ENVIRONMENTAL, SOCIAL AND GOVERNANCE REPORTING BECOMING … · ENVIRONMENTAL, SOCIAL AND GOVERNANCE...

25

HK LISTING RULES UPDATE: ENVIRONMENTAL, SOCIAL AND GOVERNANCE REPORTING BECOMING A MUST IN 2016 Melissa Fung Partner, Enterprise Risk Services, Deloitte Touche Tohmatsu 19 July 2016

Transcript of ENVIRONMENTAL, SOCIAL AND GOVERNANCE REPORTING BECOMING … · ENVIRONMENTAL, SOCIAL AND GOVERNANCE...

HK LISTING RULES UPDATE:

ENVIRONMENTAL, SOCIAL AND

GOVERNANCE REPORTING

BECOMING A MUST IN 2016

Melissa Fung Partner, Enterprise Risk Services,

Deloitte Touche Tohmatsu

19 July 2016

HK Listing Rules Update Environmental, Social and Governance Reporting Becoming a Must in 2016

Enterprise Risk ServicesDeloitte Touche Tohmatsu

Overview of ESG reporting requirementsOn December 21, 2015, the Hong Kong Stock Exchange ("HKEx") released its consultation conclusions regarding its requirements for Environmental, Social and Governance ("ESG") reporting for listed companies, set out in Appendix 27 of the Main Board Listing Rules.

The HKEx confirms the following key changes, which take effect for financial years commencing on or after January 1, 2016:

• Listed companies should publish ESG reports annually as part of their annual reports, or issue separate ESG reports, no later than three months after the publication of their annual reports. Each company's report should contain narrative disclosures of its policies and the extent of its compliance and material non-compliance with relevant regulations, etc. relating to all environmental and social aspects contained in the HKEx's ESG Guide.

• The board has overall responsibility for the company's ESG strategy and reporting. The board is also responsible for evaluating and determining the company's ESG-related risks and for ensuring that appropriate and effective ESG risk management and internal controls systems are in place.

The former recommended disclosures of key performance indicators ("KPIs") for environmental aspects to become "comply or explain" obligations from January 1, 2017.

©2016. For information, contact Deloitte Touche Tohmatsu.

