Epic research special report of 06 aug 2015

8

DAILY REPORT 06 th AUG. 2015 YOUR MINTVISORY Call us at +91-731-6642300 Global markets at a glance Overnight, the S&P 500 and Nasdaq broke a three-day los- ing streak, while the DJI Average inched down amid disap- pointment from Disney's earnings. Mainland markets down China's Shanghai Composite index opened down nearly 1%, extending a 1.6% fall from Wednesday. Asian stocks opened mixed on Thursday, tracking modest offshore gains. CSI300 index sagged 0.2%, while the smaller Shenzhen Composite slipped by the same margin. Hang Seng index shed 0.4 percent, with Wison Engineering Ser- vices in focus. The a supplier to PetroChina has been found guilty of bribery after an investigation by the Chinese gov- ernment and ordered t pay a fine of 30 million yuan. European shares rose on Wednesday with Societe Generale surging as the French bank became the latest major com- pany in the region to post forecast-beating earnings. Euro- pean carmakers, which fell in late July on concerns about a slowdown in their important Chinese market, also rallied, with Renault rising after Exane BNP Paribas increased its price target on the stock. Technology stocks were steady after weakening in the previous session following a slide in Apple shares, but Greek stocks were down for a third straight day with Athens still seeking a new bailout deal. Societe Generale rose 7.9 percent, making it the best per- former in percentage terms on the pan-European FTSEuro- first 300 index, which advanced 1.3 percent. The euro zone's blue-chip Euro STOXX 50 index rose 1.6 percent. Previous day Roundup The market rebounded smartly on Wednesday as bulls took control of Dalal Street with benchmark indices rising more than half a percent led by technology stocks. Sensex rallied 151.15pts to 28223.08 and Nifty rose 51.05pts to 8567.95. The broader markets continued outperformance with BSE Midcap and Smallcap indices gaining 0.8% and 1%, respec- tively. The market breadth remained strong as about 1803 shares advanced against 1156 shares declined on the BSE. Index stats The Market was very volatile in last session. The sartorial indices performed as follow; Consumer Durables [down 3.84pts], Capital Goods [down 98.30pts], PSU [down 6.72pts], FMCG [up 114.31pts], Realty [up 46.05pts], Power [up 17.77pts], Auto [up 200.96pts], Healthcare [up 265.67Pts], IT [down 194.36pts], Metals [down 3.14pts], TECK [up 94.17pts], Oil& Gas [up 15.79pts]. World Indices Index Value % Change D J l 17540.47 -0.06 S&P 500 2099.84 +0.31 NASDAQ 5139.95 +0.67 FTSE 100 6752.41 +0.98 Nikkei 225 20774.90 +0.78 Hong Kong 24412.07 -0.42 Top Gainers Company CMP Change % Chg INFY 1,086.65 29.40 2.78 ZEEL 413.60 10.40 2.58 BAJAJ-AUTO 2,576.10 64.20 2.56 WIPRO 574.15 14.30 2.55 LUPIN 1,681.00 40.50 2.47 Top Losers Company CMP Change % Chg BANKBARODA 188.45 2.60 -1.36 COALINDIA 437.70 5.70 -1.29 YESBANK 831.00 10.65 -1.27 SBIN 284.95 3.65 -1.26 TATAMOTORS 376.00 4.75 -1.25 Stocks at 52 Week’s HIGH Symbol Prev. Close Change %Chg AMARAJABAT 980.55 5.15 0.53 ASIANPAINT 921.90 16.20 1.79 DRREDDY 4,195.00 33.25 0.80 IBULHSGFIN 791.30 5.50 0.70 Indian Indices Company CMP Change % Chg NIFTY 8567.95 +61.05 +0.60 SENSEX 28223.08 +151.15 +0.54 Stocks at 52 Week’s LOW Symbol Prev. Close Change %Chg GAIL 345.00 0.05 0.01

