Environmental Tips for SBA Lenders -...

59

Environmental Tips for SBA Lenders Making Sure Your Reports Are Acceptable to the SBA America East August 13, 2015

Transcript of Environmental Tips for SBA Lenders -...

1

Environmental Tips for

SBA Lenders

Making Sure Your Reports Are

Acceptable to the SBA

America East

August 13, 2015

2

Agenda

1. Technical Overview

2. Overview of SBA SOP 50 10 5 (H) Environmental Policy

3. Submissions – how to make sure they are correct

4. Screen-outs – how to address them

5. Mitigating Factors – how to present them

Lenders’ Reaction to Environmental Issues…

Key Changes to Phase I’s - 2013

Who Qualifies as an

Environmental Professional?

Professional/Educational

Qualifications

Relevant

Experience

Professional engineer or professional

geologist license/registration

3 years

Federal or state license/certification to

perform environmental inquiries

3 years

B.A./B.S. degree or higher in any

science or engineering field

5 years

No B.A./B.S. degree 10 years

Page 5

New: HREC Split

Redefined Historical Recognized Environmental Condition

• Past releases addressed to unrestricted residential use

• Must consider current regulatory framework (rules change)

• HRECs are not RECs

Created new Controlled Recognized Environmental Condition term

• Past releases addressed to non-residential standard, subject to some type of

control

• CRECs are RECs and must be included in the conclusions section of the

report

de minimis” CAN be used to describe an HREC

de minimis” CAN NOT be used to describe a CREC

7

REC-HREC-CREC Relationship

Is it

de

minimis?

Contamination

in, at, or on the

target property

Has it been

Addressed?

Would

Regulatory

official view

clean up as

adequate

today?

De minimis

(Not a REC)

REC

(“Bad REC”)

HREC

(Not A REC)

CREC

(“Good REC”)

Are there

restrictions?

NO

YES

NO

YES

NO

YES

YES

NO

8

CREC Example

CREC vs. HREC distinction:

Consider a warehouse building located in a heavily industrialized area

historically used for manufacturing purposes. Past operations resulted in an

on-site release of solvents to soil and groundwater. Under the direction of

regulatory agency, remediation was conducted and the case was granted

closure. Elevated levels of contaminants (above unrestricted residential levels)

were allowed to be left in place with a land use restriction.

~ Under ASTM E1527-05, this release might have been considered an HREC

based on the fact that regulatory agencies had granted the property closure.

~ Under the E1527-13, this case would fall under a Controlled Recognized

Environmental Condition (CREC) owing to the presence of residual

contamination and an associated land-use restriction.

9

FOOTE V. FLEET FINANCIAL GROUP

The owners purchased the old general store from a bank auction.

Six months after taking out a mortgage, making significant

improvements to the 175-year-old building and moving into it, the

owners discovered that the property’s drinking water was

contaminated by discharges from an old plant on a nearby property.

In the suit, the owners claimed the bank became aware of the

contamination from an environmental report less than two months

before the property auction but failed to disclose it to the buyers and

instead dropped the price.

The Rhode Island Superior Court held the bank liable for more

than $5 million for allegedly failing to disclose knowledge of

drinking water contamination to the property purchasers.

