Essential Wealth part II - EN-11-V7...

32

THE MANY HATS OF THE MODERN WEALTH MANAGER March 2017 ESSENTIAL WEALTH

-

Upload

truongkhue -

Category

Documents

-

view

214 -

download

0

Transcript of Essential Wealth part II - EN-11-V7...

T H E M A N Y H AT S O F T H E M O D E R N W E A LT H M A N A G E R

March 2017

E S S E N T I A L W E A LT H

3

ESSENTIAL WEALTH

TABLE OF CONTENTS

Foreword 5

Introduction 7Methodology 9Key Findings 10

Part I: The Inevitability of influence 11

Part II: Deconstructing the many hats of a modern wealth advisor 13

Conclusion 27

ABOUT ONELIFEOneLife exists to overturn conventional attitudes to life assurance. As a specialist in this area with 25 years’ experience, we develop cross-border financial planning solutions for Ultra High Net Worth, High Net Worth, and High Affluent clients across Europe and beyond.

Whether it’s a question of long-term savings, inheritance planning or simply understanding how to better manage your wealth, we are dedicated to providing sophisticated, compliant and innovative solutions that are crafted to suit each individual and their evolving needs.

Together with a solid network of select partners — including private banks, family offices and independent financial advisers — our dynamic team of international experts offer a fresh approach that helps understand and anticipate the needs of wealthy clients in a world of change.

With €5bn in assets under management, OneLife is owned by J.C. Flowers & Co — one of the leading investment firms in the international finance industry.

www.onelife.eu.com

ABOUT SCORPIO PARTNERSHIPScorpio Partnership is the world’s leading market research and strategy consultancy to the global wealth industry. The common objective throughout our work is to better orient businesses to deliver what wealth needs next.

We have developed four transformational disciplines that shape our process: SEEK, THINK, SHAPE and CREATE. Each of these fields is designed to support business leaders to strategically assess, plan and drive growth. We specialise in turning high-net-worth (HNW) client insight and financial research studies into actionable strategies that can stimulate customer engagement.

To date, we have interviewed over 40,000 HNW clients from around the world on a range of issues; from their experiences with a financial provider to their hopes, fears and ambitions.

We leverage our deep insight into client needs and expectations to create practical and actionable business development strategies. We work with institutions in the wealth management, private banking, fund management, regulation, IT, technology, insurance and charity and not-for profit sectors.

For more information, visit www.scorpiopartnership.com

FOREWORD

6

emember when we were told to put our ‘thinking caps’ on in school? To indicate we are up for a particular challenge, we ‘throw our hat’ into the ring and we ‘take our hats off’ for

those we are impressed by.

Indeed, it seems that we have always been reminded that the most successful individuals are the ones who can wear many different hats; they can juggle a range of complex situations, assuming a variety of roles whatever the situation demands.

The requirement for multi-talented people could not be more essential than it is in the professional realm of wealth management.

High net worth individuals have had diverse wealth creation experiences and have increasingly complex financial requirements. The way they have achieved their success is through a myriad of factors: from hard work to luck, family help to education – as such, the way that they manage their wealth requires support that is dynamic and adaptable.

As a result, the traditional role of the advisor is transforming – the demands of high net worth individuals require advisors to increasingly expand their skill-set and adopt many different roles.

The challenges of navigating modern life’s complexity are particularly pertinent for Europe’s wealthy investors. The needs of each individual client will dictate the blend that is required from each wealth manager. In other words, financial advisors need to constantly reinvent themselves, develop new skills, and learn on a continuous basis.

FOREWORD

R

INTRODUCTION

8

INTRODUCTION

WELL-ROUNDED WEALTH“And all your future lies beneath your hat.” – John Oldham

ealth management is not a singular job. In fact, it should be thought of as an amalgamation of many different roles. The modern wealth advisor must assume a different appearance whatever the specific situation demands.

With this in mind, we set out on a mission to explore the nuances wealth managers today must take into account in order to survive and thrive. We asked 604 wealthy Europeans to tell us about their experiences with their wealth managers – and we found that clients are increasingly eager for their advisors to guide and empathize with them on a broader scale than has been done in the past.

Our research reveals that the European elite value working with an advisor who is not only their financial guru, but their counsellor, their planner and their educator as well. In other words, the modern wealth manager must wear many different hats.

Wealthy clients look for someone who can offer advice built in accordance to who they are as individuals, to how they have attained success, and how they plan to build and preserve their wealth.

European wealth creators recognize that their fortunes push their financial needs far above and beyond inadequate cookie-cutter approaches. Instead, they are looking for a well-rounded wealth manager – someone who can, when necessary, pull on whichever metaphorical hat is needed.

Marc Stevens Chief Executive Officer

W

9

ESSENTIAL WEALTH

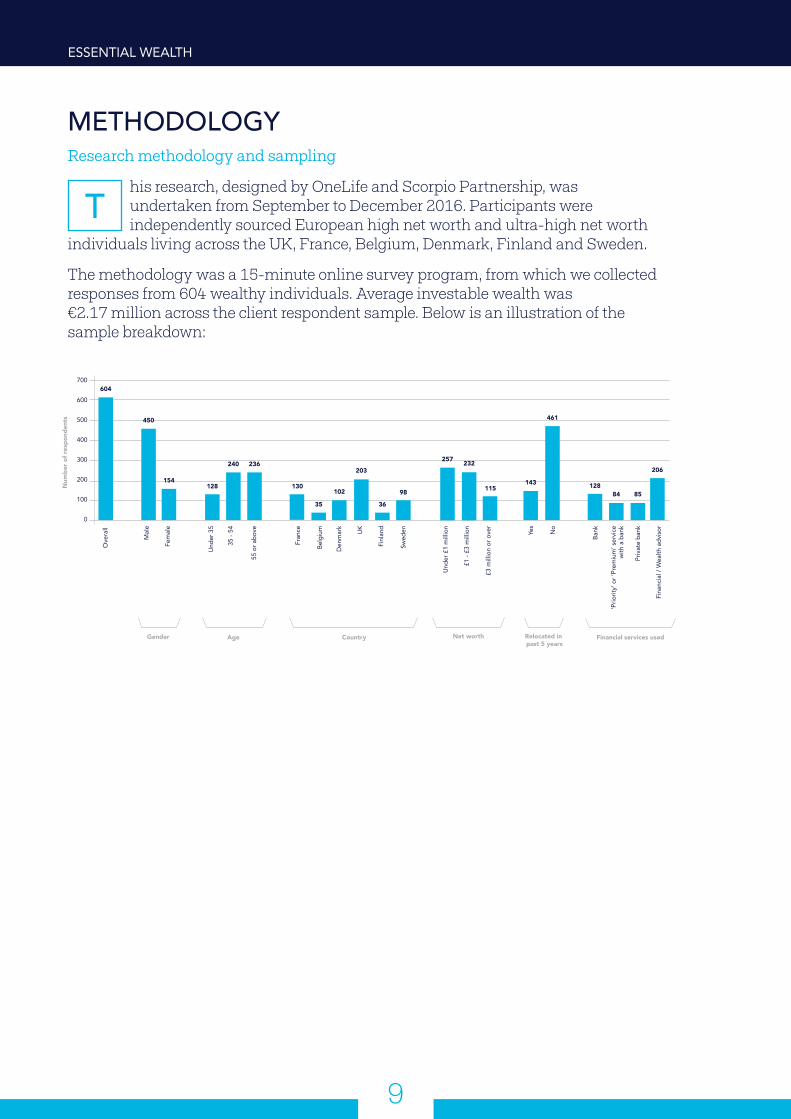

METHODOLOGY

his research, designed by OneLife and Scorpio Partnership, was undertaken from September to December 2016. Participants were independently sourced European high net worth and ultra-high net worth

individuals living across the UK, France, Belgium, Denmark, Finland and Sweden.