-

Upload

epic-research-private-limited -

Category

Business

-

view

40 -

download

0

Transcript of Epic research special report of 06 aug 2015

DAILY REPORT

06th

AUG. 2015

YOUR MINTVISORY Call us at +91-731-6642300

Global markets at a glance

Overnight, the S&P 500 and Nasdaq broke a three-day los-ing streak, while the DJI Average inched down amid disap-pointment from Disney's earnings. Mainland markets down China's Shanghai Composite index opened down nearly 1%, extending a 1.6% fall from Wednesday. Asian stocks opened mixed on Thursday, tracking modest offshore gains. CSI300 index sagged 0.2%, while the smaller Shenzhen Composite slipped by the same margin. Hang Seng index shed 0.4 percent, with Wison Engineering Ser-vices in focus. The a supplier to PetroChina has been found guilty of bribery after an investigation by the Chinese gov-ernment and ordered t pay a fine of 30 million yuan. European shares rose on Wednesday with Societe Generale surging as the French bank became the latest major com-pany in the region to post forecast-beating earnings. Euro-pean carmakers, which fell in late July on concerns about a slowdown in their important Chinese market, also rallied, with Renault rising after Exane BNP Paribas increased its price target on the stock. Technology stocks were steady after weakening in the previous session following a slide in Apple shares, but Greek stocks were down for a third straight day with Athens still seeking a new bailout deal. Societe Generale rose 7.9 percent, making it the best per-former in percentage terms on the pan-European FTSEuro-first 300 index, which advanced 1.3 percent. The euro zone's blue-chip Euro STOXX 50 index rose 1.6 percent.

Previous day Roundup

The market rebounded smartly on Wednesday as bulls took control of Dalal Street with benchmark indices rising more than half a percent led by technology stocks. Sensex rallied 151.15pts to 28223.08 and Nifty rose 51.05pts to 8567.95. The broader markets continued outperformance with BSE Midcap and Smallcap indices gaining 0.8% and 1%, respec-tively. The market breadth remained strong as about 1803 shares advanced against 1156 shares declined on the BSE.

Index stats

The Market was very volatile in last session. The sartorial indices performed as follow; Consumer Durables [down 3.84pts], Capital Goods [down 98.30pts], PSU [down 6.72pts], FMCG [up 114.31pts], Realty [up 46.05pts], Power [up 17.77pts], Auto [up 200.96pts], Healthcare [up 265.67Pts], IT [down 194.36pts], Metals [down 3.14pts], TECK [up 94.17pts], Oil& Gas [up 15.79pts].

