Equity Analysis and Valuation of B&G Foods, Inc.

181

Equity Analysis and Valuation of B&G Foods, Inc. David Hall [email protected] Juan Parra-Vazquez [email protected] Olzhas Alexandrov [email protected] Taylour Bennett [email protected] Tomy Otounga [email protected] TR 12:30-1:50 class

Transcript of Equity Analysis and Valuation of B&G Foods, Inc.

Equity Analysis and Valuation of B&G Foods, Inc.

David Hall [email protected]

Juan Parra-Vazquez [email protected]

Olzhas Alexandrov [email protected]

Taylour Bennett [email protected]

Tomy Otounga [email protected]

TR 12:30-1:50 class

B&G FOODS EVALUATION 2

Table of Contents

Executive Summary of B&G Foods, Inc. 7

Industry Analysis 7

Accounting Analysis 9

Financial Analysis 10

Valuation Analysis 13

Company Overview 14

Business Products 14

Sales Volume and Growth 15

Competitors 17

Industry: Processed and Packaged Goods 17

Market Capitalization of Firm 18

Location 18

Stock Performance 19

Introduction to the Five-Force Analysis 21

Rivalry among Existing Firms 22

Threat of new Entrants 26

Threat of Substitute Products 27

Bargaining Power of Buyers 28

Bargaining Power of Suppliers 29

Industry Sales and Growth 31

Revenue 32

Market Capitalization 33

Conclusion 34

Analysis of Key Success Factors for Value Creation in the Industry 35

First Mover Advantage 35

Diversified Products 37

Lower-Input Costs 38

Retailer Relations 40

Brand Awareness 41

B&G FOODS EVALUATION 3

Conclusion 42

Cost Leadership 43

Competitive Advantage 43

Economies of Scale and Scope 44

Efficient Production 45

Simpler Product Designs 45

Low-Cost Distribution 45

Conclusion 46

Accounting Analysis 47

Key Accounting Policies 48

Type 1 Accounting Policies 49

Cost Leadership 49

Product Quality 50

Type 2 Accounting Policies 51

Research & Development 51

Goodwill 52

Assessing Key Accounting Policies 53

Accounting strategy 53

Accounting for Goodwill 54

Accounting for pension Liabiliites 55

Conclusion 57

Evaluate Accounting Strategy 57

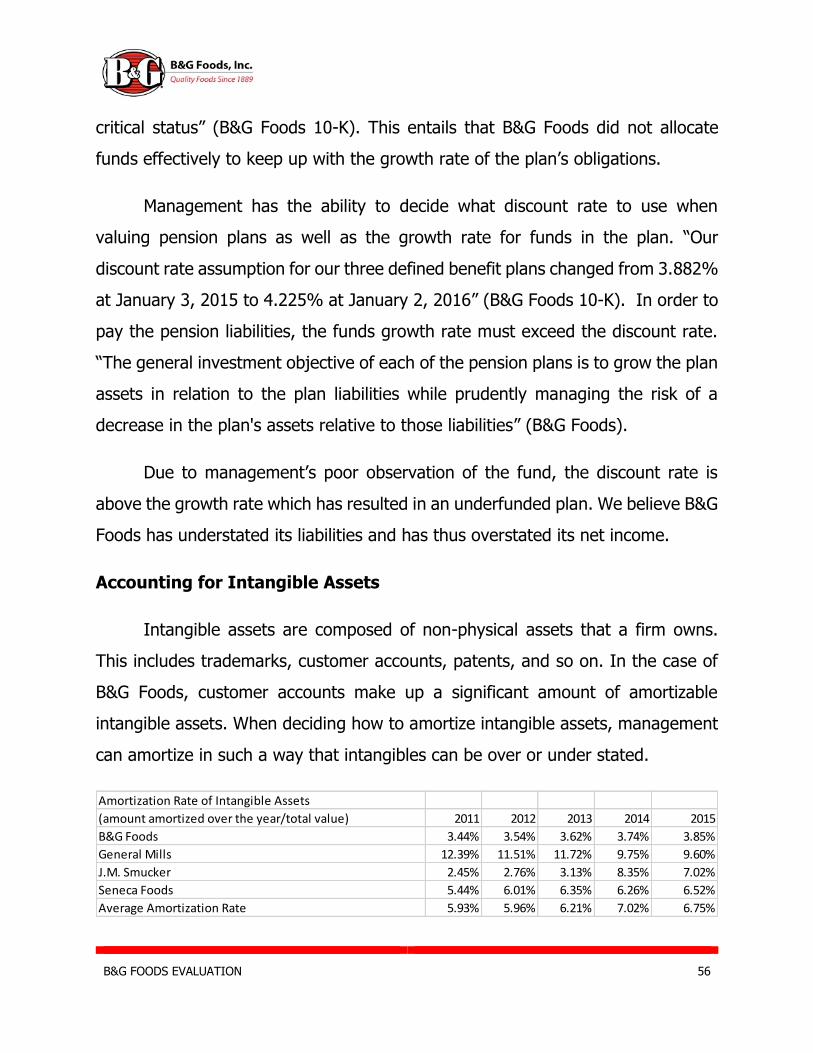

Research and Development 58

Goodwill and Intangibles 58

Capital vs. Operating leases 59

Currency Exchange 60

Conclusion 61

Quality of Disclosure 62

Internal and External control 64

Fair Value vs. Carrying value 64

