed new career scheme, regular promotions based on seniority will be replaced by a more performance-based scheme. The Office currently assesses the impact on the DBO as low, because under the new career scheme, salary increases might only slow down but not significantly change the salary upon retirement for the active employees as at 31 December 2014. No past experience is available regarding actual promotion patterns and therefore no sufficiently reliable estimate - better than the already observable pattern under

CA/20/15 e 25/118 150560004

the old scheme - is possible. According to IFRS, such a change in plan must be immediately recognised through P/L. However, based on the arguments above, any change (through P/L) would be too aggressive. We consider this an acceptable estimate of the Office.

• Moreover, a bonus scheme will be implemented to reward exceptional performance. The bonus will not give rise to any pension entitlement and will therefore not increase any pension obligation. The bonus element does not have any impact on the 2014 financial statements but has to be analysed for the purposes of recognising an accrual at the end of 2015.

109) We concur with the approach taken by the Office for the 2014 accounts. In the long run, the change in scheme might lead to a decrease in pension obligations and payments to the RFPSS.

(iii) Invalidity allowance

110) At its meeting in March 2015, the Administrative Council approved the amendments to the Service Regulations (ServRegs) and Pension Regulations (PenRegs) on invalidity and sick leave (CA/14/15). In accordance with the requirements of IFRS, the Office has appropriately disclosed this event in its notes to the financial statements (note 32). The change in the invalidity and sick-leave scheme does not have an adjusting impact on the measurement of the defined benefit obligations recognised in the statement of financial position. In the long run, it will impact on the estimate of invalidity probabilities and therefore potentially reduce the liability for post-employment benefit obligations, as entitlement to an invalidity allowance has been restricted.

(f) Tax adjustment on invalidity allowance and partial compensation

111) The Office faces several uncertainties in connection with the taxability of pensions and invalidity allowances. By re-introducing the former tax adjustment scheme in place until the end of 2008, the Office has taken measures to limit its risk exposure. The future treatment and therefore the reflection in the defined benefit obligation is described in section (e)(i) above. The risk exposure for the periods from 2009 until

CA/20/15 e 26/118 150560004

2014 has not been accounted for in the financial statements as at 31 December 2014. It is limited to cases of pensioners / invalids who have been subject to national taxation in their country of residence and are claiming reimbursement from the Office. The different categories can be summarised as follows:

(i) Taxation of invalidity allowance

112) In 2007 (CA/D 30/07) the EPO decided to significantly change its PenRegs and ServRegs with regard to invalidity benefits, with effect from 1 January 2008 to 31 December 2014. In substance the obligation for invalidity benefits due to invalids ("non-active staff") did not include any specific rules on tax adjustments on invalidity allowance.

113) For accounting purposes, the invalidity allowance and its corresponding tax adjustment were treated as post-employment benefit plan, as – based on past experience – there were very few exceptional cases of invalids coming back to work once the invalidity status was granted. A tax adjustment (for measurement, please see paragraph g) below) had been included in the provision recognised, however no such tax adjustment had been paid.

114) The taxability of the invalidity allowance is governed by the national tax laws in the country in which non-active staff are resident for tax purposes and might therefore be taxable. Some non-active staff in receipt of an invalidity allowance have been approached by tax authorities that consider the allowances to be taxable income. The EPO is supporting such staff in 84 cases, 58 of them in Germany and 26 in the Netherlands. In Germany, two court cases are still pending. In both cases, there was an adverse judgment at first instance which is now under appeal (one appeal lodged with the Bundesfinanzhof, the supreme German tax court), i.e. the courts of first instance have endorsed the tax authorities' classing of invalidity allowances as taxable income.

115) In the Netherlands, a judgment of the Hague District Court published in February 2015 declared the invalidity allowance paid to a Dutch claimant from 1 January 2008 to be an emolument within the meaning of Article 16(1) PPI and consequently exempt from national income tax. The tax office lodged an appeal in March 2015.

CA/20/15 e 27/118 150560004

116) Further actions depend on the outcome of the negotiations with the national tax authorities and of pending legal proceedings between invalids and national tax authorities.

117) We concur with the approach taken by the Office for the end of the 2014 accounting period. The overall risk exposure is not expected to be material for the Office (in total only 149 recipients of an invalidity allowance and risk exposure limited to period from 2009 to 2014).

