era.gv.at · Web viewVenture capital (VC) has been recognized to meet risk-capital need. However,...

35

FINANCIAL INSTRUMENTS CHALLENGE PAPER Mutual Learning Exercise 1

Transcript of era.gv.at · Web viewVenture capital (VC) has been recognized to meet risk-capital need. However,...

FINANCIAL INSTRUMENTS CHALLENGE PAPER

Mutual Learning Exercise

1

EUROPEAN COMMISSIONDirectorate-General for Research and InnovationDirectorate A— Policy Development and CoordinationUnit A.4 — Analysis and monitoring of national research policiesContact: Benat BILBAO OSORIO

E-mail: [email protected] [email protected]

European CommissionB-1049 Brussels

2

EUROPEAN COMMISSION

FINANCIAL INSTRUMENTS CHALLENGE PAPER

Mutual Learning Exercise

Vanja Rangus, Supervisory Board of the Venture Capital Fund Slovenia;

Jacek Warda, JPW innovation Associates Inc

June, 2015

Directorate-General for Research and Innovation

2015 EN

LEGAL NOTICENeither the European Commission nor any person acting on behalf of the Commission is responsible for the use which might be made of the following information.The views expressed in this publication are the sole responsibility of the author and do not necessarily reflect the views of

the European Commission.

More information on the European Union is available on the Internet (http://europa.eu).

Luxembourg: Publications Office of the European Union, 2015.

ISBN 978-92-79-47690-7doi: 10.2777/194026

© European Union, 2015Reproduction is authorised provided the source is acknowledged.

EUROPE DIRECT is a service to help you find answers to your questions about the European Union

Freephone number (*):00 800 6 7 8 9 10 11

(*) The information given is free, as are most calls (though some operators, phone boxes or hotels may charge you)

INTRODUCTION.........................................................................................................................................6Evolution of an innovative firm.........................................................................................................6Modes of Public Support...................................................................................................................8

INSTITUTIONAL LENDING: LOANS AND GUARANTEES...............................................................................9Guarantees.....................................................................................................................................10Improving collateral........................................................................................................................10Table 1: Guarantee schemes: country examples...........................................................................13

TAX CREDITS FOR INDIVIDUAL INVESTORS (BUSINESS ANGELS)............................................................13Key considerations.........................................................................................................................14Quality of investor..........................................................................................................................14Targeting........................................................................................................................................15Country examples..........................................................................................................................16Challenges......................................................................................................................................17Table 2: Tax incentives for investors..............................................................................................18

EQUITY INCENTIVES................................................................................................................................19Table 3: Venture Capital investment: G7 and selected European countries (percentage of

GDP)................................................................................................................................................19Government-sponsored funds........................................................................................................20Table 4: A profile of a generic co-investment fund.........................................................................21Challenges in design, implementation and evaluation...................................................................22

ALTERNATIVE FINANCE...........................................................................................................................25

[KI-04-15-284-EN-N]INTRODUCTION

Small and medium-sized enterprises (SMEs) are the driver of innovation, job creation and productivity but are facing difficulties in accessing financing through all phases of company growth. Governments have been trying to overcome this barrier for a long time.

A broad range of types of financial instruments (FI) has been developed which provide debt instruments such as loans or guarantees to companies facing difficulties in accessing finance, tax incentives or equity/risk capital to firms. Banks and related lending institutions are typically risk-averse and require collateral which young companies do not have. Governments address this problem by assuming part of the risk through loan guarantee schemes that give collateral to SMEs in order to secure loans. This initiative appears not to address needs of innovative companies that mainly depend on risk capital to finance their R&D and growth.

Venture capital (VC) has been recognized to meet risk-capital need. However, it has its own problems as generally institutional VC investors shy away from very early-stage investments due to high cost of appraisal and monitoring and long timeframes that are out of the proportion with expected return. In order to catalyze the supply of early stage VC, governments have set up their own venture capital funds of funds but these are often seen as inappropriate due to political interfering, and lack of investment skills of bureaucrats. As a remedy, a capital participation approach is currently pursued by many governments. Tax incentives, e.g., angel investment tax credits, are another form to strengthen risk capital funding and work in tandem with VC incentives, especially at seed and start-up stages of company growth.

Also alternative-finance private initiatives through on-line crowd-funding are on the rise and might play an important role in filling the finance gap, in particular for start-ups and small but rapidly growing firms. So far, governments stayed on the sidelines not intervening in this market. However, increasingly more views call for government support of the market for alternative finance - not to stifle it but to help it thrive, preserve and protect.

Evolution of an innovative firm The sources of financing for emerging innovative firms and likely the nature and design of policy instruments will change as they pass through stages of company growth.1 Generally, the growth of firms and evolving financing needs would consist of four stages (see Chart 1).

1 Bank of England, The Financing of Technology Based Small Firms, London, Bank of England, 1996.

Chart 1: Financial instruments and different life-cycle stages

Seed stage: Inventor develops the idea and conducts initial research to scope out the technical and commercial viability of the idea. At this stage, the economic potential of the idea and any investment towards its realization are characterized by great uncertainty. Typically, the financial sources will be private and largely composed of the inventor and her family or friends’ own resources. It is also possible that an independent business angel (i.e., an individual who possesses significant own capital and private investment experience) may be interested to invest in this stage.

Start-up stage: At this stage the new company performs experimental R&D and the firm is recognized as an entity with a potential commercial future. The entry costs vary depending on the technology area in which the start-up firms operate. For example, for software the entry costs are relatively modest and the revenue comes on-stream fairly quickly. This is unlike in biopharma where the start-up may require significant capital investment, considerable original research and long lead time. While revenues are still not generated, this stage calls for significant inflow of capital from both angel capitalists (who are usually offering wealth of tacit knowledge in managing the startup) and from formal venture capital funds. Government support through direct assistance or tax incentives becomes very important as it augments the amount of cash available to revenue lacking new companies.

