Equator Exploration · Performance 1 Month 3 Month 12 ... Equator is in alliance with the Indian...

20

KBC Peel Hunt Ltd 111 Old Broad Street London EC2N 1PH Telephone: +44 (0) 20 7418 8900 Facsimile: +44 (0) 20 7417 4646 www.kbcpeelhunt.com Source: Perfect Information Performance 1 Month 3 Month 12 Month Price -1 72 295 Rel to FTSE ALL -1 61 234 Equator Exploration (EEL) Oil & Gas / AIM 6 March 2006 Research Analyst: Tony Alves Tel No. +44 (0) 20 7418 8813 [email protected] Equator is an high rolling explorer playing for major stakes with large amounts of risk capital. The game plan is clearly to build a reserve base and prospect inventory that should be irresistible to resource-hungry Asian national oil companies. It is some way short of becoming a self-sustaining business and for that reason is a higher risk investment than other E&P companies of similar market capitalisation. The company has just raised $250m to add to its current $150m of cash resources. Capital investment could be up to $700 million over the next 3-4 years, over $550m in exploration, testing some prospects with reserves potential estimated by Equator to be in the billion-barrel class. The company’s activities are presently focused offshore Nigeria and in the adjacent waters of São Tomé. The key play and potentially source of greatest future value is in the Nigerian blocks OPL 323 and 321, where it is committing to its anticipated share (assumed at 20%) of $1.4 billion of signature bonus payments and committed work programmes. Drilling is currently taking place on OML 122 offshore Nigeria. This block has a discovered oil and gas field (Bilabri) and undrilled prospects, primarily thought to be gas bearing. While potential exists for material volumes, the commercial value of gas reserves in Nigeria is uncertain. This drilling programme will provide much of the short-term news flow. Equator is in alliance with the Indian state company ONGC for the acquisition of exploration interests in Nigeria and the Gulf of Guinea. As a group they were high bidders in the two blocks in the 2005 Nigerian licensing round and gained an interest in Block 2 in the Nigeria/São Tomé JDZ. The contracts on these blocks are yet to be finalized although it is expected that the first wells may be drilled in all three licences during 2007. The company has priority rights to select two blocks in the São Tomé Exclusive Economic Zone (“EEZ”). While prospective, this area is of significantly higher technical risk although the financial commitment should be lower. While the technical risks on Equator’s assets are not especially high, the shares carry significant exploration value. We estimate Core NAV of 171p and have calculated Exploration Value of 364p giving a combined NAV of 535p per share on a fully diluted basis. On this basis, we consider the stock to be on a reasonable risk-reward balance up to 500p. Short term drilling news flow may be positive for the stock but the value impact, particularly in relation to Nigerian gas, is uncertain. The real play will be in OPL 321/323. Confirmation of Equator’s interests in those blocks will remove a major uncertainty and successful drilling of some of the giant prospects in those blocks could provide the means to achieve the kind of value growth commensurate with the financial commitment. BUY A white-knuckle investment of genuine potential Major Shareholders* Everest Capital 15% Gilder Gagnon 7% Millenium 5% Perry Capital 3% Management 3% Source: Bloomberg *Approximate % holdings based on data pre- dating the recent placing. Company Statistics Price (p) 350p Market Cap (£m) £615m Activity Analysis Equator is involved in exploration for and appraisal of oil and gas fields in Nigeria, São Tomé and other West African countries. It currently has no producing interests although it aims to bring its first field into development in 2007. Divisions Turnover Profit African exploration n.a. n.a. 60 110 160 210 260 310 360 Dec 04 Feb 05 Apr 05 Jun 05 Aug 05 Oct 05 Dec 05 Feb 06 EQUATOR EXPLORATION Rel. to All Share

Transcript of Equator Exploration · Performance 1 Month 3 Month 12 ... Equator is in alliance with the Indian...

KBC Peel Hunt Ltd 111 Old Broad Street London EC2N 1PH Telephone: +44 (0) 20 7418 8900 Facsimile: +44 (0) 20 7417 4646 www.kbcpeelhunt.com

Source: Perfect Information

Performance 1 Month 3 Month 12 Month Price -1 72 295 Rel to FTSE ALL -1 61 234

Equator Exploration (EEL) Oil & Gas / AIM

6 March 2006 Research Analyst: Tony Alves Tel No. +44 (0) 20 7418 8813 [email protected]

Equator is an high rolling explorer playing for major stakes with large amounts of risk capital. The game plan is clearly to build a reserve base and prospect inventory that should be irresistible to resource-hungry Asian national oil companies. It is some way short of becoming a self-sustaining business and for that reason is a higher risk investment than other E&P companies of similar market capitalisation.

The company has just raised $250m to add to its current $150m of cash resources. Capital investment could be up to $700 million over the next 3-4 years, over $550m in exploration, testing some prospects with reserves potential estimated by Equator to be in the billion-barrel class.

The company’s activities are presently focused offshore Nigeria and in the adjacent waters of São Tomé. The key play and potentially source of greatest future value is in the Nigerian blocks OPL 323 and 321, where it is committing to its anticipated share (assumed at 20%) of $1.4 billion of signature bonus payments and committed work programmes.

Drilling is currently taking place on OML 122 offshore Nigeria. This block has a discovered oil and gas field (Bilabri) and undrilled prospects, primarily thought to be gas bearing. While potential exists for material volumes, the commercial value of gas reserves in Nigeria is uncertain. This drilling programme will provide much of the short-term news flow.

Equator is in alliance with the Indian state company ONGC for the acquisition of exploration interests in Nigeria and the Gulf of Guinea. As a group they were high bidders in the two blocks in the 2005 Nigerian licensing round and gained an interest in Block 2 in the Nigeria/São Tomé JDZ. The contracts on these blocks are yet to be finalized although it is expected that the first wells may be drilled in all three licences during 2007.

The company has priority rights to select two blocks in the São Tomé Exclusive Economic Zone (“EEZ”). While prospective, this area is of significantly higher technical risk although the financial commitment should be lower.

While the technical risks on Equator’s assets are not especially high, the shares carry significant exploration value. We estimate Core NAV of 171p and have calculated Exploration Value of 364p giving a combined NAV of 535p per share on a fully diluted basis. On this basis, we consider the stock to be on a reasonable risk-reward balance up to 500p.

Short term drilling news flow may be positive for the stock but the value impact, particularly in relation to Nigerian gas, is uncertain. The real play will be in OPL 321/323. Confirmation of Equator’s interests in those blocks will remove a major uncertainty and successful drilling of some of the giant prospects in those blocks could provide the means to achieve the kind of value growth commensurate with the financial commitment.

BUYA white-knuckle investment of genuine potential

Major Shareholders* Everest Capital 15% Gilder Gagnon 7% Millenium 5% Perry Capital 3% Management 3% Source: Bloomberg

*Approximate % holdings based on data pre-dating the recent placing.

Company Statistics Price (p) 350pMarket Cap (£m) £615m Activity Analysis

Equator is involved in exploration for andappraisal of oil and gas fields in Nigeria, SãoTomé and other West African countries. Itcurrently has no producing interests althoughit aims to bring its first field into developmentin 2007.

Divisions Turnover Profit

African exploration n.a. n.a.

60

110

160

210

260

310

360

Dec04

Feb05

Apr05

Jun05

Aug05

Oct05

Dec05

Feb06

EQUATOR EXPLORATION Rel. to All Share

KBC Peel Hunt Ltd Equator Exploration

2

Investment Summary We are initiating coverage with a speculative Buy recommendation. Equator Exploration is an exploration company currently focused in the Niger Delta. Although it could be in production by early 2007, the value primarily resides in its exploration projects. Nevertheless, it is operating in areas that contain large hydrocarbon resources with realistic chances of discovery of large reserves. It has a large financial commitments for signature bonuses and firm work programmes, for which it has recently raised $250m in an equity placing at 350p per share.

Valuation We estimate Core NAV, based on adjusted net working capital and discovered petroleum in Bilabri (OML 122) at 171p per share. We estimate Exploration Value of 364p per share, divided between four exploration ventures as shown in the summary table.

Based on moderate success with exploration drilling over the next 2-3 years, we could see the Core NAV rise to over 600p per share. Meanwhile, follow-on opportunities and new ventures could maintain a significant exploration value.

Risk Factors

Financial – Equator has an exploration spend of up to $550m over the next 3-4 years which will consume all current resources and much of the free cash flow from future Bilabri oil production.

Assets. Many of the key prospects lie within concessions in which the company’s interests are yet to be finalised. These are OPL 321, OPL 323, JDZ Block 2 and the two EEZ blocks.

Exploration risk – The company’s views on prospect size and probability of success are higher than we are assuming. This is nevertheless inherently a high risk business.

Nigerian gas – the timing of commercialisation and the potential sales price for Nigerian gas is uncertain. Significant capital investment over and above the exploration spend will be required to develop any discoveries.

News Flow

Drilling. A minimum five well programme is under way in OML 122 offshore Nigeria. Results from the ongoing Bilabri well due shortly.

Development planning for Bilabri oil may be achieved within the coming months with a view to first oil early in 2007.

Licences. Signing of JDZ Block 2 and settlement of the equity share in Nigerian blocks OPL 321 and 323 are both expected shortly. The priority blocks in the São Tomé EEZ are also to be nominated.

Brass LNG. Re-allocation of shareholdings in the Brass LNG venture to replace Chevron could influence commercialisation of gas reserves in OML 122.

New ventures. We believe Equator will be pursuing further exploration ventures in West Africa, principally in Congo and Angola, probably in alliance with ONGC.

Table of Contents Page Investment Summary 2 Background 3 Management 4 Nigeria OML 122 5 Nigeria 2005 Licensing Round 8 São Tomé 10 Finances 13 Valuation 14 Financial Forecasts 18

Figure 1: NAV Summary $m p/share

Net working capital 329 97p Bilabri oil 121 36p Bilabri gas 129 38p Core NAV 579 171p

OML 122 gas prospects 326 96p OPL 321, 323 627 186p JDZ Block 2 88 26p Sao Tome EEZ 188 55p Risked Exploration 1228 364p

Total NAV 1808 535p Source: Equator Exploration & KBC Peel Hunt estimates

KBC Peel Hunt Ltd Equator Exploration

3

Background Gulf of Guinea focus Equator Exploration has become one of the leading African-oriented oil

exploration businesses listed on AIM and has one of the few publicly quoted E&P companies operating in the Gulf of Guinea. It originated from a venture established by among others the Norwegian seismic company PGS to market multi-client seismic data on the deep water areas around the former Portuguese colony of São Tomé where it has been granted certain priority rights over areas planned to be offered for licensing within São Tomé’s exclusive economic zone (“EEZ”). The company was floated on AIM in 2004, initially just with its interests in the EEZ. It subsequently significantly expanded its interests to encompass Nigerian offshore activities, participation in the Nigeria-São Tomé Joint Development Zone (“JDZ”) and has ambitions to add ventures in other West African countries to its portfolio.

