European Subsea Cable Report & Forecast 2015-2025 · PDF fileSubsea Cables 11 4. Cable...

9

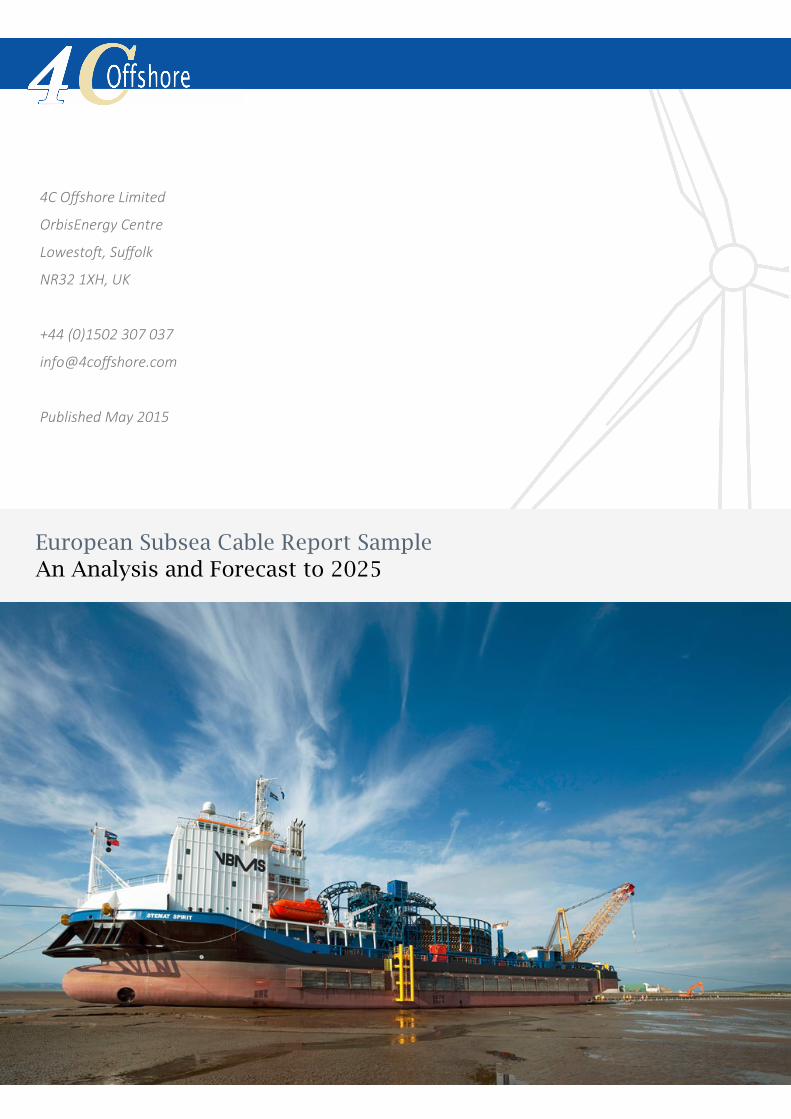

European Subsea Cable Report Sample An Analysis and Forecast to 2025 4C Offshore Limited OrbisEnergy Centre Lowestoſt, Suffolk NR32 1XH, UK +44 (0)1502 307 037 info@4coffshore.com Published May 2015

Transcript of European Subsea Cable Report & Forecast 2015-2025 · PDF fileSubsea Cables 11 4. Cable...