Early-growth stage: In this stage, the firm will likely have moved to prototype and technology demonstration but still will not have generated revenues. Nevertheless, a more reliable evaluation of the potential market for its product emerges, which should help attract investment from more diversified institutional sources. Patents or ownership of proprietary technology, along with a reliable cash flow, give the firm assets with a realizable market value. Venture capital, bank loans and government support in terms of direct assistance and/or tax incentives all play a critical role. Demand-creating government pre-commercial procurement of research results may also lend support for the firm.

7

Mature or sustained (or later) growth stage: In this stage, the company is growing steadily and has come to resemble other established corporations. At this point, early investors are likely looking to realize the profit from their investments. The follow-on investments play an important role and an IPO may happen at this stage. A key policy aspect in this stage of is the exit strategy – the point at which the venture capitalist can sell shares and release funds for new opportunities. And increasingly in this stage, strategic partnerships with established firms (with upfront payments, equity investments, future royalty streams, etc.) are displacing conventional sources of financing.

Policy intervention is required to guarantee access to capital and liquid assets. Smartly designed financial instruments play a positive role through the whole life cycle stages of companies. This includes not only seed or small entrepreneurial firms but may include larger-sized companies that require follow-on financing for their growth.

Modes of Public Support Financing innovative firms, particularly those at the pre-seed, seed and early expansion stage, is risky. First, this is because the returns to innovative activities are highly uncertain making it difficult for investors to assess risk. Second, entrepreneurs tend to know more about their company characteristics and performance than investors themselves - the so-called information asymmetry factor – causing investors to demand a risk premium or to abandon investing in start-up firms. Therefore, small entrepreneurial firms tend to have difficulty in accessing risk capital.

To ensure the supply of and demand for capital funds, government approaches include the following modes of public support:

• Through incentivizing traditional forms of finance: through subsidized (soft) loans, and loan and equity guarantees offered to banks and related institutional lenders.

• Through the tax system: chiefly through the tax relief for angel investors.2

• Through intervening in capital markets to establish seed and venture capital funds that co-invest in emerging companies along with the private equity funds.

• Through creating appropriate regulatory frameworks governing the access to and disposition of capital in the country, including protection for the evolving alternative forms of private financing.

This challenge paper is organized in sections according to the above specified modes.

INSTITUTIONAL LENDING: LOANS AND GUARANTEES

2 Angel investors are people who invest at an early stage in a company’s development when the risks are the greatest.

8

Institutional lending constitutes a major yet traditional source of funding for innovative investments. OECD data, based on the World Economic Forum’s Global Competitiveness Report, show that bank financing, stymied by the recent financial crisis, became more difficult to obtain between 2007 and 2012 (see Chart 2).

Chart 2: Ease of access to loans, 2007-08 and 2011-12

Scale from 1 to 7 from hardest to easiest, weighted averages

Source: OECD Science, Technology and Industry Scoreboard 2013, OECD, Paris, p. 200 http://dx.doi.org/10.1787/888932892974

Note: The ease of access to loans indicator measures how easy it is to obtain bank loans with only a good business plan and no collateral on a scale of one to seven; higher values suggest easier access.

Loans are one of the most common tools for access to finance for entrepreneurial companies during the entire technology life cycle. Loans need to be paid back (principal and interest). However, institutional investors such as banks and pension funds are generally unwilling to provide capital for companies that do not have collateral to secure their loans. This produces a major barrier to development of fledgling companies as the start-up or growth finance is hard to get.

There are a number of ways in which in which governments can intervene to correct this potential market failure including (a) under-writing some of the risk or uncertainty with guarantees, (b) improving the collateral situation of the firms seeking loans, or (c) seeking to improve the ability of the banks to assess and select potentially profitable projects. Governments can also offer reduced interest rate loans (subsidized or soft loans) or make loans repayable only if the project succeeds.

9

Box 1. A list of questions to address a policy challenge on loan financial instrument

How we can develop an appropriate guarantee scheme to improve the access of SMEs to loans?How we can improve the collateral of SMEs seeking loans?How we can improve the ability of banks to assess profitable projects?

Guarantees3

Guarantees largely serve as proxy for collateral. They transfer some (or all) of the risk of loss to a third party. In the case of a loan guarantee, the loan guarantor repays (some or all of) the loan to the bank if the borrowing firm becomes insolvent or defaults. The guarantor receives a guarantee or risk premium, usually financed or under-written by the public budget. Guarantees may operate horizontally and cover all sectors or be more focused and targeted. For example, equity (or loss-sharing) guarantees cover some of the risks associated with equity financing by venture capital. In some cases, guarantees can apply to portfolios rather than individual investments.

Guarantees can help to overcome some of the regulatory or prudential rules which limit the flow of finance to innovation. For example, in some cases pension funds and insurance companies are prohibited from investing in venture capital funds which are not guaranteed. Also bank regulations may make it more difficult for companies to receive bank loans without sufficient guarantees.

Entities that provide guarantees may share risks (in turn) via financial instruments called counter guarantees. Rather like re-insurance, the provider of a counter guarantee accepts a specified proportion of the risk from the guarantee originator, and receives a portion of the guarantee fee. The European Investment Fund has acted as a provider of counter guarantees to national and regional guarantee programmes and some Member States have counter-guarantee schemes. A number of guarantee schemes (both for loans and equity) exist or have been tried in Member States and an indicative list is given in the annex.

Improving collateral Governments have been increasingly looking for innovative ways to offer guarantees. The facility to exploit R&D tax credits is a way to improve the collateral position of an innovative company that seeks loan. For example, in 2010 Canada’s Export Development Corporation (EDC) introduced a program providing guarantees on loans to finance the company’s federal and provincial R&D Tax Credits. 4 EDC can provide a partial guarantee to banks that are willing to provide loans using the R&D tax credit refund as collateral. The guaranteed amount is typically 75 per cent of the loan the bank provides to company. Higher guarantee coverage is possible for small loans and when the company is making investments outside of Canada.

