European Capital of Culture 2008 Socio-Economic Impact...

82

ERM Economics Suite 8.01, 8 Exchange Quay, Manchester, M5 3EJ Telephone 0161 958 8800 Facsimile 0161 958 8888 Email [email protected] http://www.erm.com FINAL REPORT Liverpool City Council European Capital of Culture 2008 Socio-Economic Impact Assessment of Liverpool's Bid May 2003

Transcript of European Capital of Culture 2008 Socio-Economic Impact...

ERM EconomicsSuite 8.01, 8 Exchange Quay,

Manchester, M5 3EJTelephone 0161 958 8800Facsimile 0161 958 8888Email [email protected]://www.erm.com

FINAL REPORT

Liverpool City Council

European Capital of Culture 2008

Socio-Economic Impact Assessment of Liverpool's Bid

May 2003

FINAL REPORT

Liverpool City Council

European Capital of Culture 2008

Socio-Economic Impact Assessment of Liverpool's Bid

May 2003

Reference 0001778

Prepared by: Kram Sadiq, Howard Walker, Steve Hutton, Hannah Artis

For and on behalf of ERM Economics

Approved by: Kram Sadiq

Signed: ______________________________

Position: Technical Director

Date: 14th May 2003

This report has been prepared by ERM Economics, a trading name of Environmental Resources Management Limited, with all reasonable skill, care and diligence within the terms of the Contract with the client, incorporating our General Terms and Conditions of Business and taking account of the resources devoted to it by agreement with the client.

We disclaim any responsibility to the client and others in respect of any matters outside the scope of the above.

This report is confidential to the client and we accept no responsibility of whatsoever nature to third parties to whom this report, or any part thereof, is made known. Any such party relies on the report at their own risk.

CONTENTS

1 INTRODUCTION 1

1.1 TERMS OF REFERENCE 11.2 CITIES, CULTURE AND COMPETITIVENESS 11.3 STUDY APPROACH 31.4 REPORT STRUCTURE 4

2 LIVERPOOL’S CAPITAL OF CULTURE PROGRAMME 5

2.1 CAPITAL OF CULTURE OBJECTIVES 52.2 PROGRAMMING OF EVENTS 52.3 ORGANISATION AND RESOURCES 82.4 SOCIAL INCLUSION STRATEGY 92.5 TARGETS AND OUTCOMES 112.6 CONCLUSIONS 13

3 CULTURAL INDUSTRIES 14

3.1 INTRODUCTION 143.2 ECONOMIC TRENDS 143.3 CULTURAL INDUSTRIES 163.4 CULTURAL INFRASTRUCTURE INVESTMENT 203.5 CONCLUSIONS 25

4 SOCIO-ECONOMIC IMPACTS 26

4.1 INTRODUCTION 264.2 CULTURAL INDUSTRIES 274.3 CREATIVE INDUSTRIES 354.4 PARTICIPATION 374.5 CONCLUSIONS 40

5 EVALAUTION STRATEGY 42

5.1 INTRODUCTION 425.2 FRAMEWORK PRINCIPLES 425.3 EXISTING DATA SOURCES 435.4 METHODOLOGIES 455.5 RECOMMENDED EVALUATION STRATEGY 47

6 CONCLUSIONS 56

6.1 LIVERPOOL’S CAPITAL OF CULTURE PROGRAMME 566.2 BASELINE CONTEXT 566.3 CITY WIDE INVESTMENT STRATEGY 576.4 SOCIO-ECONOMIC IMPACT 576.5 MONITORING AND EVALUATION STRATEGY 58

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

1

1 INTRODUCTION

1.1 TERMS OF REFERENCE

ERM Economics was commissioned by Liverpool City Council in February 2003 to undertake a socio-economic impact assessment of the European Capital of Culture bid. The terms of reference requested the commission to:

• Establish baselines, indicators and measurement tools for a full scale economic and social impact monitoring programme; and

• Articulate and quantify how the bid submission and programme of events and activities anticipated will contribute to:

• Increased competitiveness and sustainable economic growth;• Social and cultural benefits and increased community cohesion; and• Growth of the creative industries sector.

The primary focus of the commission was on assessing the economic impact that a successful Capital of Culture award could make to the City, Merseyside and the North West region and to outline a monitoring and evaluation framework to assess the socio-economic impacts over time.

1.2 CITIES, CULTURE AND COMPETITIVENESS

There is a developing momentum of research over the relationship between the role of cities, their cultural assets and the prosperity of regions and ultimately, nation states. In the UK the Urban Renaissance agenda as set out in the Urban White Paper, and the development of programmes such as theCore Cities, reflect the new importance attached to our cities. The European Capital of Culture award in many ways brings this together and focuses one on the relationship between culture in its widest sense and successful cities.

Studies point to a strong correlation between good design, quality public realm, investment in iconic buildings, positive image promotion, commerciality mixed with art and heritage and the increasing competitiveness of cities in Europe and beyond(1). Cities that invest in these well and over a sustained period are moving up the league tables for inward investment and business growth. Those that are not are falling behind. In particular a successful city can be seen as:

• A cultural icon and artefact: Successful cities have an unmistakable brand which they have created by understanding and mobilising their unique set of cultural resources and symbolic assets.

(1) Releasing the Potential of Our Core Cities, Comedia, April 2002

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

2

• A Place of creativity and innovation: The fuel which powers successful cities is talent, and talent is both derived from and drawn to places in which there is a rich environment of cultural creativity and innovation.

• Providing culture as central to quality of life: The range of activities and experiences which raise life above the mundane, which allow self-expression and which help to define and bind a communal identification.

Research provides an indication that excellence and critical mass in culture, art, sport etc are essential prerequisites to a competitive city and national economy. Studies have shown that cities which invest in culture are places of increasing attractiveness to new investment, business growth and sustainable jobs. Cities are centres of knowledge, skills and innovation and there is increasing evidence that creative people gravitate to cities with a rich and diverse cultural base (see Box 1.1).

Box 1.1 Characteristics of a Competitive City

Source: OECD, Cities for Citizens, December 2001, page 62

The concept of ‘drawing power’ provides a methodology for assessing the links between culture and competitiveness (1). This builds its analysis of the well-being of a city based on a range of hard and soft socio–economicindicators. These indicators provide a basket of measures that assess the dynamics of the city in how well it attracts people, new investment, develops new ideas and ultimately creates wealth.

(1) The Role of Core Cities in Creating Prosperous Regions: Critical Mass in Sport and Culture for Competitive Advantage, Comedia, Draft November 2002

• Economic diversity in the manufacturing and services sector.• A supply of skilled human capital. The successful cities and regions will be those that

have the people who can operate effectively in ‘the knowledge and information based’ industries.

• The right institutional networks. A range of links between higher education, research institutions, private industry and government.

• The right environment. Cities are for living in as well as working in. This means the right physical, social, and cultural environment. Economic prosperity cannot be sustained on a sea of vast inequality.

• Good communications. Partly this means physical communications – roads, airports,railroad links, electronic communications. But communications is also cultural. This underlines the importance of international networking.

• The institutional capacity to mobilize public, private and community resources and in the long term to deliver agreed economic and social strategies.

ERM ECONOMICS DRAFT REPORT LIVERPOOL CITY COUNCIL

3

Box 1.2 Cities, New Ideas and Creativity

Source: ‘Building the Region’s Knowledge Economy.’ Centre for Urban and Regional Development Studies. University of Newcastle, May 2001 The conclusion is that cultural investment is not separate or a poor relation to other investments eg transport, public realm or business promotion, but an integral part of a bigger package to enhance economic growth (see Box 1.2). Liverpool has an aim to be recognised the world over as a “city of creativity” and to reap the social and competitive advantages that such recognition will bring. The 2008 bid process itself has provided the opportunity for the City to radically revise and re-examine the way in which culture can be made central to the whole regeneration process and how the inherent creativity of the people of the City can be best harnessed to produce future success(1).

1.3 STUDY APPROACH

Our approach has drawn on methods that have been used to assess the potential impact of major events, such as the Capital of Culture, which are difficult to assess because of their diversity and the fact that the event is some years away. Liverpool has adopted a regeneration strategy that places the cultural industries, the development of its cultural infrastructure and the delivery of the culture strategy at the centre. Therefore, the growth of the cultural industries sector is a key indicator of the success of its regeneration programme. Our study is focused on estimating the potential socio-economic impacts of the expansion of the cultural industries in Liverpool as a result of three effects; trend based growth in the sector, the impact of planned investments in the sector and the impact and contribution of a successful European Capital of Culture award.

(1) Liverpool City Council's DCMS Bid Submission Supplementary Questions 31 March 2003

“The importance of the cosmopolitan city to its region is significant. Such cities are invariably the focus of migrants and the input of new ideas flowing from this tends to make them more creative than their hinterlands. In a region with a cosmopolitan city its effects as an economic motor and centre of innovation will be profound – both in terms of the generation of business and knowledge which can overspill into surrounding towns, but in its effect on the image of the region and the ability of the wider region to attract and successfully absorb mobile investment and skilled labour. The cosmopolitan city, then, attracts knowledge intensive activity, skilled labour, international tourists and business elites, all of which in turn introduce new ideas and creativity and generate a demand for quality and high value added goods and services, which in turn creates a more attractive environment capable of attracting more activity. Such a virtuous cycle of growth creates conditions in which the local population of a city and the wider region can benefit.”

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

4

We separate out the potential contribution of a successful Capital of Culture bid to show how such an award contributes to the overall thrust of the City’s cultural regeneration strategy. This contribution comes through a number of means, but the most measurable relate to the increase in tourism growth during 2008 and the legacy effect, and the increase in participation in cultural activity that the Capital of Culture strategy could generate. These combined effects effectively increase the utilisation of the City’s cultural assets with a range of associated benefits – in terms of jobs, income, community participation, a more dynamic industrial structure and raised image of the City in Europe.

1.4 REPORT STRUCTURE

This report is structured as follows:

Section 2: sets out Liverpool’s capital of culture programme;

Section 3: examines the socio-economic context and the role of the cultural industry sector within the overall economy of Liverpool;

Section 4: presents the findings of the socio-economic impact analysis;

Section 5: outlines the monitoring and evaluation plan; and

Section 6: contains our conclusions on the potential impact of the Capital of Culture bid.

Annexes:

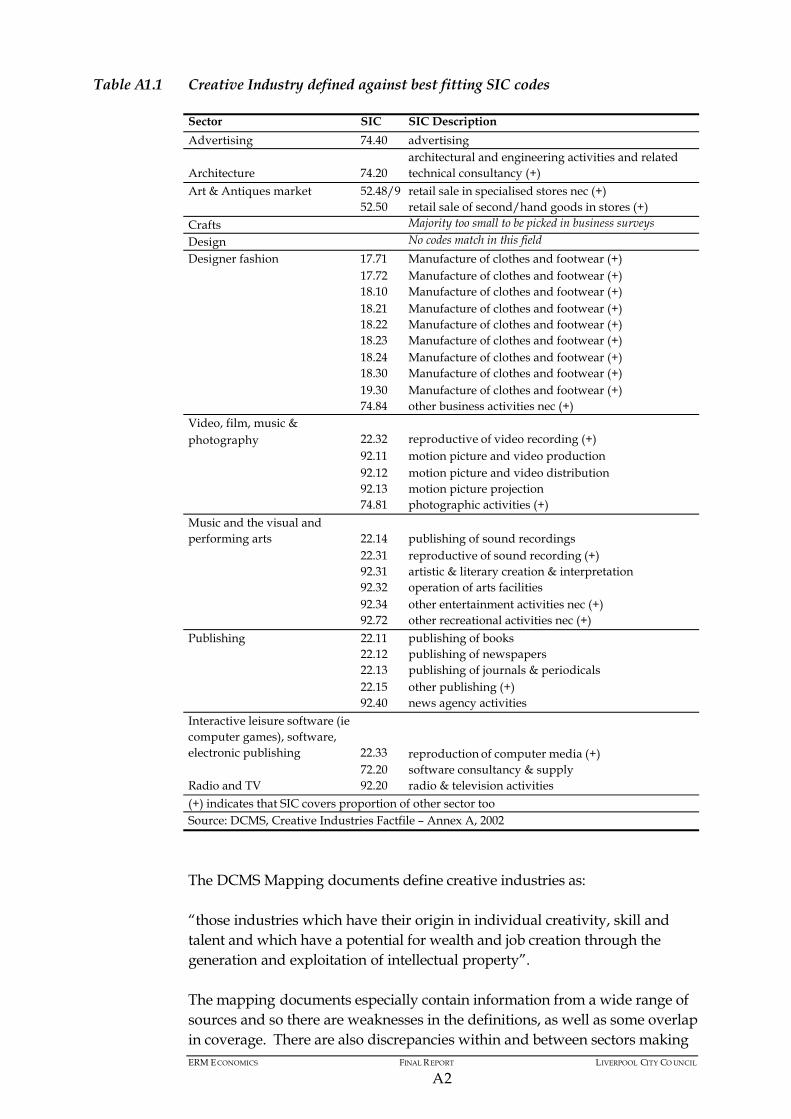

Annex A: Cultural and Creative Industries

Annex B: Socio-Economic Data

Annex C: Bibliography

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

5

2 LIVERPOOL’S CAPITAL OF CULTURE PROGRAMME

2.1 CAPITAL OF CULTURE OBJECTIVES

Liverpool’s European Capital of Culture programme is built on its history as a city with world links through trade and transportation. Liverpool’s central theme for 2008 is The World in One City. The outcomes that the City wishes to achieve through a successful Capital of Culture Bid are seen as threefold:

• Sustainable Cultural Infrastructure: To increase and enhance the culturalinfrastructure, encouraging new products, processes and enterprises in the cultural and creative industries sector;

• An Inclusive and Dynamic Community: To increase local participation in cultural activities and increase community cohesiveness; and

• A Premier European City: To improve the range and quality of the City’s infrastructure with City centre and community renewal.