Example: Lender Liability

Agency File/Records Reviews

• Clients thought it was already being done

• Consistency needed

• New language:• Should be conducted for property and adjoining properties

• If not conducted, explain why

• Alternate sources ok

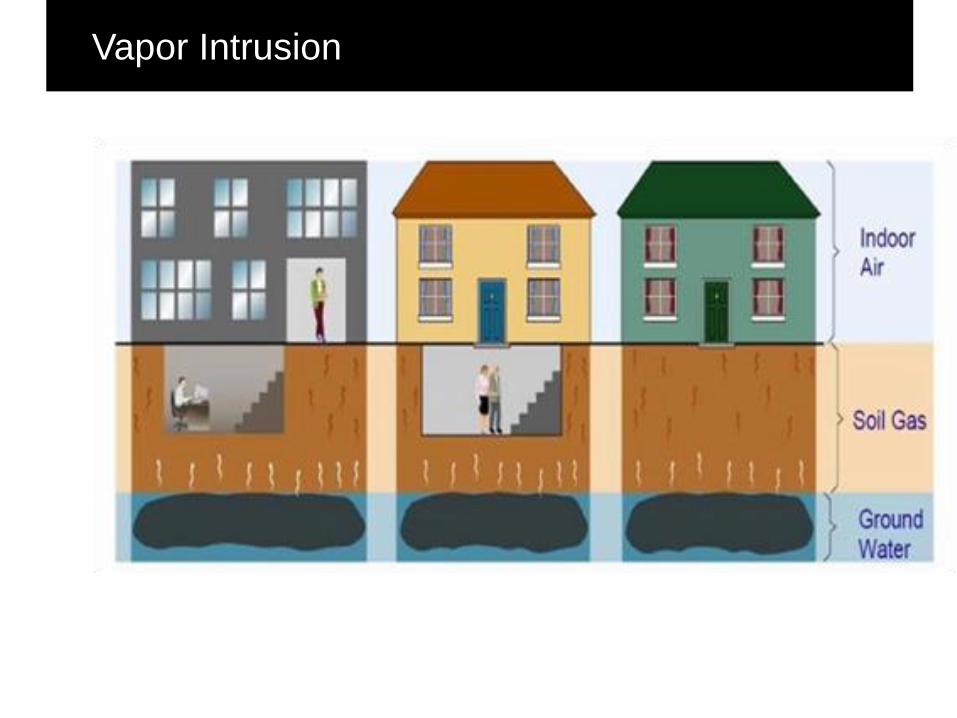

E1527 had been silent on vapor

EPA recommended the task group not ignore

the vapor pathway

2013 revision acknowledges the vapor

pathway in “migration” definition

Clarifies “Indoor Air” non-scope

Vapor

Vapor Intrusion

Task group split about 50/50

Ultimately agreed that:

Recommendations are not required by the standard.

User should consider whether recommendations are desired.