3 This section is based on Richard A. Cawley, The Challenge of Financing Innovative Investments – the Role of Banks, mimeo, unpublished,

4 Export Development Corporation, www.edc.ca10

ChallengesAs reforms to the banking and financing system in the wake of the financial crisis, such as banks’ increased capital requirements, may have reduced traditional investors’ appetite for risk, governments step in to stimulate access to traditional forms of finance for innovative companies.5 Typically, governments would offer loan guarantee scheme that gives collateral to SMEs in order to secure loans (see Table 1). There are challenges in the design and implementation of the guarantee schemes that call for the prudent proceeding by government.

Need for understanding of the market for guarantees, including the entrepreneurs and lenders

Designing a guarantee scheme requests a complex understanding of the market, especially weaknesses or gaps in the access to finance for innovative companies. Countries have to be familiar with absorption capacity or demand for loans by entrepreneurs on the one side, and the ability of banks and other private lending institutions to assess the risks of lending, on the other side. Policies that foster the recognition of opportunities on both sides such as awareness building among entrepreneurs of the availability of the instrument and educational training on how to assess the economic viability of the entrepreneurial company by banks and other lenders could be a way to help this traditional form of innovation financing gain its momentum.

Need for setting up an effective governance systemThe decision making should rather be independent of the government. One way to achieve it is through independent (not-politically selected) supervisory board. The board, however, should have appropriate skills to effectively assess and select all determinants in awarding the loan support.

Need for timely delivery of a loan/guaranteeThe decision concerning the loan should be made in a just-in-time fashion and take preferably no longer than one month. There are countries which experience close to one month timeframe (the United Kingdom) but in other countries (e.g., Slovenia) the waiting time can be more than five months.

5 OECD Science, Technology and Industry Outlook 2014, OECD, Paris, p. 17411

Need for setting an appropriate service feesCompanies that wish to obtain loan guarantee are usually obliged to pay a fee calculated on the outstanding loan amount. The fee covers administrative costs and also the guarantee. Governments have to pay attention that this fee does not became an undue financial burden on the firm, preventing the take-up of loans.

Need for fit into an overall policy mix of instruments (complementarity)The impact on social and economic development, including well-being of regions, is the most important goal for all governments. The success of the guarantee scheme can be linked to the success of an R&D grant scheme and thus the guarantee loan can be complementary to a R&D grant. In this way, structural funds would be better exploited, and for example environmental, societal challenges, and needs of less developed regions, etc. better addressed.6 Box2. A list of questions to address a policy challenge on guarantee financial instrument

Do we have an effective and politically independent governance system?Is the decision made on guarantees in a just in time fashion?Is the fee effectively calculated and is not a big burden to SMEs?How we could better exploit structural funds? Do we have any complementarity with successful R&D schemes?

6 A good example is Luxembourg ,Societe Nationale de Credit et d’Investissement

12

Table 1: Guarantee schemes: country examples

Equity Guarantee Schemes Loan Guarantee Schemes

Austria: FGG (Finanzierungsguarantee Gesellschaft)FFG supports R&D projects of companies of all industries and sizes through its general programme ("Basisprogramm"). Technology innovation projects of niche market leaders resident in Austria as well as the expansion of existing company R&D headquarters located in Austria are supported. FFG funding through these instruments consists of a mixture of loans, grants, and guarantees.7

Germany: BTU Programme (Beteiligungskapital fur kleine Technologieunternehmen) with its KfW and tbg variants.KfW is Germany's leading financier of SMEs. It provides long-term investment loans as well as working capital loans for enterprises. As a general rule, KfW grants its loans through regular banks, and to make it easier for the bank to approve the loan, KfW also assumes the bank's risk in some cases.8

France: SOFARIS (Technology Development Fund)Initially restricted to firms active in the manufacturing and business services industries. In 1995 the program was increased and new industries (construction, retail and wholesale trade, transportation, hotels and restaurants, and personal services) became eligible. SOFARIS firms experience higher employment growth. At the industry level, the availability of loan guarantees has no impact on the overall number of firms created, but makes the average new venture larger, both in terms of assets and employment. At the firm level, a loan guarantee helps newly created firms grow faster9

Germany: KfW European Recovery ProgrammeFinland: Finnevera Loan Guarantee SchemeFinnvera provides banking and loan/guarantees services for companies seeking to grow and internationalize. Its affiliates—Veraventure (funds), Seed Fund Vera (direct investments)10 Microloans and Loans for women entrepreneurs are also one of the financial product. According to Erawatch 17.036 jobs created, self-employed and startups.United Kingdom: UK Small Business Loan Guarantee Scheme11

The scheme guarantees 75% of loans from £5k to £250k over 2 to 10 years with staged repayments and the possibility of repayment holidays - most useful over tricky cash flow periods. The cost of the guarantee is two per cent per year on the outstanding amount of the loan. Results: employment and sales growth, businesses are generally younger than other businesses. The scheme appears to be very cost effective, in terms of the net economic benefits. 12

TAX CREDITS FOR INDIVIDUAL INVESTORS (BUSINESS ANGELS)

Traditionally, the mechanisms addressing the funding constraints for small companies have pertained to back-end of innovation financing through the tax

7 RIO Country Report 2015, first draft8 https://www.kfw.de/inlandsfoerderung/Unternehmen/Gr%C3%BCnden-Erweitern/index-

2.html9 Claire Lelarge, David Sraer, David Thesmar, Entrepreneurship and Credit Constraints:

Evidence from a French Loan Guarantee Program, May 201010 RIO Country Report 2015, first draft11 http://british-business-bank.co.uk/market-failures-and-how-we-address-them/enterprise-

finance-guarantee/understanding-enterprise-finance-guarantee/12 https:// www .gov.uk/government/uploads/system/uploads/attachment_data/file/85761/13-600-

economic-evaluation-of-the-efg-scheme.pdf 13

treatment of capital gains. The gains are earned (and taxed) provided there is appreciation in the value of an investment asset upon its disposition. Typically, capital gains tax incentives encompass tax exemption or reduction, capital gains rollover and loss offset.