The central theme The World in One City is underpinned by three sub-themesCreate, Participate and Regenerate, which will ensure that all involved in the year will have clear objectives and legacy from the year, illustrating the City’s history, dynamic present, and challenging vision for the future. Figure 2.1provides an overview of the programme and the way in which each element supports the overall aims of the bid.

The 2008 bid is viewed by the City Council and its partners as integral to the overall vision of Liverpool as a City. The vision is ‘For Liverpool City to become a premier European City. Achieved by build ing a more competitive economy, developing healthier, safer, and more inclusive communities and enhancing individual life chances’.

2.2 PROGRAMMING OF EVENTS

The ‘World in One City’ programme starts in 2003 with a `time-line` of themed years which aim to strengthen Liverpool’s ability to stage the Capital of Culture Year. The bid strategy recognises the importance of building up to the main event of 2008. In 2007 the City celebrates its 800th Anniversary since gaining its Royal Charter and the main programme of events planned for 2008 is the start of a process that will take the City forward with an increased level of confidence.

Renewal in local neighbourhoods

Celebrates Diversity. 800 Years of Culture.

A new urban experience

New products, innovations and businesses

New international links and

partnerships

A good place to live, work and

visit

Community involvement in corridor

improvements

Continued improvements to the

city centre offer

Travel, accommodation and service culture

Secure & enhance the cultural infrastructure

A city made whole through

cultural expression

A new expression of 21st Century

British Culture

A culture defined through participation

Inclusion

Diversity

Accessibility

Excellence

PARTICIPATE Include & Engage

CREATE Innovate & Sustain

REGENERATE Improve & Review

An Inclusive & Dynamic

Community

A Premier European City

A Sustainable Cultural Infrastructure

The World in One City

Figure 2.1 World in One City

ERM ECONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

7

Moreover, for the City it is vital that the legacy impacts are maximised. In order to achieve this after 2008 the City will run with themed years that look to the future. The year themes are:

2003: Celebrating Learning; 2004: Faiths and Community Service; 2005: Celebrating the Arts; 2006: Year of Sport; 2007: Celebrating Heritage; 2008: The World In One City; 2009: Celebrating the Environment; and 2010: Celebrating Innovation.

2.3 ORGANISATION AND RESOURCES

The delivery of the Bid programme will be through the Liverpool Culture Company (‘Culture Co’). See Figure 2.2.

Figure 2.2 The Liverpool Culture Company’s Organisational Structure

Source: Liverpool City Council

The key element of the new structure will be the appointment of a “Creative Director”, who will act as the Assistant Chief Executive of the Liverpool Culture Company and will also have a critical role as an advisor to the City Council. Working closely with the Council’s Chief Executive, the Creative Director will advise the Council’s Senior Management Team on how to

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

8

develop the creativity agenda within each Service Portfolio. This aims to ensure creativity will become a key crosscutting strand linking mainstream service delivery in the common purpose of making residents and visitors alike recognise Liverpool as an exceptional city in regional, national, European and international terms. This approach will provide added value in areas of city management while at the same time providing integration in policy and action-planning terms. Another key role for the Creative Director will be the development and delivery of events programming.

In support of the Liverpool Culture Company are the following groups:

• The Stakeholders' Group. This is a group of 100 individuals who both represent a wide range of organisations associated with the Bid and/or have a contribution to make to the culturally-driven renaissance of Liverpool;

• The Cultural Diversity Group. The cultural map of Liverpool is grounded in the experiences of traditionally under-represented groups and individuals. This Cultural Diversity Group ensured Liverpool's diverse communities were given a strong voice in the bid planning stages;

• The Regeneration Stakeholders' Group. The bid process has brought together key members of the significant number of Liverpool organisations concerned in regeneration, and

• A Communications Team and a Communications Advisory Group havemanaged the marketing of the bid. It is drawn from the radio, television, press and PR community, in the city and the wider region.

The revenue budget allocated to the Liverpool Culture Company is £54.7m to cover the core areas of administration, programming and marketing. The marketing budget will be approximately £4.3m over the period to 2008.

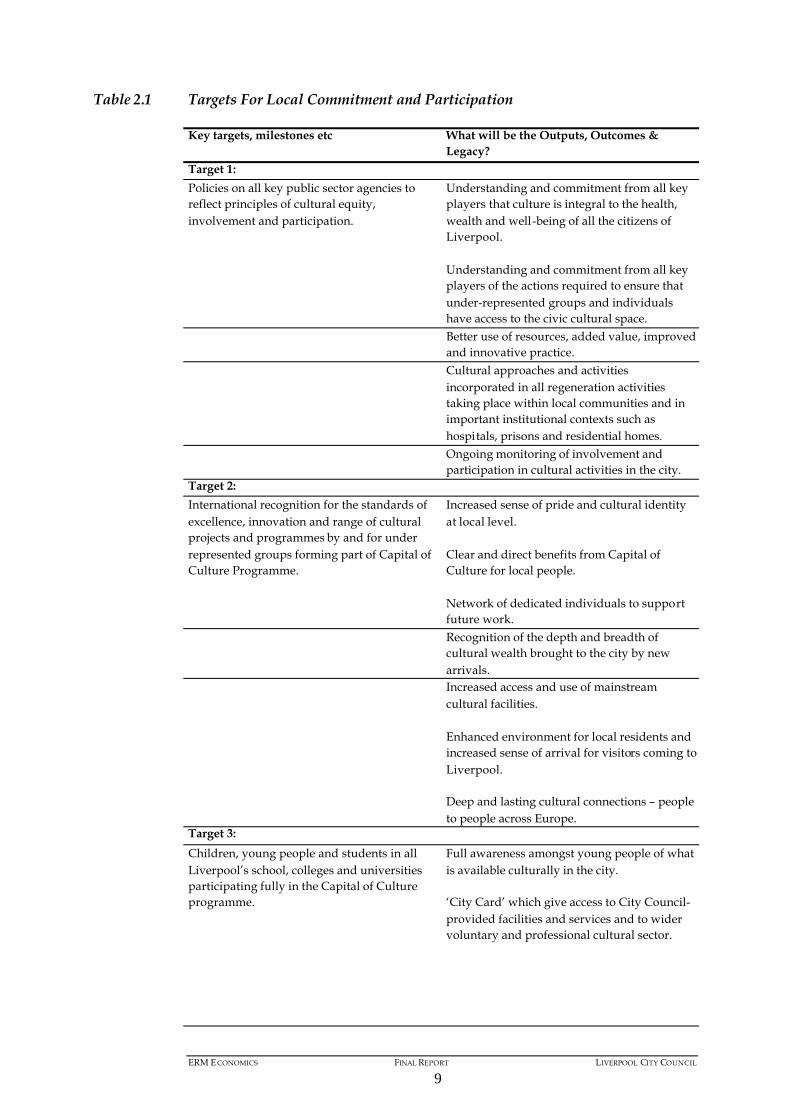

2.4 SOCIAL INCLUSION STRATEGY

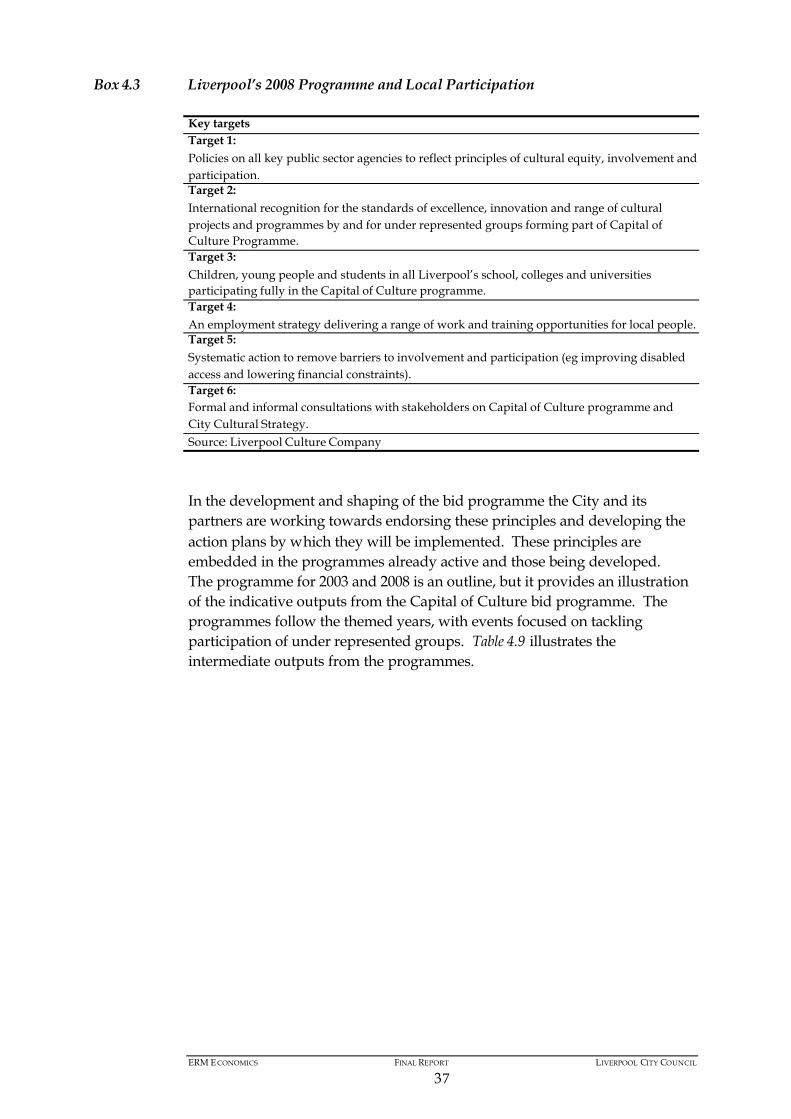

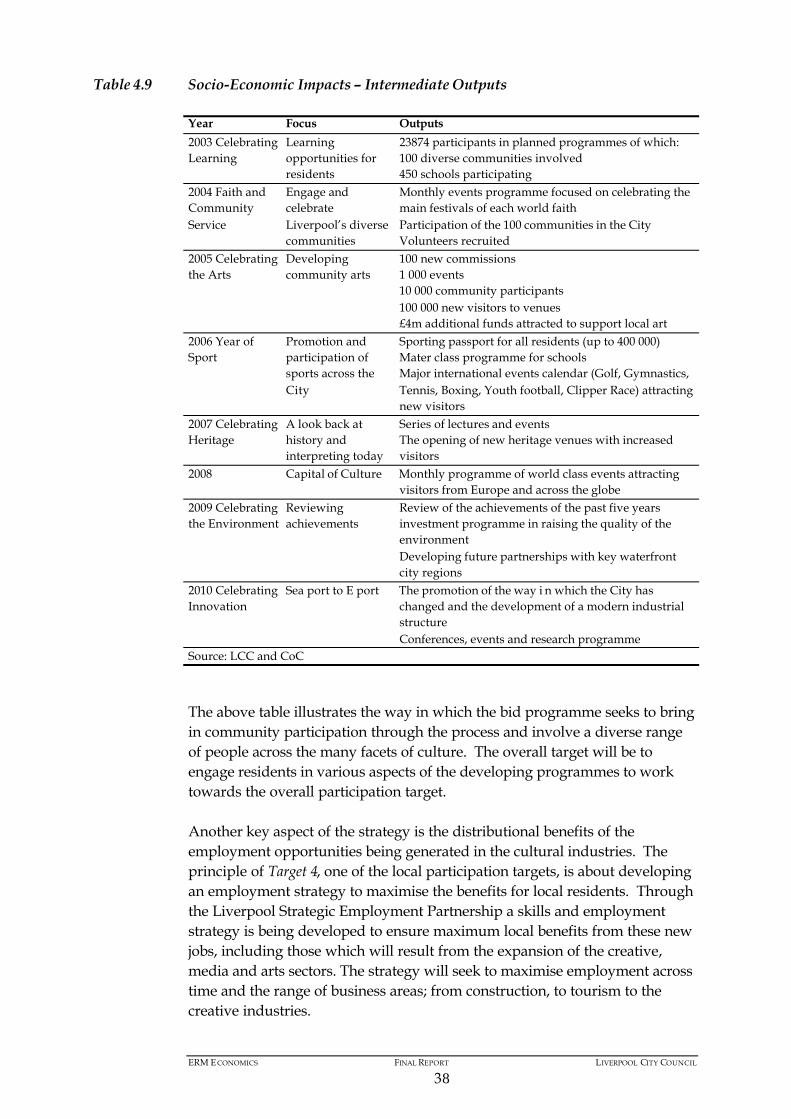

Central to the 2008 programme strategy is the increased participation of local residents cultural activities as users of cultural industry services and benefiting from employment in the sector (from leisure services to the creative industries). These principles are reflected in the bid programme through six targets related to participation and increasing participation of under -represented groups. Table 2.1 details the targets and the expected outcomes.