European Subsea Cable Report Sample

An Analysis and Forecast to 2025

4C Offshore Limited

OrbisEnergy Centre

Lowestoft, Suffolk

NR32 1XH, UK

+44 (0)1502 307 037

Published May 2015

European Subsea Cable Report & Forecast 2015-2025 - SAMPLE| 1

Table of Contents

1. Executive Summary 7

2. Market Development to Date 9

3. Subsea Cables 11

4. Cable Installation 14

5. Cable Monitoring 16

6. Cable Inspection 16

7. Cable Intervention and Repairs 17

8. Cable Faults 19

9. Weather Related Installation Delays 23

10. Market Share: Array Cable Supply 26

11. Market Share: Export Cable Supply 27

12. Market Share: Interconnector Cable Supply 28

13. Market Share: Array Cable Installation 29

14. Market Share: Export Cable Installation 30

15. Market Share: Interconnector Cable Installation 31

16. At a Glance: Subsea Cable Installation Companies and Their Assets 32

17. Transmission Policy Frameworks Overview 33

18. Country Overview: Belgium 37

19. Country Overview: Denmark 40

20. Country Overview: France 42

21. Country Overview: Germany 44

22. Country Overview: Netherlands 46

23. Country Overview: United Kingdom 49

24. Costs: Cable Supply Costs 51

25. Costs: Cable Installation Costs 53

26. Costs: Capital Expenditure 54

27. Forecasting Methodology 55

28. Forecasting Results: Cable demand and expenditure to 2025 57

29. Appendix: Project Pipelines by Country 64

30. Appendix: Future Wind Farm Opportunities 68

31. Appendix: Future Interconnector Opportunities 73

32. Appendix: Offshore Wind Subsea IMR Contracts 81

33. Appendix: Offshore Wind Subsea IMR Players Schematic 83

34. Appendix: German North Sea Grid Connections 84

35. Appendix: Baltic Sea Grid Connections 85

European Subsea Cable Report & Forecast 2015-2025 - SAMPLE| 2

Table of Figures

Figure 1. Summary of offshore wind subsea cable market development 2002-2014 7

Figure 2. Percentage of incidents by problem and median delay length 7

Figure 3. Number of players and market leaders for subsea cable and installation since 2010 8

Figure 4. Current (April 2015) and future (2025) installed capacity for the six main European markets 8

Figure 5.Offshore Wind CAPEX spend by country summed for period 2015-2025 9

Figure 6.Demand for array, export, HVDC transmission and interconnector cabling 2015-2025 (km) 9

Figure 7. Water depth and distance to shore at installed or underway European projects 10

Figure 8. Percent of capacity being exported via transmission technology (MVAC, HVAC, HVDC) 10

Figure 9. Nysted's substation (HVAC transformer) and Helwin Alpha (HVDC converter station) 10

Figure 10. Offshore wind cabling to date plotted by offshore installation start year 11

Figure 11. Preparing for installation, array cable being wound on a carousel and subsea power cable cross section 11

Figure 12. Ready for installation: export cable being wound on a carousel utilizing a tensioner 12

Figure 13. Four 66kV cable designs receiving qualification funding from the Carbon Trust's OWA 12

Figure 14. Single bipole arrangement schematic 13

Figure 15. Loading HVDC onto a cable lay vessel at the factory 13

Figure 16. Reef Subsea’s Q1000 Jet trencher, Subsea 3M Cable Plough and DeepOcean's UT-1 trencher 15

Figure 17. Typical Survey Programme for a Round 2 UK Wind Farm 17

Figure 18. Thanet Export cable replacement 18

Figure 19. Indicative CAPEX reduction potential of transmission initiatives and cost reduction options 19

Figure 20. Percentage of incidents by problem and median delay length 20

Figure 21. Actual versus expected array cable rates at Gwynt-y-Môr 23

Figure 22. Significant delays attributable to weather 24

Figure 23. Example cable installation elements and influencing metocean components 24

Figure 24. Reducing weather risk during cable installation by optimising elements of the process 25

Figure 25. Market share: array cable manufacture since 2010 26

Figure 26. Market share: export cable manufacture since 2010 27

Figure 27. Market share: interconnector cable manufacture for on and offshore cable length since 2010 28

Figure 28. Market share: array cable installation since 2010 29

Figure 29. Market share: Export cable installation since 2010 30

Figure 30. Market share: interconnector installation (subsea component) 31

Figure 31. European offshore wind and interconnector subsea cable installation companies 33