As a front-end (before the outcome) form of innovation financing, tax credits for risky investments represent a group of non-traditional incentives. They are a relatively new instrument13 and have been used at the national level chiefly in Europe. They largely target an individual investor. They all aim at improving access to finance for small emerging companies covering virtually all phases of company growth from start-up to later-stage to established larger-sized companies.

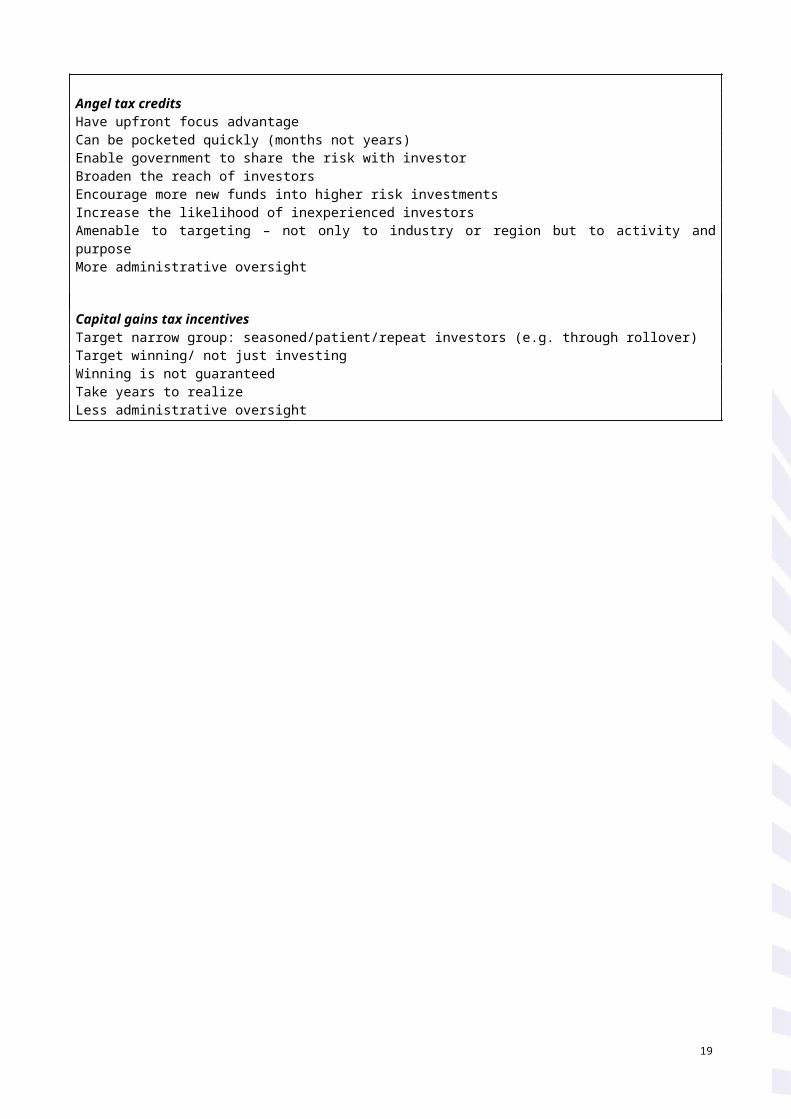

Key considerationsThe front-end focus and ability to target the desired population of investors are the key advantages of angel tax credits, especially when compared with the more traditional capital gains tax incentives. However, an angel tax credit may attract inexperienced or novice investors, making the scheme less efficient, which is a risk in itself. 14

Front-end In innovation, there are a few winners but many investors are required to make wins happen. Tax credits as an upfront incentive are best suited to attract new angel investors and create winning projects. In contrast, capital gains tax incentives are insufficient for innovation financing. They are back-end and reward winners only. In weighting the rationale for angel investments, ex-post type of incentives have little incremental effect. With risky investments, winning is not guaranteed.

Quality of investorA tax credit carries a strong psychological incentive to the investor, particularly to those less sophisticated, that there will be some quick return on the investment in terms of income tax savings generated by the credit.15 Thus tax credits have the potential of reaching broadest possible base of investors - doctors, lawyers, dentists, executives, etc. Some of these will be knowledgeable investors but some will be novices. Professional angels differ from novice investors in that they are better diversified, more patient and capable to offer advice and active involvement in running the business.

TargetingWhile designing the incentive, the question is whether and how to target the tax incentive to professional angel investors (repeat investors) or to keep its reach as broad as possible. If it is believed that a tax credit will not make angels out of non-angels, it should target repeat investors. 13 Most have been for less than 20 years in effect, unlike R&D tax credits.14 A remedy is a business angels network (BAN). Usually, BANs are very cautious who to invite into the group,

and only trustful and reliable investors are welcome. BANs have a clear plan/vision how to follow investees. However, a universal reach of the tax credit might still attract inferior investors.

15 This is important, as a tax credit is can be received in 12 months while capital gain may take 5-25 years to realize.

14

For government, angel tax credits offer good targeting opportunity to those types of companies and purposes (e.g., product development, marketing, training etc.) the government intends to support. The question is to what extent. Too much targeting may be seen as micro-managing by government resulting in an increased cost of compliance that may diminish the take up of the incentive. That is likely not what entrepreneurs and angels want. Start-ups want simple, timely and certain access to the funds generated by the tax credit. Angels want simple, timely and certain access to the tax credits they are entitled to. But too much targeting may discourage both investors and entrepreneurs from using the incentive. A balance needs to be drawn as to what level of targeting is appropriate and what is not.