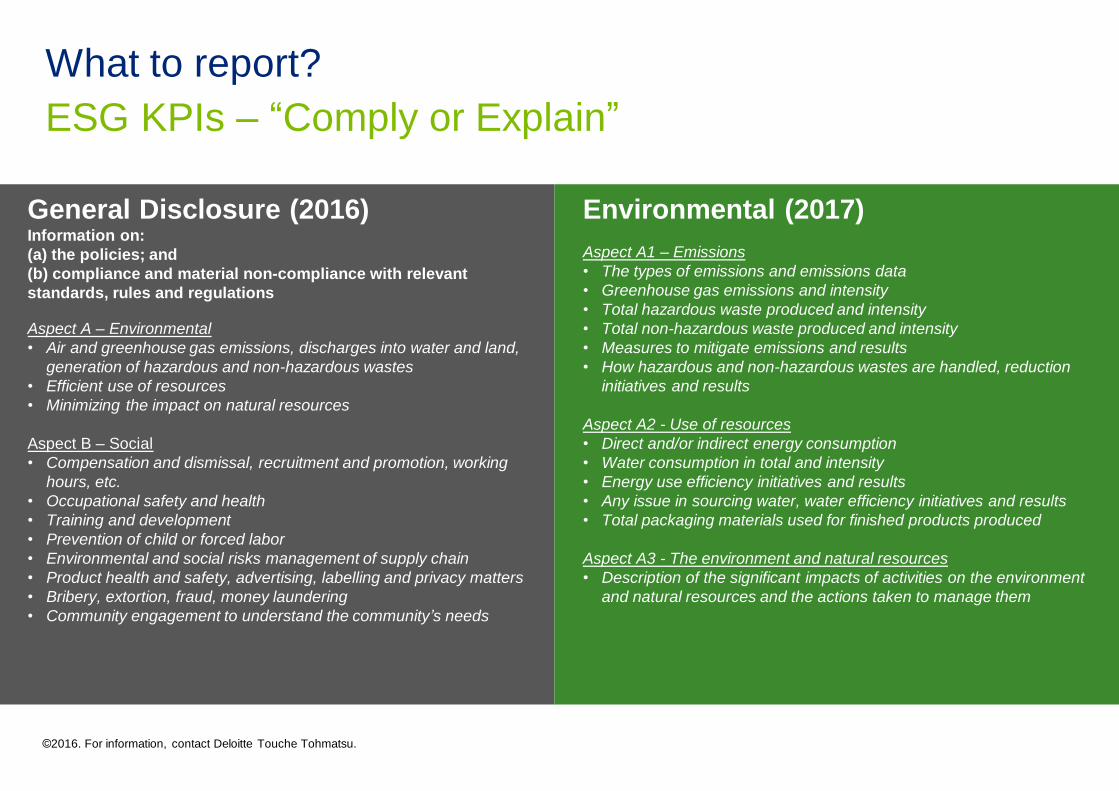

What to report? ESG KPIs – “Comply or Explain”

General Disclosure (2016)Information on:(a) the policies; and(b) compliance and material non-compliance with relevant standards, rules and regulations

Aspect A – Environmental • Air and greenhouse gas emissions, discharges into water and land,

generation of hazardous and non-hazardous wastes• Efficient use of resources • Minimizing the impact on natural resources

Aspect B – Social• Compensation and dismissal, recruitment and promotion, working

hours, etc.• Occupational safety and health• Training and development• Prevention of child or forced labor • Environmental and social risks management of supply chain• Product health and safety, advertising, labelling and privacy matters• Bribery, extortion, fraud, money laundering• Community engagement to understand the community’s needs

Environmental (2017)Aspect A1 – Emissions• The types of emissions and emissions data• Greenhouse gas emissions and intensity • Total hazardous waste produced and intensity • Total non-hazardous waste produced and intensity • Measures to mitigate emissions and results• How hazardous and non-hazardous wastes are handled, reduction

initiatives and results

Aspect A2 - Use of resources• Direct and/or indirect energy consumption • Water consumption in total and intensity • Energy use efficiency initiatives and results• Any issue in sourcing water, water efficiency initiatives and results• Total packaging materials used for finished products produced

Aspect A3 - The environment and natural resources• Description of the significant impacts of activities on the environment

and natural resources and the actions taken to manage them

©2016. For information, contact Deloitte Touche Tohmatsu.