Key financial disclosure 65

B&G FOODS EVALUATION 4

Areas lacking disclosure 67

Conclusion 68

Identify Potential Red Flags 68

Asset write-offs 69

Amortization of Intangible Assets 69

Operating Leases 70

Goodwill 71

Conclusion 71

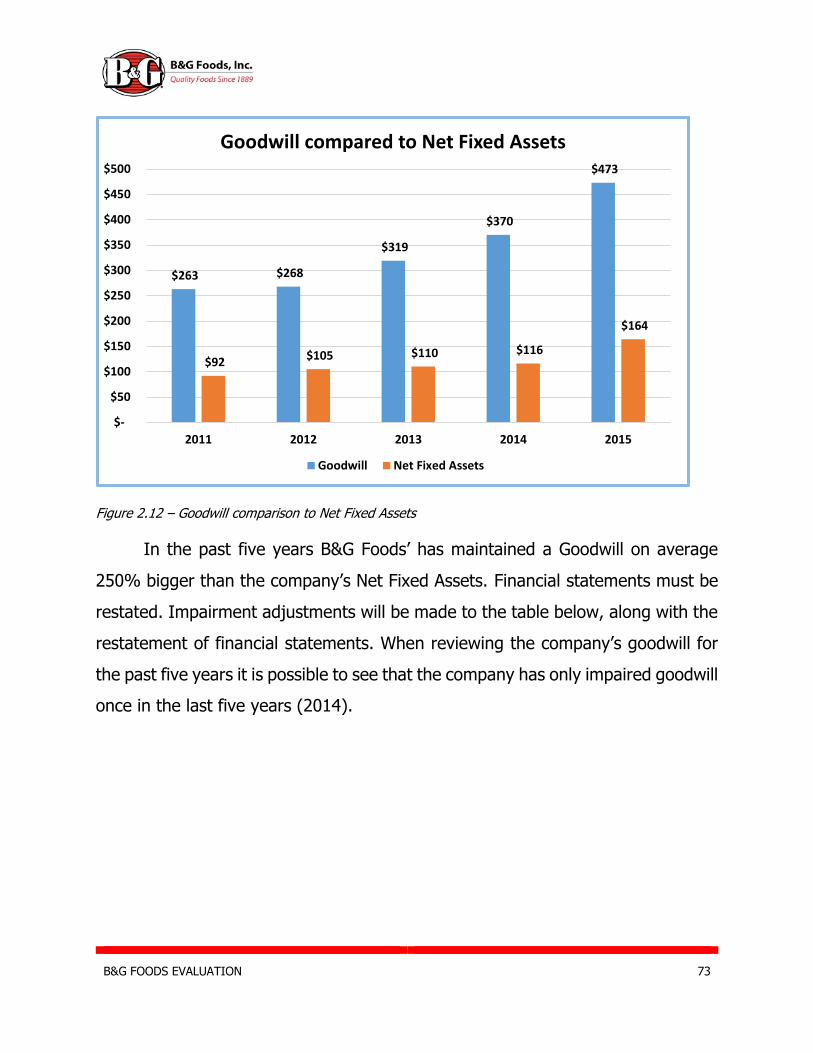

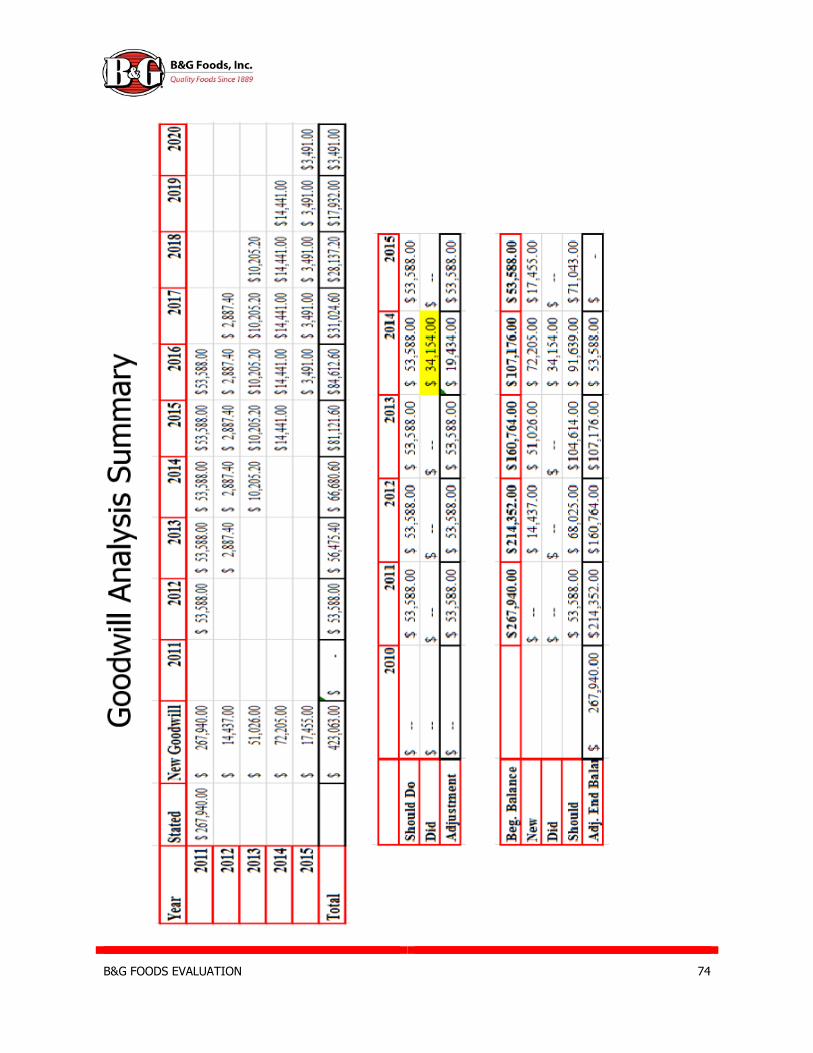

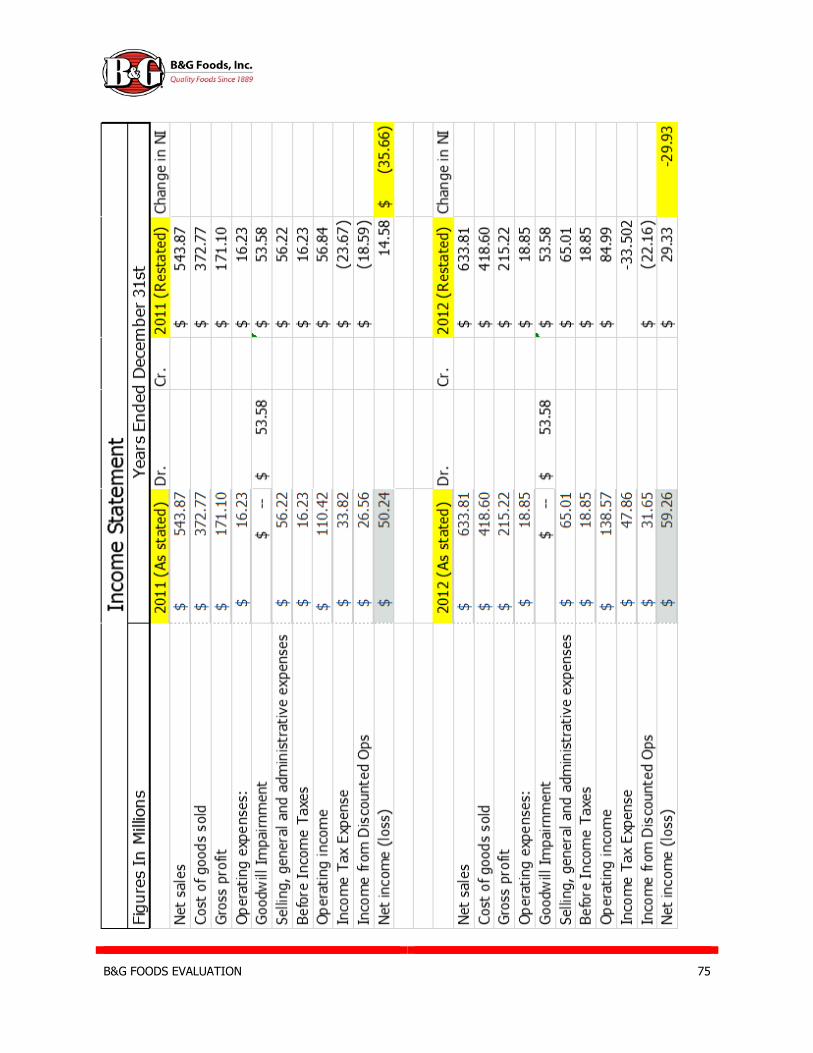

Undo Accounting Distortions 72

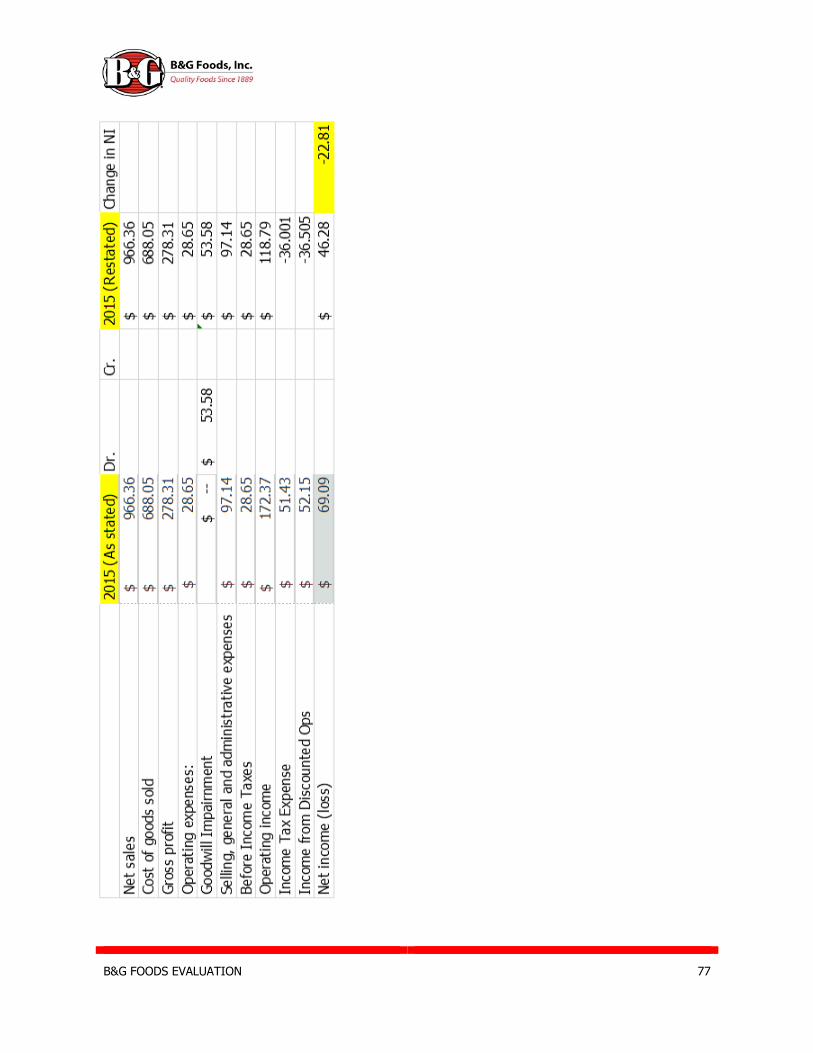

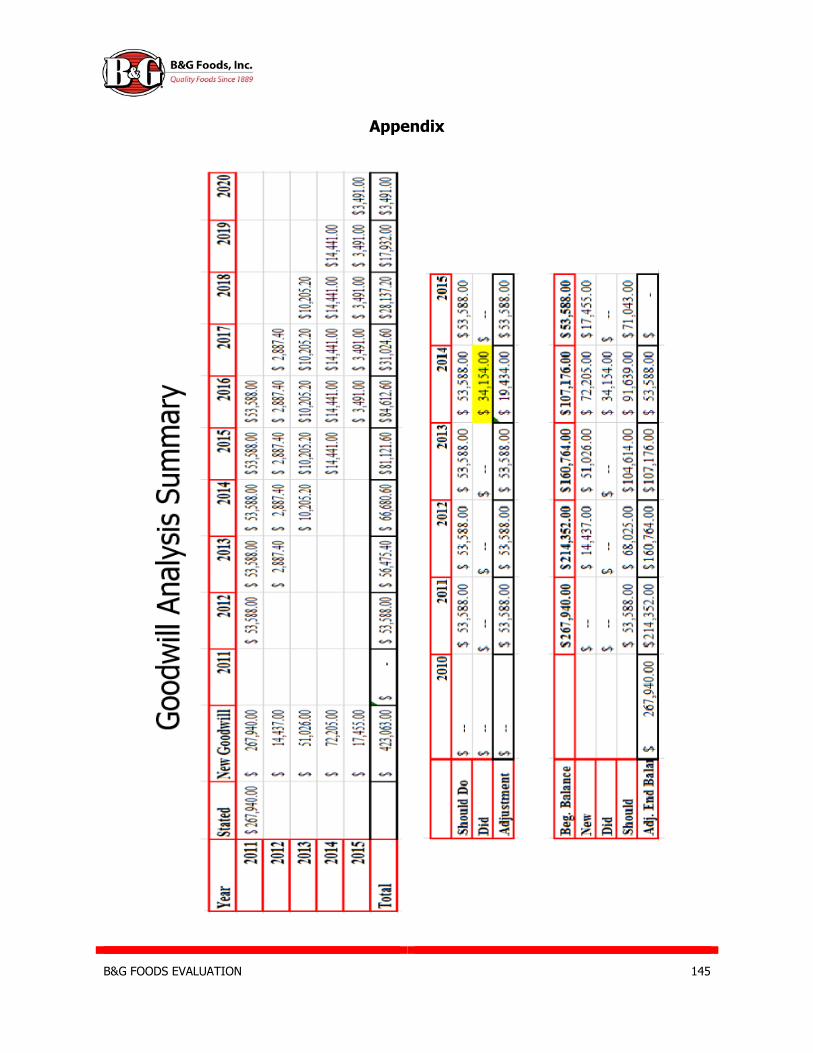

Goodwill Analysis Summary 74

Income Statement Restated 75

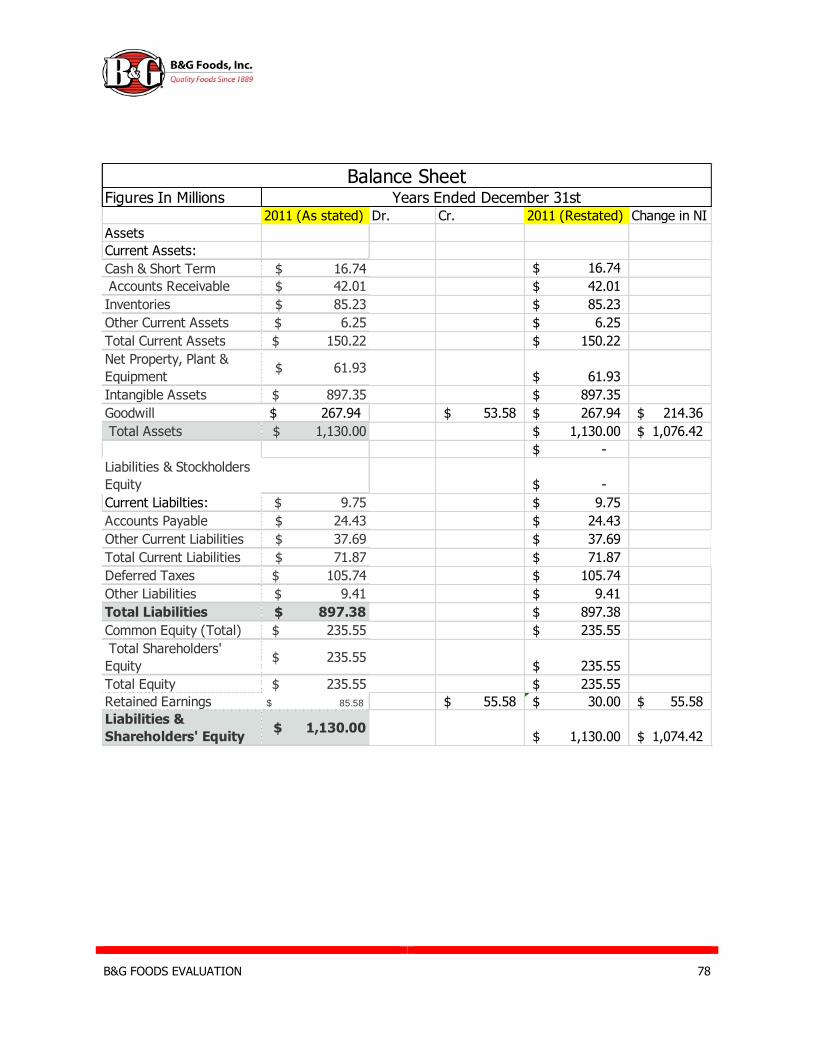

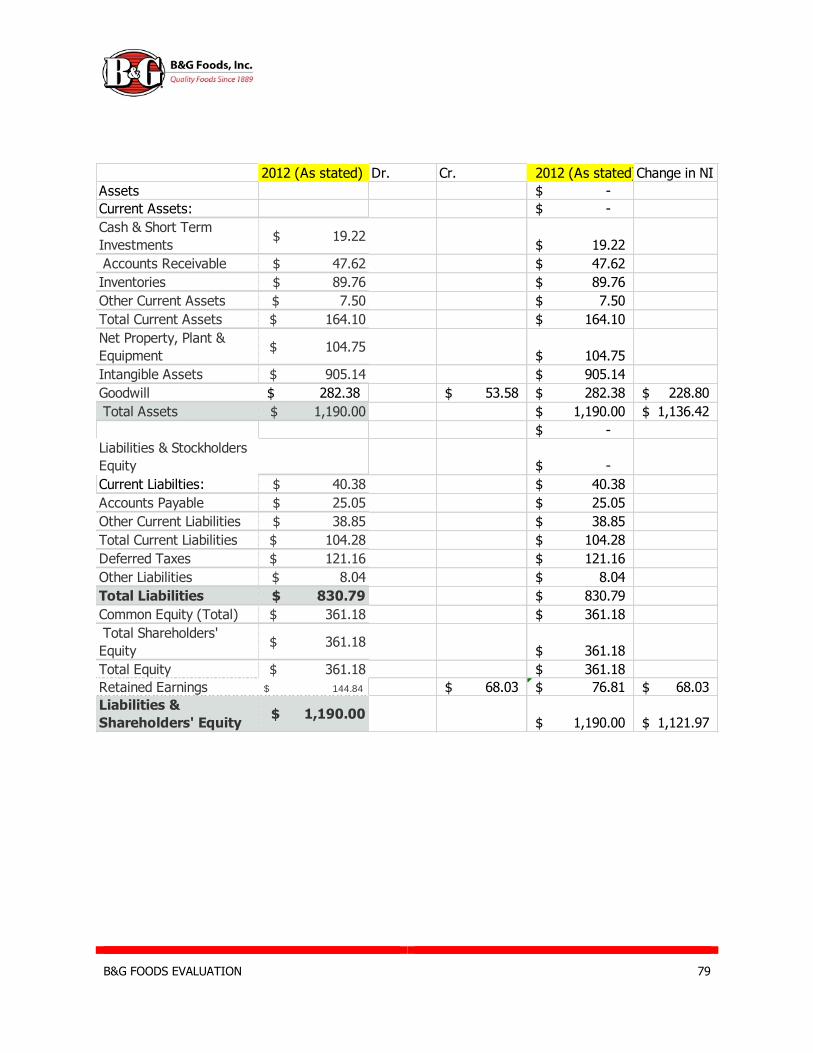

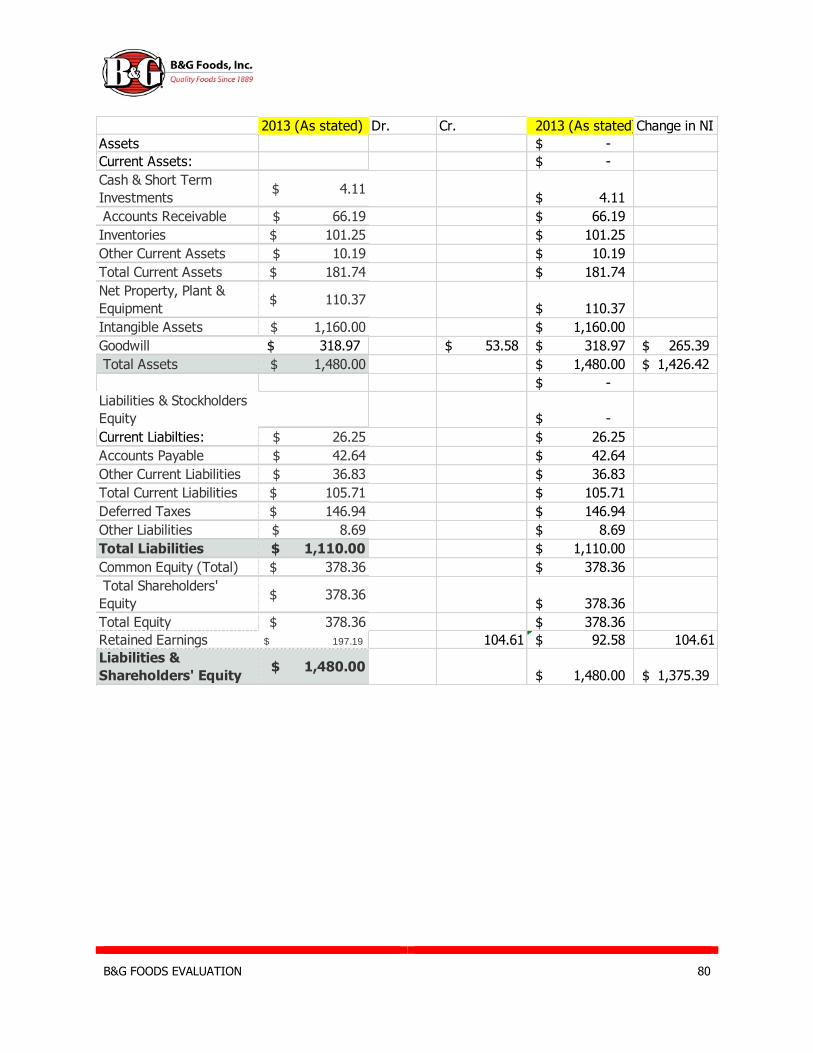

Balance Sheet Restated 78

Introduction to Financial Analysis 83

Ratio Analysis 83

Liquidity Ratios 83

Current Ratio 84

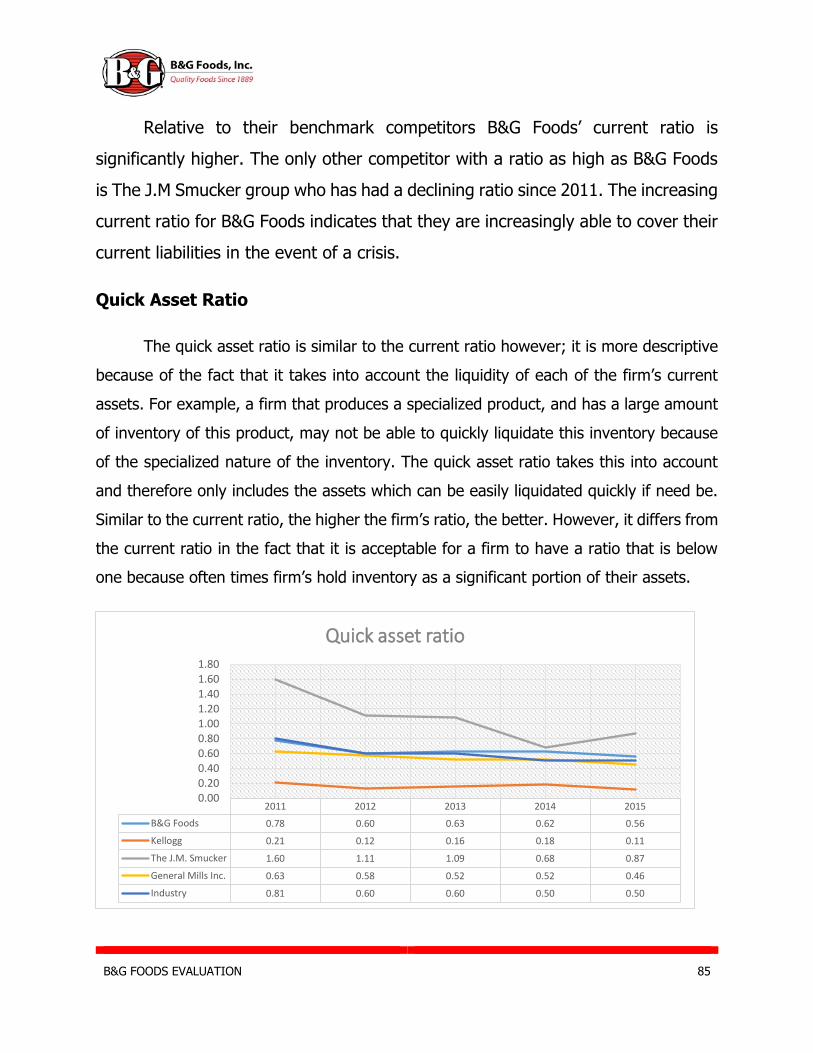

Quick Asset Ratio 85

Conclusion 86

Operating Efficiency Ratios 86

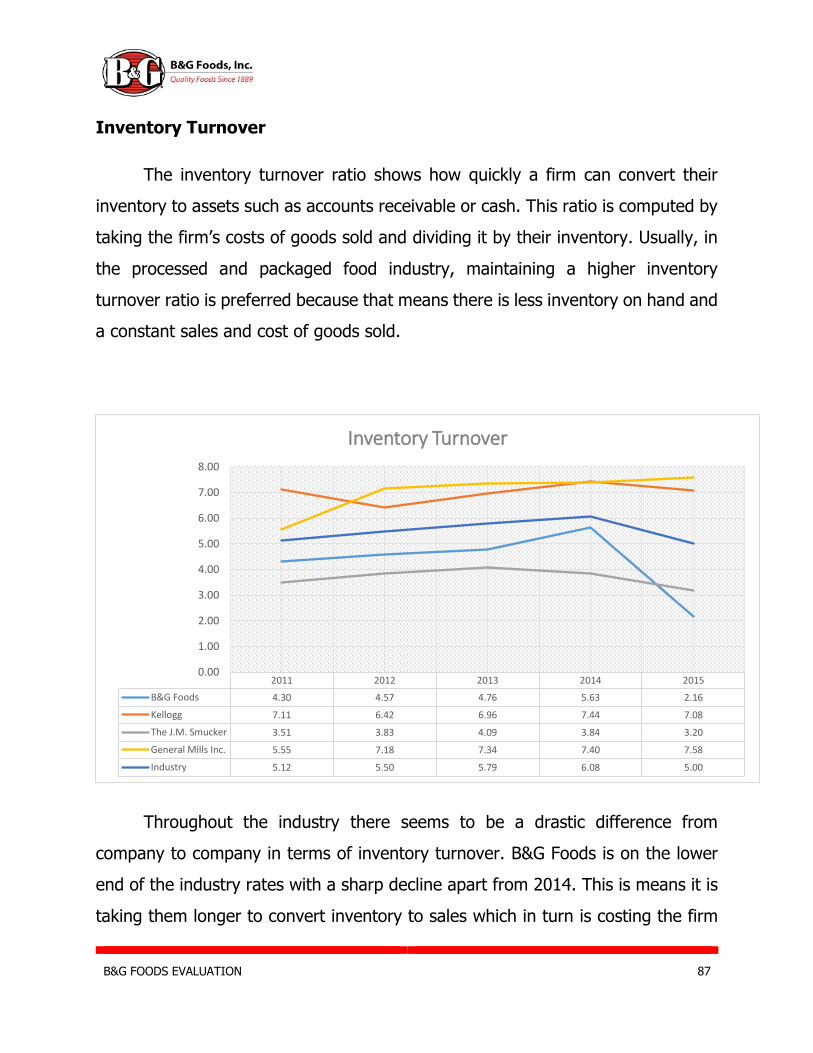

Inventory Turnover 87

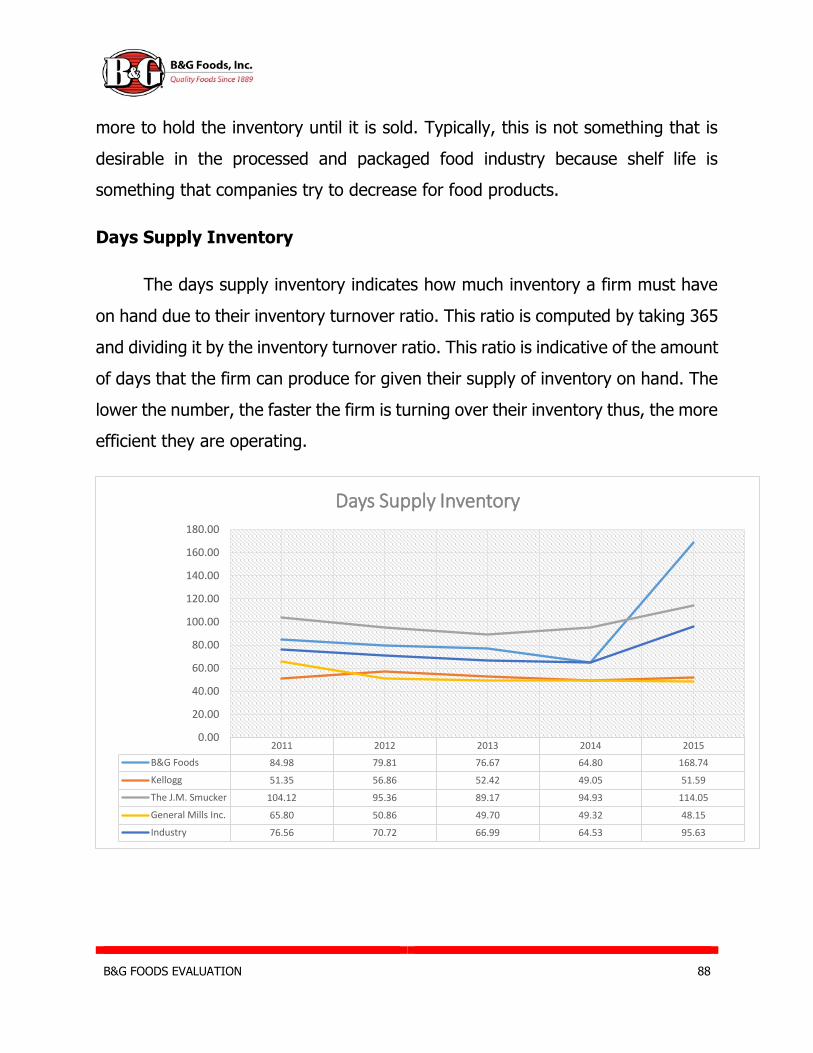

Days Supply Inventory 88

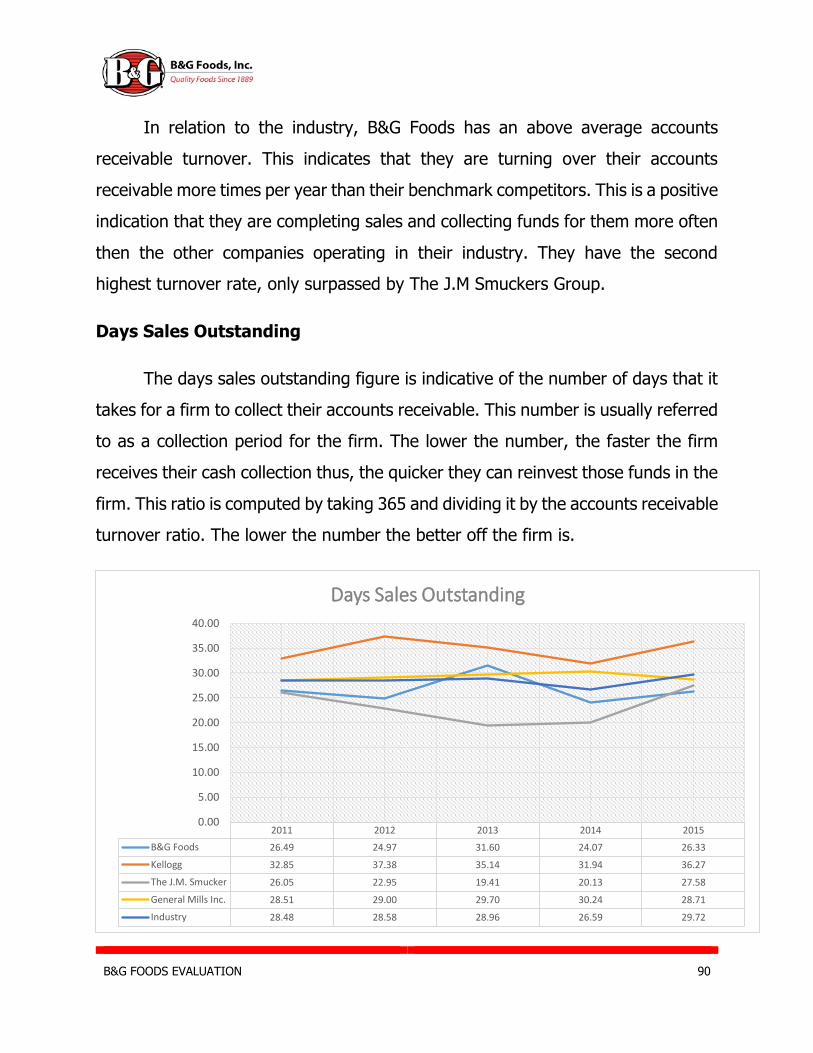

Accounts Receivable Turnover 89

Days Supply Outstanding 90

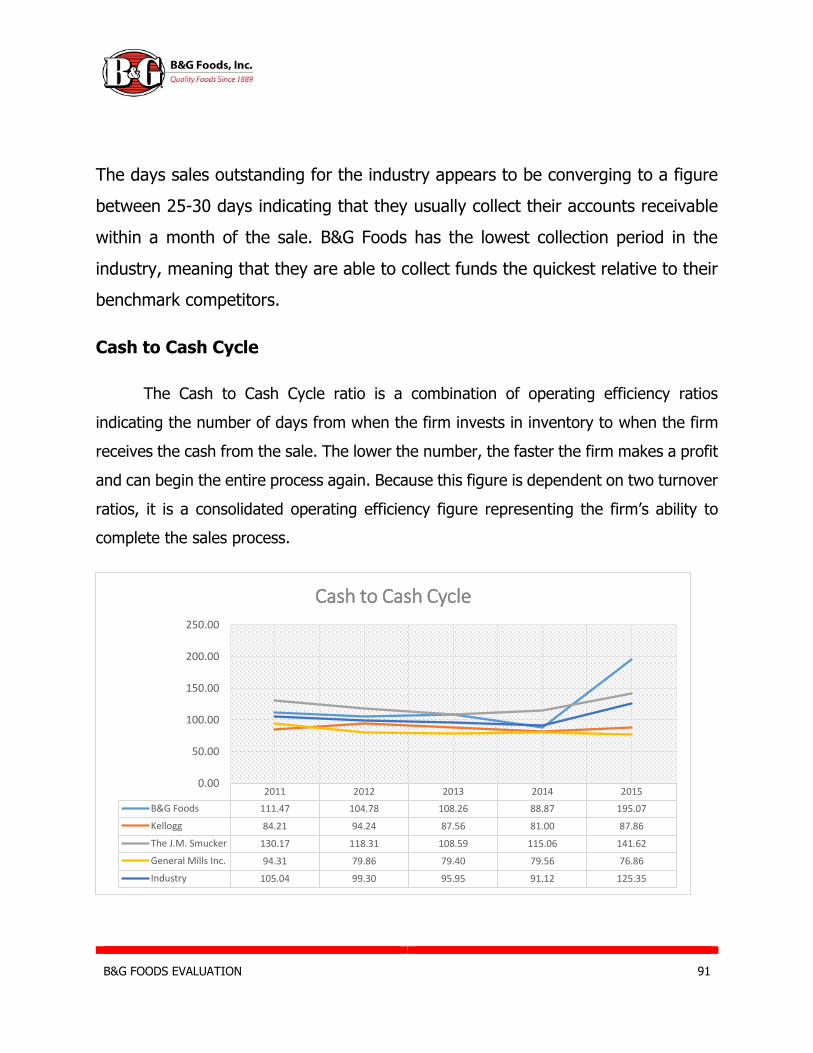

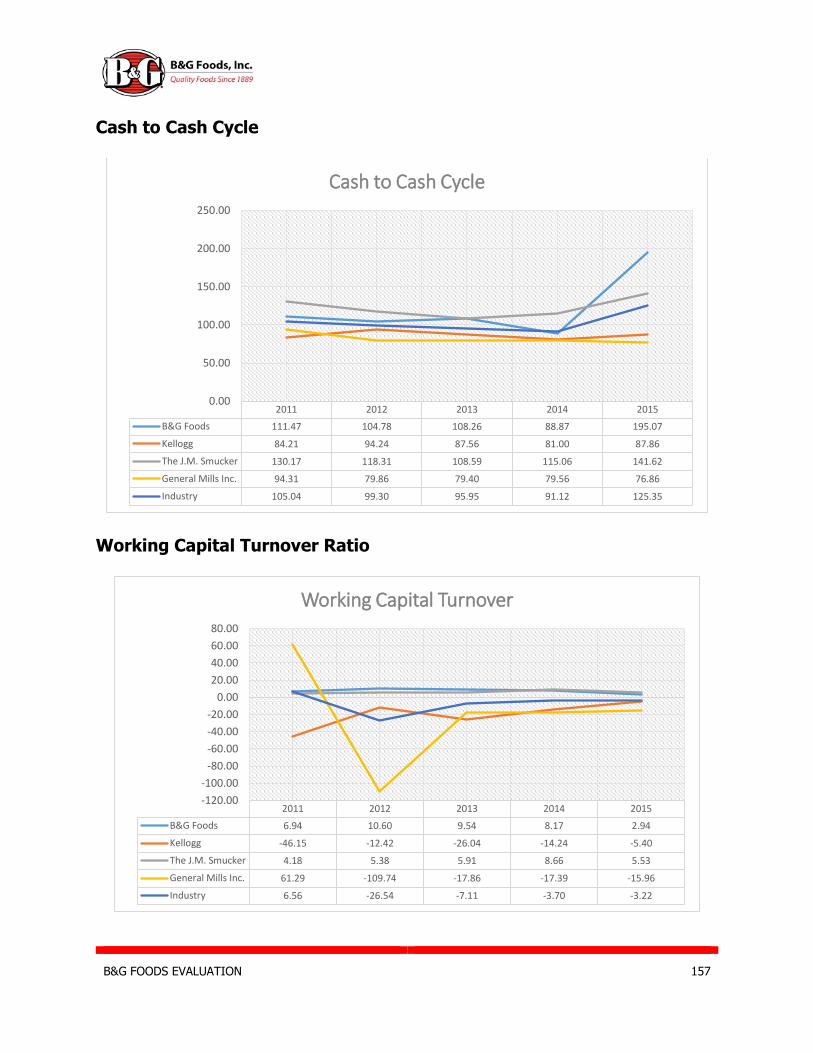

Cash to Cash Cycle 91

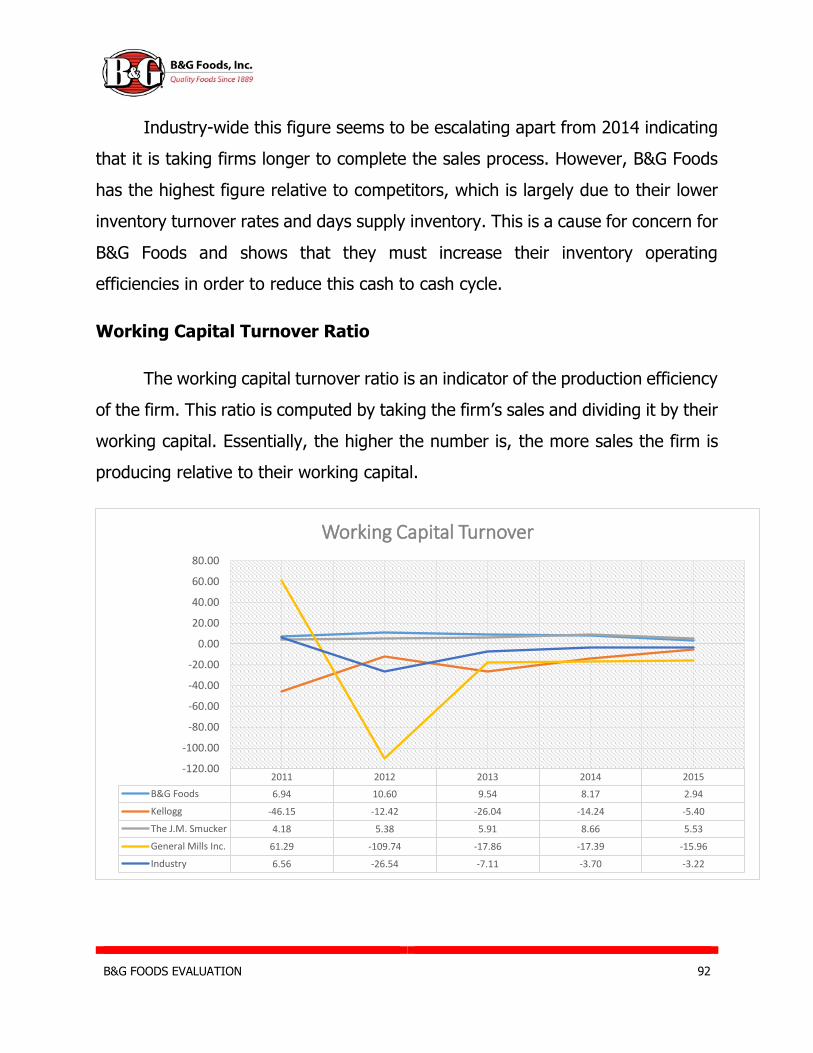

Working Capital Turnover 92

Conclusion 93

Profitability Ratios 93

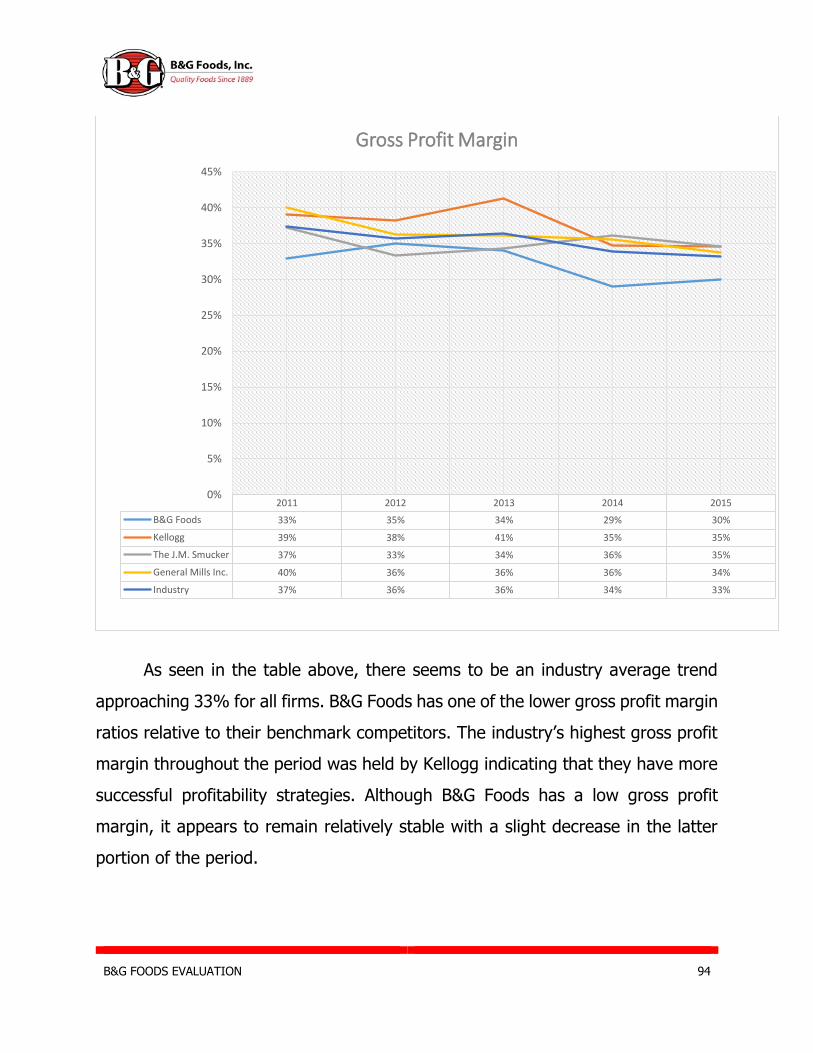

Gross Profit Margin 93

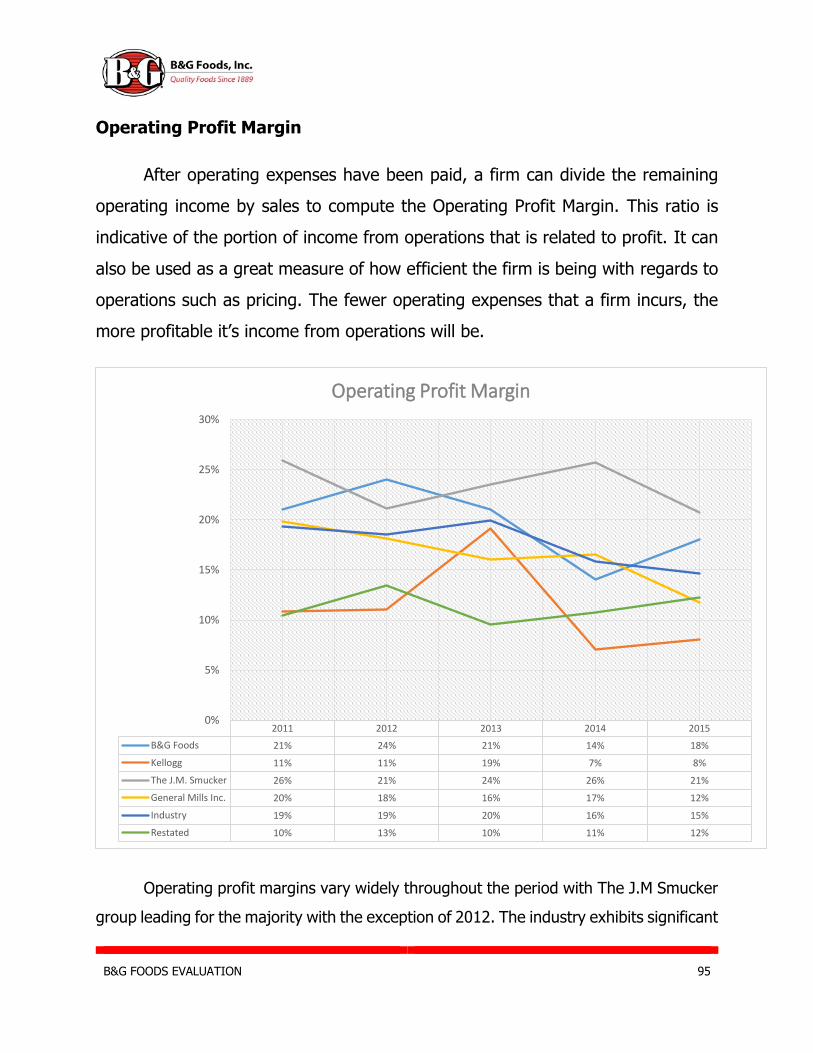

Operating Profit Margin 95

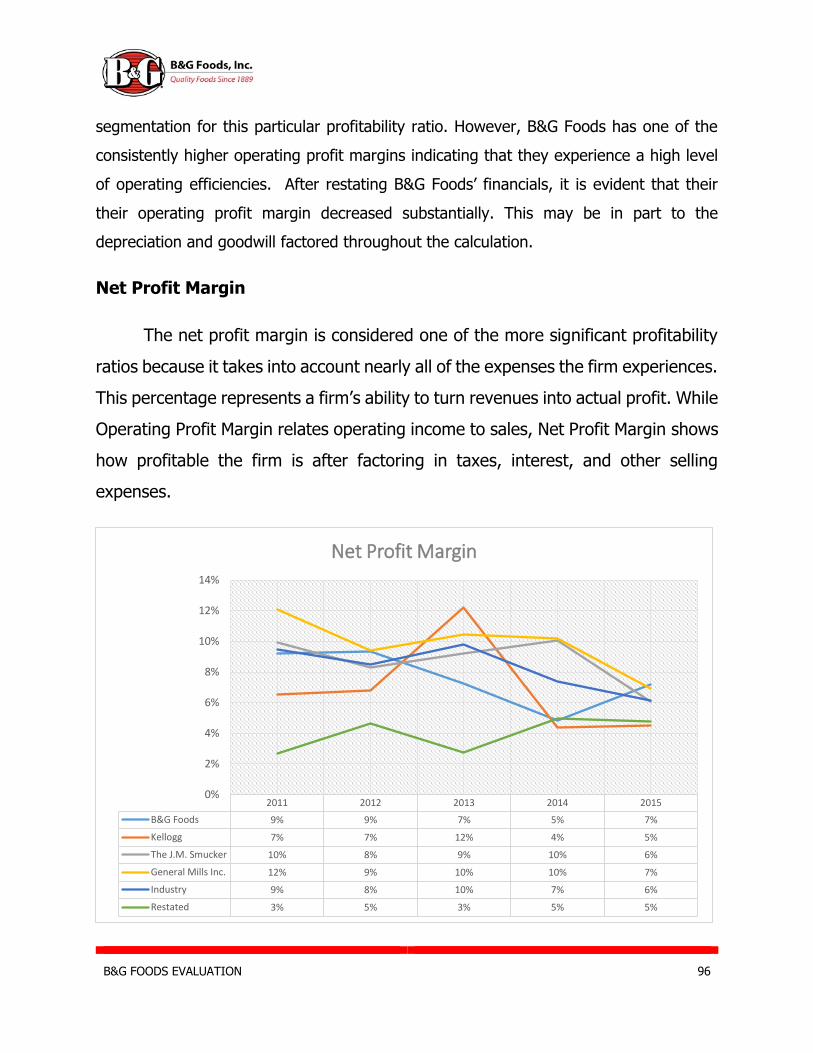

Net Profit Margin 96

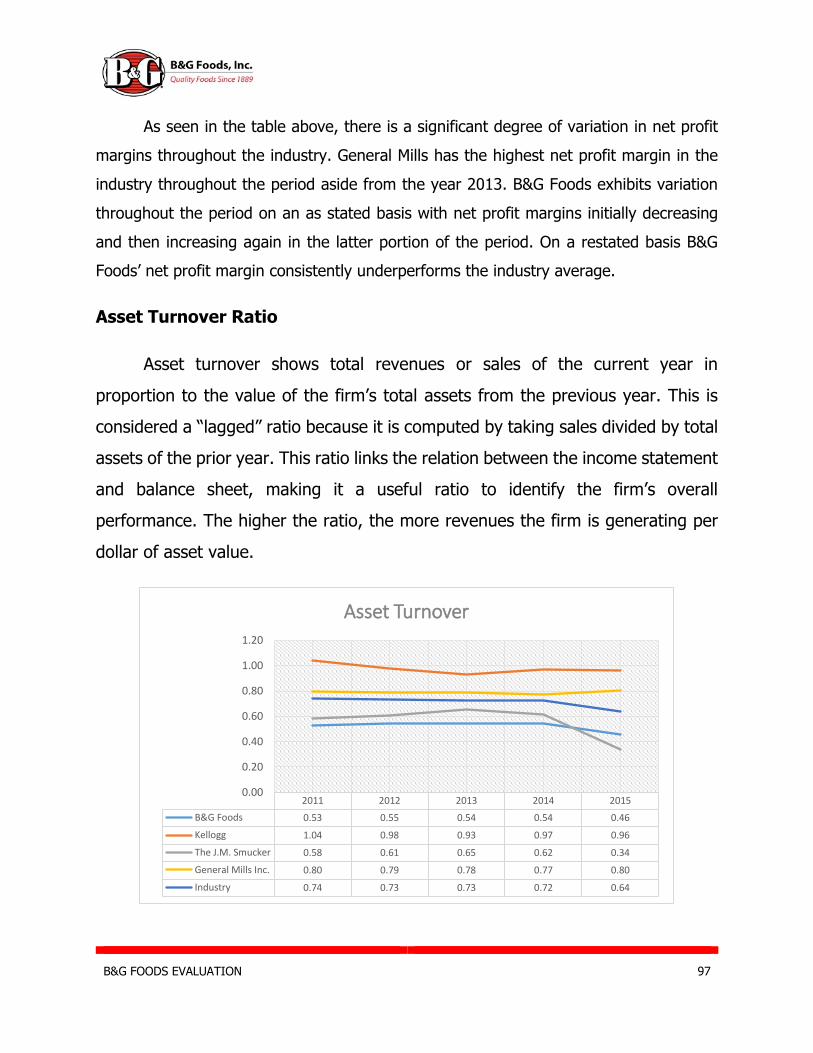

Asset Turnover Ratio 97

B&G FOODS EVALUATION 5

Return on Assets 98

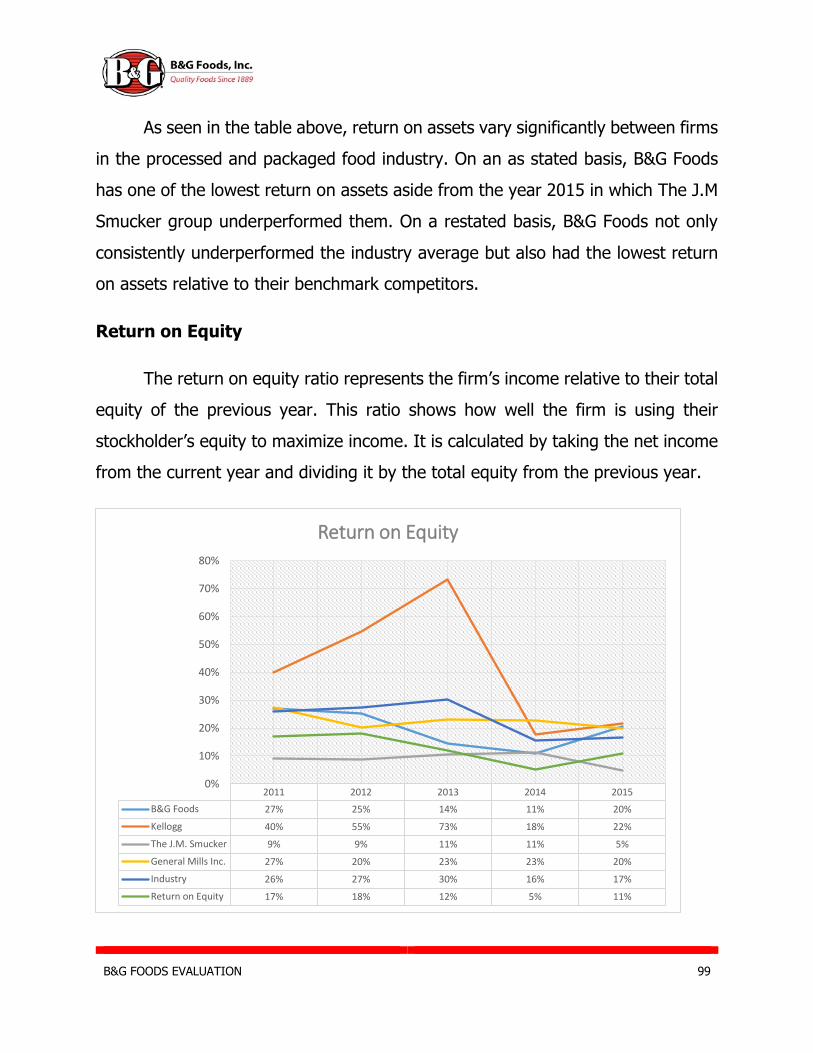

Return on Equity 98

Conclusion 100

Capital Structure Ratios 100

Debt to Equity 101

Times Interest Earned 102

Altman’s Z-Score 103

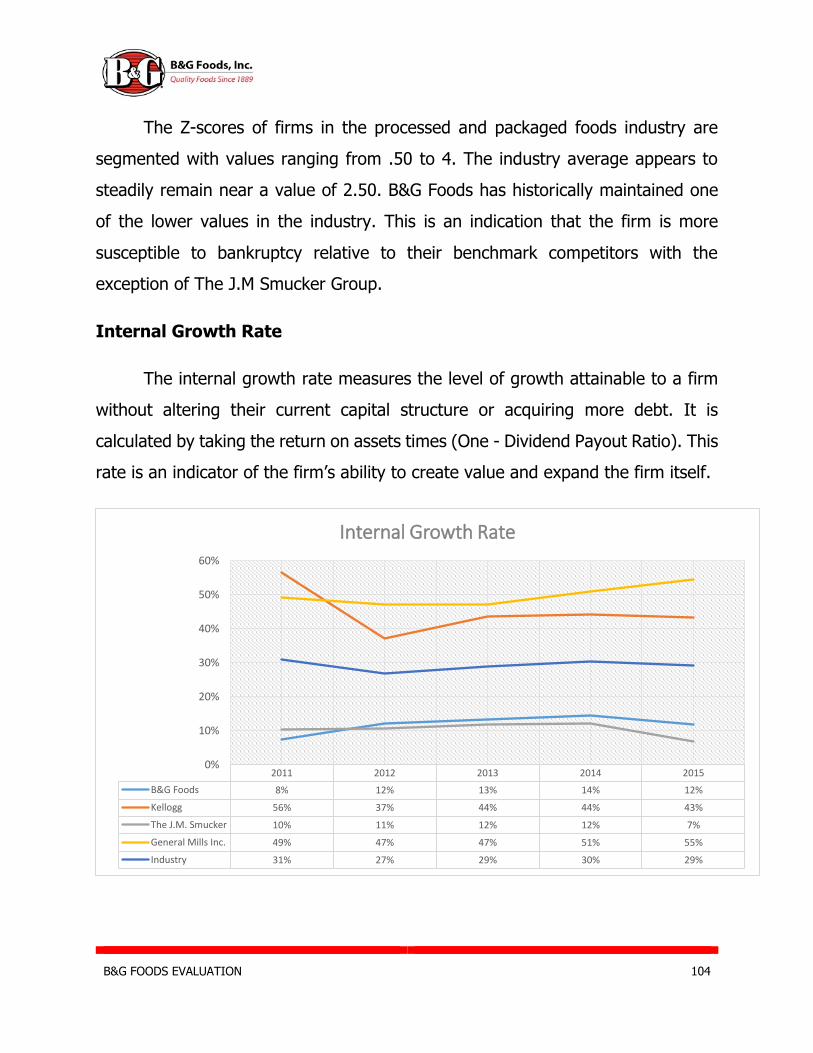

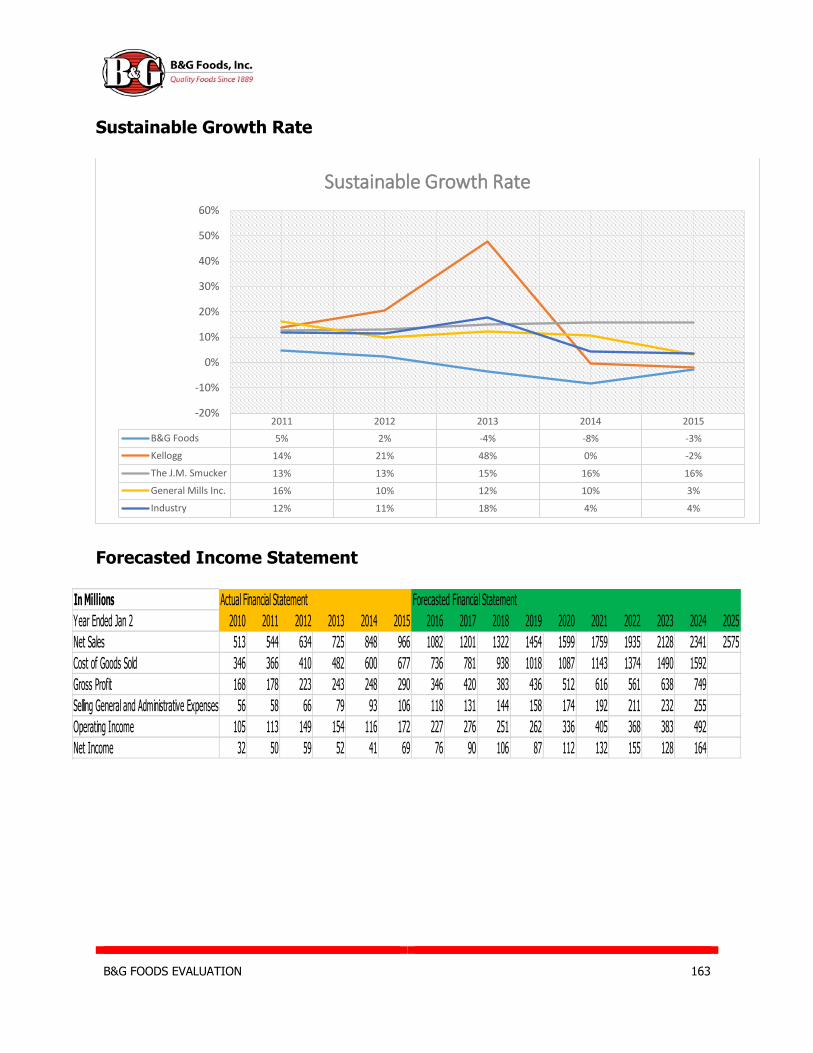

Internal Growth Rate 104

Sustainable Growth Rate 105

Conclusion 106

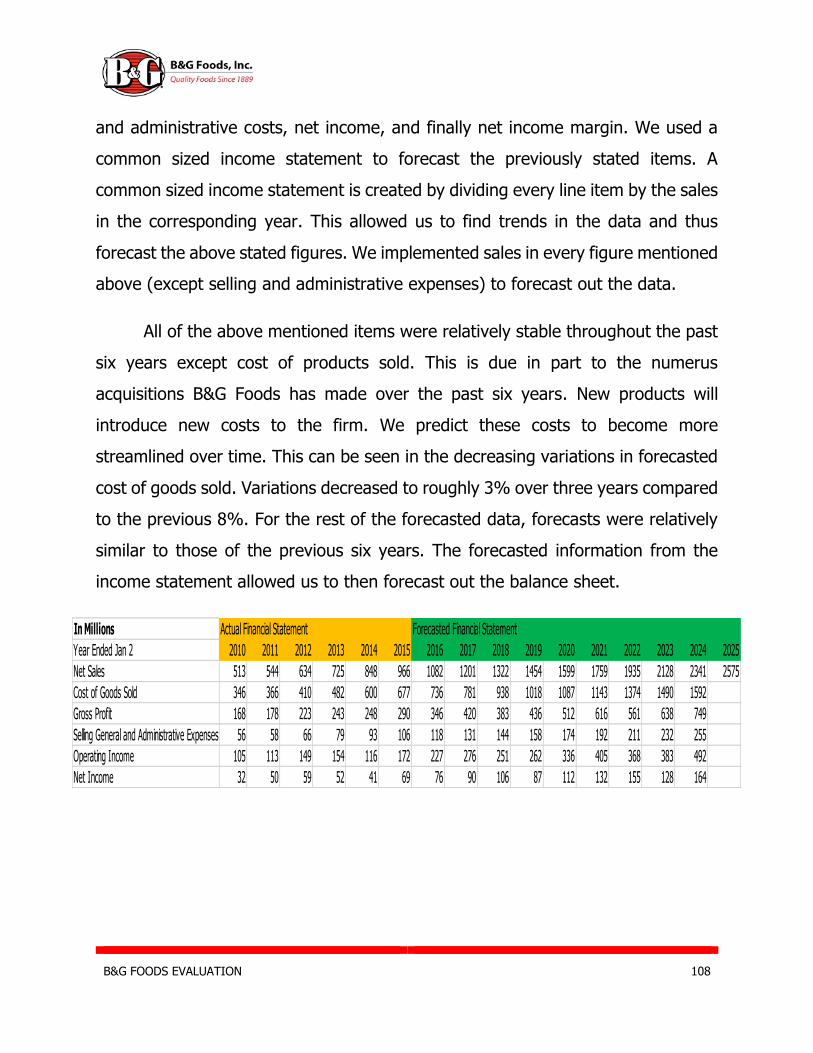

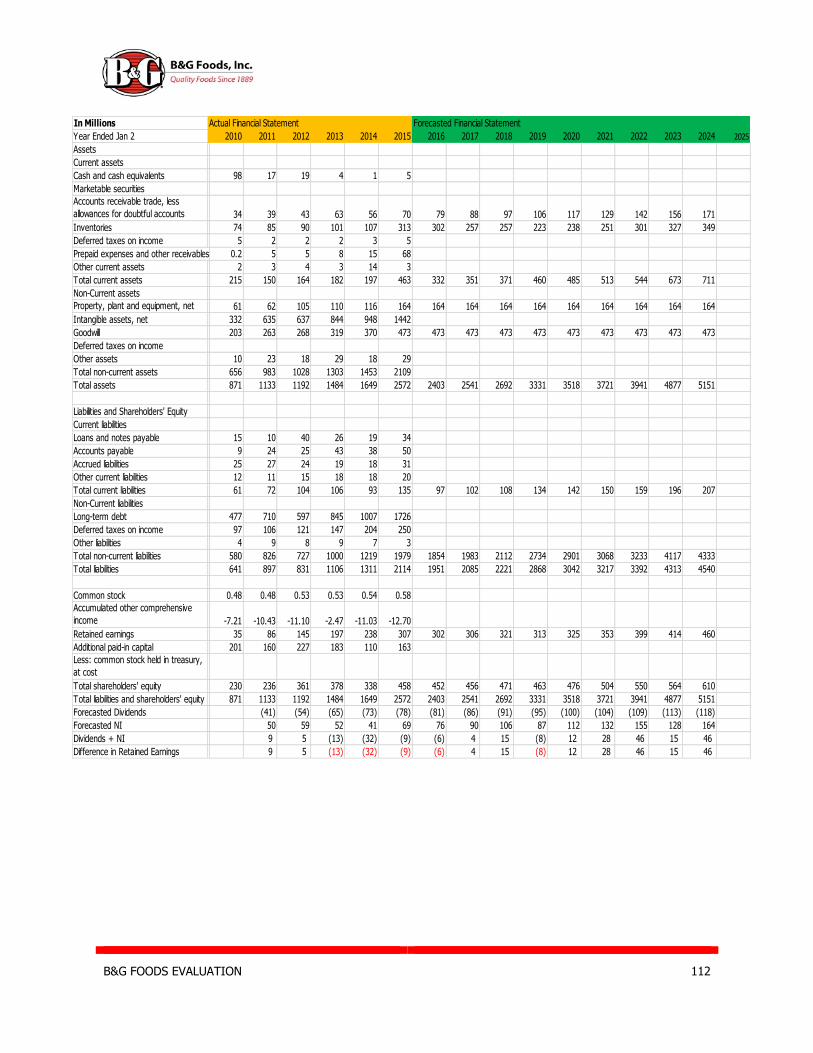

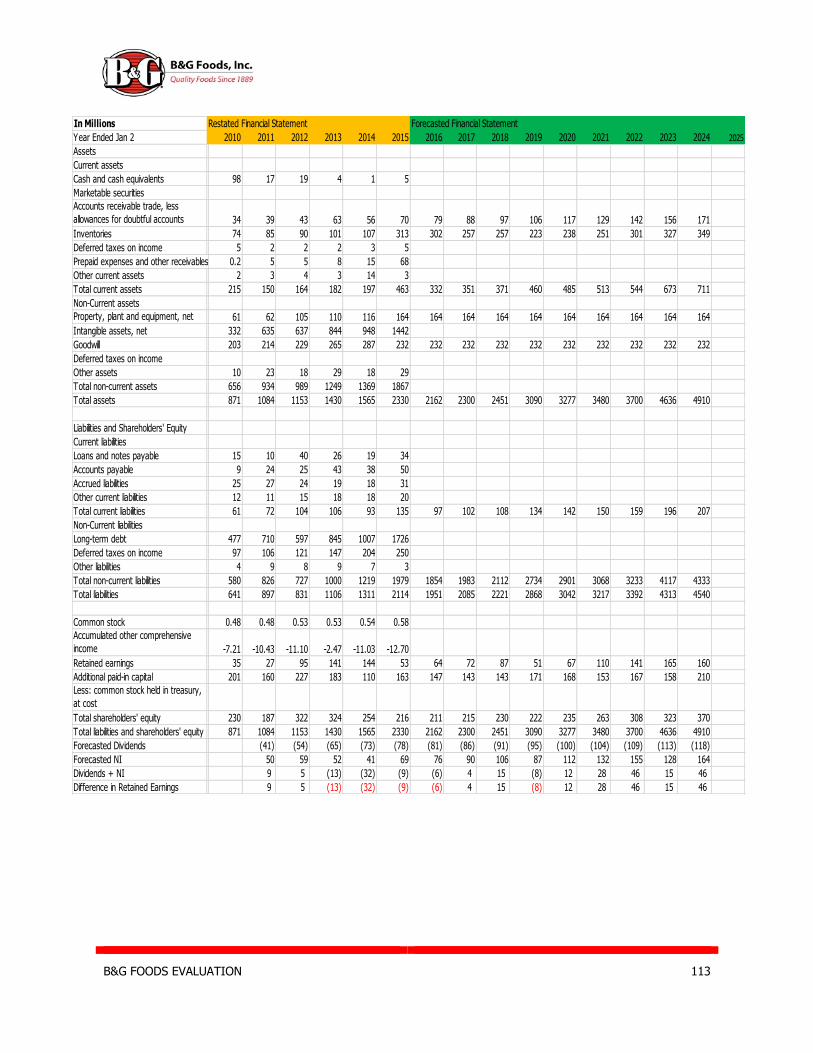

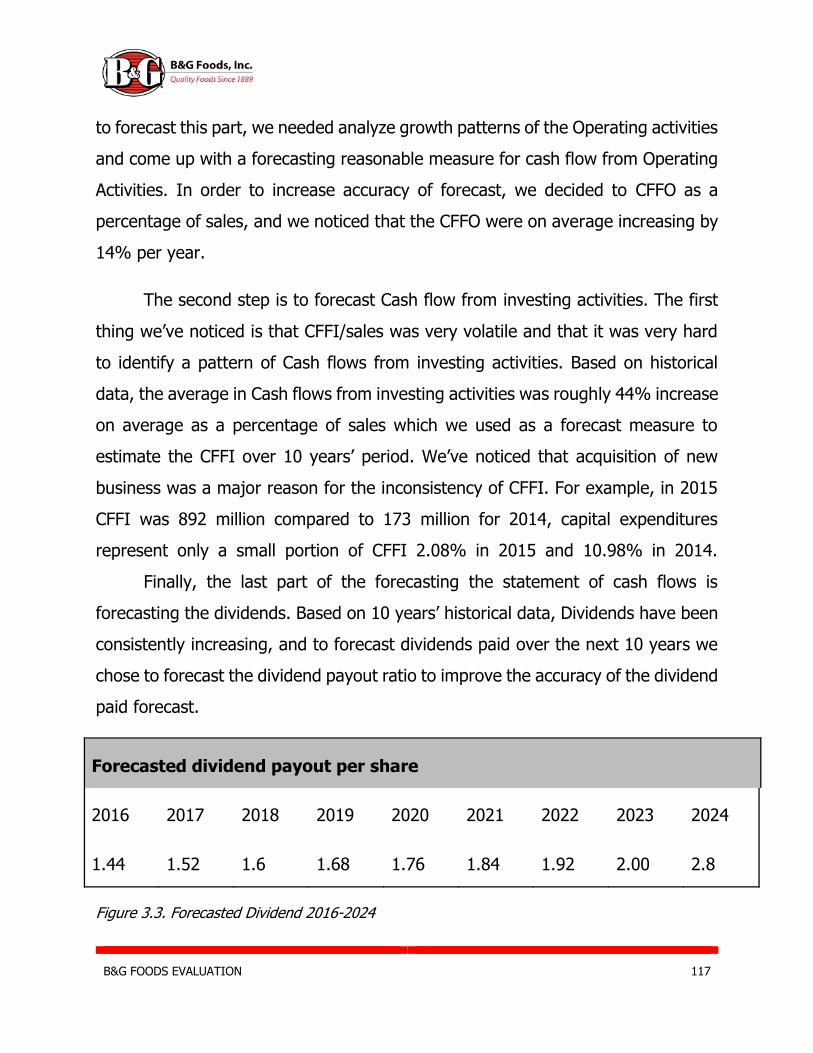

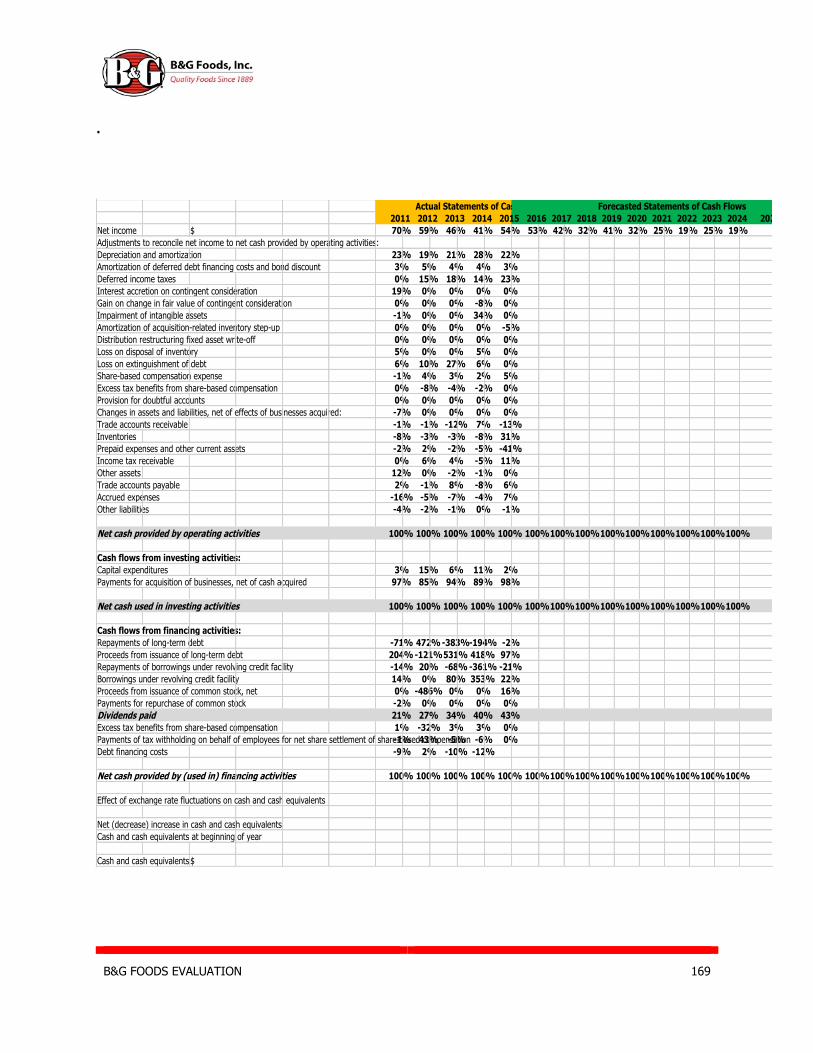

Financial Forecasting 106

Income Statement 107

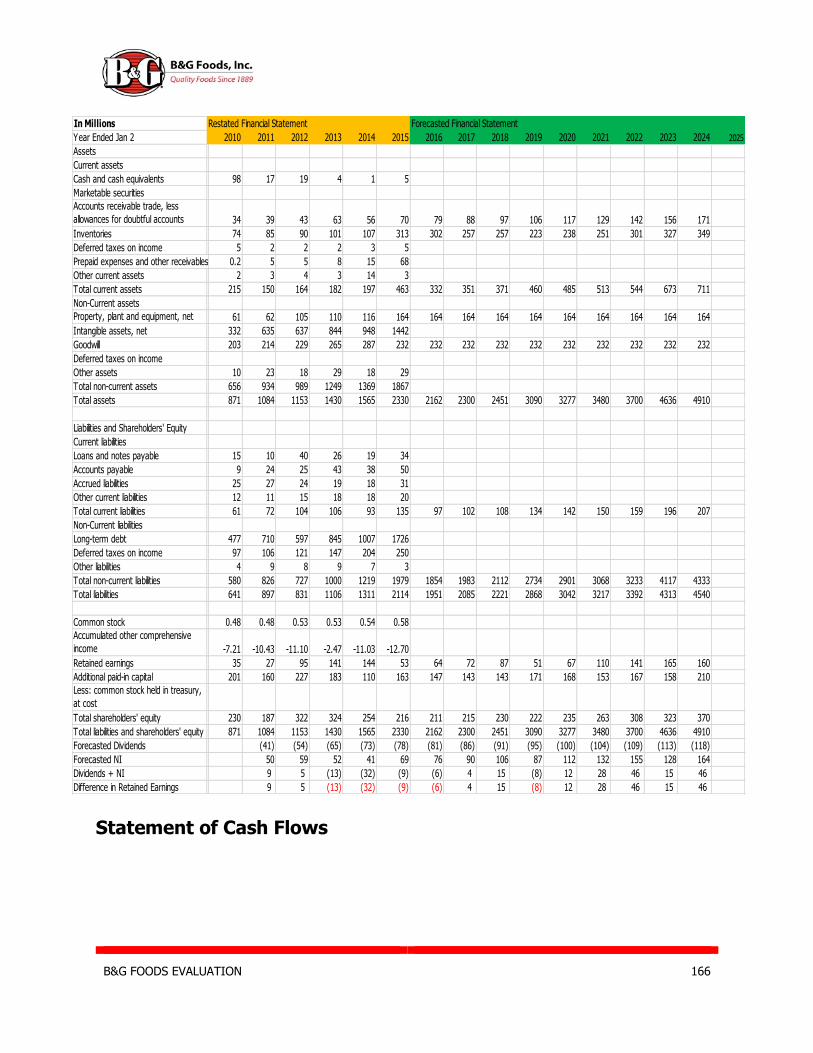