The methodology was a 15-minute online survey program, from which we collected responses from 604 wealthy individuals. Average investable wealth was €2.17 million across the client respondent sample. Below is an illustration of the sample breakdown:

Research methodology and sampling

400

500

600

700

300

200

100

0

Ove

rall

Mal

e

Fem

ale

Unde

r 35

35 -

54

55 o

r abo

ve

Fran

ce

Belg

ium

Den

mar

k

UK

Finl

and

Swed

en

Unde

r £1

mill

ion

£1 -

£3 m

illio

n

£3

mill

ion

or o

ver

Yes

No

Bank

‘Prio

rity’

or ‘

Prem

ium

’ ser

vice

with

a b

ank

Priv

ate

bank

Fina

ncia

l / W

ealth

adv

isor

Gender Age Country Net worth Financial services usedRelocated in past 5 years

604

66%450

154128

240 236

130

35

102

203

36

257

143

461

12884 85

206232

11598

Num

ber o

f res

pond

ents

T

10

INTRODUCTION

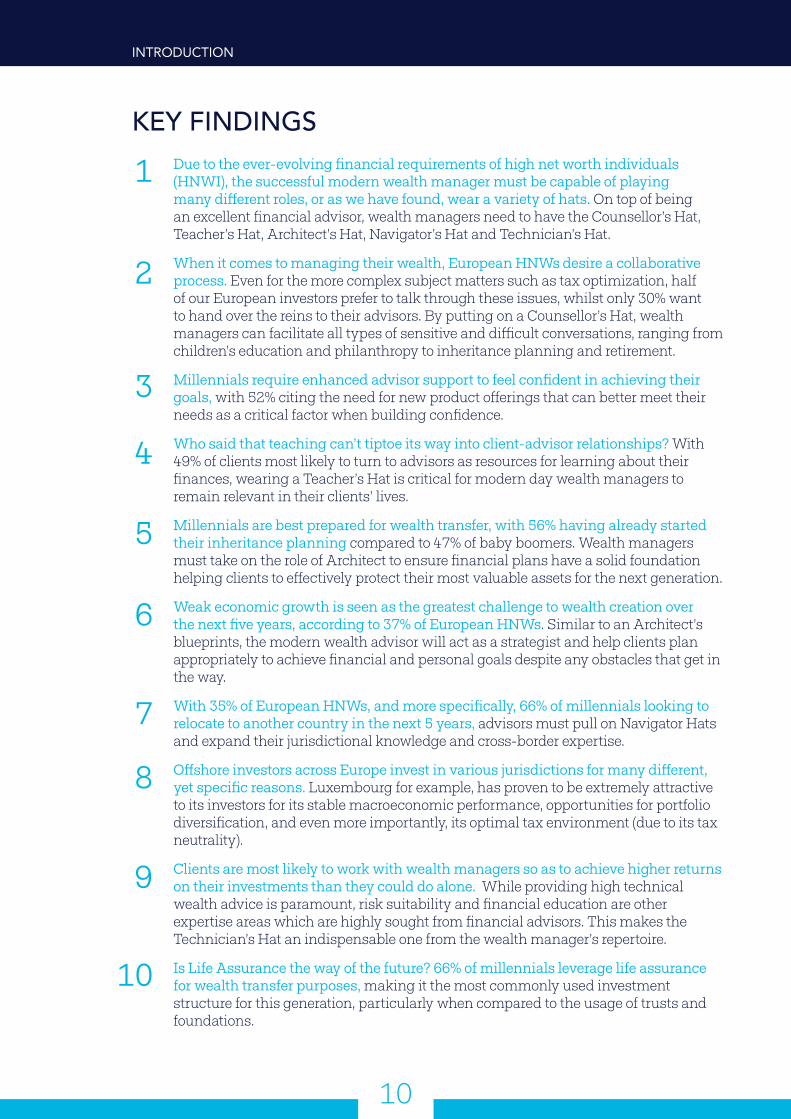

Due to the ever-evolving financial requirements of high net worth individuals (HNWI), the successful modern wealth manager must be capable of playing many different roles, or as we have found, wear a variety of hats. On top of being an excellent financial advisor, wealth managers need to have the Counsellor’s Hat, Teacher’s Hat, Architect’s Hat, Navigator’s Hat and Technician’s Hat.

When it comes to managing their wealth, European HNWs desire a collaborative process. Even for the more complex subject matters such as tax optimization, half of our European investors prefer to talk through these issues, whilst only 30% want to hand over the reins to their advisors. By putting on a Counsellor’s Hat, wealth managers can facilitate all types of sensitive and difficult conversations, ranging from children’s education and philanthropy to inheritance planning and retirement.

Millennials require enhanced advisor support to feel confident in achieving their goals, with 52% citing the need for new product offerings that can better meet their needs as a critical factor when building confidence.

Who said that teaching can’t tiptoe its way into client-advisor relationships? With 49% of clients most likely to turn to advisors as resources for learning about their finances, wearing a Teacher’s Hat is critical for modern day wealth managers to remain relevant in their clients’ lives.

Millennials are best prepared for wealth transfer, with 56% having already started their inheritance planning compared to 47% of baby boomers. Wealth managers must take on the role of Architect to ensure financial plans have a solid foundation helping clients to effectively protect their most valuable assets for the next generation.

Weak economic growth is seen as the greatest challenge to wealth creation over the next five years, according to 37% of European HNWs. Similar to an Architect’s blueprints, the modern wealth advisor will act as a strategist and help clients plan appropriately to achieve financial and personal goals despite any obstacles that get in the way.

With 35% of European HNWs, and more specifically, 66% of millennials looking to relocate to another country in the next 5 years, advisors must pull on Navigator Hats and expand their jurisdictional knowledge and cross-border expertise.

Offshore investors across Europe invest in various jurisdictions for many different, yet specific reasons. Luxembourg for example, has proven to be extremely attractive to its investors for its stable macroeconomic performance, opportunities for portfolio diversification, and even more importantly, its optimal tax environment (due to its tax neutrality).

Clients are most likely to work with wealth managers so as to achieve higher returns on their investments than they could do alone. While providing high technical wealth advice is paramount, risk suitability and financial education are other expertise areas which are highly sought from financial advisors. This makes the Technician’s Hat an indispensable one from the wealth manager’s repertoire.

