ETF Project – Management Course Costing & Finance Management

23

ETF Project – Management Course Costing & Finance Management Dr Tim Strickland – CEO, FE Sussex Dave Stokes – Deputy Principal, Plumpton College FRIDAY 6 TH JUNE 2014

-

Upload

pamelia-asker -

Category

Documents

-

view

20 -

download

0

description

ETF Project – Management Course Costing & Finance Management. FRIDAY 6 TH JUNE 2014. Dr Tim Strickland – CEO, FE Sussex Dave Stokes – Deputy Principal, Plumpton College. EDUCATION AND TRAINING FOUNDATION ETF. Why are we here?. We are here to: - PowerPoint PPT Presentation

Transcript of ETF Project – Management Course Costing & Finance Management

ETF Project – ManagementCourse Costing & Finance Management

Dr Tim Strickland – CEO, FE SussexDave Stokes – Deputy Principal, Plumpton College

FRIDAY 6TH JUNE 2014

EDUCATION AND TRAINING FOUNDATION

ETF

Why are we here?

We are here to:

•Gain an understanding of the ‘More for Less’ agenda

•Raise our understanding of effective and realistic course costing

•Assist you in costing courses against a background of continual funding reduction

•Assist in enhancing college financial performance

Why are we here?

Outcomes:

a)Identify the costs associated with an educational establishment

b)Estimate the costs of ‘income-generating’ staff time

c)List potential sources of educational income

d)Calculate approximate course costings for full recovery

Do you know?

1995 Average Level of Funding (ALF) reduced from £30 / unit to £17 / unit2000 LSC created to encourage localism (stimulated growth)

2008 general recession hits – banks bailed out

2010 fiscal tightening in education starts

School budgets (pre 16) protected

University Fees increased up to £9,000 per annum

FE experiences disproportionate cutsTypical College

2010 - £10.6m educational income2014 - £10.0m (but 150 more full time students and £600,000 extra staff costsFE – 2010 - £6,500 per full time student (750 contact hours)FE – 2014 - £5,600 per full time student (600 contact teaching hours)

So, why can‘t we just throw more staff at the increased numbers?

FE Sector Background

DoomGloom Recession Reduction Impact

FE Sector overheads – the misconceptions and myths

• It only costs £35 per hour for a part time teacher

• My bit of the college is viable – it is everyone else’s that isn’t

• Why should I pay for ‘management’• In industry this wouldn’t happen….• This isn’t a business – it’s a college….

Income sources• Schools (Junior)

• 14 – 16

• 16-18 (18year olds – 17.5%)

• 19+ SFA

• HE

• Apprenticeships

• Full cost

• Grant supported –• Personal and community related• Research grants

What costs compriseCommercial (Staff and non staff)

£3m 20%

Resources

£6m 40%

Staffing – non teaching time

£3m 20%

Staffing – teaching time

£3m 20%

The overheads of colleges

• If you were asked to identify overheads you might say

• ?• ?• ?

The commercial reality

Cost identification

Separate out the teaching related costs from the commercial activity

Teaching related costsStaffing (£6m annually)

Salary and rangeOn costs – 20% (Employers NI and pension)Teaching staff – adminTeaching staff – teachingAdmin support staff

Resources (non staff) (£6m annually) - examplesWide ranging egHeating and lighting - £320kMaintenance - £330kGeneral running (admin related) - £240kExam costs -£250kMarketing - £125kInterest - £135kBursaries and buses £600kTeaching resources £1.1mDepreciation - £1.5m

Calculating course costing – exercise 1

Resources

£8m 33.3%

Staffing – non teaching time

£8m 33.3%

Staffing – teaching time

£8m 33.3%

• Average member of staff spends 60% of their time contact teaching (900 hours annually)• Average annual salary for the teaching time (900 hours) is say £20,000 per year• (plus on costs at 20%)• The course lasts 450 hours

What is the total income required for full contribution to the costs? If the income from the funding body is £6 per individual student teaching hour, how many students do we need on the course?

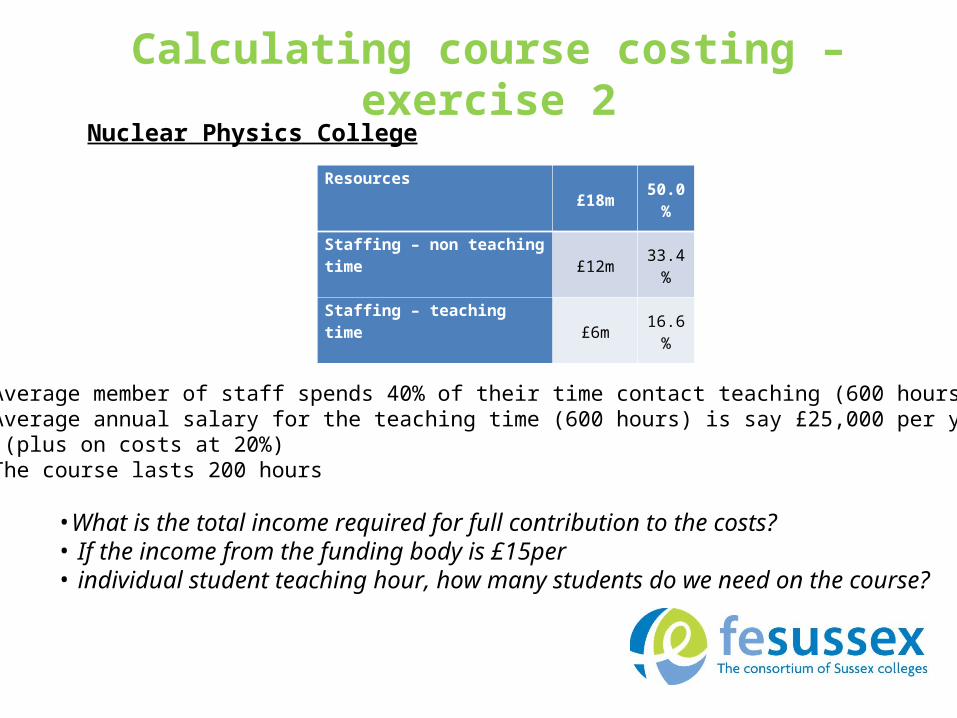

Calculating course costing – exercise 2

• Average member of staff spends 40% of their time contact teaching (600 hours annually)• Average annual salary for the teaching time (600 hours) is say £25,000 per year• (plus on costs at 20%)• The course lasts 200 hours

•What is the total income required for full contribution to the costs?• If the income from the funding body is £15per• individual student teaching hour, how many students do we need on the course?

Nuclear Physics College Resources

£18m 50.0%

Staffing – non teaching time

£12m 33.4%

Staffing – teaching time

£6m 16.6%

Costing a course

Producing a standard costing sheet:

•Determine teaching costs – number of hours, hourly rate, support time, multiplier overhead (50%?, 75%?)•Determine non-teaching overheads – materials, travel, expenses, materials – ie anything extra you will need.•Apply overhead multiplier to non-teaching overheads•Add costs together •Divide by number of learners.

•Assist in enhancing college financial performance

Costing a courseQuestions to ask yourself

•Is the final cost reasonable?

•Does it allow for contingency?

•Is there a profit in it for the college/department?

•Is it at a rate the market will stand?

The standard costing form

In summaryIdentify income

•Identify income sources

•Identify all overheads - teaching/non teaching

•Add on the appropriate margin for the college•Calculate the return to the college•Calculate the cost per learner