European Subsea Cable Report & Forecast 2015-2025 - SAMPLE| 3

Figure 32. Estimated OFTO O&M expenditure per annum 34

Figure 33. Results OFTO Tenders 1-3 and operations and maintenance body 35

Figure 34. Belgian Offshore Grid 37

Figure 35. Belgium: Projects installed 38

Figure 36. Belgium: Investor types and owners for projects that are commissioned or in construction 39

Figure 37. Cumulative installations according to 4C's 2025 projection 39

Figure 38. Denmark: Projects installed 41

Figure 39. Denmark: Investor types and owners for projects that are commissioned or in construction 41

Figure 40. Cumulative installations according to 4C's 2025 projection 41

Figure 41. French offshore wind tender results. 42

Figure 42. Supply chain investments in France 43

Figure 43. Cumulative installations according to 4C's 2025 projection 43

Figure 44. The extension of the higher initial remuneration has opened further investment in German offshore wind 45

Figure 45. Progress towards goals and grid allocation to date 45

Figure 46. Germany: Investor types and owners for projects that are commissioned or in construction 45

Figure 47. Annual installations according to 4C's 2025 projection 46

Figure 48. Map of current and future Netherlands offshore wind projects 47

Figure 49. Netherlands progress to date and scale of future tenders 48

Figure 50. Cumulative installations according to 4C's 2025 projection 49

Figure 51. UK development, licensing rounds and progress to date 50

Figure 52. Ownership of generating and under construction projects in the UK 50

Figure 53. Annual installations according to 4C's 2025 projection 51

Figure 54. Array cable manufacture costs versus array cable length; regression analysis and table of projects 52

Figure 55. HVAC cable manufacture costs versus array cable length; regression analysis and table of projects 52

Figure 56. HVDC cable manufacture costs and table of projects 53

Figure 57. Array cable supply costs versus array length; regression analysis and table of projects 53

Figure 58. Export cable supply costs versus length; regression analysis and table of projects 54

Figure 59. CAPEX modelling to 2025 55

Figure 60. Observed array cable lengths (km) plotted against the two predictive components 56

Figure 61. Observed substation capacity by construction start year and number of substations by project capacity 57

Figure 62. Observed turbine capacity by construction start year and number of confirmed turbine orders 57

Figure 63. Cumulative annual offshore wind CAPEX to 2015-2025 and breakdown by country 58

European Subsea Cable Report & Forecast 2015-2025 - SAMPLE| 4

Figure 64. Annual array cable demand (km) 2015-2025 by country 59

Figure 65. Annual MVAC export cable demand (km) 2015-2025 by country plus total MVAC cable demand by country 60

Figure 66. Annual HVAC export cable demand (km) 2015-2025 by country plus total HVAC cable demand by country 61

Figure 67. Annual HVDC export cable demand (km) 2015-2025 by country plus total HVDC cable demand by country 62

Figure 68. European HVDC interconnector cable demand for the period 2015-2025 63

Figure 69. Expenditure on HVDC interconnector cable supply and installation for the period 2015-2025 63

Figure 70. Rate of installation data set: MW/year increasing with start of offshore installation 64

Figure 71. Belgium: Project installations to 2025 65

Figure 72. Denmark: Project installations to 2025 65

Figure 73. France: Project installations to 2025 66

Figure 74. Germany: Project installations to 2025 66

Figure 75. Netherlands: project installations to 2025 67

Figure 76. United Kingdom: Project installations to 2025 67

Figure 77. Future UK offshore wind farm projects awarded cable supply and manufacture contracts 68

Figure 78. Future German offshore wind farm projects awarded cable supply and manufacture contracts 69

Figure 79. HVDC Transmission cable supply and installation contracts for German North Sea Converter Stations 70

Figure 80. Future Belgian offshore wind farm projects awarded cable supply and manufacture contracts 70

Figure 81. Future Danish offshore wind farm projects awarded cable supply and manufacture contracts and contracts 71

European Subsea Cable Report & Forecast 2015-2025 - SAMPLE| 5

7. Cable Intervention and Repairs

Cable intervention refers to protection works such as trenching and rock or mattress placement, and may be carried out on

operational cables. Repairs however, which may require replacement of an entire cable or jointing of a spare cable, require the cable

to be deenergised.