Is Life Assurance the way of the future? 66% of millennials leverage life assurance for wealth transfer purposes, making it the most commonly used investment structure for this generation, particularly when compared to the usage of trusts and foundations.

1

2

3

4

5

6

7

8

9

10

KEY FINDINGS

PART I: THE INEVITABILITY OF INFLUENCE

12

PART I: THE INEVITABILITY OF INFLUENCE

THE INEVITABILITY OF INFLUENCE

he concept of wealth is ever-evolving. Attitudes

towards success are shaped by numerous opinions, experiences, and influential figures. Family, schooling, and adopted life philosophies undeniably impact our outlook towards our financial and professional goals.

When we asked European high net worth individuals (HNWIs) about their formulas for success, their responses revealed the extent to which each individual path to wealth creation has been unique. The most commonly cited factor contributing to HNWIs current wealth levels was having a strong work ethic, followed by their character and education level.

Despite the individuality of each approach to success, there are differences in the way each generation

perceives their journey. Ultimately, older European investors believe that their success is principally down to them, personally. They describe their strong work ethic and character as the primary drivers to accumulating wealth [Figure 1].

Younger clients, on the other hand, harness a much broader set of experiences to achieve their goals. Their perceptions of success are more complex– they no longer feel that personal drive and ambition alone will get them where they want to be. External influences, such as mentoring and the support of family and friends, also contribute.

The implications for wealth advisors are two-fold. Firstly, the specificity of influences that determine an individual’s success serves as a gentle reminder that HNWIs cannot be viewed

through a single lens. Secondly, if younger clients perceive that the influences which determine their wealth creation are broader, then it is likely that their expectations of the wealth management relationship are also different.

Indeed, the findings reveal that the financial advisor currently holds a coveted role as the primary source of counsel on wealth for over half of older HNWIs. Yet among the younger generations, the proportion who regard their advisor as the main source of influence retracts to 27%.

So what does this mean for the modern wealth advisor? They must quickly adapt if they want to remain relevant. They must understand the client to their very core and determine which role they need to play.

Figure 1: Generational differences in formulas for success Q. We are trying to uncover the formula for success among modern wealth creators. To what extent do

you think each of the following factors has contributed to your current wealth level?

Strong work ethic Luck A clear sense of personal and

professional goals

Education level Professional mentoring

Emotional support from family/friends

The financial position of my family

My ability to take risks

Good financial advice

My character

Under 35 35 - 54 55 or above

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

“With hat in hand, one gets on in the world.” – Berthold Auerbach

T

PART II: DECONSTRUCTING THE MANY HATS OF A MODERN WEALTH ADVISOR

14

DECONSTRUCTING THE MANY HATS OF A MODERN WEALTH ADVISOR

“What is the hatter with me?” – Mad Hatter, Alice in Wonderland

teeped in tradition, but forever reinventing itself, the wealth management profession continues to be an eclectic medley of highly-skilled individuals. These nuances and

differences should be more readily applied and utilised to push the future of the profession forward.

Luckily, this is not just ambitious talk. Many wealth managers are already wearing multiple hats and playing several roles – they’ve understood that this is requisite in the World of Wealth 2.0.

From counsellor, to navigator, architect and teacher to technician - today’s investors are seeking wide-ranging expertise and guidance from their financial advisors, demanding that they successfully play all of these roles.

So let us deconstruct the qualities of an effective wealth manager. This combination of skill-sets unveils the way of the future…

S

15

ESSENTIAL WEALTH

THE COUNSELLOR’S HAT

Onelife’s 100% personal approachHere at OneLife, we help life assurance speak Human. We recognize that the European elite wish to live free from worry and to work alongside a reassuring financial counsellor helping them navigate the most personal of situations.

And because each of these situations are so unique, we think it is critical to ask the right questions. At OneLife, we developed essential tools to help guide initial conversations between clients and their wealth managers.

Our Succession Checklist is just one of many examples. Download it now to see the ways in which OneLife can guide you in your future financial decision-making as well.

W ealth has a way of uncovering raw, deep and

intrinsically complex emotions. Financial discussions give way to an emotional spectrum – revealing feelings of happiness, fear, satisfaction, pride and worry. But the result of this emotional overstimulation can often times leave clients feeling disoriented, unsure of the best decision to make.

Despite the various facets that contribute to individuals’ perceptions of their wealth, European investors do tend to have specific criteria

when looking for wealth managers. They know they need someone who is capable of untangling the knotty, systematic challenges that can often arise from holding significant assets.

We live in a world of intense change – and the result of volatile financial markets can shake the confidence of those individuals with just that little bit more to protect. Change creates uncertainty, and uncertainty impacts on our ability to visualize a defined path.

But this is where advisors have the opportunity to reach deep into their

professional cupboards and pull on their Counsellor Hat.

The idea that HNWIs are simply seekers of ‘hard’ investment advice is a dangerous misconception. Our research indicates that the most successful advisors, both from a client acquisition and retention perspective, are the ones who enhance their client relationships by connecting on a more meaningful level, offering financial advice on more personal life events.

Indeed, wealth managers need to demonstrate their credibility to their clients.

>>>

16

DECONSTRUCTING THE MANY HATS OF A MODERN WEALTH ADVISOR

Figure 2: Topics requiring advisor guidanceQ. Wealth is a broad topic that encompasses every area of financial management from household

budgeting to complex investments. In which areas of your wealth management do you defer to expert advice versus making more independent decisions?

Tax optimization

Investment

Wealth planning / budgeting

Inheritance

Family wealth planning

Retirement

Insurance

Real estate

Relocation

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Fully dedicate to expert Seek advice from expert Make independant decisions

30% 50% 21%

24% 53% 23%

23% 50% 27%

21% 46% 33%

21% 49% 30%

20% 52% 28%

17% 41% 42%

15% 41% 44%

15% 40% 45%

>>> Here, wealthy individuals look for a number of indicators, including a strong advisor reputation, personalized service, high quality of information, and appropriate fees.

Wearing the so-called Counsellor Hat as a wealth manager, marks advisors as a calming influence and world-class listeners, always readily available to discuss clients’ fears or concerns

Indeed, even the wealthiest clients in the world know they must remain within their means to reach their long-term financial goals. As such, they begin to pose questions such as – shall I sell my property abroad if my children are now setting up lives on the other side of the world? Can I retire next year and have enough to continue supporting a

charity close my heart? Is it wise for me to set up another business?

Additionally, the Counsellor is defined by their voice of reason, proactivity and ability to help clients preserve and grow their wealth. They should make clients feel at ease when discussing potential downfalls, and the ‘what if’ scenarios that may not even be top of mind. While conversations about a potential stock market loss, a divorce, or a needy relative may make many feel uncomfortable, the Counsellor Hat provides a filter through which conversations about the unknown are facilitated.

