Equity Market Outlook Sep 2019

28

Equity Market Outlook September 2019

Transcript of Equity Market Outlook Sep 2019

Equity Market Outlook

September 2019

Equity market outlook

Global growth trends have weakened mainly due to US-China standoff. Recent central bank actions,Brexit deal and possible US-China dispute resolution could support growth

India’s twin deficits – Fiscal and Current account in comfort zone; provide space to boost growth

Domestic lead economic indicators continue to show weakness

Consumption demand remains weak; however recent turnaround in food inflation, unspent budgetsshould support rural led recovery

Financial sector seeing fresh round of challenges, credit environment appears weak overall

Inflation continues to remain benign; offers scope for further monetary easing

Government-led infra spending to pick up in second half of the year

Government now using fiscal and monetary tools to spur economy

Domestic economy is well-placed for earnings recovery led by sectors such as Financials andIndustrials; Consumer Discretionary may remain in slow track in the short term

Large-cap valuations at 37% premium to the long-term average remain a challenge; however,valuations of midcaps and small caps have corrected and on an adjusted PE basis now trade at a 19%discount versus long term average of 14% discount

2

Global Macro

50

60

70

80

90

100

110

Jan-

05N

ov-0

5Au

g-06

May

-07

Feb-

08N

ov-0

8Se

p-09

Jun-

10M

ar-1

1D

ec-1

1Se

p-12

Jun-

13Ap

r-14

Jan-

15O

ct-1

5Ju

l-16

Apr-1

7Ja

n-18

Nov

-18

Aug-

19

U.S

. Con

sum

er C

onfid

ence

Inde

x (3

MM

A) Highest in decade

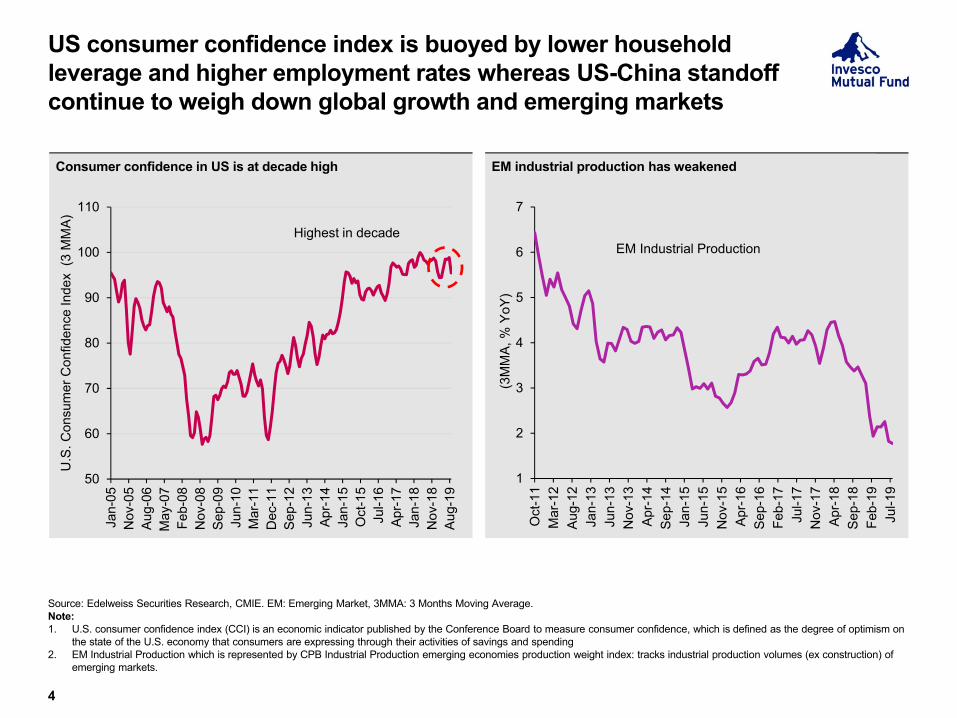

Consumer confidence in US is at decade high

1

2

3

4

5

6

7

Oct

-11

Mar

-12

Aug-

12Ja

n-13

Jun-

13N

ov-1

3Ap

r-14

Sep-

14Ja

n-15

Jun-

15N

ov-1

5Ap

r-16

Sep-

16Fe

b-17

Jul-1

7N

ov-1

7Ap

r-18

Sep-

18Fe

b-19

Jul-1

9

(3M

MA,

% Y

oY)

EM Industrial Production

EM industrial production has weakened

US consumer confidence index is buoyed by lower household leverage and higher employment rates whereas US-China standoff continue to weigh down global growth and emerging markets

4

Source: Edelweiss Securities Research, CMIE. EM: Emerging Market, 3MMA: 3 Months Moving Average.Note:1. U.S. consumer confidence index (CCI) is an economic indicator published by the Conference Board to measure consumer confidence, which is defined as the degree of optimism on

the state of the U.S. economy that consumers are expressing through their activities of savings and spending2. EM Industrial Production which is represented by CPB Industrial Production emerging economies production weight index: tracks industrial production volumes (ex construction) of

emerging markets.

18%

15%

18%

21%

24%

27%

Jan-

12

Oct

-12

Jun-

13

Mar

-14

Nov

-14

Jul-1

5

Apr-1

6

Dec

-16

Aug-

17

May

-18

Jan-

19

Sep-

19

Fede

ral R

eser

ve B

alan

ce S

heet

as

a %

of G

DP

1.56%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

Jan-

12

Dec

-12

Dec

-13

Nov

-14

Nov

-15

Nov

-16

Oct

-17

Oct

-18

Oct

-19

10 Y

ear G

-Sec

Yie

ld (%

)

Recent change of Fed stance on rates and balance sheet reduction imply easing liquidity

5

Source: Bloomberg.