Recommendations are technically considered an additional service

Recommendations

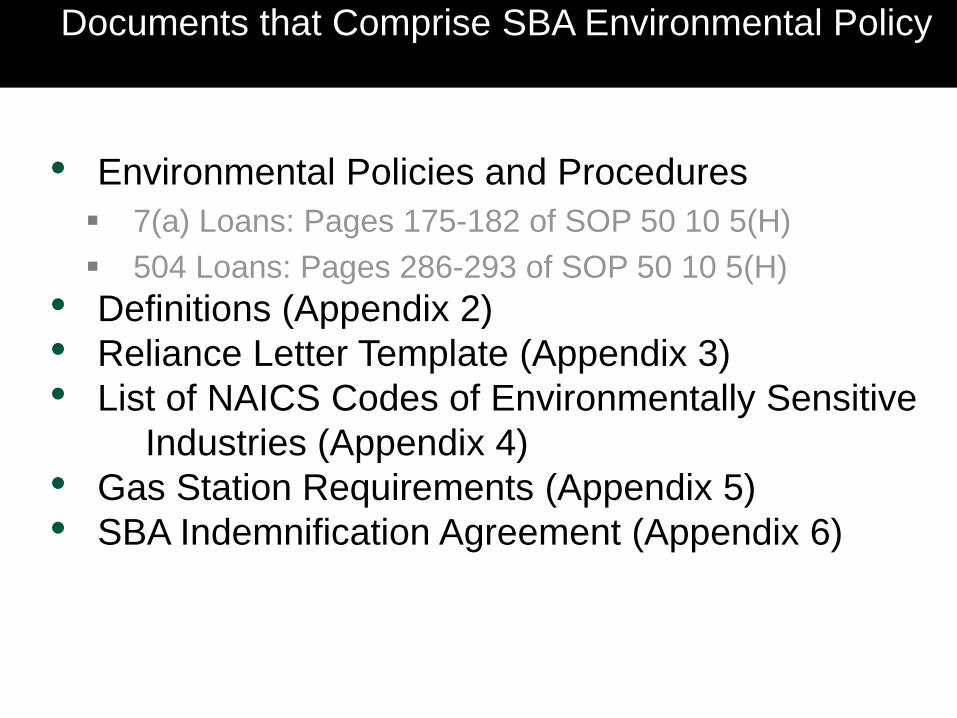

Documents that Comprise SBA Environmental Policy

• Environmental Policies and Procedures

7(a) Loans: Pages 175-182 of SOP 50 10 5(H)

504 Loans: Pages 286-293 of SOP 50 10 5(H)

• Definitions (Appendix 2)

• Reliance Letter Template (Appendix 3)

• List of NAICS Codes of Environmentally Sensitive

Industries (Appendix 4)

• Gas Station Requirements (Appendix 5)

• SBA Indemnification Agreement (Appendix 6)

When Required

• SBA requires an Environmental Investigation of

all commercial Property that will serve as

collateral for an SBA loan Environmental Investigations are no longer limited to “Primary”

Collateral

Environmental Investigations are not required for residential real

estate collateral

Tiered Approach to Environmental

Investigations

• The type and depth of the Environmental

Investigation to be performed varies with the

risks of Contamination SOP 50-10 5(H) provides the minimum standards for

Environmental Investigations

Prudent lending practices may dictate additional Environmental

Investigations or safeguards

Tiered Approach to Environmental

Investigations (Cont.)

• Five types of Environmental Investigations are

recognized by the SBA, each representing a

higher level of environmental due diligence:

Environmental Questionnaire (EQ)

Environmental Questionnaire & “Records Search with Risk Assessment” (RSRA)

Transaction Screen

Phase I Environmental Site Assessment

Phase II Environmental Site Assessment

Environmental Questionnaire

• Lenders use their own EQ, however they must include the minimum areas of inquiry in the definition of “Environmental Questionnaire” on page 329 of the SOP

• SBA will accept the ASTM questionnaire utilized for Transactions Screens (licensed through ASTM)

• The EQ must be completed or reviewed by the Lender*

• The lender must make at least one site visit to the Property

• The person completing the EQ must make a good faith effort to interview the current owner or operator of the Property

• The current owner (which may be the seller) or the operator of the site must sign the EQ. Note: If the current owner or operator of the site will not sign the EQ, an EQ cannot be used. Lender must, at a minimum, obtain a Transaction Screen.

Environmental Questionnaire &

Records Search with Risk Assessment

• An Environmental Questionnaire & Records Search with Risk Assessment for the Property and Adjoining Properties which includes:

A search of government databases (those databases identified in 40 C.F.R. § 312.26 for an AAI-compliant Phase I Environmental Site Assessment)

A search of the historical records (per AAI). Note:

The choice of historical records to be reviewed is at the discretion of the Environmental Professional

Historical records may include, but are not limited to, aerial photographs, city and reverse directories, fire insurance maps, building department records, and land records

Records Search with Risk Assessment (Cont.)

• A “risk assessment" by an Environmental

Professional based on the results of the records

search as to whether the Property is: Elevated Risk or High Risk for Contamination, or

Low Risk for Contamination

• If the risk assessment comes back as either

Elevated Risk or High Risk, a Phase I

Environmental Site Assessment is required

Records Search with Risk Assessment (Cont.)

• The Records Search with Risk Assessment must

identify by name the EP that performed the risk

assessment;

• This report does not need to be addressed to the SBA;

• This report does not need to be accompanied by a

Reliance Letter.

Transaction Screen

• Must comply with ASTM E1528-14 and will include: An interview with the owner or operator of the Property

A site visit to the Property

Completion of an EQ

Review of the Records Search

Conclusion by Environmental Professional

A Transaction Screen Must be completed within one year prior to submission to SBA.

