European Contingent Staffing Trends€¦ · 3 bn 2 bn 1 bn 0 1950 2050 15-59 0-14 60+ 2011 ......

37

© 2011 Crain Communications Inc European Contingent Staffing Trends John Nurthen, General Manager, Europe Staffing Industry Analysts Optimum Sponsors: Alexander Mann Solutions | Allegis Group Services | Fieldglass | Gibbs S3 | IQNavigator KellyOCG | Peopleclick Authoria | ProcureStaff Technologies | Volt Consulting Group | WorkforceLogic Pinnacle Sponsors: Monday, 20 June | 12:00 pm| Ballroom I-III

Transcript of European Contingent Staffing Trends€¦ · 3 bn 2 bn 1 bn 0 1950 2050 15-59 0-14 60+ 2011 ......

© 2011 Crain Communications Inc

European Contingent Staffing Trends

John Nurthen, General Manager, Europe

Staffing Industry Analysts

Optimum Sponsors: Alexander Mann Solutions | Allegis Group Services | Fieldglass | Gibbs S3 | IQNavigatorKellyOCG | Peopleclick Authoria | ProcureStaff Technologies | Volt Consulting Group | WorkforceLogic

Pinnacle Sponsors:

Monday, 20 June | 12:00 pm| Ballroom I-III

© 2011 Crain Communications Inc

European and North American Staffing Markets

Source: Staffing Industry Analysts

Size of staffing market 2010 = €91 Billion

Forecast Growth 2011 = 11%

Size of staffing market 2010 = €60 Billion

Forecast Growth 2011 = 12%

© 2011 Crain Communications Inc

European Staffing Market by Sector

Source: Staffing Industry Analysts

23%

50%

12%

4%4%

5%

1% 1%

© 2011 Crain Communications Inc

Agency Temp Employment Has Returned to Growth

Source: Staffing Industry Analysts and US Bureau of Labor Statistics. ABU Netherlands, Pole Emploi France, BAP Germany - Note: Based on change in employment or hours worked as available

Year-Over-Year Change in Temp Employment for Select Countries

US

France

Netherlands

Germany

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

Jan-08

Apr-08

Jul-08

Oct-08

Jan-09

Apr-09

Jul-09

Oct-09

Jan-10

Apr-10

Jul-10

Oct-10

Jan-11

Apr-11

© 2011 Crain Communications Inc

Top 10 European Staffing Companies

Rank Company Latest Annual Sales (€m)

Change over prior year

1 Adecco 12,126 +24%2 Randstad 11,343 +10%3 ManpowerGroup 9,281 +17%4 USG People 3,099 +3%5 Hays 1,792 +10%6 Synergie 1,207 +30%7 Groupe CRIT 1,094 +16%8 Trenkwalder 1,000 +27%9 Impellam 983 +13%10 Kelly Services 763 +2%

Source: Company Financials and Staffing Industry Analysts

© 2011 Crain Communications Inc

Staffing Industry Stock Index (SISI) Performance 2009 to 2011

80

90

100

110

120

130

140

150

160

170

180

Apr-09 Jun-09 Aug-09 Oct-09 Dec-09 Feb-10 Apr-10 Jun-10 Aug-10 Oct-10 Dec-10 Feb-11 Apr-11

SISI MSCI

The Stock Market is Bullish on Staffing

Source: Yahoo Finance and Staffing Industry AnalystsNote: SISI is market capitalization weighted and includes a selection of global staffing stocks. Adecco, Randstad, ManpowerGroup and Robert Half make up approximately ¾ of the index value based on market cap.