Indian Macro

0%

3%

6%

9%

12%

15%

Mar

-00

Mar

-01

Mar

-02

Mar

-03

Mar

-04

Mar

-05

Mar

-06

Mar

-07

Mar

-08

Mar

-09

Mar

-10

Mar

-11

Mar

-12

Mar

-13

Mar

-14

Mar

-15

Mar

-16

Mar

-17

Mar

-18

Mar

-19

Mar

-20

% o

f GD

P

PSE BorrowingsCombined Fiscal Deficit (inc. off-budget items)Augmented (inc PSE Borrowings)

-1.99%

-8%

-6%

-4%

-2%

0%

2%

Q1

FY12

Q3

FY12

Q1

FY13

Q3

FY13

Q1

FY14

Q3

FY14

Q1

FY15

Q3

FY15

Q1

FY16

Q3

FY16

Q1

FY17

Q3

FY17

Q1

FY18

Q3

FY18

Q1

FY19

Q3

FY19

Q1

FY20

CAD as % of GDP CAD excl. gold as % of GDP

5.15%3.28%

1%

5%

9%

13%

Jan-

12

Aug-

12

Mar

-13

Oct

-13

May

-14

Dec

-14

Jul-1

5

Feb-

16

Sep-

16

Apr-1

7

Dec

-17

Jul-1

8

Feb-

19

Sep-

19

Repo CPI

3.08%

3.00%3.50%4.00%4.50%5.00%5.50%6.00%6.50%7.00%7.50%

Aug-

10

Mar

-11

Oct

-11

May

-12

Nov

-12

Jun-

13

Jan-

14

Jul-1

4

Feb-

15

Sep-

15

Apr-1

6

Oct

-16

May

-17

Dec

-17

Jun-

18

Jan-

19

Aug-

19

% o

f GD

P

Fiscal Deficit (12 months trailing) Augmented Fiscal Deficit

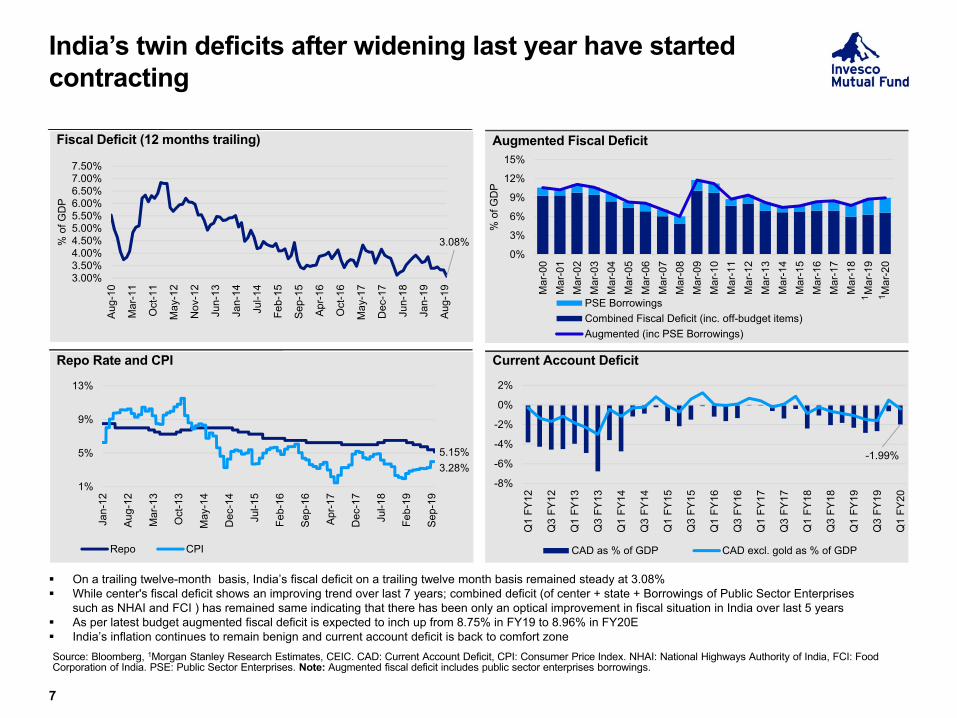

India’s twin deficits after widening last year have started contracting

7

Source: Bloomberg, 1Morgan Stanley Research Estimates, CEIC. CAD: Current Account Deficit, CPI: Consumer Price Index. NHAI: National Highways Authority of India, FCI: Food Corporation of India. PSE: Public Sector Enterprises. Note: Augmented fiscal deficit includes public sector enterprises borrowings.

Repo Rate and CPI Current Account Deficit

On a trailing twelve-month basis, India’s fiscal deficit on a trailing twelve month basis remained steady at 3.08% While center's fiscal deficit shows an improving trend over last 7 years; combined deficit (of center + state + Borrowings of Public Sector Enterprises

such as NHAI and FCI ) has remained same indicating that there has been only an optical improvement in fiscal situation in India over last 5 years As per latest budget augmented fiscal deficit is expected to inch up from 8.75% in FY19 to 8.96% in FY20E India’s inflation continues to remain benign and current account deficit is back to comfort zone