As we’ve seen, advisors play a very influential role in the decision-making of European investors. For a majority,

this means engaging in open dialogue over their wealth. HNWIs are keen to be actively involved in the conversations with their wealth managers. Less than a third want to hand over autonomy for decision-making to advisors in any area of wealth management. To them, the process should be more collaborative.

The modern wealth advisor needs to sensitively recognize which topics their clients want them to take full control of, and which they seek help with. It would be easy to assume that when it comes to technically complex areas like tax optimization, that HNWIs would be willing to delegate decision-making to their advisors. Yet even here, half of clients prefer talking through the issues at hand.

>>>

17

ESSENTIAL WEALTH

Figure 3: Millennials require enhanced advisor support to feel confidentQ. Is there anything your wealth manager could do to increase your confidence in meeting your goals?

Be more proactive in discussing goals

Offer new products that better meet my needs

Provide more comprehensive reports that track / assess progress towards goals

Deliver greater transparency in portfolio allocations and how

they will contribute to achieving goals

I am already satisfied with my wealth manager’s services

0%

10%

60%

50%

40%

30%

20%

Under 35 35 - 54 55 or above

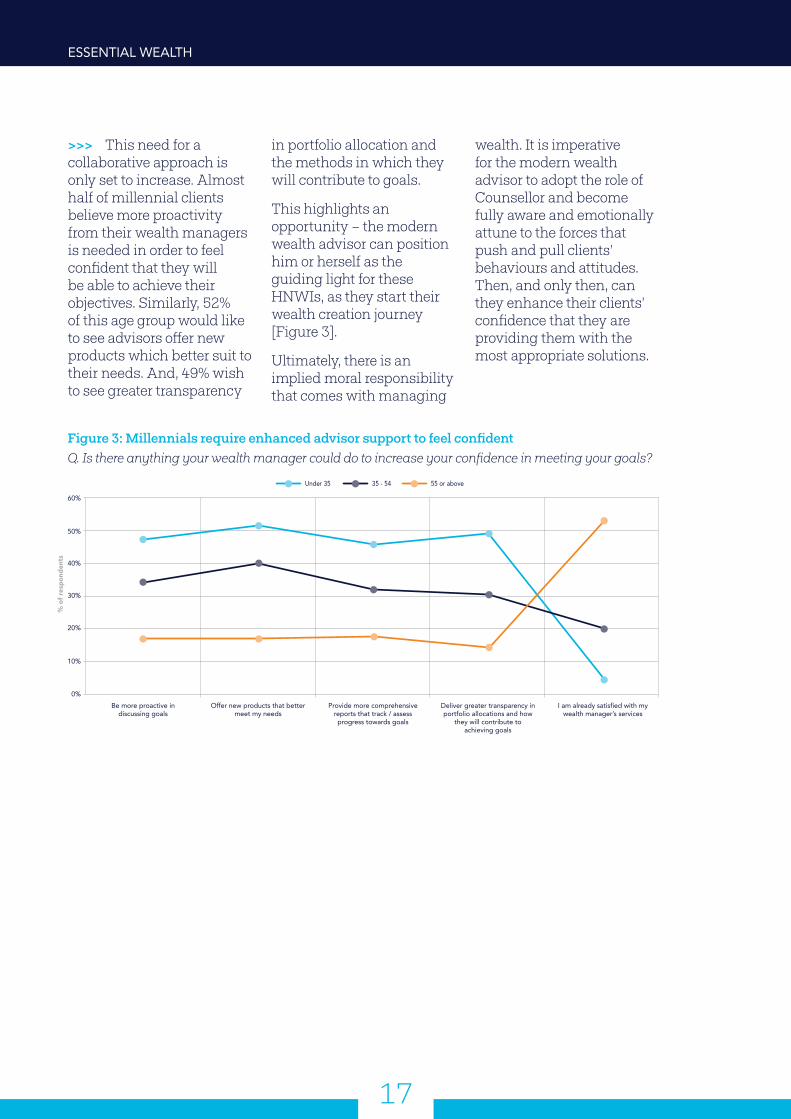

>>> This need for a collaborative approach is only set to increase. Almost half of millennial clients believe more proactivity from their wealth managers is needed in order to feel confident that they will be able to achieve their objectives. Similarly, 52% of this age group would like to see advisors offer new products which better suit to their needs. And, 49% wish to see greater transparency

in portfolio allocation and the methods in which they will contribute to goals.

This highlights an opportunity – the modern wealth advisor can position him or herself as the guiding light for these HNWIs, as they start their wealth creation journey [Figure 3].

Ultimately, there is an implied moral responsibility that comes with managing

wealth. It is imperative for the modern wealth advisor to adopt the role of Counsellor and become fully aware and emotionally attune to the forces that push and pull clients’ behaviours and attitudes. Then, and only then, can they enhance their clients’ confidence that they are providing them with the most appropriate solutions.

18

THE TEACHER’S HAT

The sharing economyWealth managers must take their role as financial educators very seriously.

At OneLife, we are committed to providing our partners with high-quality, industry-leading insights. Our teaching often comes in the form of technical events, but we also distribute our content on a variety of digital platforms – ranging from newsletters, blog posts, and digital guides.

We are dedicated to highlighting the myriad of benefits life assurance can bring to wealth planning strategies. In teaching our partners about its intricacies, we not only reinforce our relationship with them, but in turn better their service to our common end-clients.

he modern-day holistic advisor has a lot on their plate.

The multiplicity of factors being juggled by wealth managers can sometimes feel overwhelming.

Amongst the focus, time and energy spent on managing client relationships and implementing financial strategies, the importance of the advisor’s role as a source and fountain of knowledge can fall to the wayside. But embracing the role of educator should not be taken lightly by wealth professionals.

Because whilst there is investment guidance, counselling, and confidence-building – the real heart of the client relationship lays within the ability of the wealth manager to pull on a Teacher’s Hat. Ultimately, clients need someone to help guide them through the complexities and

technicalities of the financial world.

Just over half of the European super-wealthy over the age of 55 state that their wealth manager acts as their primary educational source when learning about managing wealth. It is clear that this structured instruction is a crucial layer of the professional wealth relationship [Figure 4]. Intriguingly however, it is the youngest clients that are seeking out less structured education from their professional advisors – instead preferring to learn from a much wider range of sources. In a world of instantly accessible information, being an educator for the younger generation may then, require a radical shift in activity and positioning from the wealth manager’s perspective.

>>>

T

DECONSTRUCTING THE MANY HATS OF A MODERN WEALTH ADVISOR

19

ESSENTIAL WEALTH

THE TEACHER’S HAT

Figure 4: Client groups leveraging various resources to learn about wealthQ. Which of the following resources have you used to learn about managing your wealth?

Formal education programmes

Through a school / university curriculum

Via discussions with my parents /

grandparents

From my spouse or partner

Conversations with a wealth manager / private banker

Blogs or online resources

Financial press or newspaper

Other0%

10%

60%

50%

40%

30%

20%

Under 35 35 - 54 55 or above

>>> Perhaps millennials have become disillusioned with the idea that an advisor should act as an educator?