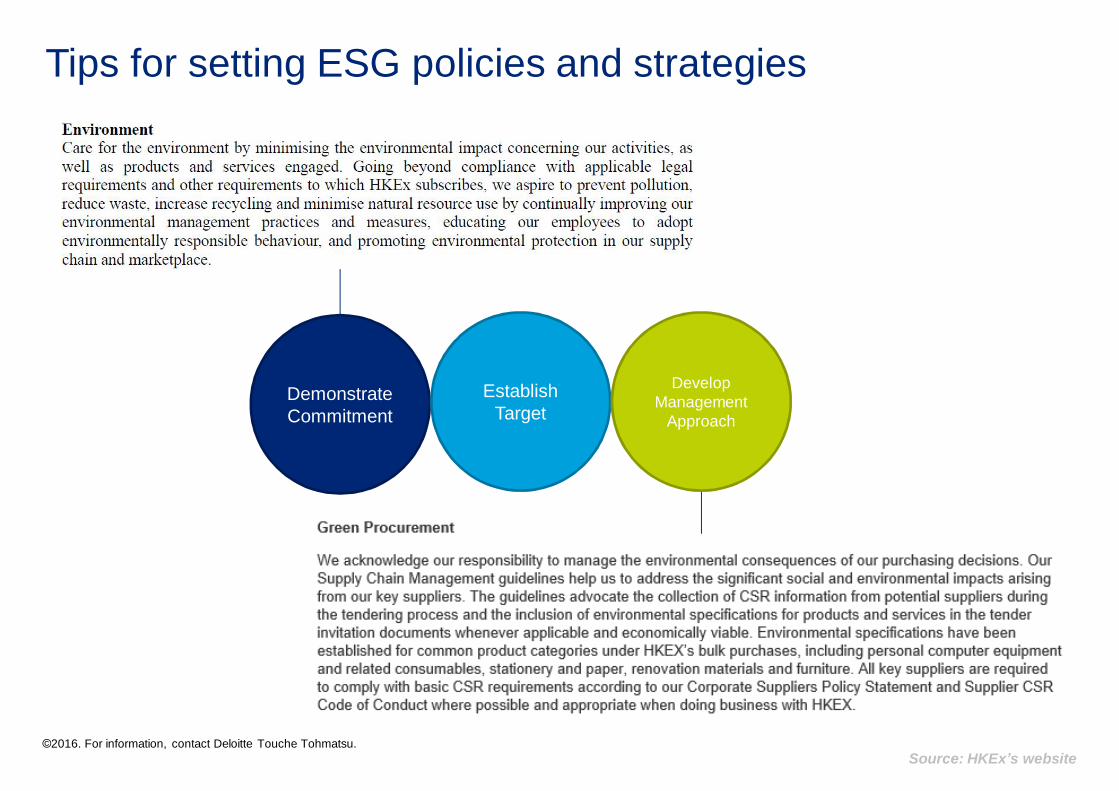

Tips for setting ESG policies and strategies

Demonstrate Commitment

Establish Target

Develop Management

Approach

Source: HKEx’s website©2016. For information, contact Deloitte Touche Tohmatsu.

What to report? ESG KPIs – “Recommended”

Social - Employment and LabourStandards

Aspect B1- Employment • Total workforce • Employee turnover rate

Aspect B2 - Health and safety• Number and rate of work-related fatalities.• Lost days due to work injury• Description of occupational health and safety measures, and their

implementation and monitoring

Aspect B3 - Development and training• The percentage of employees trained • The average training hours

Aspect B4 - Labor standards• Description of measures to review employment practices to avoid child

and forced labor• Description of steps taken to eliminate such practices when

discovered

Social - Operating practices & communityAspect B5 - Supply chain management• Number of suppliers • Practices relating to engaging suppliers, number of suppliers engaged

Aspect B6 - Product responsibility• % of total products sold or shipped subject to recalls for safety and health

reasons• Number of complaints and how they are dealt with• Practices relating to observing and protecting intellectual property rights• Quality assurance and recall procedures• Consumer data protection and privacy policies

Aspect B7 - Anti-corruption• Number of concluded legal cases and the outcomes of the cases• Preventive measures and whistle-blowing procedures

Aspect B8 - Community investment• Focus areas of contribution • Resources contributed to the focus area

©2016. For information, contact Deloitte Touche Tohmatsu.

What to report? HKEx vs GRI

What is GRI?

• Global Reporting Initiative (“GRI”) is the world’s leading Sustainability Reporting framework

• Over 80% of the world’s issued Sustainability Reports apply GRI

• GRI focuses on reporting processes, materiality assessment and performance indicators

• GRI emphasizes that companies should only have Sustainability indicators for the areas defined as material

©2016. For information, contact Deloitte Touche Tohmatsu.