SISI

MSCI World Index

© 2011 Crain Communications Inc

Temporary Staffing Growth Forecasts

Source: Staffing Industry Analysts’ Forecast

Country Structural Legislative Economic GDP 2011 GrowthRate

Sweden 4.2% 21%

Germany 2.6% 20%

Italy 1.0% 20%

Austria 2.4% 15%

Norway 2.7% 15%

Denmark 1.7% 14%

☺☺

☺

☺ ☺

☺

☺☺☺

© 2011 Crain Communications Inc

Temporary Staffing Growth Forecasts

Source: Staffing Industry Analysts’ Forecast

Country Structural Legislative Economic GDP 2011 GrowthRate

France 1.8% 12%

Finland 3.7% 12%

Belgium 2.4% 12%

Switzerland 1.9% 9%

Netherlands 1.9% 8%

Spain 0.8% 7%

☺

☺

☺

☺☺☺

☺ ☺

☺

© 2011 Crain Communications Inc

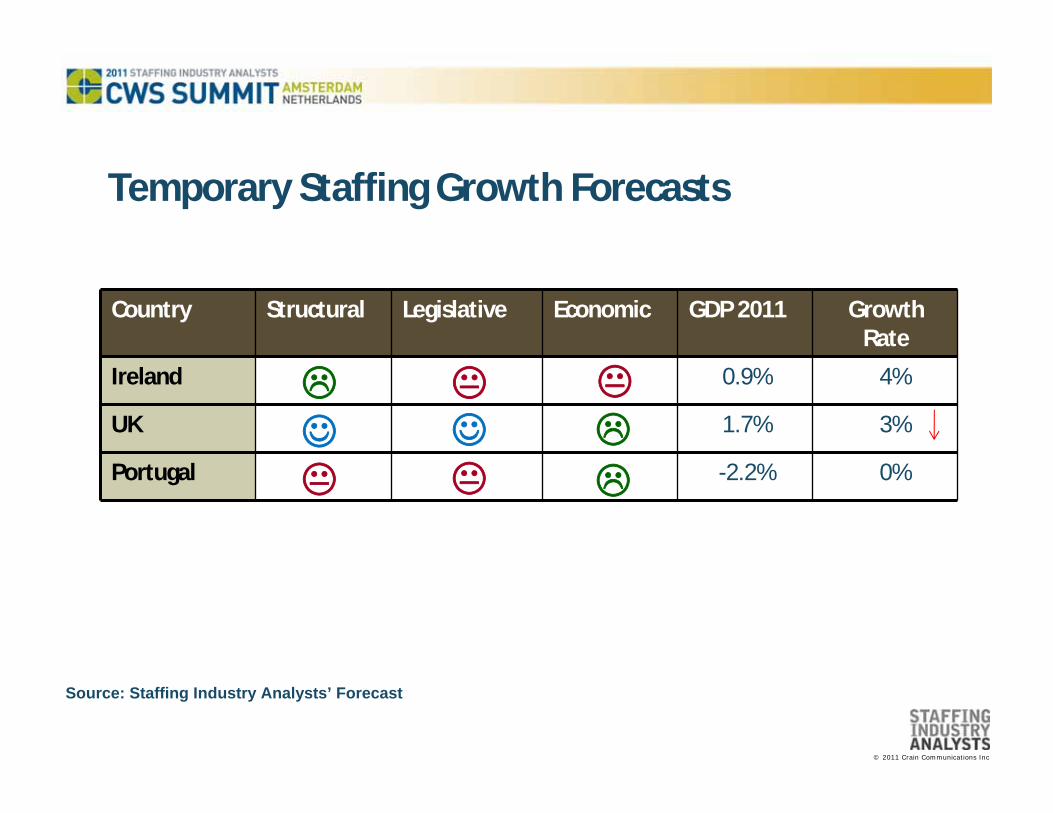

Temporary Staffing Growth Forecasts

Source: Staffing Industry Analysts’ Forecast

Country Structural Legislative Economic GDP 2011 GrowthRate

Ireland 0.9% 4%

UK 1.7% 3%

Portugal -2.2% 0%

☺☺

© 2011 Crain Communications Inc

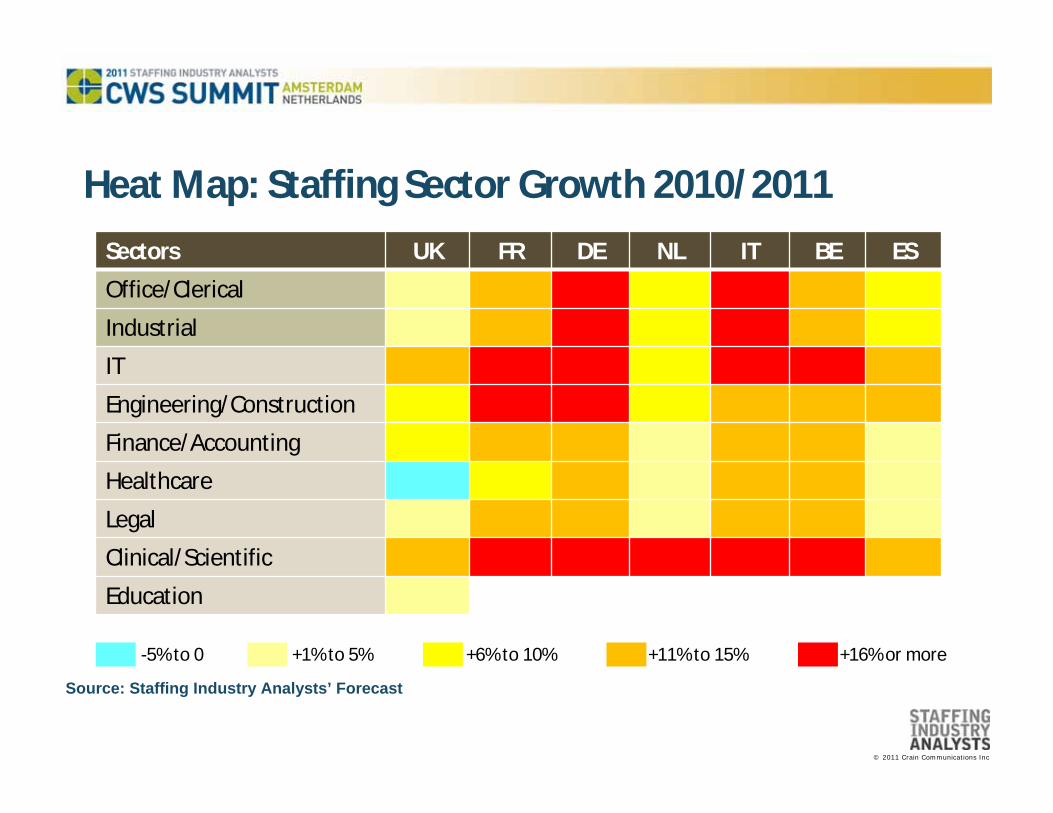

Heat Map: Staffing Sector Growth 2010/2011

Sectors UK FR DE NL IT BE ES

Office/Clerical

Industrial

IT

Engineering/Construction

Finance/Accounting

Healthcare

Legal

Clinical/Scientific

Education

Source: Staffing Industry Analysts’ Forecast

+16% or more+11% to 15%+6% to 10%+1% to 5%-5% to 0

© 2011 Crain Communications Inc