11

-38.71%-60%-40%-20%

0%20%40%60%80%

100%

Apr-1

0

Nov

-10

Jun-

11

Jan-

12

Aug-

12

Mar

-13

Oct

-13

May

-14

Dec

-14

Jul-1

5

Feb-

16

Sep-

16

Apr-1

7

Nov

-17

Jun-

18

Jan-

19

Aug-

19

9.92%0%5%

10%15%20%25%30%

Apr-1

0

Nov

-10

Jun-

11

Jan-

12

Aug-

12

Mar

-13

Oct

-13

May

-14

Dec

-14

Jul-1

5

Feb-

16

Sep-

16

Apr-1

7

Nov

-17

Jun-

18

Jan-

19

Aug-

19

-6.05%-40%

-20%

0%

20%

40%

60%

Apr-1

0O

ct-1

0M

ay-1

1N

ov-1

1Ju

n-12

Dec

-12

Jul-1

3Fe

b-14

Aug-

14M

ar-1

5O

ct-1

5Ap

r-16

Nov

-16

May

-17

Dec

-17

Jul-1

8Ja

n-19

Aug-

19

-8.70%-15%

-10%

-5%

0%

5%

10%

15%

Apr-1

0O

ct-1

0M

ay-1

1N

ov-1

1Ju

n-12

Dec

-12

Jul-1

3Fe

b-14

Aug-

14M

ar-1

5O

ct-1

5Ap

r-16

Nov

-16

May

-17

Dec

-17

Jul-1

8Ja

n-19

Aug-

19

Railway Freight Growth (%) Export Growth (%)

Lead indicators suggest weak trends

8Source: Kotak., Jefferies.

Commercial Vehicles (CV) Sales Growth (%) Credit Growth (%)

Lead indicators continue to suggest weak trends across the board Credit growth after last years revival has slow down to sub 10% Export growth continue to remain lackluster while freight remains muted with railway down 6% and ports up 3.5% YoY Commercial vehicles sales have slow down while electricity generation declined 0.3% YoY

11.10%

-7.50%

1.60%

25.50% 25.70%15.70%

2.90%

7.30%7.90%

3.00%

6.90%14.80%

4.90%

-14.80%-25%

-15%

-5%

5%

15%

25%

Mar

-07

Mar

-08

Mar

-09

Mar

-10

Mar

-11

Mar

-12

Mar

-13

Mar

-14

Mar

-15

Mar

-16

Mar

-17

Mar

-18

Mar

-19

Aug-

19

YoY(

%)

Two wheeler sales Average Growth

Average: 7.50%

-3.50%

0.60%

32.20%

19.80%11.30%

-1.70%

20.20%

-13.00%-10.50%

18.00%

22.10%

10.20%

-14.00%

Mar

-08

Mar

-09

Mar

-10

Mar

-11

Mar

-12

Mar

-13

Mar

-14

Mar

-15

Mar

-16

Mar

-17

Mar

-18

Mar

-19

Aug-

19

YoY(

%)

Tractor Domestic Sales growth Average Growth

Average: 7.05%

1.77%3.57%

-10%-5%0%5%

10%15%20%25%30%35%

Feb-

13

Sep-

13

Mar

-14

Sep-

14

Apr-1

5

Oct

-15

May

-16

Nov

-16

May

-17

Dec

-17

Jun-

18

Dec

-18

Jul-1

9

%

YoY(%) YoY(%), 3MMA

Domestic two wheeler sales

6.60% 6.60% 6.90%

2.50%

5.20%

8.00%

4.60%

FY14 FY15 FY16 FY17 FY 18 FY 19 1QFY20

YoY(

%)

Staples volume growth

Consumption – cyclical slowdown in last few months

9

Source: Bloomberg, Morgan Stanley, CEIC, Axis Capital. CPI: Consumer Price Index, 3 MMA: 3 months moving average. For consumer staple sector Britannia, Colgate, Dabur, Emami, GSK Consumers, Hindustan Unilever, Marico and Godrej Consumer Products have been taken and this is not exhaustive list. There are other companies operating in the same sector having different volume growth.

Air Passenger Traffic – Number of Passengers Flown Tractor sales growth

Tractor sales declined while both two wheelers and four wheeler sales continue to decelerate further. The slow down which started in H2FY19 will now start playing up in base and things could improve optically from hereon.

3.88%

3.06%

1.99%2.22%

2.46%

2.10%

1.70% 1.80%

2.50%

1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19 1Q20%

of p

revi

ous

year

adv

ance

s

10.28%9.91%

9.16%8.45%

8.01%7.64%

6.70%

5.80% 5.80%

1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19 1Q20

% o

f tot

al a

dvan

ces

Impaired asset as % of total advances Gross slippages outside stress pool as % of previous year advances