(ii) Obligation of the EPO to reimburse the invalid for any tax paid under national tax regulations:

118) Contrary to the pension scheme (as stipulated in the PenRegs), which lays down a right to reimbursement and a formula for the amount of tax adjustment for employees recruited before 1 January 2009, the invalidity allowance plan applicable from 2009 until 2014 (as stipulated in the ServRegs) remained silent on tax adjustments. However, triggered by the requests from national tax authorities, invalids have contacted the Office in this matter and the Office assumes that there is a significant risk that a majority of the well-interconnected invalids will claim a tax reimbursement from the Office if the local tax authorities prevail in their assessment that the invalidity allowance is taxable. Precedents have been set since 2009, when the Office began supporting invalids in their negotiations with tax authorities.

119) The Office has taken countermeasures by changing the scheme (see paragraph (e)(iii) above), as it considered the risk exposure to be very high that all current invalids and all potential future invalids with a date of entry before 1 January 2009 will actually have to pay national income tax and then claim reimbursement.

120) The Office has continued to support invalid staff in legal and court proceedings and has paid them advances on their current tax payments. It has paid approximately EUR 206k to invalids in 2014. The amount is presented in the line item "Other receivables – staff and related accounts". These payments have neither been charged as expenses nor presented as utilisation of provisions, but have been capitalised as other assets.

CA/20/15 e 28/118 150560004

121) The Office will deal with all cases for the period 2009 to 2014 on an individual, i.e. case-by-case, basis. We concur with the approach taken by the Office for the end of the 2014 accounting period. The overall risk exposure is not expected to be material for the Office (in total only 149 recipients of invalidity allowance and risk exposure limited to period from 2009 to 2014).

(iii) Taxation of partial compensation

122) Although the EPO is not a party to the legal proceedings, it provides legal support to pensioners who have been asked to pay taxes on partial compensation by national tax authorities. In total, the Office knows of and is supporting pensioners in 361 cases (out of 1 149 recipients of partial compensation). These mainly concern pensioners resident in Germany (186), the Netherlands (104), Belgium (68) and, to a lesser extent, Luxembourg. Legal proceedings are pending in all these countries. Only in Luxembourg has a final court decision has been published concluding tax exemption. In Belgium and Germany, court proceedings are pending either at first instance or on appeal. In a judgment of 26 February 2015, concerning a Dutch pensioner, the Hague District Court found the partial compensation payment to be exempt from national tax in the member states according to Article 16(1) PPI. The Office maintains its position that no reimbursement of taxes paid on partial compensation will be made to pensioners, as there is no legal or constructive obligation. The Office is currently analysing whether agreements with the respective member states can be reached to settle the period from 2009 to 2014. Discussions are ongoing with all major countries concerned. As in previous periods, the Office has not recognised any liability regarding the potential risk of pensioners claiming reimbursement for national taxes paid on partial compensation when relying on Article 16(1) PPI, i.e. the non-taxability of partial compensation.

123) The Office considers the risk of any obligation remote and not reliably measurable at this stage, because it depends on:

• first, the outcome of legal proceedings between pensioners and national tax authorities, and

• second, an assessment regarding the obligation of the Office based on then prevailing regulations and measures.

CA/20/15 e 29/118 150560004

124) The proceedings could continue for several years. It cannot be excluded that liability might have to be recognised in future.

125) By re-introducing the former tax adjustment scheme, the Office has limited its risk exposure for future years. The Office will deal with cases for the period from 2009 to 2014 on an individual basis.

(iv) Salary savings plan

126) All staff joining the Office from 1 January 2009 are compulsorily members of the "salary savings plan", a deferred compensation model. The contributions are paid by the Office (two thirds) and the employees themselves (one third) and are subject to internal tax under Article 16(1) PPI. Consequently, the Office takes the position that no national tax can be additionally levied and has not provided for any potential risk for reimbursement of taxes as at 31 December 2014. The Office aims to reach an agreement on the taxability of the salary savings plan in the context of overall discussions with national tax authorities. Given that the corresponding obligation as at 31 December 2014 amounts to EUR 30 166k, any potential impact from tax adjustment is considered immaterial, but may become material over time and as more and more employees join the scheme.

(v) Summary

127) Regarding all three cases (tax adjustment on invalidity allowance, partial compensation for pensioners and salary savings plan), we concur with the accounting position taken by the Office. No provision has been recognised, as the risk is considered remote (probability below 50%), but extensive and appropriate descriptions of the risks have been provided in note 28 "Contingencies and Risks" to the financial statements in line with requirements stipulated in IAS 37.86 for contingent liabilities.