EU Agency Workers Directive

• Effective Date: 5 December 2011

• Two main features— Equal treatment for basic working and

employment conditionsMain impact in UK and Ireland

– Agency Workers RegulationsNo impact in Germany and Sweden

— Review of existing staffing legislation— Remove or justify

© 2011 Crain Communications Inc

Restrictions Still in Place

© 2011 Crain Communications Inc

Staffing Company Gross Margin Trends

Average Latest Period Year on Year Comparison

Change

All Companies 24.33% 23.39% +0.94

Very Large Companies* 24.62% 23.80% +0.82

Large Companies* 29.00% 27.29% +1.71

Medium Companies* 18.54% 18.81% -0.27

Small Companies* 33.58% 30.40% +3.18

Highest 55.04% 43.13% +11.91

Lowest 7.60% 7.96% -0.36

Source: Staffing Industry Analysts

*Determined by Annual Revenue: Very Large = over €500m, Large= €50m-€500m, Medium = €5m-€50m, Small = less than €5m

© 2011 Crain Communications Inc

European Staffing Company M&A

• 100 staffing company deals in Europe during 2010

~ Healthcare by far the most active sector (18% of all deals)

~ Recent significant dealso Adecco: Spring & MPS o Manpower: Comsyso Blackstone Private Equity: ICS Nursing and Pulseo Allegis: Aston Carter (IT)o Trenkwalder: Droege Capital GmbH

• US acquirers are establishing themselves in countries where their key US clients need help