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

9

Table 2.1 Targets For Local Commitment and Participation

Key targets, milestones etc What will be the Outputs, Outcomes & Legacy?

Target 1:Policies on all key public sector agencies to reflect principles of cultural equity, involvement and participation.

Understanding and commitment from all key players that culture is integral to the health, wealth and well-being of all the citizens of Liverpool.

Understanding and commitment from all key players of the actions required to ensure that under-represented groups and individuals have access to the civic cultural space.Better use of resources, added value, improved and innovative practice.Cultural approaches and activities incorporated in all regeneration activities taking place within local communities and in important institutional contexts such as hospitals, prisons and residential homes.Ongoing monitoring of involvement and participation in cultural activities in the city.

Target 2:International recognition for the standards of excellence, innovation and range of cultural projects and programmes by and for under represented groups forming part of Capital of Culture Programme.

Increased sense of pride and cultural identity at local level.

Clear and direct benefits from Capital of Culture for local people.

Network of dedicated individuals to supportfuture work.Recognition of the depth and breadth of cultural wealth brought to the city by new arrivals.Increased access and use of mainstream cultural facilities.

Enhanced environment for local residents and increased sense of arrival for visitors coming to Liverpool.

Deep and lasting cultural connections – people to people across Europe.

Target 3:Children, young people and students in all Liverpool’s school, colleges and universities participating fully in the Capital of Culture programme.

Full awareness amongst young people of what is available culturally in the city.

‘City Card’ which give access to City Council-provided facilities and services and to wider voluntary and professional cultural sector.

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

10

Key targets, milestones etc What will be the Outputs, Outcomes & Legacy?

Target 4:An employment strategy delivering a range of work and training opportunities for local people.

A highly professional cultural and creative industries workforce, capable of leading regional and national as well as city developments.

Target 5:Systematic action to remove barriers to involvement and participation (eg improving disabled access and lowering financial constraints).

Raised levels of mental and physical well-being.

More engaged citizens.Target 6:Formal and informal consultations with stakeholders on Capital of Culture programme and City Cultural Strategy.

A city where the stakeholders have a proper sense of ownership and involvement in its ongoing Cultural Strategies.

Source: Liverpool Capital of Culture

2.5 TARGETS AND OUTCOMES

The bid programme contains 12 overall targets linked to the potential outcomes with a selection based on local, regional, national, European and Worldwide objectives.

Table 2.2 Targets and Outcomes

LOCAL Objectives Targets Outcomes

1. A stakeholding residential base that is proud of its city and committed to the project.

1.1 25 000 ‘champions’ by 2007

A society of stakeholders

2. A culturally aware and active community.

2.1 ‘Cluster’ areas linked together through cultural programmes and events.

2.2 75% of the residential population involved in some cultural activity and attendance figures rise to over 100 on national index.

2.3 One unique, world-classcultural event/year 2005 – 7; 4 in 2008.

More residents involved in all aspects of the cultural life of the city – sense of pride, ownership, personal fulfilment.

Improved attendances at performances, events and exhibitions generating sustainability.

Credibility of City’s cultural claim.

3. Reinforce image as a visitor friendly city

3.1 1000 cabbies trained;

3.2 3000 frontliners trained.

Sustainability of improvement to tourism.

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

11

REGIONAL Objectives

4. Consolidating Liverpool’s regional role for business and tourism.

4.1 Liverpool as a key destination in the North West for cultural, creative and tourism businesses.

A strong regional position.

Higher levels of inward investment.

5. Enhancing regional partnerships and campaigns.

5. 1A dynamic and fruitful relationship with all marketing partners across the North West.

Best value and maximum impact.

6. Increasing visitor number from rest of region.

6. 1 An increase of 30% above benchmark by 2008.

Significant increase in visitors from the region.

NATIONAL Objectives

7. Re-positioning the city’s national image – to be in top 10 in UK image league.

7. 1 An increase in the propensity to visit Liverpool.

Significant increase in visitor enquiries against benchmark.

8. Increasing numbers and length of stay of visitors from UK – leisure and conference.

8.1 Anticipated 10% growth year on year until 2005 and accelerating to an average of 15% growth until 2010

Significant increase in visitor numbers and length of stay.

EUROPEAN Objectives

9. Reposition with cultural image focusing on strengths, especially in visual arts and popular culture.

9.1 An increase in the propensity to visit Liverpool.

Significant increase in visitor enquiries against benchmark.

10. Increasing numbers andlength of stay of visitors from Europe.

10.1 Anticipated 6 – 7%growth year on year

(3 – 4% above standard).

Significant increase in visitor numbers and lengths of stay.

WORLDWIDE Objectives

11. Building on cultural reputation to promote Liverpool as a world city.

11.1 An increase in the propensity to visit Liverpool.

Significant increase in visitor enquiries against benchmark.

12. Establish as premier ‘must do’ destination on UK itinerary – increasing numbers and length of stay visitors from the rest of the world – particular focus on USA and Japan.

12.1 Increase proportion of overseas visitors to 40% (2000 base = 24%)

Significant increase in visitor numbers and lengths of stay.

Source: Liverpool City Council

The outcomes are to be achieved through the synergy of existing city-wideinvestment programmes and activities with the potential impact that Capital of Culture could realise in the run up to 2008, the year itself and through the legacy effect.

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

12

2.6 CONCLUSIONS

The Liverpool European Capital of Culture bid is based around a set of themed years that cover the wide spectrum of activity that forms modern culture. These themed years run to 2008 and beyond, reflecting the City’s approach which places emphasis on not just 2008, but the build up and the legacy impact. The programme is supported by 12 targets which identify the areas which the bid programme seeks to influence at the local, regional, national and world level. These targets will form the basis of the monitoring programme.

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

13

3 CULTURAL INDUSTRIES

3.1 INTRODUCTION

In this section we provide a baseline of the role of the cultural industries in Liverpool. This covers employment and growth of the sector, as well as participation by residents in the services provided by cultural industries.Firstly we recap on recent socio-economic trends in Merseyside and the City.

3.2 ECONOMIC TRENDS

3.2.1 Recent Growth

The Merseyside economy over the late 1990s is a tale of slower than regional and national growth in gross value added (GVA) and faster growth in employment(1). The slower growth in value added is as a result of industry structure and growth biased to lower value added (and therefore lower average wage) sectors. It is interesting to note that if Halton district – heavily affected by the restructuring of the Chemicals sector - is excluded from the analysis then GVA growth over the period 1995 to 2001 was positive at 1 per cent and slightly above the region. Growth in value added has been led by Knowsley (1.8 per cent) and Liverpool (1.0 per cent).

Employment growth was greatest in Knowsley (12.9 per cent), St Helens (7.7 per cent) and Liverpool (2.3 per cent). A third of employment in the conurbation is located in Liverpool. Employment growth has been driven by the health sector, communications, financial and business services, and cultural and leisure services.

The Merseyside Economic Review 2002 points to other key trends including:

• Faster growth in R&D expenditure: since 1995 Merseyside has seen R&D spending grow almost three times as fast as the rest of the UK;

• Increased income: the earning gap between Merseyside and the North West has closed over the period 1999 – 2001;

• Falling unemployment: reflecting the growth in employment, there has been a sharp fall in unemployment between 1999 and 2001 (from 11. 2 per cent to 5.7 per cent);

• Unemployment falling in deprived areas: the fall in unemployment has been felt in the more deprived areas of the conurbation;

(1) Merseyside Economic Review 2002

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

14

• Increase in Skills and Qualifications: the change in the skills base is mixed, but with a marked improvement in the number of residents with NVQ 3, 4, and 5;

• Slow down in population decline: the population of the conurbation has declined but at a slower rate; and

• City centre expansion: the City centre has acted as a key driver of growth in employment over the past five years.

3.2.2 City Centre Renaissance

The population of Liverpool is 439 473 and it is the fifth largest city in England and Wales. Whilst the City has seen a fall in population over the last 10 years (1991-2001) of 8.2 per cent, there has been slow down in the decline and a change in the location of residents showing signs of an urban renaissance.Research carried out jointly by Liverpool City Council and the University of Liverpool in 1999(1), found that since 1991 the city centre's population has grown by almost 300 per cent - from 2340 in 1991 to approximately 9000 by 1999. The results of a city centre living survey found that new residents moving into the city centre. Car ownership amongst professionals in the city centre is lower than in the city as a whole, and there is a noticeably higher proportion of people who walk to work. The research concluded that in Liverpool, city centre living does appear to promote more sustainable lifestyles. It is having a positive effect on social mix.

The city centre has seen fast employment growth at 7 per cent during the period 2001 to 2006. The city centre is identified as a strategic site for the region and an important contributor to economic and employment growth in the future.

3.2.3 Economic Prospects

The forecast for Merseyside is that, over the medium term, economic growth is expected to increase. It is forecast that growth in value added will accelerate rapidly to 2005 by an average of 1.4 per cent(2). This projection remains slower than the region and the UK, but is expected to be fast enoughto narrow the gap between Merseyside and the region/UK. This growth is expected to be led by the knowledge sectors such as health, education, financial services, communications and cultural and leisure activities.

The 2008 Capital of Culture bid programme and the development of the cultural infrastructure over the next five years will contribute to the expected changes in the economy over the medium to long term. The Merseyside Economic Assessment recognises the importance of the city centre and the

(1) “City Centre Living as the Spring Board for Regeneration? Some lessons from Liverpool” by Moss Madden, Vicki Popplewell and Ian Wray. University of Liverpool Department of Civic Design, Working Paper 59, May 2001.(2) Experien Business Strategies Ltd forecast as part of the Merseyside Economic Review.

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

15

major cultural investments (such as the FACT centre and Kings Waterfront) in promoting increased growth in the City.