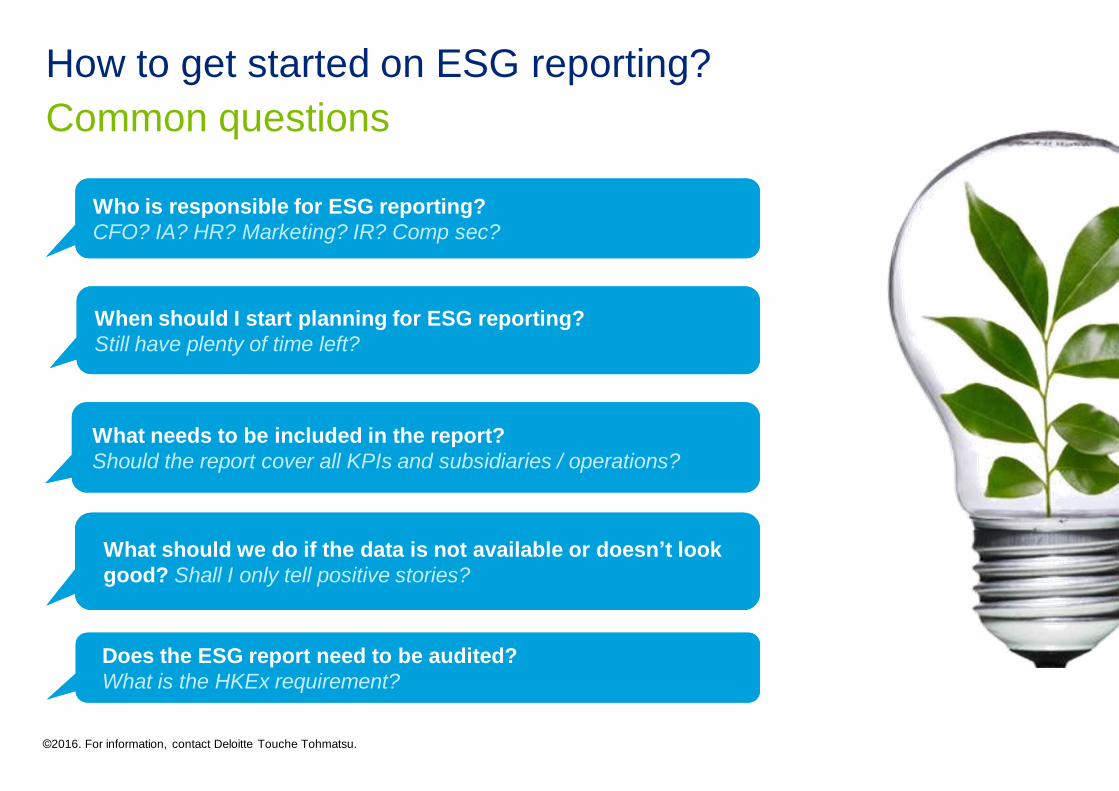

How to get started on ESG reporting? Common questions

What needs to be included in the report?Should the report cover all KPIs and subsidiaries / operations? What needs to be included in the report?Should the report cover all KPIs and subsidiaries / operations?

What should we do if the data is not available or doesn’t look good? Shall I only tell positive stories? What should we do if the data is not available or doesn’t look good? Shall I only tell positive stories?

When should I start planning for ESG reporting? Still have plenty of time left?When should I start planning for ESG reporting? Still have plenty of time left?

Who is responsible for ESG reporting?CFO? IA? HR? Marketing? IR? Comp sec?Who is responsible for ESG reporting?CFO? IA? HR? Marketing? IR? Comp sec?

Does the ESG report need to be audited?What is the HKEx requirement? Does the ESG report need to be audited?What is the HKEx requirement?

©2016. For information, contact Deloitte Touche Tohmatsu.