Following the location of the cable fault via monitoring and a survey of the location, deburial and cutting of the cable using a

combination of ROV and grapnel techniques will be carried out. The choice of repair methodology varies and can be dependent on

the fault location:

It is often more economical to replace array cables rather than to repair them.

Where the fault is near the end of a cable then a repair with a single joint may be possible by performing a single cut to

remove the damaged cable and jointing in the new cable section to the end and re-terminating.

Where the fault is within an export or interconnector cable the repair process typically involves deburial of the cable;

cutting of the cable at the seabed using a grapnel or ROV; recovery of the first cable end, removal of damaged cable,

jointing of the spare cable and laydown of the first joint; recovery of the second cable end, removal of damage, jointing to

the spare cable’s other end; laydown of second joint and repair bight (the loop of additional cable) and reburial of the

cable.

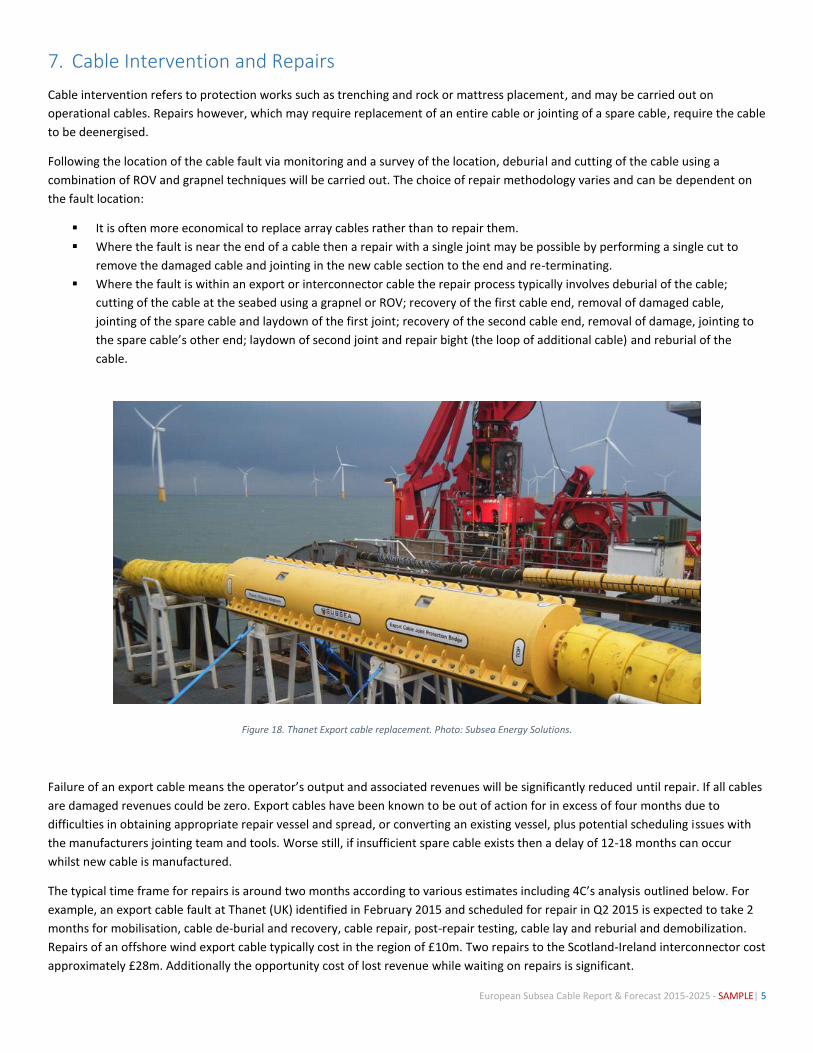

Figure 18. Thanet Export cable replacement. Photo: Subsea Energy Solutions.

Failure of an export cable means the operator’s output and associated revenues will be significantly reduced until repair. If all cables

are damaged revenues could be zero. Export cables have been known to be out of action for in excess of four months due to

difficulties in obtaining appropriate repair vessel and spread, or converting an existing vessel, plus potential scheduling issues with

the manufacturers jointing team and tools. Worse still, if insufficient spare cable exists then a delay of 12-18 months can occur

whilst new cable is manufactured.