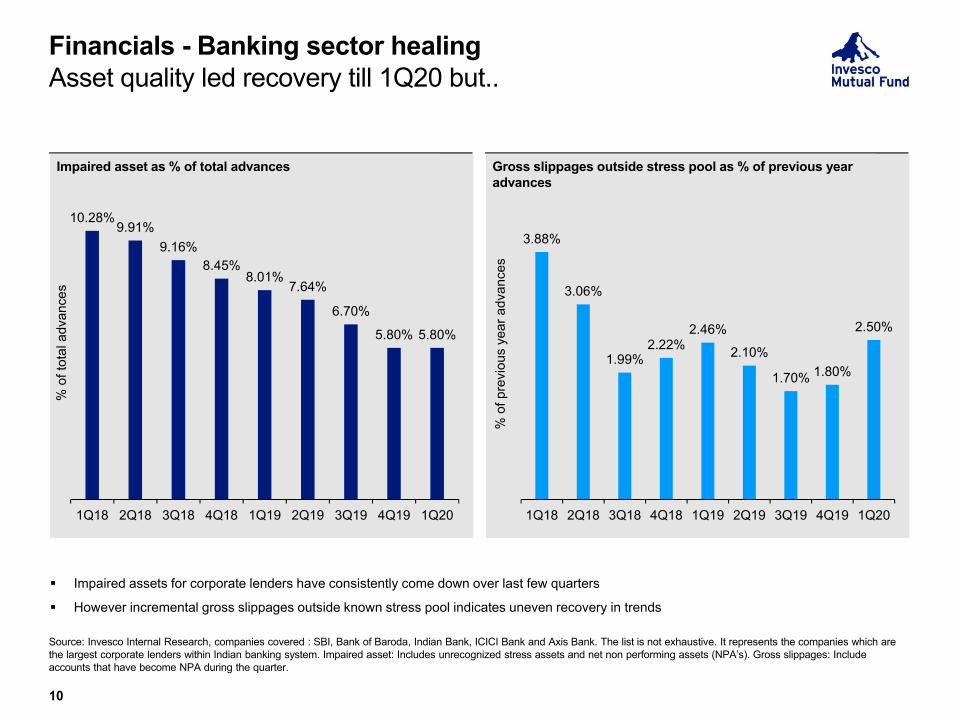

Financials - Banking sector healing Asset quality led recovery till 1Q20 but..

10

Source: Invesco Internal Research, companies covered : SBI, Bank of Baroda, Indian Bank, ICICI Bank and Axis Bank. The list is not exhaustive. It represents the companies which are the largest corporate lenders within Indian banking system. Impaired asset: Includes unrecognized stress assets and net non performing assets (NPA’s). Gross slippages: Include accounts that have become NPA during the quarter.

Impaired assets for corporate lenders have consistently come down over last few quarters

However incremental gross slippages outside known stress pool indicates uneven recovery in trends

3.49

%

2.48

%

0.67

%

0.89

% 2.94

%

1.33

%

0.82

%

1.33

%

2.08

%

0.72

%

0.63

% 3.31

%

5.11

%

1.96

%

1.62

% 5.63

%

1.84

%

2.60

% 6.06

%

25.3

8%

2010

-11

2011

-12

2012

-13

2013

-14

2014

-15

2015

-16

2016

-17

2017

-18

2018

-19

2019

-20

% o

f tot

al ra

ted

debt

Upgrades Downgrades

0%10%20%30%40%50%60%70%80%90%

100%

2010

-11

2011

-12

2012

-13

2013

-14

2014

-15

2015

-16

2016

-17

2017

-18

2018

-19

2019

-20

% o

f tot

al ra

ted

debt

Highest Safety (AAA) Other Investment GradeNon-Investment Grade

Upgrades v/s Downgrades of corporate debt securities

Asset Quality – Fresh round of Pain

11

Source: SEBI; combined data of all rating agencies. Note: Other investment grade includes securities with High Safety (AA), Adequate Safety (A) and Moderate Safety (BBB) ratings

The financial sector has struggled with fresh round of delinquencies, however, downgrades still higher than upgrades indicating increasing vigilance and residual pain ahead.

Ratings assigned for long-term corporate debt securities (maturity > 1 year)

(Apr

19

–Au

g 19

)

(Apr

19

–Au

g 19

)

5.50%

6.30%

7.10%

7.90%

8.70%

9.50%

10.30%

Apr-19 May-19 Jun-19 Jul-19 Aug-19 Sep-19

CP

rate

s (%

)

Chola Bajaj Fin IIFL EdelJM Fin PEL HDFC LIC HF

9% 13% 17%30%

20%10%

6%

18%21%

26%

25%

19%

FY 2014 FY 2015 FY 2016 FY 2017 FY 2018 FY 2019E

Syst

em lo

an g

row

th (%

)

HFCs NBFCs

NBFCs/HFCs – major drivers of system loan growth in recent years

14%11%

-4%Strong Parentage and

Long VintageStrong Parentage but

Low VintageAll othersTo

tal B

orro

win

gs fr

om S

ep-1

8 to

Ju

ne-1

9 (%

cha

nge)

Strong NBFCs continues to have access to markets

NBFC – Divergence between strong and weak

12

Source: RBI, Company data, Morgan Stanley Research, Credit Suisse. Strong Parentage and Long Vintage companies are: HDFC, PFC, REC, LICHF, BAJAJ Finance, SHTF, MMFS, Cholamandalam, Sundaram Finance, SCUF, Gruh Finance; Strong Parentage but Low Vintage companies are: L&T Finance, PNB Housing Finance, Piramal Capital Housing; All others companies are: IHFL, Edelweiss, IIFL Finance, Muthoot Finance, SREI Equipment, BHAFIN, JM Financial , Magma Fincorp, Manappuram, SREI Infra, Repco Home Finance, Indostar, MAS Financial, Aspire Home Finance, Muthoot Capital

Funding cost for strong NBFCs has started coming down

5

15

25

35

45

55

65

Jul-1

5

Oct

-15

Jan-

16

Apr-1

6

Jul-1

6

Oct

-16

Jan-

17

Apr-1

7

Jul-1

7

Oct

-17

Jan-

18

Apr-1

8

Jul-1

8

Oct

-18

Jan-

19

Apr-1

9

Jul-1

9

Oct

-19

Spre

ads

(bas

is p

oint

s)

NBFC spreads over similar rated corporates normalizing

5.50

5.70

5.90

6.10

6.30

6.50

6.70

6.90

7.10

7.30

7.50

8.50%

9.00%

9.50%

10.00%

10.50%

11.00%

Jan-

18M

ar-1

8Ap

r-18

May

-18

May

-18

Jun-

18Ju

l-18

Aug-

18Se

p-18

Oct

-18

Nov

-18

Dec

-18

Jan-

19Fe

b-19

Mar

-19

Apr-1

9M

ay-1

9Ju

n-19

Jul-1

9Au

g-19

Sep-

19

yoy

(%)

M3 Money Supply (%) (LHS) Money Multiplier - (RHS)

7,361

9100

5,000

10,000

15,000

20,000

25,000

FY 2

013-

14

FY 2

014-

15

FY 2

015-

16

FY 2

016-

17

FY 2

017-

18

FY 2

018-

19

1H 2

018-

19

1H 2

019-

20

Rs

Bn

Flow of financial resources to the commercial sector Money multiplier and M3 broad money

Commercial sector faces liquidity shock amid risk aversion

13

Source: RBI, Citi Research. Money multiplier: It is the amount of money the banking system generates with each rupee of reserves.