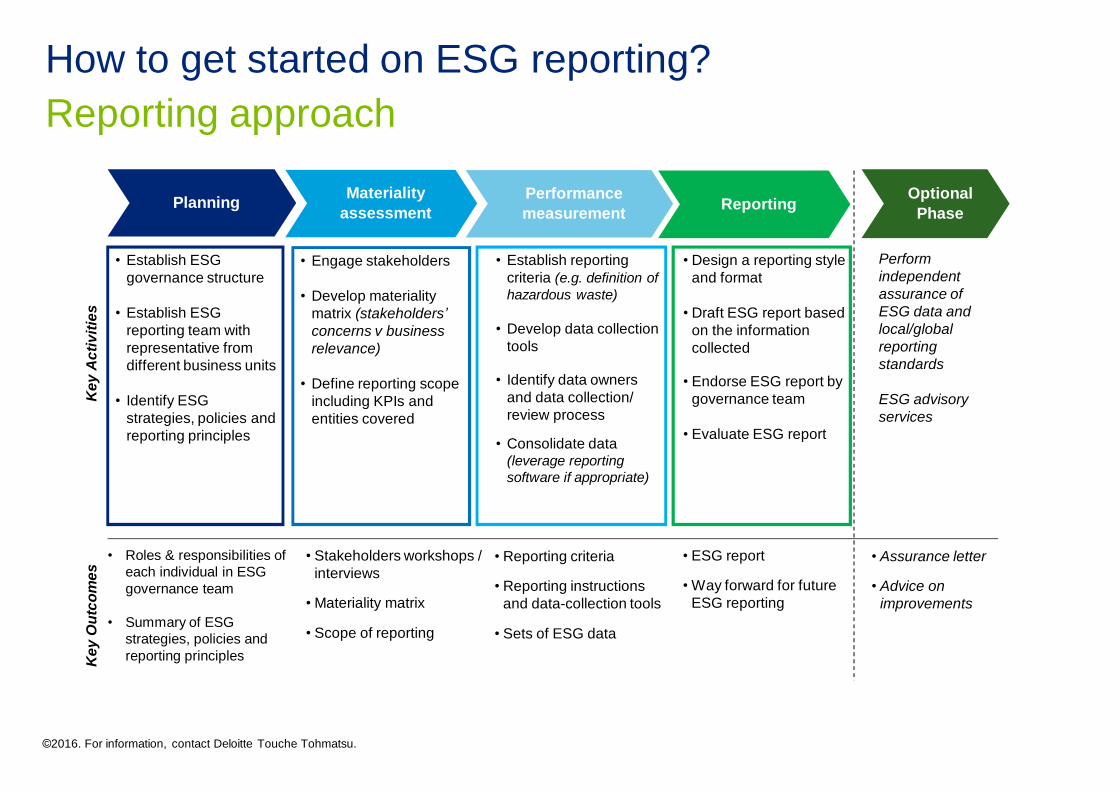

How to get started on ESG reporting? Reporting approach

• Reporting criteria

• Reporting instructions and data-collection tools

• Sets of ESG data

Planning Materiality assessment

Performance measurement

• Establish ESG governance structure

• Establish ESG reporting team with representative from different business units

• Identify ESG strategies, policies and reporting principles

• Engage stakeholders

• Develop materiality matrix (stakeholders’ concerns v business relevance)

• Define reporting scope including KPIs and entities covered

• Establish reporting criteria (e.g. definition of hazardous waste)

• Develop data collection tools

• Identify data owners and data collection/ review process

• Consolidate data (leverage reporting software if appropriate)

• Design a reporting style and format

• Draft ESG report based on the information collected

• Endorse ESG report by governance team

• Evaluate ESG report

Key

Act

iviti

esK

ey O

utco

mes

• Roles & responsibilities of each individual in ESG governance team

• Summary of ESG strategies, policies and reporting principles

• Stakeholders workshops / interviews

• Materiality matrix

• Scope of reporting

Reporting

• ESG report

• Way forward for future ESG reporting

Perform independent assurance of ESG data and local/global reporting standards

ESG advisory services

• Assurance letter

• Advice on improvements

Optional Phase

©2016. For information, contact Deloitte Touche Tohmatsu.

How to get started on ESG reporting? Example of ESG governance structure

Producton Marketing Purchase Logistics PR Finance Sales HR

CEOESG

Committee

Board of Directors

Legal

ESG Reporting Team

©2016. For information, contact Deloitte Touche Tohmatsu.

How to get started on ESG reporting? Setting the scene for ESG

Establish a sustainability vision

Formulate policies and strategy

Define roles and responsibilities for ESG reporting

©2016. For information, contact Deloitte Touche Tohmatsu.

How to get started on ESG reporting? Identify your stakeholders, and their expectations

Customers

Media / NGOs

Top management Investors

Local communities

INEDs / Audit Committee

Industry Associations

ESG Employees

©2016. For information, contact Deloitte Touche Tohmatsu.

How to get started on ESG reporting? Stakeholder engagement

Source: CLP Sustainability Report 2013

©2016. For information, contact Deloitte Touche Tohmatsu.

How to get started on ESG reporting? Example of materiality assessment

Source: China Mobile Sustainability Report 2013

©2016. For information, contact Deloitte Touche Tohmatsu.