Balance Sheet 110

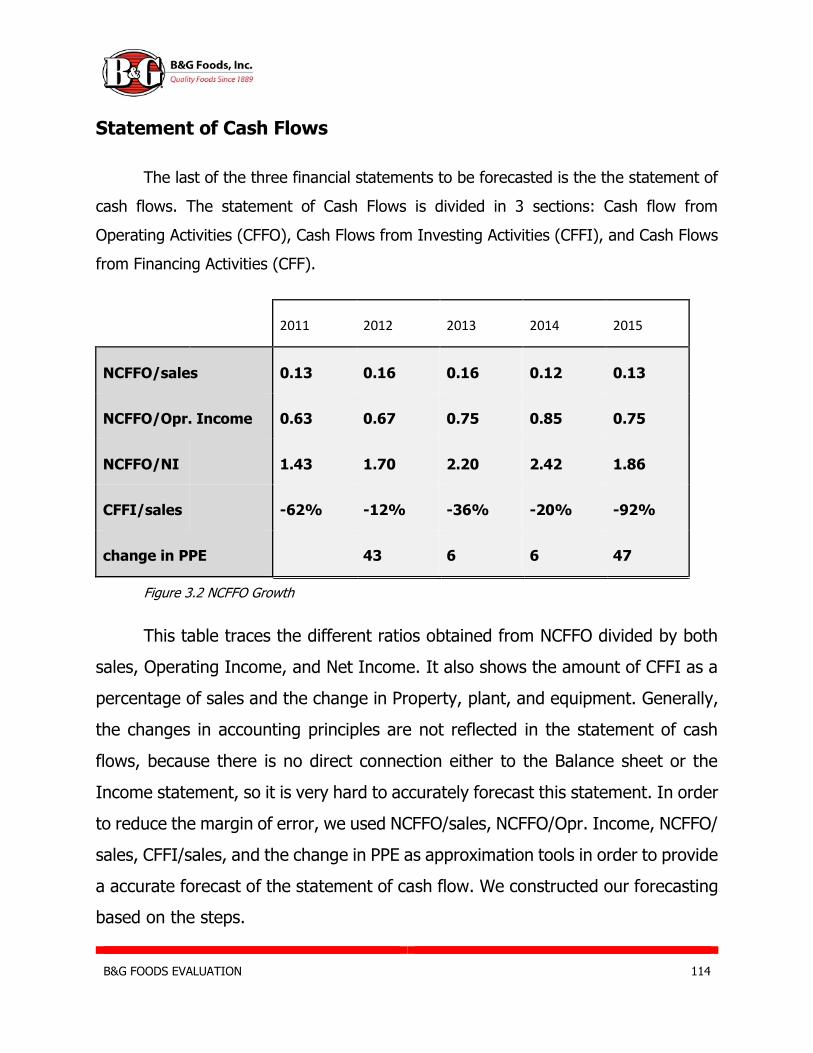

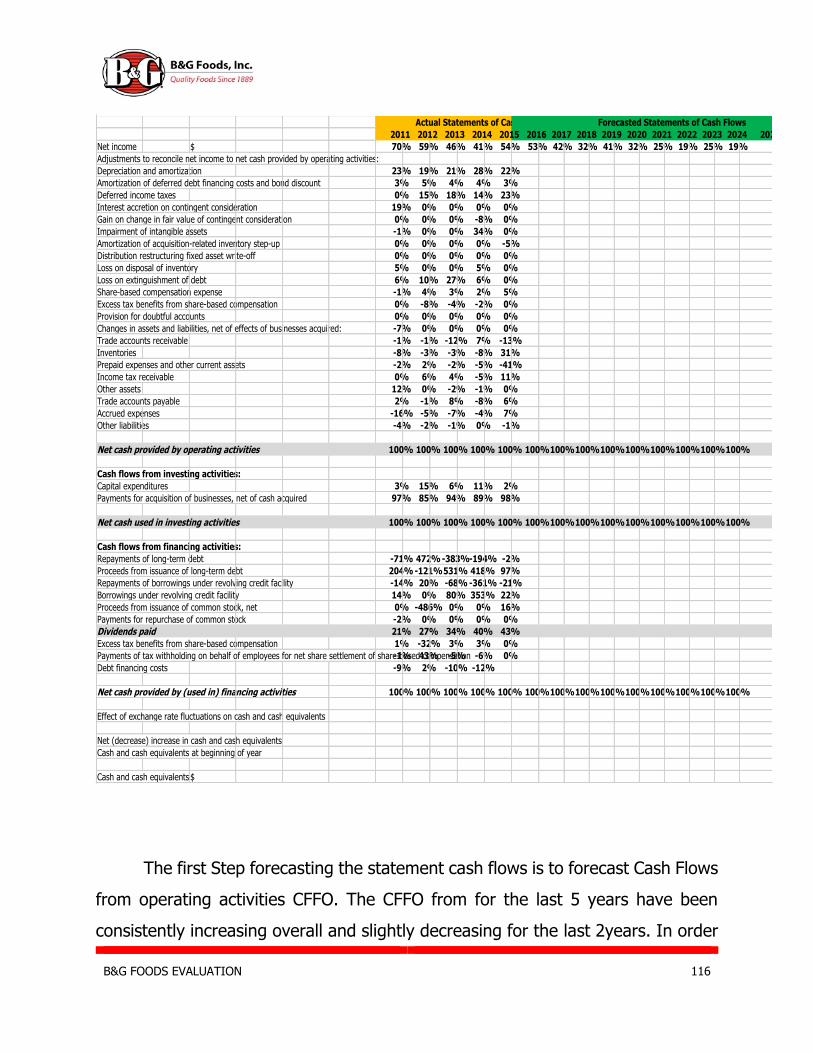

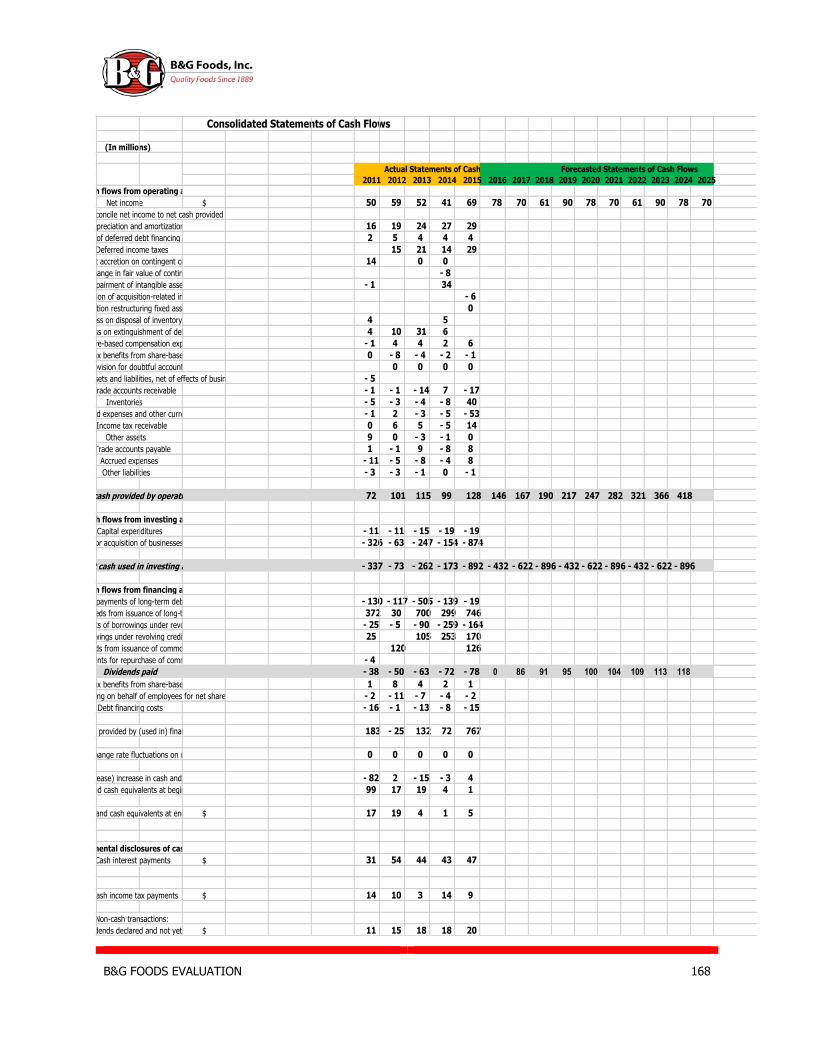

Cash Flow Statement 114

Conclusion 117

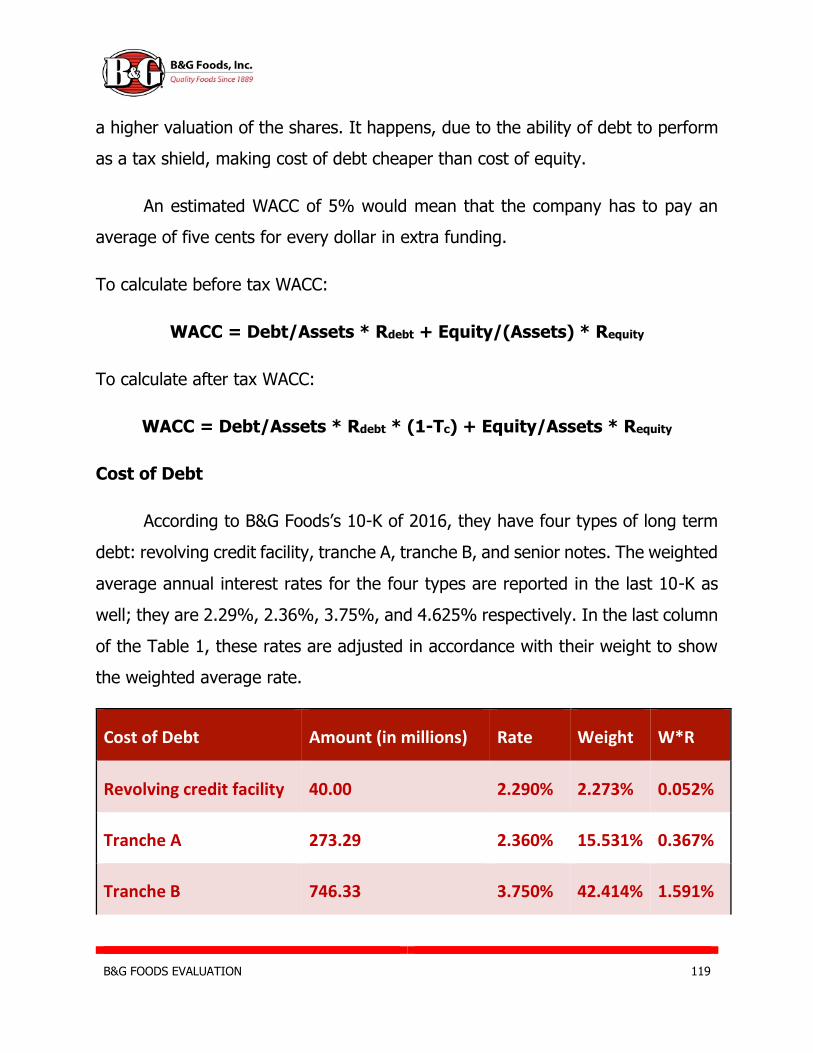

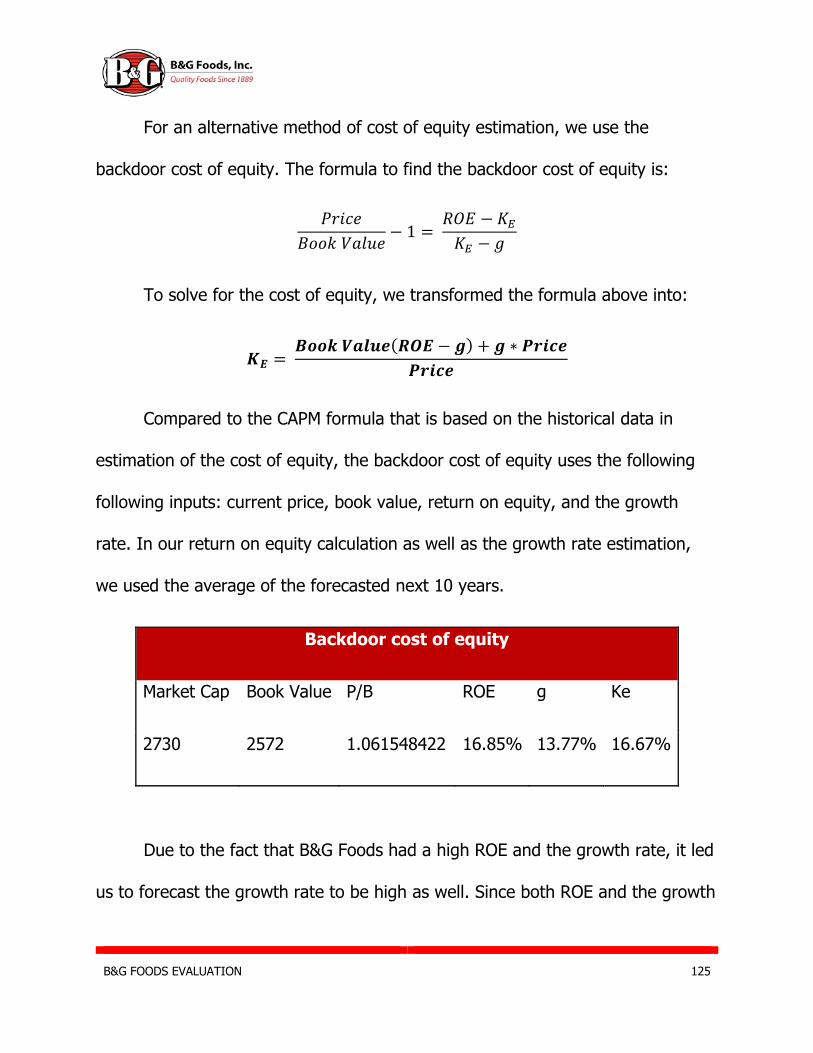

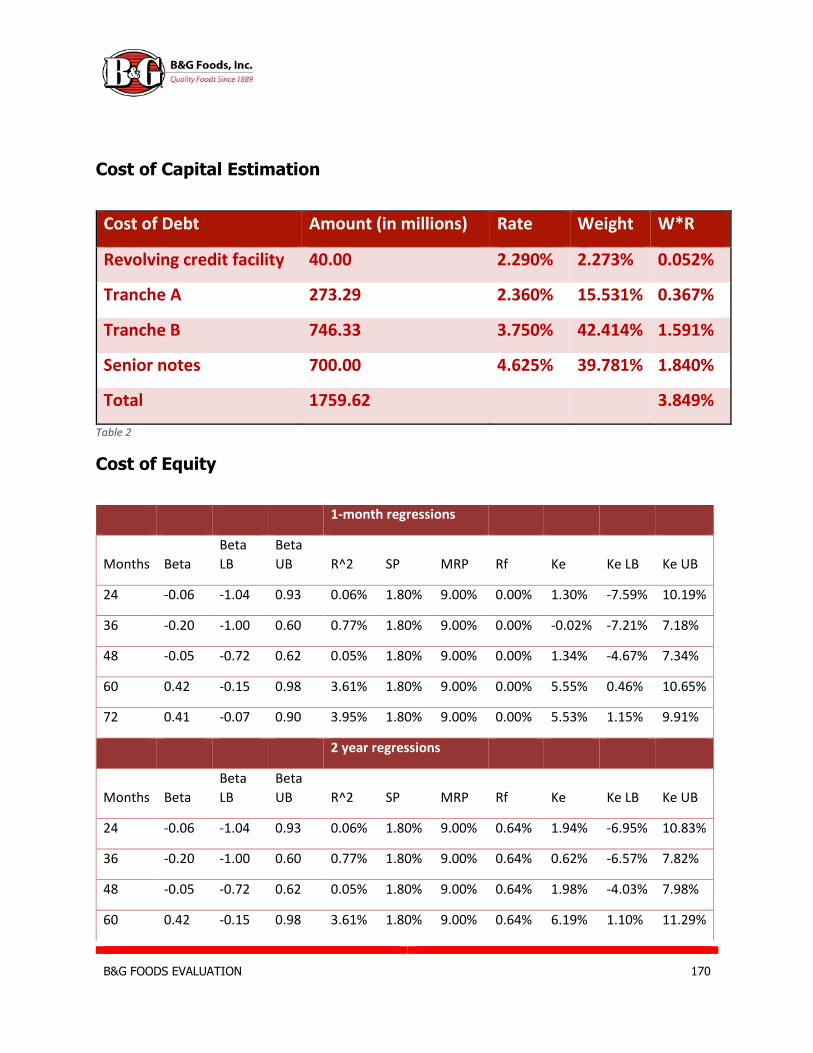

Cost of Capital Estimation 118

Cost of Debt 119

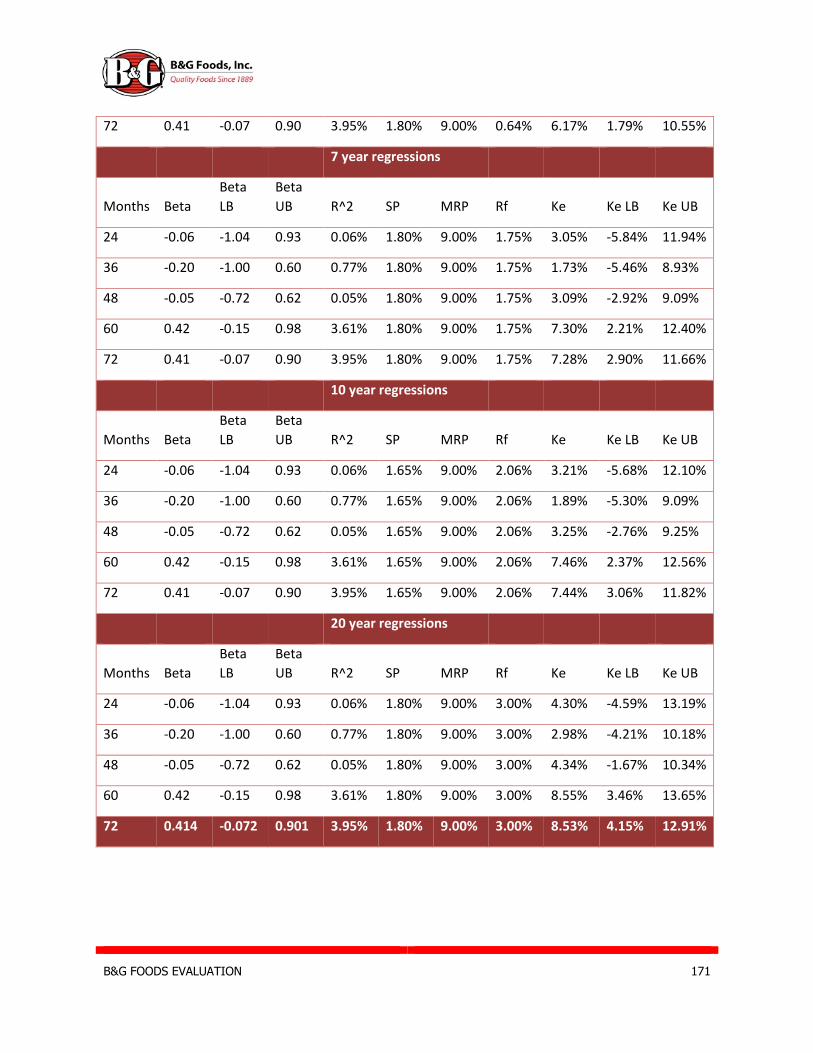

Cost of Equity 120

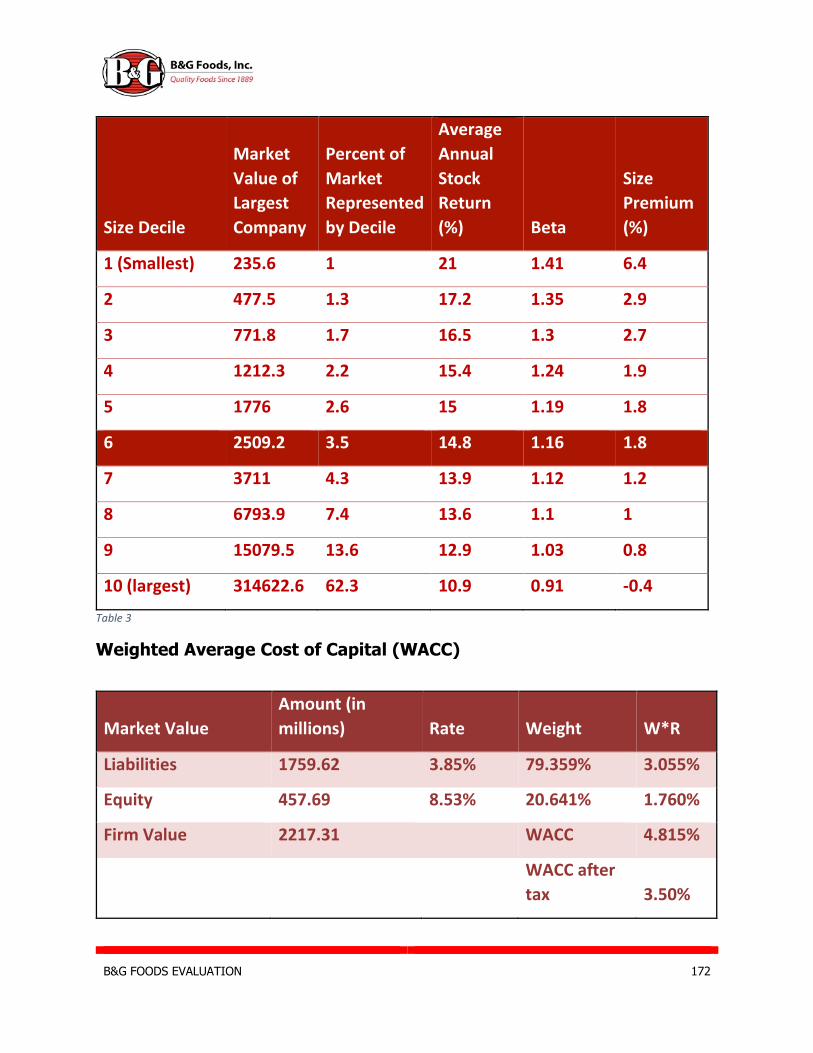

WACC 124

Conclusion 126

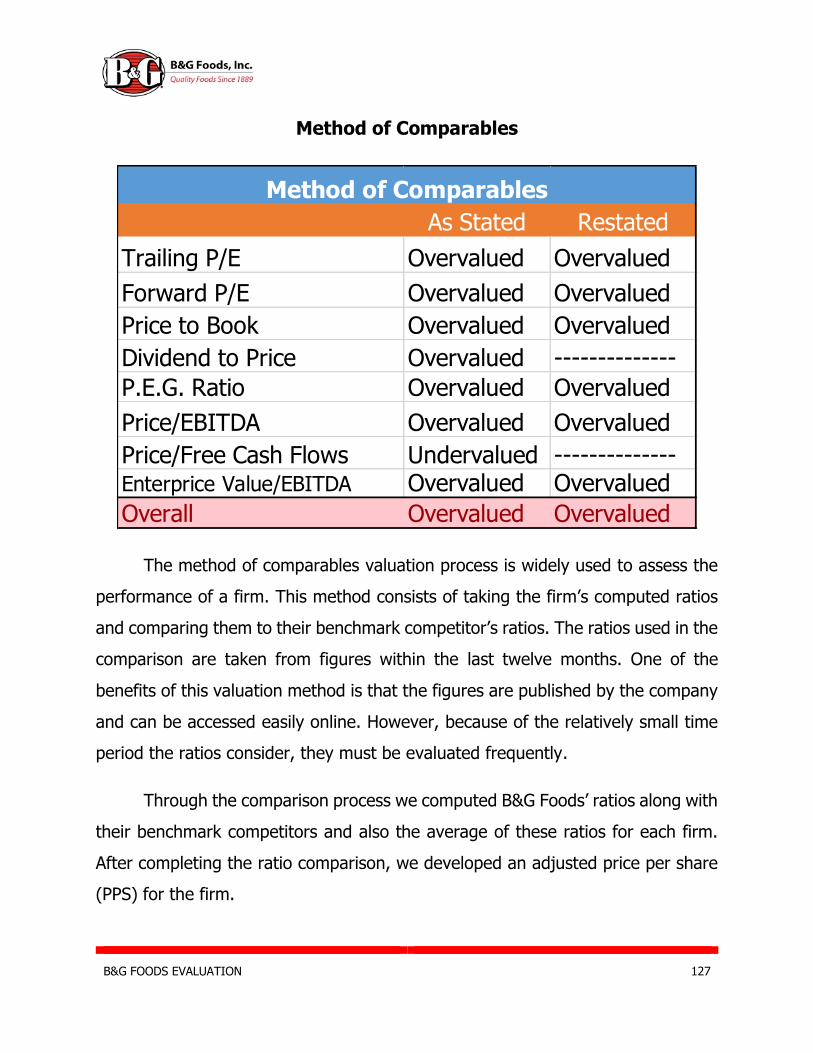

Method of Comparables 127

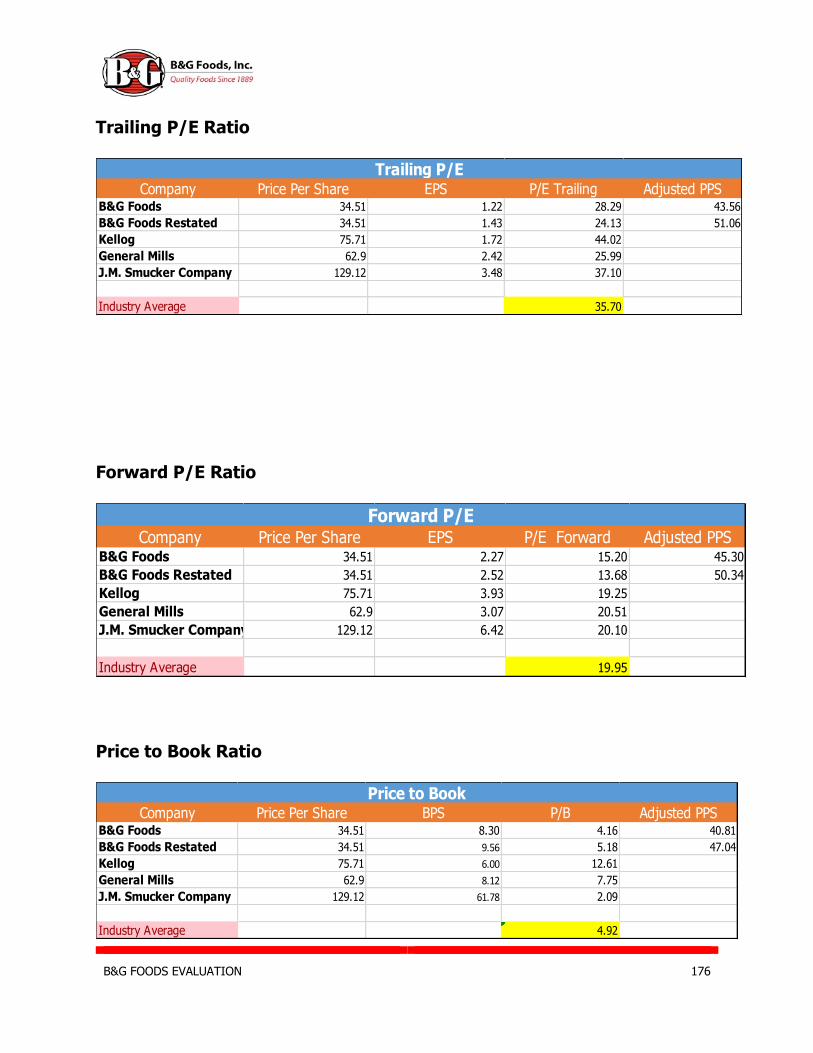

PE Ratio 128

PE Trailing Ratio 129

Price to Book 130

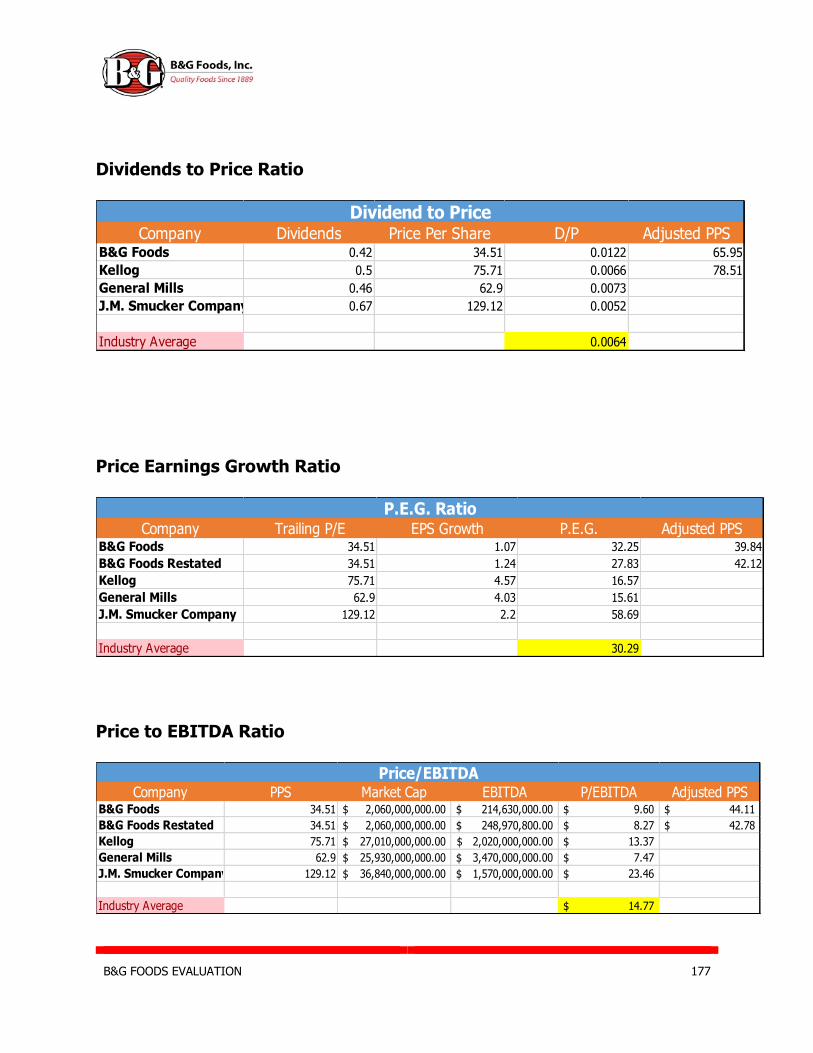

Dividend to Price 130

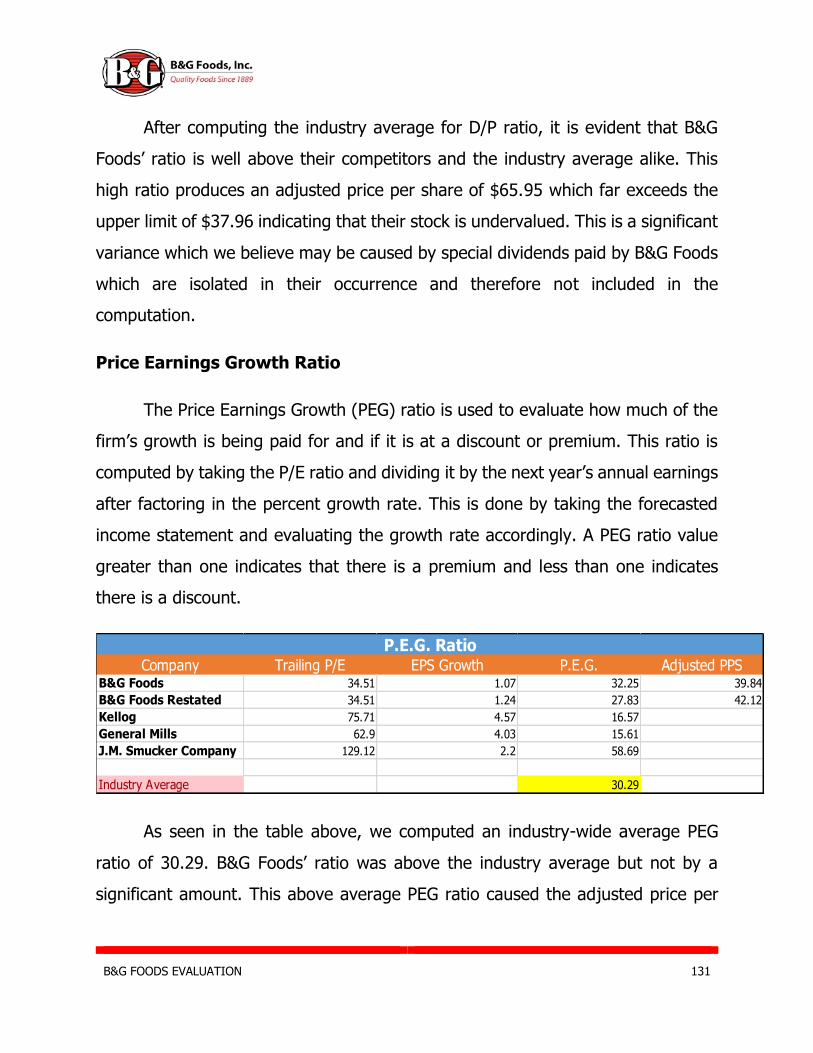

P.E.G. Ratio 131

Price to EBITDA Ratio 132

Price to Free Cash Flow Ratio 133

Enterprise Value 133

Intrinsic Valuation Methods 134

Discounted Dividends 134

B&G FOODS EVALUATION 6

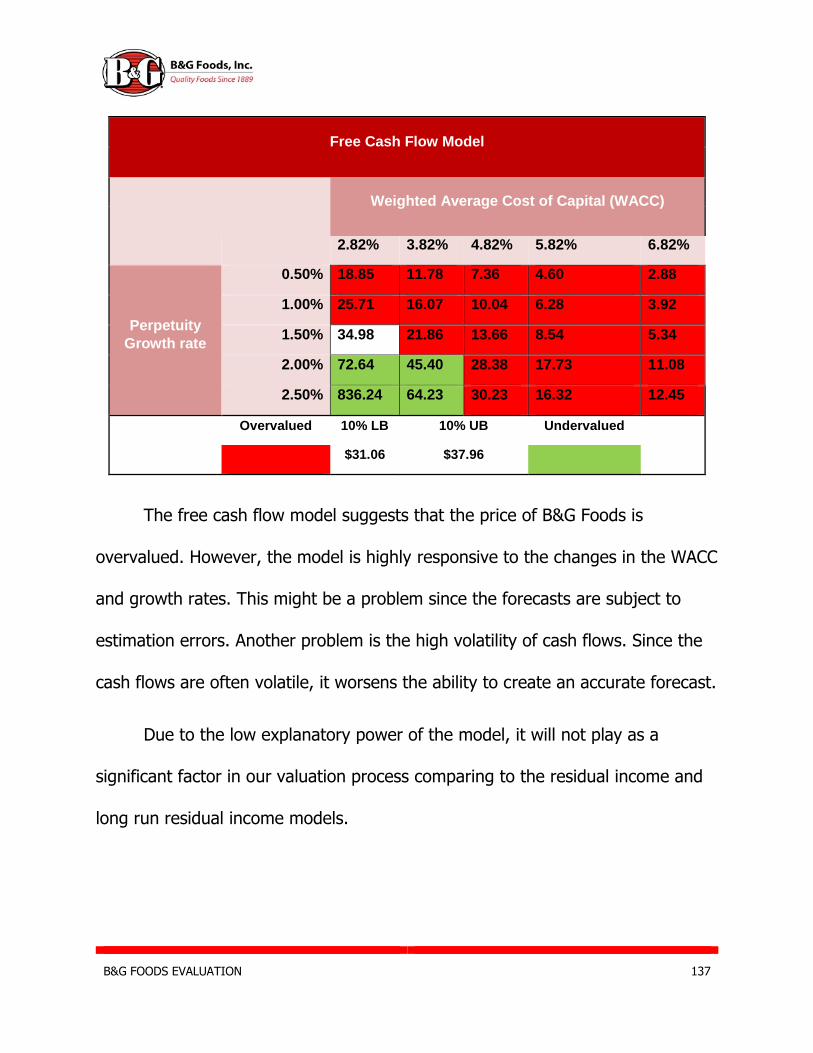

Discounted Free-Cash Flows 136

The Residual Income Method 138

Abnormal Earnings Approach 139

Residual Income Perpetuity 141

Works Cited 143

Appendix 145

B&G FOODS EVALUATION 7

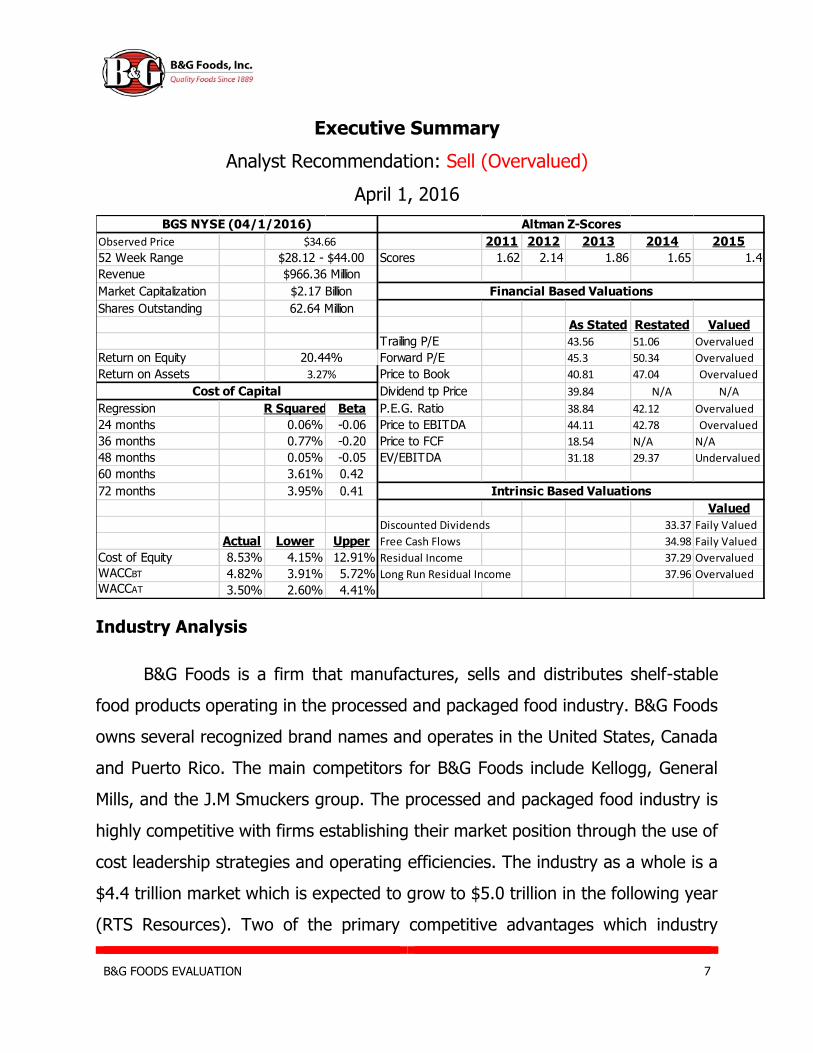

Executive Summary

Analyst Recommendation: Sell (Overvalued)

April 1, 2016

Industry Analysis

B&G Foods is a firm that manufactures, sells and distributes shelf-stable

food products operating in the processed and packaged food industry. B&G Foods

owns several recognized brand names and operates in the United States, Canada

and Puerto Rico. The main competitors for B&G Foods include Kellogg, General

Mills, and the J.M Smuckers group. The processed and packaged food industry is

highly competitive with firms establishing their market position through the use of

cost leadership strategies and operating efficiencies. The industry as a whole is a

$4.4 trillion market which is expected to grow to $5.0 trillion in the following year

(RTS Resources). Two of the primary competitive advantages which industry

Observed Price 2011 2012 2013 2014 2015

52 Week Range Scores 1.62 2.14 1.86 1.65 1.4

Revenue

Market Capitalization

Shares Outstanding

As Stated Restated Valued

Trailing P/E 43.56 51.06 Overvalued

Return on Equity Forward P/E 45.3 50.34 Overvalued