Risk Aversion has stemmed credit flow to commercial sector. Total flow of financial resources to the commercial sector fell sharply by 88% (yoy) to INR 910bn in H1FY20

Velocity has gone down which explains a slowdown in overall demand

519 442

-200-100

0100200300400500600

Jun-

11

Dec

-11

Jun-

12

Dec

-12

Jun-

13

Dec

-13

Jun-

14

Dec

-14

Jun-

15

Dec

-15

Jun-

16

Dec

-16

Jun-

17

Dec

-17

Jun-

18

Dec

-18

Jun-

19

Rs.

billi

on10.00%10.40%

0%2%4%6%8%

10%12%14%16%18%

Sep-

15

Dec

-15

Mar

-16

Jun-

16

Sep-

16

Dec

-16

Mar

-17

Jun-

17

Sep-

17

Dec

-17

Mar

-18

Jun-

18

Sep-

18

Dec

-18

Mar

-19

Jun-

19

Sep-

19

%

Deposit growth (%, yoy) Credit growth (%, yoy)

9.27%

6%7%8%9%

10%11%12%13%14%

Q1F

Y17

Q2F

Y17

Q3F

Y17

Q4F

Y17

Q1F

Y18

Q2F

Y18

Q3F

Y18

Q4F

Y18

Q1F

Y19

Q2F

Y19

Q3F

Y19

Q4F

Y19

Q1F

Y20

Q2F

Y20

%

1

-1,000,000-500,0000500,0001,000,0001,500,0002,000,0002,500,000

5%6%6%7%7%8%8%

Apr-1

9

Apr-1

9

May

-19

Jun-

19

Jun-

19

Jul-1

9

Jul-1

9

Aug-

19

Sep-

19

Sep-

19

Rs.

Crs

%

Net liquidity position surplus (+)/deficit (-) (RHS)Repo (LHS)India 10 year G-sec yield (%) (LHS)

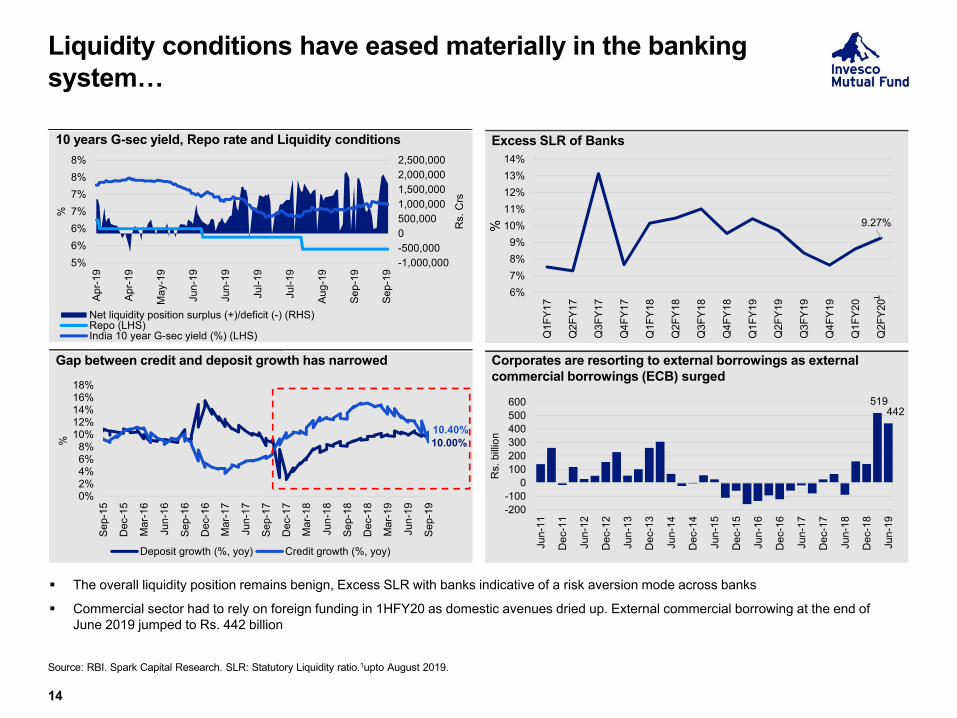

10 years G-sec yield, Repo rate and Liquidity conditions Excess SLR of Banks

Liquidity conditions have eased materially in the banking system…

14

Source: RBI. Spark Capital Research. SLR: Statutory Liquidity ratio.1upto August 2019.