Phase I

• Must be “AAI” compliant (i.e., prepared in accordance with EPA’s regulations for “All Appropriate Inquiries” – An SBA requirement since November 2006)

• A Phase I prepared pursuant to ASTM E1527-13 is “AAI” compliant

• The Environmental Professional must conclude that either: (1) the risk of Contamination at the Property is minimal and no further investigation is warranted, or (2) the risk is sufficient to warrant additional investigation.

(The EP is not required to use this exact phrase but rather may use words to this effect).

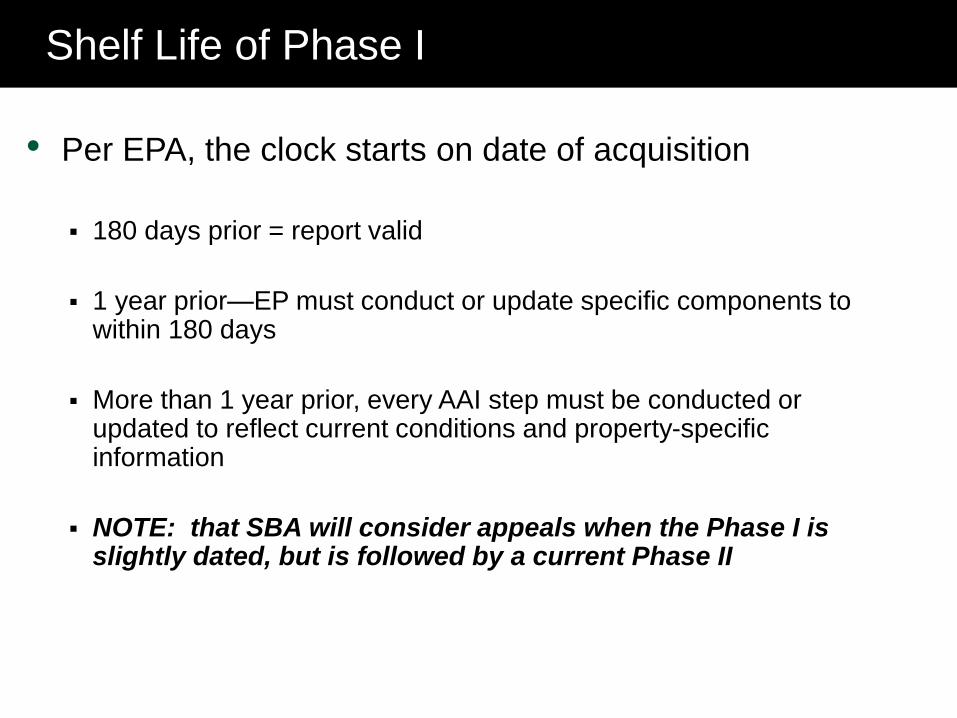

Shelf Life of Phase I

• Per EPA, the clock starts on date of acquisition

180 days prior = report valid

1 year prior—EP must conduct or update specific components to within 180 days

More than 1 year prior, every AAI step must be conducted or updated to reflect current conditions and property-specific information

NOTE: that SBA will consider appeals when the Phase I is slightly dated, but is followed by a current Phase II

Phase II

• Performed by Environmental Professional

• Sampling for contamination in soil and/or groundwater

• Report stating:• Whether Contamination quantities exceed reportable/actionable levels

• Whether Remediation is necessary

• An estimate of Remediation costs

• Any projected completion date for Remediation

Reliance Letter

• All Transaction Screens, Phase I and Phase II reports must be accompanied by the SBA’s template Reliance Letter that appears in Appendix 3 of SOP 50 10 5(F). The Reliance Letter may not be modified in any respect.

• The Reliance Letter must be addressed to the Lender and to SBA.

• Evidence of the Environmental Professional’s Errors & Omissions Liability Insurance with minimum coverage of $1 million per claim (or occurrence) must be attached to the Reliance Letter. (Lender and SBA do not have to be named insureds or loss payees).