World Indices

Index Value % Change

D J l 17540.47 -0.06

S&P 500 2099.84 +0.31

NASDAQ 5139.95 +0.67

FTSE 100 6752.41 +0.98

Nikkei 225 20774.90 +0.78

Hong Kong 24412.07 -0.42

Top Gainers

Company CMP Change % Chg

INFY 1,086.65 29.40 2.78

ZEEL 413.60 10.40 2.58

BAJAJ-AUTO 2,576.10 64.20 2.56

WIPRO 574.15 14.30 2.55

LUPIN 1,681.00 40.50 2.47

Top Losers

Company CMP Change % Chg

BANKBARODA 188.45 2.60 -1.36

COALINDIA 437.70 5.70 -1.29

YESBANK 831.00 10.65 -1.27

SBIN 284.95 3.65 -1.26

TATAMOTORS 376.00 4.75 -1.25

Stocks at 52 Week’s HIGH

Symbol Prev. Close Change %Chg

AMARAJABAT 980.55 5.15 0.53

ASIANPAINT 921.90 16.20 1.79

DRREDDY 4,195.00 33.25 0.80

IBULHSGFIN 791.30 5.50 0.70

Indian Indices

Company CMP Change % Chg

NIFTY 8567.95 +61.05 +0.60

SENSEX 28223.08 +151.15 +0.54

Stocks at 52 Week’s LOW

Symbol Prev. Close Change %Chg

GAIL 345.00 0.05 0.01

DAILY REPORT

06th

AUG. 2015

YOUR MINTVISORY Call us at +91-731-6642300

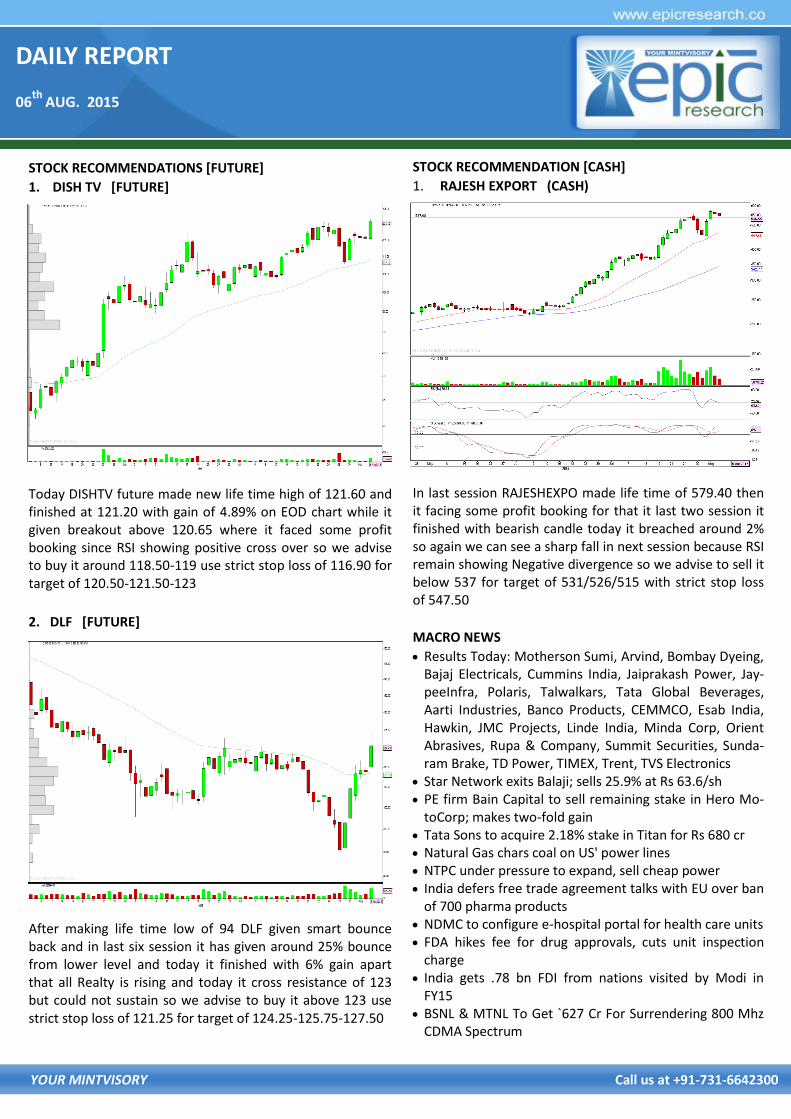

STOCK RECOMMENDATION [CASH]

1. RAJESH EXPORT (CASH)

In last session RAJESHEXPO made life time of 579.40 then it facing some profit booking for that it last two session it finished with bearish candle today it breached around 2% so again we can see a sharp fall in next session because RSI remain showing Negative divergence so we advise to sell it below 537 for target of 531/526/515 with strict stop loss of 547.50

MACRO NEWS

Results Today: Motherson Sumi, Arvind, Bombay Dyeing, Bajaj Electricals, Cummins India, Jaiprakash Power, Jay-peeInfra, Polaris, Talwalkars, Tata Global Beverages, Aarti Industries, Banco Products, CEMMCO, Esab India, Hawkin, JMC Projects, Linde India, Minda Corp, Orient Abrasives, Rupa & Company, Summit Securities, Sunda-ram Brake, TD Power, TIMEX, Trent, TVS Electronics

Star Network exits Balaji; sells 25.9% at Rs 63.6/sh PE firm Bain Capital to sell remaining stake in Hero Mo-

toCorp; makes two-fold gain Tata Sons to acquire 2.18% stake in Titan for Rs 680 cr Natural Gas chars coal on US' power lines NTPC under pressure to expand, sell cheap power India defers free trade agreement talks with EU over ban

of 700 pharma products NDMC to configure e-hospital portal for health care units FDA hikes fee for drug approvals, cuts unit inspection

charge India gets .78 bn FDI from nations visited by Modi in

FY15 BSNL & MTNL To Get `627 Cr For Surrendering 800 Mhz

CDMA Spectrum

STOCK RECOMMENDATIONS [FUTURE]

1. DISH TV [FUTURE]

Today DISHTV future made new life time high of 121.60 and finished at 121.20 with gain of 4.89% on EOD chart while it given breakout above 120.65 where it faced some profit booking since RSI showing positive cross over so we advise to buy it around 118.50-119 use strict stop loss of 116.90 for target of 120.50-121.50-123

2. DLF [FUTURE]

After making life time low of 94 DLF given smart bounce back and in last six session it has given around 25% bounce from lower level and today it finished with 6% gain apart that all Realty is rising and today it cross resistance of 123 but could not sustain so we advise to buy it above 123 use strict stop loss of 121.25 for target of 124.25-125.75-127.50