Return on Assets Price to Book 40.81 47.04 Overvalued

Dividend tp Price 39.84 N/A N/A

Regression R Squared Beta P.E.G. Ratio 38.84 42.12 Overvalued

24 months 0.06% -0.06 Price to EBITDA 44.11 42.78 Overvalued

36 months 0.77% -0.20 Price to FCF 18.54 N/A N/A

48 months 0.05% -0.05 EV/EBITDA 31.18 29.37 Undervalued

60 months 3.61% 0.42

72 months 3.95% 0.41

Valued

33.37 Faily Valued

Actual Lower Upper Free Cash Flows 34.98 Faily Valued

Cost of Equity 8.53% 4.15% 12.91% Residual Income 37.29 Overvalued

WACCBT 4.82% 3.91% 5.72% 37.96 OvervaluedWACCAT 3.50% 2.60% 4.41%

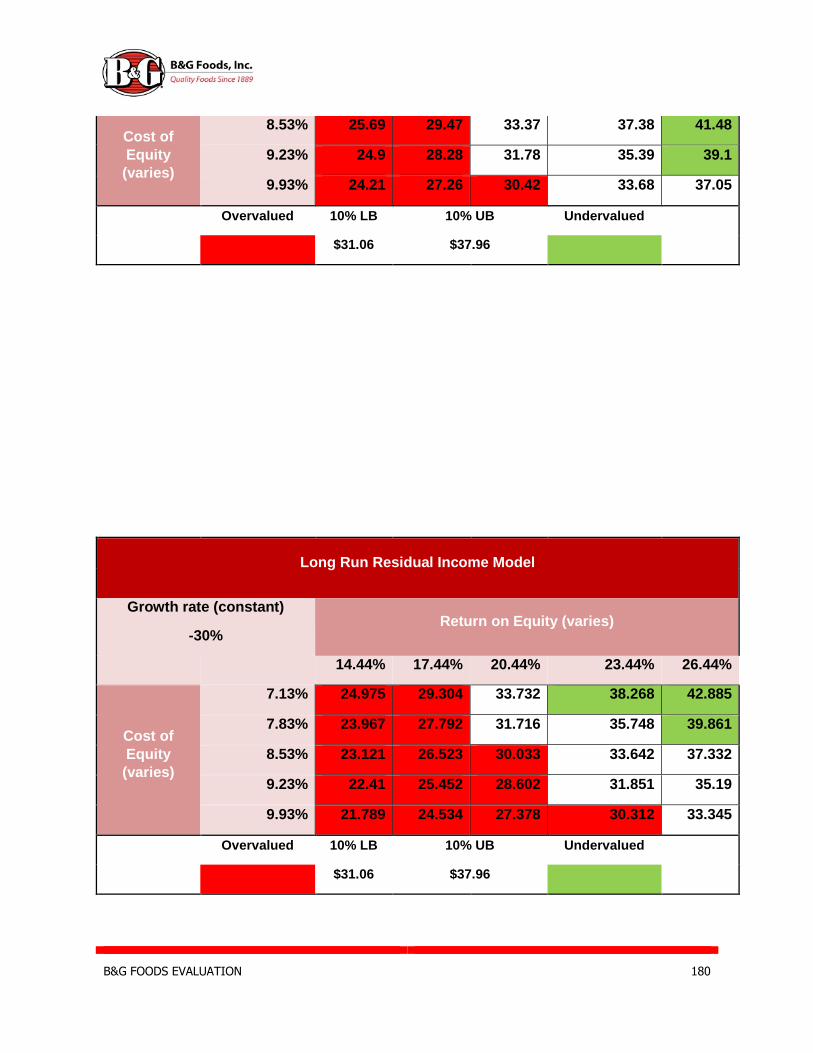

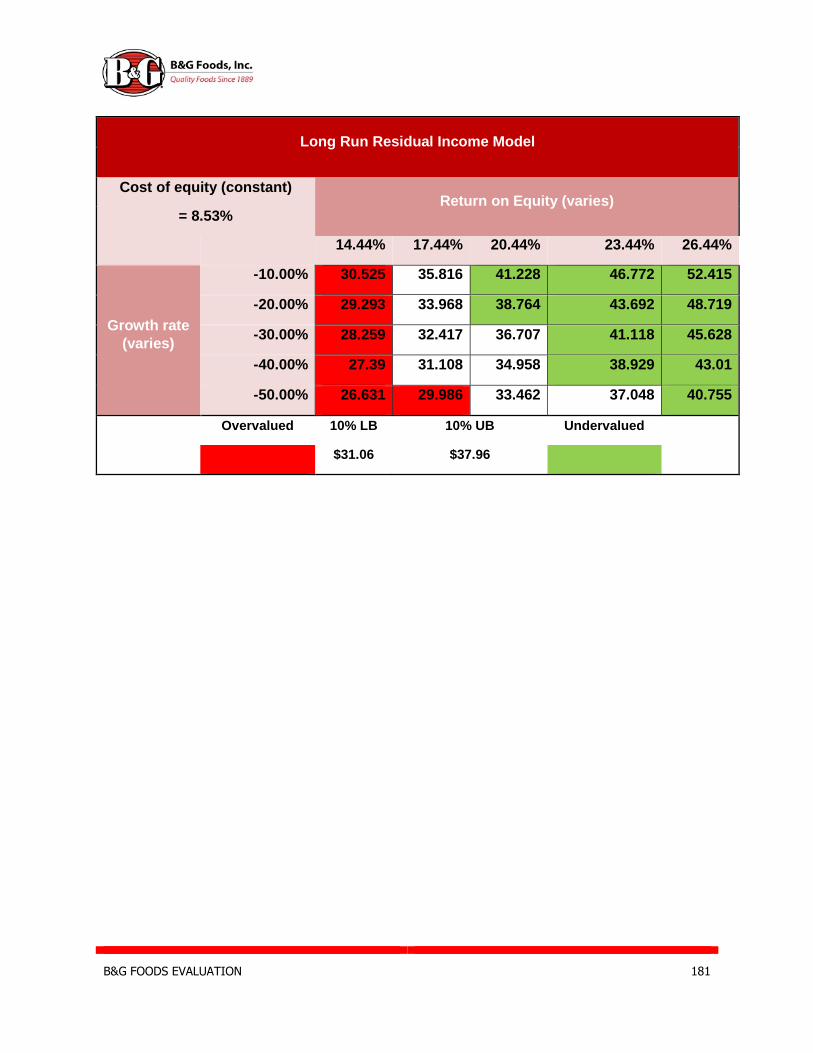

Long Run Residual Income

Discounted Dividends

Intrinsic Based Valuations

BGS NYSE (04/1/2016) Altman Z-Scores

$34.66

Financial Based Valuations

Cost of Capital

$28.12 - $44.00

$2.17 Billion

62.64 Million

$966.36 Million

20.44%

3.27%

B&G FOODS EVALUATION 8

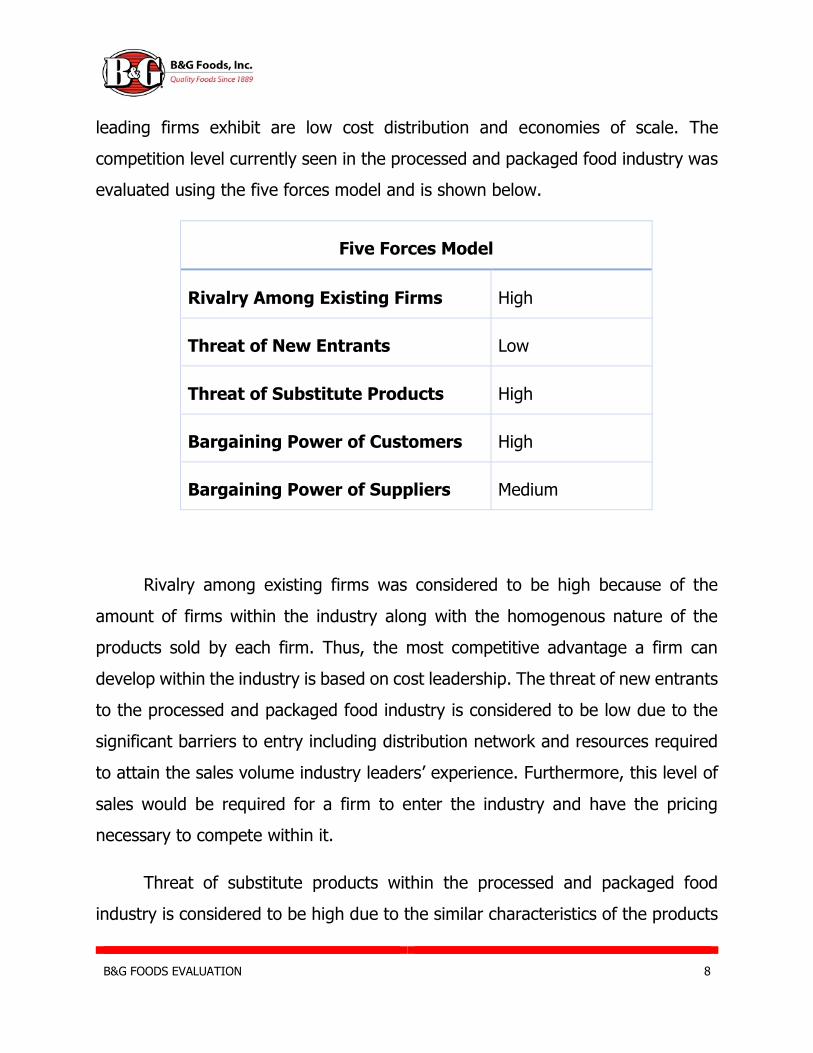

leading firms exhibit are low cost distribution and economies of scale. The

competition level currently seen in the processed and packaged food industry was

evaluated using the five forces model and is shown below.

Five Forces Model

Rivalry Among Existing Firms High

Threat of New Entrants Low

Threat of Substitute Products High

Bargaining Power of Customers High

Bargaining Power of Suppliers Medium

Rivalry among existing firms was considered to be high because of the

amount of firms within the industry along with the homogenous nature of the

products sold by each firm. Thus, the most competitive advantage a firm can

develop within the industry is based on cost leadership. The threat of new entrants

to the processed and packaged food industry is considered to be low due to the

significant barriers to entry including distribution network and resources required

to attain the sales volume industry leaders’ experience. Furthermore, this level of

sales would be required for a firm to enter the industry and have the pricing

necessary to compete within it.

Threat of substitute products within the processed and packaged food

industry is considered to be high due to the similar characteristics of the products

B&G FOODS EVALUATION 9

sold by firms. The synonymous nature of the products sold in this industry causes