The typical time frame for repairs is around two months according to various estimates including 4C’s analysis outlined below. For

example, an export cable fault at Thanet (UK) identified in February 2015 and scheduled for repair in Q2 2015 is expected to take 2

months for mobilisation, cable de-burial and recovery, cable repair, post-repair testing, cable lay and reburial and demobilization.

Repairs of an offshore wind export cable typically cost in the region of £10m. Two repairs to the Scotland-Ireland interconnector cost

approximately £28m. Additionally the opportunity cost of lost revenue while waiting on repairs is significant.

European Subsea Cable Report & Forecast 2015-2025 - SAMPLE| 6

The telecoms sector’s solution to this cable-repair problem is the Atlantic Cable Maintenance & Repair Agreement (ACMA), a non-

profit cable maintenance programme with 62 members who are provided access to vessels staffed permanently with dedicated

repair teams. Such an agreement, with its strong performance targets ensuring efficient repairs does not exist between offshore

wind developers. Recognising that ACMA vessels are less suitable for power cable maintenance Global Marine Systems Ltd (GMSL),

now Prysmian, are working with Transmission Capital (an OFTO) to upgrade the deck layout, turntable, equipment of vessel Wave

Sentinal, a current ACMA telecom-cable repair vessel to provide it with power cable repair capabilities. The vessel’s draught means it

will not be able to operate in shallow waters but is expected to be able to repair 80% of OFTO cable faults. In parallel, a universal

jointing system will be developed capable of joining power cables from different suppliers, and a team of appropriately qualified

staff will be trained and assigned to the vessel. Upon completion ACMA network participants will have access to the new power

cable repair service from 2017. A DNVGL survey (DNV, 2014) found that 15% of industry respondents cited a cable repair framework

agreement as a potential route to cost reduction in offshore transmission.

Currently some park and transmission operators employ framework agreements for cable maintenance and repair. For example in

2011 the Briggs Group secured a five year agreement with SSE to repair and maintain a network comprising 102 live cables over a

distance of 515km. Briggs provides 24/7 immediate mobilisation and specialist end-to-end support, including network surveys, cable

protection work, cable installation, repair and testing through all seasons. Similarly Transmission Capital has contracted Global

Marine (GM) under a framework where GM is the preferred repair contractor offering a 24/7 call out facility. Other UK OFTOs are

known to be exploring framework agreements.