Key differences

Angel tax creditsHave upfront focus advantageCan be pocketed quickly (months not years)Enable government to share the risk with investorBroaden the reach of investorsEncourage more new funds into higher risk investmentsIncrease the likelihood of inexperienced investorsAmenable to targeting – not only to industry or region but to activity and purposeMore administrative oversight

Capital gains tax incentivesTarget narrow group: seasoned/patient/repeat investors (e.g. through rollover)Target winning/ not just investingWinning is not guaranteedTake years to realizeLess administrative oversight

15

Country examplesAngel investor tax credits exist in several European countries. In North America, these incentives operate only at a regional level in several states in the United States and in a few provinces in Canada.

United KingdomThe United Kingdom operates presumably the most advanced set of programs of tax incentives for individual investors. There are two such tax programs at the national level: the Enterprise Investment Scheme (EIS) and a Seed Enterprise Investment Scheme (SEIS).

The EIS is designed for larger individual investments in advanced early to late stages of development. It allows a credit from personal income tax and full capital gains tax exemption upon the disposition of property. As of April 2012, the EIS has been reformed by increasing the rate of income tax relief to 30 per cent from 20 per cent and the size of recipient company from 50 to 250 full time employees. The limit for investment that a company can raise increased from £2 million to £10 million, and the individual investor limit doubled to £1 million per annum.16

Although a strengthened policy instrument, with the new changes, a possible adverse effect is that very small, high-risk investments no longer have the EIS advantage over their bigger competitors from a fundraising perspective. It is plausible that funding from private individuals may transfer from small to medium-sized enterprises, thereby defeating a key objective of EIS – stimulation of small company investment. To mitigate this situation, a new investment incentive for start-ups has been introduced - the Seed Enterprise Investment Scheme (SEIS).

The SEIS incentive is designed to support very small entrepreneurial companies. The scheme targets small investments into seed and early start-up companies. The scheme provides a higher (50 per cent) rate of income tax relief for individual investors. SEIS investors can invest £100,000 in a single tax year and the amount can be spread over a number of companies. The recipient company must have fewer than 25 employees, be no more than two years old and must have assets of less than £200,000. The company can raise no more than £150,000 in total via SEIS investment. Notably, investors cannot control the company as their stake cannot exceed 30 per cent of the company’s share value.17

The EIS was evaluated twice (in 2003 and 2008) with regard to its impact on additional financing and overall cost effectiveness. In both cases, the evaluation was positive, especially for capacity building in recipient companies, although the studies concede that these effects remain small. More than half of the funds invested would not have been committed in the absence of the

16 http://www.hmrc.gov.uk/eis/index.htm17 SEIS Background, http://www.hmrc.gov.uk/seedeis/index.htm

16

scheme. There were also positive spillover effects into the wider economy and any negative internal and external effects appeared to be moderate.18

Other EU countriesIn Ireland, there are tax incentives for private individuals who invest in private equity and venture capital funds through the Business Expansion Scheme (BES). It allows individual investors to obtain income tax relief on investments in each tax year. Companies can receive up to EUR 2 million of BES investment; however, no more than EUR 1.5 million can be raised in one year. An individual may obtain tax relief on investments up to a maximum of EUR 150,000 per annum under BES. Where an investor cannot obtain relief on all of the investments in a year of assessment, the unrelieved amount can be carried forward to the following years, subject to the normal limits. Non-Irish resident investors are also exempt from Irish income tax.

In France, business angels benefit from a tax credit of 22 per cent (in 2010 ) of the amount invested with the limit of EUR 50,000 . The investment must be held for at least 5 years and the company must be an SME.

Finland has established a temporary (2013-15) tax incentive for business angels. The incentive has been utilized very little so far. A challenge is keeping administrative burden light enough in order to make the incentive attractive for investors. An evaluation is on-going and will be available in 2015.

ChallengesOverall, tax credits appear to be more convenient than capital gains tax treatment to obtain seed finance just because they act quickly and target broader spectrum of risky investments and investors. An important question is the cost of running the tax credit as a national program. What costs in terms of tax expenditure and administrative oversight and compliance will it entail? Regarding oversight the cost will depend on how interventionist the government wants to be. In any case, such cost will likely be greater than the cost of administering capital gains tax incentives, which do not require any administrative apparatus.

18 NIC BOYNS, MARK COX, ROD SPIRES AND ALAN HUGHES, RESEARCH INTO THE ENTERPRISE INVESTMENT SCHEME AND VENTURE CAPITAL TRUSTS: SUMMARY OF THE REPORT, PUBLIC AND CORPORATE ECONOMIC CONSULTANTS, PACEC, CAMBRIDGE, APRIL 2003; SEE ALSO COWLING M, BATES P, JAGGER N, MURRAY G (SOBE, UNIVERSITY OF EXETER), STUDY OF THE IMPACT OF ENTERPRISE INVESTMENT SCHEME (EIS) AND VENTURE CAPITAL TRUSTS (VCT) ON COMPANY PERFORMANCE, RESEARCH REPORT HMRC 44, HM REVENUE & CUSTOMS, MAY 2008

17

A broader question, though, remains: Is the program really capable of bridging the financing gap for the early start-up companies and at what cost? Will the rate of return on government investment in tax credit be socially justified? Authorities pondering the introduction of angel tax credits remain ill-equipped as there is scarcity of informed evaluations of direct investment tax credit schemes largely because the programs in existence are relatively new. Still, the angel tax credit could be a preferred incentive mechanism because it is both front-end and targetable to desired policy objectives. As experienced, wealthy and informal investors, business angels tend to invest in early and riskier stages and play a crucial role in filling the financing gap between the early and the later growth stages.19 See, Table 2 for features summary.