the customer to seek out the lowest pricing rather than selecting a product based

on brand loyalty. Bargaining power of customers was found to be high within this

industry because of the similarity of products leading to a high availability of

substitute products. The bargaining power of the supplier is regarded as medium

primarily because of the differentiation present in the industry. Suppliers with a

larger network of clients are able to employ higher quality and lower distribution

costs therefore implementing cost leadership strategies.

After evaluating the five forces model, cost leadership proved to be the most

significant competitive advantage present in the industry. These cost leadership

strategies are achieved through the use of low cost distribution, economies of scale

and inventory management.

Accounting Analysis

In order to find the value of a company, it is necessary to look at key accounting

policies and how they affect the overall financials of the firm. Variability exists in

the reporting of key accounting policies as the Generally Accepted Accounting

Policies allows for it. This can drastically affect how a firm is valued and thus,

whether it is over or undervalued.

The amount a firm discloses in its financial reporting affects how assuredly a firm

can be accurately valued. By evaluating B&G Foods type 1 accounting policies, the

key success factors of the industry, and type 2 accounting policies, regarding

operating leases, we were able to determine possible red flag accounting policies

that could affect B&G Foods’ valuation.

B&G FOODS EVALUATION 10

Type 1 accounting policies dealt with the key success factors of firms in the

industry. B&G Foods has good disclosure of type 1 accounting policies in that they

meet or exceed the industry standard in information reported. Type 2 accounting

policies dealt with the disclosure of operating lease structures. B&G Foods had a

substantial amount of goodwill when compared to net fixed assets, which was thus

analyzed further for distortion. We found that B&G Foods’ goodwill needed to be

restated to accurately value the company. Overall, B&G Foods had a relatively low

amount of disclosure related to type 2 accounting policies.