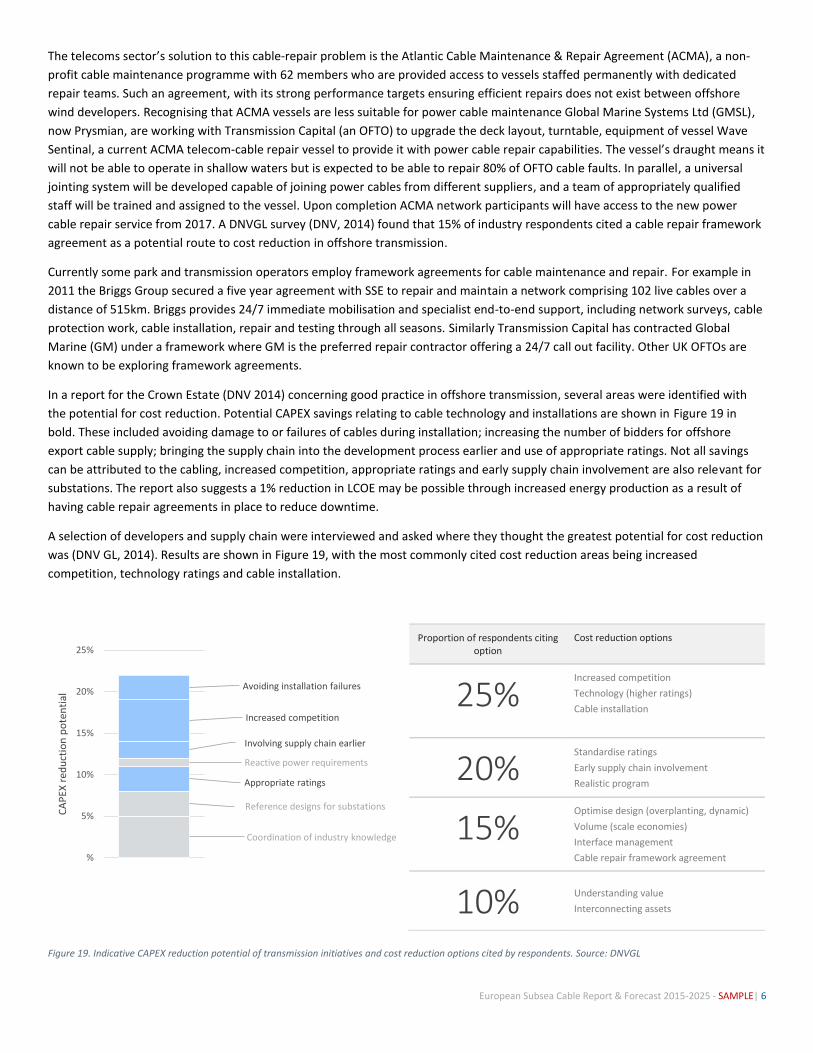

In a report for the Crown Estate (DNV 2014) concerning good practice in offshore transmission, several areas were identified with

the potential for cost reduction. Potential CAPEX savings relating to cable technology and installations are shown in Figure 19 in

bold. These included avoiding damage to or failures of cables during installation; increasing the number of bidders for offshore

export cable supply; bringing the supply chain into the development process earlier and use of appropriate ratings. Not all savings

can be attributed to the cabling, increased competition, appropriate ratings and early supply chain involvement are also relevant for

substations. The report also suggests a 1% reduction in LCOE may be possible through increased energy production as a result of

having cable repair agreements in place to reduce downtime.

A selection of developers and supply chain were interviewed and asked where they thought the greatest potential for cost reduction

was (DNV GL, 2014). Results are shown in Figure 19, with the most commonly cited cost reduction areas being increased

competition, technology ratings and cable installation.

Proportion of respondents citing option

Cost reduction options

25% Increased competition

Technology (higher ratings)

Cable installation

20% Standardise ratings

Early supply chain involvement

Realistic program

15% Optimise design (overplanting, dynamic)

Volume (scale economies)

Interface management

Cable repair framework agreement

10% Understanding value

Interconnecting assets

Figure 19. Indicative CAPEX reduction potential of transmission initiatives and cost reduction options cited by respondents. Source: DNVGL

Coordination of industry knowledge

Reference designs for substations

Appropriate ratings

Reactive power requirements

Involving supply chain earlier

Increased competition

Avoiding installation failures

%

5%

10%

15%

20%

25%

CA

PEX

red

uct

ion

po

ten

tial

European Subsea Cable Report & Forecast 2015-2025 - SAMPLE| 7

8. Cable Faults

Cabling has become synonymous with cost overruns and delays in offshore wind. According to 2012 estimates from offshore

insurance company Codan, cables account for 90% of the number of offshore wind claims and 70% of the actual cost of all offshore

wind claims. This is highly disproportionate to the CAPEX associated with their manufacture and installation. It is reported that the

majority of claims are due to incorrect installation and load out of cables (GCube), and that there is no evidence to date of damage

during operations by e.g. anchor strike (Offshore Wind Accelerator (OWA), 2015). According to the OWA between 2007 and 2014,

the cumulative cost to insurers was £75 million with over 60 incidents alone resulting in pay outs of between £0.5 million and £13.5

million per claim.

Historically offshore wind projects have used the Burial Protection Index (BPI) to set the optimum Depth of Lowering in the seabed

for adequate protection from external threats. A weakness of this approach however is that it does not optimize for actual levels of

external risk and therefore can be overly conservative, increasing time and cost of installation and even introducing risk through

excessive handling of cabling by trenching equipment. To address these shortcomings and unify emerging best practices, a

repeatable and probabilistic Cable Burial Risk Assessment Methodology (CBRA) has been published (OWA, 2015) which is “practically

and economically achievable whilst providing adequate protection”.