DAILY REPORT

06th

AUG. 2015

YOUR MINTVISORY Call us at +91-731-6642300

FUTURE & OPTION

MOST ACTIVE PUT OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY PE 8,500 71.60 4,56,440 33,93,150

NIFTY PE 8,400 45.90 3,91,589 40,54,775

BANKNIFTY PE 18,000 61.00 33,716 5,69,000

CANBANK PE 300 10.50 3,178 6,83,000

TATASTEEL PE 260 8.25 1,821 4,20,000

RELIANCE PE 980 16.35 1,813 3,52,000

ICICIBANK PE 300 3.85 1,788 17,65,000

SBIN PE 260 2.05 1,779 21,27,000

MOST ACTIVE CALL OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY CE 8,700 60.20 4,65,370 39,30,575

NIFTY CE 8,800 30.85 3,48,312 47,98,625

BANKNIFTY CE 19,500 165.90 41,596 5,39,325

ADANIENT CE 100 5.50 4,434 8,24,500

TATASTEEL CE 270 7.10 3,958 14,06,000

INFY CE 1,100 19.40 3,775 10,04,500

RELAINCE CE 1,000 19.50 3,769 8,57,000

TATA-MOTORS

CE 400 7.40 3,406 17,73,000

FII DERIVATIVES STATISTICS

BUY OPEN INTEREST AT THE END OF THE DAY SELL

No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores NET AMOUNT

INDEX FUTURES 56228 1312.17 29041 713.86 643185 15426.10 598.31

INDEX OPTIONS 307174 7509.63 292654 7070.65 2511138 67422.94 438.98

STOCK FUTURES 101086 2933.89 96094 2706.35 1795430 50426.56 227.55

STOCK OPTIONS 55963 1517.23 54629 1480.17 87177 2416.66 37.06

TOTAL 1301.90

STOCKS IN NEWS Maruti Suzuki S-Cross launched at a starting price of Rs

8.34 lakh Cognizant Q2 net at $420.1 mn; raises revenue guid-

ance to $3.14 bn OBC cuts deposit rates by 0.25% in select maturities RelCap deal: CCI lets off Sumitomo Mitsui without fine Marico Q1 profit jumps 28% Rs 238cr, volume growth

5% Canara Bank Q1 profit down 41%, NPA up NIFTY FUTURE

NIFTY FUTURE moved around 60 points yesterday. The Index almost remained steady along the day Nifty. Nifty Future though breaks the resistance of 8600 but did not close above it. So for tomorrow we advise you to buy it around 8550 for 8630-8750 with stop loss of 8400