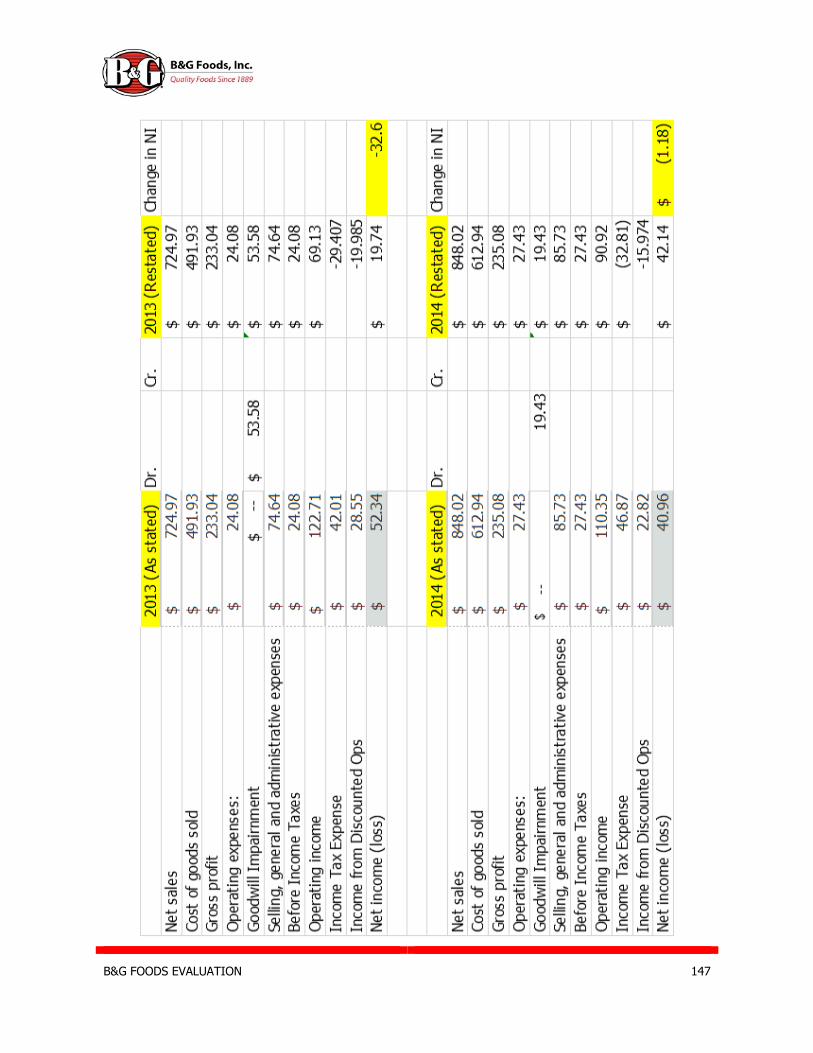

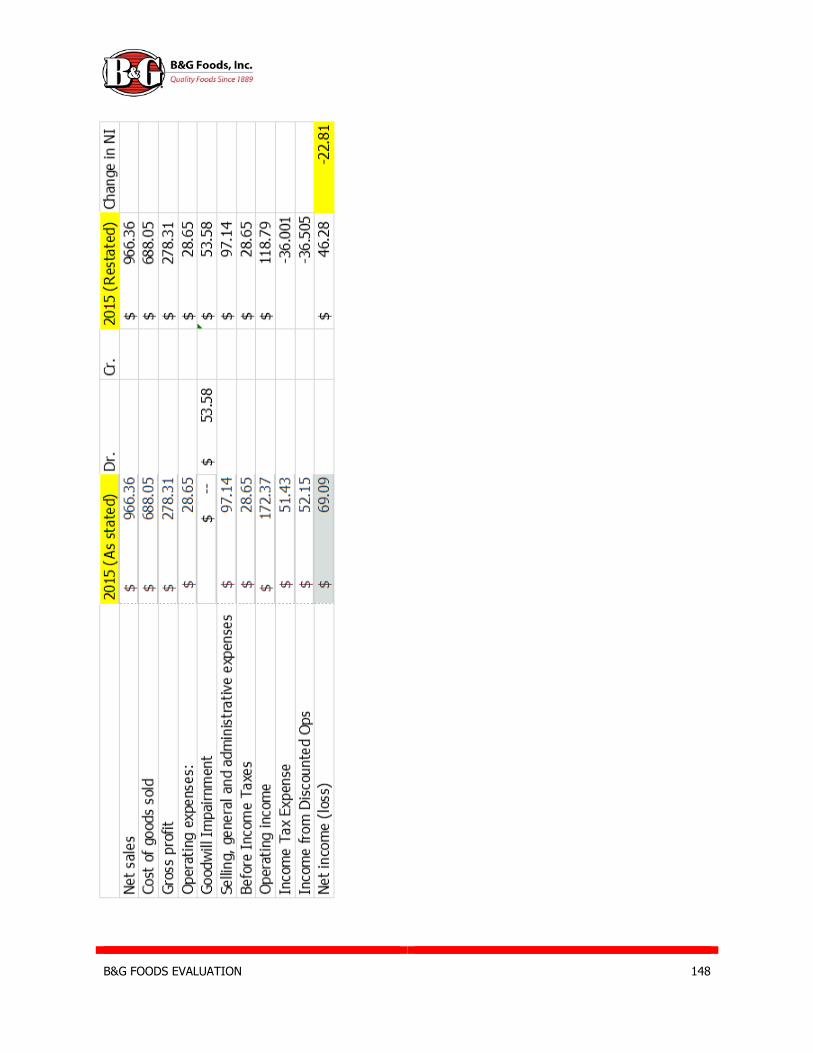

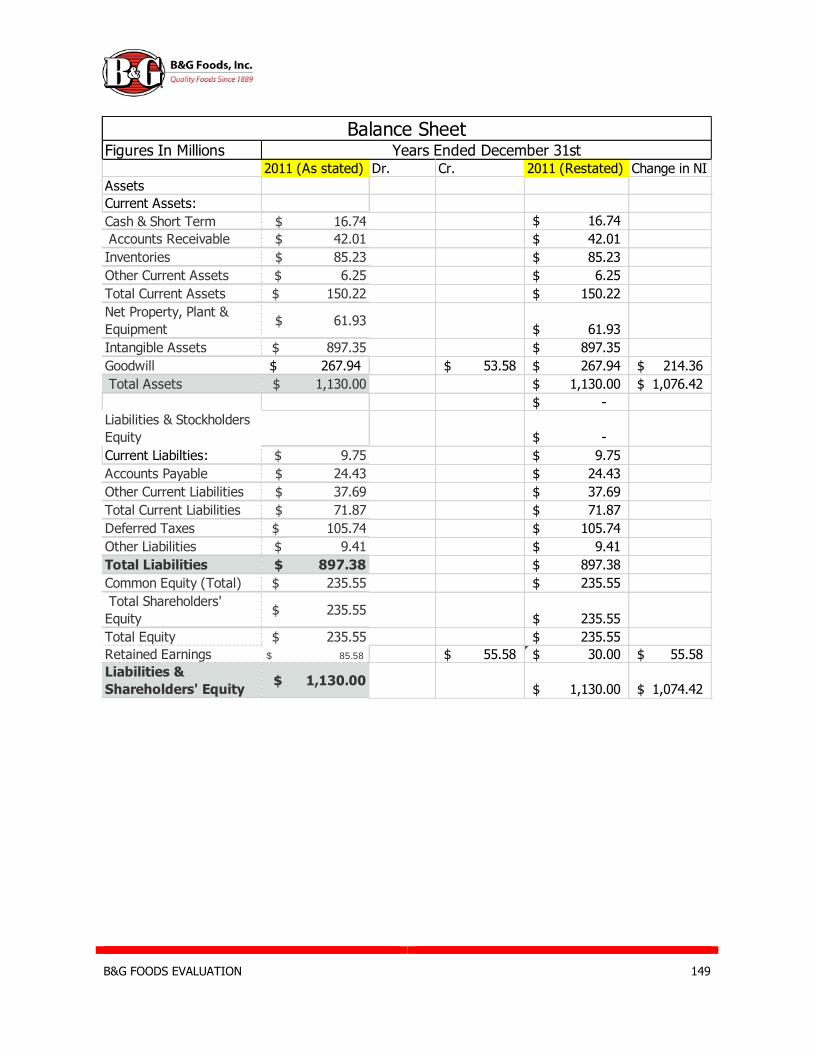

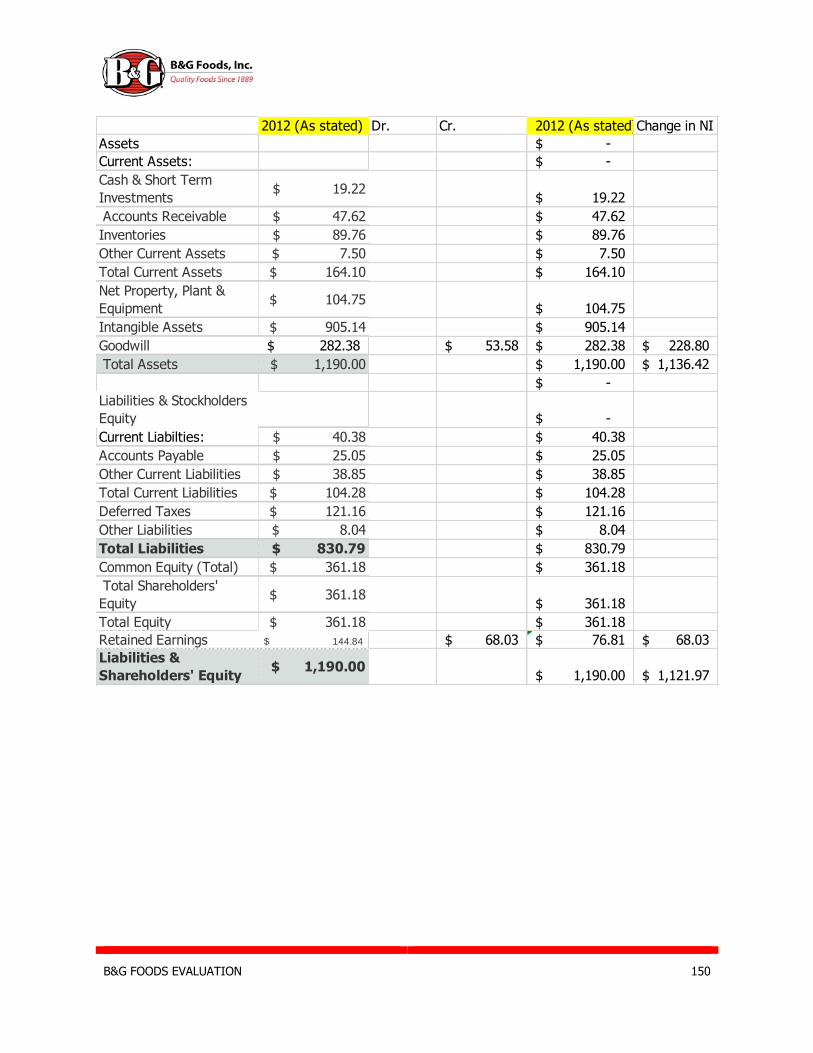

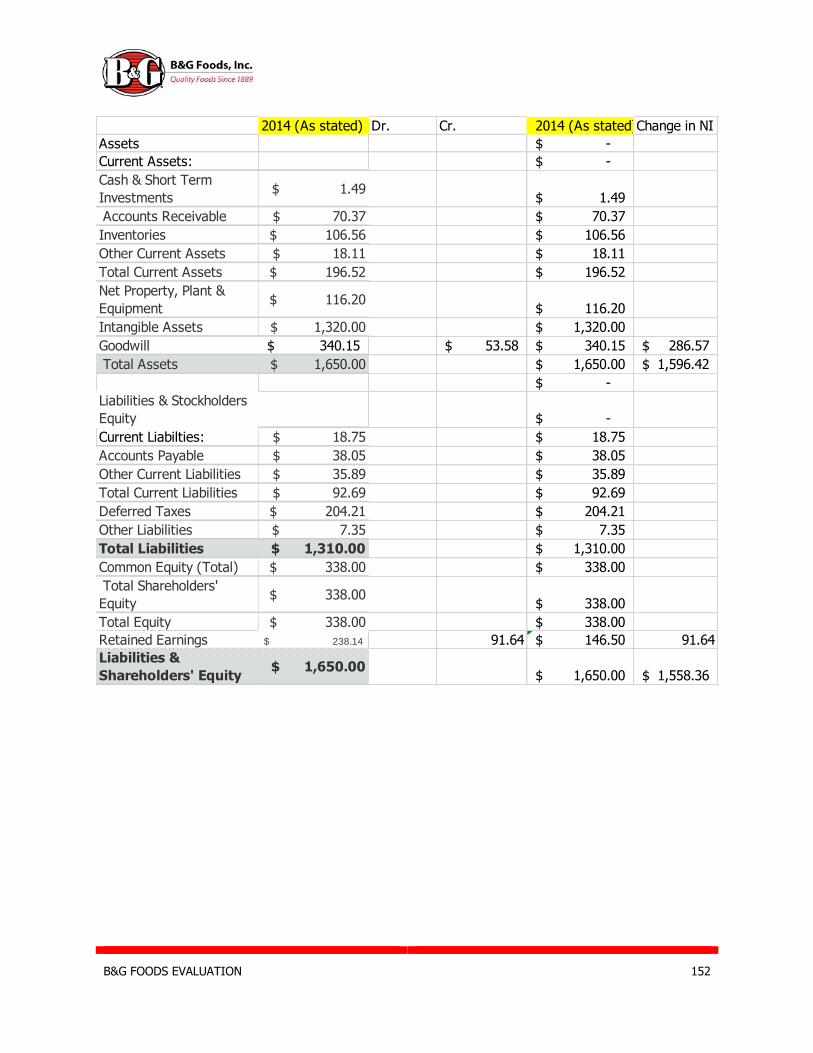

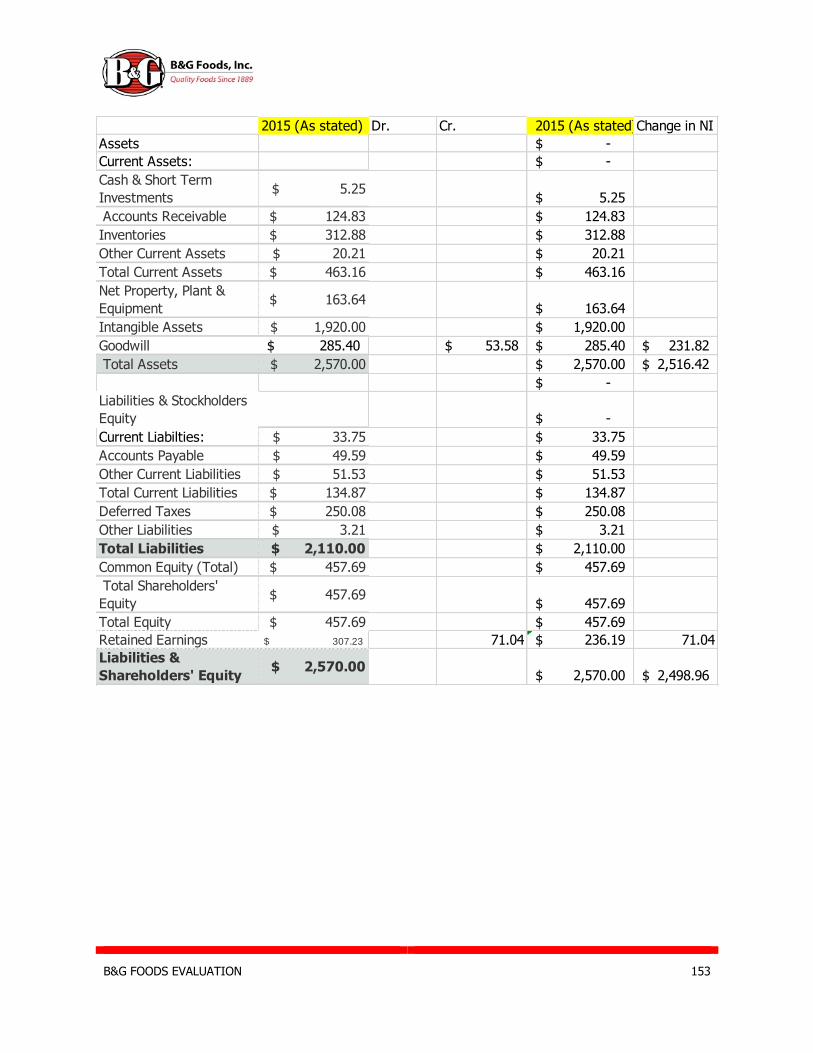

Since goodwill is over 20% of net fixed assets, we had to restate the

financials to accurately display goodwill. In order to do so, we amortized goodwill

over a five year period. By doing so, we were able to restate the goodwill later in

the report, leading to higher disclosure allowing us to more accurately value the

firm. Due to the lack of financial disclosure in type 2 accounting policies, we found

that we could not accurately value B&G Foods. Therefore, it was necessary to

restate the financial statements to find an accurate valuation of the company.

Financial Analysis

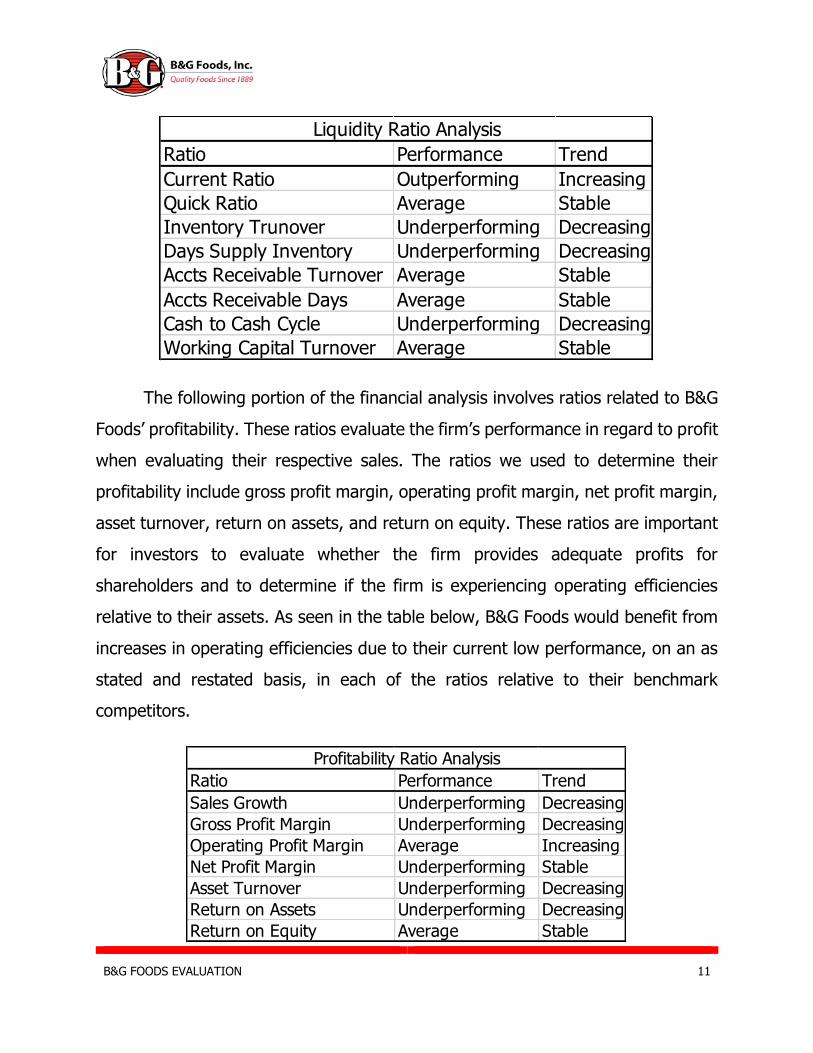

Conducting a financial analysis of a firm consists of evaluating their liquidity,

profitability and capital structure ratios in order to assess their performance

relative to their benchmark competitors. Liquidity ratios are used to determine a

firm’s ability to repay their obligations in case they experience an unfavorable

economic event. The liquidity ratios we used include the quick asset, current,

inventory turnover, accounts receivable turnover, days’ supply inventory, accounts

receivable days, cash to cash cycle, and working capital turnover. Below is a table

listing B&G Foods’ standing in each of the liquidity ratios along with their relative

competitors.

B&G FOODS EVALUATION 11

The following portion of the financial analysis involves ratios related to B&G

Foods’ profitability. These ratios evaluate the firm’s performance in regard to profit

when evaluating their respective sales. The ratios we used to determine their

profitability include gross profit margin, operating profit margin, net profit margin,

asset turnover, return on assets, and return on equity. These ratios are important

for investors to evaluate whether the firm provides adequate profits for

shareholders and to determine if the firm is experiencing operating efficiencies

relative to their assets. As seen in the table below, B&G Foods would benefit from

increases in operating efficiencies due to their current low performance, on an as

stated and restated basis, in each of the ratios relative to their benchmark

competitors.

Ratio Performance Trend

Current Ratio Outperforming Increasing

Quick Ratio Average Stable

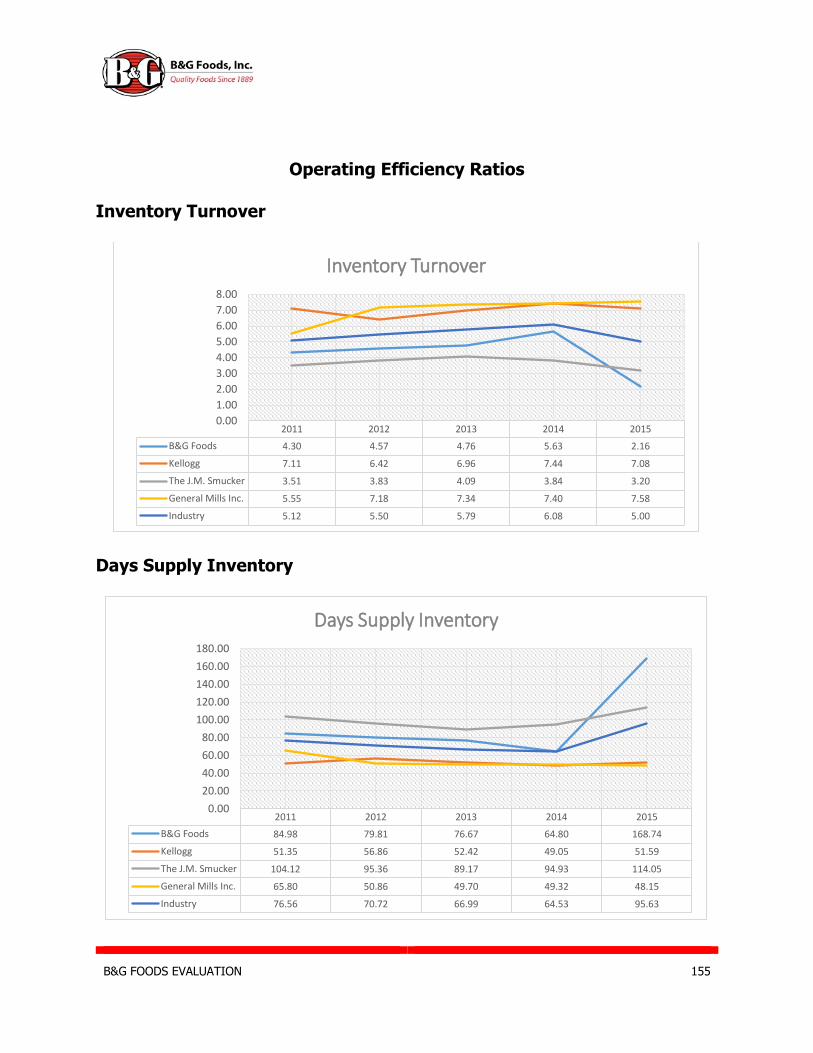

Inventory Trunover Underperforming Decreasing

Days Supply Inventory Underperforming Decreasing

Accts Receivable Turnover Average Stable

Accts Receivable Days Average Stable

Cash to Cash Cycle Underperforming Decreasing

Working Capital Turnover Average Stable

Liquidity Ratio Analysis

Ratio Performance Trend

Sales Growth Underperforming Decreasing

Gross Profit Margin Underperforming Decreasing

Operating Profit Margin Average Increasing

Net Profit Margin Underperforming Stable

Asset Turnover Underperforming Decreasing

Return on Assets Underperforming Decreasing

Return on Equity Average Stable

Profitability Ratio Analysis

B&G FOODS EVALUATION 12

The final step in completing the financial analysis for B&G Foods involves

evaluating how the firm finances their assets. This portion of the financial analysis

is used to see what mix of debt financing and equity financing the firm is currently

using. The ratios we used to evaluate B&G Foods’ capital structure include debt to

equity, times interest earned and Altman’s Z-Score. Debt financing is considered

to be riskier for a firm due to the pressure to meet interest payments and avoid

bankruptcy. The Altman’s Z-Score is used to determine a firm’s bankruptcy

likelihood. Scores below 1.8 indicate the firm is likely to experience bankruptcy,

and scores above 3.0 indicate that the firm is unlikely to face bankruptcy. As seen

below, B&G Foods has historically maintained a low Altman Z-Score and also seems

to be underperforming their benchmark competitors in some of these capital

structure metrics.

Valuation Analysis

In order to conduct the valuation analysis two major valuation methods are

used: the method of comparables and the intrinsic models of valuation. The

intrinsic models of valuation are more accurate and reliable than the method of

comparables overall. Our team conducted the analysis based on the stock price on

April 1, 2016; its price at the moment was $34.66 per share. The method of

comparables consists of 8 different processes (shown in the following table) with

Ratio Performance Trend

Debt to Equity Average Increasing

Times Interest Earned Underperforming Stable

Altman's Z-Score Underperforming Stable

Capital Structure Ratio Analysis

B&G FOODS EVALUATION 13

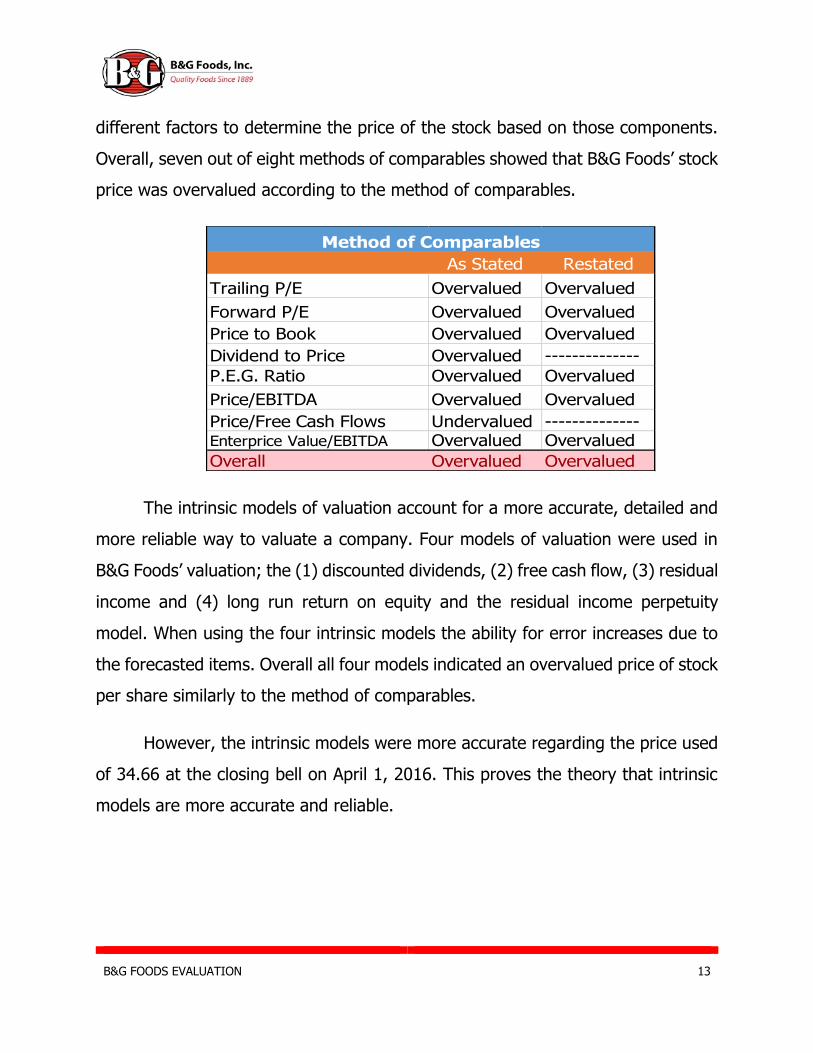

different factors to determine the price of the stock based on those components.

Overall, seven out of eight methods of comparables showed that B&G Foods’ stock

price was overvalued according to the method of comparables.

The intrinsic models of valuation account for a more accurate, detailed and

more reliable way to valuate a company. Four models of valuation were used in

B&G Foods’ valuation; the (1) discounted dividends, (2) free cash flow, (3) residual

income and (4) long run return on equity and the residual income perpetuity

model. When using the four intrinsic models the ability for error increases due to

the forecasted items. Overall all four models indicated an overvalued price of stock

per share similarly to the method of comparables.

However, the intrinsic models were more accurate regarding the price used

of 34.66 at the closing bell on April 1, 2016. This proves the theory that intrinsic

models are more accurate and reliable.

As Stated Restated

Trailing P/E Overvalued Overvalued

Forward P/E Overvalued Overvalued

Price to Book Overvalued Overvalued

Dividend to Price Overvalued --------------

P.E.G. Ratio Overvalued Overvalued

Price/EBITDA Overvalued Overvalued

Price/Free Cash Flows Undervalued --------------Enterprice Value/EBITDA Overvalued Overvalued

Overall Overvalued Overvalued

Method of Comparables

B&G FOODS EVALUATION 14

Company Overview

B&G Foods, Inc. is a parent holding company that operates as a

manufacturer, distributor, and seller of a variety of shelf-stable food products

under several recognized brand names. B&G Foods, along with its wholly owned

subsidiaries operates in the United States, Canada and Puerto Rico. B&G Foods

has been in business for over 125 years. The company originally started as a street

market in Manhattan, New York at the end of the 19th century under the

supervision of the Bloch & Guggenheimer families; that is where the actual name

is derived from (B&G). The company joined the New York Stock Exchange (NYSE)

on May 23, 2007 under the ticker “BGS,” the company is headquartered in

Parsippany, New Jersey, B&G Foods’ fiscal year ends on December 31, or the

Saturday closest. (B&G Foods 10-K.)

Business Products

According to B&G Foods the company holds 41 different food brands.

