Estate Planning For The 21st Century - NAELA Tab/Estate... · Estate Planning For The 21st Century...

25

Estate Planning For The 21st Century Presenter’s Name Event Date

Transcript of Estate Planning For The 21st Century - NAELA Tab/Estate... · Estate Planning For The 21st Century...

Estate Planning For The

21st Century

Presenter’s Name

Event Date

IMPORTANT SLIDE INFORMATION

NAELA Members

The following slides were graciously provided by NAELA Member Rajiv Nagaich from Washington state. NAELA members have permission to reuse these slides for their own firm’s purpose. Use of the NAELA logo is limited to active NAELA

members only.

The slides were created to provide a foundation for presenting information on Estate Planning and Long Term Care Planning and MAY NOT provide accurate or current information for your specific state To ensure the accuracy of your presentation, you MUST

review and update the contents of the slides with your state’s legal requirements

Traditional Notions of Estate Planning

Who gets what when I die

Who manages my checkbook and health needs when I can no longer attend to those needs myself

Do I want to be kept alive if I am comatose and cannot communicate

ASSUMPTIONS

Go to sleep and not wake up

My agents will know what to do

Biggest issues are:

Providing for quality of life

Avoiding probate

Avoiding estate taxes

Making it easy for beneficiaries

Assumptions do not apply today

We are living longer – but not necessarily living healthier

One out of eight Americans over 65 dependent on others for day-to-day living activities

One out of every two Americans over 85 dependent on others for day-to-day living activities

Source: Alzheimer’s Disease Facts and Figures, 2007, Alzheimer’s Association

Issues Created

Financing health care costs, many of which may not be covered by Medicare or health insurance

Managing Quality of Life

Financing Long Term Care

Medicare / Health Insurance

Cover acute care needs

Do not cover chronic care needs

Unless . . .

Where Medicare or Health Insurance leave off:

Private assets (including Long Term Care Insurance)

VA

Medicaid

Limitations

Long Term Care Insurance is NOT widely embraced

VA and Medicaid benefits are limited

VA Benefits

Aid and Attendance – non-service connected disability is dependent upon your qualification* up to:

Veteran: $1,645 per month

Spouse of Veteran: $1,057 per month

Married Veteran: $1,945 per month

*http://www.canhr.org/factsheets/misc_fs/html/fs_aid_&_attendance.htm

Medicaid Benefits

Food, shelter and medicine

Income used as deductible towards care costs; $55.45 / $60.78 /$90.00 per month personal needs allowance [state specific, changes annually – please update with your state’s requirements]

All clients treated the same

DME

Semiprivate rooms

Limited personal care needs

What is missing?

ESTATE PLANNING

- Eligibility is Not Automatic

VA Eligibility

Service Requirements

90 days in active duty with 1 day in war time period

World War I: April 6, 1917, through November 11, 1918

World War II: December 7, 1941, through December 31, 1946

Korean War: June 27, 1950, through January 31, 1955

Vietnam War: August 5, 1964 (February 28, 1961, for veterans who served "in country" before August 5, 1964), through May 7, 1975

Persian Gulf War: August 2, 1990, through a date to be set by Presidential Proclamation or Law.

24 months if enlisted after September 7, 1980

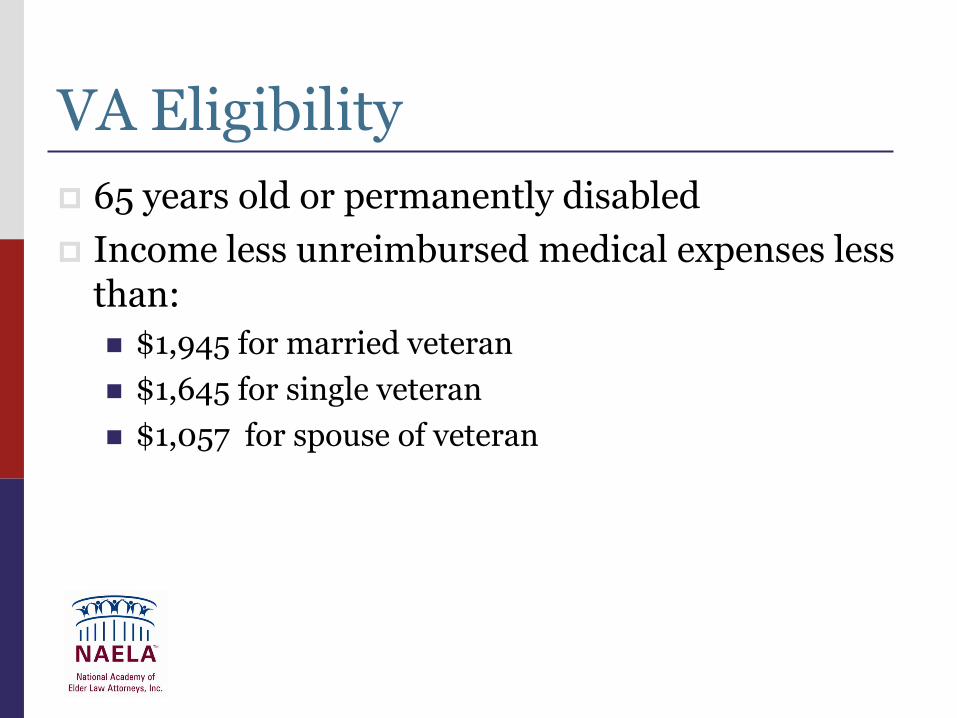

VA Eligibility

65 years old or permanently disabled

Income less unreimbursed medical expenses less than:

$1,945 for married veteran

$1,645 for single veteran

$1,057 for spouse of veteran

VA Eligibility

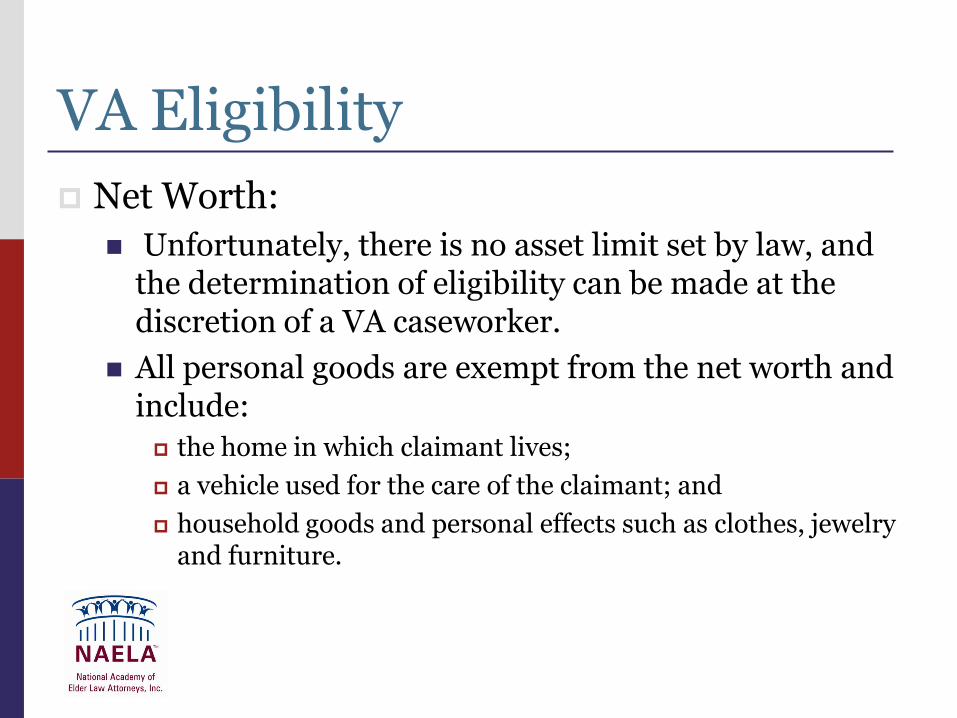

Net Worth:

Unfortunately, there is no asset limit set by law, and the determination of eligibility can be made at the discretion of a VA caseworker.

All personal goods are exempt from the net worth and include:

the home in which claimant lives;

a vehicle used for the care of the claimant; and

household goods and personal effects such as clothes, jewelry and furniture.

Resource Test [state specific, changed every year – please update with your state’s requirements]

Single Applicant:

$2,000

House (with equity of up to $500,000 [$750,000 in some statee])

One automobile (any value)

Prepaid funeral plan (irrevocable and of reasonable value) – burial plots for family members

$1,500 cash value in life policy

Personal property (any value)

BUT- Assets subject to state Medicaid lien

Married Applicant:

$2,000

Spouse of Applicant

House (any value)

One automobile (any value)

Between $74,820 and $109,560

Prepaid funeral plan (irrevocable and of reasonable value) – burial plots for family members

$1,500 cash value in life policy

Personal property (any value)

Who Should Worry?

Middle class Americans

Between $50,000 and $1,500,000 in assets

Estate Planning Solutions

Pre-crisis options

Crisis planning options

Pre-Crisis Planning

Utilize Special Needs Trusts

Utilize Income Only Trusts

Decedent’s share

Survivingspouse owns

all assets

Entire estate subject to spend down to access.

Typical Estate Plan (married)

Surviving Spouse’s share

Decedent’s share

To Testamentary Special Needs

Trust for surviving spouse

Surviving spouse owns

only half estate

Special Needs Trust protected

Way Around the Problem

Surviving spouse’s share

Surviving spouse’s share

subject to spend down

Decedent’s estate

Assets owned by testator during life

Nearly entire estate must be spent down to access VA or Medicaid benefits

Typical Estate Plan (unmarried)

Gift of some assets to irrevocable trust or trusted individual

Trustee can provide funds to beneficiary, who can use funds as beneficiary sees fit.

Assets in irrevocable trust or Safe Harbor Trust protected (subject to look back period)

Way Around the Problem

Settlor cannot be a beneficiary of the principal

Pre-Crisis Planning Update Community Property Agreements (only in community property

states)

Revocable by one party

Update Powers of Attorney

Gifting Powers

Care Management mandate

No authority to enter into arbitration agreements

Living Wills

Update Living Wills after Terry Shiavo

Update Health Care Proxy in states where they are separately required

Pre-Crisis Planning

Discuss your plan with named fiduciaries

Crisis Planning

Financing the costs

Medicare

VA

Medicaid

Develop plan to address quality of life issues

Address Estate Planning issues