Cable Delay and Fault Study

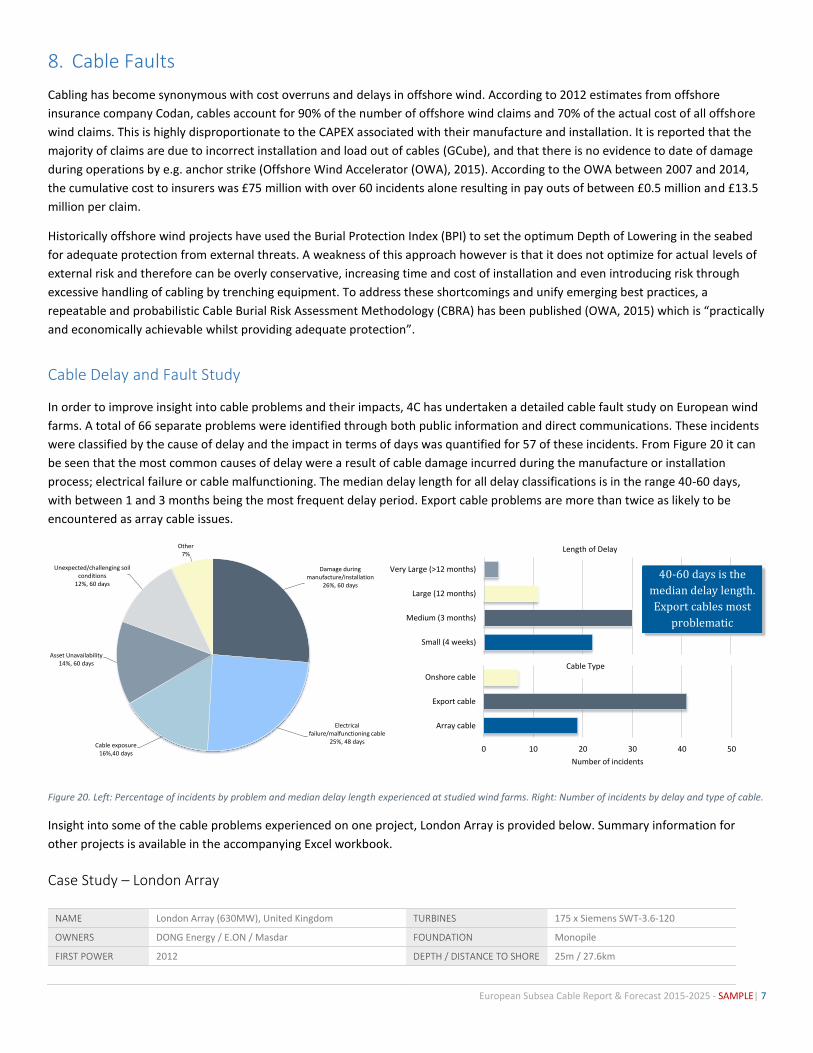

In order to improve insight into cable problems and their impacts, 4C has undertaken a detailed cable fault study on European wind

farms. A total of 66 separate problems were identified through both public information and direct communications. These incidents

were classified by the cause of delay and the impact in terms of days was quantified for 57 of these incidents. From Figure 20 it can

be seen that the most common causes of delay were a result of cable damage incurred during the manufacture or installation

process; electrical failure or cable malfunctioning. The median delay length for all delay classifications is in the range 40-60 days,

with between 1 and 3 months being the most frequent delay period. Export cable problems are more than twice as likely to be

encountered as array cable issues.

Figure 20. Left: Percentage of incidents by problem and median delay length experienced at studied wind farms. Right: Number of incidents by delay and type of cable.

Insight into some of the cable problems experienced on one project, London Array is provided below. Summary information for

other projects is available in the accompanying Excel workbook.