Table 2: Tax incentives for investorsStrengths Opportunities

Front-end incentive as opposed to back-end

(capital gains tax exemption) Risk sharing with government

has a positive psychological effect

Greater access to tax credits for everyone who wants to invest

Can be targeted to desired investors, industries and activities

Better ability to address the ‘equity gap’ encountered by small, high-risk companies

Improvement in the after-tax rate of return for investors, thereby encouraging them to invest more in the companies covered by the schemes

Greater competitiveness of small firms

Weaknesses Threats

May attract inexperienced investors

May attract those who would invest anyway in the absence of the incentive (deadweight cost)

High compliance costs for businesses and possibly investors due to complex rules and regulations

May involve more government scrutiny

A too generous design may open the floodgates for investment, well beyond government cost expectations

Box 3. A list of questions to address a policy challenge on tax incentive financial instrument

Whether and how to target the tax incentive to professional angel investors (repeat investors) or to keep its reach as broad as possible?To what extent of support do we target (e.g., product development, marketing, training etc.)?What costs in terms of tax expenditure and administrative oversight and compliance will it entail?Is the program really capable of bridging the financing gap for the early start-up companies and at what cost?

19 OECD Science, Technology and Industry Outlook 2014, OECD, Paris, p. 17418

Will the rate of return on government investment in tax credit be socially justified?EQUITY INCENTIVES

Most government interventions in venture capital markets date back to 2000-2001, around the time of the technology boom-and-bust. More recently, stemming from the tightening of credit markets as a result of the recent global recession, many governments have introduced measures to increase the supply of venture capital and risk financing available to innovative SMEs. Beyond support for the supply of risk capital, governments support entrepreneurs and early-stage firms through business development programs such as incubators and accelerators that improve entrepreneur investment readiness.

Venture capital (VC) is a major source of funding for new technology-based firms. It plays an important role in promoting innovation and is one of the key determinants of entrepreneurship. VC has strengthened in the United States and Canada since 2009, the crisis year for VC funding. The same cannot be said about many EU countries, which have had difficulty to return to their previous levels of VC funding (see Table 3).

Table 3: Venture Capital investment: G7 and selected European countries (percentage of GDP)

Country 2008 2009 2012

United States 0.122 0.088 0.171

Canada 0.083 0.031 0.080

United Kingdom 0.207 0.049 0.038

France 0.091 0.051 0.027

Japan 0.007* 0.026

Germany 0.048 0.030 0.020

Italy 0.025 0.004 0.005

Denmark 0.298 0.055 0.033

Finland 0.225 0.069 0.041

Sweden 0.211 0.080 0.054

Ireland 0.152 0.070 0.054

Netherlands 0.148 0.034 0.029

Spain 0.095 0.017 0.011

Source: OECD Science, Technology and Industry Scoreboard 2013, http://dx.doi.org/10.1787/888932892993 (for 2012 data); and Scoreboard 2011, http://dx.doi.org/10.1787/888932487362 (for 2009 data); and Scoreboard 2009 (for 2008 data); * 2006

19

In general, the lack of collateral and corporate history, and high costs of valuation and monitoring limit the availability of conventional funding to early-stage companies. Availability of venture capital from private funds is also limited as returns from early stage VC are high-risk and generally have been poor.20 Many European countries use public sector funds to leverage private financing in order to reduce this financing gap. Policies for promoting availability of risk capital to innovative SMEs are concentrated on early stages of the financing of the firm. Some equity incentives, however, tend to cover a spectrum of company growth from seed stage to early phase to late stage (e.g., young innovative company fund – JITU21 – in Austria, France Investment in France, and Enterprise Capital Funds – in the United Kingdom.) Frequently, there are different fund measures to address a different stage of company development. For example, in Germany under umbrella of Technology Venture Capital Programmes (VCP), there are five funds that deliver for different points in company growth cycle. Similarly, in Netherlands’ TechnoPartner family of programs there are different programs for different company growth stages. Measures are typically of generic type, available universally to all eligible industries. (See Annex 1 for overview of early-stage co-investment instruments.)

Government-sponsored fundsThe capital participation approach is now adopted by many governments.22 Types of initiatives include: Government venture capital funds (GOVCs) that are owned by

government and are typically associated with development banks or they may also be directly affiliated with government departments. GOVCs obtain all of their funding from government or, in some cases, at the same time look for a private capital on a deal basis.

Government supported venture capital funds (GSVCs) get financial support from government programs. GSVC obtain some of their funding from government and the remainder from private sources (co-investments funds). 23

(For more detailed comparison of these types of government involvement see Appendix 1.)

Co-investment funds based on capital participation approach represent a public-private partnership between the government and private sector funds, including venture capital organizations and business angels for investments chiefly in seed and early-stage companies. (See Table 4 for a profile of the generic fund.)

20 Colin Mason, “A Critical Review: Public Policy Support for the Informal Venture Capital Market in Europe” University of Strathclyde, Glasgow, International Small Business Journal

21 Förderung von Gründung und Aufbau junger innovativer technologieorientierte Unternehmen (JITU), by AWS (Austria Wirtschaftsservice)

22 An option for governments to run their own venture capital funds has been largely rejected due to the possibility of political interfering and lack of investment skills of bureaucrats.

