Entrepreneurial Finance - Lunds universitet · Entrepreneurial finance (in theory and practice) is...

22

2015-04-21 1 Entrepreneurial Finance Hans Landström Sten K. Johnson Centre for Entrepreneurship Lund University Email: [email protected] PhD course: Commercializing your research Lund, 21 April 2015 Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship Today: Entrepreneurial Finance 9.15-9.30 Sum-up from last meeting SOL 9.30-12.00 Lecture: Entrepreneurial Finance (theory) HLa 12.00-13.00 LUNCH 13.00-13.45 Lecture: ”Soft money” and the innovation support system SOL 13.45-16.30 Project work Business Advisors 16.30-17.15 Reflections SOL HLa

Transcript of Entrepreneurial Finance - Lunds universitet · Entrepreneurial finance (in theory and practice) is...

2015-04-21

1

Entrepreneurial Finance Hans Landström

Sten K. Johnson Centre for Entrepreneurship

Lund University

Email: [email protected]

PhD course:

Commercializing your research

Lund, 21 April 2015

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Today: Entrepreneurial Finance

9.15-9.30 Sum-up from last meeting SOL

9.30-12.00 Lecture: Entrepreneurial Finance

(theory)

HLa

12.00-13.00 LUNCH

13.00-13.45 Lecture: ”Soft money” and the

innovation support system

SOL

13.45-16.30 Project work Business

Advisors

16.30-17.15 Reflections SOL

HLa

2015-04-21

2

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

AGENDA

1. What’s the problem?

2. Financial bootstrapping

3. Financial sources for entrepreneurial ventures

4. Venture Capital Institutional Venture Capital

Informal Venture Capital

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Financial characteristics in young

ventures

Liability of smallness/newness (Stinchcombe, 1965)

Investors’ perspective: High information asymmetries, absence of a

financial operating history, lack of collaterals, lack of knowledge, high

ex ante failure risk.

Difficulties in getting resources, not least financial resources

Entrepreneurs’ perspective: Lack of management and knowledge, but

also a private and informal way of operating the business (including

the intertwining between the firm and the individual/family).

Difficulties in using/manage the resources efficiently

2015-04-21

3

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

The Big Money Assumption

Entrepreneurial finance (in theory and practice) is based

on a ‘big money’ assumption i.e. entrepreneurs/small

business managers need a lot of capital in order to buy

resources necessary on the market.

Focus

High-tech firms

Growth-oriented firms

Industries (telecom/biotech/life science/etc.)

Supply of capital is regarded as the problem

Venture Capital is in the forefront of the interest

Investors’ perspective and approach

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

“Big money” assumption … could be

questioned!

New ventures constitute a heterogeneous group of firms

with a lot different needs for capital.

In general the need for capital is limited The majority of new ventures begins with very limited resources, and

generally with no employees or only family members to share the work. Many resources have become less expensive through the web, open

innovation, etc. Even high growth companies start with small amounts of initial finance:

”… according to an analysis of the Inc500 ’America’s fastest

growing private companies’ in 2000, 16% started with less than

$1,000, 42% with $10,000 or less, and 58% with $20,000 or

less.” Inc. Magazine, October 17, 2000, p. 65.

2015-04-21

4

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

InfoGate AB

Consultancy: web-solutions

Start: 1999

Customers: Golf industry

Develop/host/managing

administrative systems for

golf clubs

Ulf Isacson Employees: 12

Founder and CEO Sold to SYSteam

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Resource management in Infogate

Individual-based

resources

Social-based

resources

Contract-based

resources

Period 1 Teacher (university)

No salary

Credit card

(Loan) from mother

Student colleagues

Period 2 Family

Founding team

First customer

Period 3 Retained earnings Bank loan

Customers

Business Angel

2015-04-21

5

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Bootstrapping

Bootstrapping is a strategy through which small business

managers acquire and use resources without the need to

raise equity or borrow money. (Vanacker & Sels, 2009)

Bootstrapping can takes two forms:

1. to minimize the need for external finance, and

2. to creatively acquire resource without using bank finance or outside equity.