Alliance with ONGC Equator also has an alliance with Indian state oil company ONGC Videsh targeted at securing material deep water exploration opportunities in the greater Niger Delta area. This alliance secured the JDZ interest referred to above and was high bidder for two deep water blocks: OPL 321 and OPL 323 offshore Nigeria.

The exploration credentials and prospectivity of West Africa generally and the Niger Delta specifically are well known and hardly need to be repeated in this note. The company’s strategy is best encapsulated in the following quote:

“Equator’s strategy is to identify, acquire and explore high quality prospects with the potential for large oil and gas reserves. The company intends to leverage its financial and industry expertise and experience, as well as its network of contacts, to select attractive exploration opportunities and to secure them on favourable terms. Equator will initially focus its efforts in West Africa.”

High impact drilling The company is currently completing the first well of a multi well exploration, appraisal and development drilling programme in the Nigerian offshore block OML 122. This should deliver the company’s first oil production in early 2007 from the 40 mmbbl Bilabri field and prove up a gas resource of between 1 and 5 TCF in the block. These form the basis of our 171p per share Core NAV estimate.

It is now at the start of a major high impact exploration campaign, which could see the company participate in at least six material wells, testing multi-hundred million or billion barrel prospects with equities of between 8% and 20%. These activities obviously do not come cheaply. We estimate the firm exploration commitments to be of the order of $400m over the next 3-4 years, while discretionary exploration and development expenditure on Bilabri could take the total up to $700m.

US$250 million equity offering In this context, the recently announced equity placement of $250m was required for the company to deliver the planned activity. In theory, cash flow from Bilabri combined with current resources should see the company through the next 3-4 years without recourse to further funding.

With some luck, Equator will finish the exploration programme with up to 3 TCF of gas reserves and up to two material oil discoveries, providing a prospective Core NAV of up to 600p per share. If it gets really lucky it would be possible to see the value over £10 per share.

KBC Peel Hunt Ltd Equator Exploration

4

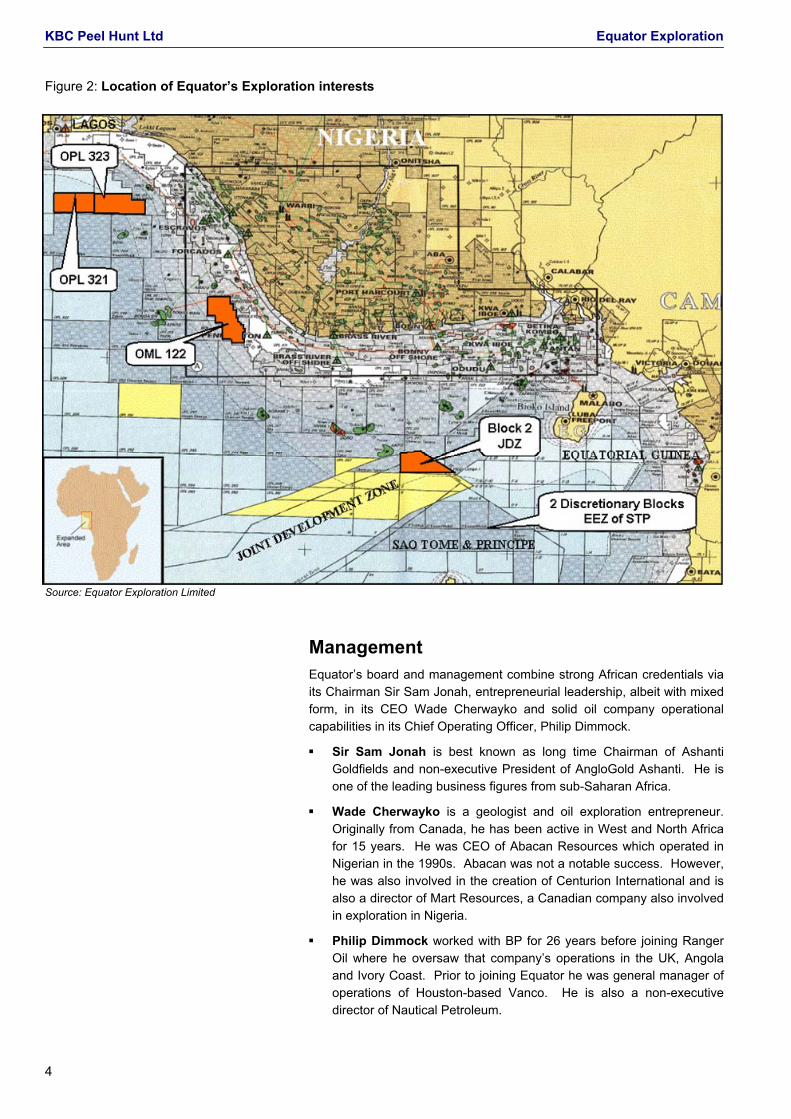

Figure 2: Location of Equator’s Exploration interests

Source: Equator Exploration Limited

Management Equator’s board and management combine strong African credentials via its Chairman Sir Sam Jonah, entrepreneurial leadership, albeit with mixed form, in its CEO Wade Cherwayko and solid oil company operational capabilities in its Chief Operating Officer, Philip Dimmock.

Sir Sam Jonah is best known as long time Chairman of Ashanti Goldfields and non-executive President of AngloGold Ashanti. He is one of the leading business figures from sub-Saharan Africa.

Wade Cherwayko is a geologist and oil exploration entrepreneur. Originally from Canada, he has been active in West and North Africa for 15 years. He was CEO of Abacan Resources which operated in Nigerian in the 1990s. Abacan was not a notable success. However, he was also involved in the creation of Centurion International and is also a director of Mart Resources, a Canadian company also involved in exploration in Nigeria.

Philip Dimmock worked with BP for 26 years before joining Ranger Oil where he oversaw that company’s operations in the UK, Angola and Ivory Coast. Prior to joining Equator he was general manager of operations of Houston-based Vanco. He is also a non-executive director of Nautical Petroleum.

KBC Peel Hunt Ltd Equator Exploration

5

Nigeria OML 122 In April 2005, Equator signed a farm in agreement with local independent Peak Petroleum to undertake the potential development of two oil and gas discoveries and drill a significant exploration prospect in Oil Mining Lease (OML) 122, offshore Nigeria. OML 122 is located 25 to 60 km offshore in water depths of 40 to 300 metres and covers an area of 1,295 km2 on the Western Niger Delta, east of Shell’s Bonga Field (estimated 1.4 billion barrels) on OML 118 and southwest of Shell’s EA Field on OML 79.

Under the terms of the farm-in arrangement, Equator pays 100% of exploration expenditure and the costs of appraising and developing the Bilabri oil field in OML 122 and recovers its costs from production. The profit oil is then divided between Equator and Peak on approximately a 40:60 basis. Development activity beyond the Bilabri oil project is carried out on a direct working interest basis with EEL having a 40% share of both costs and revenues.

Although the block contains discovered oil, it is in a very gassy area and this has historically held back the development of small oil finds. In recent years, the development of gas infrastructure – primarily driven to provide feedstock for the various LNG schemes and with other gas utilisation projects such as gas fired power – has made the handling of associated and non-associated gas technically and economically viable.

The expected wellhead realisations for gas are currently not high. Theoretically, a $6.60/mcf Henry Hub gas price in the US (a level consistent with our long term $40 Brent oil price scenario) should net back through the LNG value chain to a wellhead gas price of $2.40/mcf in Nigeria. However, the commercial reality is that the owners of the LNG liquefaction plants have vast amounts of equity gas and have no pressing need to purchase third party gas. Moreover, LNG netbacks are highly sensitive to a downturn in gas markets. If the US price were to drop to $4.00 per mcf, the netback pricing would render Nigerian gas development sub-economic.

With the current high costs of rigs, equipment and services, it is therefore unlikely that gas would provide strong returns on a stand-alone basis. On the other hand, provided the reserves are sufficiently large and productive and the gas has a reasonable liquids content, the economics would be robust on our current pricing scenario.

Equator has indicated that there is significant interest in securing long term gas supplies from OML 122 and that a memorandum of understanding may be reached with one of the LNG operators later in 2006. Meanwhile, we are assuming in our financial model that it will realise $2.00 per mcf for its gas (effectively a 15% discount to the calculated netback price) and that gas production will not start before 2009.

Strategically, a good option would be to get a foothold on the LNG value chain, starting with an equity position in a liquefaction plant. Such a position may come available – for example, it seems that ChevronTexaco is examining its options about remaining in the Brass LNG scheme – but these things come with a large capital investment requirement and very long payback times.

Farm-in to appraisal of discovered reserves.

Gas prone block – good volume potential but commercially challenging

Aiming for a position in the LNG value chain?