INDICES R2 R1 PIVOT S1 S2

NIFTY 8,614.55 8,591.25 8,568.55 8,545.25 8,522.55

BANK NIFTY 19,133.65 19,065.28 18,966.97 18,830.23 18,731.92

DAILY REPORT

06th

AUG. 2015

YOUR MINTVISORY Call us at +91-731-6642300

RECOMMENDATIONS

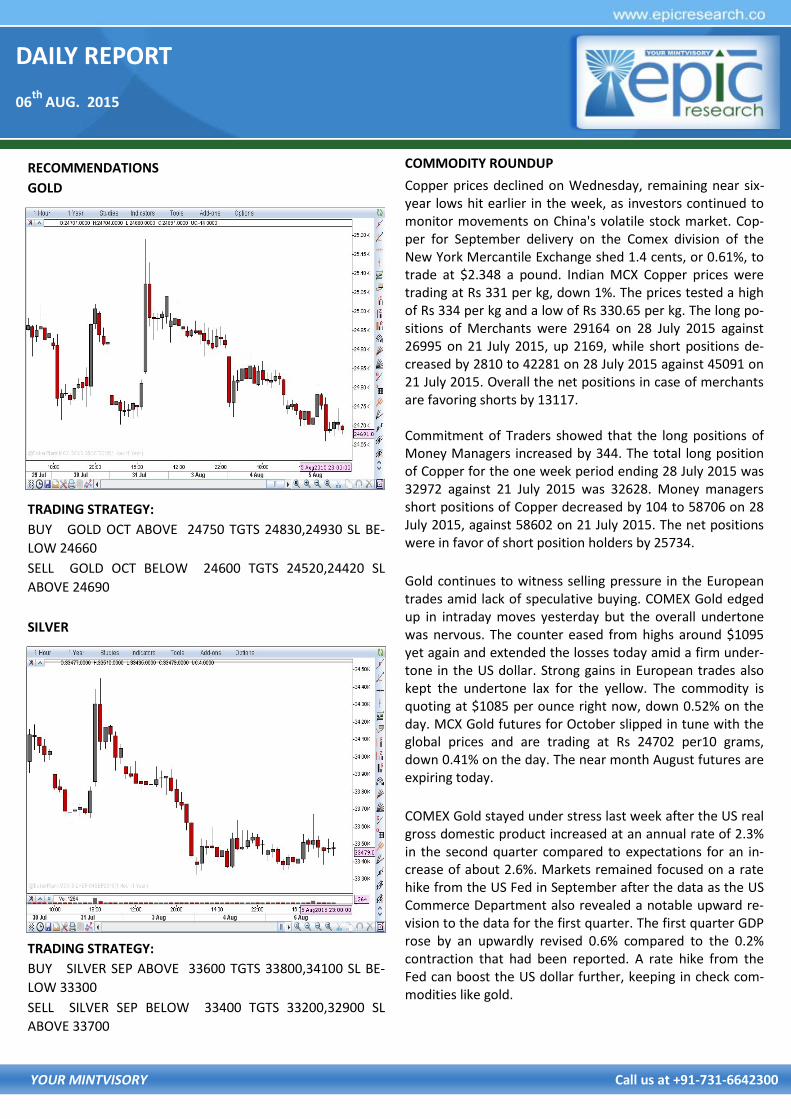

GOLD

TRADING STRATEGY:

BUY GOLD OCT ABOVE 24750 TGTS 24830,24930 SL BE-

LOW 24660

SELL GOLD OCT BELOW 24600 TGTS 24520,24420 SL

ABOVE 24690

SILVER

TRADING STRATEGY:

BUY SILVER SEP ABOVE 33600 TGTS 33800,34100 SL BE-

LOW 33300

SELL SILVER SEP BELOW 33400 TGTS 33200,32900 SL

ABOVE 33700

COMMODITY ROUNDUP

Copper prices declined on Wednesday, remaining near six-year lows hit earlier in the week, as investors continued to monitor movements on China's volatile stock market. Cop-per for September delivery on the Comex division of the New York Mercantile Exchange shed 1.4 cents, or 0.61%, to trade at $2.348 a pound. Indian MCX Copper prices were trading at Rs 331 per kg, down 1%. The prices tested a high of Rs 334 per kg and a low of Rs 330.65 per kg. The long po-sitions of Merchants were 29164 on 28 July 2015 against 26995 on 21 July 2015, up 2169, while short positions de-creased by 2810 to 42281 on 28 July 2015 against 45091 on 21 July 2015. Overall the net positions in case of merchants are favoring shorts by 13117. Commitment of Traders showed that the long positions of Money Managers increased by 344. The total long position of Copper for the one week period ending 28 July 2015 was 32972 against 21 July 2015 was 32628. Money managers short positions of Copper decreased by 104 to 58706 on 28 July 2015, against 58602 on 21 July 2015. The net positions were in favor of short position holders by 25734.

Gold continues to witness selling pressure in the European trades amid lack of speculative buying. COMEX Gold edged up in intraday moves yesterday but the overall undertone was nervous. The counter eased from highs around $1095 yet again and extended the losses today amid a firm under-tone in the US dollar. Strong gains in European trades also kept the undertone lax for the yellow. The commodity is quoting at $1085 per ounce right now, down 0.52% on the day. MCX Gold futures for October slipped in tune with the global prices and are trading at Rs 24702 per10 grams, down 0.41% on the day. The near month August futures are expiring today.

COMEX Gold stayed under stress last week after the US real gross domestic product increased at an annual rate of 2.3% in the second quarter compared to expectations for an in-crease of about 2.6%. Markets remained focused on a rate hike from the US Fed in September after the data as the US Commerce Department also revealed a notable upward re-vision to the data for the first quarter. The first quarter GDP rose by an upwardly revised 0.6% compared to the 0.2% contraction that had been reported. A rate hike from the Fed can boost the US dollar further, keeping in check com-modities like gold.