Examples:

Use your social network

Use available resources

Borrow resources

Obtain payment in advance from customers

Lease instead of buy

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Bootstrapping ‘modes’

Mode Characteristics Examples

1 Owner financing Use manager’s credit card, loan from relatives and

friends, withholding managers salary

2 Minimization of

account receivable

Cease business relations with late payers, routines to

speed up invoices

3 Customer-related Tapping resources from customer, prepayment of

prototypes, etc.

4 Joint utilization Borrow equipment from others, coordinate purchase

with others, barter instead of buying

5 Delaying payment Lease equipment, delay payment to suppliers

6 Minimizing capital

in stock

Routines to minimize stock, best conditions from

suppliers

7 Subsidy finance Subsidies from different governmental agencies

2015-04-21

6

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Advice for entrepreneurs

◘ Don’t start thinking in terms of external capital use your creativity even when acquire resources.

◘ Bootstrapping is an approach that is convenient and an easily obtainable source (don’t require a business plan or collaterals), and it stimulates a ‘lean’ mindset and ‘resourceful’ solutions.

◘ However, be aware of …

- the necessary speed of launching the product/service

- growth potential of the product/service

◘ There is always ‘an other side of the coin’ – pay back

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Case: Flex Prop

Propellers for passenger boats and cargo ships based on a composite

material that makes the propeller blade flexible.

Karl-Otto Strömberg Propeller for turbines

CEO and power stations

Propeller for ships

2015-04-21

7

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Financial markets for entrepreneurial

ventures (Black & Gilson, 1998)

Bank-oriented Equity-oriented

markets markets

Government-oriented

markets

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Sources of finance for

entrepreneurial ventures

Business size Business age

Very young and Small ventures Growth-oriented small ventures with high growth ventures with an potential but international limited track record market Internal finance Informal VC Public equity - Personal savings Institutional VC - Credit cards Customers - Gifts/loans/equity Suppliers (trade credits) from FFF Research funding Short-term loans (banks) Governmental finance Long-term loans (e.g. banks) - VINNOVA - ALMI - LUIS

2015-04-21

8

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Venture capital

Equity capital

Minority ownership

Temporary partners

Active partnership

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Institutional venture capital vs informal venture capital (DeClerq et al, 2006)

Informal VC (BA) Institutional VC

Status Wealthy individuals Limited partnership

Type of investments Start up/very early stage Generally more mature

projects

Amounts invested €0.03m to €0.4m €0.8m to €6m

Time horizon 4-6 years 6-8 years

Speed of decision Weeks Months

Selection criteria Commercial

Entrepreneurial

Strictly commercial

Syndication Yes Yes

2015-04-21

9

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Governance structure of venture capital

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Structure of a VC fund

Investor (limited partners) (e.g. individuals, pension funds insurance companies, foundations, etc.) Capital Return on investment

Management

VC firm Capital

(general Mgmt fee VC fund Venture partner) Sale of

Return on equity investment Monitoring and

advising

2015-04-21

10

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Time restrictions of a VC fund

Year

1 2 5 8 9 10

Structure Investments Add value Add value Fund

of fund (first round) Investments Harvest raising

(second round)

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

The venture capital process

2015-04-21

11

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

The venture capital process

Investment

process

Structuring

Monitoring and

add value

Exit

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

The venture capital process

Investment

process 1. Deal generation

• Unsolicited deal flow negative

• Personal network flow +/-

Structuring • VC search positive

2. Initial screening

Monitoring and Non-negotiable criteria

add value • Industry

• Amount of money

• Geographical location

Exit • VCs investment strategy

• etc.