KBC Peel Hunt Ltd Equator Exploration

6

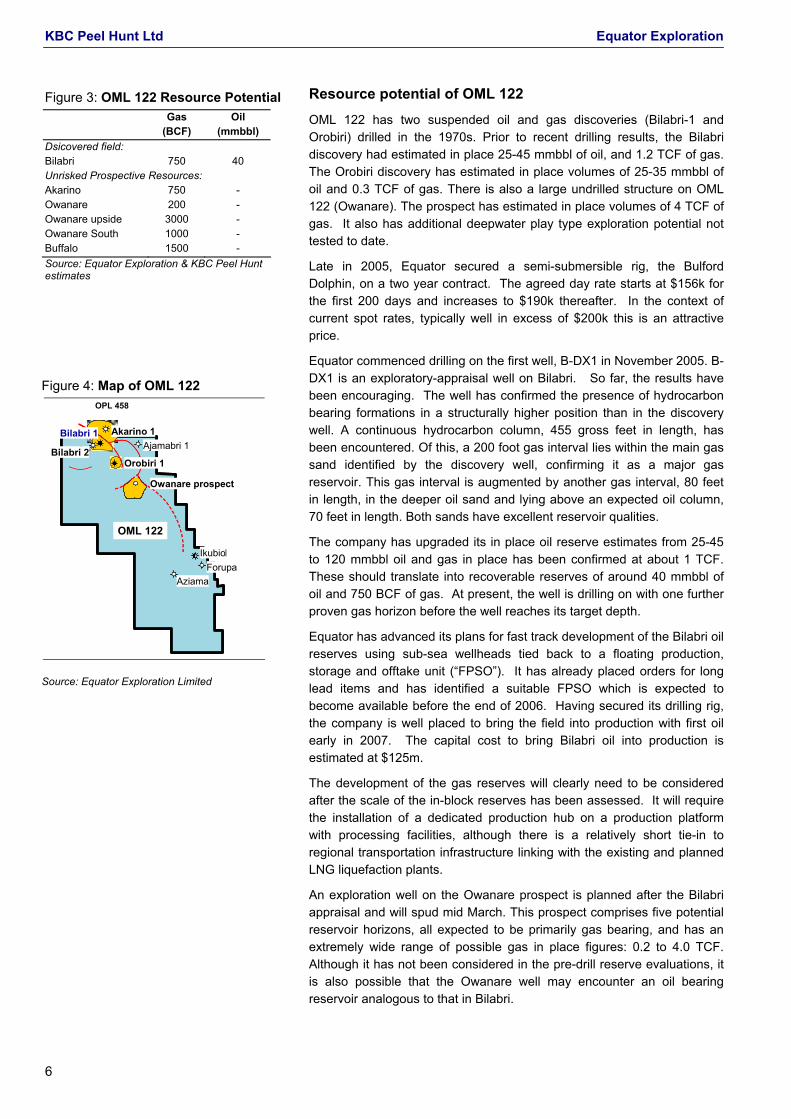

Resource potential of OML 122 OML 122 has two suspended oil and gas discoveries (Bilabri-1 and Orobiri) drilled in the 1970s. Prior to recent drilling results, the Bilabri discovery had estimated in place 25-45 mmbbl of oil, and 1.2 TCF of gas. The Orobiri discovery has estimated in place volumes of 25-35 mmbbl of oil and 0.3 TCF of gas. There is also a large undrilled structure on OML 122 (Owanare). The prospect has estimated in place volumes of 4 TCF of gas. It also has additional deepwater play type exploration potential not tested to date.

Late in 2005, Equator secured a semi-submersible rig, the Bulford Dolphin, on a two year contract. The agreed day rate starts at $156k for the first 200 days and increases to $190k thereafter. In the context of current spot rates, typically well in excess of $200k this is an attractive price.

Equator commenced drilling on the first well, B-DX1 in November 2005. B-DX1 is an exploratory-appraisal well on Bilabri. So far, the results have been encouraging. The well has confirmed the presence of hydrocarbon bearing formations in a structurally higher position than in the discovery well. A continuous hydrocarbon column, 455 gross feet in length, has been encountered. Of this, a 200 foot gas interval lies within the main gas sand identified by the discovery well, confirming it as a major gas reservoir. This gas interval is augmented by another gas interval, 80 feet in length, in the deeper oil sand and lying above an expected oil column, 70 feet in length. Both sands have excellent reservoir qualities.

The company has upgraded its in place oil reserve estimates from 25-45 to 120 mmbbl oil and gas in place has been confirmed at about 1 TCF. These should translate into recoverable reserves of around 40 mmbbl of oil and 750 BCF of gas. At present, the well is drilling on with one further proven gas horizon before the well reaches its target depth.

Equator has advanced its plans for fast track development of the Bilabri oil reserves using sub-sea wellheads tied back to a floating production, storage and offtake unit (“FPSO”). It has already placed orders for long lead items and has identified a suitable FPSO which is expected to become available before the end of 2006. Having secured its drilling rig, the company is well placed to bring the field into production with first oil early in 2007. The capital cost to bring Bilabri oil into production is estimated at $125m.

The development of the gas reserves will clearly need to be considered after the scale of the in-block reserves has been assessed. It will require the installation of a dedicated production hub on a production platform with processing facilities, although there is a relatively short tie-in to regional transportation infrastructure linking with the existing and planned LNG liquefaction plants.

An exploration well on the Owanare prospect is planned after the Bilabri appraisal and will spud mid March. This prospect comprises five potential reservoir horizons, all expected to be primarily gas bearing, and has an extremely wide range of possible gas in place figures: 0.2 to 4.0 TCF. Although it has not been considered in the pre-drill reserve evaluations, it is also possible that the Owanare well may encounter an oil bearing reservoir analogous to that in Bilabri.

Figure 3: OML 122 Resource Potential Gas Oil

(BCF) (mmbbl) Dsicovered field: Bilabri 750 40 Unrisked Prospective Resources: Akarino 750 - Owanare 200 - Owanare upside 3000 - Owanare South 1000 - Buffalo 1500 - Source: Equator Exploration & KBC Peel Hunt estimates

Figure 4: Map of OML 122

Akarino-1-1-

-

Ikubio-1Forupa-1

Aziama-1

Ajamabri-Akarino 1

-1-1

-1

Ajamabri 1

Owanare prospect

Orobiri 1

Bilabri 1

Bilabri 2

IkubioForupa

Aziama

OML 122

OPL 458

Akarino-1-1-

-

Ikubio-1Forupa-1

Aziama-1

Ajamabri-Akarino 1

-1-1

-1

Ajamabri 1

Owanare prospect

Orobiri 1

Bilabri 1

Bilabri 2

IkubioForupa

Aziama

OML 122

OPL 458

Source: Equator Exploration Limited

KBC Peel Hunt Ltd Equator Exploration

7

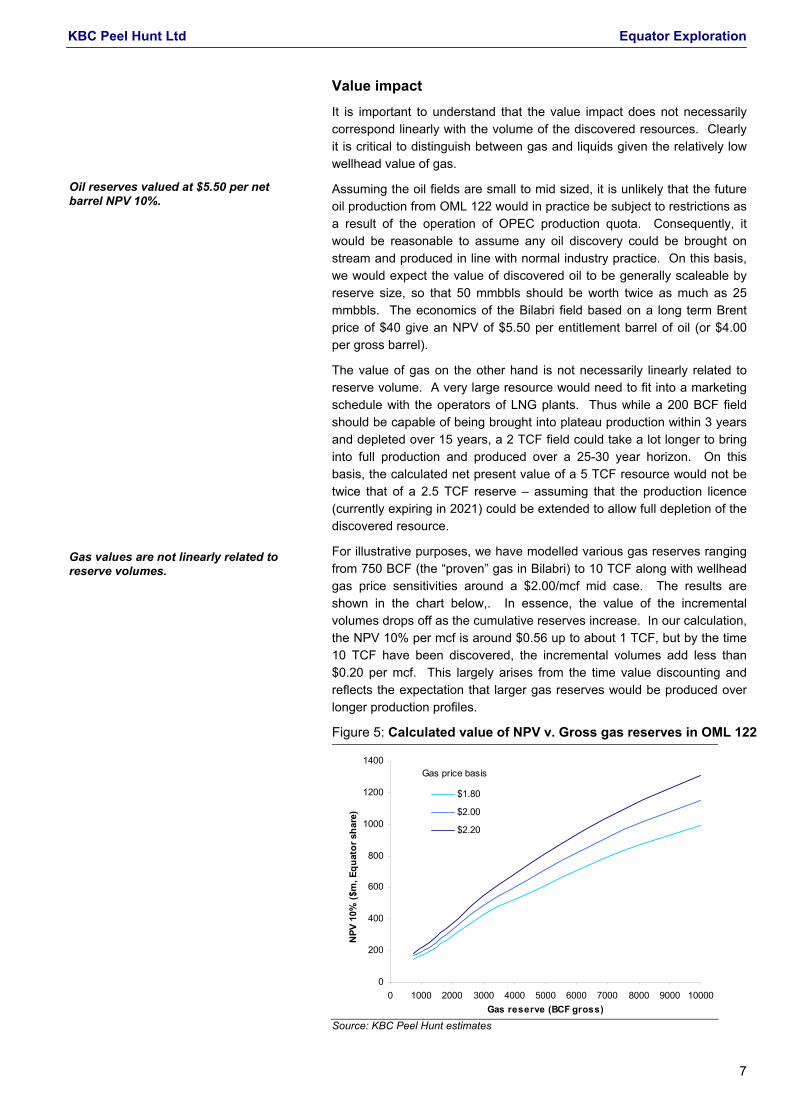

Value impact It is important to understand that the value impact does not necessarily correspond linearly with the volume of the discovered resources. Clearly it is critical to distinguish between gas and liquids given the relatively low wellhead value of gas.

Assuming the oil fields are small to mid sized, it is unlikely that the future oil production from OML 122 would in practice be subject to restrictions as a result of the operation of OPEC production quota. Consequently, it would be reasonable to assume any oil discovery could be brought on stream and produced in line with normal industry practice. On this basis, we would expect the value of discovered oil to be generally scaleable by reserve size, so that 50 mmbbls should be worth twice as much as 25 mmbbls. The economics of the Bilabri field based on a long term Brent price of $40 give an NPV of $5.50 per entitlement barrel of oil (or $4.00 per gross barrel).

The value of gas on the other hand is not necessarily linearly related to reserve volume. A very large resource would need to fit into a marketing schedule with the operators of LNG plants. Thus while a 200 BCF field should be capable of being brought into plateau production within 3 years and depleted over 15 years, a 2 TCF field could take a lot longer to bring into full production and produced over a 25-30 year horizon. On this basis, the calculated net present value of a 5 TCF resource would not be twice that of a 2.5 TCF reserve – assuming that the production licence (currently expiring in 2021) could be extended to allow full depletion of the discovered resource.

For illustrative purposes, we have modelled various gas reserves ranging from 750 BCF (the “proven” gas in Bilabri) to 10 TCF along with wellhead gas price sensitivities around a $2.00/mcf mid case. The results are shown in the chart below,. In essence, the value of the incremental volumes drops off as the cumulative reserves increase. In our calculation, the NPV 10% per mcf is around $0.56 up to about 1 TCF, but by the time 10 TCF have been discovered, the incremental volumes add less than $0.20 per mcf. This largely arises from the time value discounting and reflects the expectation that larger gas reserves would be produced over longer production profiles.

Figure 5: Calculated value of NPV v. Gross gas reserves in OML 122

Source: KBC Peel Hunt estimates

Oil reserves valued at $5.50 per net barrel NPV 10%.

Gas values are not linearly related to reserve volumes.