3.3 CULTURAL INDUSTRIES

3.3.1 Introduction

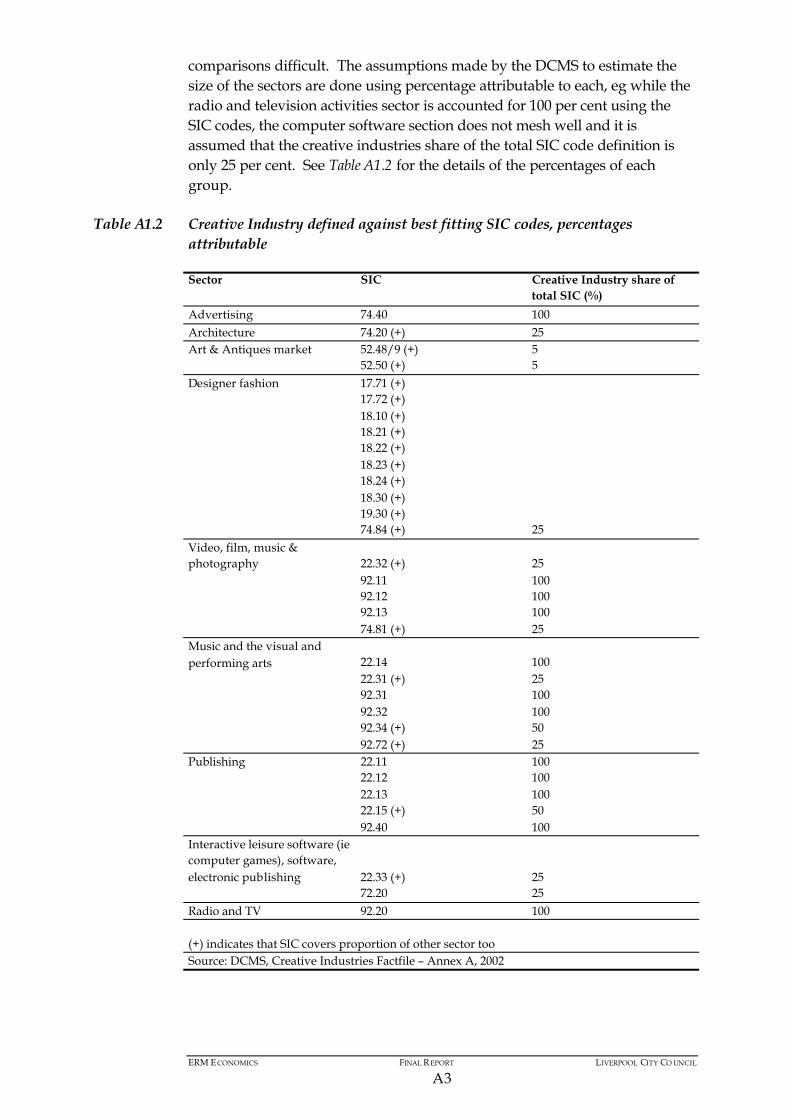

The strategy adopted by Liverpool in its 2008 bid programme and its broader approach to the regeneration of the City is to view the cultural industries in its entirety, recognising the importance of the creative industries for the future of the City. In this report we define the ‘cultural industries’ as the combination of tourism, creative industries, sports and heritage and examine the recent trends in the development of this broad sector, as part of the overall growth of Liverpool. (Annex A provides a summary on the classification of the sector).

In this section we present baseline analysis of the cultural industries sector based on two key sources. The first is the preliminary results of a cultural industries benchmarking study for the North West and Merseyside and the second source uses information from the annual business surveys. The later provides data at the Liverpool as well as other spatial levels, over time.

3.3.2 Regional Benchmarking Study

The North West Benchmarking Study conducted by the Regional Intelligence Unit (March 2003) provides a more up to date and comprehensive overview of the cultural industries sector than national datasets. The study looked at the North West and therefore enables a comparison with the North West using the same methodology.

The analysis shows that there is an estimated 393 000 employees in the cultural industries (defined as including creative industries, tourism and heritage, and sports and leisure) in the North West, of which 61 000 are employed on Merseyside. This scale of employment is higher than that captured by the annual employment surveys and is partly accounted for by including the self-employed.

Of these 61 000 some 10 000 are estimated to be self-employed, the majority of which are in the creative industry sub sector. Over a third of the workforce in the creative industries sub-sector are self-employed, compared to 6 per cent in tourism and 9 per cent in sport. The number of cultural industry enterprises is estimated at 5745 across the conurbation.

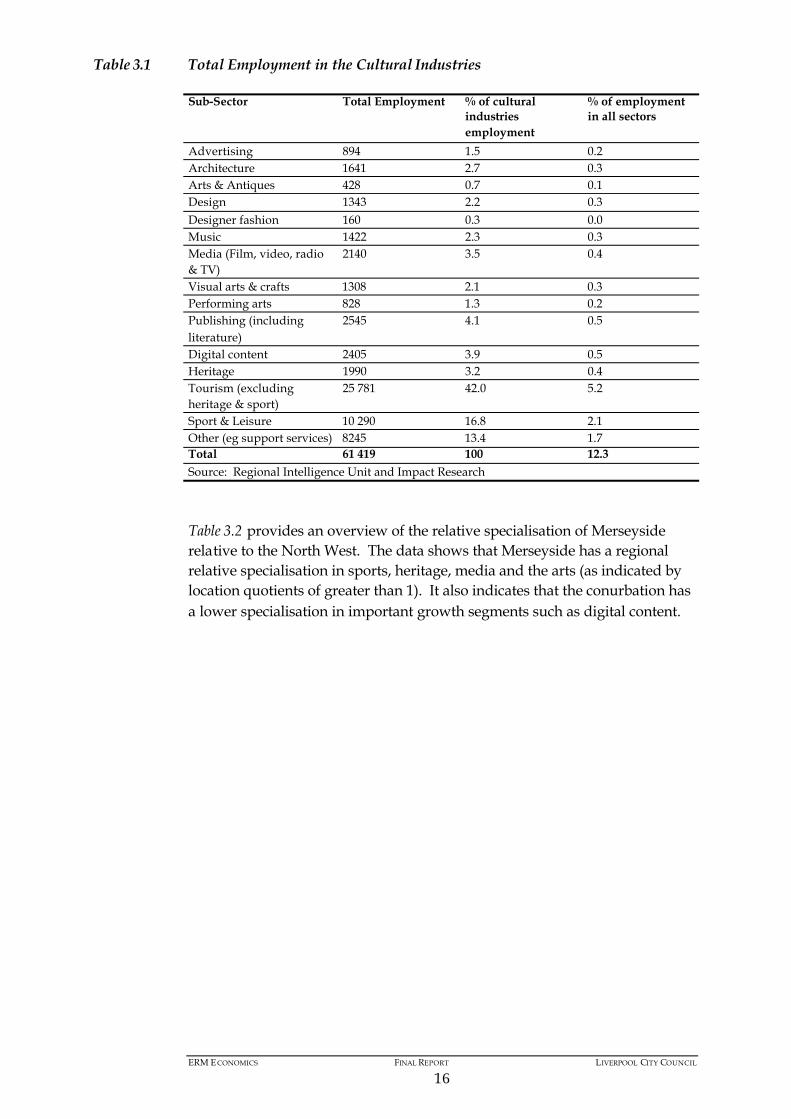

Table 3.1 provides details of employment by activity. This shows that tourism is the biggest sub-sector employing some 42 per cent of the cultural industries workforce, followed by the creative industries at 38 per cent. Publishing, digital content and media are important elements of the creative industries.

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

16

Table 3.1 Total Employment in the Cultural Industries

Sub-Sector Total Employment % of cultural industriesemployment

% of employment in all sectors

Advertising 894 1.5 0.2Architecture 1641 2.7 0.3Arts & Antiques 428 0.7 0.1Design 1343 2.2 0.3Designer fashion 160 0.3 0.0Music 1422 2.3 0.3Media (Film, video, radio & TV)

2140 3.5 0.4

Visual arts & crafts 1308 2.1 0.3Performing arts 828 1.3 0.2Publishing (including literature)

2545 4.1 0.5

Digital content 2405 3.9 0.5Heritage 1990 3.2 0.4Tourism (excluding heritage & sport)

25 781 42.0 5.2

Sport & Leisure 10 290 16.8 2.1Other (eg support services) 8245 13.4 1.7Total 61 419 100 12.3Source: Regional Intelligence Unit and Impact Research

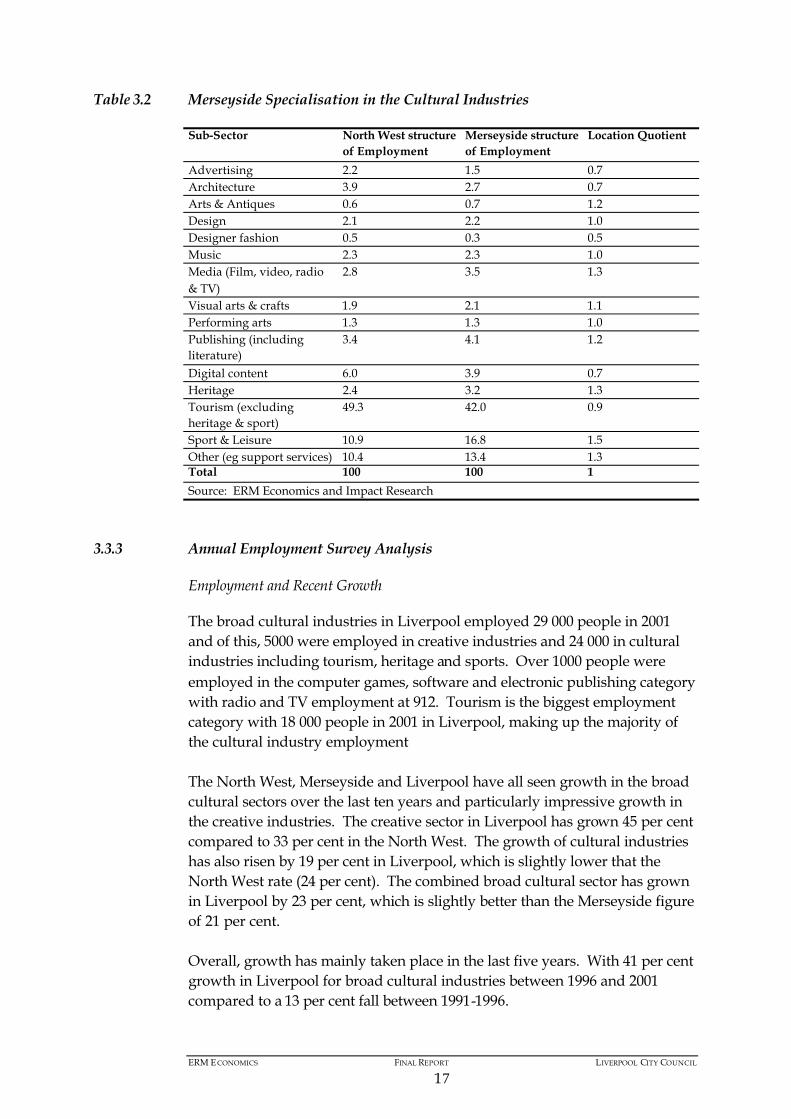

Table 3.2 provides an overview of the relative specialisation of Merseyside relative to the North West. The data shows that Merseyside has a regional relative specialisation in sports, heritage, media and the arts (as indicated by location quotients of greater than 1). It also indicates that the conurbation has a lower specialisation in important growth segments such as digital content.

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

17

Table 3.2 Merseyside Specialisation in the Cultural Industries

Sub-Sector North West structure of Employment

Merseyside structure of Employment

Location Quotient

Advertising 2.2 1.5 0.7Architecture 3.9 2.7 0.7Arts & Antiques 0.6 0.7 1.2Design 2.1 2.2 1.0Designer fashion 0.5 0.3 0.5Music 2.3 2.3 1.0Media (Film, video, radio & TV)

2.8 3.5 1.3

Visual arts & crafts 1.9 2.1 1.1Performing arts 1.3 1.3 1.0Publishing (including literature)

3.4 4.1 1.2

Digital content 6.0 3.9 0.7Heritage 2.4 3.2 1.3Tourism (excluding heritage & sport)

49.3 42.0 0.9

Sport & Leisure 10.9 16.8 1.5Other (eg support services) 10.4 13.4 1.3Total 100 100 1Source: ERM Economics and Impact Research

3.3.3 Annual Employment Survey Analysis

Employment and Recent Growth

The broad cultural industries in Liverpool employed 29 000 people in 2001 and of this, 5000 were employed in creative industries and 24 000 in cultural industries including tourism, heritage and sports. Over 1000 people were employed in the computer games, software and electronic publishing category with radio and TV employment at 912. Tourism is the biggest employment category with 18 000 people in 2001 in Liverpool, making up the majority ofthe cultural industry employment

The North West, Merseyside and Liverpool have all seen growth in the broad cultural sectors over the last ten years and particularly impressive growth in the creative industries. The creative sector in Liverpool has grown 45 per cent compared to 33 per cent in the North West. The growth of cultural industries has also risen by 19 per cent in Liverpool, which is slightly lower that the North West rate (24 per cent). The combined broad cultural sector has grown in Liverpool by 23 per cent, which is slightly better than the Merseyside figure of 21 per cent.

Overall, growth has mainly taken place in the last five years. With 41 per cent growth in Liverpool for broad cultural industries between 1996 and 2001 compared to a 13 per cent fall between 1991-1996.

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

18

The creative sector growth was 43 per cent for Liverpool between 1991 and 1996, which was significantly higher than either Merseyside (30 per cent) or the North West (9 per cent). In the same period the level of employment in the cultural sector fell, causing the overall growth in the broad cultural industries to decrease.

The cultural industries grew strongly from 1996 to 2001 in Liverpool, Merseyside and the North West. Liverpool’s cultural industries grew by 55 per cent and Merseyside and the North West by 34 per cent and 25 per cent respectively.