(g) Valuation of the tax adjustment / partial compensation

128) For valuation purposes regarding the tax adjustment on invalidity allowance, the Office has not undertaken a detailed assessment regarding the country of tax-residence of non-active staff/pensioners and their marital status, but has taken a "loading factor" of 19% and 21% on the defined benefit obligation regarding current and future invalids/pensioners respectively. In 2008, these factors have been derived

CA/20/15 e 30/118 150560004

by using past experience of tax adjustments actually paid in relation to retirement pensions. No update of these factors has been undertaken since 2008 as they are still considered valid. So, for accounting purposes, the Office assumes that the country of residence in the case of invalidity/retirement mirrors the country of residence of EPO's retired workforce and the amount of tax adjustments to be reimbursed corresponds to the amount that would have to be paid on a corresponding retirement pension. A sanity check of the actual payments for partial compensation made in 2014 (based on most recent information for actual payments from 2009 until 2014) versus the basis pension payments lead to a factor of 20.9% (2013: 21.4%). The actual payment for partial compensation is based on PenRegs and derived from theoretical national income tax according to the Inter-Organisations Section of the Co-ordinated Organisations, considering the fiscal situation of the beneficiaries regarding marital status and country of residence.

129) We concur with the position taken by the Office, but highlight the level of estimate involved and recommend an annual analysis of the appropriateness of the loading factor for both invalids/pensioners and active staff.

2.2. Repurchase value Caisse Nationale de Prévoyance (CNP)

130) In its capacity as legal successor of the Institut International des Brevets ("IIB"), the Office accounts for the repurchase value of funds of former IIB-members for pension payments as well as outstanding interest thereon of EUR 55.7m (31 December 2013: EUR 54.4m). The increase is due to accrued interest for 2014. Since July 2007 no payments or reimbursements have been made by CNP to the Office. The amount is confirmed by CNP in its yearly statement provided to the EPO. Since 2000, the EPO has aimed to have these funds transferred from Caisse Nationale de Prévoyance ("CNP") to the Office, with a subsequent contribution to the RFPSS. The Office has terminated the contract with CNP, negotiations have been held and a conclusion had almost been reached in 2007, subject to all ex-IIB members concerned approving the transfer (condition set by CNP). Progress has been made and approval has been obtained from all relevant ex-IIB members in the meantime. An internal legal analysis performed by the Office in 2010 has not revealed any concern regarding the Office's entitlement to these assets. Administrative procedures for the transfer are ongoing and a draft protocol has been prepared, but not signed yet. The Office expects that the payment might be received in the course of 2015.

CA/20/15 e 31/118 150560004

2.3. IT Roadmap

Background:

131) In 2011, the IT Roadmap project was initiated to develop and implement improvements in the patent grant process through integrated IT tools.

132) For accounting purposes the EPO has performed an initial analysis of the three streams of the project to define the intangible assets which will be generated and qualify for recognition under IFRS (IAS 38). Stream 1 comprises short-term efficiency projects as well as reengineering of the patent grant process. Stream 2 involves investments designed to improve the efficiency and quality of the tools used by the examiners. Both streams are eligible for capitalisation. Stream 3 mainly deals with a new infrastructure. No eligible costs incurred in 2014 financial year (i.e. no costs capitalised as at 31 December 2014 for stream 3).

133) Costs capitalised under IFRS are summarised below:

in EUR '000

2011 2012 2013 2014 Total

Incl. for IT systems

Incl. for construction in

progress Stream I 269 8 280 9 337 9 428 27 314 14 337 12 977 Internal costs 87 3 369 1 955 2 443 7 854 5 370 2 484 External costs 182 4 911 7 382 6 985 19 460 8 967 10 493

Stream II 389 1 985 2 019 1 423 5 816 2 172 3 644 Internal costs 74 1 010 486 493 2 063 904 1 159 External costs 315 975 1 533 930 3 753 1 268 2 485

CA/20/15 e 32/118 150560004

Recommendation:

134) We concur with the accounting treatment applied by the Office, but recommend the following:

135) Performing a sanity check of internal costs incurred against planning in order to identify any excess costs, which would have to be expensed immediately (internal costs are not budgeted).