2015-04-21

12

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

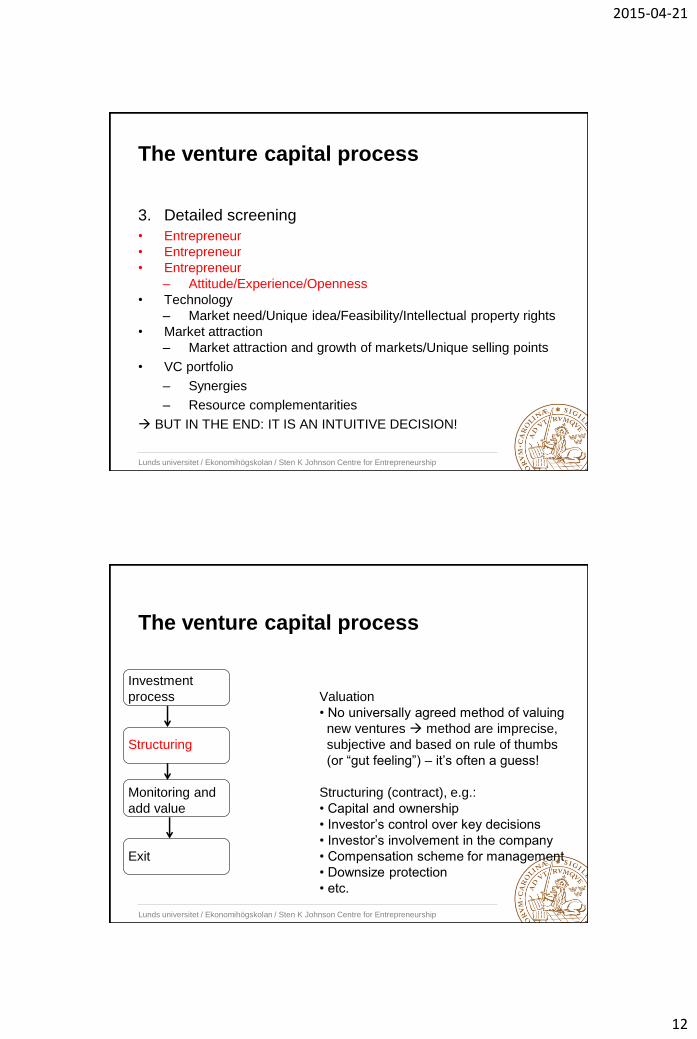

The venture capital process

3. Detailed screening

• Entrepreneur

• Entrepreneur

• Entrepreneur

– Attitude/Experience/Openness

• Technology

– Market need/Unique idea/Feasibility/Intellectual property rights

• Market attraction

– Market attraction and growth of markets/Unique selling points

• VC portfolio

– Synergies

– Resource complementarities

BUT IN THE END: IT IS AN INTUITIVE DECISION!

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

The venture capital process

Investment

process Valuation

• No universally agreed method of valuing

new ventures method are imprecise,

Structuring subjective and based on rule of thumbs

(or “gut feeling”) – it’s often a guess!

Monitoring and Structuring (contract), e.g.:

add value • Capital and ownership

• Investor’s control over key decisions

• Investor’s involvement in the company

Exit • Compensation scheme for management

• Downsize protection

• etc.

2015-04-21

13

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

The venture capital process

Investment

process Activities:

1. Monitoring

2. Providing value-added

Structuring • Management support

- Strategic issues

- Recruit and compensate key individuals

Monitoring and - Routines/discipline (adm./board)

add value - Financial management/raising capital

• Ownership goals

- Joint goals/Distinct milestones

Exit - Market focus

• Legitimize

• Network

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

The venture capital process

Investment

process Exit strategies:

• Initial Public Offering (IPO)

• Acquisition (or trade sale)

Structuring • Secondary sale

• Buyback or management buy out

• Write-off, reconstruction, bankruptcy, etc.

Monitoring and

add value General performance:

2-3 failures

4-6 “living deads”

Exit 2-3 successes

2015-04-21

14

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Performance of venture capital

Actual returns on investments (in % per annum)

Source: Leleux, 2007

Europe USA

5 years 10 years 5 years 10 years

Early stage -7.5 -0.1 -8.6 45.8

Later stage -2.7 7.6 -4.2 17.0

All ventures -4.0 5.3 -6.3 25.4

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Advice for entrepreneurs

• Are you sure that you want an external investor in your venture?

• Develop a comprehensive and competitive business plan.

• A venture capital investment is often a once in life-time investment learn as much as possible about the market and the venture capitalists’ way of work in order to find the best venture capitalist for your venture.

• Your venture must be ’investment ready’ e.g. management team, board of directors, economic control system, etc.

2015-04-21

15

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Critics against venture capital

• More or less ‘impossible’ multiples of exits necessary to

generate required rate of returns, due to: – Limitations in finding growth-oriented companies.

– The lack of successful exit markets.

• Rate on returns on VC investments have been low and the

inflow of capital into the market has been very low.

