Estate Planning What? Why? How? Insurance Concepts.

24

Estate Planning Estate Planning What? Why? How? Insurance Concepts

-

Upload

marcia-marsh -

Category

Documents

-

view

223 -

download

0

Transcript of Estate Planning What? Why? How? Insurance Concepts.

Estate PlanningEstate Planning

What? Why? How?

Insurance Concepts

DefinitionDefinition

Estate planning consists of using legitimate government sanctioned tax-planning strategies to ensure that you and your survivors do not pay out more than is legally required.

Introduction

In the broadest sense, estate planning consists of:

Deciding who you would like to have your property and possessions after your death. Defining and taking care of your responsibilities. Determining the most effective way to carry out your wishes.

Things to consider….Things to consider….

wills powers of attorney family trusts charitable gifting programs (view our power

point presentation) estate freezes (view our power point

presentation) buy-sell agreements (view our power point

presentation) living wills funeral/memorial plans

Why bother?Why bother? Those who die without having first put their

financial house in order often leave behind a complicated, time consuming and expensive task that has to be completed by their surviving family and friends— hardly a pleasant experience for those already in mourning.

Those who die without an estate plan have also relinquished their right to make decisions. Failing to plan ahead means that the fate of their money and their family is now in the hands of other people.

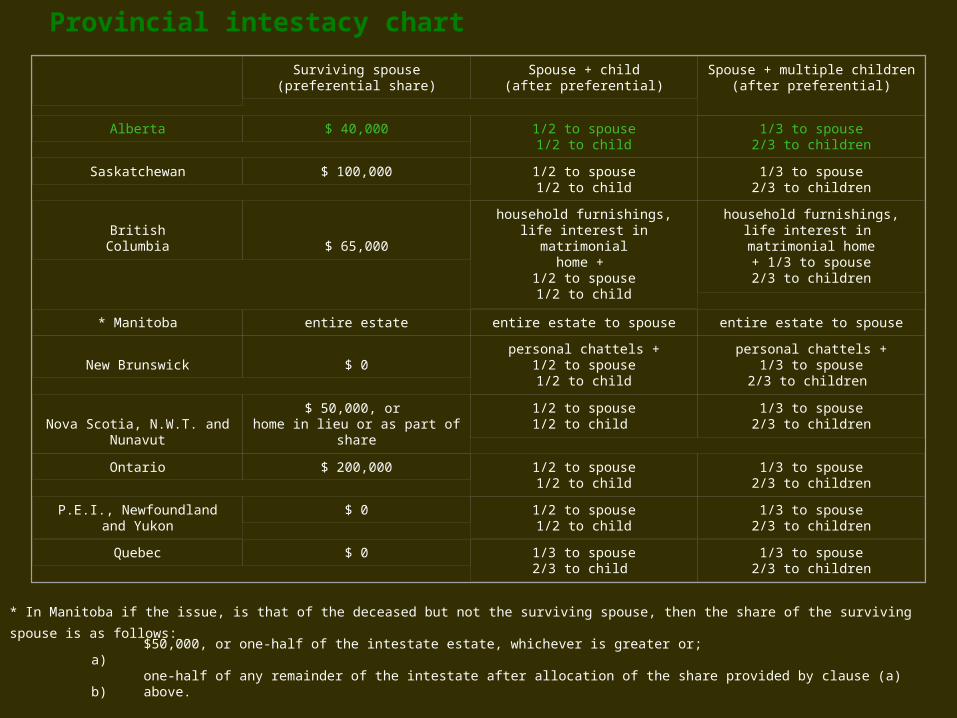

Provincial intestacy chart

Surviving spouse(preferential share)

Spouse + child(after preferential)

Spouse + multiple children (after preferential)