• Lender or SBA may provide Borrower with a copy of the Environmental Investigation for informational purposes only.

Steps of the Environmental Investigation

• NAICS Codes – Lenders and CDCs first determine the NAICS codes for the property’s current and known prior uses and compare them to the list of NAICS codes of environmentally sensitive industries in Appendix 4. If there is a match, then the environmental investigation must begin with a Phase I.

Exception:1. If the property is multi-unit building, lenders may begin with a Records Search with Risk Assessment (RSRA)

If no NAICS Code match….

• Loans up to $150,000 – The investigation may begin with an Environmental Questionnaire (EQ). If the EQ reveals that contamination is unlikely, this is sufficient.

• Loans over $150,000 – The investigation must, at a minimum, begin with an Environmental Questionnaire and a “Records Search with Risk Assessment.” (RSRA)

• Properties identified on the RSRA as “Elevated Risk” or “High Risk” require a Phase I. Properties identified as “Low Risk” are cleared, provided the Environmental Questionnaire is also clean (if not, a TSA is an option).

Sample SBA Policy Matrix

Minimum Due Diligence Requirements

Real Estate Loan

Type

<$150K $150K < $5MM

Low Risk Loans Questionnaire RSRA/TSA

High Risk* Loans –

NAICS Codes

Phase I Phase I

Gas Station Phase I + Evidence of UST

Compliance

Phase I + Evidence of UST

Compliance

Dry Cleaners Phase I Phase I

Dry Cleaner (older than 5

years old)

Phase I and Phase II Phase I and Phase II

Special Use Facilities

(i.e. Daycare)

More specific requirements (i.e.

Lead Paint Testing, Lead in

Drinking Water, etc)

More specific requirements (i.e.

Lead Paint Testing, Lead in

Drinking Water, etc)

NAICS Codes Match – Special Rule if Current

Use is as a Gasoline Station

• If there is a NAICS code match is to a gas station

(NAICS Code 447 – Gasoline stations with or without

convenience stores) and the use of the property will be

as a gas station, lenders must refer to the

“Requirements Pertaining to Gas Station Loans” in

Appendix 5.

• In addition to Phase I, gas station loans must include a

determination by the EP stating whether or not the gas

station is in compliance with all state requirements, if

any, pertaining to tank and equipment testing.

Collateral is

CRE?yes

no

No EI needed

Appendix 4

NAICS Code match?(Environmentally

Sensitive Industry)

Loan Amount?

yes Dry Cleaner or

Gas Station? Appendix 5

(Gas Station)

> $150,000$150,000 or <

EQ EQ + RSRA

Phase I

Phase II

Other Further Investigation

Remediation

RSRA

Submit to SBA or if

Elevated or High Risk resultSubmit to SBA or if

Further Investigation Warranted

no no

Submit to SBA or if

Further Investigation Warranted

GENERAL STEPS OF AN SBA ENVIRONMENTAL INVESTIGATION (EI)

SBA Reece/Last updated 5.27.2014

Note: This chart is for guidance purposes only. For a more detailed explanation of the EI process, including exceptions and additional

requirements for gas stations, commercial condominiums and special use facilities, such as child care centers and dry cleaners, refer to

SOP 50 10 5(F), effective January 1, 2014, beginning at page 174 for 7(a) loans and at page 288 for 504 loans.

Submit to SBA or if

Elevated or High Risk result

Submit to SBA

No matter the

loan amount

Section H

(Dry Cleaner)

Contaminated Properties

• If requesting approval of funds with known

contamination, on-going remediation, monitoring, or

CRECs on the property, then

Ensure all information is submitted in accordance with SBA SOP

50 10 5(H), Subsection G, Approval and Disbursement of Loans

When There is Contamination or Remediation.

• If the environmental professional concludes that no

further investigation is warranted, but the Phase I

Assessment reveals “contamination” at the property, a

response to Subsection G is required.