© 2011 Crain Communications Inc

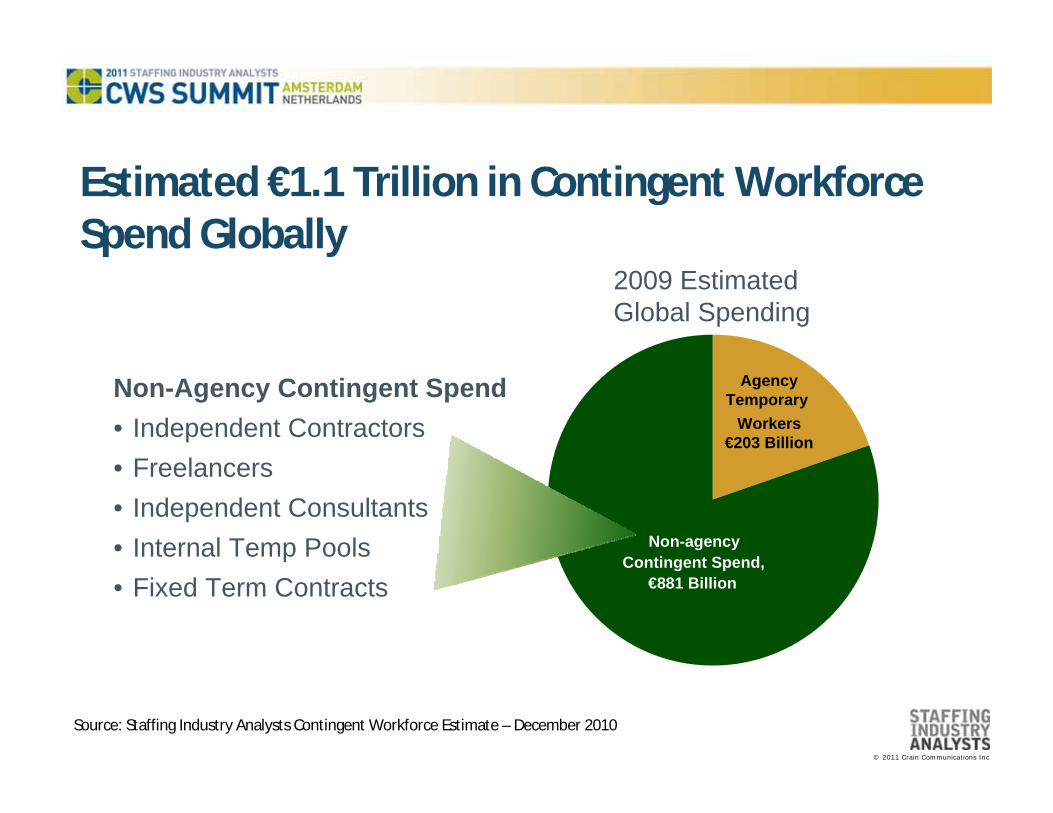

Estimated €1.1 Trillion in Contingent Workforce Spend Globally

Source: Staffing Industry Analysts Contingent Workforce Estimate – December 2010

2009 EstimatedGlobal Spending

AgencyTemporary

Workers€203 Billion

Non-agency Contingent Spend,

€881 Billion

Non-Agency Contingent Spend• Independent Contractors• Freelancers• Independent Consultants• Internal Temp Pools• Fixed Term Contracts

© 2011 Crain Communications Inc

AgencyTemps

Non-Agency Contingent Workers

© 2011 Crain Communications Inc

AgencyTemps

Non-Agency Contingent

WorkersTraditional Workers

© 2011 Crain Communications Inc

The Demographic Crisis: It’s Back!

Source: UN Department of Economic & Social Affairs

World Population by Age Group

6 bn

5 bn

4 bn

3 bn

2 bn

1 bn

01950 2050

15-59

0-14

60+

2011

Europe Population by Age Group

1950 2050

500m

400m

300m

200m

100m

0

15-59

0-14

60+

2011

© 2011 Crain Communications Inc

Contingent Workforce Buyer Survey 2011

© 2011 Crain Communications Inc

Contingent Workforce Buyer Survey

gggg

<€50 million

€50 million -€99 million

€100 million -€199 million

€200 million -€399 million

€400 million -€699 million

>€700 million

Survey Composition Europe: Estimated Annual Spend on Contingent Work

Source: 2011 Contingent Workforce Buyer Survey

31%

25%

19%

10%

10%

4%

© 2011 Crain Communications Inc

Question:What do you think is the “right” or “healthy” proportion of contingent

workers for your organisation today?