Gas price basis

0

200

400

600

800

1000

1200

1400

0 1000 2000 3000 4000 5000 6000 7000 8000 9000 10000Gas reserve (BCF gross)

NPV

10%

($m

, Equ

ator

sha

re)

$1.80

$2.00

$2.20

KBC Peel Hunt Ltd Equator Exploration

8

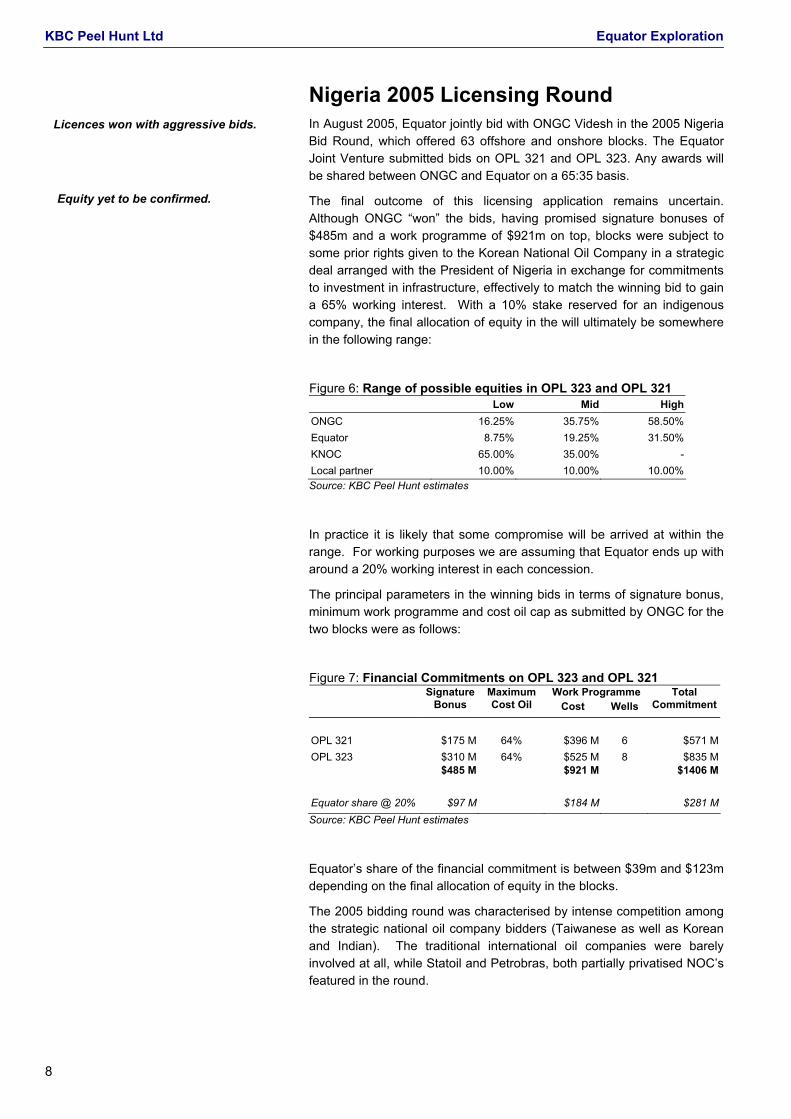

Nigeria 2005 Licensing Round In August 2005, Equator jointly bid with ONGC Videsh in the 2005 Nigeria Bid Round, which offered 63 offshore and onshore blocks. The Equator Joint Venture submitted bids on OPL 321 and OPL 323. Any awards will be shared between ONGC and Equator on a 65:35 basis.

The final outcome of this licensing application remains uncertain. Although ONGC “won” the bids, having promised signature bonuses of $485m and a work programme of $921m on top, blocks were subject to some prior rights given to the Korean National Oil Company in a strategic deal arranged with the President of Nigeria in exchange for commitments to investment in infrastructure, effectively to match the winning bid to gain a 65% working interest. With a 10% stake reserved for an indigenous company, the final allocation of equity in the will ultimately be somewhere in the following range:

Figure 6: Range of possible equities in OPL 323 and OPL 321 Low Mid HighONGC 16.25% 35.75% 58.50%Equator 8.75% 19.25% 31.50%KNOC 65.00% 35.00% -Local partner 10.00% 10.00% 10.00%Source: KBC Peel Hunt estimates

In practice it is likely that some compromise will be arrived at within the range. For working purposes we are assuming that Equator ends up with around a 20% working interest in each concession.

The principal parameters in the winning bids in terms of signature bonus, minimum work programme and cost oil cap as submitted by ONGC for the two blocks were as follows:

Figure 7: Financial Commitments on OPL 323 and OPL 321 Work Programme Signature

Bonus Maximum Cost Oil Cost Wells

Total Commitment

OPL 321 $175 M 64% $396 M 6 $571 MOPL 323 $310 M 64% $525 M 8 $835 M

$485 M $921 M $1406 M

Equator share @ 20% $97 M $184 M $281 MSource: KBC Peel Hunt estimates

Equator’s share of the financial commitment is between $39m and $123m depending on the final allocation of equity in the blocks.

The 2005 bidding round was characterised by intense competition among the strategic national oil company bidders (Taiwanese as well as Korean and Indian). The traditional international oil companies were barely involved at all, while Statoil and Petrobras, both partially privatised NOC’s featured in the round.

Licences won with aggressive bids.

Equity yet to be confirmed.

KBC Peel Hunt Ltd Equator Exploration

9

The general view on the prospectivity of the deep water blocks on offer was that it was reasonably good, although some of the blocks were regarded as fairly high risk.

OPL 321 and 323 both lie at the western side of the western slope of the Niger delta, due south of Lagos, in water depths ranging from 1,000 to 2,500 metres.

OPL 321 OPL 321 contains five mapped structures, including one that is particularly large. According to an Equator presentation, the prospects add up to 13 billion barrels. The key risk is whether there is a migration path from the known source rock into the structures. The winning ONGC bid was well above those from the losing parties and it is noticeable that apparently no bids were received from traditional players.

Clearly the size of the Elephant structure of between 5 and 12 billion barrels recoverable dominates the prospectivity and may have skewed the ONGC bid.

OPL 323 OPL 323 contains six mapped structures with potential of 4.4 to 9.6 billion barrels. There is a stronger technical case for this block and it apparently attracted strong competition from Addax Petroleum as well as bids from both Devon Energy/Amerada Hess and ENI.

The following table is extracted from a recent Equator presentation and reflects the company’s views on the reserve potential and prospect risking. As will be seen later, we have taken a more conservative view on both of these factors.

Figure 8: Prospect Inventory in OPL 321/323 Unrisked Reserves POS Risked Reserves

Low High Low High

OML 323 Whale 1,480 3,220 46% 681 1,481 Lobster 800 1,400 30% 240 420 Gorilla 1,280 3,220 46% 589 1,481 Turtle 270 500 30% 81 150 Giraffe 80 480 61% 49 293 Octopus 520 740 17% 88 126 Total OML 323 4,430 9,560 39% 1,728 3,951 OML 321 Elephant 5,100 11,900 46% 2,346 5,474 Cobra 100 210 30% 30 63 Anaconda 290 600 46% 133 276 Dolphin 50 240 30% 15 72 Total OML 321 5,540 12,950 46% 2,524 5,885 Source: Equator Exploration presentation

Large prospects but commonly regarded as high risk

More numerous prospects and more moderate risk profile.

Company view on prospect size and risk factors is more optimistic than ours.

KBC Peel Hunt Ltd Equator Exploration

10

São Tomé The Democratic Republic of São Tomé and Príncipe, to give it is proper title, is a tiny two-island nation in the Gulf of Guinea. The main region of petroleum interest is sandwiched between territorial waters of Nigeria and Equatorial Guinea. In 2001, the governments of São Tomé and Nigeria reached an agreement over a long-standing maritime border dispute and the countries established the Joint Development Zone (JDZ) governing the previously disputed territory. The principal area of interest to the oil industry is in the JDZ, a jointly administered area between São Tomé and Nigeria.

This area is recognised as an extension to the prolific Nigerian deep water play in which several giant oil and gas accumulations have been discovered in blocks adjacent to the JDZ. A study of the prospects in the JDZ carried out before licensing identified exploration leads with potential resources of up to 4.5 billion barrels.

Chaotic Licensing Process The licensing process, which was initiated in 2003, has been muddied by domestic political conflict and complications, with three separate groups Mobil (now ExxonMobil), ERHC Energy, a small US listed company controlled by a Nigerian businessman, and PGS/Equator having secured various prior rights. Of these, the ERHC position has been a cause of greatest concern.

ERHC had been granted the rights to take between 15% and 30% interests in certain of the JDZ blocks free of signature bonus. The company had secured partnerships with two leading US independents, Pioneer and Noble, which were to operate respectively in Block 2 and Block 4. In December there were reports in the Wall Street Journal that the government of São Tomé had requested for ERHC to be investigated for breach of US anti-corruption laws. First Noble and more recently Devon Energy and Pioneer withdrew their applications and have been replaced respectively by Sinopec and Swiss-based Addax Petroleum, both of which are not impacted by US anti-corruption legislation.

So far, only one PSC has been signed in the JDZ, on Block 1, which was won by Chevron with a $123m signature bonus. AIM-listed Afren Energy (AFR.L) is a 4.4% participant in this block via its joint venture with Nigerian independent Dangote. The first exploration well in the current round is being drilled in Block 1. There is speculation that the signs from this well are encouraging, although the participants are refraining from comment.

While awards for Blocks 2 to 6 were announced in May 2005, the chaos surrounding the ERHC position has made it unclear whether the ratification of the licence awards can meet the latest deadline of end of March 2006. Equator’s position, however, appears to be settled. It was awarded a 5.25% interest as part of a consortium including ONGC and a Nigerian independent Southampton. Equator purchased a further 2.75% its interest recently for a nominal consideration. It is possible that the 35% stake offered to Pioneer and apparently taken up by Sinopec may drop into ONGC’s and Equator’s possession although it is also understood that Chevron may be a strong contender, given that it has strong credentials as an operator and already operates Block 1.

Prospective areas in the outer reaches of the Niger delta.

Licensing process skewed by competing “prior” claims and allegations of corruption.

PSCs on Blocks 2 – 6 to be signed shortly?