32

Screenout Reasons and Tips to Avoid them

7(a) Loans Environmental reviews• PLP lenders conduct their own reviewsOther 7(a) Lenders must follow the Authorization which requires Lenders to obtain the Center’s concurrence before disbursement.

Exception- When there is known contamination, it must have Center counsel concurrence prior to authorization approval.

• Center has no forms, but follow SOP strictly.• Jurisdictional questions are referred to local

District Counsel. For example, in Michigan, there’s a Baseline Environmental Assessment (BEAs).

Screenout Reasons and Tips to Avoid them

Submission to Sacramento Loan Processing

Center (SLPC)

• Ensure all documents are legible, all

appendices and attachments are included.

• Use “EX-16 Environmental” when using the

E504 system.

• CDC Checklist (with loan number or control

number) included with comments matching

EP’s recommendations and conclusions.

Screenout Reasons and Tips to Avoid them

• More than one property? Need a CDC

Checklist for each one.

• More than one SBA 504 loan? –Submit a copy

of the environmental along with any previous

SBA environmental approvals for SBA to cross-

reference. All submittals will be re-reviewed.

Screenout Reasons and Tips to Avoid them

Reliance Letters• Included with any TSAs, Phase I or Phase II, along

with the Certificate of Professional Liability Insurance.

• Text must not be altered. No need to insert name of EP firm as it slows down the processing. See next slide showing highlights of what needs to be filled out.

• Only CDC and SBA need be named in reliance letters.

• CDC should be named as “Lender” in the template. Not Third party lender.

37

Screenout Reasons and Tips to Avoid them

Address Changes:

• Addresses on CDC Checklist, environmental

documents and loan authorizations should

match. If not, provide explanation.

• Resubmissions- send only what is requested

and follow instructions provided in the response

from Sacramento Loan Processing Center

(SLPC)

Mitigating Factors

1. Indemnification Lender must perform an analysis of the financial resources of the

proposed Third Party Indemnitor and conclude that sufficient

resources exist to complete remediation;

The template SBA Indemnification Agreement in Appendix 6 must

be utilized

The SBA Environmental Indemnification

Agreement

The SBA Environmental Indemnification

Agreement Cannot be modified, except for formatting and completing blank

lines, signature blocks and notary acknowledgments

Must also be executed by the Borrower and, for an EPC/OC loan,

the Operating Company

Must have a copy of the Environmental Investigation Report

attached

The SBA Environmental

Indemnification Agreement (Cont.)

• All lenders (except when submitting requests through PLP, SBA Express and the Pilot Loan Programs) must submit the finalized SBA Environmental Indemnification Agreement to SBA for review and approval prior to funding the loan.

• For 504 loans, this includes PCLP CDCs. Submission must be made no less than 2 weeks prior to the CDC’s Loan Closing Package cutoff date of the District Counsel where the loan will be sent for closing.

• A Memorandum of the SBA Environmental Indemnification Agreement, once approved, must be recorded in the applicable land records.

Mitigating Factors (Cont.)

2. Completed Remediation – If government entity

has affirmed in writing that active remediation is

complete but addition monitoring is required,

approval or disbursement may occur if: Monitoring Results for first year obtained;

Environmental Profession affirms that there is no unacceptable

increase in contamination;

Property owner is in compliance with any continuing obligations

imposed by the governmental entity.

Mitigating Factors (Cont.)

3. “No Further Action” – If a lender obtains a “no further action letter” or “closure letter” from a governmental stating that no further remediation or monitoring is required.

4. “Minimal Remediation” – If the extent of contamination and cost of remediation is minimal in relation to the value of the Property and/or the resources of the person responsible for remediation, and remediation is projected to be completed within one year.

Mitigating Factors (Cont.)

5. Clean-up Funds – If there is evidence from a governmental entity that the borrower or the property has been approved by a fund to pay for or reimburse remediation costs, and the amount allocated is sufficient to cover remediation. The Lender must also address the financial capability of the fund.

