Estate Valuation Amy C. Floyd, JD Allstate Financial.

31

Estate Valuation Amy C. Floyd, JD Amy C. Floyd, JD Allstate Financial Allstate Financial

-

Upload

ashley-doyle -

Category

Documents

-

view

249 -

download

0

Transcript of Estate Valuation Amy C. Floyd, JD Allstate Financial.

Estate ValuationEstate Valuation

Amy C. Floyd, JDAmy C. Floyd, JD

Allstate FinancialAllstate Financial

© 2010 Allstate Insurance Company 10/10

Please note that Allstate Life Insurance Company, Allstate

Life Insurance Company of New York or the agents and

representatives of those entities cannot give tax or legal

advice. The brief discussion of taxes and/or tax related

terms in this presentation may not be complete or current.

The laws and regulations are complex and subject to

change. For complete details, consult your attorney or tax

advisor. This material is intended for general educational

purposes only.

© 2010 Allstate Insurance Company 10/10

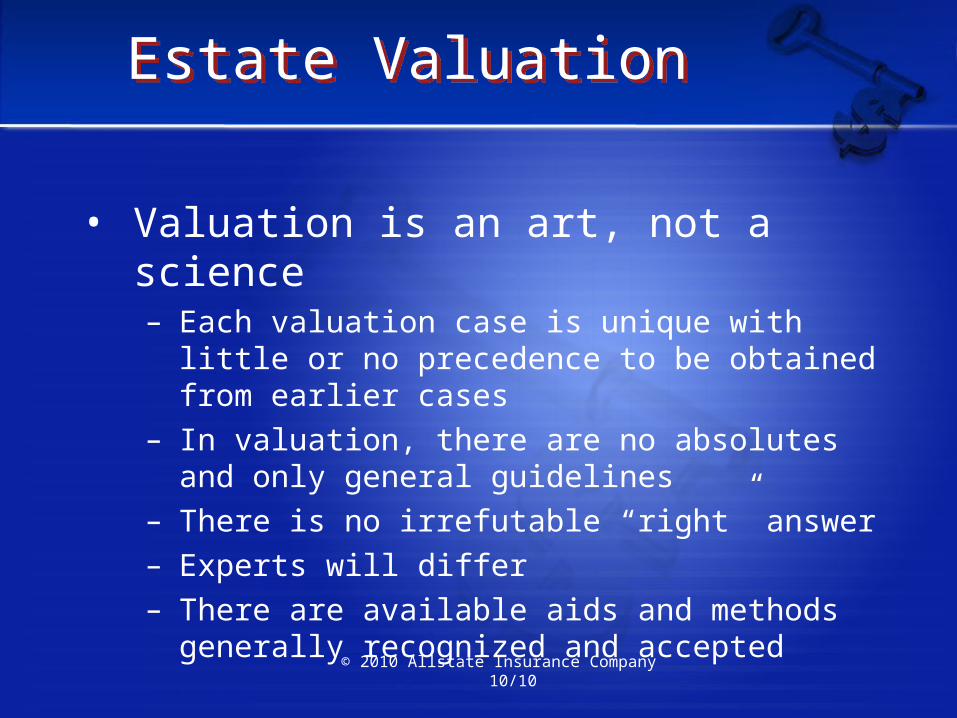

Estate ValuationEstate Valuation

• Valuation is an art, not a science– Each valuation case is unique with little or no

precedence to be obtained from earlier cases– In valuation, there are no absolutes and only general

guidelines– There is no irrefutable “right” answer– Experts will differ– There are available aids and methods generally

recognized and accepted

© 2010 Allstate Insurance Company 10/10

FAIR MARKET VALUEFAIR MARKET VALUE

• Valuation is based on the concept of Fair Market Value– Defined as “the price at which property would

change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or sell and both having reasonable knowledge of the relevant facts”.

© 2010 Allstate Insurance Company 10/10

Price At Which Property Would Change Hands….Price At Which Property Would Change Hands….