Gap between credit and deposit growth has narrowed Corporates are resorting to external borrowings as external commercial borrowings (ECB) surged

The overall liquidity position remains benign, Excess SLR with banks indicative of a risk aversion mode across banks

Commercial sector had to rely on foreign funding in 1HFY20 as domestic avenues dried up. External commercial borrowing at the end of June 2019 jumped to Rs. 442 billion

20.00% 20.00%15.00% 15.00% 13.00%

11.00%17.40%

21.90%

-11.90%

5.10%7.00%

15.60%

FY 14 FY 15 FY 16 FY 17 FY 18 FY 19

Ord

er F

low

(%Yo

Y)

Guidance Actual

19%

-15%

-5%

5%

15%

25%

35%

Feb-

11

Sep-

11

Mar

-12

Sep-

12

Apr-1

3

Oct

-13

May

-14

Nov

-14

May

-15

Dec

-15

Jun-

16

Dec

-16

Jul-1

7

Jan-

18

Jul-1

8

Feb-

19

Aug-

19

Cre

dit t

o in

frast

ruct

ure

(ex

pow

er

and

tele

com

) (3M

MA,

%Yo

Y)

Sharp rebound

-

20,000

40,000

60,000

80,000

Dec

-09

Jun-

10

Jan-

11

Aug-

11

Mar

-12

Oct

-12

May

-13

Dec

-13

Jul-1

4

Feb-

15

Sep-

15

Mar

-16

Oct

-16

May

-17

Dec

-17

Jul-1

8

Feb-

19

Sep-

19

INR

bn

Government Private

-

200

400

600

800

1,000

1,200

1,400

1,600

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20

Rs.

bn

Investment trends - Green shoots visible but weak overallCapex led by Government projects holds up

15

Source: Government Documents, SBICAP securities, Investec Research, Companies, Powergrids, Media Reports, Motilal Oswal Research. 1Revised estimates. 2Budget estimates.

India’s largest Industrial company order guidance vs actual performance over years

After two strong years (FY17, FY18), FY19 was weak for road order awards; However central plan outlay for roads continues to rise indicating improvement ahead

After a gap of many years, India’s largest Industrial company was able to meet his order inflow guidance Share of Government capex in gross projects continues to remain high as private sector continues to deleverage

Share of Government capex has increased

Bank lending to infrastructure has improved significantly Central Plan outlay for roads on rise

21

32.9%

34.3%

28.6%

22%

24%

26%

28%

30%

32%

34%

36%

FY99

FY00

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

% o

f GD

P

India’s investment (GFCF) rate increases from lows of FY 2018

Investment trends - Green shoots visible but weak overallCapex trends indicate prolonged under-investment in economy

16

Source: Motilal Oswal. GFCF: Gross Fixed Capital formation

Gross Fixed capital formation has slowed materially in last 5 years v/s a decade prior

As system capacity utilization approaches peak, this downtrend could likely reverse

30%28%

25% 25% 25% 25%24% 23.2%

20% 20% 20% 20%

17%

Philip

pine

s

Sri L

anka

Bang

lade

sh

Chi

na

Indo

nesi

a

Kore

a

Mal

aysi

a

Japa

n

Cam

bodi

a

Taiw

an

Thai

land

Viet

nam

Sing

apor

e

Cor

pora

te ta

x ra

te

Base corporate tax rate of major Asian economies, Calendar year-ends, 2019 (%)

Recent corporate tax rate can further spur capex over longer term; makes India competitive

17

Source: PWC. Deloitte, KPMG, Kotak Institutional Equities. 1New manufacturing company must be incorporated on or after 1 March 2016. 2New manufacturing company must be incorporated on or after 1 October 2019, must start production before March 2023. Surcharge and cess as applicable. Tax benefits are subject to the provisions of the Income Tax Act, 1961 and are subject to amendments, from time to time. Investors should be aware that the fiscal rules/ tax laws may change and there can be no guarantee that the current tax position may continue indefinitely. In view of individual nature of tax consequences, each investor is advised to consult his/ her own professional tax advisor.

Indian Corporate Tax Rates

Type of Domestic Company Base Tax Rate

Minimum Alternative Tax

Rate

Company claiming exemption 30% 15%

Company having total turnover during FY 2017-18 not exceeding INR 400 crores

25% 15%

Company engaged in manufacturing1 25% 15%

Company not claiming exemption 22% Not applicable

New Manufacturing Companies2 15% Not applicable

With recent tax rate changes, corporate India to become more competitive compared with other Asian economies

4.65%

0%

2%

4%

6%

8%

10%

Apr-1

5

Sep-

15

Jan-

16

May

-16

Sep-

16

Jan-

17

May

-17

Oct

-17

Feb-

18

Jun-

18

Oct

-18

Feb-

19

Jul-1

9

Nom

inal

rura

l wag

e gr

owth

(%

yoy)

5%

-10%-5%

-50%-40%-30%-20%-10%

0%10%20%30%

June

1st

W

June

2nd

W

June

3rd

W

June

4th

W

July

1st

W

July

2nd

W

July

3rd

W

July

4th

W

Aug

1st W

Aug

2nd

W

Aug

3rd

W

Aug

4th

W

Sep

1st W

Sep

2nd

W

Sep

3rd

W

Sep

4th

WRai

nfal

l as

% o

f LPA

2019 2018 2017

Good rainfall bodes well for the Kharif and upcoming rabi crops

-50%-30%-10%10%30%50%70%90%

110%

May

-09

Dec

-09

Jun-

10D

ec-1

0Ju

n-11

Dec

-11

Jun-

12Ja

n-13

Jul-1

3Ja

n-14

Jul-1

4Ja

n-15

Aug-

15Fe

b-16

Aug-

16Fe

b-17

Aug-

17Fe

b-18

Sep-

18M

ar-1

9Se

p-19

% y

oy

Sugar Rs./quintal wheat Rs./metric ton Pulses Rs./quintalMilk Rs./litre Soyabean Rs./15kg

Agri prices have started inching up – Milk, Pulses, Wheat and Soybean prices are up