23 See, Annex1: Early stage co-investment instruments overview by countries20

Table 4: A profile of a generic co-investment fund Type Public-private partnership

Size €10 million to €20 million

Life 12 – 15 years (5 years for investment and at least 7 for disinvestment)

Sources of public funding Can be 15% (national)/85% (EU) but also can be 100% national

Private/public ratioPari passu (50:50), in some case upside rewards more in favour of private investors

Average investmentSeed: (€50000-€150000), start-up: (€150000-€300000), expansion up to €3 million

Sector focus Universal: all sectors mainly

Location Regional investments mainly

These funds need to be attractive enough in terms of risk-reward profile for the uptake by private investors. In general, there is skepticism regarding the role of government in VC finance. Critical reviews point out that, in some cases, the operating costs of these funds are too high, and funds are further constrained by having an upper limit on how much they can invest in any business.24 This prevents such funds from providing follow-on funding. Critics also doubt whether governments can improve upon private sector VC activity and many fear that government intervention in VC markets might be associated with problems arising from political pressures, rent-seeking, and general bureaucratic inefficiency. On the other hand, there are some positive news from government intervention. Enterprises receiving mixed private and government VC funding received significantly more investment than enterprises receiving private support only. Mixed funding is also associated with a higher probability of a successful exit.25

Evaluations are few but some show that these public-private funds work well. For example, the overall impact of the UK Innovation Investment Fund (UKIIF) on business development appears greater than its investment level (turnover, employment over three-fold in three years). All surveyed recipient businesses are currently developing highly innovative products/services which are likely to benefit the United Kingdom economy and half have products that are potential global leaders, whilst others expect them to become so. Also in Germany, High-tech Gründerfonds (HTGH) resulted in several success stories in terms of good investments in companies and ERP-Startfonds has financed roughly 470 technology-intensive firms since its creation. In Denmark, the fund’s investments led to short-term direct effects of €270m increase in GDP and the creation of 3,000 jobs. In Ireland, the National Policy Statement on Entrepreneurship noted that €55 million in funding was provided to 186 enterprises through the Seed and Venture Capital Fund in 2013.

24 Colin Mason, “A Critical Review.” 25 James A. Brander, Qianqian Du and Thomas Hellmann, The Effects of Government-Sponsored Venture Capital:

International Evidence, March 201421

Challenges in design, implementation and evaluationNeed for capacity building for entrepreneursMany businesses seeking finance are not “investment ready”. A lack of profitable investment frequently occurs as a bottleneck especially in less developed countries. Capacity building is needed that is beyond the business plan for start-up companies. For entrepreneurs, it can help them to articulate their demand for risk funding. Governments could set a certain percentage of the fund for capacity building or coaching activities relating to market analysis and access, technology validation, etc.

Need for capacity building for investorsInvestment education (e.g., training programs) is part of the critical infrastructure for effective capital markets. It can provide investors with the specialist knowledge and skills that they require to invest successfully. For entrepreneurs, it can help them to articulate their demand for risk funding. Future capacity-building efforts need to include the training of intermediaries, such as accountants, lawyers, bankers, consultants, and business incubator managers who can be a significant source of financial advice for entrepreneurs. Government could have a lead role in facilitating such activity. For example, government could set a certain percentage of the fund for capacity building.

Relevant questions: • Do governments plan any financial support for boosting private

investors in the form of capacity building? • Do governments plan any financial support for the activities of

business angel networks (BANs) as for scouting, investment selection, due diligence, intellectual property, etc?

Need for different co- investment vehiclesGovernments are now establishing co-investment funds that invest alongside angel groups to enable them to make larger and follow-on investments. These funds differ in terms of how they operate. At one extreme are passive funds, such as the Scottish Co-Investment Fund, which follows the lead of its private sector partners who have been approved to invest under the scheme. It does not undertake its own due diligence and plays no part in the investment. Other co-investment funds are more actively managed, inviting investors to bring deals to them (or may approve deals from particular sources, such as business angel networks), but make their own investment decision and may invest on different terms and conditions to those of the angel group. For example, London Seed Capital co-invests with the London Business Angels Network, and the Great Eastern Investment Forum (GEIF) has a co-investment fund that only invests in companies that receive investments from GEIF angels.

22

Need for correct proportion of profit distributionObtaining venture capital is substantially different from raising debt or receiving a loan. Lenders have a legal right to interest on a loan and repayment of the capital irrespective of the success or failure of a business. Venture capital is invested in exchange for an equity stake in the business. The return of the venture capitalist as a shareholder depends on the growth and profitability of the business. This return is generally earned when the venture capitalist "exits" by selling his shareholdings when the business is sold to another owner. Venture capitalists are typically very selective in deciding what to invest in; as a result, funds are looking for the rare qualities such as innovative technology, potential for rapid growth, a well-developed business model, and an impressive management team. Of these qualities, funds are most interested in ventures with exceptionally high growth potential, as only such opportunities are likely capable of providing financial returns and a successful exit within the required time frame (typically 3–7 years) that venture capitalists expect. This is in contrast with government priorities. Seeking and responding to voters, governments are more in favour of broader goals, notably securing and creating new jobs and regional economic development.

Need for measurement of impactThe lack of data on angel investing, in particular, means that there is very little evidence on the impact of these forms of intervention. Government could again play a lead role in this area by investing in development of methodologies, which can accurately measure investment trends in the early-stage venture capital market, and specifically angel investment activity, so that the need for public sector intervention can be demonstrated and the impact of such interventions can be measured.

Questions when designing and implementing VC co-investment instruments

Below are a few important questions that have to be answered when designing a VC co-investment instrument.

How to set up a governance system?Majority of equity funds are managed by a private company. A private management company is responsible for all activities: deal sourcing, due diligence, investment, monitoring and divestment and gets a fee for their work. In some cases, the funds are managed by a European Investment Fund (EIF) manager. This can be of particular added value in the less developed countries, where there is a need for capacity-building initiatives and transfer of know-how between local institutions and EIF.26 There is also a possibility to involve European Angels Fund (EAF) that enters long-term contractual relationships with business angels.27

26 There are seven currently signed National Holding Fund agreements (in Greece, Romania, Slovakia, Lithuania, Cyprus, Bulgaria and Malta) and six Regional Holding Fund agreements (in France Languedoc Roussillon, Provence-Alpes-Cote d’Azur and Italy – Campania, Calabria and Sicily).