Maybe they have witnessed too much of a lack of educational initiative? Whatever the reason, we feel that this is most certainly a missed opportunity.

Advisors should reorient their educational approach

when looking to collaborate with these younger investors. They should leverage the fact that they are now coming face to face with a generation who is self-reliant, and for the large part, tech-savvy.

Pointing these clients to interesting information resources as well as providing helpful materials will demonstrate a keenness

to get involved, but facilitate the independent approach of these ‘do-it-yourselfers’.

Wealth managers need to polish off their mortarboard hats and become accustomed to the changing requirements of the younger generation when it comes to information consumption, adapting their own teaching styles to fit those needs.

20

here is a level of intuition that comes into planning

clients’ futures. This calls for the Architect’s Hat to be carefully placed on advisors’ heads, assuring clients that a high degree of preparation will be integrated into their wealth management. But this planning is not to be confined to pre-developed designs. The master Architect leverages the very latest materials, tools and techniques to create an innovative blueprint, while being aware of technical limitations which could disrupt their plan.

Relationships are built on trust – and trust is gained when advisors can extensively demonstrate their capability to become involved in the planning of a clients’ wider wealth spectrum.

As it happens, millennials prove to be incredibly well-versed in the concept of planning. When asked whether they had yet started creating a wealth transfer plan, just over half of under 35’s said they had.

This forward-looking attitude resonated less with older client bases, with 41% of high net worth individuals between the ages of 35 and 54 stating they had embarked on the wealth transfer planning journey, and 47% of over 55’s saying the same [Figure 5].

Despite being the age group furthest from retirement, millennials appear to not want to be caught off guard by any unexpected economic or personal turbulence – even if that turbulence lays decades ahead. Perhaps because they came of age during a global financial crisis or

because their instant access to data and information makes them broadly more aware of the importance of planning ahead – this particular group of clients are acutely aware of the ephemerality of wealth.

As such, they will do anything – or at least be slightly more preventative than older generations – to protect it. And as a result, they require someone who can appropriately and intelligently facilitate discussions around wealth transfer and wider life goals.

Trust can similarly be gained and strengthened during said challenging economic times. The wealth manager should be perceived as the strategist clients can turn to when deciding how to pre-empt the impact of their finances on future life decisions.

>>>

THE ARCHITECT’S HAT

T

Figure 5: Wealth transfer plan creation Q. Have you started your wealth transfer planning?

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

Ove

rall

(N=4

98)

Mal

e (N

=366

)

Fem

ale

(N=1

32)

Unde

r 35

(N=1

22)

35 -

54 (N

=220

)

55 o

r abo

ve (N

=156

)

Fran

ce (N

=123

)

Belg

ium

(N=3

1)

Den

mar

k (N

=70)

UK (N

=163

)

Finl

and

(N=2

6)

Swed

en (N

=85)

Unde

r £1

mill

ion

(N=2

12)

£1 -

£3 m

illio

n (N

=188

)

£3

mill

ion

or o

ver (

N=9

8)

Yes (

N=1

36)

No

(N=3

62)

Bank

(N=1

06)

‘Prio

rity’

or ‘

Prem

ium

’ ser

vice

with

a b

ank

(N=6

7)

Priv

ate

bank

(N=7

2)

Fina

ncia

l / W

ealth

adv

isor (

N=1

63)

Gender Age Country Net worthFinancial services used

Relocated in past 5 years

10%

9%

35%

46%

10%

9%

34%

47%

10%

8%

36%

45%

7%7%

31%

56%

9%

8%

42%

41%

14%

12%

27%

47%

6%2%

41%

50% 50%

13%

16%

32%

39%

13%

16%

21%

48%

11%

14%

27%

43%

13%

8%

36%

46%

8%

11%

35%

54%

8%

7%

31%

40%

11%

11%

38%

47%

8%

12%

32%

51%

7%

18%

24%

54%

10%1%

35%

39%

13%

7%

40%

65%

7%2%

26%

43%

10%

8%

39%

42%

15%

42%

Yes Not yet No I do not plan to I have not decided whether or not I want to set up a wealth transfer plan yet

DECONSTRUCTING THE MANY HATS OF A MODERN WEALTH ADVISOR

21

ESSENTIAL WEALTH

Figure 6: Future challenges to wealth creationQ. Which of the following do you anticipate will be the greatest challenge to your wealth creation over

the mid-term (1-5 years)?

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

Ove

rall

(N=5

64)

Mal

e (N

=420

)

Fem

ale

(N=1

44)

Unde

r 35

(N=1

19)

35 -

54 (N

=230

)

55 o

r abo

ve (N

=215

)

Fran

ce (N

=122

)

Belg

ium

(N=3

0)

Den

mar

k (N

=94)

UK (N

=195

)

Finl

and

(N=3

4)

Swed

en (N

=89)

Unde

r £1

mill

ion

(N=2

40)

£1 -

£3 m

illio

n (N

=217

)

£3

mill

ion

or o

ver (

N=1

07)

Yes (

N=1

35)

No

(N=4

29)

Bank

(N=1

14)

‘Prio

rity’

or ‘

Prem

ium

’ ser

vice

with

a b

ank

(N=7

8)

Priv

ate

bank

(N=8

0)

Fina

ncia

l / W

ealth

adv

isor (

N=1

99)

Gender Age Country Net worth Financial services usedRelocated in past 5 years

37%

13%

11%

15%

21%

40%

12%

10%

15%

21%

29%

17%

15%

15%

23%

22%

26%

14%

17%

21%

30%

16%

13%

17%

23%

53%

2%

8%

12%

20%

22%

17%

10%

26%

25%

30%

17%

3%

20%

30%

35%

13%

15%

11%

23%

29%

18%

16%

20%

13%

40%

12%

11%

13%

23%

34%

15%

10%

17%

22%

40%

12%

14%

18%

16%

20%

23%

19%

24%

15%

36%

19%

8%

11%

25%

55%

6%

8%8%

22%

31%

15%

15%

20%

19%

39%

12%

13%

16%

18%

43%

10%

9%

13%

23%

9%

74%

15%

59%

3%

6%3%

2%26%

Low interest rate Asset protection Volatile exchange rate Weak economic growth Strong inflation Other