The percentage of the workforce of creative and cultural industries employment compared to total employment has been steadily increasing. In Liverpool the creative industries accounted for 2 per cent of the total workforce in 1991 growing to 3 per cent by 2001. Cultural industries rose from 10 per cent in 1991 to 11 per cent in 2001, with the broad cultural industries accounting for 14 per cent of total workforce in 2001, compared to 12 per cent for Merseyside and the North West.

Sub Sector Analysis

The creative industries break-down to include film, music, architecture, publishing, computer games, software, electronic publishing, radio and TV, advertising, designer fashion and arts/antique trade. As described, Liverpool has seen an overall growth in the last ten years of its creative industries and the leaders in this growth have been radio and TV (183 per cent), designer fashion (191 per cent), and computer games, software and electronic publishing (154 per cent). This compares to the North West leading creative industries being designer fashion (202 per cent) and computer games, software and electronic publishing (165 per cent), with radio and TV growing only 86 per cent in the North West.

Box 3.1 Did you know?

Looking at five year interval growth advertising grew 380 per cent from 1991 to 1996 and computer games, software and electronic publishing 141 per cent.From 1996 to 2001 radio and TV (126 per cent) and designer fashion (176 per cent) had the strongest growth, advertising have a negative growth figure of 85 per cent and computer games, software and electronic publishing slowing to 6 per cent growth.

Mersey Television is the largest regional independent production company in the UK, with a turnover of £3.9 million in 1998/9. New Media, Film and Television employs over 62,000 and the sector has a combined turnover of C£6.45 billion.

Sector profile for ICT/New Media in the North West Region, Amtek, 2000 report estimated that the total value of the sector to the regional economy £6.45 billion, with concentrations of activity in Liverpool (£757 million) and Manchester (£1.26 billion).

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

19

The cultural industries are heritage, sport, entertainment and tourism and of these tourism is by far the largest. Liverpool experienced a 55 per cent increase in heritage and tourism from 1991 to 2001.

City Comparisons

Within the creative industries we have seen that Liverpool has had 45 per cent growth compared to Oxford with 62 per cent and the nearest competitor, Cardiff, with 33 per cent.

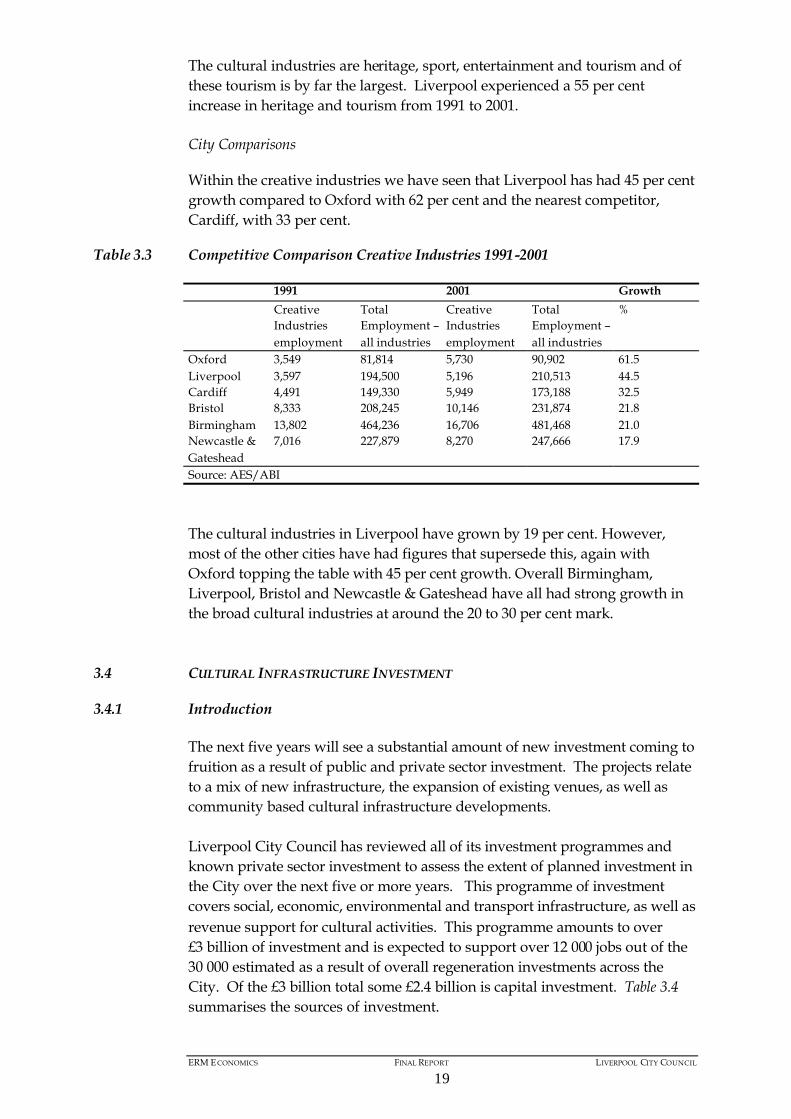

Table 3.3 Competitive Comparison Creative Industries 1991-2001

1991 2001 GrowthCreativeIndustriesemployment

TotalEmployment –all industries

CreativeIndustriesemployment

TotalEmployment –all industries

%

Oxford 3,549 81,814 5,730 90,902 61.5Liverpool 3,597 194,500 5,196 210,513 44.5Cardiff 4,491 149,330 5,949 173,188 32.5Bristol 8,333 208,245 10,146 231,874 21.8Birmingham 13,802 464,236 16,706 481,468 21.0Newcastle & Gateshead

7,016 227,879 8,270 247,666 17.9

Source: AES/ABI

The cultural industries in Liverpool have grown by 19 per cent. However, most of the other cities have had figures that supersede this, again with Oxford topping the table with 45 per cent growth. Overall Birmingham, Liverpool, Bristol and Newcastle & Gateshead have all had strong growth in the broad cultural industries at around the 20 to 30 per cent mark.

3.4 CULTURAL INFRASTRUCTURE INVESTMENT

3.4.1 Introduction

The next five years will see a substantial amount of new investment coming to fruition as a result of public and private sector investment. The projects relate to a mix of new infrastructure, the expansion of existing venues, as well as community based cultural infrastructure developments.

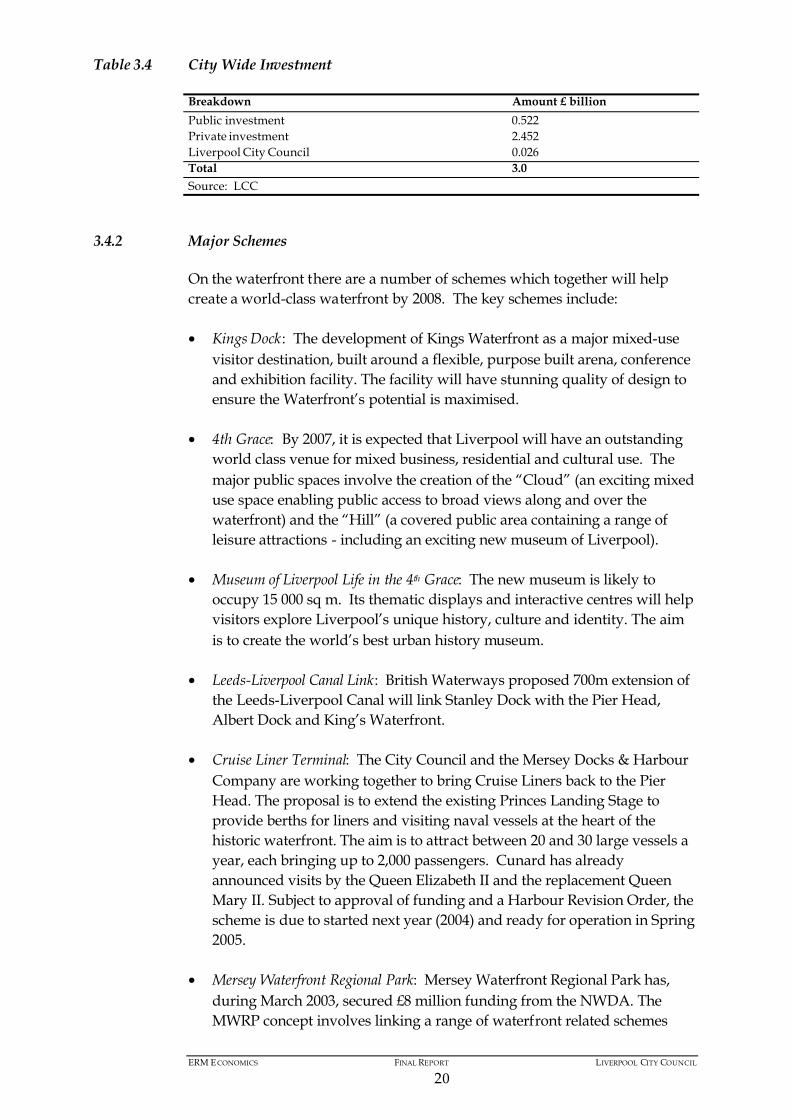

Liverpool City Council has reviewed all of its investment programmes and known private sector investment to assess the extent of planned investment in the City over the next five or more years. This programme of investment covers social, economic, environmental and transport infrastructure, as well as revenue support for cultural activities. This programme amounts to over £3 billion of investment and is expected to support over 12 000 jobs out of the 30 000 estimated as a result of overall regeneration investments across the City. Of the £3 billion total some £2.4 billion is capital investment. Table 3.4summarises the sources of investment.

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

20

Table 3.4 City Wide Investment

Breakdown Amount £ billionPublic investment 0.522Private investment 2.452Liverpool City Council 0.026Total 3.0Source: LCC

3.4.2 Major Schemes

On the waterfront there are a number of schemes which together will help create a world-class waterfront by 2008. The key schemes include:

• Kings Dock: The development of Kings Waterfront as a major mixed-usevisitor destination, built around a flexible, purpose built arena, conference and exhibition facility. The facility will have stunning quality of design to ensure the Waterfront’s potential is maximised.

• 4th Grace: By 2007, it is expected that Liverpool will have an outstanding world class venue for mixed business, residential and cultural use. The major public spaces involve the creation of the “Cloud” (an exciting mixed use space enabling public access to broad views along and over the waterfront) and the “Hill” (a covered public area containing a range of leisure attractions - including an exciting new museum of Liverpool).

• Museum of Liverpool Life in the 4th Grace: The new museum is likely to occupy 15 000 sq m. Its thematic displays and interactive centres will help visitors explore Liverpool’s unique history, culture and identity. The aim is to create the world’s best urban history museum.

• Leeds-Liverpool Canal Link: British Waterways proposed 700m extension of the Leeds-Liverpool Canal will link Stanley Dock with the Pier Head, Albert Dock and King’s Waterfront.

• Cruise Liner Terminal: The City Council and the Mersey Docks & HarbourCompany are working together to bring Cruise Liners back to the Pier Head. The proposal is to extend the existing Princes Landing Stage to provide berths for liners and visiting naval vessels at the heart of the historic waterfront. The aim is to attract between 20 and 30 large vessels a year, each bringing up to 2,000 passengers. Cunard has already announced visits by the Queen Elizabeth II and the replacement Queen Mary II. Subject to approval of funding and a Harbour Revision Order, the scheme is due to started next year (2004) and ready for operation in Spring 2005.

• Mersey Waterfront Regional Park: Mersey Waterfront Regional Park has, during March 2003, secured £8 million funding from the NWDA. The MWRP concept involves linking a range of waterfront related schemes

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

21

under one umbrella and adding value to them where appropriate. Mersey Waterfront has been recognised by partners in the Northwest as an asset of international importance.

Other wider developments include:

• The FACT Centre: The £10.5 million Film, Art, Creative Technology (FACT) centre opened in February 2003. Located at the heart of the city centre, it comprises 3 state of the art cinemas, 2 galleries and exhibition and event spaces showcasing an international programme of film, videoand new media projects, alongside resources, spaces, programmes and partnerships dedicated to the development and production of new and emerging forms of creativity using digital media technologies.

• Liverpool Philharmonic Centre: The proposed Liverpool Philharmonic Centre development remains central to the achievement of the Royal Liverpool Philharmonic’s vision. It is expected that significant further work on partnerships, design and fundraising for this project will start in 2004, and that building work is unlikely to commence before 2007, should the Centre’s further development and planning be successfully completed.

• The Bluecoat: Bluecoat Arts Centre is at an advanced stage (RIBA Stage C+) of an £8m project to renovate and extend its beautiful 18th century Grade 1 listed building. The development will restore the historic fabric of this Queen Anne building and construct a new wing that will house a gallery for its award winning exhibition programme and a performance space for dance, music, literature, live art and community projects.