KBC Peel Hunt Ltd Equator Exploration

11

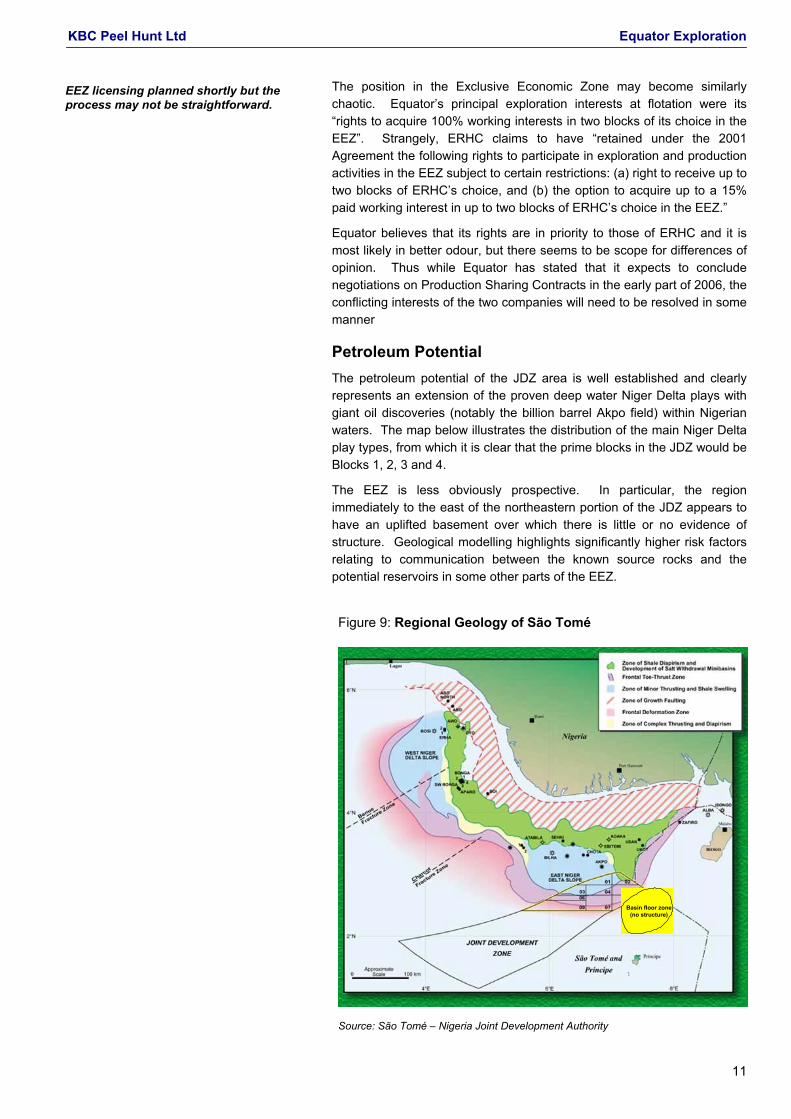

Figure 9: Regional Geology of São Tomé

Basin floor zone(no structure)

Basin floor zone(no structure)

Source: São Tomé – Nigeria Joint Development Authority

The position in the Exclusive Economic Zone may become similarly chaotic. Equator’s principal exploration interests at flotation were its “rights to acquire 100% working interests in two blocks of its choice in the EEZ”. Strangely, ERHC claims to have “retained under the 2001 Agreement the following rights to participate in exploration and production activities in the EEZ subject to certain restrictions: (a) right to receive up to two blocks of ERHC’s choice, and (b) the option to acquire up to a 15% paid working interest in up to two blocks of ERHC’s choice in the EEZ.”

Equator believes that its rights are in priority to those of ERHC and it is most likely in better odour, but there seems to be scope for differences of opinion. Thus while Equator has stated that it expects to conclude negotiations on Production Sharing Contracts in the early part of 2006, the conflicting interests of the two companies will need to be resolved in some manner

Petroleum Potential The petroleum potential of the JDZ area is well established and clearly represents an extension of the proven deep water Niger Delta plays with giant oil discoveries (notably the billion barrel Akpo field) within Nigerian waters. The map below illustrates the distribution of the main Niger Delta play types, from which it is clear that the prime blocks in the JDZ would be Blocks 1, 2, 3 and 4.

The EEZ is less obviously prospective. In particular, the region immediately to the east of the northeastern portion of the JDZ appears to have an uplifted basement over which there is little or no evidence of structure. Geological modelling highlights significantly higher risk factors relating to communication between the known source rocks and the potential reservoirs in some other parts of the EEZ.

EEZ licensing planned shortly but the process may not be straightforward.

KBC Peel Hunt Ltd Equator Exploration

12

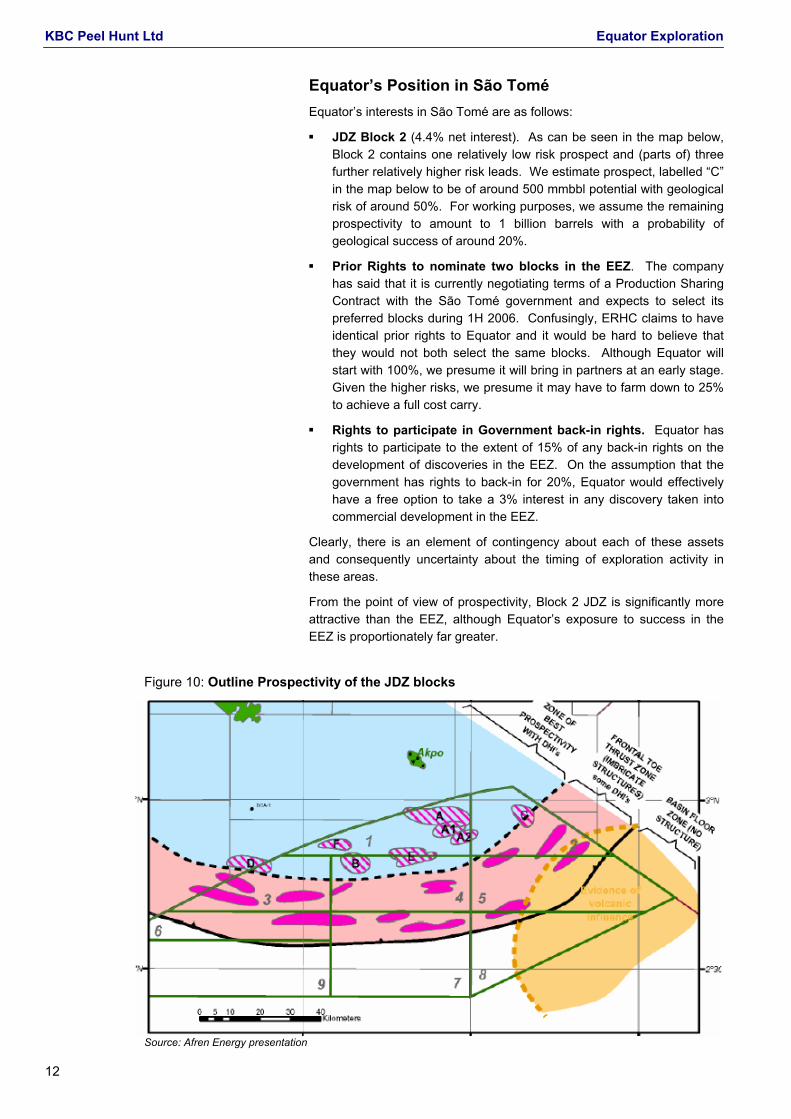

Equator’s Position in São Tomé Equator’s interests in São Tomé are as follows:

JDZ Block 2 (4.4% net interest). As can be seen in the map below, Block 2 contains one relatively low risk prospect and (parts of) three further relatively higher risk leads. We estimate prospect, labelled “C” in the map below to be of around 500 mmbbl potential with geological risk of around 50%. For working purposes, we assume the remaining prospectivity to amount to 1 billion barrels with a probability of geological success of around 20%.

Prior Rights to nominate two blocks in the EEZ. The company has said that it is currently negotiating terms of a Production Sharing Contract with the São Tomé government and expects to select its preferred blocks during 1H 2006. Confusingly, ERHC claims to have identical prior rights to Equator and it would be hard to believe that they would not both select the same blocks. Although Equator will start with 100%, we presume it will bring in partners at an early stage. Given the higher risks, we presume it may have to farm down to 25% to achieve a full cost carry.

Rights to participate in Government back-in rights. Equator has rights to participate to the extent of 15% of any back-in rights on the development of discoveries in the EEZ. On the assumption that the government has rights to back-in for 20%, Equator would effectively have a free option to take a 3% interest in any discovery taken into commercial development in the EEZ.

Clearly, there is an element of contingency about each of these assets and consequently uncertainty about the timing of exploration activity in these areas.

From the point of view of prospectivity, Block 2 JDZ is significantly more attractive than the EEZ, although Equator’s exposure to success in the EEZ is proportionately far greater.

Figure 10: Outline Prospectivity of the JDZ blocks

Source: Afren Energy presentation

KBC Peel Hunt Ltd Equator Exploration

13

Finances Equator has recently raised a total of $310m by way of a two equity placements: $60m in December 2005 and $250m in February 2006 augmenting its cash position which at 30th June was approximately $130 million. At present the company has no significant cash income other than interest on cash balances and, based on the 1H 2005 financials, has an annualised corporate cash burn of $10.0 million.

It also has significant exploration commitments as follows:

Nigeria OML 122. The company has taken a semi submersible rig for a 5 well programme. Assuming an average 60 day per well operation and a day rate of $200k, this amounts to a $60m commitment. The overall costs for other services and consumables associated with a 5 well programme would probably take the total spend to around $90 million.

Nigeria OPL 321 and 323. Depending on the level of equity finally allocated, Equator would need to commit funds of between $13 and $42m for the signature bonuses and a further $25 to $81m for the committed work programme, which however would be spread over a 3-5 year term.

JDZ Block 2. As it has a small working interest, this is a light commitment, estimated at $3.0m representing a 5.25% share of two $30 million wells.

São Tomé EEZ. Equator has to pay in total $4.5m for the two option blocks on signature. It has indicated that it would undertake a seismic programme prior to farming out. This should be manageable with a $10 million budget.

In total, the various commitments total exploration commitments in hand amount to between $263m and $553m, depending on the extent of equity allocation in OPL 321 and OPL 323 in Nigeria.