• Actual sale is the best indicator of value• Hypothetical “sale” price

– Generally a sale for cash or cash equivalent– If seller receives payments in installments, the

price will be artificially inflated to compensate the seller for greater risk, but shouldn’t be considered as part of the “sale” price

© 2010 Allstate Insurance Company 10/10

…Between a Willing Buyer and Willing Seller……Between a Willing Buyer and Willing Seller…

• State of mind• Different from the absence of a compulsion to

buy or sell• Willing Buyer and Willing Seller are

hypothetical persons• Both must be considered

© 2010 Allstate Insurance Company 10/10

…Neither Being Under Compulsion to Buy or Sell……Neither Being Under Compulsion to Buy or Sell…

• If buyer is compelled to buy, price is artificially high

• If seller is compelled to sell, price is artificially low

• Court forbids valuation based on compulsion. (Estate of Bright V. United States, 658 F.2d999, USTC 13,436)

© 2010 Allstate Insurance Company 10/10

…Both Having Reasonable Knowledge of Relevant Facts……Both Having Reasonable Knowledge of Relevant Facts…

• Hypothetical sale must assume that both buyer and seller have a reasonable knowledge of the facts about the property.– Standard is based on not what is actually known,

rather the facts that are discoverable through reasonable investigation

© 2010 Allstate Insurance Company 10/10

MarketplaceMarketplace

• Includes consideration of the location of the marketplace

• Type of market– e.g. wholesale or retail

• Defined by the regulations as the marketplace within which that item is most commonly sold to the public

© 2010 Allstate Insurance Company 10/10

Real Estate ValuationReal Estate Valuation

• Market Approach– Involves comparison of values of actual sales

• Income Approach – Project anticipated income– Determine capitalization rate

• Income of Comparable = Rate Price of Comparable

• Cost Approach– Reproduction costs less depreciation

© 2010 Allstate Insurance Company 10/10

Valuation of Closely Held Business InterestsValuation of Closely Held Business Interests

• Fair Market Value• Revenue Ruling 59-60

– Type of Business– Economic Outlook– Net Asset Valuation (Book Value)– Earnings Value/Comparables– Dividend Paying Capacity– Goodwill– Sales of Stock of Company

© 2010 Allstate Insurance Company 10/10

Type of BusinessType of Business

• Nature of the company– Various industries weight price/earnings ratios

differently. Follow standard by industry

• History of the company– Corporate minute books and stock ledgers reveal

past history

© 2010 Allstate Insurance Company 10/10

Economic OutlookEconomic Outlook

• View stock in the context of how the financial markets view the overall economy

• If regional company, look at regional economy• Past fluctuations in costs and earnings generally can

be explained by reference to the national economy

© 2010 Allstate Insurance Company 10/10

Net Asset ValuationNet Asset Valuation

• Book value more than historical value of corp’s assets where a liquidation is in process or imminent

• Should use book value for minority interests or where holding company is involved

• Book value adjusted for inventory reserves or correcting excess depreciation to arrive at “adjusted book value” or “net asset value”