Ac’cent B&G B&M Baker’s Joy

Bear Creek Country Kitchens Brer Rabbit Canoleo

Cary’s Cream of Rice Cream of Wheat Devonsheer

Don Pepino Emeril’s Grandma’s Molasses

JJ Flats

Joan of Arc Las Palmas MacDonald’s Maple Grove Farms

Molly McButter Mrs. Dash New York Flatbreads

New York Style

Old London Original Tings Ortega Pirate’s Booty

Polaner Red Devil Regina Rickland Orchards

B&G FOODS EVALUATION 15

Sa-són Sclafani Smart Puffs Spring Tree

Sugar Twin Trappey’s TrueNorth Underwood

Vermont Maid Wright’s

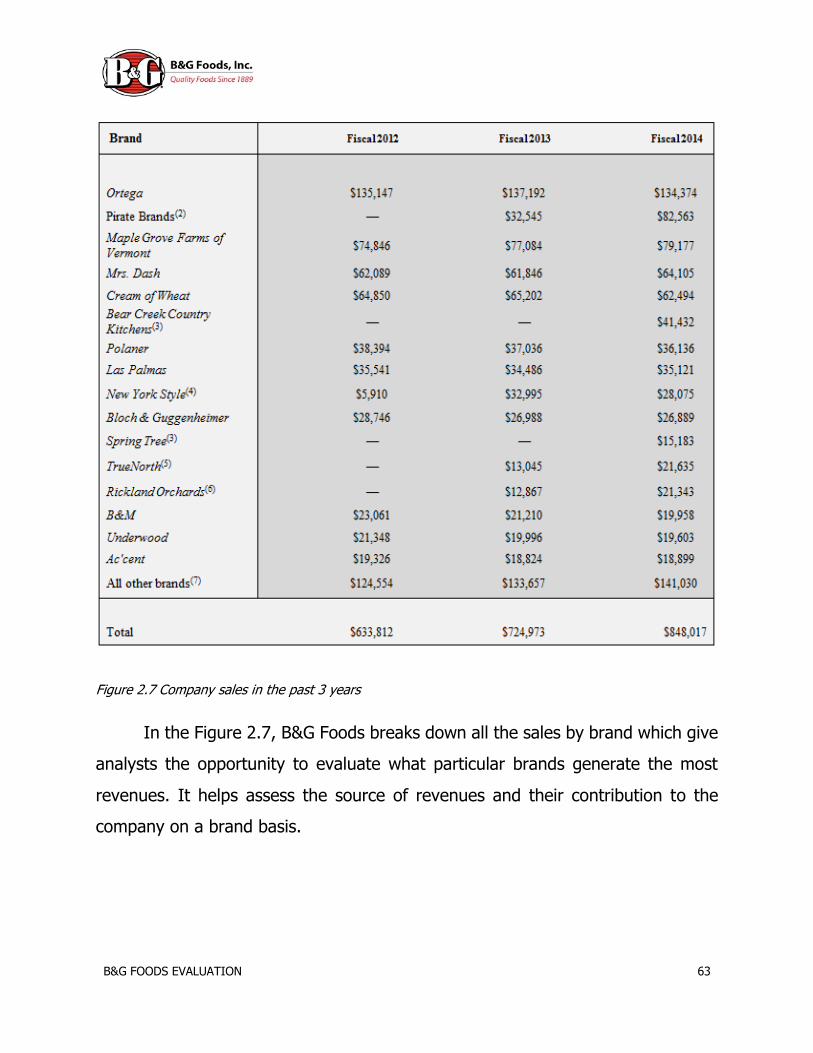

Figure 1.1 B&G Foods’ subsidiaries (B&G Foods 2015 10-K)

B&G Foods specializes in producing shelf-stable food products. As described on

the company’s website profile, the range of foods produced by B&G Foods, Inc.

includes:

“Hot cereals, fruit spreads, canned meats and beans,

bagel chips, spices, seasonings, hot sauces, wine vinegar,

maple syrup, molasses, salad dressings, Mexican-style sauces,

dry soups, taco shells and kits, salsas, pickles, peppers,

tomato-based products, puffed corn and rice snacks, nut clusters,

Greek yogurt coated granola bars and bites, and other specialty products.”

Sales Volume & Growth

B&G Foods has been experiencing a positive increase in sales over the last

five fiscal years; the company’s sales have been increasing at a volatile growth

rate. From 2011 to 2012 sales surged from $543.87 million to $633.81 million

causing a 14% increase in growth rate compare to the period 2014-2015 that had

a small increase of just 2% due to slow market activity.

B&G FOODS EVALUATION 16

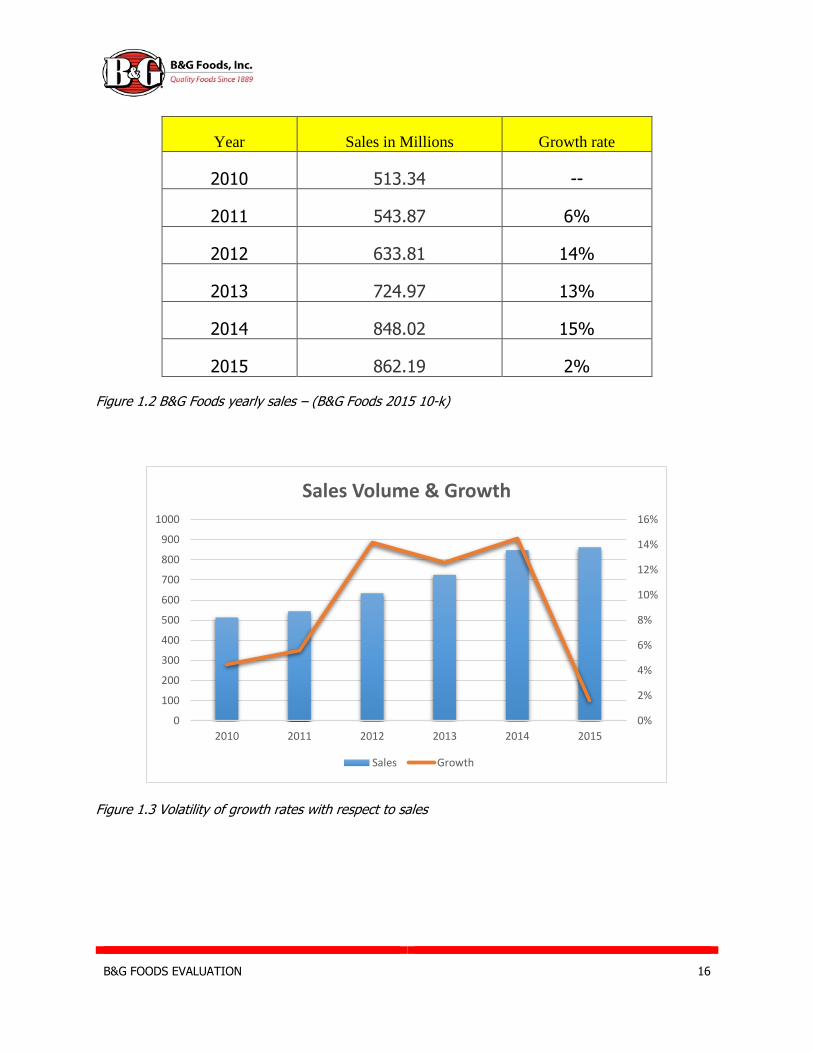

Year Sales in Millions Growth rate

2010 513.34 --

2011 543.87 6%

2012 633.81 14%

2013 724.97 13%

2014 848.02 15%

2015 862.19 2%

Figure 1.2 B&G Foods yearly sales – (B&G Foods 2015 10-k)

Figure 1.3 Volatility of growth rates with respect to sales

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

100

200

300

400

500

600

700

800

900

1000

2010 2011 2012 2013 2014 2015

Sales Volume & Growth

Sales Growth

B&G FOODS EVALUATION 17

Competitors

B&G Foods operates as a supplier in processed and packaged goods

industry, an industry that is characterized by the high degree of competition among

firms; moreover, the profit margin rarely exceeds above 30% (Food Industry

Costs, Profits, and Productivity.)

B&G Foods’ direct market competitors are (1) The J.M. Smucker Company

(SJM), (2) General Mills (GIS), Inc. and (3) The Seneca Food Corporation (SENEA).

B&G Foods’ competitors are subsidiaries holders similar to B&G Foods. All three

competitors offer a wide range of shelf-stable products very similar to those of

B&G Foods. Substitute products are extremely common within the food industry.

Nonetheless, food is the most basic product people consume, and the demand for

food and beverages continues to increase year after year because it is directly

linked to the growth rate of the population as a whole.

Industry: Processed and Packaged Goods

The Processed and Packaged Goods industry is a $4.4 trillion market that

will expand to $5.0 trillion in the following year (RTS Resources.) The processed

and packaged goods industry consists of enclosed food products, a variety of

different materials is used to enclose said products; ranging from plastic to

aluminum canning to preserve the goods for a long period of time. As previously

mentioned the processed and packaged goods industry is correlated to economic

growth, disposable income and population growth.

B&G FOODS EVALUATION 18

Market Capitalization of Firm

Firms are classified as either small, medium or large sized caps. A small-

sized firm has a market value of less than $2.0 Billion, a medium-sized firm has a

market value of more than $2.0 Billion but less than $10.0 Billion. Moreover, a

large-sized has a market value of more than $2.0 Billion but less than $10.0 Billion

(The Mutual Fund Store.) Based on the previous information, and by implementing

the market capitalization formula (Market Price per share x No. of Shares

Outstanding) B&G Foods is worth $2.04 Billion. Therefore, the company is

classified as a medium-sized cap.

Location

B&G Foods’ headquarters are located in Parsippany, New Jersey; the

company operates seven manufacturing facilities of which six are corporately

owned and only one is leased. B&G Foods’ seven manufacturing facilities serve as

warehouse/storage deposits as well.

As seen in the company’s latest “10-K” the manufacturing/warehouse

facilities, distribution centers, headquarters and the sales office (which is required

by “Wal-Mart” located in Bentonville, Arkansas) are located in the following cities.

B&G FOODS EVALUATION 19

Figure 1.4 B&G Foods facilities across the country – (B&G Foods 10-k)

Stock Performance

On May 23, 2007 B&G Foods conducted their Initial Public Offering (IPO)

with the New York Stock Exchange (NYSE). With an initial selling price of $13.60.

The company hit its lowest stock price of $2.56 on October 19, 2008 as a

consequence of the Subprime Mortgage Crisis. Nonetheless, the stock has

maintained an average growth rate of about 38.89% a year ever since 2008;

leading to the current price of $35.44.

B&G FOODS EVALUATION 20

Analyzing B&G Foods’ performance for the last five years indicates the yearly

growth rate that company has experienced. The company’s stock has increase in

price primarily because of their increased in sales year after year for the past five

years. The company’s stock traded at its highest historical price of $38.07 in the

last quarter of their fiscal year ending on November 25, 2015.

As illustrated in the graph below a steady growth rate can be observed regardless

of the price fluctuations in the stock in the last five years.

Figure 1.5 B&G Foods stock performance over the last five years – finance.yahoo/BGS

B&G FOODS EVALUATION 21

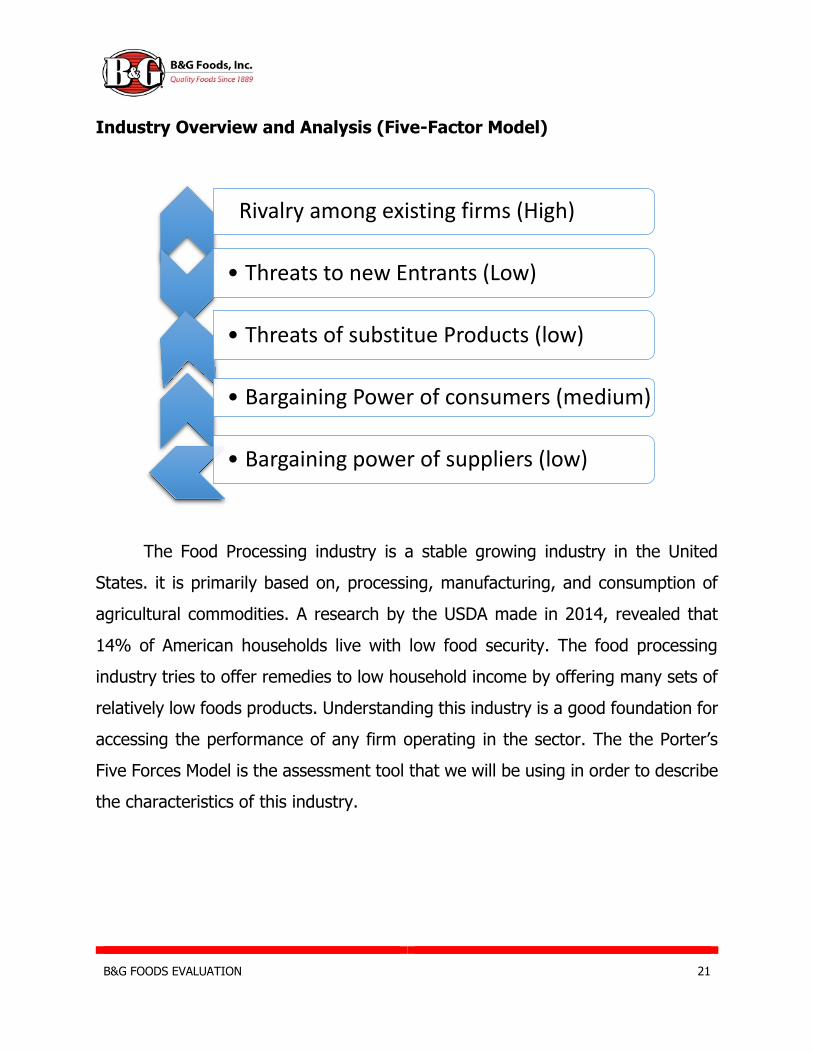

Industry Overview and Analysis (Five-Factor Model)

The Food Processing industry is a stable growing industry in the United

States. it is primarily based on, processing, manufacturing, and consumption of

agricultural commodities. A research by the USDA made in 2014, revealed that

14% of American households live with low food security. The food processing

industry tries to offer remedies to low household income by offering many sets of

relatively low foods products. Understanding this industry is a good foundation for

accessing the performance of any firm operating in the sector. The the Porter’s

Five Forces Model is the assessment tool that we will be using in order to describe

the characteristics of this industry.

Rivalry among existing firms (High)

• Threats to new Entrants (Low)

• Threats of substitue Products (low)

• Bargaining Power of consumers (medium)

• Bargaining power of suppliers (low)

B&G FOODS EVALUATION 22

Rivalry Among existing firms

The degree of rivalry among firms is the most viable scenario for an efficient

use of resources. The economic conditions of the US have shaped the food

processing industry as highly competitive sector. The industry is mainly Business

to Business, therefore firms need to battle to promote their products with whole

sellers and create healthy relationship with both distributors and suppliers. In their

2014 10-k under their competition section, B&G Foods one of the competitor in

the industry briefly explain the role of competition in their sector: “We face

competition in each of our product lines. Numerous brands and products compete

for shelf space and sales, with competition based primarily on product quality,

convenience, price, trade promotion, consumer promotion, brand recognition and

loyalty, customer service, advertising and other activities and the ability to identify

and satisfy emerging consumer preferences.” They talked about key success

factors that help a company stay in business in a very competitive industry.

This creates an environment where were no firm has a real advantage

resulting in low concentration, because no competitor is holding most of the

market share. All the competitors have a decent share in the market.

Switching cost

In the Food processing sector, the switching cost is relatively low, because

companies who charge higher price are most likely to be pushed out of the market

by customers purchasing competitors’ products of the same value at lower price.

The size of company in this industry is very important because it helps firms

increase their share of the market and reducing their costs (economy of scale).

Therefore, Companies need to be Efficient and effective to make profit.

B&G FOODS EVALUATION 23

Small companies are less likely to weaken bigger companies position in the short

run, but they are most likely to be acquired or absorb by with larger companies in

the long term. Merging and Acquiring give company a marketing advantage. Here

is a small selection of brand offered under the same companies (B&G Foods and

General Mills).

B&G Foods brands:” Certain of our brands, including Cream of Wheat,

Ac'cent, Crock Pot seasoning mixes, Underwood, Polaner, Static

Guard, Mrs. Dash, New York Style, Sugar Twin and Rickland Orchards…”

General Mills’ brands: ” Green Giant, Uncle Toby’s, Mountain High, el

Paso, Yoki, Häagen-Dazs, Pillsbury, Totino’s, Progresso, Green Giant, Yoplait

etc.”

By having different brand and products, companies take a step ahead

reducing the effect of switching cost.

In highly competitive industries often provides customers with a set of pretty

similar products, which is the case in this industry where companies have pretty

homogenous products (Low differentiation). It mainly causes the industry have

low differentiation. We’ve selected 4 firms in the industry, and we’ve found that in

all their 10-Ks, they all cited Wal-Mart as one of their most active buyers at roughly

22% of their sales on average.

B&G FOODS EVALUATION 24

percentage of sale by Wal-Mart

B&G Foods 19%

JM Smucker 27%

General Mills 21%

Kellogg 21%

average 22%

Which shows the level of competition in this industry is such that no

company has a real advantage over the other ones’. It also show that there is a

consistency in Walmart purchases of their products with.

Fixed Cost

As manufacturer, most of the fixed cost will come from Property plants and equipment’s

(warehouse, Machinery, land etc.).

PPE Total Assets PPE/TA

Kellogg 3,769 15,153 24.87%

B&G Foods 116 1649 7.04%

General Mils

3,783.30 21,964.50 17.22%

Average 16.38%

B&G FOODS EVALUATION 25

We created a table showing property, Plants, and equipment as a

percentage of Total assets in order to have a better assessment of the fixed costs.

We’ve learned that Net PPE represent on average 16.5% of total Assets with

intangible assets excluded. It shows that this industry relies on fixed costs to

reduce their productions costs while having a high level of output.

Variable costs will be mainly influence by the commodities market and his

fluctuations. The use of futures and forward contracts regarding commodities

comes very handy. In Kellogg 10-K for example, they state that:” The cost of such

commodities may fluctuate widely due to government policy and regulation,

weather conditions, climate change or other unforeseen circumstances.” How can

companies reduce risk from the commodities market? By locking a price in with

forward and futures contracts, companies can protect themselves from price

increase. Relationship with suppliers (contracts) is a big determinant of how

efficient a company is, because it helps control the risk from the commodities

market.

The exit barriers for the food industry are very reasonable exit costs. Most

of them comes from long term liabilities, intangible assets (Goodwill, copyrights

etc.) For example, Kellogg had approximately $5.9 Billions in long term liabilities,

Goodwill of 5.9 Billion and about $2.3 billions in intangible assets (Kellogg’ 2015

10-k page 39). Another example, General Mills had about $7.6 billions of long term

liabilities, Goodwill of $8.9Billions, and 4.7 of intangible Assets (general Mills’ 2015

10k page 53.) Those are components that make it, in those particular cases, a

relatively thoughtful process. It is important that the size of the company is

important, the bigger the company, the higher the exits barrier for those specific

companies.

B&G FOODS EVALUATION 26

Conclusion

The industry where B&G Foods operates is highly competitive. Companies

in this industry have competition in every product line. The industry has a low

concentration, meaning that all firms have no real advantages.

The switching cost is relatively low; it happens due to the inability of

suppliers to charge higher for the same goods. Otherwise, they would be pushed

out of the market since customers would simply purchase goods of other

companies. This leads us to the conclusion that this industry has a low

differentiation.

The fixed costs come primarily from the plants and equipment (warehouse,

machinery, land, etc.). The exit barriers for the food industry go in accordance

with the size of a company. Overall, we present affirm that this industry is

characterized by a high degree of competition.

Threats to New Entrant

In highly competitive industries, the level of threats to new entrants is relatively low,

because of the homogeneity of production throughout the industry. The size of a company often

determines how effectively the entrance of a new company in the market can affect the position

of existing companies. For example, B&G Food has a relatively good share in the US market ($1.7

Billion company) won’t really feel the presence of a new startup company in short run, but in the

long run the market “self-structured” which means the market adjust itself as the startup company

grows. The first mover advantage is low in this industry, but it is attainable through Research and

development (R&D). Companies in the industry are allocating budget in this sense with General

Mills spending $229millions in 2014, $199millions in 2014. New technologies to produce higher

quality products at lower cost for example, a company can differentiate itself for a short term,

but in the long term his competitors will have to update their resources to avoid lost sales.

B&G FOODS EVALUATION 27

The most difficult for new entrants will be contract with suppliers and platforms to display

their products, which can be very complicated for new entrants, how to increase their share? and

how does customers and distributors react to a new brand in a perfectly competitive industry?

Those are two questions that new entrants tend to answer throughout their business strategy

while entering the market.

The Food industry is a highly regulated industry due to the relationship between food and

health. Compliance to all those departments, government and agencies can make it a long process

for a new competitor to enter the market and to quickly compete effectively. In their 2015 10-K

B&G Foods makes statement about all the agencies that they need to comply to: “As a

manufacturer and marketer of food and household products, our operations are subject to

extensive regulation by the United States Food and Drug Administration (FDA), the United States

Department of Agriculture (USDA), the Federal Trade Commission (FTC), the Consumer Product

Safety … federal, state, local and foreign authorities. In addition, our meat processing operation

in Portland, Maine is subject to daily inspection by the USDA.” Which states the amount of

regulations in the Food processing industry.

Conclusion

Since the industry is highly competitive, the threats to new entrants is relatively low. The

main threats are the necessity to find platforms for product distribution and the logistics between

a supplier of raw materials and the marketplace. The industry is highly regulated, and Innovation

may help a company to earn economic profit, but in the long run every other competitor will

follow. The first mover advantage in the industry is not significant: First mover advantage is

relatively low.

Threats of substitute products

The treats to substitute represents the alternative products available to consumers that

are relatively capable of offering the same or really close amount of satisfaction. Their willingness

to switch often depends on the trade off from the evaluation of alternatives and the actual

product. In this industry, The Threats of substitute is relatively low, because it is commodity

based industry. There are few alternatives available to consumers. One would to produce

B&G FOODS EVALUATION 28

themselves what they will consumes as food, another one would be to take whatever is available.

A major discovery in R&D for example, could also create new products that could negatively affect

the demand for the Processed and packaged goods.

Consumers’ willingness is mainly based on price and incentives (coupon, discount, loyalty

program) that the market offers to make their products more appealing to consumers. One more

threat could be the decrease in price of healthy and organic food, with more and more awareness

in this sense, the healthy and organic interest group could possibly in the long-term represent a

serious threat to the processed food industry.

Conclusion

The threats of substitute products represent the alternatives available to the consumers that can

provide them with the same satisfaction. We found that a threat to substitutes will be the price

because it is a incentives for consumers to guide their consumption for specific products. In this

sense, the threat for substitutes products is actually low, because there is no actual alternative

beside consumers growing their own that can represent a direct threat to the processed food

industry.

Bargaining Power of Buyers

The buyers’ ability to drive price come from his ability to substitute products (low switching

cost) and influence firms’ revenues by decreasing sales is medium. Buyers are the core of any

business activities, therefore they play a huge role in the survival of businesses. Consumers could

influence the market by dragging the price low, thus reducing the profit margin of the firms. For

the Food industry, there is an interdependence between the consumers’ needs (primary need:

eat) and business opportunities. Which make this industry pretty stable and sustainable in long

run. For example, B&G Foods had an increase in sales in the United stated by 4.1% (2015 10-K

page 23). There will always be a demand for Food. There is an infinite consumer’s base, but

consumption processing food depends also on the geographic location of consumers.

B&G FOODS EVALUATION 29

Conclusion

Buyers have the ability to drive prices due to a variety of different suppliers and the low

potential switching costs between them. However, since there is always need for food, the buyers

still cannot push the reasonable degree of prices in this industry. There is a mutual interest

between the businesses, trying to make profits, and the consumers trying to feed themselves by

meeting their foods’ expectation. Overall the bargaining power of the buyers is medium, because

still considerable, but can definitely be overcome, because of the necessity of consumers to feed

themselves.

Bargaining Power of Suppliers

Looking at Supply chain, Suppliers play a major role in providing resources for businesses

to provide consumers with quality products. The decision of choosing a supplier is very important,

because the quality of your raw materials will affect the quality of the products produced. The

demand for food is slowly but very sustainably growing over the last years (Graph SALES

GROWTH).

In the Supplier side, the industry is very competitive, so it requires firms to have a large

amount of suppliers to try to reduce cost and most important reduce the risk of raw material

shortages. “The amount of bargaining power of suppliers can also be determined by their

geographic location. Which is very relevant in the effectiveness of companies’ supply chain, and

it can definitely reduce their production costs. “Kellogg in their 2015 10-K explains how they get

raw materials: “The principal ingredients in the products produced by us in the United States

include corn grits, wheat and wheat derivatives, potato flakes, oats, rice, cocoa and chocolate,

soybeans and soybean derivatives, various fruits, sweeteners, vegetable oils, dairy products,

eggs, and other filling ingredients, which are obtained from various sources.”

They produce some of their raw material in order to have better control on supplies.

The quality may vary from places to places. On this end, firms must maintain a certain

standard of quality in order to meet consumers’ expectations. For example, the beef produce in

Venezuela won’t necessarily have the same characteristics as the beef produce in West.

B&G FOODS EVALUATION 30

In a competitive market, a significant way by which businesses can hedge risk and improve

revenues is by being cost efficient while delivering the highest quality product possible. Those

are assessments needed for businesses to determine the choice of suppliers.

Accessing the number of suppliers in the market is nearly impossible to do, but Food

processing industry’s suppliers works in Associations, who mainly in the American continent, but

also internationally. The goal of those associations of suppliers is to facilitate connection between

food manufacturers and suppliers. For US industry those associations regroup suppliers from the

Americas mainly (Canada, Mexico, Puerto Rico etc.)

Conclusion

In this industry, there is a large amounts of suppliers, but companies can

also effectively grow (Commodities) their own raw materials, or even more

reasonably, produce and buy some of it just like Kellogg. On the other end, there

is a significant trade off that is largely influence by the business decisions of the

firm when deciding on which business strategy to use (Make or Buy). In this sector

of the food market, the bargaining power of suppliers is relatively low due to the

fact that companies might prefer the buying alternative because it gives more

variety of choice in term of quality, and more flexibility to switch from one supplier

to another one.

Conclusion

Finally, we can deduct that the Food and packaged good industry is a

competitive market that is characterized under the fives forces model by the

following aspects: low differentiation, low concentration, low threats to substitute,

medium bargaining powers of consumers, and finally low bargaining powers of

suppliers. there are relatively low barriers to entry. The first mover advantage

creates economic profit in the short run, not the long run. The barriers to exit are

medium due to some important usage properties, plant, and equipment needed

B&G FOODS EVALUATION 31

for the manufacturing process. Regardless of their importance in the business

activities, companies in the industry are price takers, most of the bargaining power

comes from consumers’ influence over the price, then Companies, and suppliers

comes last. Regardless of their importance in the business cycle of companies,

Suppliers bargaining remains low, because there are alternatives available on the

market weaken their influence in this industry.

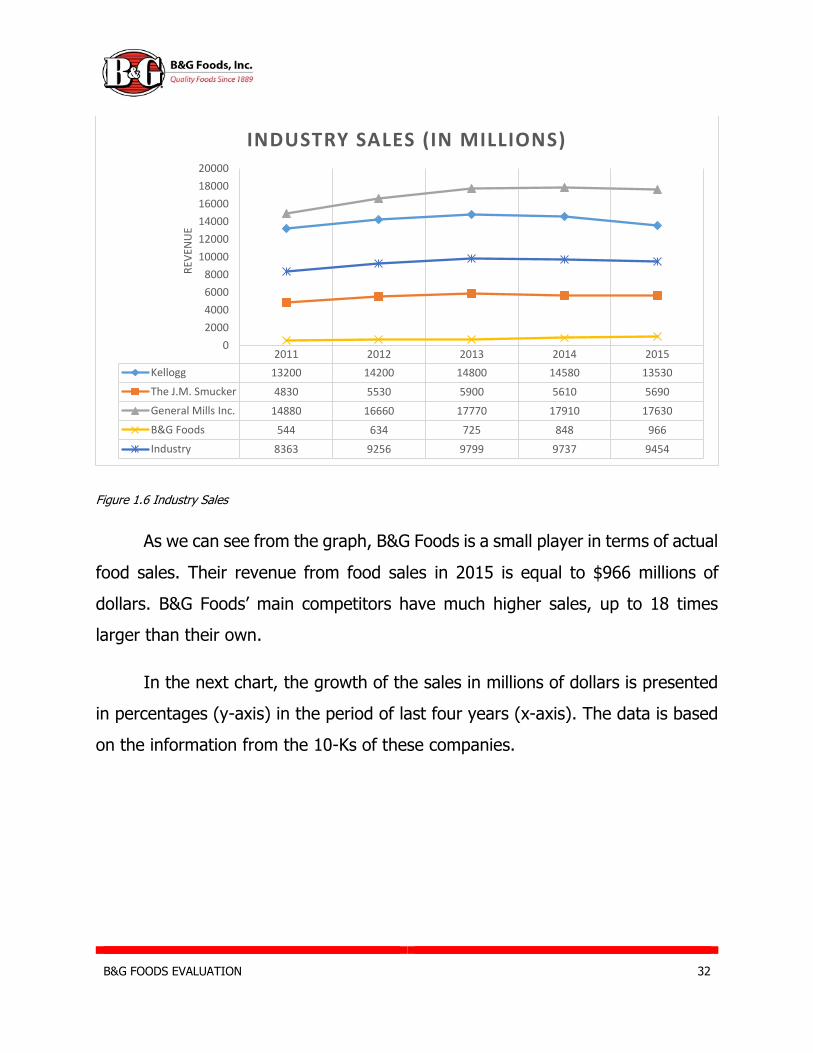

Industry Sales and Growth

The industry sales and growth are analyzed based on the revenue of

companies in the processed and packaged goods industry. The data is obtained

from the 10-Ks of B&G Foods and their competitors.