Figure 11: Exploration Commitments Year End: 31 December 2006 2007 2008 2009 Total

Nigeria OML 122 90.0 90.0Nigeria OPL 321/323* 97.0 61.3 61.3 61.3 281.0JDZ Block 2 15.0 15.0EEZ signature & seismic 5.0 15.0 20.0Total Commitments 192.0 91.3 61.3 61.3 406.0* assumes 20% equity in the blocks

Source: KBC Peel Hunt estimates

Clearly the activity over the coming years will go beyond the minimum financial commitments, specifically to include at least development of the Bilabri oil resources and some additional new venture and discretionary exploration spending. In addition, there will be the need to cover G&A cash burn for the period before the start of production revenues.

We summarise in the table below Equator’s Sources and Uses of funds for the four year period 2006-2009. From this we surmise that the company would in theory be able to deliver an aggressive drilling programme over and above the firm commitments provided all of the free

KBC Peel Hunt Ltd Equator Exploration

14

cash flow from Bilabri is reinvested. It is important to recognise that by the end of 2009, more than half of the Bilabri oil reserves will have been produced.

Figure 12: Sources and Uses of Funds 2006-2009 $ M

Working Capital at 31 Dec 2005 160.0

Placement - February 2006 250.0

Bilabri operating cash flow (2007-2009) 300.7

Total Sources 710.7

Exploration commitments 406.0

Bilabri development 140.0

G&A Cash burn 40.0

Discretionary Exploration Spend 120.0

Total Uses 706.0 Source: KBC Peel Hunt estimates

The above analysis does not take into account development of the gas resources in OML 122, let alone development of any possible discovery in the other exploration areas. At this point, it is probably sensible to continue to treat Equator as primarily a front-end explorer and assume it will either sell on discoveries or sell itself in its entirety at the end of the period contemplated above. It is without doubt some distance (and a lot of additional capital investment) short of becoming a self-sustaining oil company and is for that reason likely to remain a speculative investment.

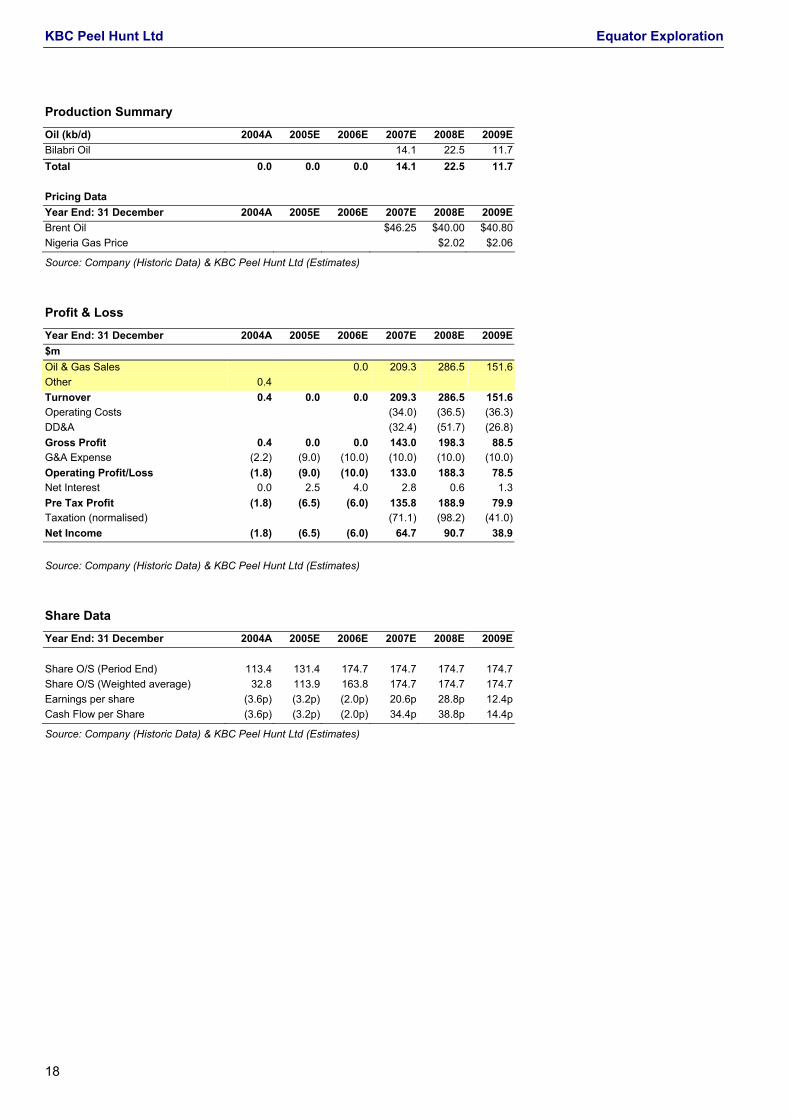

The financial projections included in pages 18-10 below include estimated production only from the Bilabri oil project (i.e. no gas development).

Valuation Equator is rather a difficult stock to put an objective value on at present. Its Core NAV comprises primarily its working capital and the Bilabri oil and gas. Obviously the cash and a sizeable proportion of the value of Bilabri oil will be invested in future exploration and the future direction of the Core NAV will be highly dependent on the success or otherwise of exploration drilling.

As a starting point, we deal with our EMV analysis of the company’s present prospect portfolio. The asset-by-asset breakdown is shown in the following table. In principle we have attempted to focus on the primary prospects in each of the exploration projects. Effectively this involves a degree of high grading what we know about the prospect inventory in each licence area, selecting one of two from each area that would most likely be tested in the next 2-3 years.

The risked valuation clearly depends largely on one’s view of risk. Equator has helpfully provided its views on the geological risks associated with many of its prospects. However, there are also commercial risks need to be taken into account. There is also one further awkward fact: most fields turn out significantly smaller than their pre-drill estimates outnumbering those that turn out larger by a factor of at least 100. Put another way, geologists are not too bad at estimating the chance of geological success but they often overestimate the reserve impact.

Valuation rests on judgements on prospect size and probability of success.

KBC Peel Hunt Ltd Equator Exploration

15

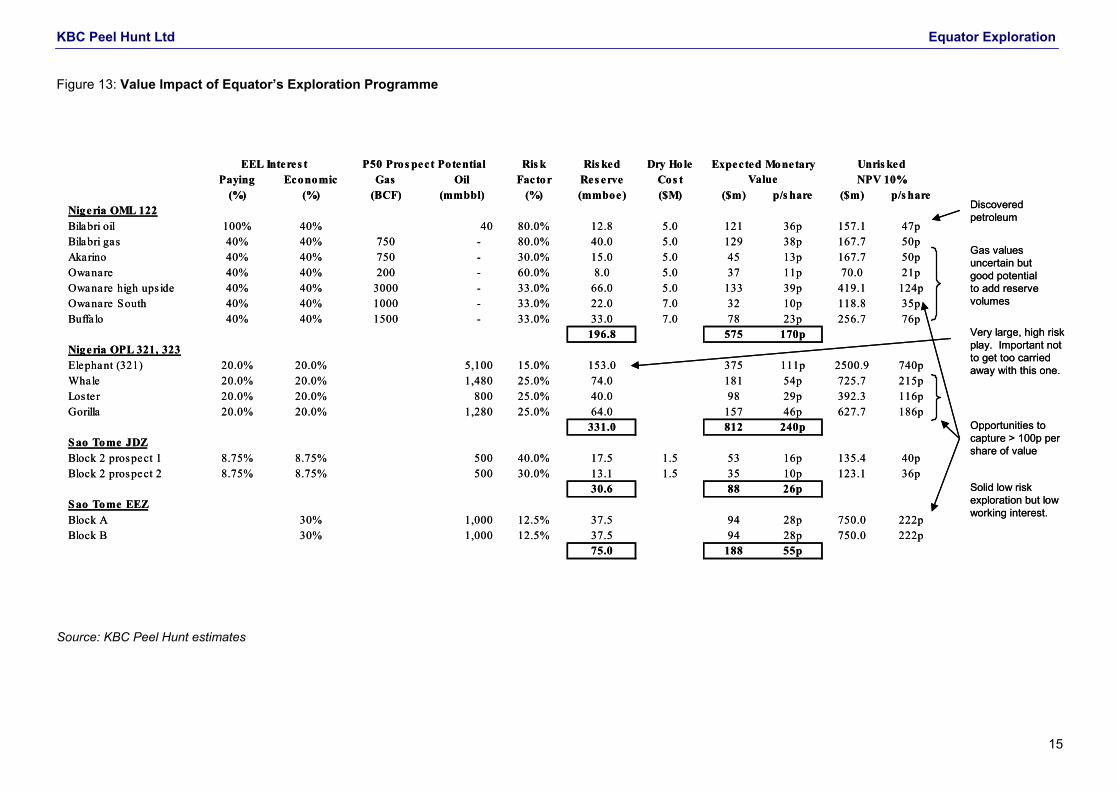

Figure 13: Value Impact of Equator’s Exploration Programme

Source: KBC Peel Hunt estimates

Ris k Ris ked Dry HolePaying Economic Gas Oil Factor Res erve Cos t

(%) (%) (BCF) (mmbbl) (%) (mmboe) ($M) ($m) p/s hare ($m) p/s hareNigeria OML 122Bilabri oil 100% 40% 40 80.0% 12.8 5.0 121 36p 157.1 47pBilabri gas 40% 40% 750 - 80.0% 40.0 5.0 129 38p 167.7 50pAkarino 40% 40% 750 - 30.0% 15.0 5.0 45 13p 167.7 50pOwanare 40% 40% 200 - 60.0% 8.0 5.0 37 11p 70.0 21pOwanare high ups ide 40% 40% 3000 - 33.0% 66.0 5.0 133 39p 419.1 124pOwanare South 40% 40% 1000 - 33.0% 22.0 7.0 32 10p 118.8 35pBuffa lo 40% 40% 1500 - 33.0% 33.0 7.0 78 23p 256.7 76p

196.8 575 170pNigeria OPL 321, 323Elephant (321) 20.0% 20.0% 5,100 15.0% 153.0 375 111p 2500.9 740pWhale 20.0% 20.0% 1,480 25.0% 74.0 181 54p 725.7 215pLos ter 20.0% 20.0% 800 25.0% 40.0 98 29p 392.3 116pGorilla 20.0% 20.0% 1,280 25.0% 64.0 157 46p 627.7 186p

331.0 812 240pSao Tome JDZBlock 2 prospect 1 8.75% 8.75% 500 40.0% 17.5 1.5 53 16p 135.4 40pBlock 2 prospect 2 8.75% 8.75% 500 30.0% 13.1 1.5 35 10p 123.1 36p

30.6 88 26pSao Tome EEZBlock A 30% 1,000 12.5% 37.5 94 28p 750.0 222pBlock B 30% 1,000 12.5% 37.5 94 28p 750.0 222p

75.0 188 55p

P50 Pros pect PotentialEEL Interes t Unris kedExpected Monetary Value NPV 10%

Gas values uncertain but good potential to add reserve volumes

Discovered petroleum

Very large, high risk play. Important not to get too carried away with this one.