The National Museums and Galleries on Merseyside (NMGM) have a number of project planned including:

• The Walker Art Gallery: A £4.3m scheme to renovate and improve the Walker was re-opened by the Queen in July 2002. In 2004, the final stage of the renovation will be completed with the opening of a Crafts and Design Gallery.

• Sudley House : Conservatory renovation and structural repairs to the conservatory of this Grade II listed house, museum and gallery are planned. The installation of level access from the courtyard is also planned for autumn 2003 costing £58 000. This will greatly improve access to the building.

• Liverpool Museum: A £30m development will be completed in winter 2004/05 and will provide eight new attractions, including a World Cultures Gallery, a new aquarium and the InfoWorld theatre for multi-media presentations and performance. These developments will be complemented by the development of a £1.5m space, ‘Impact’, which will explore the wide range of forces that created the planet and continue to

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

22

shape its surface. The developments will form a key part of the strategy to double the number of visits to Liverpool Museum by the end of 2005.

• St George’s Hall: Liverpool City Council, with support from the Heritage Lottery Fund and ERDF, is undertaking a major £18m refurbishment project to restore the Hall as Liverpool’s premier cultural venue. Work commenced on site in September 2002 and it is programmed to take 18 months to complete. The Hall will be re-launched in April 2005 as a venue for cultural, community, civic, corporate and performing arts activities.

• Film Studios: The Film Studios, which are five spaces in total, opened in June 2003 at a total cost of £1.5million. The Directors would like to extend the studios for which they need a further £0.5 million. They have applied for a Special Investment Loan. So far many commercials and short films have been shot there, as well as one full-length feature ‘The Virgin of Liverpool’. The lettable parts of the complex, which amount to some 400 units in total, are now 75 per cent let.

• Libraries: The Central Library and Archive will be redeveloped as the £30m “World Discovery Centre”, designed to radically enhance this Grade II* listed building. Visits will increase from 600 000 to 1 million per year with the Liverpool Record Office, the busiest local authority record office outside of Kew, being rebuilt. Now out to tender, interviews for the consortia to develop outline design proposals take place in April, prior to a Heritage Lottery Fund application. DCMS PFI credits for 2005/06 are also being bid for.

• Paradise Street Development Area: The PSDA retail-led mixed use development, due for completion in 2007/08, represents a wholly private sector, £750 million direct capital investment, and is a key element of Liverpool’s wider regeneration strategy. It includes part of the nominated World Heritage site, and will provide for economic and social growth and improvement through a high quality, integrated and fully accessible development. It will benefit not only the continuing physical renaissance of the City Centre, but also the wider area, whilst preserving and enhancing historic fabric of international importance.

• Liverpool Football Club: Liverpool Football Club has announced its intention to build a new 60,000 seat stadium close to its existing home at Anfield. Planning permission will be sought this summer for the £100m development. The new stadium will be a catalyst for the regeneration of the Anfield area. It will include a new Education Innovation Centre; a replacement Vernon Sangster Sports Centre and will also result in a net increase in greenspace for use by the local community.

• Merseytram: On the 10th December 2002, the Government announced the go-ahead for Merseytram by giving outline approval of £170 million towards the £225 million cost of building Line 1 of the proposed 3-line

ERM ECONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

23

network. Subject to progress Merseytram Line 1 is planned to open in 2006/07.

• Lime Street Station: The station and its surrounding environment will be

dramatically transformed in terms of facilities, access and overall environment in an initiative being developed as a partnership between Liverpool Vision, MerseyTravel and Network Rail. Phase 1 of the scheme is estimated to cost approximately £15 million. One of the most noticeable early outcomes of the scheme will be the return of the entrance façade to its former state.

3.4.3 Summary of Investment

Based on an analysis of the database of project supplied by Liverpool City Council, we have estimated the number of planning projects that will contribute to the broad cultural infrastructure of the City. The infrastructure is broadly spilt between core cultural infrastructure projects and wider investments that will enhance the City and surrounding area – the key projects having been outlined above. These projects have an important impact on the quality of the City and its ability to attract and retain people and businesses. Table 3.5 and 3.6 summarises the details.

Table 3.5 Culture Projects

Theme Number of Projects

Cost of Project (£m) Jobs

Arts 4 5.9 83 Arts and Heritage 3 8.2 City Life 1 0.2 Create 38 132.8 Creativity and Innovation 3 115 3000 E C o C 5 9.5 60 Faith and Community Service

1 4.2 12

Heritage 5 22.7 33 Participate 8 72.6 71 Regenerate 5 393.3 3500 Unspecified 4 116.5 109 Total 83 984 6868 Source: LCC

The investments have been broken down according to the broad categories in terms of how they contribute to the aims of the Capital of Culture bid submission. The number of projects and associated outputs where known are indicated. The total investment outlined amounts to over £2 billion of public and private sector investment.

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

24

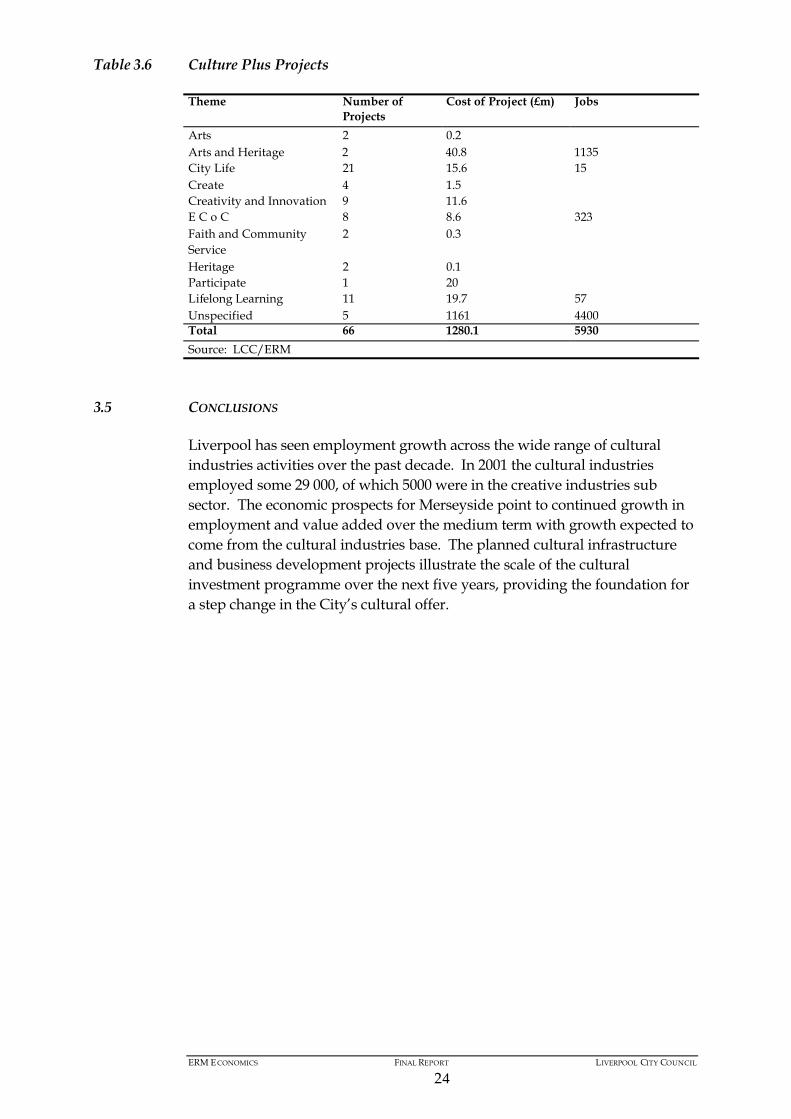

Table 3.6 Culture Plus Projects

Theme Number of Projects

Cost of Project (£m) Jobs

Arts 2 0.2Arts and Heritage 2 40.8 1135City Life 21 15.6 15Create 4 1.5Creativity and Innovation 9 11.6E C o C 8 8.6 323Faith and Community Service

2 0.3

Heritage 2 0.1Participate 1 20Lifelong Learning 11 19.7 57Unspecified 5 1161 4400Total 66 1280.1 5930Source: LCC/ERM

3.5 CONCLUSIONS

Liverpool has seen employment growth across the wide range of cultural industries activities over the past decade. In 2001 the cultural industries employed some 29 000, of which 5000 were in the creative industries sub sector. The economic prospects for Merseyside point to continued growth in employment and value added over the medium term with growth expected to come from the cultural industries base. The planned cultural infrastructure and business development projects illustrate the scale of the cultural investment programme over the next five years, providing the foundation for a step change in the City’s cultural offer.

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

25

4 SOCIO ECONOMIC IMPACTS

4.1 INTRODUCTION

The European Capital of Culture award was established in 1985 and has a strong profile throughout the continent. Since its launch, the initiative has been more and more successful amongst European citizens and has had a growing cultural and socio-economic impact on the numerous visitors it has attracted. Furthermore, the experience of previous cities suggests that the social and economic impacts of awarding the title ‘Capital of Culture’ is a two-way street, with selected cities experiencing significant economic and social benefits as a consequence. Such benefits have been felt through increased visitor numbers (both during the year itself and thereafter, as a legacy of the title), higher expenditure in the cultural sector, an improved cultural ‘offer’ for tourists and residents alike and improved image domestically and internationally.

The terms of reference for this study asked that we consider the potential impact of a successful Capital of Culture bid on the following three key areas:

• Increased competitiveness and sustainable economic growth;• Social and cultural benefits and increased community cohesion; and• Growth of the creative industries sector.

Based on the bid programme developed to date this section sets out the way in which Liverpool could benefit if the City were to win the award. Given the complex nature of the potential benefits we have adopted an approach that focuses on three key areas. These are:

• Increased competitiveness: The extent to which the tourism product of Liverpool becomes more competitive from the cultural investment taking place;

• Creative industries: The promotion of creative industries within the Capital of Culture bid programme and the supporting wider investment programme; and

• Participation: The proposed range of activities and how the bid programme seeks to increase the involvement of the resident population and under represented groups.

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

26

4.2 CULTURAL INDUSTRIES

4.2.1 Introduction

This section explores some of the benefits that are forecast for Liverpool,should the city be awarded the European Capital of Culture for 2008.

4.2.2 Existing Visits to Liverpool

The Merseyside 2000 Visitor Survey Report undertaken by North West Tourist Board (NWTB) Research Services (2001) estimated that in 2000, tourism in Merseyside contributed some £604 million to the local economy. This injection into the Merseyside economy is thought to support in the region of 21 000 jobs.

The survey found that tourism in Liverpool contributed the largest proportion of income generated by tourism to the Merseyside economy. This was estimated to be £261 million in 2000. This amount of tourism expenditure in Liverpool was thought to support some 9500 jobs in the city.

The survey found that the city of Liverpool attracted some 7.54 million visits in 2000, of which some 6.69 million (89 per cent) were day trips with the remainder (some 848 000) being staying visits. These figures are consistent with those used elsewhere and were employed as the base year figures on which subsequent forecasts were estimated.

4.2.3 Forecast Visits to Liverpool, 2003 - 2012

Table 4.2 shows forecast visits to Liverpool, for 2003 – 2012. This period includes the Capital of Culture year of 2008 itself, each of the themed years planned in the run up to the Capital of Culture year, starting with the LifetimeLearning theme in 2003, as well as Liverpool’s 800th anniversary year, due to be celebrated in 2007.

Overall estimates of visits comprise three sets of estimates overlaid. These are:

• The trend – the number of visits that are expected to take place regardless of other activities;

• Additional growth associated with new investment in infrastructure and tourist attractions; and

• The specific one-off effect of the Capital of Culture.

Growth Trend

The trend is a reflection of what is likely to happen to the Liverpool tourism market without the Capital of Culture award and without the implementation of new projects planned and underway. The start point for the trend is the

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

27

baseline year 2000 figures presented above (ie 7.5m visits and an associated spend of £261 million). Thereafter, a year on year growth figure of three per cent per annum up to and including 2008 is applied, with a figure of 1.5 per cent growth per annum being used thereafter. For Merseyside, which has been experiencing relatively strong growth in recent years, such a target is likely to be achievable provided some degree of innovation and successful marketing is realised.

Factoring in these rates of growth implies an expected 9.5 million visits in 2008, of which some 1.5 million would be staying visits. Together, these visits would generate expenditure of some £460 million at the Liverpool level.