27 EAF grants a predefined amount of equity for co-investments (up to 5 million euro) upfront to each fund for future investments. Decision on investment is taken by a fund, investment on pari passu (50:50) basis.

23

What is the ownership structure of the fund?

Bottom line is avoiding political interfering.

Who will manage the fund: a private manager or leave management to EIF?

If a private manager: does she have skills? Does she know business, market, how to attract private capital, and evaluate investments, etc.? If an EIF manager: pros include better access to knowledge and cons likely a higher management cost.

How to design the financial instrument for regional environments?

Setting up a new financial instrument often requires a delicate balancing act between achieving desired local objectives such as creation of employment, an often politically motivated goal, and addressing the impact of the instrument on social well-being and sustainability of knowledge intensive companies in the region.

Other relevant questions may include the following:• Do we have a smart specialization strategy, where socio-economic,

entrepreneurial dimension and ecosystem are clearly described? • Is the new financial instrument a part of the national operational

programme? • Is there any ex ante assessment? • Why to involve private sector? • What type of companies to support and why? • What should be the size of the equity fund? • How to ensure a seamless exit for investors?• What about the national legislation to set up an equity fund: Is it

already there or new regulation is needed? 28

28 For example, in Croatia it is considered difficult even to establish a co-investment fund due to the law, which is very complicated.

24

Box4. A list of questions to address a policy challenge on equity incentives financial instrumentHow to set up a governance system?What is the ownership structure of the fund?Who will manage the fund: a private manager or leave management to EIF?How to design the financial instrument for regional environments?Do we plan any complementarity with other instruments as grants and tax incentives?Do we plan any combination also with coaching, mentoring?Do we plan any financial support for entrepreneurs in the form of capacity building?Do we plan any financial support for the activities of business angel networks ?Do we like to play and active or passive role in making decision on investments?Do we have enough willingness to take risk?How do we intent to distribute the profit?Do we plan any resources for impact measurement?Other relevant questions as:

Do we have a smart specialization strategy, where socio-economic, entrepreneurial dimension and ecosystem are clearly described?

Is the new financial instrument a part of the national operational programme? Is there any ex ante assessment? Why to involve private sector? What type of companies to support and why? What should be the size of the equity fund? How to ensure a seamless exit for investors? What about the national legislation to set up an equity fund: Is it already there or

new regulation is needed?

ALTERNATIVE FINANCE

Alternative financing, often identified with crowd-funding, can be defined as an open appeal to the general public by the private on-line based initiators to raise funds with a specific objective. The concept itself is far from new and has been embedded in human culture since its early days. Historically, people have been raising money to achieve certain objectives for the common good. Numerous examples of charitable donation campaigns can be found in early history, however, the term ‘crowd-funding’ typically denotes raising funds through the use of the Internet. The emergence of online crowd-funding dates back to more than a decade ago, but the use of a dedicated platform for several crowd-funding campaigns has only gained traction in recent years.

Since the global financial crisis, alternative finance – which includes financial instruments and distributive channels that emerge outside of the traditional financial system – has thrived in the United States, the United Kingdom and continental Europe.29 In particular, online alternative finance, from equity-based crowd-funding to peer-to-peer business lending, and from reward-based crowd-funding to debt-based securities, is supplying credit to SMEs, providing

29 Benchmarking analysis of 255 web based platforms points to a significant growth of the European alternative finance market - by 144 per cent last year - from €1,211 million in 2013 to €2,957 million in 2014. The largest online alternative finance markets are in the United Kingdom, France, Germany, Sweden, Netherlands and Spain. For more information, see Robert Wardrop, Bryan Zhang, Raghavendra Rau and Mia Gray, Moving Mainstream: The European Alternative Finance Benchmarking Report, University of Cambridge, February 2015

25

venture capital to start-ups, offering more diverse and transparent ways for consumers to invest or borrow money, fostering innovation, generating jobs and funding worthwhile social causes.

The current crowd-funding market appears to be sufficiently self-regulated. Up to now, no systemic evidence of abuse or fraud on the crowd-funding platforms has emerged. This is not to say that governments do not have a role to play, not as interveners but as supporters of the fledgling market through appropriate regulations and protection of investors. Box5. A list of questions to address a policy challenge on alternative financial instrument

Do we plan any awareness raising on alternative financing?

Do we have an appropriate regulations for protection of private investors?

Do we plan any complementarity with mentoring and coaching schemes?

Appendix 1: Major characteristics of government-sponsored venture capital funds

Government-owned venture capital funds (GOVCs)

Government-supported venture capital funds (GSVCs)

Long and difficult procedures entering the private company ownership

Equity capital or financing is money raised by a business in exchange for a share of ownership in the company.

Co investment fund as a private company easy enter into business.

Only public money Public and private money from business angels or other investors who are usually looking also for other trusted co-investors out of the fund

Lack of knowledge on industries or technologies

Typically invest in ventures involved in industries or technologies with which they are personally familiar

The investment is made only by public money

Co-invest with trusted friends and business associates. In these situations, there is usually one influential lead investor (“archangel”) whose judgment is trusted by the rest of the group of angels.

Lack of skills on venture capital process (due diligence, investment, exit strategy), lack of business experience and skills

In co-investment funds, private investors in-charge seek to contribute their experience, knowledge and contacts to the benefit of their investee.

The whole risk is on government, collateral requested

Often take bigger risks or accept lower rewards when they are attracted to the non-financial characteristics of an entrepreneur’s proposal

26

Government-owned venture capital funds (GOVCs)

Government-supported venture capital funds (GSVCs)

High level of bureaucracy hinders fast decision on investment

Decision on investment is faster

Political lobbying possible Professionalism

Government priority is employment creation not innovation

Equity providers require a higher rate of return (ROI)

doi: 10.2777/194026

27