Opportunities to capture > 100p per share of value

Solid low risk exploration but low working interest.

Ris k Ris ked Dry HolePaying Economic Gas Oil Factor Res erve Cos t

(%) (%) (BCF) (mmbbl) (%) (mmboe) ($M) ($m) p/s hare ($m) p/s hareNigeria OML 122Bilabri oil 100% 40% 40 80.0% 12.8 5.0 121 36p 157.1 47pBilabri gas 40% 40% 750 - 80.0% 40.0 5.0 129 38p 167.7 50pAkarino 40% 40% 750 - 30.0% 15.0 5.0 45 13p 167.7 50pOwanare 40% 40% 200 - 60.0% 8.0 5.0 37 11p 70.0 21pOwanare high ups ide 40% 40% 3000 - 33.0% 66.0 5.0 133 39p 419.1 124pOwanare South 40% 40% 1000 - 33.0% 22.0 7.0 32 10p 118.8 35pBuffa lo 40% 40% 1500 - 33.0% 33.0 7.0 78 23p 256.7 76p

196.8 575 170pNigeria OPL 321, 323Elephant (321) 20.0% 20.0% 5,100 15.0% 153.0 375 111p 2500.9 740pWhale 20.0% 20.0% 1,480 25.0% 74.0 181 54p 725.7 215pLos ter 20.0% 20.0% 800 25.0% 40.0 98 29p 392.3 116pGorilla 20.0% 20.0% 1,280 25.0% 64.0 157 46p 627.7 186p

331.0 812 240pSao Tome JDZBlock 2 prospect 1 8.75% 8.75% 500 40.0% 17.5 1.5 53 16p 135.4 40pBlock 2 prospect 2 8.75% 8.75% 500 30.0% 13.1 1.5 35 10p 123.1 36p

30.6 88 26pSao Tome EEZBlock A 30% 1,000 12.5% 37.5 94 28p 750.0 222pBlock B 30% 1,000 12.5% 37.5 94 28p 750.0 222p

75.0 188 55p

P50 Pros pect PotentialEEL Interes t Unris kedExpected Monetary Value NPV 10%

Gas values uncertain but good potential to add reserve volumes

Discovered petroleum

Very large, high risk play. Important not to get too carried away with this one.

Opportunities to capture > 100p per share of value

Solid low risk exploration but low working interest.

KBC Peel Hunt Ltd Equator Exploration

16

These caveats aside, risked reserves and Expected Monetary Value provide some useful benchmarks and guide to assessing whether the shares represent fair risk-reward balance. The key issue as far as Equator is concerned is that the prospects are located more or less in the right address – among several of the larger and more productive offshore fields that can be found anywhere in the world today. It is white knuckle exploration but with a reasonably founded expectation of some success.

The table above summarises our calculation of exploration for Equator’s portfolio. The numbers to focus on are Expected Monetary Value, calculated by applying the risk factor (or more accurately probability of success) to the unrisked NPV value. For any individual prospect, the EMV is meaningless as with even the lowest risk exploration prospect, the most likely outcome is a dry hole. Nevertheless, for a sufficiently broad portfolio (which amounts to between 8 and 12 prospects), the calculations begin to match actual outcomes for real exploration programmes.

There are a few points we would like to draw from the above calculation:

There is a cross-section of relatively low risk exploration and appraisal type assets, led by OML 122 in Nigeria which offers proven oil in Bilabri. The JDZ Block 2 falls into this mainly because of the low equity level although of course the scale of the prospect is quite large.

The gas in OML 122 offers the potential to add quite large volumes of reserves but the value impact is very uncertain. We are of the view that the establishment of gross reserve of 3 TCF (net 1.2 TCF) would be a reasonable expectation for the OML 122 drilling programme. Assuming a wellhead realisation of $2.00 per mcf, our analysis suggests a net present value of around $490m or 145p per share net to Equator. This is on top of the value of Bilabri oil as discussed above.

OPL 321 and 323 are the big hitting plays. The calculated EMV, which is based on an assumption that Equator runs with a 20% interest, is an impressive $812 million. Offsetting this is the signature bonus of $107m and the committed work programme of $184m. It is important to remember that it includes two huge prospects, suitably named Elephant and Whale which skew the risk profile of this. We only point out that it would be unwise to get too carried away about this play prior to drilling. Naturally, if drilling on these is successful, the impact would be transforming.

No data is currently available on the EEZ blocks, not least because Equator is yet to announce which blocks it is selecting, although we recognise that they constitute a significant exploration value to Equator. We have put is our model a working assumption that prospects of at least 1 billion barrels can be identified in each block and that Equator will farm down to 30% after acquiring seismic.

Our NAV estimate recasts the EMV sums and serves to provide a snapshot of current value. In the first instance, it is important to recognise that a good deal of the cash resources are effectively spoken for. Nevertheless, we estimate that the company has discretionary cash at present of around $330m or 97p per share.

On top of this, the Bilabri reserve is reasonably certain, at least in respect of the oil and the gas volumes. The above form today’s Core NAV of 171p.

Good spread of prospects but still heavily skewed towards OPL 321/ 323.

Strong working capital position but will be spend in 2-3 years.

KBC Peel Hunt Ltd

17

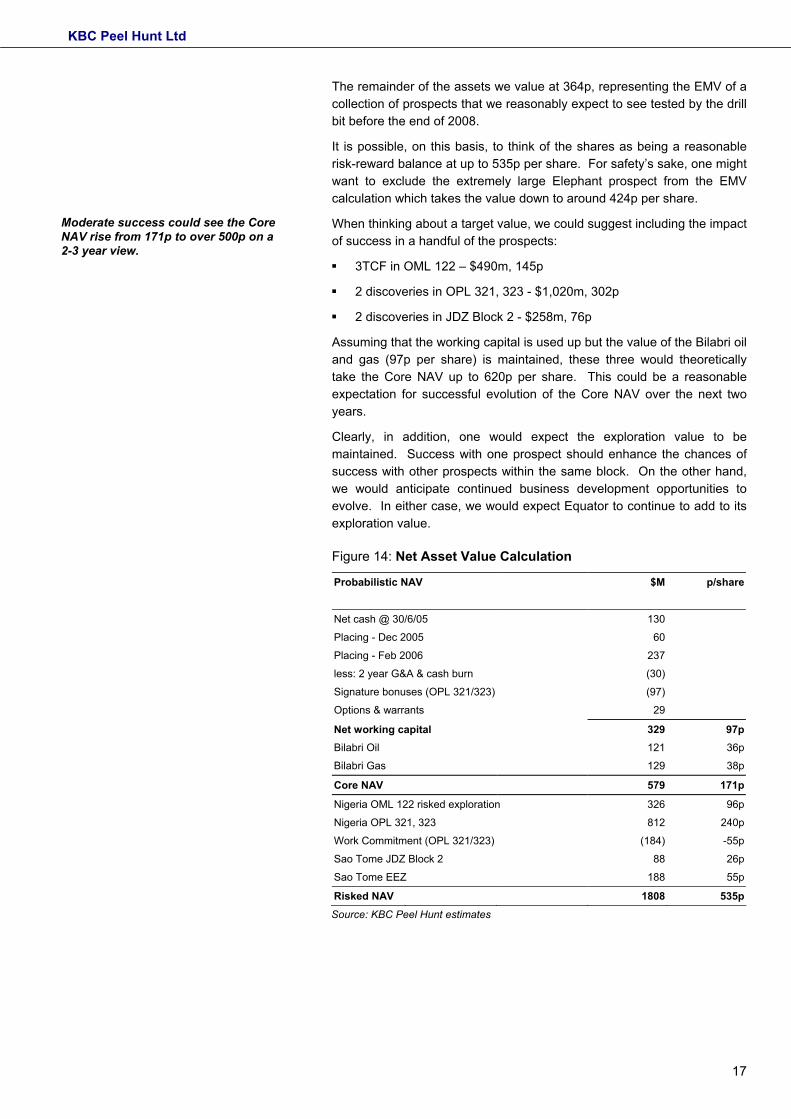

The remainder of the assets we value at 364p, representing the EMV of a collection of prospects that we reasonably expect to see tested by the drill bit before the end of 2008.

It is possible, on this basis, to think of the shares as being a reasonable risk-reward balance at up to 535p per share. For safety’s sake, one might want to exclude the extremely large Elephant prospect from the EMV calculation which takes the value down to around 424p per share.

When thinking about a target value, we could suggest including the impact of success in a handful of the prospects:

3TCF in OML 122 – $490m, 145p

2 discoveries in OPL 321, 323 - $1,020m, 302p

2 discoveries in JDZ Block 2 - $258m, 76p

Assuming that the working capital is used up but the value of the Bilabri oil and gas (97p per share) is maintained, these three would theoretically take the Core NAV up to 620p per share. This could be a reasonable expectation for successful evolution of the Core NAV over the next two years.

Clearly, in addition, one would expect the exploration value to be maintained. Success with one prospect should enhance the chances of success with other prospects within the same block. On the other hand, we would anticipate continued business development opportunities to evolve. In either case, we would expect Equator to continue to add to its exploration value.

Figure 14: Net Asset Value Calculation

Probabilistic NAV $M p/share

Net cash @ 30/6/05 130

Placing - Dec 2005 60

Placing - Feb 2006 237

less: 2 year G&A & cash burn (30)

Signature bonuses (OPL 321/323) (97)

Options & warrants 29

Net working capital 329 97pBilabri Oil 121 36p

Bilabri Gas 129 38p

Core NAV 579 171p

Nigeria OML 122 risked exploration 326 96p

Nigeria OPL 321, 323 812 240p

Work Commitment (OPL 321/323) (184) -55p

Sao Tome JDZ Block 2 88 26p

Sao Tome EEZ 188 55p

Risked NAV 1808 535pSource: KBC Peel Hunt estimates

Moderate success could see the Core NAV rise from 171p to over 500p on a 2-3 year view.