Venture Capital

Performance in

the US

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Critics against venture capital

• The transformation of the original US business model into

other contexts has been difficult. – The rate of returns lower outside the US.

– Few governmental initiatives to stimulate the VC market have

been successful.

– Lack of good quality venture capitalists outside the US.

2015-04-21

16

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Informal venture capital

Private individuals who invest risk capital (equity capital)

directly in unquoted ventures in which they have no family

connection (Mason & Harrison, 2000)

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Market characteristics

Capital

High Capital-oriented Classical Business

role Angel role

Low Micro-investors Knowledge-oriented

role (crowd funding) role

Low High

Knowledge

2015-04-21

17

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Micro-investors role

Capital

High Capital-oriented Classical Business

role Angel role

Low Micro-investors Knowledge-oriented

role (crowd funding) role

Low High

Knowledge

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Case: HVR Water Purification

Remove all contaminants from tap water (membrane distallation)

Financed by share issues to ‘micro investors’

Today: app 2 500 share holders (through five share issues)

Aapo Saask

CEO

2015-04-21

18

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Crowdfunding

The collective effort of individuals who network and

pool their money, usually via the Internet (e.g. platforms such

as “FundedByMe” and “Kickstarter”), to support efforts

initiated by other people or organizations

Example of forms of crowdfunding:

Equity-based

Donation-based

Debt-based

Buy-based Advertising

First product

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Classical business angel role

Capital

High Capital-oriented Classical Business

role Angel role

Low Micro-investors Knowledge-oriented

role (crowd funding) role

Low High

Knowledge

2015-04-21

19

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Case: Probi

PhD thesis in medicine at LU: Lactobacillus plantarum 299v (that improve

digestion and decrease acidity of the stomach).

Biotech company that develops probiotics with well-documented

beneficial health effects (functional food).

Kaj Vareman

Business Angel

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Business Angels in Sweden (See also Kelly, 2007)

Gender (male) 96% Age 58 years (mean) 40 years or less 6.1% 65 years or more 24.9 % Number of ventures in portfolio 4.4 companies Number of informal investments made the last three years 4 investments (mean) 1 or less investments 16.5% 7 or more investments 11.7% Capital invested in informal investments 1.4 m€ (mean) 0.26 m€ (median)

2015-04-21

20

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Business Angels’ investment

portfolio

27%

14%8%

2%

30%

7% 2%

11%

Stocks in quoted companies

Informal investments

Privately ow ned companies

Bonds

Art

Real-estate

Insurances

Other

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

What do business angels look for?

General criteria Average

1 Leadership potential of lead entrepreneur 4.3

2 Market/sales capabilities of team 4.2

3 Track record of lead entrepreneur 4.1

4 Recognized industry expertise in management team 4.0

5 Information available to investor on investment 4.0

6 Organizational/administrative capabilities of team 3.9

7 Degree of product-market understanding of team 3.8

8 Financial/accounting capabilities of team 3.8

9 Market growth and attractiveness 3.7

10 Production capabilities of team 3.6

11 Expected rate of return 3.5

12 Ability to cash-out 3.5

13 Uniqueness of product 3.3

14 Relative familiarity of BA with industry and technology 3.3

15 Ability to create post-entry barriers in market 3.1

2015-04-21

21

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Advice for entrepreneurs

◘ The first question to ask: Do you have any money to invest for the

moment?

◘ Make detailed assessments of the potential investor

◘ Business Angels are no philanthropists, it is a heterogenous market

and business angels use different investment criteria, but ’first

impression’ and a trustworthy management team important.

◘ Value added from business angels is individual and related to

the situation ( look for experience)

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Learn more about Venture Capital

Hans Landström (ed.),

2007, Handbook of

Research on Venture

Capital, Volume 1,

Cheltenham: Edward

Elgar.

Hans Landström and Colin

Mason (eds.), 2012,

Handbook of Research on

Venture Capital, Volume 2,

Cheltenham: Edward Elgar.

Colin Mason and Hans

Landström (eds.), 2016,

Handbook of Research on

Venture Capital, Volume 3,

Cheltenham: Edward Elgar.

2015-04-21

22

Lunds universitet / Ekonomihögskolan / Sten K Johnson Centre for Entrepreneurship

Q&A

Thank you for your attention!

Hans Landström