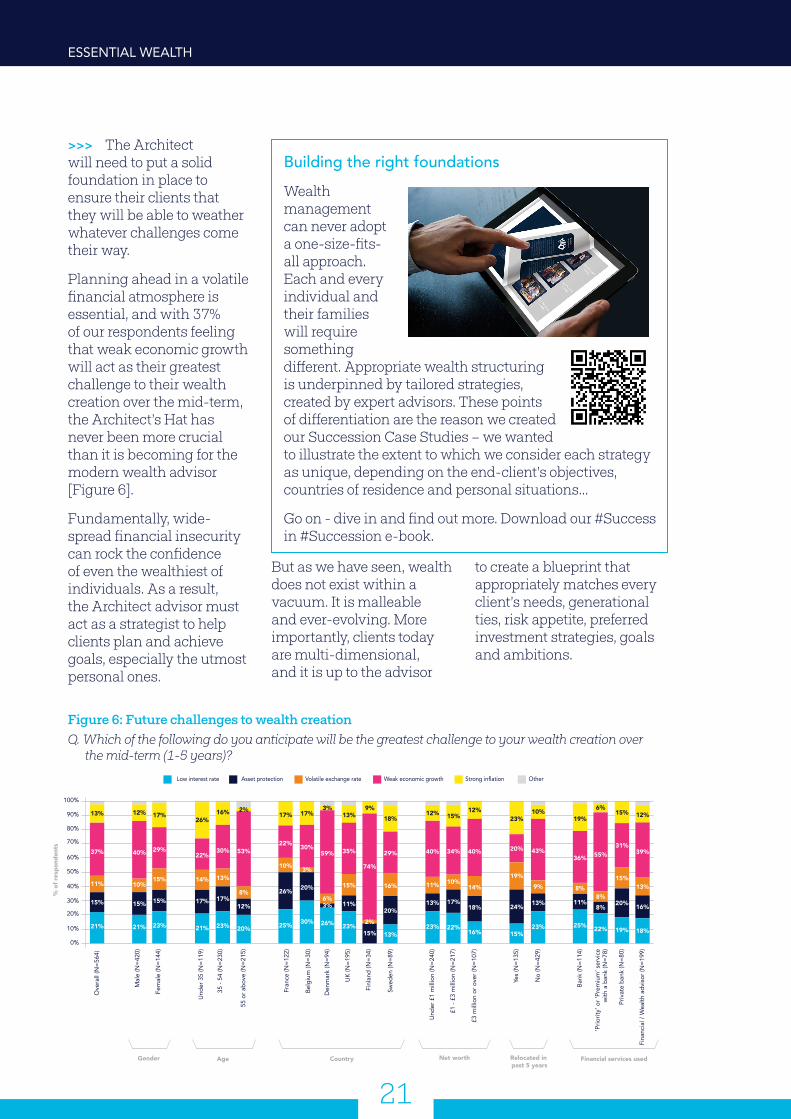

>>> The Architect will need to put a solid foundation in place to ensure their clients that they will be able to weather whatever challenges come their way.

Planning ahead in a volatile financial atmosphere is essential, and with 37% of our respondents feeling that weak economic growth will act as their greatest challenge to their wealth creation over the mid-term, the Architect’s Hat has never been more crucial than it is becoming for the modern wealth advisor [Figure 6].

Fundamentally, wide-spread financial insecurity can rock the confidence of even the wealthiest of individuals. As a result, the Architect advisor must act as a strategist to help clients plan and achieve goals, especially the utmost personal ones.

But as we have seen, wealth does not exist within a vacuum. It is malleable and ever-evolving. More importantly, clients today are multi-dimensional, and it is up to the advisor

to create a blueprint that appropriately matches every client’s needs, generational ties, risk appetite, preferred investment strategies, goals and ambitions.

THE ARCHITECT’S HATBuilding the right foundationsWealth management can never adopt a one-size-fits-all approach. Each and every individual and their families will require something different. Appropriate wealth structuring is underpinned by tailored strategies, created by expert advisors. These points of differentiation are the reason we created our Succession Case Studies – we wanted to illustrate the extent to which we consider each strategy as unique, depending on the end-client’s objectives, countries of residence and personal situations…

Go on - dive in and find out more. Download our #Success in #Succession e-book.

22

Figure 7: High net worths intending to re-locateQ. Do you intend to move to another country to live and / or work in the next 5 years?

40%

50%

60%

70%

80%

90%

100%

30%

20%

10%

0%

Ove

rall

(N=6

04)

Mal

e (N

=450

)

Fem

ale

(N=1

54)

Unde

r 35

(N=1

28)

35 -

54 (N

=240

)

55 o

r abo

ve (N

=236

)

Fran

ce (N

=130

)

Belg

ium

(N=3

5)

Den

mar

k (N

=102

)

UK (N

=203

)

Finl

and

(N=3

6)

Swed

en (N

=98)

Unde

r £1

mill

ion

(N=2

57)

£1 -

£3 m

illio

n (N

=232

)

£3

mill

ion

or o

ver (

N=1

15)

Yes (

N=1

43)

No

(N=4

61)

Bank

(N=1

28)

‘Prio

rity’

or ‘

Prem

ium

’ ser

vice

with

a b

ank

(N=8

4)

Priv

ate

bank

(N=8

5)

Fina

ncia

l / W

ealth

adv

isor (

N=2

06)

Gender Age Country Net worth Financial services usedRelocated in past 5 years

65%

35%

68%

32%

55%

45%

34%

66%

56%

44%

90%

10%

41%

59%

46%

54%

67%

33%

72%

28%

66%

34%

67%

33%

65%

35%

59%

41%

21%

79%

73%

27%

74%

26%

53%

47%

68%

32%

78%

22%

92%

8%

Yes No

n wealth, every story is unique. And for Europe’s wealthy

wanderers, life choices and financial goals are set within a global context. In an ever more connected world, international mobility is becoming the norm.

Yet the complexity caused by international wealth can be intimidating and overwhelming. Actually, it should be seen as exciting and inspiring. Advisors have the opportunity to offer a refreshing sense of comfort to their clients by demonstrating that they are able to not only understand their clients’ needs, but pre-empt them internationally as well.

Wealth managers need to firmly pull on their Navigator hats if they want to keep up with their increasingly international client base. The modern wealth advisor will be able to harness the unique opportunities in different locations across the globe; putting on the Navigator Hat will enable advisors to identify and understand those opportunities.

With 35% of European investors intending to move countries in the next 5 years, and this percentage catapulting up to 66% amongst millennials, it is clear that advisors need to have extensive knowledge of clients’ potential

international investments and the jurisdictional variances of different geographies [Figure 7].

>>>

THE NAVIGATOR’S HAT

I Free of all bordersHeadquartered in Luxembourg, the leading cross-border life assurance center in Europe, OneLife is well-positioned to combine a large range of varied expertise, ranging from tax, to legal and civil matters. As a result of this technical proficiency, we can develop solutions adapted to meet a variety of local regulations, especially in the case of a client’s relocation.

DECONSTRUCTING THE MANY HATS OF A MODERN WEALTH ADVISOR

23

ESSENTIAL WEALTH

THE NAVIGATOR’S HAT >>> Financial expertise is not bound by geographic limits – and as a result, high net worth individuals are keen to track down advisors whose knowledge expands across borders, so that they are reassured that their international lifestyle and multi-jurisdictional needs can be appropriately managed.

Naturally, clients’ investments are mainly held in their home market. Yet, many of our European respondents have additional offshore investments as well – and interestingly, different

markets were prioritised for very different reasons [Figure 8].

This dynamic interplay between specific markets and the benefits they reap across a broad spectrum of wealth factors is hugely important for modern advisors. Without a Navigator Hat at hand, advisors may not be adequately informed about varying jurisdictional differences, and the differing cultural perceptions about wealth. Understanding these cultural nuances is key when identifying the

best and most applicable investment opportunities for their clients.