Impact of New Projects

A second layer of visits has been estimated to reflect the additionalinfrastructure and tourist attractions that are to be constructed. The rationale for this additional layer of visits is that because of the extraordinary scale of the investment and the iconic nature of some of the projects involved, additional visits beyond those expected as part of the normal growth rate can be expected. The new projects which will generate these additional visits include the Fourth Grace, Kings Dock, the National Museums and Galleries of Merseyside initiatives, St George’s Hall improvements and the newly opened FACT centre.

The impact of these projects begins on a relatively small scale (40 000 net additional visits in 2003), and, as more projects come on stream (including the Fourth Grace and Kings Dock), rises to 1.04 million in 2008. The 2008 visits are associated with expenditure of some £42m.

Capital of Culture Effect

The estimate of an additional 700 000 visits reflecting the Capital of Culture year in 2008 (which represents a rise of some seven per cent relative to the previous year) is reasonably conservative given the experiences of Capital of Culture cities elsewhere. This experience is presented in Table 4.1.

ERM ECONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

28

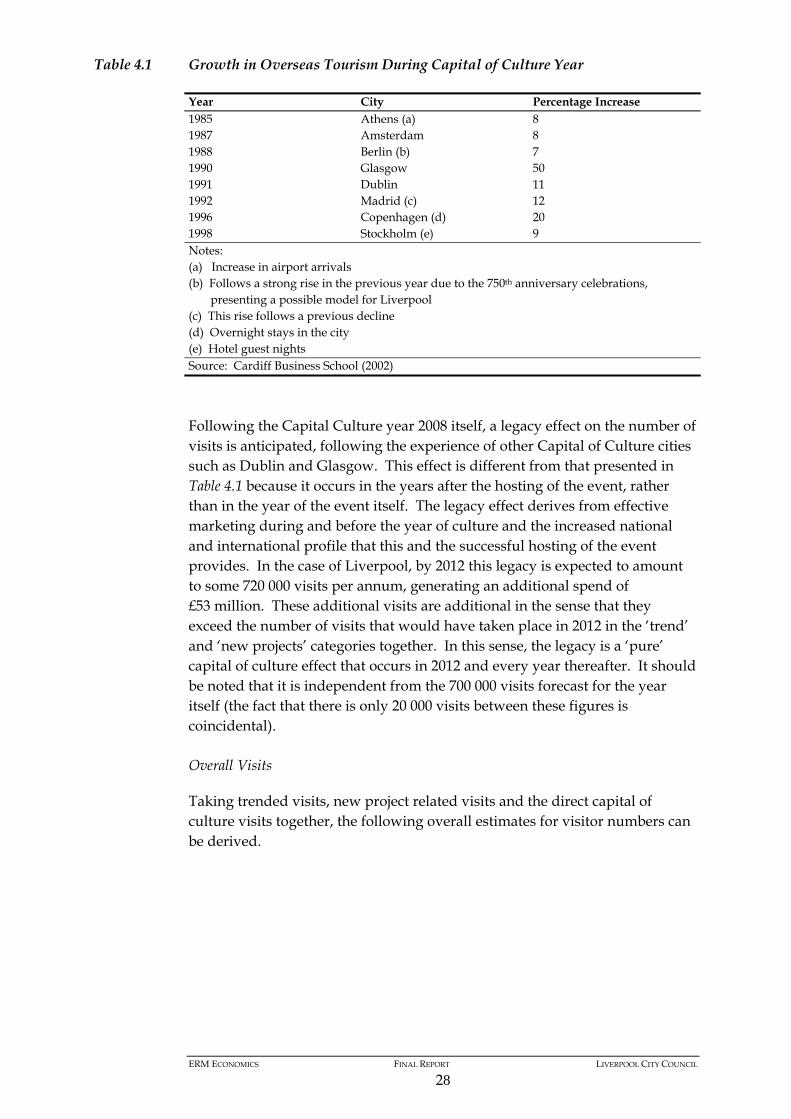

Table 4.1 Growth in Overseas Tourism During Capital of Culture Year

Year City Percentage Increase 1985 Athens (a) 8 1987 Amsterdam 8 1988 Berlin (b) 7 1990 Glasgow 50 1991 Dublin 11 1992 Madrid (c) 12 1996 Copenhagen (d) 20 1998 Stockholm (e) 9 Notes: (a) Increase in airport arrivals (b) Follows a strong rise in the previous year due to the 750th anniversary celebrations,

presenting a possible model for Liverpool (c) This rise follows a previous decline (d) Overnight stays in the city (e) Hotel guest nights Source: Cardiff Business School (2002)

Following the Capital Culture year 2008 itself, a legacy effect on the number of visits is anticipated, following the experience of other Capital of Culture cities such as Dublin and Glasgow. This effect is different from that presented in Table 4.1 because it occurs in the years after the hosting of the event, rather than in the year of the event itself. The legacy effect derives from effective marketing during and before the year of culture and the increased national and international profile that this and the successful hosting of the event provides. In the case of Liverpool, by 2012 this legacy is expected to amount to some 720 000 visits per annum, generating an additional spend of £53 million. These additional visits are additional in the sense that they exceed the number of visits that would have taken place in 2012 in the ‘trend’ and ‘new projects’ categories together. In this sense, the legacy is a ‘pure’ capital of culture effect that occurs in 2012 and every year thereafter. It should be noted that it is independent from the 700 000 visits forecast for the year itself (the fact that there is only 20 000 visits between these figures is coincidental). Overall Visits

Taking trended visits, new project related visits and the direct capital of culture visits together, the following overall estimates for visitor numbers can be derived.

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

29

Table 4.2 Projected Visits to Liverpool, 2003 – 2008 (Thousand visits)

Year Total Visits Trend New Projects One-off2000 7540 7540 - -2001 7766 7766 - -2002 7999 7999 - -2003 8279 8239 40 -2004 8588 8486 102 -2005 8858 8741 117 -2006 9120 9003 117 -2007 9678 9273 405 -2008 11 127 9551 876 700Source: ERM Estimates

By 2012, total visits are estimated to have risen to 11.897 million, which comprises:

• A trend number of visits of 10.14 million;• New projects driven visits of 1.04 million;• A legacy effect of 0.72 million.

Day/Staying Visit Forecasts

The NWTB Research Services (2001) found that there were some 848 000 staying visits in 2000. These visits are of particular interest because they result in a higher spend than do day visits.

Table 4.2 shows that overall, between 2000 and 2008, total visits to Liverpool are forecast to rise by nearly 50 per cent. Staying visits are expected to more than double over the period, to some 1.8 million. The expected split between day, staying, domestic and overseas visits is shown in Table 4.3.

Table 4.3 Actual and Projected Day and Staying Visits to Liverpool, 2002 and 2008

Type of visit Visits in 2000 (thousands) Visits in 2008 (thousands)Day visits 6692 9347Staying visits: 848 1780 of which, UK staying visits 695 1068 and overseas staying visits 153 712Source: ERM estimates

The staying visitors make up a relatively small proportion of the total, initially 11 per cent. This figure is estimated to peak at 16 per cent in the Capital of Culture year itself before dropping to 15 per cent in the following year and 14 per cent by 2012. The majority of staying visitors will be domestic. At the beginning of the period, some 82 per cent of visits are estimated to be made by domestic visitors, with the balance of 18 per cent of staying visits being madeby overseas visitors.

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

30

The target split between domestic and overseas staying visitors is 60:40.Indeed, there is some evidence (albeit from a relatively small sample) that this target is already being achieved. Consequently, in 2005, 2006 and 2007, the balance between overseas and domestic staying visitors has been increased in favour of domestic visitors. It is assumed that in 2007 (Liverpool’s 800th

anniversary) and thereafter, the 60:40 split is achieved.

Length of Visits

Forecast spend (presented in Section 3.4) is estimated by multiplying average spend per visit by number of visits. This process is done in two stages, firstly for UK residents, and secondly for overseas residents.

Latest data for Liverpool is presented in Table 4.4.

Table 4.4 Length of Visit to Liverpool 2001 (Nights)

Type of visit Domestic visitor Overseas visitor TotalLong holiday 5.5 - -Short holiday 1.9 - -All holidays 2.9 3.8 3.0Business 2.2 2.4 2.2Visiting friends and relatives

2.4 7.9 2.8

Other 2.9 3.6 3.1Overall average 2.6 4.7 2.8Note: For overseas trips, the model does not differentiate between long and short holidaysSource: Economic Impact Model for Liverpool 2001 (NWTB Research Services March 2003)

Hotel Supply

Relatively high growth in the numbers of staying visitors will have implications for the hotel market in Liverpool and beyond.

The number of hotel rooms in Liverpool in 2001, when there were 848 000 staying visits, was estimated at 2307 (Tourism Enterprise and Management/Tourism Solutions, 2003). At the estimated occupancy rate of 66 per cent (which is used in the above report), this implies:

2307 rooms x 365 days x 66 per cent = 555 750 room nights annual capacity.

NWTB Research Services (2001) note that the proportion of staying visitors using hotels for accommodation had dropped off from 50 per cent in 1995. By 2000, 40 per cent of staying visitors were using hotels, with just over half of them staying with friends and relatives, and the remainder making other arrangements such as flat rental. Drawing on this statistic implies that in 2000 there would have been some 340 000 visits to hotels (848 000 x 40 per cent).The ratio of nights to visits was therefore 555 750/340 000 or 1.63, implying that the average stay in a Liverpool hotel that year was 1.63 nights.

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

31

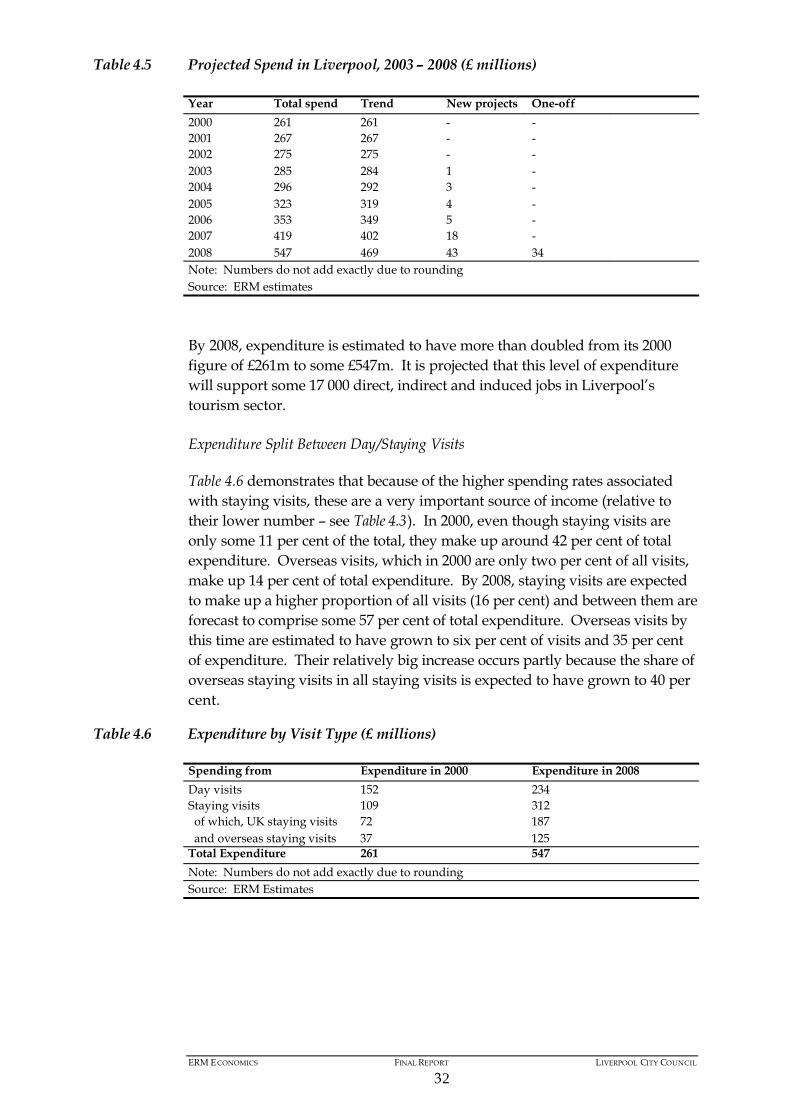

Looking to 2008, Liverpool’s Capital of Culture year, it is estimated that some 1.8 million staying visits will take place. By 2008, hotel capacity is projected to have risen to 4589 rooms (Tourism Enterprise and Management/ Tourism Solutions, 2003). A rise in the hotel occupancy rate for 2008 has also been projected, from the 66 per cent estimated in 2000 to 70 per cent by 2008 (ibid).This implies that capacity in the city will be:

4589 rooms x 365 days x 70 per cent = 1 172 000 room nights annual capacity.