Alberta $ 40,000 1/2 to spouse1/2 to child

1/3 to spouse2/3 to children

Saskatchewan $ 100,000 1/2 to spouse1/2 to child

1/3 to spouse2/3 to children

BritishColumbia $ 65,000

household furnishings,life interest in matrimonial

home + 1/2 to spouse1/2 to child

household furnishings,life interest in

matrimonial home+ 1/3 to spouse2/3 to children

* Manitoba entire estate entire estate to spouse entire estate to spouse

New Brunswick $ 0personal chattels +

1/2 to spouse1/2 to child

personal chattels +1/3 to spouse

2/3 to children

Nova Scotia, N.W.T. and Nunavut

$ 50,000, or home in lieu or as part of share

1/2 to spouse1/2 to child

1/3 to spouse2/3 to children

Ontario $ 200,000 1/2 to spouse1/2 to child

1/3 to spouse2/3 to children

P.E.I., Newfoundlandand Yukon

$ 0 1/2 to spouse1/2 to child

1/3 to spouse2/3 to children

Quebec $ 0 1/3 to spouse2/3 to child

1/3 to spouse2/3 to children

* In Manitoba if the issue, is that of the deceased but not the surviving spouse, then the share of the surviving spouse is as follows: a) $50,000, or one-half of the intestate estate, whichever is greater or;

b) one-half of any remainder of the intestate after allocation of the share provided by clause (a) above.

Notes:A preferential spousal share is generally an amount determined by statute to which the intestate's spouse is entitled (to the extent possible) in preference to all other beneficiaries

In all provinces and territories except Quebec if there is a surviving spouse with no surviving children, the spouse receives all of the intestate deceased's estate – in Quebec, if relatives exist – 1/3 to spouse, 1/3 to parents, 1/3 to brothers or sisters (nieces or nephews); if no parents – ½ to spouse, ½ to relatives; if no relatives – ½ to spouse, ½ to parents

In most provinces and territories, if a person is survived by his or her child or children or in the situation where the child or children are deceased but have living issue at the time of the death of the testator, the estate will go the child or children equally and the share of the deceased child shall be divided amongst that child's heirs (under the appropriate intestacy rules found in provincial statute).

As of January 2002 – subject to change where amendments to As of January 2002 – subject to change where amendments to provincial legislation and regulations occursprovincial legislation and regulations occurs

An estate planning teamAn estate planning teamNo one advisor can complete every task associated with estate planning. It’s a job that calls for the contributions

ofseveral different professionals, namely:

The Accountant, who can offer advice about possible tax consequences.The Financial Advisor, who can recommend products and strategies.The Lawyer, who can draft the will and provide other

legal advice.

Stages of life ………Stages of life ………Many people believe that estate planning is something only

to be considered in one’s old age, after having amassed a small

fortune.

In fact, estate planning is virtually for everyone. Indeed, those

with less money should take a particular interest in making sure the

funds they do have go as far as possible.

Young couples, single professionals, as well as seniors should all

consider how to minimize costs while providing the maximum

amount of money to their chosen heirs.

WillsWillsThe will is the roadmap of the estate planning highway, outlining in detail where your property should go after your death.

Those who die without this document lose all say in the matter — the assets in their estate will be divided up according to a formula in

their province’s legislation.

Legal expertiseLegal expertise While it is possible to write your own Will by hand

(known as a holograph will), it is preferable to use the services of a lawyer, who is an expert in the field and able to avoid any ambiguity in the phrasing of this important document.

Besides keeping your original Will in a safe place, where it

cannot be lost or destroyed, your lawyer will also have the document entered in the Register of Wills, making it easy to locate after your death.

Wills – How to keepWills – How to keep costs costs downdown Before meeting with a lawyer, you should consider

the following: 1. Beneficiaries - that is, who do I want to get my

possessions after I die. Make a list of what you own. Obviously if you are a homeowner that will be first on the list, but also have a list of investments, RRSPs, business interests, as well as other property such as a cottage, family heirlooms and jewelry. Take along the documents for each of these if you have them. With something like your home, the lawyer will need to check as to the type of joint ownership. With appraised jewelry, for example, the appraiser’s description can assist in the description used in the will.