2.4. Negative equity of the EPO

136) As in 2013, the EPO's negative equity is not covered by the net present value of potential future renewal fees for granted European patents:

In EURm 2014 2013 2012 Equity -12.340 -4.585 -5.143 Potential future renewal fees 3.877 3.647 3.491 "Not covered" -8.463 -938 -1.652

Source: CA/60/15; CA/60/14

137) In 2014, the EPO generated a negative operating result compensated by a positive financial and therefore an overall positive net result in 2014. The negative operating result has been expected and is mainly caused by a high level of service costs on defined benefit obligations (current and past service cost of EUR 521m). Despite the positive net result, the actuarial losses of EUR 7.050m recognised in comprehensive income led to an increase in the EPO's negative equity from EUR -4.585m to EUR -12.340m. The expected charges from current service costs in 2015 are forecasted to amount to EUR 1.011m (actual 2014 figure: EUR 511m).

138) The actuarial losses on defined benefit obligations mainly result from decreased interest rates (from 3.89% in 2013 to 1.61% for the pension obligation in 2014), i.e. the equity is mainly impacted by general market developments outside the control of the EPO. The accounting treatment is in line with IAS 19 and consistent to prior year.

CA/20/15 e 33/118 150560004

139) We recognise that the Office has taken measures and is closely monitoring the development of equity through regular controlling reports, balanced scorecard and actuarial forecasts as well as Finance Study, regularly updated contribution rates, efficiency attempts, new career scheme, invalidity scheme, Salary Savings Plan and pension reform. Moreover, from an accounting perspective there are no consequences from negative equity as - according to article 40 of the EPC - the EPO cannot become insolvent. Therefore the going concern assumption for preparation of the financial statements is appropriate.

NEW ISSUES

2.5. Unitary Patent ("UNIP")

140) The European Parliament set the prerequisites for a European patent with unitary effect ("UNIP"). It will be the task of the Office to grant these patents as well as to administer the granted patents. The UNIP will be a European patent granted by the Organisation under the provisions of the EPC to which unitary effect for the territory of the participating states is given after grant, at the patentee’s request. The UNIP will thus be treated as normal application. After grant, the Organisation will administer the patent, collect the renewal fees and remit their share of these fees to the participating states. Regulation (EU) 1257/2012, in Recital 20, states that all costs of the tasks entrusted to the Office should be fully covered by the resources generated by the European patents with unitary effect and that, together with the fees to be paid to the Office during the pre-grant stage, the revenues from the renewal fees should ensure a balanced budget of the Office.

141) The costs of the Office at current stage mainly comprise costs for IT Set-up as well as administrative costs. These are accounted for in line with general accounting policies of the office regarding capitalisation of development costs. Entire IT Set-up costs for administration of requests and renewal fees (i.e. software cost and implementation of SAP PSCD module), Micado adjustment and IT development for the Unitary Patent Procedure are estimated to amount to EUR 2 533k. All other costs relating to process set-up, administration of the Select Committee as well as any other cost incurred by the Office are considered to be part of its ordinary business within its tasks under the EPC and are currently not separately measured by the Office.

CA/20/15 e 34/118 150560004

142) We concur with the accounting treatment as under IFRS costs are not eligible for capitalisation if costs cannot be reliably measured. The question if this is in line with Part IX of the EPC (cf. Art. 142, Art. 147) is irrelevant for accounting purposes.

2.6. Calculation of employee-related notes disclosures

Background:

143) To derive accurate and precise values for employee related accruals, relating notes disclosures and disclosures on related party transactions with key management, certain automated standard procedures and documentation should be in place. Relevant information should be available directly in SAP or derived from SAP in due course using standardised reporting formats. These include amongst others working hours, usage of flexi time or vacation as well as other time budgets and other information relevant for determining cost rates or related party notes disclosures. The information underlying related party disclosures shall be documented in a consistent, reliable and auditable way.

Recommendation:

144) In light of good practice of financial reporting we recommend completing timesheets in due course and freezing the time budgets in SAP within a reasonable timeframe. For financial reporting as well as for auditing purposes, such information should be readily available in the SAP-system and reproducible at any time, i.e. allow static reporting as of a selected date. Moreover, any HR information relevant to financial reporting should be well documented and provided in a standard format on a timely basis (i.e. on time for preparing the financial statements) suitable also for audit purposes.

3. GENERAL COMMENTS ON BUDGET IMPLEMENTATION

3.1. Forecast income statement

145) The IFRS plan figures as per CA/D/13 and CA/10/15 and the actual ones as per CA/60/15 are juxtaposed in Annex III/1.