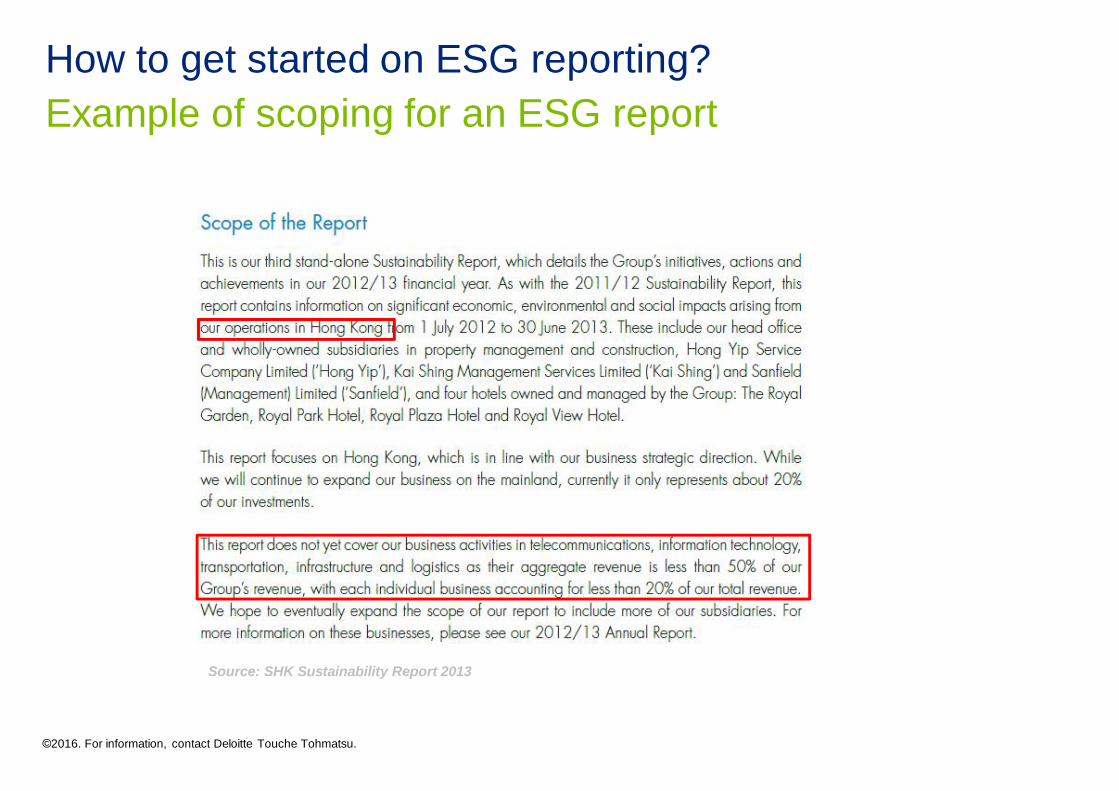

How to get started on ESG reporting? Example of scoping for an ESG report

Source: SHK Sustainability Report 2013

©2016. For information, contact Deloitte Touche Tohmatsu.

How to get started on ESG reporting? Example of reporting criteria

Source: Pacific Andes Sustainability Report 2014

©2016. For information, contact Deloitte Touche Tohmatsu.

How to get started on ESG reporting? Controls over ESG reporting

©2016. For information, contact Deloitte Touche Tohmatsu.

How to get started on ESG reporting? Ten challenges for first-time reporters

1. Adopting a Sustainability vision and business practices – compliance vs value-driven/target

2. Establishing leadership for Sustainability within the organization – additional workload/responsibility

3. Carrying out materiality assessment/stakeholder engagement – resources constraint/limited KPIs

4. Establishing a top-down centralized reporting structure – alignment between different locations/operations

5. Communication between Sustainability team and other departments – level of authority

6. Defining scope/boundary and reporting principles – lack of knowledge and availability of data

7. Revising existing processes/controls to ensure new accountabilities – process re-engineering

8. Educating non-finance staff on reporting – completeness, presentation, interpretation

9. Availability and accuracy of data – change in scope of reporting

10. Lack of documentation and audit trail – challenge in quality assurance

©2016. For information, contact Deloitte Touche Tohmatsu.

How to get started on ESG reporting? What makes a good ESG report?

Does the report provide explanations on the ESG performance?

Does the report cover both good news and bad news?

Has the information in the report been validated?

Have the ESG stories been identified and communicated effectively?

©2016. For information, contact Deloitte Touche Tohmatsu.

Why ESG matters?Values of ESG reporting

Competitive advantages enabled by effective ESG reporting are:• Risk management• Innovation and growth• Enhanced reputation• Operating efficiency• Increased competitiveness

A ESG report provides:• a medium for communicating to stakeholders based

on their expectations• a strategic management tool to help focus on

important issues

Company’s Vision

Value Creation for Stakeholders

of CFOs believe there is a direct link between sustainability program and business performance.

Source: The Deloitte CFO Survey: Sustainability and the CFO

93%©2016. For information, contact Deloitte Touche Tohmatsu.