6. Escrow Account – If an escrow account is established which equals a minimum of 150% of the total estimated cost of the remediation, which escrow account is controlled by the 7(a) lender or first mortgage holder on a 504 loan.

Mitigating Factors (Cont.)

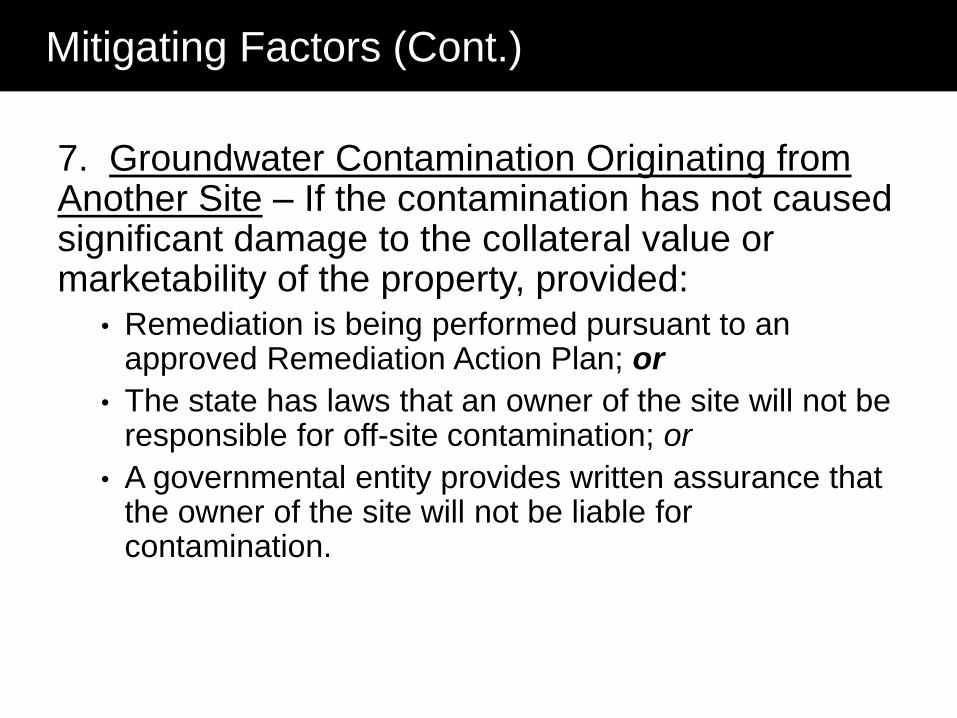

7. Groundwater Contamination Originating from Another Site – If the contamination has not caused significant damage to the collateral value or marketability of the property, provided:

• Remediation is being performed pursuant to an approved Remediation Action Plan; or

• The state has laws that an owner of the site will not be responsible for off-site contamination; or

• A governmental entity provides written assurance that the owner of the site will not be liable for contamination.

Mitigating Factors (Cont.)

8. Additional or Substitute Collateral – If additional

or substitute collateral is being pledged, or an

additional equity contribution is being made,

sufficient to overcome the potential loss due to

Contamination, then approval or disbursement

may be considered.

Mitigating Factors (Cont.)

9. “Other Factor(s)” – Lender or SBA may rely upon factors other than those outlined above, including but not limited to adequate environmental insurance, bonds, agreements from the Governmental Entity not to sue present and future property owners, Engineering Controls, Institutional Controls or Restrictive Covenants in land records.

***Note: Use of Other Factors alone requires approval from the SBA Environmental Committee for all lenders, including PLP lenders and PCLP CDCs***

Gas Stations

• For contaminated gas stations, at a minimum, the

SBA Indemnification Agreement must always be

obtained and signed by the seller.

• A Phase I Environmental Site Assessment should

always be obtained if the business sells, supplies, or

dispenses fuel, gasoline, or heating oil, even if the

NAICS code for the business is not identified on the

list of environmentally sensitive industries.