Source: 2011 Contingent Workforce Buyer Survey

© 2011 Crain Communications Inc

Source: 2011 Contingent Workforce Buyer Survey

© 2011 Crain Communications Inc

Question:What do you think is the “right” or “healthy” proportion of contingent

workers for your organisation ideally?

Source: 2011 Contingent Workforce Buyer Survey

© 2011 Crain Communications Inc

Source: 2011 Contingent Workforce Buyer Survey

© 2011 Crain Communications Inc

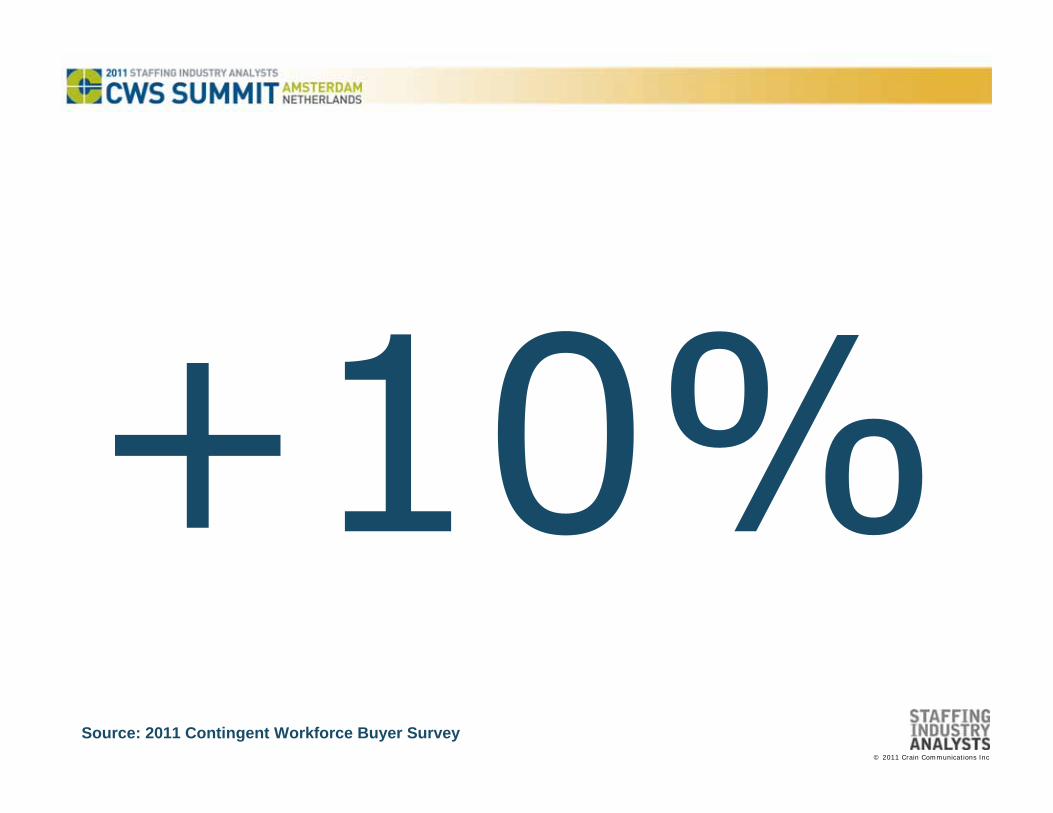

Question:What is your best estimate as to how much your Organisation’s

expense budget would change if you had no contingent workers?