2.Executor - who do I want to be in charge of my estate. Who do I trust to do what I want done. The key word here is trust, not friendship. Trust both in integrity and judgement. You want someone who understands what you want done and how you would want it done.

3. Guardian - who do I want to raise my children (be sure and run this by them first!)

4. Back-ups - who do I want to be second choice for beneficiary, trustee or guardian if the first choice is unable or unwilling to act?

Define your obligations and Define your obligations and responsibilities…..responsibilities…..Obligations:Obligations:

Mortgages and other debts such as loans and credit cardsFinal taxesCosts of settling the estate, such as probate fees and legal fees

Responsibilities:Responsibilities:Income for spouse and dependant childrenFunds to support dependant relatives such as elderly parentsLifelong support for disabled children

ProbateProbate Probate is act of officially proving the authenticity

and validity of a Will in the Courts. Not only does probate slow down the settlement of the succession, it also results in additional legal fees.

A Will drawn up by a lawyer is not subject to probate because the law recognizes lawyers as public officers, and allows them to confer authenticity on their Wills.

It is also possible to avoid probate through the

use of products like life insurance and segregated funds.

Next steps…..Next steps…..

Prepare a Will

Select an executor

Establish a power of attorney

Enduring Power of AttorneyEnduring Power of Attorney

It is important to note that the Power of Attorney document (general, limited or financial) will not be valid if you become mentally incapacitated unless it specifically states that the attorney's authority is to be maintained under this circumstance.

Additional wording is necessary to ensure the document is considered enduring in subsequent mental incapacity. This is commonly referred to as an "enduring Power of Attorney".

Living WillsLiving Wills

The purpose of a living Will is to provide instructions regarding your medical care if you were to become incapacitated and unable to state your wishes. This document may indicate the type of treatment you may or may not wish to receive. A living Will should be created with the assistance of a lawyer or notary and discussed with your family physician and family members.

TrustsTrustsTrusts are a way for an individual to transfer assets to other people while still retaining some control. There are two basic kinds of trusts:

Inter-vivos trusts, which are created during one’s lifetime (the name is Latin, meaning between the living)Testamentary trusts, which are created in the will at the time of death.

Depending on the situation, one or both of these trusts may be required as part of the estate planning process to for example, reduce taxes, pay for the education of children, or to provide ongoing support for a disabled relative.

Beneficiary designationsBeneficiary designationsBesides making provisions for heirs in the Will, it’s also possible to name beneficiaries directly on insurance polices, company pension plans and segregated funds. Under certain conditions, beneficiary designations can allow assets to pass directly to the person named without having

tobecome part of the estate or go through the probate

process.If you haven’t named a beneficiary, the money will flow through to your estate by default.

It is not possible to name a beneficiary on a mutual fund account (depending of It is not possible to name a beneficiary on a mutual fund account (depending of the the

province’s legislation)province’s legislation). But because of their special insurance status, it . But because of their special insurance status, it isis possible topossible to

appoint a beneficiary on segregated fund accounts.appoint a beneficiary on segregated fund accounts.

Irrevocable and revocableIrrevocable and revocable

In Quebec, if you name your legal spouse as beneficiary, that

designation is deemed to be irrevocable unless otherwise

specified – that means you will not be able to change it later

on without his or her approval in writing.

Revocable designations, on the other hand, can be changed

unilaterally in the future and allow for greater flexibility.

Charitable donationsCharitable donationsIn many cases, leaving money to a charity is a win-winproposition—a worthy organization receives funding, whileyour estate obtains a credit that can be applied against

taxes owning elsewhere.Recent changes to tax legislation have also made it

possible toname a charity as beneficiary on a life insurance policy. If

youhave insurance you no longer require for personal or business reasons, you can name your favourite charity asbeneficiary and your estate will receive a credit for the

faceamount of the policy at the time of your death. View our power point on Charitable Giving

Estate PlanningEstate Planning

Next stepsHas this discussion raised any questions or concerns that you’d like to discuss in greater detail?Please feel free to contact us.

Email:[email protected]

Thank You