Positive signs for Rural Economy

18

Source: Spark Capital. W: Week. LPA: Long Period Average

3.3%

-25.0%-20.0%-15.0%-10.0%

-5.0%0.0%5.0%

10.0%15.0%20.0%

Jan-

12Ju

l-12

Dec

-12

May

-13

Oct

-13

Mar

-14

Aug-

14Ja

n-15

Jun-

15N

ov-1

5Ap

r-16

Oct

-16

Mar

-17

Aug-

17Ja

n-18

Jun-

18N

ov-1

8Ap

r-19

Sep-

19

Glo

bal F

ood

Pric

e In

dex

(yoy

%)

Global food prices have started inching up, which is likely to keep domestic agri prices momentum

Rural nominal wage growth has also inched up

Good rainfall, improvement in agricultural prices and increase in nominal wages bode well for rural consumption growth ahead

1.2%

19.4% 20.7%

11.0% 9.8%

62.9%

11.2%

FY15 FY16 FY17 FY18 FY19 FY20(BE)

FY20(April toAugust)

Cen

tral g

over

nmen

t rur

al s

pend

ing

(%,Y

oY)

Central government is increasing rural spending

769

981

Amounts given in FY18 andFY19 budgets

Amounts left to be disbursedFa

rm lo

an w

aive

r dis

burs

ed b

y st

ates

(IN

R b

n)

States still have to disburse 60% of farm loan waiver in next two years

Increase in disbursals by government could provide impetus to rural economy…

19

Source: RBI, State budgets, central government budget documents, Edelweiss Research. PM-KISAN: Pradhan Mantri Kisan Samman Nidhi Scheme Mahatma Gandhi National Rural Employment Guarantee Act

Government push through schemes like MGNREGA, PM-Kisan likely to improve rural growth

Slew of recent reforms / measures by Government to spur economy

Corporate tax rate has been made more competitive

Promoting manufacturing through preferential base rate of 15% corporate tax for new entities1

Reversal of proposed higher surcharge on FPI

Consolidation of PSU banks

Rs 100bn for unfinished housing projects / relaxation of ECB norms for affordable housing

Automated refund route for input tax credit on GST to release working capital for industry

Boost to exports through scheme of remission of taxes and duties on export products

RBI’s recommendation on policy-linked lending rates to improve rate transmission

20

Source :Motilal Oswal. Government Publications. Fed: Federal Reserve. PE: Price to Earning. FPI: Foreign Portfolio Investor. GST: Goods & Services Tax. ECB: External Commercial Borrowing. 1New manufacturing company must be incorporated on or after 1 October 2019, must start production before March 2023. Surcharge and cess as applicable. Tax benefits are subject to the provisions of the Income Tax Act, 1961 and are subject to amendments, from time to time. . Investors should be aware that the fiscal rules/ tax laws may change and there can be no guarantee that the current tax position may continue indefinitely. In view of individual nature of tax consequences, each investor is advised to consult his/ her own professional tax advisor.

-7.8

7% -6.2

0%-6

.33%

-4.1

7%3.

04%

1.44

%4.

35%

5.83

%10

.31%

9.72

%10

.90% 13

.90%

15.2

9%16

.10%

26.1

1%22

.30%

10.4

3%6.

72%

1.33

%

Mar

-15

Jun-

15Se

p-15

Dec

-15

Mar

-16

Jun-

16Se

p-16

Dec

-16

Mar

-17

Jun-

17Se

p-17

Dec

-17

Mar

-18

Jun-

18Se

p-18

Dec

-18

Mar

-19

Jun-

19Se

p-19

1

Nifty Sales growth (%)

Earnings – Near term pain, but tax cuts may help FY 20 earnings

21

Source: Kotak, Nifty companies Profit Growth. PAT: Profit After Tax. 1E: Estimates. CAGR: Compounded Annualised Growth Rate. EPS: Earning Per Share

-9.0

7%6.

45%

-1.5

9%-1

.39%

3.06

%0.

83%

9.63

%10

.43%

14.6

2%-7

.55%

13.5

0%12

.70%

-8.8

5%13

.00%

11.2

3%3.

33%

18.6

2%3.

11%

-6.5

4%

Mar

-15

Jun-

15Se

p-15

Dec

-15

Mar

-16

Jun-

16Se

p-16

Dec

-16

Mar

-17

Jun-

17Se

p-17

Dec

-17

Mar

-18

Jun-

18Se

p-18

Dec

-18

Mar

-19

Jun-

19Se

p-19

1

Nifty PAT Growth (%)

398

384

439 449 48

0

558

690

Mar

-15

Mar

-16

Mar

-17

Mar

-18

Mar

-19

Mar

-20

Mar

-21 11

EPS Growth

For 2Q20E, Sales and earnings growth are expected to be weak as explained by weakness in consumption demand and global commodities However for FY20E Earnings growth is expected to recover strongly led by recovery in earnings of Financials & Healthcare and corporate tax

rate cut

1.73%2.03%

2.91%

4.54%

5.29%5.73%

6.89%7.27%

5.15%5.70%

5.34%

3.83%3.78%

3.50%3.31%

2.67% 2.75%

1.71%

2.67%

Average : 4.04%

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

PAT (% of GDP) Average

Corporate profit as a share of GDP is lowest in more than a decade

Corporate profit as a percentage of GDP still significantly below average

22

Source: CMIE, IIFL Research. Based on a standalone financials of more than 5,500 companies are considered for FY 19, whereas from FY 01 – FY 18 it ranged from 9,000 to 22,800 companies. PAT: Profit After Tax.