DAILY REPORT

06th

AUG. 2015

YOUR MINTVISORY Call us at +91-731-6642300

NCDEX

RECOMMENDATIONS

DHANIYA

BUY CORIANDER SEP ABOVE 10840 TARGET 10865 10905

SL BELOW 10810

SELL CORIANDER SEP BELOW 10700 TARGET 10675 10635

SL ABOVE 10730

GUARSGUM

BUY GUARGUM OCT ABOVE 8170 TARGET 8220 8290 SL BE

LOW 8110

SELL GUARGUM OCT BELOW 7970 TARGET 7920 7850 SL

ABOVE 8030

NCDEX ROUNDUP

Fresh buying was seen in mustard seed futures from lower levels on the account of shortage of oilseed in local mandies along with strong millers demand. The NCDEX futures added 0.48% today. As per market sources, daily supplies have been reduced to around 0.50-0.60 lakh bags in the major mandies. These were almost 40 percent lower than the last year due to poor production estimates for the cur-rent year. This has created a shortage of mustard seed in all the mandies. Though strong sowing progress was reported on kharif front. As per latest data release by government , the area under major kharif oilseed has been increased by almost 32% as on 28th July due to strong sowing of soya-bean ,groundnut and sunflower. The NCDEX September fu-tures swelled by 0.48percent today to close at Rs 4161 per quintal. Local Sugar futures soared today amid hopes that the gov-ernment would unveil a fresh slew of measures to prop up the local sugar industry. Most of the participants expect the government to make it compulsory for sugar mills to export surplus supplies in world markets. This is expected to push up the prices in local markets over medium term and can make it the overall scenario viable for the saddled sugar mills. The NCDEX Sugar futures for October are trading at Rs 2288 per quintal, up 2.55% on the day. The counter has edged up throughout the session. While the global sugar prices have constantly cascaded lower, the local market has also witnessed a similar deterioration. The spot market prices are under Rs 20 per kg right now. It is estimated that 25 MT of sugar will be consumed in next season.

NCDEX INDICES

Index Value % Change

CAETOR SEED 3978 -0.30

CHANA 4464 -0.84

CORIANDER 10527 -3.99

COTTON SEED 1897 -0.26

GUAR SEED 3602 +1.67

JEERA 14800 -2.73

MUSTARDSEED 4123 +0.17

REF. SOY OIL 566.85 -0.45

SUGAR M GRADE 7240 -2.27

TURMERIC 1490 -0.07

DAILY REPORT

06th

AUG. 2015

YOUR MINTVISORY Call us at +91-731-6642300

RBI Reference Rate

Currency Rate Currency Rate

Rupee- $ 63.8159 Yen-100 51.2900

Euro 69.3104 GBP 99.1508

CURRENCY

USD/INR

BUY USDINR AUG ABOVE 64.1 TARGET 64.23 64.38 SL BELO

W 63.9

SELL USDINR AUG BELOW 64 TARGET 63.87 63.72 SL ABOVE

64.2

EUR/INR

BUY USDINR AUG ABOVE 64.1 TARGET 64.23 64.38 SL BELO

W 63.9

SELL USDINR AUG BELOW 64 TARGET 63.87 63.72 SL ABOVE

64.2

CURRENCY MARKET UPDATES:

Recovering from initial losses, the rupee on Wednesday closed barely steady at 63.75 against the US dollar on fresh selling of the greenback by banks and exporters amid sus-tained foreign capital inflows in equities. The rupee re-sumed weak at 63.90 against previous closing of 63.74 at the Interbank Forex market and fell further to 63.93 on initial dollar demand from banks and importers on higher greenback in overseas markets. However, it recovered af-terwards to 63.72 on fresh selling of dollars by banks and exporters before finishing at 63.75. The local currency moved in a range of 63.72 and 63.93 per dollar during the day. Meanwhile, the dollar index was up by 0.12% against a basket of six currencies in afternoon trade. The US dollar reversed gains against the other major cur-rencies on Wednesday, after data showed that U.S. non-farm private employment rose less than expected in July, dampening expectations for a U.S. rate hike in September. Earlier in the day, the dollar had strengthened broadly af-ter Federal Reserve Bank of Atlanta President Dennis Lock-hart said Tuesday it would take a “significant deterioration in the economic picture” for him to not support a rate hike in September. The U.S. dollar index, which measures the greenback's strength against a trade-weighted basket of six major currencies, was down at 97.71, after rising to highs of 98.33 earlier in the day. Meanwhile, the euro rose to 1.0904 versus the greenback, off session lows of 1.0849. Data showed that euro zone service sector growth slowed in July, as activity in France and Italy slowed. The euro area services purchasing man-agers' index fell to 53.9 from June's four year high of 54.2. Another report showed that retail sales in the region fell by a larger than forecast 0.6% in June. As against the pound, the dollar pushed lower, with GBP/USD up 0.48% at 1.5640. Data earlier showed that Markit's U.K. services PMI fell to 57.4 in July from 58.5 in June, com-pared to expectations for a reading of 58.0. USD/JPY down 0.19% at 124.12.