In the following scatter graph, we evaluate the revenue of the four

companies (y-axis), in the last five years (x-axis). It is important to emphasize that

despite having much more sales in terms of value of the sold items, it does not

necessarily mean that one company is performing better than the other.

According to Yahoo! Finance, the main competitors of B&G Foods are

General Mills Inc. (GIS), The J. M. Smucker Company (SJM), and Kellogg.

The industry data is the average of these four firms.

B&G FOODS EVALUATION 32

Figure 1.6 Industry Sales

As we can see from the graph, B&G Foods is a small player in terms of actual

food sales. Their revenue from food sales in 2015 is equal to $966 millions of

dollars. B&G Foods’ main competitors have much higher sales, up to 18 times

larger than their own.

In the next chart, the growth of the sales in millions of dollars is presented

in percentages (y-axis) in the period of last four years (x-axis). The data is based

on the information from the 10-Ks of these companies.

2011 2012 2013 2014 2015

Kellogg 13200 14200 14800 14580 13530

The J.M. Smucker 4830 5530 5900 5610 5690

General Mills Inc. 14880 16660 17770 17910 17630

B&G Foods 544 634 725 848 966

Industry 8363 9256 9799 9737 9454

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

REV

ENU

E

INDUSTRY SALES (IN MILLIONS)

B&G FOODS EVALUATION 33

Figure 1.7 Sales Growth

It is a growing industry, and the data shows that in the past five years, the

sales have been growing with a period of stagnation between 2014 and 2015. On

the other hand, the B&G Foods demonstrates growing sales in the last four years.

These facts lead us to an optimistic view of the future developments of the B&G

Foods.

Market Capitalization

In this section, market capitalization is analyzed based on the data gathered

from Yahoo! Finance.Investors use market capitalization, also called as market

cap, to understand how big a company is, which is composed of the number of

outstanding shares times stock price.

2012 2013 2014 2015

Kellogg 7.58% 4.23% -1.49% -7.20%

The J.M. Smucker 14.49% 6.69% -4.92% 1.43%

General Mills Inc. 11.96% 6.66% 0.79% -1.56%

B&G Foods 16.54% 14.38% 16.97% 13.95%

Industry 10.67% 5.86% -0.63% -2.91%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%G

RO

WTH

IN %

SALES GROWTH

B&G FOODS EVALUATION 34

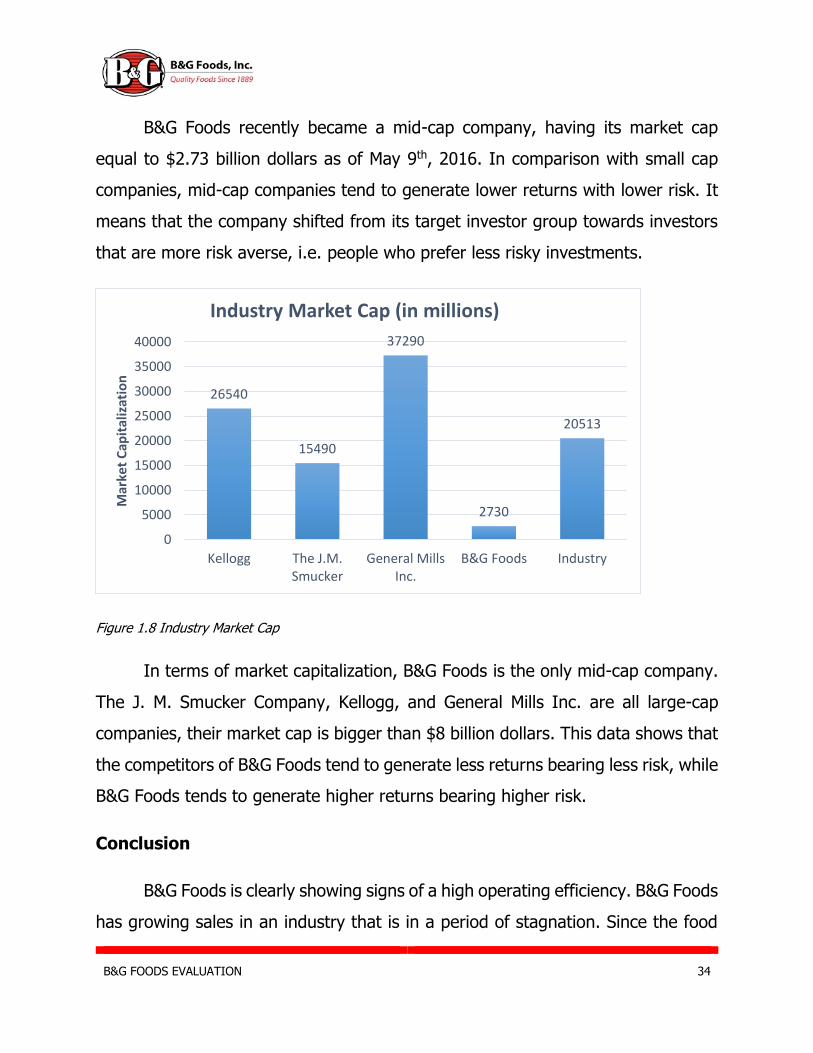

B&G Foods recently became a mid-cap company, having its market cap

equal to $2.73 billion dollars as of May 9th, 2016. In comparison with small cap

companies, mid-cap companies tend to generate lower returns with lower risk. It

means that the company shifted from its target investor group towards investors

that are more risk averse, i.e. people who prefer less risky investments.

Figure 1.8 Industry Market Cap

In terms of market capitalization, B&G Foods is the only mid-cap company.

The J. M. Smucker Company, Kellogg, and General Mills Inc. are all large-cap

companies, their market cap is bigger than $8 billion dollars. This data shows that

the competitors of B&G Foods tend to generate less returns bearing less risk, while

B&G Foods tends to generate higher returns bearing higher risk.

Conclusion

B&G Foods is clearly showing signs of a high operating efficiency. B&G Foods

has growing sales in an industry that is in a period of stagnation. Since the food

26540

15490

37290

2730

20513

0

5000

10000

15000

20000

25000

30000

35000

40000

Kellogg The J.M.Smucker

General MillsInc.

B&G Foods Industry

Mar

ket

Cap

ital

izat

ion

Industry Market Cap (in millions)

B&G FOODS EVALUATION 35

sales have increased in the past years. Based on the analyzed data, this company

has lower sales than their competitors. On the other hand, since their market

capitalization is less than the average, they tend to generate higher returns bearing

higher risks. B&G Foods has recently grown to a mid-cap company in February,

2016, their market capitalization reached $2 billion dollars in that month.

Analysis of Key Success Factors for Value Creation in the Industry

In the highly competitive processed and packaged goods industry, constant

value creation by firms is required to compete in the volatile global and regional

markets. There are many factors that contribute to the volatility of processed and

packaged goods industry markets and it is important to understand how effectively

managing these problems can create value. “Numerous brands and products

compete for shelf space and sales, with competition based primarily on product

quality, convenience, price, trade promotion, consumer promotion, brand

recognition and loyalty, customer service, advertising and other activities and the

ability to identify and satisfy emerging consumer preferences” (B&G Foods 10-K).

(Value creation is the performance of actions that increase the worth of goods,

services or even a business - Business Dictionary)

The following section will include a detailed analysis of specific value creating

strategies and how they directly impact the industry as a whole.

First Mover Advantage

With numerous firms competing in the processed and packaged goods

industry, value creation needs to be high enough to offset the fixed and variable

costs of implementing value creating strategies. Therefore, it is essential to not

only look at how a certain strategy might affect one area of the industry (such as

B&G FOODS EVALUATION 36

packaging), but also how it affects the overall economic strength (value) of the

industry. An example of this can be seen when analyzing how firms in the industry

adapt to trends in consumer tastes.

Over the past decade, consumer food trends have been rapidly evolving,

and PPFI firms have had to adapt accordingly. “Our success depends in part on

our ability to anticipate and offer products that appeal to the changing tastes,

dietary habits and product packaging preferences of consumers in the market

categories in which we compete” (B&G Foods 10-K). One such change can be seen

in consumers’ movement away from name brand foods to private label foods.

“These customers are also reducing their inventories and increasing their emphasis

on private label products” (B&G Foods 10-K). This change creates new niche

markets that allow firms to create new value adding goods. However, these new

goods need to be produced in a way that costs the firm less than the premium

that customers are willing to pay in a specific niche market.

Firms in the industry need to evaluate whether new products can create

enough value to outweigh the costs of introducing the new product to the niche

market. Successful implementation of new product introduction in niche markets

has created massive value for firms such as Chobani.

It is important to note however, that firms that initially introduce products

to a market niche typically find more value in their venture. This value adding

strategy is called the first mover advantage and has allowed many new firms to

enter the processed and packaged goods industry.

While it is harder for large companies to quickly adapt to new trends due to

specialized facilities with long production lines, small firms with relatively short

B&G FOODS EVALUATION 37

production lines can quickly adapt to trends and get their product to market first.

Big firms have had to adapt to this strategy by finding new ways to quickly

introduce products to market. They cannot construct a new facility in a timely

manner in order to capitalize on the first mover strategy, so most firms like General

Mills and B&G Foods Inc. have turned to the acquisition of firms exhibiting strong

first mover advantage value.

Diversified Products

Product diversification is essential for firms in the processed and packaged

goods industry that are seeking long term success. “Product diversification is a

process by which businesses attempt to expand their market reach and customer

base by delivering products somewhat different than the ones for which they are

known. These new products can simply be extensions of existing brands or they

may be entirely new. By engaging in product diversification, a company can extend

its business into new areas and markets, thereby increasing their opportunities for

profit” (Wise Geek).

For firms like B&G Foods, acquisitions are a value adding way to go about

diversifying their products. “A major part of our strategy is to grow through

acquisition” (B&G Foods 10-K). New niches in the processed and packaged goods

industry are repeatedly emerging and big firms with specialized facilities cannot

readily adapt to consumer tastes in a timely manner. These facilities are capable

of producing a wide range of related products, but struggle with highly diversified

products. Therefore, these big firms turn to small, highly specialized firms easily

capable of producing desired goods.

B&G FOODS EVALUATION 38

Buying out a small firm does not require a substantial amount of capital

allowing diversification against risk. The niches that show a positive growth attract

additional investments from the parental companies. If firms decided to take on

the diversification themselves, the main brand/company (Coca-Cola producing all

of its products under the Coca-Cola name) could be damaged by the potential

failure of the subsidiaries, thus increasing the risk of the venture.

Lower-Input Costs

It’s not always valuable to acquire a firm, however. It is more profitable in

some instances, to expand existing facilities within the main company. “We

regularly evaluate our co-packing arrangements to ensure the most cost-effective

manufacturing of our products and to utilize company-owned manufacturing

facilities most effectively” (B&G Foods 10-K). Such is the case with General Mills

and their cereal production. General Mills produces a number of cereals with similar

production processes. General Mills’ factories are capable of handling multiple

cereals by implementing machines that are capable of different functions. In this

case, it is much cheaper, and thus value adding to invest in an adaptable

production line than to go out and acquire a company that is capable of a specific

function.

As stated in the paragraph above, General Mills adopts such a strategy by

making sure that its cereal producing factories are able to meet the needs of future

consumer trends in cereal. With 12 different cereals, General Mills is able to

efficiently produce a large portion of their cereals without having to heavily modify

its existing infrastructure. Furthermore, new cereals will be introduced down the

line with relatively little startup costs due to factories that are able to handle a

wide-range of cereals.

B&G FOODS EVALUATION 39

Supply contracts are also necessary for keeping a low input cost.

“Supply contracts are types of contracts that establish the terms of a

working relationship between a vendor and a customer. A supply contract

is often necessary in order to lock in discounted pricing and other benefits

that the supplier is agreeing to provide to the client for a specific period of

time” (Wise Geek).

With an agreed upon discounted price, firms in the industry can produce

their products at a low, stable price. This strategy is particularly valuable when

commodity prices are increasing (currently they are) because it allows firms to pay

a low price for a set period of time regardless of the current market prices , thus

adding value to the firm. If costs are unexpectedly driven down, firms can

renegotiate, as long as the supplier is willing, the price down to meet future

expectations.

Regardless of the volatility of commodity markets in which firms in the

industry participate in, supply contracts provide relative stability to future costs

incurred by the firm. “Vegetables for the Green Giant brand are primarily purchased

under dedicated acreage supply contracts from a number of growers prior to each

growing season with the remaining demand being sourced directly from third

parties. We purchase certain other agricultural raw materials in bulk or pursuant

to short-term supply contracts” (B&G Foods 10-K). This can be particularly useful

when gauging how to allocate funds in the future. With this being said, suppliers

can set the terms to the contract as easily as firms can. This is especially true

when firms are supplier dependent. Supplier dependent means to rely heavily or

entirely on one supplier to supply the good a firm needs to produce its goods.

Suppliers in this instance can use this to their advantage by requiring higher

B&G FOODS EVALUATION 40

payments for their goods. Therefore, it is also value adding to ensure that a firm

is not supplier dependent.

Retailer Relations

In the processed and packaged goods industry, most firms do not sell their

products directly to individual consumers. It is very difficult for processed and

packaged goods firms to directly sell their products to individual consumers since

they produce in bulk quantities. Instead they sell to retailers such as Walmart.

Maintaining a good relationship with retailers is key if firms in the industry want to

distribute their products in sizeable volumes.

“In the past decade, the retail side of the food industry has seen a continuing

shift of sales to alternate food outlets such as supercenters, warehouse clubs,

dollar stores and drug stores”(B&G Foods 10-K).

All firms in the industry are price takers meaning that whatever retailers are

willing to pay for the goods is what suppliers can sell those goods for. Despite this,

if retailers are unwilling to buy the goods, suppliers will have a large stock of

expiring food in its inventory. Delivering products on time and ensuring quality are

some value adding ways firms in the industry can maintain good relations with

retailers.

Good relations are not important however, if a product is not selling.

Regardless of how favorable a firm is, a retailer will not sell an inferior good. Firms

in the industry need to ensure the quality of their products through buyback

programs. A buyback program is a guarantee on the quality of products sold to a

retailer. Products that are inferior can be shipped back to the supplier for a refund.

Regardless of quality, a product’s sales might dip in certain conditions.

B&G FOODS EVALUATION 41

To offset this, firms can implement a promotional program to save individual

consumers money and compensate the retailors for the loss through trade sales

promotions or some other means. “Our marketing organization is aligned by brand

and is responsible for the strategic planning for each of our brands. We focus on

deploying promotional dollars where we believe the spending will have the greatest

impact on sales” (B&G Foods 10-K). A value seeking firm should only implement a

promotional program if the firm believes the dip in demand or increase in

competition is only short term. It should not be used as a permanent fix to an

underselling product.

Brand Awareness

Product identification is important in how a certain product will sell. For

example, for products that list “value brand” on them consumers will immediately

identify the product as relatively cheap and of low quality. “Value brand” products

will attract those customers who value price over quality. “Our marketing

organization is aligned by brand and is responsible for the strategic planning for

each of our brands. We focus on deploying promotional dollars where we believe

the spending will have the greatest impact on sales” (B&G Foods 10-K). Therefore

it is important to know how to market a specific product in order to draw in the

target customer.

With many PPFI firms this problem becomes increasingly more complex.

Different products need to reach a different audience without conflicting with each

other. What we mean by this is if a company sells a “value brand” of a certain

category of food, they need to make sure any future endeavors into the category

target a different type of customer. Any conflict could potentially create additional

B&G FOODS EVALUATION 42

competition and thus lower sales. Correctly implementing a strategy where a PPFI

firms products can reach a wide range of customers is value adding.

Advertising is a key component to a brand’s image and appeal to customers.

Advertising can dramatically change how a product is received. “Our sales strategy

is centered on individual brands. We allocate promotional spending for each of our

brands and our regional sales managers coordinate promotions with customers.

Additionally, our marketing department works in conjunction with the sales

department to coordinate special account activities and marketing support, such

as couponing, public relations and media advertising” (B&G Foods 10-K).

With effective advertising, it is possible to increase a customer base for a

product by relating to a wide range of consumers. Effective advertising can also

relay to consumers why your product is unique from other products. With effective

advertising, firms in the industry can attract new consumers and stimulate

increased demand for their products thus adding value.

Conclusion

There are many ways to potentially add value to a firm. However, poor

implementation can result in a loss of value as with any strategy. It is crucial that

a firm looks at its available options and considers total firm impact to evaluate

whether a strategy is truly value adding. In many cases, in order to outperform

the market a company needs to make a strategy in a unique, efficient way.

Therefore, when valuing a firm it is crucial to look at a strategy’s efficiency and

implementation to find an accurate way of adding value. Only then can we truly

get a good idea of how much value is being added to the firm.

B&G FOODS EVALUATION 43

Competitive Advantage

Due to the large number of competitors present in the the processed and

packaged goods industry, it is increasingly important to achieve significant

competitive advantages over other firms. Some of the aspects B&G Foods focuses

on that create these competitive advantages include, economies of scale,

economies of scope, low cost distribution, and competitive pricing. One of B&G

Foods’ most valuable competitive advantages is low pricing without compromising

quality of the product, or shelf life. Product preservation is something that B&G

Foods is able to specialize in due to their respective economies of scale, and

economies of scope, within every product line. Through the use of these methods,

B&G Foods is able to achieve a competitive advantage that will be shown in detail

throughout the following sections.

Cost Leadership

As seen throughout the food industry, competitive pricing is essential to

success among competing firms. An effective pricing/cost strategy employed by

B&G Foods to compete with larger firms within the industry, that may be able to

achieve lower production costs, is to search for firms with which B&G Foods may

reach a contractual agreement with to manufacture, and package products at a

reduced cost.

“In addition to our own manufacturing facilities, we source a significant

portion of our products under ‘co-packing’ arrangements, a common

industry practice in which manufacturing is outsourced to other companies.

We regularly evaluate our co-packing arrangements to ensure the most cost-

B&G FOODS EVALUATION 44

effective manufacturing of our products and to utilize company-owned

manufacturing facilities most effectively.” (B&G Foods 10-K)

This cost strategy is essential to B&G Foods’ competitive pricing abilities,

and their market position in the food industry. Another cost leadership approach

B&G Foods implements, is the purchase of raw materials in bulk from wholesale

distributors ranging from agriculture producers, to companies specializing in

wholesale shipping and packaging materials such as cardboard, glass jars, etc.

Due to potential fluctuations in factors affecting the input prices of these raw

material suppliers, B&G Foods primarily focuses on establishing short-term

contracts to minimize cost volatility risk from said wholesalers, and maintain a

profitable contract with each respectively.

Economies of Scale and Scope

Although B&G Foods is considered one of the smaller companies operating

within the food industry, it effectively achieves both economies of scale and scope

through various different means. As previously discussed, B&G Foods relies heavily

on their contractual agreements with large manufacturers to obtain significant

profit margins on their products, essentially creating economies of scale that would

otherwise be unattainable to a firm of it’s size. In 2015 B&G Foods reported total

assets of $1.6 billion dollars, which is relatively small in the processed and

packaged goods industry. However, despite it’s small market share within the

industry, B&G Foods has established significant economies of scope in their

product lines. These economies of scope have been attained by B&G Foods

through the diversification of their product lines, and the use of existing

manufacturing facilities to produce these expansions within each product line.

B&G FOODS EVALUATION 45

Efficient Production

Efficient production is something that B&G Foods bases their entire

manufacturing process around, sticking to what their facilities are efficiently

capable of, and outsourcing the rest to the lowest cost manufacturer. Their

constant evaluation of profitability among the outsourced manufacturing insures

that they are operating at the lowest cost available and limits overhead costs to a

minimum.

“During the past three years, our cost saving measures and sales price

increases have substantially offset increases to our raw material, ingredient,

and packaging costs.” (B&G Foods 10K)

An attest to this statement is observed in B&G Foods’ constant research of

competing costs and pricing currently available.

Low-Cost Distribution

The distribution costs associated with the products manufactured by B&G

Foods are partially incurred by our wholesale customers such as Walmart, which

provide an access to their respective economies of scale and reduced costs. Due

to the nature of the industry in which B&G Foods operates, the distribution costs

related to the output of their products are directly related to the resources available

to the retailer which they sell to. Thus, B&G Foods’ primary concern when

considering potential wholesale customers, is to what extent customers can

facilitate distribution and minimize costs of transportation.

B&G FOODS EVALUATION 46

Inventory

Turnover

2011 2012 2013 2014 2015

B&G Foods 4.30 4.57 4.76 5.63 2.16

Kellogg 7.11 6.42 6.96 7.44 7.08

J.M.

Smucker

3.51 3.83 4.09 3.84 3.20

General

Mills Inc.

5.55 7.18 7.34 7.40 7.58

Figure 1.9 Inventory Turnover Table

There is an industry trend for inventory turnover values between 5-6 with

Kellogg having the highest throughout all periods. B&G Foods has one of the lowest

inventory turnovers in the industry with a decreasing value recently. This is an

indication that B&G Foods would benefit from an increase in inventory efficiency

in order to reduce costs and compete with firms within the processed and

packaged food industry.

Conclusion

B&G Foods has used several competitive advantages within their industry to

strategically position themselves and establish their market share. Their market

share, through the use of economies of scale, economies of scope, and low cost

distribution is one that is continually growing yearly. By simplifying product design,

lowering distribution costs, minimizing input costs, and manufacturing at the

highest efficiency possible, B&G Foods has achieved competitive advantages that

B&G FOODS EVALUATION 47

would otherwise be unattainable for firms of their size. Although B&G Foods is a

mid-sized competitor in the processed and packaged goods industry, their use of

competitive advantages has provided increased growth of their market share.

Accounting Analysis When a company lists shares of their corporation through an initial public

offering, they become subjected to the rules and regulations of the Securities and

Exchange Commission (SEC). These regulations mandate the public accessibility

of financial information concerning the daily operations of each firm. This

monitoring is essential to protect shareholders of all firms from receiving

information that may be misrepresented by the issuing firm in order to maximize

their stock value.

As previously discussed, firms must effectively leverage their use of the key

success factors they possess within the packaged and processed food industry in

order to further develop a competitive advantage in the market. When evaluating

financial statements released by a firm, it is important to understand the level of

disclosure implemented by the firm in order to identify any potential overstated or

understated occurrences. Even firms that are in compliance with Generally

Accepted Accounting Principles (GAAP) must be analyzed further in order to

determine the true value of the firm.

The degree to which firms release financial information apart from what is

required by GAAP varies from industry to industry, this is known as the firms

accounting strategy. The quality of the information which the firm may or may not

release is significant due to the consequential effect it may have to investors if it

is misstated. This is one of the primary reasons that firms must maintain a certain

B&G FOODS EVALUATION 48

level of transparency in their documents in order to instill trust in the shareholders

and provide them with the relevant information needed to make quality investment

decisions.

The accounting analysis process contains several steps in order to

accumulate, analyze, and interpret data correctly. Some factors which must be

constantly considered are the accuracy of the information released by the firm and

the form which they released it in. These factors dictate how useful the information

is to a current shareholder or potential investor. If any significant financial

information contained in the document the firms release is misstated or otherwise

faulty, it may negatively impact shareholders and is thus considered a red flag. In

the following sections we will discuss in further detail this accounting analysis

process and how to interpret and potentially restate this information in a manner

that may prove to be ultimately more informative.

Key Accounting Policies

In order to complete a successful accounting analysis, a firm’s key

accounting policies must first be identified. These policies vary from company to

company even within the same industry, this is in part due to the significance of

said policies. Although every firm must comply with the United States Generally

Accepted Accounting Principles (GAAP), the policies they wish to employ while

doing so are chosen by the firm. Sometimes firms may present some of their

financials in a way that may produce an over-optimistic representation of their

financials, thus it is important to review these key accounting policies in order to

develop a more accurate and objective understanding of the firm’s financial

performance.

B&G FOODS EVALUATION 49

Type One Key Accounting Policies

Type one accounting policies describe how a firm uses key success factors

to separate themselves from other firms within their industry and gain a

competitive advantage. How a firm develops a way to make their service unique

and provide value for their customers is called differentiation. There are several

ways that firms can stand out from their competitors, some of the methods include

product quality and variety, and cost leadership. In the processed and packaged

food industry differentiation is essential to remain competitive and retain

customers.

Cost Leadership

Reducing costs is an important part of any industry however, within the

packaged and processed food industry it is essential to stay competitive. There are

several ways which a firm can achieve cost leadership and they include low

distribution costs, economies of scale and efficient operations. When a company

expands its production capabilities or begins to see an increase in sales volume,

they may have a marginally reduced cost per item due to the constant overhead

expense and increased production, this is known as economies of scale. Another

way that a company may achieve economies of scale is through contractual

agreements with other larger companies to produce and manufacture products for

them at a rate that is lower than if the same volume were to be produced using

the own firms’ facilities. This production outsourcing is one of B&G Foods’ primary

key success factors which gives them a significant competitive advantage over

their direct competitors.

B&G FOODS EVALUATION 50

Within the processed and packaged food industry there are more than

30,000 competing suppliers to retailers which consequently leads the industry to

be price-takers rather than price-setters. Due to this increased competition,

retailers are able to leverage their bargaining power to select only the firms which

provide them with the cheapest costs or the largest profit margin. This forces

suppliers to maximize cost efficiencies in the manufacturing and distribution areas

in order to stay competitive.

Product Quality and Variety

Within the processed and packaged food industry there are many substitutes

for products among firms. Therefore, it is essential for firms to produce a variety

of options for the products they manufacture. B&G Foods has a wide variety of

high quality products food items within each of their product lines making them

one of the more diversified firms in the industry. Furthermore, when it comes to

products in the processed and packaged food industry, customers demand a high

quality at a reasonable price. B&G Foods provides customers with high quality

products through the use of contractual agreements with the industry’s leading

suppliers.

Although B&G Foods’ benchmark competitors strive to provide high variety

in their product lines, they often do so at the expense of quality. Differentiation

through quality is something which B&G Foods exemplifies through the use of

higher quality ingredients. Although there are cheaper alternatives to products

within B&G Foods’ manufacturing lines, they are able to entice customers through

this quality differentiation to other firms in the industry.

B&G FOODS EVALUATION 51

Type Two Key Accounting Policies

The way in which companies present their financial statements is considered

to be their type two accounting policies. These policies policies allow businesses

to report their financial statements in several different ways which can often lead

to a distorted presentation of their financials. Therefore, these accounting policies

must be examined in further detail in order to develop an objective understanding

of the firm’s financial performance.

These types of accounting policies are directly related to the firm’s reporting

of research and development expenses along with goodwill amortization. Although

the way in which a firm reports these elements of their financial statements is

legal, it is important to understand them to gain a clear knowledge of their

financials.

Research and Development

When considering Research and Development (R&D) in the processed and

packaged food industry, it is important to note the impact these expenses have on

the firm’s financial documents. In order for firms to be in compliance with GAAP

regulations they must expense the costs they incur relating to R&D in the year

which they were incurred. Consequently, firms who invest heavily in R&D may

report an income statement in which their expenses are overstated leading to an

overstatement in net income and equity on the balance sheet.

In that case a restatement of these expenses would present a more transparent

view of the impact that R&D expenses have on potential future profit. In the case

of B&G Foods, they list no R&D expenses meaning that there is no need for a

restatement because the firm does not allocate any funds to the activity

B&G FOODS EVALUATION 52

Goodwill

Goodwill is considered to be a form of an intangible asset which provides

value for the company during mergers and acquisitions. When goodwill is

expensed it reduces the value of the company assets and consequently many

companies often exclude any capitalized goodwill from their financial statements.

This is a very significant accounting strategy to consider when evaluating a firm

because it can be manipulated into presenting an overstated asset balance to show

a more positive company performance. Below in Figure 2-5 the goodwill listed on

B&G Foods annual reports is listed along with their respective PP&E, and total

assets.

B&G Foods Goodwill

(thousands) 2011 2012 2013 2014 2015

Goodwill 263,000 267,940 319,292 370,424 TBA

PP&E 92,000 104,746 110,374 116,197 TBA

Total Assets 1,133,000 1,192,000 1,484,343 1,649,353 TBA

Figure 2.1 B&G Foods Goodwill

Considering the fact that annual goodwill is a much greater than the net