Source: 2011 Contingent Workforce Buyer Survey

© 2011 Crain Communications Inc

Source: 2011 Contingent Workforce Buyer Survey

© 2011 Crain Communications Inc

Supplier Report Card

• How would you rate the overall performance of your primary staffing supplier? B

0%5%

10%15%20%25%

0 1 2 3 4 5 6 7 8 9 10

Detractors Promoters

ExtremelyLikely

ExtremelyUnlikely

Passives

• How likely are you to recommend them to a friend?• Net promoter score: Europe = -8, North America = +26

© 2011 Crain Communications Inc

Buyers Plan Increased Use of Contingent Work

Source: 2008-2011 Contingent Workforce Buyer Survey

Median estimate of Percent of CW

0%

2%

4%

6%

8%

10%

12%

14%

16%

2008 2009 2010 2011 2013 (P)

NA

WE

© 2011 Crain Communications Inc

Source: 2004-2011 Contingent Workforce Buyer Survey

0%

10%

20%

30%

40%

50%

60%

70%

80%

2004 2005 2006 2007 2008 2009 2010 2011

NA

WE

Buyers More Focused on Contingent Work

Per Cent of Buyers who spent more than 50% of time on CW Issues

© 2011 Crain Communications Inc

Source: 2008-2011 Contingent Workforce Buyer Survey

Growing Interest in Global Contingent Workforce Programme Management

Per Cent of Buyers who manage CW on a global basis

0%

10%

20%

30%

40%

50%

60%

70%

2008 2009 2010 2011 2013 (P)

NA

WE

© 2011 Crain Communications Inc

Procurement in Lead

Source: 2005-2011 Contingent Workforce Buyer Survey

Per Cent of Buyers with Procurement taking lead in Staffing Supplier selection

0%

10%

20%

30%

40%

50%

60%

70%

80%

2005 2006 2007 2008 2009 2010 2011

NA

WE

© 2011 Crain Communications Inc

Supplier Management Strategies in Place

Source: 2011 Contingent Workforce Buyer Survey

Per Cent of Buyers with

strategies in place

82%

70%

63%

50%

46%

44%

40%

38%

37%

36%

35%

35%

31%

30%

30%

16%

Approved supplier list

Consolidating suppliers

Supplier tiering list

Master supplier

VMS

Significant use of domestic outsourcing

Increasing minority suppliers

Independent contractor compliance

Significant use of offshoring

MSP

Try new suppliers

Including SOW/consultants in programme

CW planning part of strategic planning

RPO

HRO

Global CW management

© 2011 Crain Communications Inc

Source: 2011 Contingent Workforce Buyer Survey

Per Cent of Buyers with

strategies planned over

next two years

Supplier Management Strategies Planned 9%

18%

23%

18%

39%

21%

24%

26%

23%

35%

30%

48%

56%

28%

26%

40%

Approved supplier list

Consolidating suppliers

Supplier tiering list

Master supplier

VMS

Significant use of domestic outsourcing

Increasing minority suppliers

Independent contractor compliance

Significant use of offshoring

MSP

Try new suppliers

Including SOW/consultants in programme

CW planning part of strategic planning

RPO

HRO

Global CW management

© 2011 Crain Communications Inc

Contingent Workforce Buyer Compensation

Source: 2011 Contingent Workforce Buyer Survey

<€49k

€50-74k

€75-99k

€100-149k

>€150k

Annual Base Salary 2010

Average Annual Base Salary 2010 = €88,200

Average Annual Increase 2009/2010 = 3.7%

13%

26%

26%

27%

8%

© 2011 Crain Communications Inc

Contingent Workforce Buyer Compensation

Source: 2011 Contingent Workforce Buyer Survey

None<€10k€10-19k€20-29k€30-39k>€40k

Annual Bonus (or other compensation ) 2010

Average Annual Bonus 2010 = €15,279

Median 2010= €10,000

11%

36%

22%

13%

9%

9%

© 2011 Crain Communications Inc

Any Questions?

20 June | 12:45 pm | Foyer Okura, Amstel, Heian I, White Leeuw

Optimum Sponsors: Alexander Mann Solutions | Allegis Group Services | Fieldglass | Gibbs S3 | IQNavigatorKellyOCG | Peopleclick Authoria | ProcureStaff Technologies | Volt Consulting Group | WorkforceLogic

Pinnacle Sponsors:

© 2011 Crain Communications Inc

Networking Lunch and Exhibit Time

Sponsored by:

20 June | 12:45 pm | Foyer Okura, Amstel, Heian I, White Leeuw