DAILY REPORT

06th

AUG. 2015

YOUR MINTVISORY Call us at +91-731-6642300

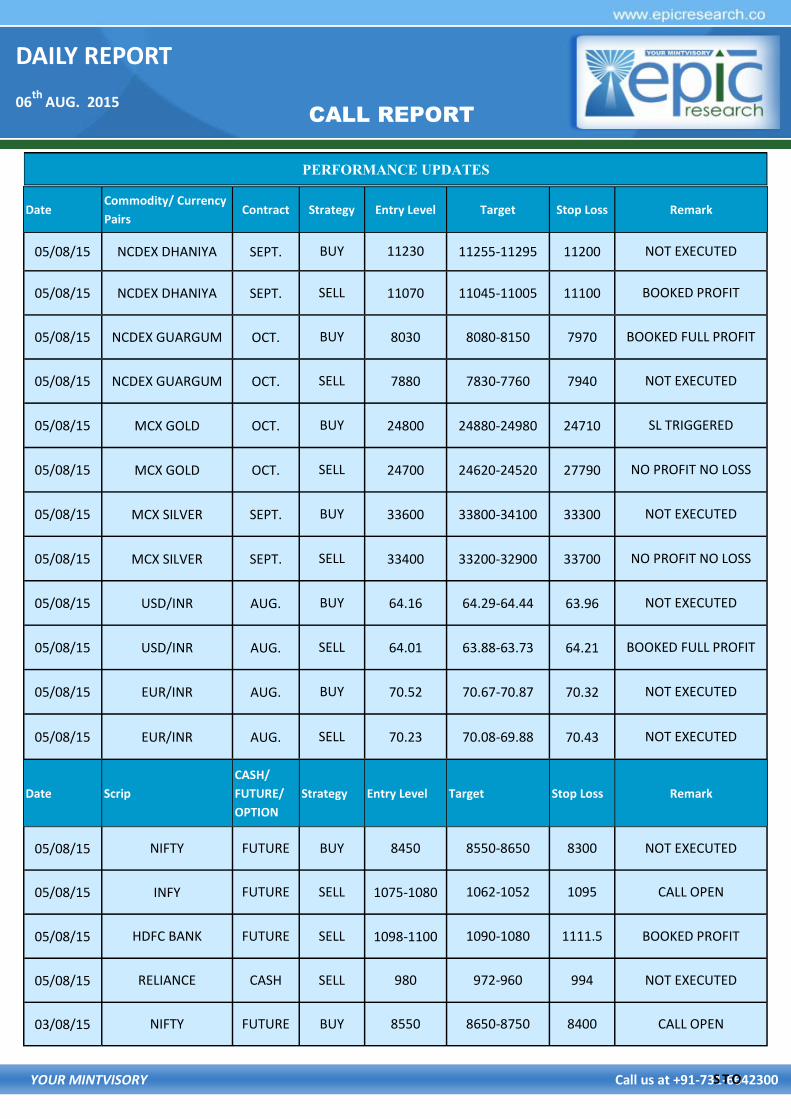

CALL REPORT

S T O

PERFORMANCE UPDATES

Date Commodity/ Currency

Pairs Contract Strategy Entry Level Target Stop Loss Remark

05/08/15 NCDEX DHANIYA SEPT. BUY 11230 11255-11295 11200 NOT EXECUTED

05/08/15 NCDEX DHANIYA SEPT. SELL 11070 11045-11005 11100 BOOKED PROFIT

05/08/15 NCDEX GUARGUM OCT. BUY 8030 8080-8150 7970 BOOKED FULL PROFIT

05/08/15 NCDEX GUARGUM OCT. SELL 7880 7830-7760 7940 NOT EXECUTED

05/08/15 MCX GOLD OCT. BUY 24800 24880-24980 24710 SL TRIGGERED

05/08/15 MCX GOLD OCT. SELL 24700 24620-24520 27790 NO PROFIT NO LOSS

05/08/15 MCX SILVER SEPT. BUY 33600 33800-34100 33300 NOT EXECUTED

05/08/15 MCX SILVER SEPT. SELL 33400 33200-32900 33700 NO PROFIT NO LOSS

05/08/15 USD/INR AUG. BUY 64.16 64.29-64.44 63.96 NOT EXECUTED

05/08/15 USD/INR AUG. SELL 64.01 63.88-63.73 64.21 BOOKED FULL PROFIT

05/08/15 EUR/INR AUG. BUY 70.52 70.67-70.87 70.32 NOT EXECUTED

05/08/15 EUR/INR AUG. SELL 70.23 70.08-69.88 70.43 NOT EXECUTED

Date Scrip

CASH/

FUTURE/

OPTION

Strategy Entry Level Target Stop Loss Remark

05/08/15 NIFTY FUTURE BUY 8450 8550-8650 8300 NOT EXECUTED

05/08/15 INFY FUTURE SELL 1075-1080 1062-1052 1095 CALL OPEN

05/08/15 HDFC BANK FUTURE SELL 1098-1100 1090-1080 1111.5 BOOKED PROFIT

05/08/15 RELIANCE CASH SELL 980 972-960 994 NOT EXECUTED

03/08/15 NIFTY FUTURE BUY 8550 8650-8750 8400 CALL OPEN

DAILY REPORT

06th

AUG. 2015

YOUR MINTVISORY Call us at +91-731-6642300

NEXT WEEK'S U.S. ECONOMIC REPORTS

ECONOMIC CALENDAR

The information and views in this report, our website & all the service we provide are believed to be reliable, but we do not accept any

responsibility (or liability) for errors of fact or opinion. Users have the right to choose the product/s that suits them the most. Sincere ef-

forts have been made to present the right investment perspective. The information contained herein is based on analysis and up on sources

that we consider reliable. This material is for personal information and based upon it & takes no responsibility. The information given

herein should be treated as only factor, while making investment decision. The report does not provide individually tailor-made invest-

ment advice. Epic research recommends that investors independently evaluate particular investments and strategies, and encourages in-