Assuming 40 per cent of visitors continue to require hotel services, then in 2008 there will be some 720 000 visits to hotels (1.8 million x 40 per cent). The ratio of nights to visits is therefore expected to be 1 172 000/712 000, or 1.63.This ratio is the same as that in 2000, implying that hotel supply is predicted to rise at the same rate as the demand for staying visits.

If these expectations are on target, it is clear that hotel demand and supply will balance. Moreover, not only will the additional demand drive the new hotel capacity development, but it will also drive higher occupancy rates forLiverpool hotels in general (from an estimated 66 per cent in 2000 to 70 per cent in 2008).

Forecast Spend in Liverpool, 2003 - 2012

NWTB Research Services (2001) found that the mean average expenditure for a day trip in Liverpool was £22.79. Average expenditure for staying visits is a function of various determinants including origin of traveller (foreign or domestic) and whether the visitor is staying with friends or relatives or in a hotel. Mean average figures used for staying visits are £103 per trip for domestic visitors and £245 per trip for overseas visits.

These rates (£22.79 for day trip, £103 for domestic staying visits and £245 per trip for overseas visits) are used up until 2008, at which point it is assumed that they rise by 10 per cent. For 2008 and thereafter, spend rates are therefore £22.79, £113.30 and £269 respectively for day visits, domestic and overseas staying visitors.

All expenditure figures are presented in current prices (inflation is not built into the model). These do not change with scenario – ie average spend per visit remains the same for trend visits and for visits driven by new projects, capital of culture, and capital of culture legacy. Total value of expenditure is affected only by the volume of visits and the split between day/staying visits and domestic and overseas staying visits.

Table 4.5 shows forecast spend for Liverpool, for 2003 – 2012.

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

32

Table 4.5 Projected Spend in Liverpool, 2003 – 2008 (£ millions)

Year Total spend Trend New projects One-off2000 261 261 - -2001 267 267 - -2002 275 275 - -2003 285 284 1 -2004 296 292 3 -2005 323 319 4 -2006 353 349 5 -2007 419 402 18 -2008 547 469 43 34Note: Numbers do not add exactly due to roundingSource: ERM estimates

By 2008, expenditure is estimated to have more than doubled from its 2000 figure of £261m to some £547m. It is projected that this level of expenditure will support some 17 000 direct, indirect and induced jobs in Liverpool’s tourism sector.

Expenditure Split Between Day/Staying Visits

Table 4.6 demonstrates that because of the higher spending rates associated with staying visits, these are a very important source of income (relative to their lower number – see Table 4.3). In 2000, even though staying visits are only some 11 per cent of the total, they make up around 42 per cent of total expenditure. Overseas visits, which in 2000 are only two per cent of all visits, make up 14 per cent of total expenditure. By 2008, staying visits are expected to make up a higher proportion of all visits (16 per cent) and between them are forecast to comprise some 57 per cent of total expenditure. Overseas visits by this time are estimated to have grown to six per cent of visits and 35 per cent of expenditure. Their relatively big increase occurs partly because the share of overseas staying visits in all staying visits is expected to have grown to 40 per cent.

Table 4.6 Expenditure by Visit Type (£ millions)

Spending from Expenditure in 2000 Expenditure in 2008 Day visits 152 234Staying visits 109 312 of which, UK staying visits 72 187 and overseas staying visits 37 125Total Expenditure 261 547Note: Numbers do not add exactly due to roundingSource: ERM Estimates

ERM ECONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

33

4.2.4 Sensitivity Testing

Analyses were carried out to assess the likely impact of changes in three variables: • Straightforward, proportionate changes in all visit numbers; • Changes in assumptions about trend growth; and • Changes in the numbers of visits attracted by the Capital of Culture and

New Projects. Proportionate Changes in All Visit Numbers

Sensitivity testing was carried out to estimate what might happen if the number of overall visits were to change, and also if the number of staying visits were to change. In each case estimated outputs were tested for a rise in visits of 10 per cent and for falls of 10 and 20 per cent. The estimated impact of these changes is presented in Table 4.7.

Table 4.7 Estimated Impact of Changes in All Visit Numbers

Level Visitor numbers in 2008 (000s)

Expenditure in 2008 (£m)

Reduced by 20 per cent 8928 439 Reduced by 10 per cent 10 029 493 Standard assumptions 11 127 547 Increased by 10 per cent 12 221 601 Source: ERM Estimates

The findings demonstrate that across the board changes simply feed through to overall visits and expenditure in the same proportion (ie changes of 10 per cent in the number of visits lead to changes of approximately 10 per cent in estimated total spend). Changes in Assumptions of Trend Growth

The impact of changes in assumptions of the trend growth was then assessed. The analysis showed that visitor numbers and spend appeared to be fairly sensitive to changes in the assumptions of trend growth. The base case assumption of trend was that visits are expected to grow by three per cent per annum until 2008, and then by 1.5 per cent per annum thereafter. Such an assumption would lead to an estimated 11.1 million visits in 2008, associated with estimated expenditure of £547m. The revised assumption investigated was that trend growth was reduced from 3 per cent per annum to 1.5 per cent per annum throughout the period. The impact of this was to reduce 2008 visitor numbers to 10 088 and to cut estimated expenditure to £496m – a fall of 9 per cent.

ERM ECONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

34

Changes in Visitor Numbers Attracted by New Projects and Capital of Culture

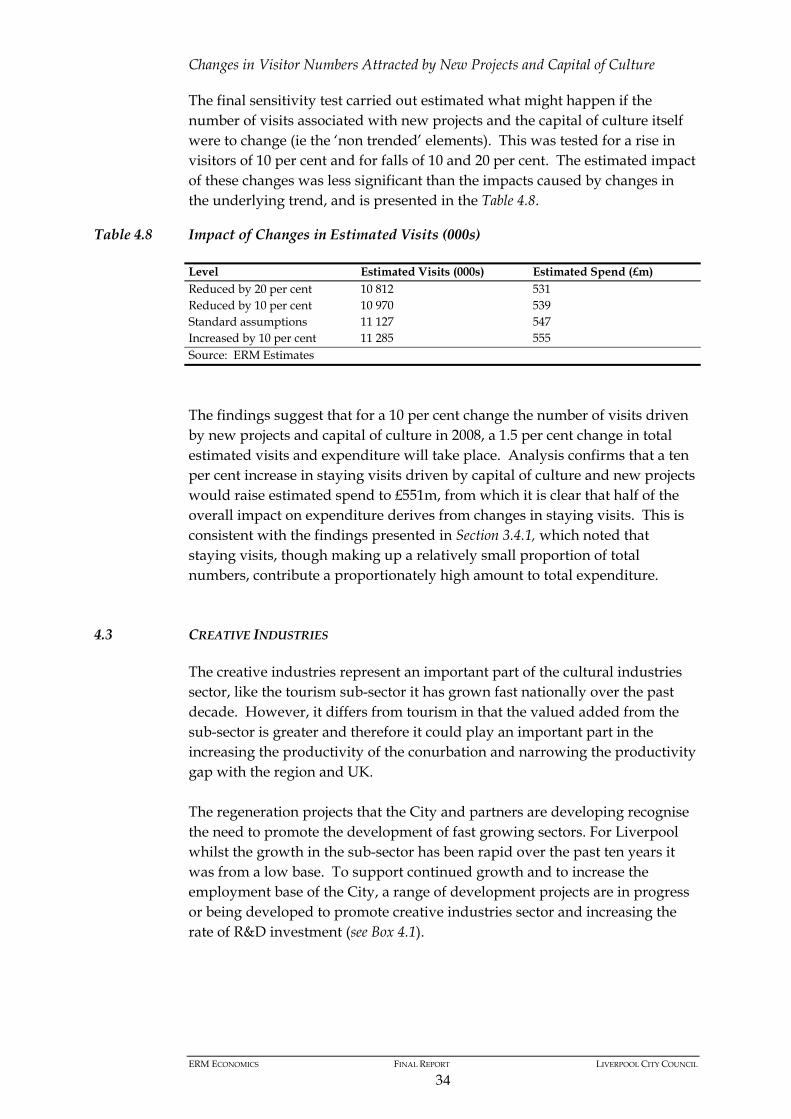

The final sensitivity test carried out estimated what might happen if the number of visits associated with new projects and the capital of culture itself were to change (ie the ‘non trended’ elements). This was tested for a rise in visitors of 10 per cent and for falls of 10 and 20 per cent. The estimated impact of these changes was less significant than the impacts caused by changes in the underlying trend, and is presented in the Table 4.8.

Table 4.8 Impact of Changes in Estimated Visits (000s)

Level Estimated Visits (000s) Estimated Spend (£m) Reduced by 20 per cent 10 812 531 Reduced by 10 per cent 10 970 539 Standard assumptions 11 127 547 Increased by 10 per cent 11 285 555 Source: ERM Estimates

The findings suggest that for a 10 per cent change the number of visits driven by new projects and capital of culture in 2008, a 1.5 per cent change in total estimated visits and expenditure will take place. Analysis confirms that a ten per cent increase in staying visits driven by capital of culture and new projects would raise estimated spend to £551m, from which it is clear that half of the overall impact on expenditure derives from changes in staying visits. This is consistent with the findings presented in Section 3.4.1, which noted that staying visits, though making up a relatively small proportion of total numbers, contribute a proportionately high amount to total expenditure.

4.3 CREATIVE INDUSTRIES

The creative industries represent an important part of the cultural industries sector, like the tourism sub-sector it has grown fast nationally over the past decade. However, it differs from tourism in that the valued added from the sub-sector is greater and therefore it could play an important part in the increasing the productivity of the conurbation and narrowing the productivity gap with the region and UK. The regeneration projects that the City and partners are developing recognise the need to promote the development of fast growing sectors. For Liverpool whilst the growth in the sub-sector has been rapid over the past ten years it was from a low base. To support continued growth and to increase the employment base of the City, a range of development projects are in progress or being developed to promote creative industries sector and increasing the rate of R&D investment (see Box 4.1).

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

35

Box 4.1 Example of Digital Industries Initiative - International Centre for Digital Content (ICDC), Liverpool

ICDC provides support to enhance the levels of skills, knowledge, and expertise necessary to see the region as an international contender in the knowledge economy. It aims to provide the region with a real competitive edge and to take advantage of the region’s creative and innovative talent. In addition ICDC researches into existing and emerging technologies with partners such as Nokia, BBC, Channel 4 and Hewlett Packard, to discover new forms of digital content that bring technology to life.

The importance of the Capital of Culture bid and the wider investment that is planned for the City is that such activities are reinforcing, helping to create the conditions for a successful city. The quality of the infrastructure, the values of the City and its cultural depth help generate, attract and retain successful enterprise in the leading edge sectors. For the City there are a number of strategic investments that will support the growth of the creative industries sector, including:

• University Science Park: The development of the Merseyside Science Park project in partnership with the University and partners to provide incubator facilities;

• Digital Technology Campus: The proposed development of a digital industries park as part of the Eastern Approaches Strategic Investment Area built around the Marconi site;

• National Biotechnology Centre: The proposed national centre of excellence at Speke;

• JMU expansion of services: The expansion of ICT and media related education and training; and

• Wavertree Technology Park extension: As part of the Eastern Approaches SIA there is the planned expansion of the technology park.

The proposed projects indicate that Liverpool could grow its creativeindustries at a faster rate over the next decade. The historical growth rate of the sub-sector has been 4 per cent per annum over the last ten years. We have projected additional employment in the sector based on the continued trend growth rate, plus a potential for additional jobs from the above range of projects. Our cautious assessment is that employment in the creative industries could grow by 5950 to 2012, of which 3150 additional jobs are above what would be expected based on trend growth. This excludes the potential from SMEs generated through the revenue support programmes that form part of the Objective 1 programme.

ERM E CONOMICS FINAL REPORT LIVERPOOL CITY COUNCIL

36

4.4 PARTICIPATION

The socio-economic impacts and outcomes of a Capital of Culture award are complex in that that the aim is to promote an inclusive and dynamic community. The means by which this can be achieved is by building within the Capital of Culture programmes the mechanisms to ensure participation by residents of Liverpool and the wider area. Participation means many things, from the planning of the programme, participating in events, being given the opportunity to access employment in the growing cultural industries sector.The outcome of this process will feed into one of the key characteristics of what makes a successful City, a reduction in the inequality of how people participate in cultural activities and benefit from the income generated by the sector (see Box 4.2).

Box 4.2 Raising Aspirations

Source: Giving Voices, Dreaming Dreams Community Planned Projects for the LiverpoolCapital of Culture Bid, February 2002