Varying tax environments are undoubtedly a top concern for Europe’s wealth creators. Twenty-six percent of offshore clients who invest in Luxembourg claim to have done so for its optimal tax environment. Furthermore, its stable macroeconomic performance and portfolio diversification opportunities also rank highly amongst these HNWs.

Figure 8: Various jurisdictional investments Q. What is the primary reason you have invested in each of these jurisdictions? [Offshore only]

Finland

France

Ireland

Luxembourg

Monaco

Sweden

Switzerland

UK

Other

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Strong investment performance

Stable macroeconomic performance

Diversification of my portfolio

Regional products on offer

Referred by my relationship manager / the person that manages my account

Lower fees

Regulatory environment

Political stability

Tax environment

None of these

Denmark

Belgium 11% 3% 19% 14% 3% 11% 8% 3%

3%

3%

5%

5%

2%

3%

4%

1%

3%

14%

6%

6%

8%

17%

26%

21%

4%

18%

4%

6%

10%

11%

5%

7%

13%

15%

11%

19%

5%

4%

3%

8%

3%

7%

4%

8%

5%

7%

5%

2%

14% 14%

6%

11%

3%

10%

7%

8%

2%

10%

13%

4%

29%

11%

12%

14%

7%

10%

13%

4%

9%

14%

6%

11%

20%

10%

7%

8%

9%

7%

8%

4%

10%

17%

27%

21%

15%

3%

27%

9%

24%

23%

19%

11%

3%

2%

15%

8%

5%

7%

7%

6%

6%

11%

12%

7%

4%

18%

20%

16%

21%

23%

24

Figure 9: Reasons for working with a wealth managerQ. For which of the following reasons do you work with a wealth manager?

0% 10% 20% 30% 40% 50%

Other 1%

To help me plan for a major life event 14%

To have someone to discuss ideas with 25%

For peace of mind that I can preserve my wealth 29%

To develop a strategic plan that can help me reach my goals 29%

To save me the time and effort of managing my own investments 32%

To enhance my expertise in wealth of finance 34%

To make sure my investments match my risk appetite 38%

For higher returns in my investments than I would achieve myself 44%

n an era driven by instant access to information,

data over-crowding, and changing tax environments, it is little wonder that clients feel overwhelmed by it all. Am I still making the right investments? How are the stocks doing today? Should I continue using the same bank I always have? Concerns rooted in technical expertise can shake a client’s confidence if they do not have a reliable sounding board on which they can bounce off ideas and questions.

Adamant to safeguard their wealth, private clients are on the look-out for advisors who can consistently demonstrate that their expertise and technical know-how is cutting edge.

As such, wealth managers need to have the meticulousness of a Technician – all aspects and parts of their professional expertise need to be aligned and functioning. Clients are hungry for information and a consistent reassurance that their portfolios and risks are being managed effectively. As a result, advisors must be fully up to date in the industry, continuously seeking to enhance their knowledge across a range of areas.

In asking our wealthy respondents for which reasons they decided to work with a wealth manager, 44% said it was to achieve higher returns on their investments than they could achieve themselves [Figure 9].

>>>

THE TECHNICIAN’S HAT

I Trusted and innovative expertise We like to consider ourselves as always being ahead of the curve.

OneLife has extensive expertise in traditional and non-traditional assets to meet the evolving needs of a sophisticated clientele.

We investigate future wealth management trends and life assurance expectations to ensure we continuously innovate and pinpoint how we can help clients achieve more, by leveraging all of the benefits life assurance contracts can offer.

DECONSTRUCTING THE MANY HATS OF A MODERN WEALTH ADVISOR

25

ESSENTIAL WEALTH

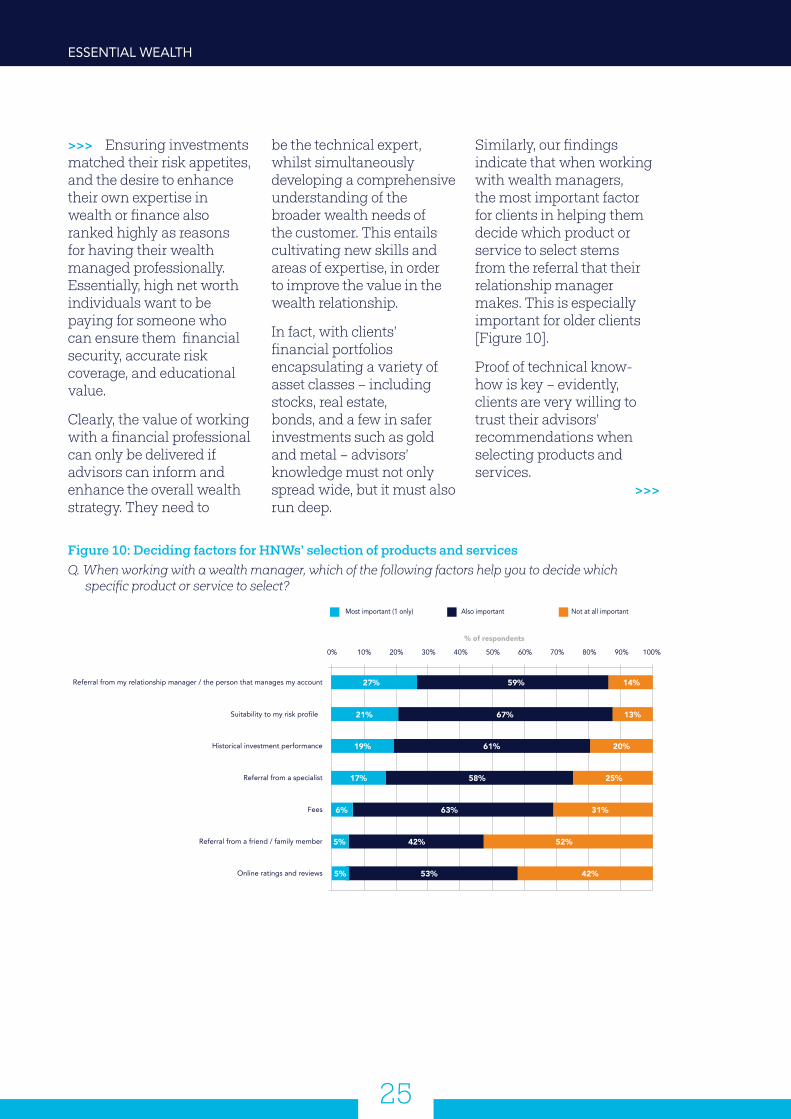

THE TECHNICIAN’S HAT >>> Ensuring investments matched their risk appetites, and the desire to enhance their own expertise in wealth or finance also ranked highly as reasons for having their wealth managed professionally. Essentially, high net worth individuals want to be paying for someone who can ensure them financial security, accurate risk coverage, and educational value.