Cyclically low corporate profits have significant room to recover FY19 profitability has recovered from the bottom of FY 2018 but still has a long way to reach the average

26.95

0

5

10

15

20

25

30

35

Sep-

04

Oct

-05

Nov

-06

Dec

-07

Jan-

09

Feb-

10

Feb-

11

Mar

-12

Apr-1

3

May

-14

Jun-

15

Jun-

16

Jul-1

7

Aug-

18

Sep-

19

Sensex PE Ratio (trailing twelve months)

While valuations presently are at a premium to long term average…

23

Source: MOSL, Invesco Asset Management (India) Research, Bloomberg. PE: Price to Earning. Data as on 30 September 2019

Average since September 2004 : 19.69x

Sensex continues to trade at 37% premium to long term average

-19%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

Jan-

06Se

p-06

May

-07

Jan-

08O

ct-0

8Ju

n-09

Feb-

10O

ct-1

0Ju

l-11

Mar

-12

Nov

-12

Jul-1

3Ap

r-14

Dec

-14

Aug-

15Ap

r-16

Dec

-16

Sep-

17M

ay-1

8Ja

n-19

Oct

-19

(Dis

coun

t) / P

rem

ium

13 Years Average: -14%

-1%

-50%

-20%

10%

40%

70%

100%

130%

160%

Jan-

06Se

p-06

May

-07

Jan-

08O

ct-0

8Ju

n-09

Feb-

10O

ct-1

0Ju

l-11

Mar

-12

Nov

-12

Jul-1

3Ap

r-14

Dec

-14

Aug-

15Ap

r-16

Dec

-16

Sep-

17M

ay-1

8Ja

n-19

Oct

-19

(Dis

coun

t) / P

rem

ium

13 Years Average: 9%

Valuation of Mid cap vs. Large Caps - trailing twelve months (Mid caps over large caps)

Valuation of Mid cap vs. Large Caps - trailing twelve months positive PE (excluding loss making companies)(Mid caps over large caps)

Mid-caps now trade at attractive valuations versus large Caps

24

Source: Invesco Asset Management (India) Research, Bloomberg, Data as on 14 October 2019. Note: Valuations are based on FY19 Price to Earning MultiplePast performance may or may not be sustained in future.

While overall valuations continue to remain challenging, Midcap Index (Nifty Midcap 100) valuation has improved and now trades at a discount of 1% as compared to 9% premium being the long term average

And if one excludes loss-making companies, midcap index trades at 19% discount to large caps as compared to 14% discount being long term average

Market Outlook

25

Global growth trends have weakened mainly due to US-China standoff. Recent central bank actions, Brexit deal andpossible US-China dispute resolution could support growth

India’s twin deficits in comfort zone; provide fiscal space to boost growth

India’s lead indicators continue to show weakness. Consumption demand remains weak but improving liquidity and continued benign trends in inflation and fall in interest rates should improve growth characteristics

Financial sector seeing fresh round of challenges, credit environment appears weak overall. Liquidity conditions have improved however, risk aversion by banks has stemmed credit flow to commercial sector

Government now using both fiscal and monetary tools to spur economy

Building blocks in place for cyclical recovery in earnings over next few years largely led by improvement in asset quality for financials and improved order inflow for Industrials. Consumption growth may exhibit weak trends in the short run

Earnings are suppressed as compared to long term average and there is scope for mean reversion. Tax rate cuts could help in improvements of earnings

The Sensex is trading at a P/E of 25.6x trailing twelve months EPS, which is a 37% premium to the long-term average. Midcap and small cap valuations are now attractive as compared to their past and offer value to investors

Our portfolio stance remains pro-cyclical; current overweight sectors include industrials and consumer discretionary. We are also turning constructive on utilities sector due to combination of falling interest rates, improved earnings trajectory and attractive valuations

Note: The sectors referred above should not be construed as recommendations from Invesco Asset Management (India) Private Limited and/or Invesco Mutual Fund. The schemes may or may not have any present or future positions in these sectors.

Disclaimer

Disclaimer: This presentation is for information purposes only and is not an offer to sell or a solicitation to buy any mutual fund units/securities. The information alone is not sufficient and shouldn’t be used for the development or implementation of an investment strategy. It should not be construed as investment advice to any party. All opinions, figures, charts/graphs and data included in this presentation are as on date and are subject to change without notice. The sectors referred in this presentation are for illustrative purposes only and should not be construed as recommendations from Invesco Asset Management (India) Private Limited and/or Invesco Mutual Fund. Schemes of Invesco Mutual Fund may or may not have any present or future positions in these sectors. The content of this document is intended solely for the use of the addressee. If you are not the addressee or the person responsible for delivering it to the addressee, any disclosure, copying, distribution or any action taken or omitted to be taken in reliance on it is prohibited and may be unlawful. The data used in this presentation is obtained by Invesco Asset Management (India) Private Limited from the sources which it considers reliable. While utmost care has been exercised while preparing this document, Invesco Asset Management (India) Private Limited does not warrant the completeness or accuracy of the information and disclaims all liabilities, losses and damages arising out of the use of this information. Neither Invesco Asset Management (India) Private Limited nor any person connected with it accepts any liability arising from the use of this information. The recipient(s) before acting on any information herein should make his/their own investigation and seek appropriate professional advice.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

26

Get in Touch

Corporate Office:Invesco Asset Management (India) Private Limited2101 A, 21st Floor, A- Wing, Marathon Futurex, N.M. Joshi Marg, Lower Parel, Mumbai – 400 013+91 22 67310000 F +91 22 23019422

To invest:Call 1800-209-0007 ∆ sms ‘Invest’ to 56677Invest Online www.invescomutualfund.com

Follow us on