• Useful for valuation of investment companies

© 2010 Allstate Insurance Company 10/10

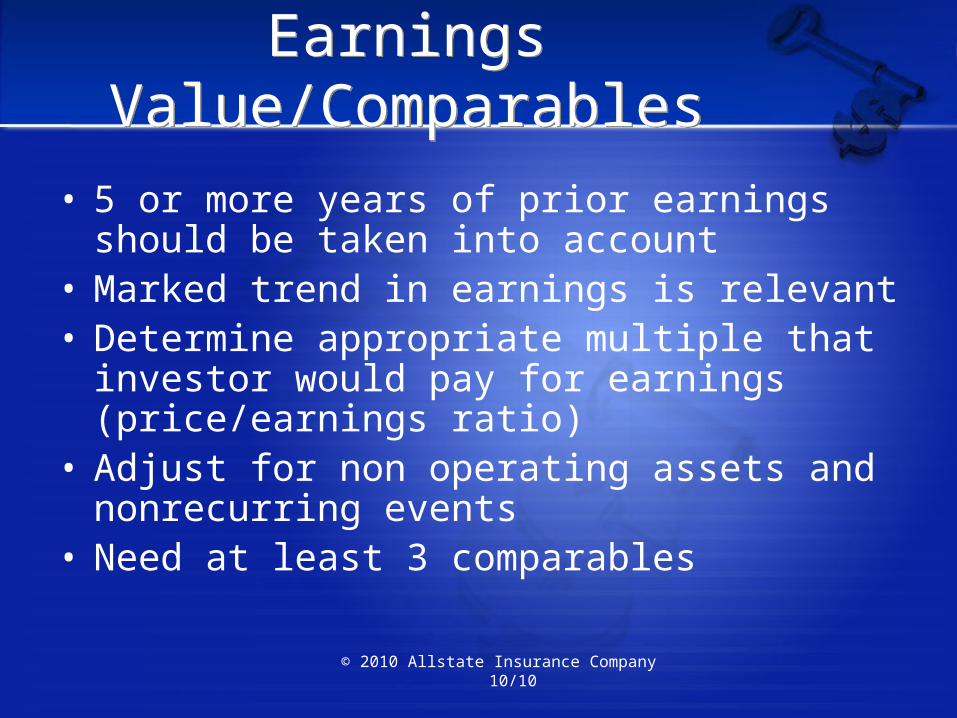

Earnings Value/ComparablesEarnings Value/Comparables

• 5 or more years of prior earnings should be taken into account

• Marked trend in earnings is relevant• Determine appropriate multiple that investor would

pay for earnings (price/earnings ratio)• Adjust for non operating assets and nonrecurring

events• Need at least 3 comparables

© 2010 Allstate Insurance Company 10/10

Dividend Paying CapacityDividend Paying Capacity

• Actual dividend yield may be gross understatement of company’s ability to pay dividends

• Look at company’s current need for surplus corporate funds

© 2010 Allstate Insurance Company 10/10

GoodwillGoodwill

• Goodwill is defined as the excess of earnings over and above a fair rate of return on net tangible assets.

• Demonstrated earning power is evidence of goodwill.

© 2010 Allstate Insurance Company 10/10

Sales of Stock of Subject CompanySales of Stock of Subject Company

• Prior sales of stock in the subject company should be taken into consideration as one of best indicators of value

• Look to determine “willingness” of buyer and seller• Smaller lots than one being valued should be given

less weight. • Proximity of sales to valuation date is also important

© 2010 Allstate Insurance Company 10/10

Other Valuation MethodsOther Valuation Methods

• Discounted Future Earnings– Rather than use past earnings data, forecast future

prospects from the valuation date forward

• Discounted Cash Flow– Net profits after tax are estimated for the desired future

period– Added to depreciation and amortization– Adjust for loan payments, then present value the cash

flow.