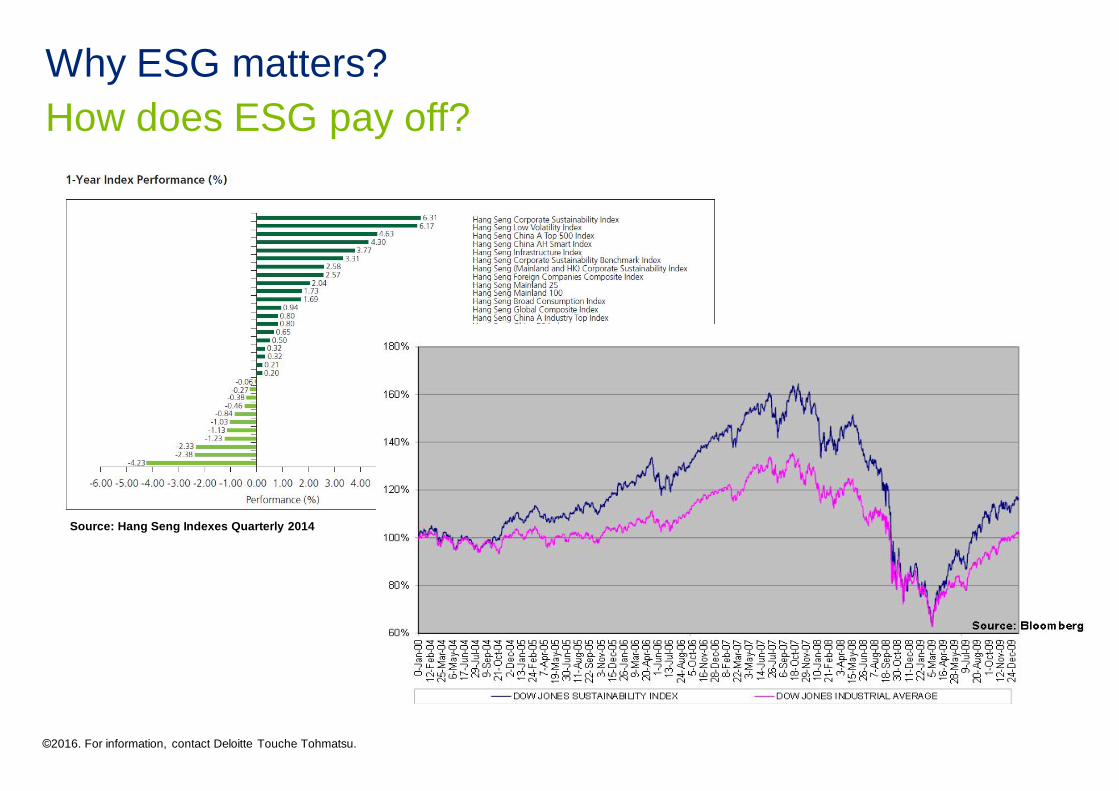

Why ESG matters?How does ESG pay off?

Source: Hang Seng Indexes Quarterly 2014

©2016. For information, contact Deloitte Touche Tohmatsu.

About Deloitte Global Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee ("TTL", its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as "Deloitte Global" does not provide services to clients. Please see www.deloitte.com/cn/en/about for a more detailed description of DTTL and its member firms.

Deloitte provides audit, tax, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 150 countries and territories, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex business challenges. Deloitte's more than 200,000 professionals are committed to becoming the standard of excellence.

About Deloitte in Greater ChinaWe are one of the leading professional services providers with 22 offices in Beijing, Hong Kong, Shanghai, Taipei, Chengdu, Chongqing, Dalian, Guangzhou, Hangzhou, Harbin, Hsinchu, Jinan, Kaohsiung, Macau, Nanjing, Shenzhen, Suzhou, Taichung, Tainan, Tianjin, Wuhan and Xiamen in Greater China. We have nearly 13,500 people working on a collaborative basis to serve clients, subject to local applicable laws.

About Deloitte ChinaThe Deloitte brand first came to China in 1917 when a Deloitte office was opened in Shanghai. Now the Deloitte China network of firms, backed by the global Deloitte network, deliver a full range of audit, tax, consulting and financial advisory services to local, multinational and growth enterprise clients in China. We have considerable experience in China and have been a significant contributor to the development of China's accounting standards, taxation system and local professional accountants.

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the "Deloitte Network" is, by means of this communication, rendering professional advice or services. No entity in the Deloitte network shall be responsible for any loss whatsoever sustained by any person who relies on this communication.

©2016. For information, contact Deloitte Touche Tohmatsu.

›Q & A

› Please submit your text

questions and comments

using the Questions Panel.

THANKS

Your needs are always our highest concern.

We cordially invite you to answer the following questions to enable us to further enhance our services to you.

Thank You!