Clearly, the value of working with a financial professional can only be delivered if advisors can inform and enhance the overall wealth strategy. They need to

be the technical expert, whilst simultaneously developing a comprehensive understanding of the broader wealth needs of the customer. This entails cultivating new skills and areas of expertise, in order to improve the value in the wealth relationship.

In fact, with clients’ financial portfolios encapsulating a variety of asset classes – including stocks, real estate, bonds, and a few in safer investments such as gold and metal – advisors’ knowledge must not only spread wide, but it must also run deep.

Similarly, our findings indicate that when working with wealth managers, the most important factor for clients in helping them decide which product or service to select stems from the referral that their relationship manager makes. This is especially important for older clients [Figure 10].

Proof of technical know-how is key – evidently, clients are very willing to trust their advisors’ recommendations when selecting products and services. >>>

Figure 10: Deciding factors for HNWs’ selection of products and servicesQ. When working with a wealth manager, which of the following factors help you to decide which

specific product or service to select?

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Most important (1 only) Also important Not at all important

15%

Referral from my relationship manager / the person that manages my account 27% 59% 14%

Fees 6% 63% 31%

Referral from a friend / family member 5% 52%42%

Online ratings and reviews 5% 42%53%

Referral from a specialist 17% 58% 25%

Historical investment performance 19% 61% 20%

Suitability to my risk profile 21% 67% 13%

26

>>> There does however need to be enough proof to give them the confidence that they can do so. Younger clients’ confidence and trust in their advisors can be validated through alternative mediums such as competitive fees and having access to specialists within their wealth firms.

Notably, with 63% of our European investors stating they have investments in pensions, 53% in life assurance, and 25% in trusts, advisors must ensure their expertise across such structures is fine-tuned.

Interestingly however, when asked about which investment vehicles they intend to leverage for wealth transfer, 66% of

high net worth millennials pinpointed life assurance as the most leveraged investment structure for wealth transfer [Figure 11].

Although life assurance appears to have less traction among the older audience, it is in fact an ideal solution for those whose wealth spans borders, due to the high level of customization and flexibility it provides.

Life assurance contracts enable a gamut of benefits – from tax optimization to investments, wealth planning and inheritance planning, its structure leverages a platform which facilitates a range of wealth planning activities. In fact, when we probed our respondents about what

they considered to be their greatest challenge when transferring wealth, 32% expressed concern around inheritance tax.

So, carpe diem. The time to seize life assurance for all of the advantages this product can bring, is now. Life assurance does appear to already be making a name for itself amongst younger clients all over Europe. Wealth managers therefore should jump on the opportunity and aim to increase their clients’ awareness of life assurance’s tax benefits, inheritance planning advantages, and wider wealth planning.

Figure 11: Life Assurance investmentsQ. What investment vehicles do you intend to leverage for this wealth transfer? [Life assurance]

40%

50%

60%

70%

30%

20%

10%

0%

Ove

rall

(N=2

31)

Mal

e (N

=171

)

Fem

ale

(N=6

0)

Unde

r 35

(N=6

8)

35 -

54 (N

=90)

55 o

r abo

ve (N

=73)

Fran

ce (N

=62)

Belg

ium

(N=1

2)

Den

mar

k (N

=35)

UK (N

=70)

Finl

and

(N=1

1)

Swed

en (N

=41)

Unde

r £1

mill

ion

(N=9

1)

£1 -

£3 m

illio

n (N

=87)

£3

mill

ion

or o

ver (

N=5

3)

Yes (

N=8

8)

No

(N=1

43)

Bank

(N=5

0)

‘Prio

rity’

or ‘

Prem

ium

’ ser

vice

with

a b

ank

(N=3

4)

Priv

ate

bank

(N=3

9)

Fina

ncia

l / W

ealth

adv

isor (

N=6

4)

Gender Age Country Net worth Financial services usedRelocated in past 5 years

51% 49%

55%

66%

58%

27%

53%58%

31%

57%

64%

46% 46%

38%

56%53%53%

49%53% 53%

47%66%

DECONSTRUCTING THE MANY HATS OF A MODERN WEALTH ADVISOR

CONCLUSION

28

or Europe’s wealth hunters, the world really is their oyster. They have worked hard to create and safeguard their fortunes, and as a result have developed a very clear sense of what they need and

expect from their wealth advisors.

Crucially, the global elite have a variety of options when it comes to safeguarding and managing their wealth, so when initiating a professional financial relationship, they are not purely looking for the advisor with the highest investment performance scorecard. They are looking for an advisor who can add real value to several layers of their lives – someone who can wear many different hats, and as a result provide them with stellar investment performance, a strong and trusting relationship, and a capability to adapt these skills across geographic borders.

This will become even more critical for advisors looking to attain and retain the new set of young and internationally mobile high net worth individuals whom have emerged. We have seen signs that this segment, and their requirements of advisors, will grow rapidly in the future.

In essence, the modern wealth manager will need to accurately understand and forecast the current and imminent requirements of their clients. They will need to take into account the myriad of factors, situations, attitudes and experiences that affect particular clients’ views on how they want and need their wealth managed.

CONCLUSION

F

MOVING WITH THE TIMES

29

ESSENTIAL WEALTH

Our recommendation to advisors? Start dusting off the professional hats that you may have stuffed away over the years – because in order to reach your greatest potential, you must experience change and force yourselves to adapt across a range of skill-sets, investment structures, personal scenarios and difficult conversations.

There is an old adage that goes, “You can’t change your situation, the only thing you can change is how you choose to deal with it.” And this statement couldn’t be truer than it is in the context of the changing wealth management industry. The mixed picture of clients’ changing needs in their wealth management is expected in this day and age.

But here at OneLife, we want to assure high net worth individuals that we can go above and beyond effectively dealing with their fluctuating needs and requirements. We want to offer life assurance contracts that can help these wealth creators live with freedom from worry, confident that all of their bases are covered. We want to create a space where the wealthy can openly discuss the meaning of their wealth, whilst being supported by products and services of the highest quality.

But most importantly, we want to ensure they know they are working with advisors versed in a variety of expertise areas – advisors with many, many hats.

The content of this report is intended solely to provide general guidance to the reader of these pages on the future of life insurance market and the services offered by the life assurance companies member of the OneLife Group (OneLife), based on an independent survey conducted by Scorpio Partnership. The information contained within these pages is not intended as an offer or solicitation for the purchase or sale of any life assurance product. Neither is the information intended to constitute any form of legal, fiscal or investment advice and it should therefore be used only in conjunction with appropriate professional advice obtained from a suitable qualified professional source. OneLife does not guarantee that the information contained within these pages is complete, accurate or up to date. OneLife therefore expressly disclaims any and all liability to any person in respect of anything, done or omitted to be done wholly or partly in reliance upon the whole or any part of the content of this report.

Connect with us

Graphic design & conception : Quadra-Com / quadra-com.fr

linkedin.com/company/the-onelife-company [email protected]

onelife.eu.com/blogtwitter.com/the1lifeco

ON

E/N

C/N

C/C

OR

P/00

70/E

N/0

01/1

703

onelife.eu.com