48

Special Use Properties

If a property is a dry cleaning facility and has

been in operation for more than 5 years, a

Phase I and Phase II Environmental Site

Assessment are required.

49

The Phase II Environmental Site Assessment must

be conducted by a Professional Engineer (PE) or a

Registered Geologist (RG)

Special Use Properties

If a property is a daycare center, child care

center, nursery school or a residential care

facility occupied by children and the date of

construction is prior to 1980, a lead risk

assessment (for lead based paint) and testing

for lead in drinking water are required.

50

Concentrated Animal Feeding Operations

(CAFO)

If a property is a CAFO, include the following with your environmental

submission:

•A copy of a CAFO Environmental Questionnaire.

•A copy of the Comprehensive Nutrient Management Plan (CNMP).

•A copy of the CAFO permit.

•A statement from the borrower setting forth how the animal waste and deceased

animals will be disposed.

•A copy of the NPDES Permit

(if treated waste is discharged into a water source)

•A copy of the Land Based Discharge Permit

(if the waste will be disposed of on land)

51

Energy Reports

• All energy reports submitted to meet the Energy Public

Policy Goals are currently being reviewed by SBA

environmental engineers. Energy goals include: a)

reduction of existing energy use, b) use of sustainable

designs, and c) use of renewable energy sources.

• The energy report must include the qualifications of

the party performing the energy audit, engineering

report, or other professional evaluation, each of which

must be performed by an independent third party (an

entity other than the applicant, the interim lender, the

third party lender or any of their respective affiliates).

52

Energy Reports

Energy Reduction Goal – $5.5 million eligibility

• The energy report must demonstrate 10% energy reduction. If

the project involves the construction or acquisition of a

facility (the “new facility”), the new facility must replace an

existing facility and the new facility must use 10% less energy

than the existing facility.

• The new facility must be located in the same local area (e.g.

the same city, town, county, zip code, metropolitan statistical

area or as otherwise deemed appropriate by SBA).

• If the project involves the retrofit of an applicant’s existing

facility, the retrofit must reduce energy consumption of that

facility by at least 10%, regardless of the energy usage of any

other facilities that the applicant may operate.

53

Energy Reports

Renewable Energy Policy Goal - $5.5 million eligibility

• The energy report must demonstrate that renewable energy

sources generate more than a de minimus amount (SBA

interprets “more than a de minimus amount” to mean at

least 10%) of the energy used by the applicant at the project

facility.

• All improvements or equipment required to generate the

renewable energy or renewable fuels must be included in the

project costs.

• Energy reports prepared by the vendor who will supply the

renewable energy system are not acceptable; a report from

an independent consultant is needed.

54

Appeals Process

• The SBA has an appeals process in the event of an adverse environmental determination.

• Appeals, including exceptions to environmental policy, are reviewed by the Environmental Committee.

• Lenders who believe that a decision rendered by SBA is inconsistent with the SOP, or who seek an exception to policy, may appeal to the committee by sending a copy of the decision, supporting documentation and an explanation to [email protected]

Appeals Process (Cont.)

• Environmental appeals are reviewed by the SBA Environmental Committee which is comprised of attorneys appointed by the Associate General Counsel for Litigation

• The SBA Environmental Committee may consult with SBA’s Environmental Engineers or another Environmental Professional

• The Associate General Counsel for Litigation has authority to overrule decisions rendered by the SBA Environmental Committee

Questions:

• Questions regarding SBA’s environmental

policy can be directed to local field counsel

where the property is located.

• Exceptions to policy are reviewed by SBA’s

Environmental Committee

Environmental Best Practices

• Have as much control of the process as possible

• Train your lending partners

• Make the submission “look” good

Make it easy for the reviewer to review the information

• Make sure things are correct prior to submitting

Correct any mistakes prior to submitting

Stay off the “radar screen”

Contact Information

• Derek Ezovski ([email protected])

• Ashley Hou ([email protected])

• Jeffrey Oelrich ([email protected])