© 2010 Allstate Insurance Company 10/10

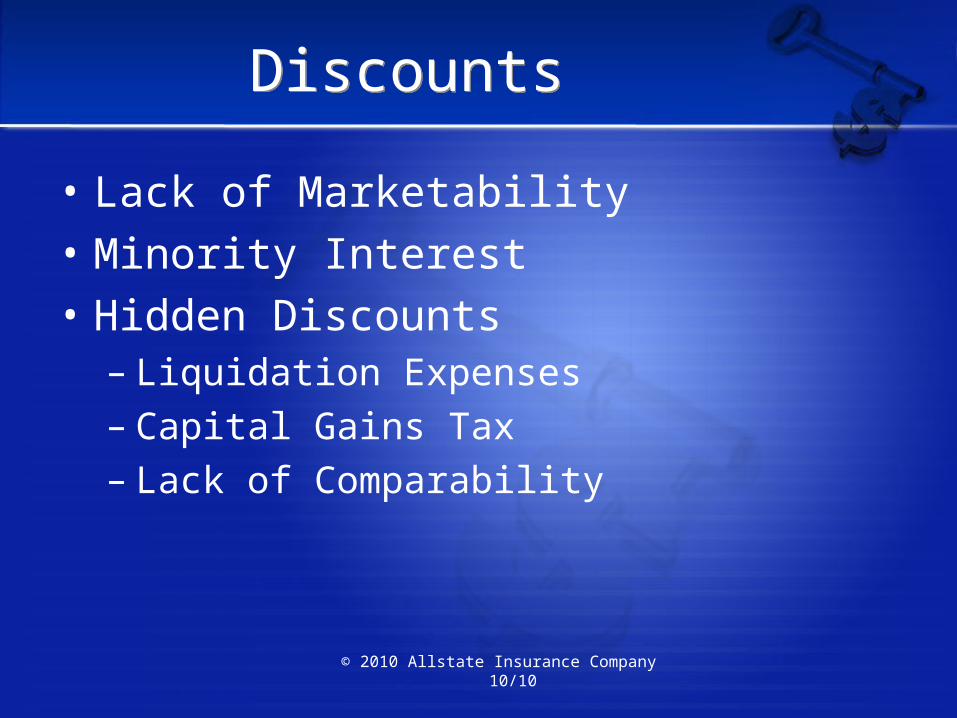

DiscountsDiscounts

• Lack of Marketability• Minority Interest• Hidden Discounts

– Liquidation Expenses– Capital Gains Tax– Lack of Comparability

© 2010 Allstate Insurance Company 10/10

Use of Restrictive AgreementsUse of Restrictive Agreements

• Mandatory Buy-Sell Agreements• Agreement Effective Only at Death• Right of First Refusal• Purchase Options

© 2010 Allstate Insurance Company 10/10

Business PurposeBusiness Purpose

• Maintenance of ownership and control within the family

• Providing continuity of management• With testamentary devices, business purpose is not

enough. Need to show it is not a device to transfer property to family member for less than adequate consideration

© 2010 Allstate Insurance Company 10/10

Actual Estate ValueActual Estate Value

• Value as of date of death

• Alternate valuation – Six months after date of death or– Sale date, whichever is earlier

© 2010 Allstate Insurance Company 10/10

Estate ValuationEstate Valuation

Proving Estate Value:– Certified Evaluation by Professional Estate

Valuation Appraiser on assets where FMV not readily available

– Statement from Tax Advisor/Accountant– Copies of Profit and Loss statement, assets and

liabilities for past 3 years on family business

© 2010 Allstate Insurance Company 10/10

Estate Valuation Case StudyEstate Valuation Case Study

Gross Estate = $10 million estimateReal Estate (farm) $1 million

Real Estate (US residential & rental) $1.5 millionReal Estate (Foreign) $ 500,000Readily Marketable Securities $2 millionClosely Held Business $1 millionRetirement Funds $1 millionPersonal Property (including art) $1 millionClosely Held Partnership Interests $1.5 millionTrust Assets $ 500,000

© 2010 Allstate Insurance Company 10/10

Estate Valuation Case StudyEstate Valuation Case Study

Real Estate (farm) $1 millionReal Estate (US residential & rental) $1.5 millionReal Estate (Foreign) $ 500,000

Real Estate Issues 1. Highest and best use or current use?2. Certified appraisal of all properties?3. Issues with foreign real estate such as long term lease versus outright fee simple ownership and ability to convey ownership rights

© 2010 Allstate Insurance Company 10/10

Estate Valuation Case StudyEstate Valuation Case Study

Closely Held Business $1 million

Issues with closely held business• Valuation issues covered earlier• Valuation discount opportunities

– Fractional ownership– Minority ownership– Lack of marketability

© 2010 Allstate Insurance Company 10/10

Estate Valuation Case StudyEstate Valuation Case Study

Closely Held Partnership Interests $1.5 million

Valuation issues related to closely held partnerships

• Same issues as with closely held business• What about Family Limited Partnerships• Is owner a general partner or limited partner

– Is there a gifting plan in place– Is there a buy sell plan in place

© 2010 Allstate Insurance Company 10/10

Estate Valuation Case StudyEstate Valuation Case Study

Personal Property (including art) $1 millionTrust Assets $ 500,000

Unique issues• Jewelry & Art• Collections • Interests in trusts

– Income & principal rights versus ownership– Currently distributable?– Designed to be outside of taxable estate?– Transfer during lifetime or at death?

© 2010 Allstate Insurance Company 10/10

UnderwritingUnderwriting

• Takes about 30-60 Days• Higher Face Amounts = More Experienced

Underwriter• Include a Cover Letter with Details

– Listing of Estate Assets• Copies of certified appraisals• Valuations of closely held assets and info on prior sales• If family business, years in business plus tax returns• Copies of any estate plan that would include projection of estate

taxes and costs• The more documentation, the better

© 2010 Allstate Insurance Company 10/10

QuestionsQuestions

????