KBC Peel Hunt Ltd Equator Exploration

18

Production Summary

Oil (kb/d) 2004A 2005E 2006E 2007E 2008E 2009EBilabri Oil 14.1 22.5 11.7Total 0.0 0.0 0.0 14.1 22.5 11.7

Pricing Data Year End: 31 December 2004A 2005E 2006E 2007E 2008E 2009EBrent Oil $46.25 $40.00 $40.80Nigeria Gas Price $2.02 $2.06

Source: Company (Historic Data) & KBC Peel Hunt Ltd (Estimates)

Profit & Loss

Year End: 31 December 2004A 2005E 2006E 2007E 2008E 2009E$m Oil & Gas Sales 0.0 209.3 286.5 151.6 Other 0.4 Turnover 0.4 0.0 0.0 209.3 286.5 151.6 Operating Costs (34.0) (36.5) (36.3)DD&A (32.4) (51.7) (26.8)Gross Profit 0.4 0.0 0.0 143.0 198.3 88.5 G&A Expense (2.2) (9.0) (10.0) (10.0) (10.0) (10.0)Operating Profit/Loss (1.8) (9.0) (10.0) 133.0 188.3 78.5 Net Interest 0.0 2.5 4.0 2.8 0.6 1.3 Pre Tax Profit (1.8) (6.5) (6.0) 135.8 188.9 79.9 Taxation (normalised) (71.1) (98.2) (41.0)Net Income (1.8) (6.5) (6.0) 64.7 90.7 38.9

Source: Company (Historic Data) & KBC Peel Hunt Ltd (Estimates)

Share Data

Year End: 31 December 2004A 2005E 2006E 2007E 2008E 2009E

Share O/S (Period End) 113.4 131.4 174.7 174.7 174.7 174.7Share O/S (Weighted average) 32.8 113.9 163.8 174.7 174.7 174.7Earnings per share (3.6p) (3.2p) (2.0p) 20.6p 28.8p 12.4p Cash Flow per Share (3.6p) (3.2p) (2.0p) 34.4p 38.8p 14.4p

Source: Company (Historic Data) & KBC Peel Hunt Ltd (Estimates)

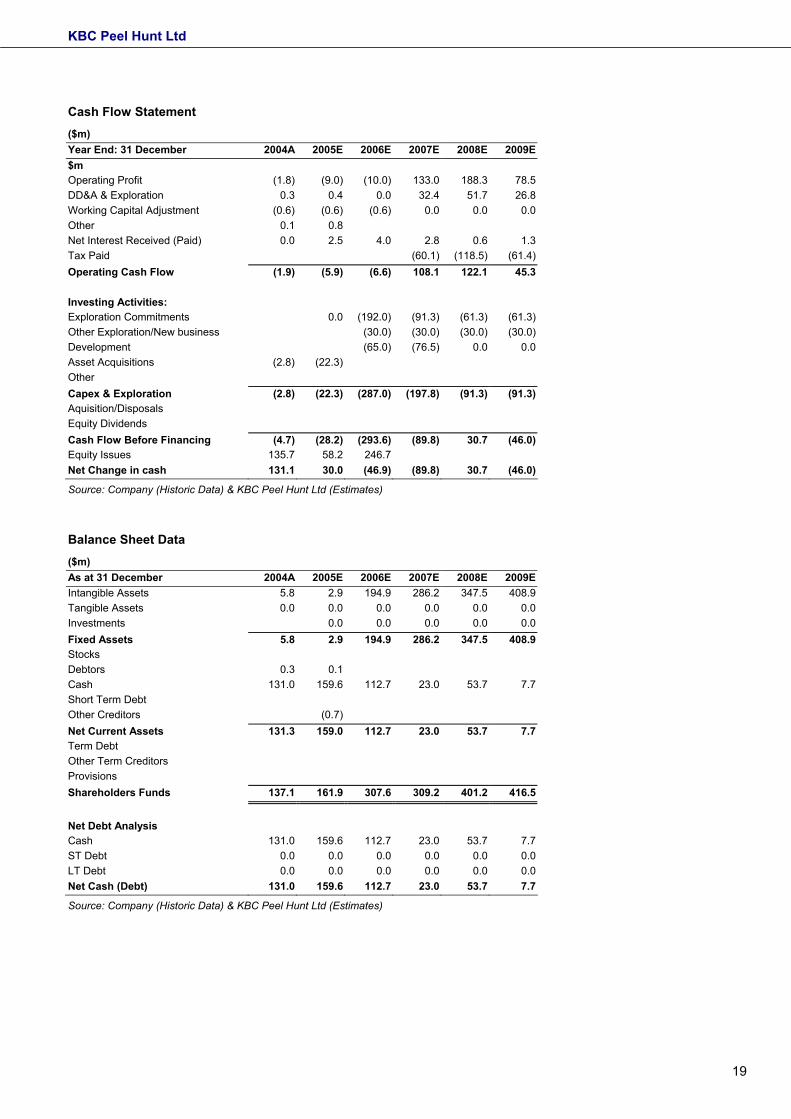

KBC Peel Hunt Ltd

19

Cash Flow Statement ($m) Year End: 31 December 2004A 2005E 2006E 2007E 2008E 2009E$m Operating Profit (1.8) (9.0) (10.0) 133.0 188.3 78.5 DD&A & Exploration 0.3 0.4 0.0 32.4 51.7 26.8 Working Capital Adjustment (0.6) (0.6) (0.6) 0.0 0.0 0.0 Other 0.1 0.8 Net Interest Received (Paid) 0.0 2.5 4.0 2.8 0.6 1.3 Tax Paid (60.1) (118.5) (61.4)Operating Cash Flow (1.9) (5.9) (6.6) 108.1 122.1 45.3

Investing Activities: Exploration Commitments 0.0 (192.0) (91.3) (61.3) (61.3)Other Exploration/New business (30.0) (30.0) (30.0) (30.0)Development (65.0) (76.5) 0.0 0.0 Asset Acquisitions (2.8) (22.3)Other Capex & Exploration (2.8) (22.3) (287.0) (197.8) (91.3) (91.3)Aquisition/Disposals Equity Dividends Cash Flow Before Financing (4.7) (28.2) (293.6) (89.8) 30.7 (46.0)Equity Issues 135.7 58.2 246.7 Net Change in cash 131.1 30.0 (46.9) (89.8) 30.7 (46.0)

Source: Company (Historic Data) & KBC Peel Hunt Ltd (Estimates)

Balance Sheet Data ($m) As at 31 December 2004A 2005E 2006E 2007E 2008E 2009EIntangible Assets 5.8 2.9 194.9 286.2 347.5 408.9 Tangible Assets 0.0 0.0 0.0 0.0 0.0 0.0 Investments 0.0 0.0 0.0 0.0 0.0 Fixed Assets 5.8 2.9 194.9 286.2 347.5 408.9 Stocks Debtors 0.3 0.1 Cash 131.0 159.6 112.7 23.0 53.7 7.7 Short Term Debt Other Creditors (0.7)Net Current Assets 131.3 159.0 112.7 23.0 53.7 7.7 Term Debt Other Term Creditors Provisions Shareholders Funds 137.1 161.9 307.6 309.2 401.2 416.5

Net Debt Analysis Cash 131.0 159.6 112.7 23.0 53.7 7.7 ST Debt 0.0 0.0 0.0 0.0 0.0 0.0 LT Debt 0.0 0.0 0.0 0.0 0.0 0.0 Net Cash (Debt) 131.0 159.6 112.7 23.0 53.7 7.7

Source: Company (Historic Data) & KBC Peel Hunt Ltd (Estimates)

KBC Peel Hunt Ltd Equator Exploration

20

Regulatory disclosures and Disclaimer KBC Peel Hunt Makes a market in this company. This research is an initiation of coverage on this stock.

Recommendation structure, and distribution*

No: %Buy > +20% expected absolute price performance over 12 months 58 22Add +10% to +20% expected absolute price performance over 12 months 12 4.5Hold +/-10% range expected absolute price performance over 12 months 81 31Reduce -10% to -20% expected absolute price performance over 12 months 12 4.5Sell > -20% expected absolute price performance over 12 months 15 6Corporate # 83 32

*Distribution during period 1October 2005 to 31 December 2005

# KBC Peel Hunt Ltd is committed to providing objective investment research, however KBC Peel Hunt Ltd is broker and/or nominated adviser to, or is retained by, this company and is therefore unlikely to be perceived as objective. This research should therefore be considered as non-objective research.

This document is issued by KBC Peel Hunt Ltd, which is authorised and regulated in the United Kingdom by the Financial Services Authority and is a member of the London Stock Exchange; KBC Peel Hunt Ltd is subsidiary of KBC Bank NV.

This document is for the use of the addressees only. It may not be copied or distributed to any other person without the written consent of KBC Peel Hunt Ltd and may not be distributed or passed on, directly or indirectly, to any other class of persons, although KBC Peel Hunt Ltd may in its discretion distribute this document to any other person to whom it could lawfully be distributed by an unauthorised person and without its content being approved by an authorised person.

This document has been prepared using sources believed to be reliable, however we do not represent it is accurate or complete. Neither KBC Peel Hunt Ltd, nor any of its directors, employees or any affiliated company accepts liability for any loss arising from the use of this document or its contents.

This research does not constitute a personal recommendation or take into account the particular investment objectives, financial situations or needs of individual clients.

Analysts are paid in part based on the profitability of KBC Peel Hunt Ltd, which includes remuneration received from investment banking transactions.

KBC Peel Hunt Ltd, its directors, employees or any affiliated company may have a position or holding in any of the securities mentioned herein or in a related instrument.

This document is for distribution in or from the United Kingdom only to persons who are authorised persons or exempted persons within the meaning of the Financial Services and Markets Act 2000 of the United Kingdom or any order made thereunder or to investment professionals as defined in Section 19 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2001.

This research is not for distribution to persons in the United States except that KBC Peel Hunt Ltd may distribute this research in reliance on Rule 15a-6(a)(2) of the Securities Exchange Act 1934 to persons that are major US institutional investors. Orders in any securities referred to herein by any U.S. investor should be placed with KBC Financial Products USA, Inc. and not with any of its foreign affiliates.

In the United States this publication is being distributed to U.S. Persons by KBC Financial Products USA, Inc., which accepts responsibility for its contents.

Where this research is deemed to be objective, KBC Peel Hunt Ltd has published a Conflicts of Interest Policy that is available at http://www.kbcpeelhunt.com/PublicConflictsPolicy.pdf which summarises how KBC Peel Hunt meets the FSA's requirements in this respect. Please note that the share price used in this note was the mid-market price at 3.30pm on 3rd March, 2006.