Case Study – London Array

NAME London Array (630MW), United Kingdom TURBINES 175 x Siemens SWT-3.6-120

OWNERS DONG Energy / E.ON / Masdar FOUNDATION Monopile

FIRST POWER 2012 DEPTH / DISTANCE TO SHORE 25m / 27.6km

Damage during manufacture/installation

26%, 60 days

Electrical failure/malfunctioning cable

25%, 48 daysCable exposure

16%,40 days

Asset Unavailability14%, 60 days

Unexpected/challenging soil conditions

12%, 60 days

Other7%

Array cable

Export cable

Onshore cable

0 10 20 30 40 50

Number of incidents

Cable Type

Small (4 weeks)

Medium (3 months)

Large (12 months)

Very Large (>12 months)

Length of Delay

40-60 days is the

median delay length.

Export cables most

problematic

European Subsea Cable Report & Forecast 2015-2025 - SAMPLE| 8

Array Cables Export Cables

TOTAL LENGTH 209km TOTAL LENGTH 214km

MANUFACTURER JDR Cable Systems Ltd MANUFACTURER Nexans

INSTALLER Visser & Smit Marine Contracting INSTALLER Visser & Smit Marine Contracting

VESSEL Pontra Maris / Stemat Oslo / Normand Flower / CS Sovereign / Jan Steen / Cable Innovator / Costal Explorer

VESSEL Stemat Spirit

Electrical Failure – Delay of approximately 214 days

On the 28th March 2012, a cable at the Cleve Hill onshore substation experienced a failure despite being fully tested, commissioned

and in service for just 127 hours. Investigations found that the failure was most likely due to a defect in the cable termination. All six

cable terminations were replaced partly under warranty at an additional cost of £1.145 million by an alternative contractor,

Sudkabel who was able to replace four weeks earlier than the original contractor ABB. With the project generating power, revenues

were being lost. First power, scheduled for March 2012 (when the failure occurred) was consequently delayed until 8 months later.

Cable Exposure – 180 Days

Remedial work concerning a number of turbine and array cable locations was undertaken from the 15th October 2013,

lasting around a month. Array cable exposure was seen at eight locations with exposure lengths varying between 5m and

926m. The problems came to light shortly after the construction phase, meaning the construction delays were possibly

attributable to cable lay and burial problems.

On the 4th April 2014, further reburial work commenced and lasted until the end of August 2014.

Malfunctioning Export Cable – 126 days

Delays were seen in the delivery of the export cable from Nexans, with £12.1m attributed to having vessels on standby. The export

cables experienced a range of problems including failures identified during Factory Acceptance Testing (FAT) and spooling. Several

factory joints were required and three cables were manufactured to a revised design in the hope of avoiding any repeat damage (a

transition ring between two types of armour was added to avoid burn damage seen in testing). The replacement joints and the

developer’s independent survey, plus increased project management overhead led to increased costs. Furthermore a revised

installation methodology was developed requiring additional jetting in place of ploughing, and at an additional expense.

Whilst the developer was liable for the standby costs of the cable-lay vessel, some liquidated damages were claimed from Nexans

(£7,555,540), which offset a proportion of the vessel costs arising from the late delivery.

Damage during Manufacture / Installation – 139 Days

A distortion was noticed on the first cable during load out. A 31.5 hour delay was incurred whilst a cable specialist inspected

the cable and then granted permission for the load out to restart.

The third export cable was damaged in March 2012 whilst attempting shallow water installation. On the 8th May 2012

Pharos Offshore Group began export cable repair and burial works utilising the cable-lay vessel CS Responder. Operations

continued throughout June and July of 2012, adding a four month delay to the cable installation programme.

Other – 73 Days

The first export cable pull in was delayed whilst waiting for Germanisher Lloyd (GL) certification, resulting in additional

vessel standby and associated costs.

The cable manufacture delayed the installation schedule by around four months forcing the cable installation to take place

over the course of the winter period where adverse seasonal weather conditions incurred further vessel standby costs. The

shallow water encountered during the installation of the export cables meant that the weather had a profound impact on

the construction schedule.

End of sample