vestors to seek the advice of a financial adviser. Epic research shall not be responsible for any transaction conducted based on the infor-

mation given in this report, which is in violation of rules and regulations of NSE and BSE. The share price projections shown are not nec-

essarily indicative of future price performance. The information herein, together with all estimates and forecasts, can change without no-

tice. Analyst or any person related to epic research might be holding positions in the stocks recommended. It is understood that anyone

who is browsing through the site has done so at his free will and does not read any views expressed as a recommendation for which either

the site or its owners or anyone can be held responsible for . Any surfing and reading of the information is the acceptance of this dis-

claimer. All Rights Reserved. Investment in equity & bullion market has its own risks. We, however, do not vouch for the accuracy or the

completeness thereof. We are not responsible for any loss incurred whatsoever for any financial profits or loss which may arise from the

recommendations above epic research does not purport to be an invitation or an offer to buy or sell any financial instrument. Our Clients

(Paid or Unpaid), any third party or anyone else have no rights to forward or share our calls or SMS or Report or Any Information Pro-

vided by us to/with anyone which is received directly or indirectly by them. If found so then Serious Legal Actions can be taken.

Disclaimer

TIME REPORT PERIOD ACTUAL CONSENSUS

FORECAST PREVIOUS

MONDAY, AUG. 03

8:30 AM PERSONAL INCOME JUNE 0.4% 0.5%

8:30 AM CONSUMER SPENDING JUNE 0.2% 0.9%

8:30 AM CORE INFLATION JUNE 0.1% 0.1%

9:45 AM MARKIT PMI JULY -- 53.8

10 AM ISM JULY 53.2% 53.5%

10 AM CONSTRUCTION SPENDING JUNE 0.7% 0.8%

TBA MOTOR VEHICLE SALES JULY 17.2 MLN 17.1 MLN

TUESDAY, AUG. 04

10 AM FACTORY ORDERS JUNE 1.5% -1.0%

WEDNESDAY, AUG. 05

8:15 AM ADP EMPLOYMENT JULY -- 237,000

8:30 AM TRADE DEFICIT JUNE -$45.8 BLN -$41.9 BLN

10 AM ISM MANUFACTURING JULY 56.0% 56.0%

THURSDAY, AUG. 06

8:30 AM WEEKLY JOBLESS CLAIMS AUG. 1 N/A N/A

FRIDAY, AUG. 07

8:30 AM NONFARM PAYROLLS JULY 215,000 223,000

8:30 AM UNEMPLOYMENT RATE JULY 5.3% 5.3%

8:30 AM AVERAGE HOURLY EARNINGS JULY 0.2% 0.0%

3 PM CONSUMER CREDIT JUNE -- $16 BLN