CA/20/15 e 35/118 150560004

146) The 2014 operating result is negative (EUR -5m) and so EUR 70m below the forecast figure of EUR +65m. Whilst income was forecast very accurately and deviated by just 0.8%, the forecast for employee benefit expenses was EUR 127m (9.9%) too low and that for other operating expenses around EUR 44m (14%) too high.

147) At EUR 156m, the financial result was EUR 260m higher than forecast (EUR 267m due to higher finance income and EUR 7m to higher finance costs).

148) Other comprehensive income was EUR 7 906 under the forecast of zero.

3.2. Forecast balance-sheet figures

149) The IFRS plan figures as per CA/D/13 and CA/10/15 and the actual ones as per CA/60/15 are juxtaposed in Annex III/2.

150) Assets deviated from plan by EUR 628m (7.7%), with non-current assets EUR 925m (13.1%) over plan and current assets EUR 298m (28%) under plan. Overall, RFPSS net assets were EUR 691m and current and non-current securities EUR 391m over plan, while cash and cash equivalents were EUR 414m under plan.

151) Liabilities were EUR 10 583m (100.4%) over plan. This is attributable to the higher defined benefit liability of EUR 10 638m.

3.3. Comparison of budget as adopted and as implemented

152) The basic figures (as per CA/10/15) for comparing the budget as adopted and as implemented are given in Annex II.

153) In CA/D 1/13, the AC adopted an authorisation budget within the meaning of Article 25(1)(a) FinRegs totalling EUR 2 079m. The actual budget outturn was EUR 2 048m, i.e. EUR 31m less (-1.5%).

154) Income from designation and renewal fees (Chapter 53) was EUR 37m over budget (3.7%). Income from filing and search (Chapter 50) was EUR 29m below budget (7.5%); likewise general operating income by EUR 19m (8.7%).

CA/20/15 e 36/118 150560004

155) There were underspends in all operating expenditure chapters. They totalled EUR 152m, including EUR 110m for staff, EUR 11m for co-operation and meetings, EUR 10m for IT equipment maintenance and EUR 14m for general operating expenditure.

156) There was a budget surplus (Chapter 49) of EUR 332m, which is EUR 172m higher than budgeted (EUR 160m).

157) For the pension and social security schemes, income and expenditure were both below budget, at EUR 26m (7.9%) and EUR 21m (10.2%). The transfer to the RFPSS was just under EUR 5m (3.9%) below budget.

Appropriation transfers

158) The appropriation transfers under Article 34 FinRegs are shown in Annex II/4. The figures are taken from CA/10/15.

159) Transfers under Article 34(1) FinRegs (within the same chapter) totalled EUR 1m.

160) Those under Article 34(2) FinRegs (between chapters and not exceeding 20% of the appropriations of the chapters concerned) amounted to EUR 3m.

161) There were no transfers under Article 34(3) FinRegs (decision by the BFC or AC).

CA/20/15 e 37/118 150560004

D. INTERNAL CONTROL SYSTEM

1. INTERNAL AUDITING (DIRECTORATE 0.6.1)

162) In accordance with the International Professional Practices Framework (IPPF) for internal audit (issued by the Institute of Internal Auditors – IIA), heads of internal audit units must develop and maintain a quality assurance and improvement programme covering all their unit's activities and including an independent quality assessment at least every five years.

163) In 2014, Internal Auditing (D 0.6.1) was the subject of an external quality assessment conducted by the German Institut für Interne Revision (internal audit institute - DIIR), which certified that the directorate's practices meet the IPPF standards.

164) The DIIR assesses quality on the following scale:

165) The results of the DIIR's assessment were as follows:

166) We will especially monitor implementation of recommendations relating to practices which scored 1 or 0 at a more detailed assessment level.

Target achievement Points Assessment> 90% 3 Fully achieved

75%-90% 2 Slight improvement potential50%-75% 1 Significant improvement potential

<50% 0 Deficient

Requirements AssessmentOrganisation of internal audit activity 87,3%Audit planning and preparation 85,7%Audit performance and reporting 84,4%Audit rework and follow-up 95,8%Internal Auditing's personnel and quality assurance 95,0%

CA/20/15 e 38/118 150560004

2. GOVERNANCE OF THE RFPSS

2.1. Control system

167) We have selected 80 transactions from the year 2014 and checked the proper functioning of the internal control system including segregation of front office and back office and the proper documentation of controls. We also have checked the proper recording of all transactions by the custodian (=physical delivery). We found no exceptions.